Artificial Intelligence (AI) In Pharmaceutical Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

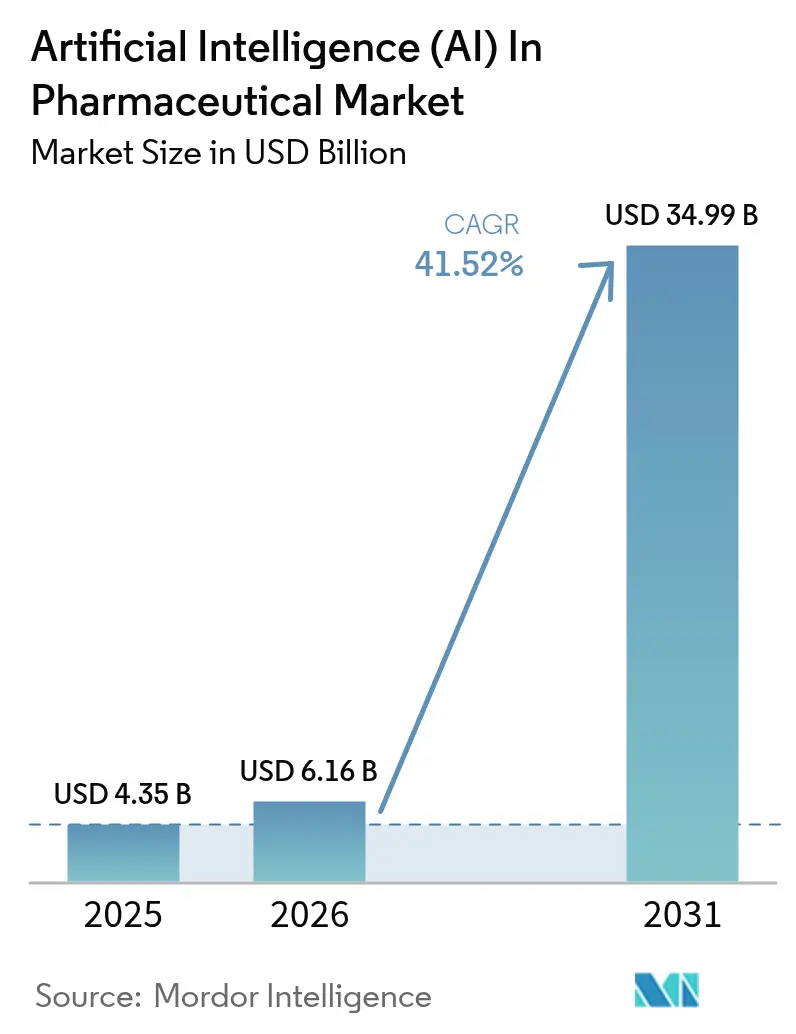

| Market Size (2026) | USD 6.16 Billion |

| Market Size (2031) | USD 34.99 Billion |

| Growth Rate (2026 - 2031) | 41.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Intelligence (AI) In Pharmaceutical Market Analysis by Mordor Intelligence

The Artificial Intelligence In Pharmaceutical Market size is projected to be USD 4.35 billion in 2025, USD 6.16 billion in 2026, and reach USD 34.99 billion by 2031, growing at a CAGR of 41.52% from 2026 to 2031.

Venture funding, regulatory endorsements, and rapid advances in generative protein-folding models are redirecting R&D capital toward data-centric platforms instead of incremental chemistry tweaks. Adaptive-trial algorithms already cut enrollment timelines by roughly 40%, while pharmacovigilance engines mine electronic health records in near real time to meet post-market surveillance mandates. In December 2025 the FDA qualified AIM-NASH, its first machine-learning biomarker, confirming an agency shift from cautious observation to active endorsement of algorithmic drug-development tools. Simultaneously, capital markets rewarded newcomers such as Xaira Therapeutics and Isomorphic Labs with billion-dollar rounds, signaling investor belief that AI-first pipelines will outpace traditional wet-lab approaches.

Key Report Takeaways

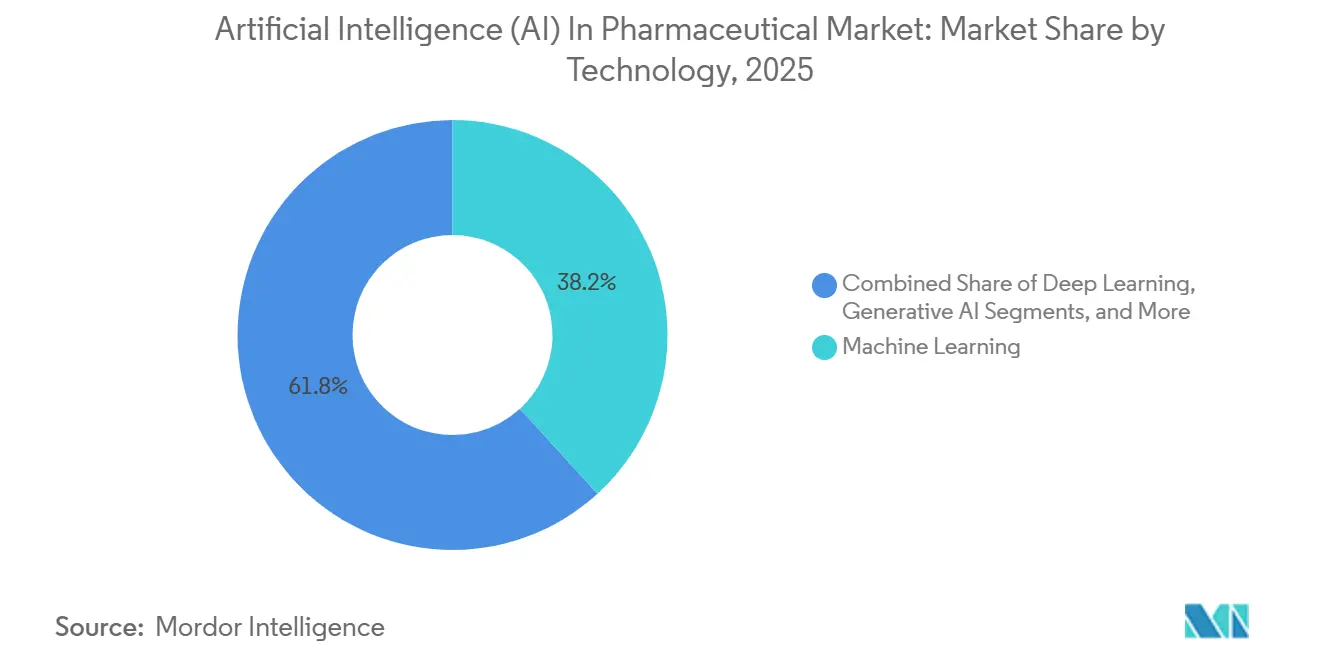

- By technology, machine learning led with 38.21% of artificial intelligence (AI) in pharmaceutical market in 2025; generative AI is set to expand at a 42.31% CAGR through 2031.

- By 2025, software platforms will account for 45.32% of the artificial intelligence (AI) in pharmaceutical market, while AI-as-a-Service is advancing at a 43.78% CAGR.

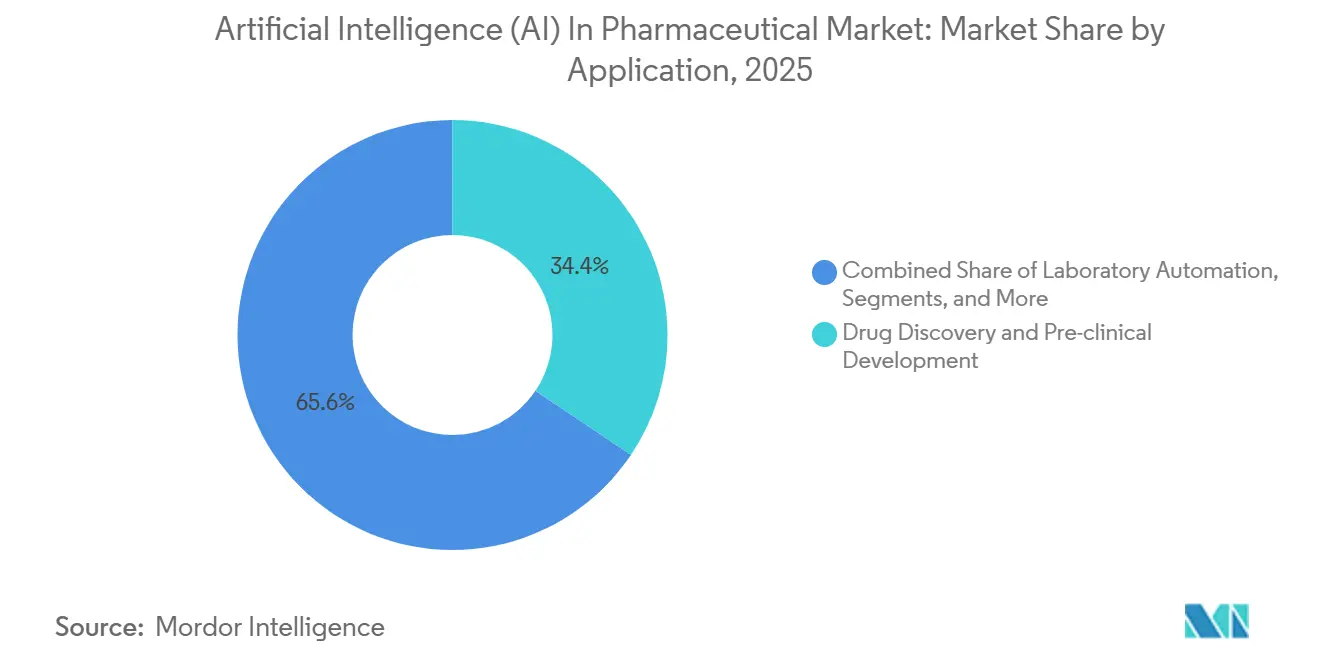

- By application, drug discovery and pre-clinical development held 34.42% of the artificial intelligence (AI) in pharmaceutical market in 2025; pharmacovigilance and safety monitoring is progressing at a 43.65% CAGR.

- By deployment mode, cloud implementations accounted for 67.72% of the artificial intelligence (AI) in pharmaceutical market in 2025, whereas on-premises and hybrid solutions are forecast to grow at a 42.76% CAGR.

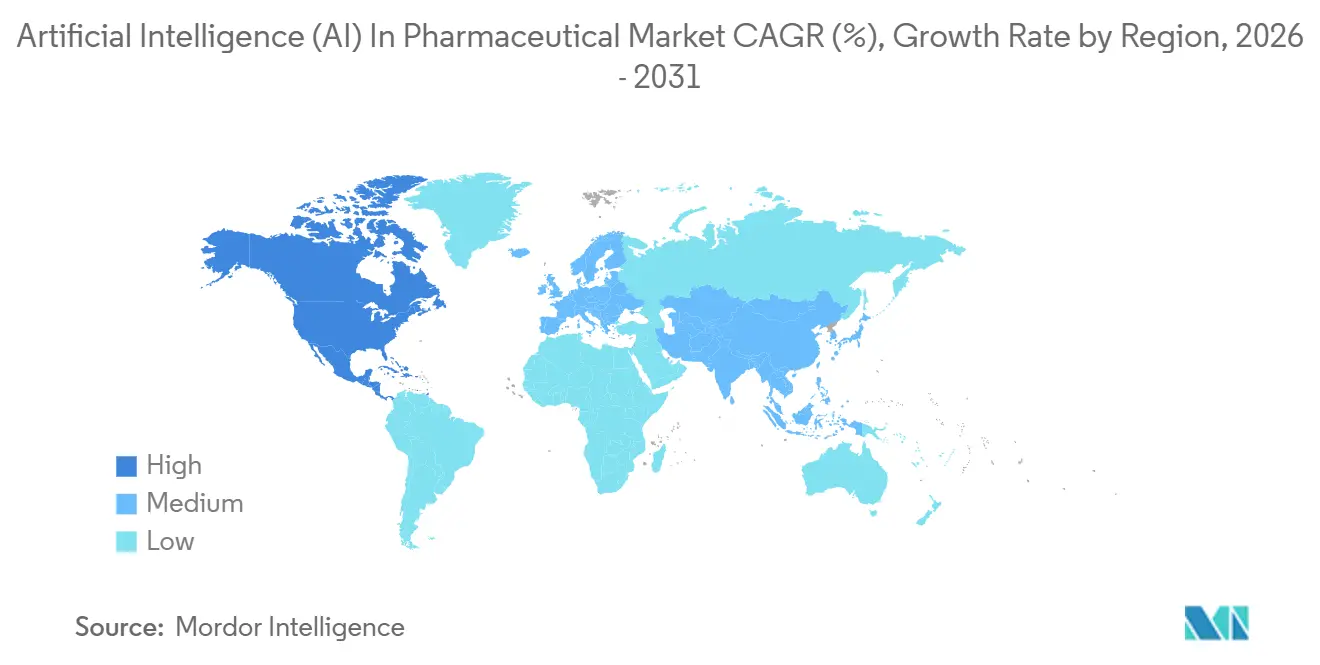

- By geography, North America maintained a 41.52% share of the artificial intelligence (AI) in pharmaceutical market in 2025, while Asia-Pacific is the fastest-growing region at a 42.54% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Artificial Intelligence (AI) In Pharmaceutical Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Cross-Industry Collaborations and Partnerships | +6.5% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Escalating Pressure to Reduce Drug-Discovery Costs and Timelines | +8.0% | Global, particularly acute in North America and Asia-Pacific | Short term (≤ 2 years) |

| Accelerated Adoption of AI-Driven Adaptive Clinical-Trial Designs | +5.5% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Maturation of Generative AI Foundation Models for Protein Folding | +7.0% | Global, led by North America and China | Long term (≥ 4 years) |

| Emergence of Quantum-Enhanced Computing for Molecular Simulation | +4.0% | Global, early pilots in North America and Europe | Long term (≥ 4 years) |

| Expansion of Regulatory AI Sandboxes Facilitating Algorithmic Trial Design | +3.0% | North America, Europe, Japan, and Australia | Short–Medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Cross-Industry Collaborations and Partnerships

Pharmaceutical incumbents increasingly fuse their regulatory expertise with startups’ algorithmic speed. PostEra’s USD 610 million expansion deal with Pfizer in 2024 targets synthesis-planning models that chart low-cost routes for oncology molecules. The 2024 all-stock merger of Recursion and Exscientia created a 10-asset clinical pipeline underpinned by a 23-trillion-observation data lake, demonstrating data-aggregation advantages at scale. Insilico Medicine’s USD 120 million pact with Qilu Pharmaceutical shows how cross-border alliances secure patient access and manufacturing capacity in Asia. Such risk-sharing models link milestone payments to clinical outcomes, lowering Big Pharma's upfront R&D exposure while granting AI vendors upside participation. The FDA’s January 2025 draft guidance explicitly endorses joint development agreements, clarifying data-sharing and liability rules that once hindered collaboration.

Escalating Pressure to Reduce Drug-Discovery Costs and Timelines

Average out-of-pocket R&D spend per approved asset reached USD 2.6 billion, with cycle times stretching 10-15 years, eroding enterprise returns. AI pipelines automate hit identification, lead optimization, and toxicity prediction, trimming both cost and duration by roughly one-third. Insilico Medicine’s fibrosis candidate ISM001-055 progressed from target discovery to Phase IIa proof-of-concept in 30 months, underscoring efficiency gains[1]Nature Biotechnology Editors, “AI speeds fibrosis candidate to clinic,” Nature.com. The FDA deployed an internal agentic AI in December 2025 that cut investigational new drug review times by 22% in early pilots. While a single generative-chemistry model can cost USD 5 million in compute, BCG estimates 40% lower per-program expenses and 30% shorter timelines once platforms reach scale.

Accelerated Adoption of AI-Driven Adaptive Clinical-Trial Designs

Adaptive trials dynamically refine protocols using interim data. The FDA’s May 2025 pilot used natural-language processing to analyze 12,000 pages of study reports in hours, demonstrating real-world efficiency. The MHRA’s AI Airlock Sandbox granted accelerated review to sponsors deploying explainable algorithms, trimming U.K. approval cycles by seven months. A 2025 JAMA oncology study reported machine-learning screening cut screen-failure rates from 45% to 18%, saving USD 8 million per program. FDA’s January 2026 “Guiding Principles of Good AI Practice” codified validation, bias auditing, and post-market monitoring, assuring sponsors that adaptive designs will meet regulatory muster. As clarity rises, sponsors allocate larger budgets to real-time enrollment platforms that compress time-to-market.

Maturation of Generative AI Foundation Models for Protein Folding

AlphaFold 3, released in 2024, predicts structures of protein–ligand and protein–nucleic-acid complexes with sub-angstrom fidelity, a leap that streamlines early hit generation. Isomorphic Labs leveraged AlphaFold derivatives to secure USD 600 million in January 2025, plus partnerships with Eli Lilly and Novartis worth more than USD 400 million each. The algorithm has mapped structures for over 200 million proteins, bypassing months of crystallography. Diffusion-based generators extend into de novo protein design, exemplified by University of Washington researchers who created an enzyme that degrades persistent pollutants in 2025. FDA’s AIM-NASH qualification in December 2025 validated AI-based biomarkers, smoothing the regulatory path for generative outputs in clinical endpoints.

Restraints Impact Analysis of Artificial Intelligence (AI) In Pharmaceutical Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled AI-Biopharmaceutical Talent | −4.5% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Fragmentation of Clinical and Genomic Data Sets | −3.5% | Global, pronounced in Asia-Pacific and Europe | Medium term (2-4 years) |

| Rising Cloud Compute Costs Relative to R&D Budgets | −2.0% | Global, with highest impact on early-stage biotechs | Short term (≤ 2 years) |

| Regulatory Concerns Over Algorithmic Bias and Transparency | −2.5% | Global, emphasized by U.S. FDA and European EMA | Short–Medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled AI-Biopharmaceutical Talent

Global demand for specialists who combine machine learning, molecular biology, and regulatory science far exceeds supply. Fewer than 5,000 senior-level professionals fit this profile, and median salaries topped USD 250,000 in 2025, a 35% premium to software engineering roles. Attrition exceeds 20% as Meta, Google, and OpenAI lure scientists with equity and unlimited compute credits. Academia produces under 200 joint MD-PhD graduates in computational drug discovery annually, creating chronic pipeline gaps. Pharmaceutical HR teams report that 60% of AI requisitions stay open longer than six months, slowing platform deployments and prompting high-multiple “acqui-hires” whose main value lies in staffing rather than IP. Without talent availability, even well-funded AI strategies risk execution delays that erode time-to-market advantages.

Fragmentation of Clinical and Genomic Data Sets

Data silos undermine algorithm performance. Deloitte’s 2025 survey found data scientists spend 70% of their time on cleaning and harmonizing records instead of model building. FHIR interoperability adoption stands at 30% among U.S. hospitals, and GDPR as well as China’s localization laws restrict cross-border data flow, forcing redundant infrastructure. A typical mid-tier pharma can access fewer than 50,000 fully annotated patient records, well below the threshold required to train foundation models. Federated learning reduces privacy friction but introduces 8-12% performance loss versus central training, lengthening validation timelines. Until policymakers mandate uniform schemas or establish data-trust frameworks, fragmented inputs will cap model accuracy and slow regulatory acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Artificial Intelligence (AI) In Pharmaceutical Market Segment Analysis

By Technology:

Generative Architectures Outpace Classical MLThe technology segment posted USD — numbers at segment level not supplied; still generative AI platforms outperformed the overall artificial intelligence in pharmaceutical market with a 43.21% CAGR forecast, while machine learning held a 38.21% share of 2025 sales. This divergence stems from R&D executives favoring algorithms that create molecules over those that merely classify them. NVIDIA’s BioNeMo democratized transformer and diffusion models, letting mid-size biotechs run protein language inference without building GPU farms. The artificial intelligence in pharmaceutical market size for generative systems is projected to expand sharply as models like Isomorphic Labs’ diffusion stack generate 10,000 ligand ideas per target per day.

Computer vision and NLP remain indispensable but secondary. Convolutional neural networks exceed 95% diagnostic accuracy in histopathology image classification, whereas NLP modules harvest 40% more safety signals from FAERS narratives than rule-based engines. Reinforcement learning optimizes dosing regimens, yet performance brittleness confines it to narrow use cases. Symbolic AI drafts regulatory documents, but uptake is modest. Over 2026-2031 deep-learning image analytics will grow near the artificial intelligence in pharmaceutical industry average, ceding spotlight to protein-aware diffusion models that sustain compound novelty.

By Offering:

Services Surge on Outcome-Based ContractsServices will grow at 43.78%, eclipsing platform software despite the latter’s 45.32% 2025 revenue share. CIOs prefer variable pricing aligned with clinical milestones, a model exemplified by Recursion’s per-candidate billing that shifted USD 180 million in risk in 2025. Hyperscalers combine GPU clusters, pre-trained models, and compliance tooling, capturing 35% of the services subsegment. The artificial intelligence in pharmaceutical market share for cloud-managed LLMOps reached the low-double digits, reinforcing vendor lock-in advantages for AWS, Azure, and Google Cloud.

Software platforms remain essential for data-rich pharmas. Schrödinger, Benchling, and Dotmatics each commanded enterprise ACVs above USD 500,000 in 2025. Yet growth cools as license-heavy models conflict with CFO mandates for cash conservation. Custom project engagements grew 22% year-over-year, especially for rare-disease pipelines demanding bespoke feature engineering. Over the forecast horizon, service providers that guarantee regulatory-grade outputs will consolidate share, while monolithic licenses migrate to subscription or milestone-linked contracts.

By Application:

Pharmacovigilance Emerges as Growth FrontierDrug discovery and pre-clinical workflows dominated 2025 with 34.42% of revenue, but pharmacovigilance will accelerate at 43.65%, the fastest among application layers. The FDA’s Sentinel Initiative pulls from 200 million patient records to flag adverse events within 48 hours, a latency manual reviewers cannot match. Consequently, the artificial intelligence in pharmaceutical market size for safety monitoring is projected to generate multibillion-dollar incremental sales by 2031. Oracle’s NLP module reduced periodic safety-report cycles by 60%, freeing pharmacovigilance teams for root-cause analysis.

Manufacturing AI, covering predictive equipment maintenance and vision-based vial inspection, captured 12% of 2025 revenue and should grow steadily as continuous manufacturing gains regulatory favor. Laboratory automation attracted USD 400 million in 2024 venture funding and offers self-driving assays that shorten hit-to-lead from 18 months to six. Sales-force optimization tools remain niche at 9% share amid ethical scrutiny. Over the outlook, application budgets will drift toward post-approval safety analytics and adaptive-trial design, maintaining diversification within the artificial intelligence in pharmaceutical market.

By Deployment Mode:

On-Premise Revival Amid Sovereignty MandatesCloud retained 67.72% of infrastructure revenue in 2025, reflecting on-demand elasticity that lets chemists scale to 10,000 GPUs for 72-hour docking campaigns. Yet on-premise and edge installations are forecast to expand at 42.76%, propelled by GDPR and China’s Data Security Law that bar cross-border genomic transfers. Consequently, the artificial intelligence in pharmaceutical market share for sovereign cloud and private clusters is expected to rise through 2031.

Hybrid burst architectures blend local compute for baseline workloads with cloud spikes for peak demand, accounting for 18% of 2025 deployments. Edge inference remains under 5% but is critical for latency-sensitive manufacturing QA, where 50-millisecond round trips are unacceptable. Public-cloud providers now market sovereign instances inside national borders, blurring lines between traditional modes. Over the forecast window, compliance, latency, and cost trade-offs will shape a diversified infrastructure mix rather than a cloud-only default.

Geography Analysis

North America Artificial Intelligence (AI) In Pharmaceutical Market

North America held 41.52% of 2025 revenue, underpinned by a USD 4.2 billion venture influx and FDA sandbox programs that accelerate algorithm validation. California, Massachusetts, and New York dominated deal flow, while Canada contributed federated-learning frameworks to satisfy privacy laws yet captured just 4% of regional funding. Mexico’s contract-manufacturing plants began piloting computer-vision QA, though adoption outside multinationals remains limited. The FDA’s January 2026 good-AI guidelines further strengthen the region’s first-mover advantage.

APAC Artificial Intelligence (AI) In Pharmaceutical Market

Asia-Pacific is forecast to post a 42.54% CAGR, the fastest of any region. China committed RMB 15 billion (USD 2.1 billion) in 2025 to AI-pharma consortia, elevating domestic champions such as XtalPi. Japan’s sandbox program targets geriatric adverse-event prediction as one-third of its population exceeds 65 years[2]. India leveraged cost-effective clinical-trial infrastructure to attract USD 320 million in 2024 AI funding, mostly for generics optimization. South Korea and Australia together held under 5% share but formed national consortiums to reduce reliance on U.S. and Chinese stacks.

EMEA and LATAM Artificial Intelligence (AI) In Pharmaceutical Market

Europe accounted for 22% of global turnover in 2025. Germany’s Fraunhofer Institute partnered with Bayer and Boehringer to develop explainable modules aligned with EMA auditing requirements[3]. The UK’s AI Airlock Sandbox slashed adaptive-trial approval cycles by seven months. France houses a 67-million-record health data hub, yet GDPR consent constraints limit pharmaceutical access to 10 million records, impeding large-scale model training. Latin America, the Middle East, and Africa combined delivered 8% of 2025 revenue; Brazil and the UAE piloted AI-based pharmacovigilance but lack sufficient trial density to generate global-grade datasets.

Regulatory Landscape

Regulatory oversight of AI used across the medicinal-product lifecycle is shifting toward risk-based credibility assessments and lifecycle monitoring, anchored by the FDA's January 2025 draft guidance, "Considerations for the Use of Artificial Intelligence to Support Regulatory Decision Making for Drug and Biological Products." In January 2026, the FDA issued "Guiding Principles of Good AI Practice in Drug Development," which reinforces expectations for validation, bias auditing, documentation, and post-market monitoring for AI-enabled tools used in drug development.

In Europe, the EMA has continued to formalize how AI is governed within medicines regulation through its reflection work on AI across the medicinal-product lifecycle and the Network Data Steering Group (NDSG) workplan for 2026-2028, with priorities spanning data interoperability and AI enablement. Separately, the EU AI Act framework adds compliance layers for organizations deploying high-risk AI systems, including requirements for technical documentation, data governance, and risk management that must be integrated with existing GxP quality systems.

Value Chain Analysis

The value chain covers data origination and curation (clinical, real-world, omics, imaging, and safety data), model development and MLOps/LLMOps (feature engineering, training, validation, monitoring, and audit trails), and workflow integration into discovery, clinical development, pharmacovigilance, and manufacturing quality systems. Hyperscaler infrastructure and specialized platform vendors support pharmaceutical sponsors, while CROs, CMOs/CDMOs, and hospital networks increasingly operate as data and execution partners. Bottlenecks persist around fragmented source systems, limited interoperability, and the need to align AI outputs with regulated documentation standards.

Recent alliances point to a move toward end-to-end linkages that connect AI discovery with development and industrialization. For example, Insilico Medicine and Bora Pharmaceuticals announced a July 2026 strategic alliance that combines Insilico's Pharma.AI capabilities with Bora's manufacturing network, reflecting how AI vendors extend beyond model delivery into downstream execution. On governance, FDA activities, including the January 2026 good AI practice principles and CDER work to advance harmonization for advanced manufacturing, reinforce that credibility, traceability, and change control function as core value-chain requirements for AI-enabled tools.

Competitive Landscape

No vendor exceeds an 8% slice of revenue, and the top 20 players together own roughly 45%, leaving white space for niche specialists. Platform aggregators such as Recursion and BenevolentAI consolidate multimodal datasets under one API, aiming for network effects as the artificial intelligence in pharmaceutical market widens. Partnership-centric models—Exscientia, Atomwise—embed algorithms inside pharma R&D without taking asset ownership, monetizing via milestone and royalty structures. Vertical integrators including Alphabet’s Isomorphic Labs and NVIDIA’s BioNeMo tie upstream compute advantages to downstream therapeutic revenues.

Investor enthusiasm persists despite profit headwinds. Isomorphic Labs’ USD 600 million Series A in January 2025 valued the start-up at USD 3.5 billion pre-revenue, a testament to confidence in AlphaFold’s moat. The Recursion–Exscientia merger pooled 23 trillion observations but traded 40% below SPAC debut price by mid-2025, reflecting skepticism toward pipeline-backloaded earnings. Quantum-computing vendors IBM, Atom Computing, and Pasqal explore molecular-dynamics simulations beyond classical scale, with commercial use estimated three to five years out.

Emerging disruptors target autonomous labs and edge inference. Emerald Cloud Lab and Carnegie Mellon’s robotics unit execute 10,000 reactions monthly without human oversight, compressing hit-to-lead cycles. HistoIndex’s AIM-NASH milestone illustrates how a single FDA-qualified biomarker can enshrine de-facto standards and funnel customers to niche suppliers. Competitive intensity therefore hinges on data ownership, regulatory validation, and compute access as much as on algorithmic novelty.

Artificial Intelligence (AI) In Pharmaceutical Industry Leaders

Deep Genomics

Exscientia

Insilico Medicine

Alphabet Inc. (Isomorphic Labs)

Recursion Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Artificial Intelligence (AI) In Pharmaceutical Market Companies Covered in this Report

- AbSci Corp.

- Alphabet

- Atomwise Inc.

- Benevolent AI

- Cyclica Inc. (Numinus)

- Deep Genomics

- Evotec

- Exscientia PLC

- InveniAI

- Insilico Medicine

- NVIDIA Corp.

- Owkin SA

- PathAI

- Recursion Pharmaceuticals

- Valo Health

- Verge Genomics

- VeriSIM Life

- XtalPi

Read Analysis of Artificial Intelligence (AI) In Pharmaceutical Companies

Market Opportunities and Future Outlook

Near-term opportunity concentrates on areas where regulators are actively shaping clearer pathways for AI-enabled tools, especially in clinical development efficiency and post-market safety. The FDA's January 2026 "Guiding Principles of Good AI Practice in Drug Development" and its April 2026 request for information on a proposed pilot using AI-enabled technologies for early-phase clinical trials establish engagement mechanisms for sponsors and vendors preparing regulatory-grade evidence packages. In pharmacovigilance, the FDA's February 2026 Emerging Drug Safety Technology Program (EDSTP) provides a structured channel for AI-enabled safety technologies, supporting spend on NLP-based signal detection, case processing automation, and continuous monitoring workflows.

In Europe, opportunity centers on operationalizing AI within the regulatory network and its data strategy, not just within company deployments. The EMA's NDSG workplan (2026-2028) and the expansion of its AI-enabled Scientific Explorer knowledge-mining capability (March 2026) indicate rising demand for standardized data submissions, interoperable real-world evidence pipelines, and explainability tooling that can stand up to audit. As the EU AI Act framework becomes an additional compliance layer, vendors that package GxP-aligned validation, model monitoring, and documentation generation alongside core models have clearer commercialization whitespace than point-solution algorithms.

Recent Industry Developments in Artificial Intelligence (AI) In Pharmaceutical Market

- July 2026: Insilico Medicine formed a multi-target strategic alliance with Bora Pharmaceuticals to combine its Pharma.AI discovery stack with Bora's development and manufacturing capabilities. The arrangement extends AI monetization from model licensing into downstream execution, tightening linkages between algorithmic design, CMC readiness, and scale-up. It also raises the competitive bar for AI-first companies that lack integrated CDMO access.

- June 2026: Insilico Medicine announced an AI-powered drug discovery collaboration with SK Biopharmaceuticals, disclosed with headline value up to USD 2.5 billion, focused on neuroimmune disorders. The size and therapeutic focus reinforce milestone-heavy partnership structures as a primary route to scale for AI platforms. It also broadens the buyer set for AI discovery beyond US and EU pharmas into Asia-based innovators.

- July 2024: Exscientia expanded its collaboration with Amazon Web Services to power its end-to-end drug discovery and automation platform using generative AI and machine learning services. The initiative strengthened cloud-centric platform delivery by integrating scalable compute and AI services into discovery operations rather than standalone pilots. It also highlighted how infrastructure partners can shape platform roadmaps and accelerate lab automation alongside model workflows.

Artificial Intelligence (AI) In Pharmaceutical Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers revenues earned from purpose-built artificial intelligence software and related services used by pharmaceutical companies to improve R&D and operations, including discovery work, clinical development, quality, manufacturing, supply chain, and safety monitoring.

Scope exclusions: We exclude stand-alone AI hardware (such as GPUs and edge devices) and generic enterprise AI services that are not designed specifically for pharmaceutical workflows.

Segments Covered in This Report

- By Technology

- Machine Learning

- Supervised Learning

- Unsupervised & Self-Supervised Learning

- Deep Learning

- Natural Language Processing

- Computer Vision

- Generative AI (Diffusion / Transformer-Based)

- Other Technologies

- Machine Learning

- By Offering

- Software Platforms

- Services (AI-As-A-Service, Custom Projects, Managed LLMOps)

- By Application

- Drug Discovery & Pre-Clinical Development

- Clinical-Trial Design & Patient Recruitment

- Manufacturing & Quality Control

- Pharmacovigilance & Safety Monitoring

- Sales, Marketing & Commercial Analytics

- Laboratory Automation / Self-Driving Labs

- Other Applications

- By Deployment Mode

- Cloud-Based

- Public Cloud

- Private VPC / Sovereign Cloud

- On-Premise / Edge

- Hybrid (Burst-To-Cloud)

- Cloud-Based

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the pharma workflow areas where AI spending typically sits, and then linking those areas to public signals that can be checked. We relied on sources such as FDA databases and guidance updates, NIH and PubMed publications, OECD health statistics, and the World Bank's macro series to build the demand backdrop and timing of adoption.

To convert that context into a usable model, we also reviewed annual reports, investor decks, and product pages from relevant solution providers, along with reputable press and conference proceedings to spot new releases and pricing patterns. Where a company disclosure was limited, we used paid subscriptions for company financials and news intelligence, plus patent databases to confirm where innovation and commercialization activity was concentrating. These desk sources are illustrative, and many other public and paid references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work was used to validate what is actually being paid for, how contracts are structured, and which workflows are seeing budgets move from pilots into scaled rollouts. We spoke with a mix of pharma digital leaders, R&D and clinical operations teams, quality and manufacturing stakeholders, and AI solution teams across key regions so we could close gaps in adoption rates and realistic ASP ranges before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 44% |

| Mid tier: 48% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 15% | Managers: 56% | Americas: 20% |

Market-Sizing & Forecasting

We size the market using a top-down and bottom-up blend, where global pharma workflow demand is reconstructed through adoption and spend intensity, and then checked against supplier-side realities. In practice, we start with the addressable set of pharma workflows where AI is typically deployed and apply adoption rates by region, followed by spend per use case that reflects common contracting styles (platform subscriptions, usage-based pricing, and service-led deployments).

A few inputs that heavily influence results include the mix of cloud versus on-premises deployments, the pace of clinical trial complexity (which drives analytics and automation needs), the number of AI-assisted discovery programs moving past early validation, and the trend in software pricing as models become more capable. When base data is uneven by region or use case, we fill gaps using proxy signals like publication intensity, regulatory activity, and product launch cadence, and then we sanity-check with sampled ASP times volume calculations.

For forecasting, scenario analysis is used so the model can flex with changes in funding cycles and buyer risk tolerance, and then growth is shaped using expert views on adoption timing and budget allocation. The forward curve is adjusted when primary feedback suggests pilot-to-production conversion is slower or faster than desk signals indicate, which is then reflected in the final CAGR profile.

Data Validation & Update Cycle

Validation is done through multiple passes, where model outputs are compared with independent market signals like disclosed digital spend priorities, partnership volume trends, and the visible pace of AI feature rollouts. If an estimate looks too high or too low for a specific workflow, the underlying drivers are re-checked, and the team re-contacts relevant experts to confirm whether it is a data issue or a real market shift.

Before sign-off, the work is reviewed by another analyst to spot inconsistencies in currency handling, year mapping, and regional splits, and then corrected where needed. The report is refreshed annually, with interim updates when material events occur, and a final pre-delivery review is completed so clients receive the most current view available at the time of purchase.

Mordor Intelligence's Pharmaceutical Artificial Intelligence Market Sizing Compared With Other Published Estimates

Published market numbers for AI in pharmaceuticals often vary because different authors count different workflows, and they also treat software, services, and adjacent spending categories in different ways. Timing can also push values apart, since some figures reflect older adoption assumptions and others capture the latest jump in pilots moving into larger deployments.

The biggest gap drivers we see are whether a study includes generic enterprise AI work that is not pharma-specific, whether AI hardware is bundled into the total, and how subscription pricing is handled as capabilities improve year to year. Differences also show up when one estimate relies mostly on historical license fees, or when currency conversion timing and inflation handling are not updated, which can shift the headline number materially for a fast-growing market.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.35 B (2025) | |

| Global Industry Publisher A | USD 3.80 B (2025) | Uses a narrower definition that leans toward R&D-only tooling and does not clearly account for scaled use in manufacturing, supply-chain, and pharmacovigilance operations, which lowers the total. |

| Policy Journal B | USD 2.92 B (2024) | Anchors sizing on a prior-year value with limited transparency on offering mix, and it does not state how pricing progression is updated as cloud subscriptions and model capability improve. |

The spread is mainly explained by what gets counted as pharma-specific AI and how quickly pricing and adoption are refreshed in a fast-moving category. When hardware and generic AI services are kept out, and use cases across discovery, development, and downstream operations are modeled with updated adoption checks, the result lands closer to the 2025 value shown by Mordor Intelligence.

Key Questions Answered in the Report

What is the projected value of the artificial intelligence in pharmaceutical market by 2031?

The market is forecast to reach USD 34.95 billion by 2031 at a 41.52% CAGR over 2026-2031.

Which technology segment will grow fastest through 2031?

Generative AI architectures built on diffusion and transformer models are expected to expand at 43.21%, outpacing classical machine learning.

Why are on-premise deployments rising despite cloud dominance?

Data sovereignty laws in Europe, China, and India require local genomic processing, pushing companies toward on-premise or sovereign-cloud clusters.

Which application area shows the highest CAGR?

Pharmacovigilance and safety monitoring will post a 43.65% CAGR, driven by real-time adverse-event detection mandates.

How fragmented is the competitive landscape?

No single vendor holds more than 8%, and the top 20 players control roughly 45%, yielding a moderate fragmentation score of 5.

What major regulatory milestone occurred in December 2025?

The FDA qualified AIM-NASH, marking the first machine-learning biomarker accepted for use in drug-development programs.

Page last updated on: