AI In Pharmaceutical Quality Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

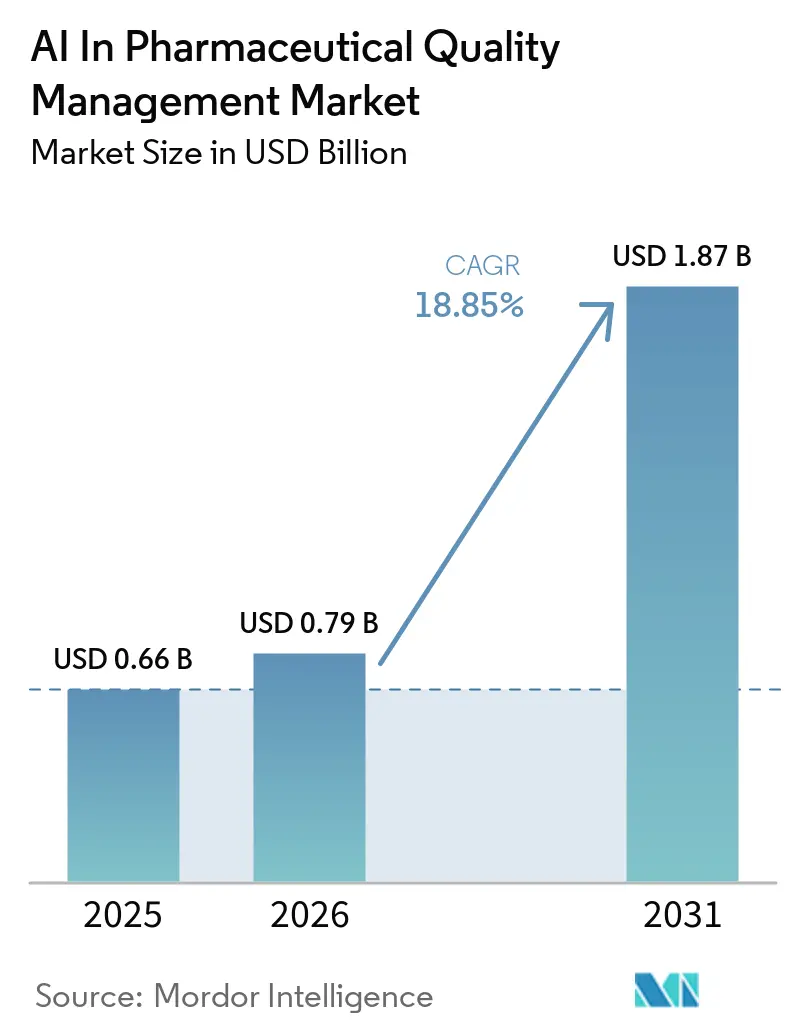

| Market Size (2026) | USD 0.79 Billion |

| Market Size (2031) | USD 1.87 Billion |

| Growth Rate (2026 - 2031) | 18.85% CAGR |

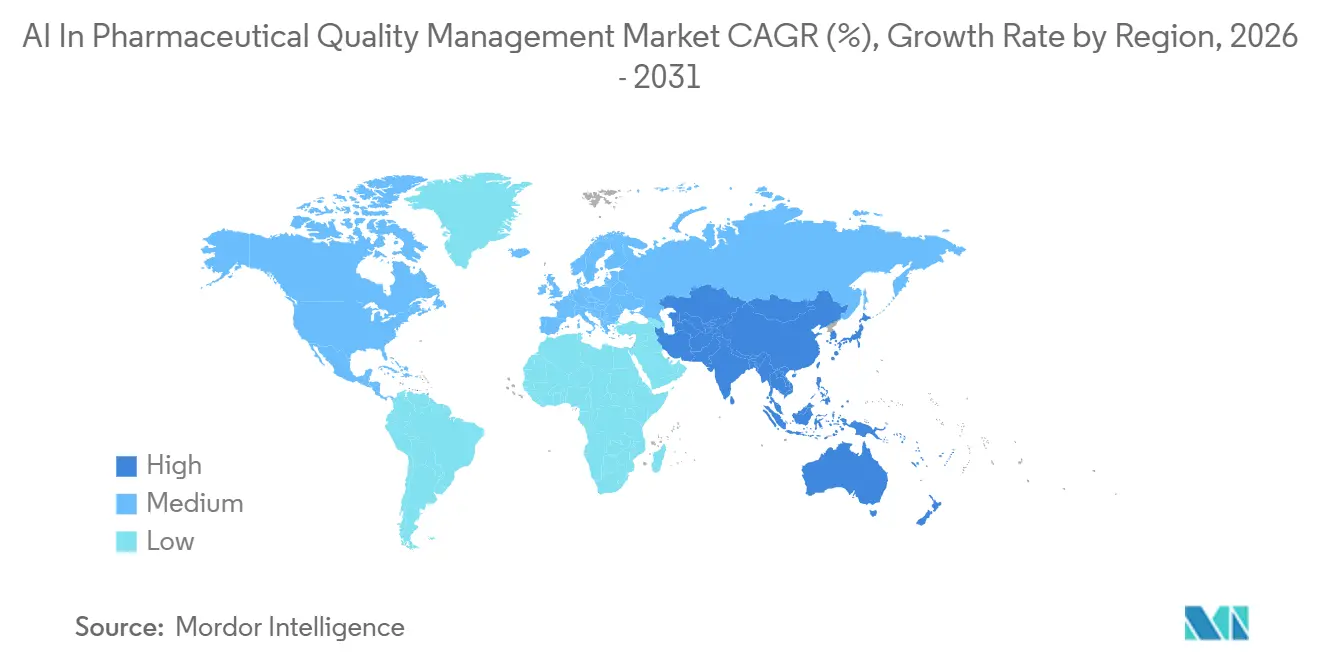

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Pharmaceutical Quality Management Market Analysis by Mordor Intelligence

The AI In Pharmaceutical Quality Management Market size is expected to grow from USD 0.66 billion in 2025 to USD 0.79 billion in 2026 and is forecast to reach USD 1.87 billion by 2031 at 18.85% CAGR over 2026-2031.

The market is moving away from paper-based and reactive quality systems toward real-time, AI-supported control that is built into daily manufacturing and compliance activity. The FDA’s Computer Software Assurance guidance, finalized in September 2025 and updated in February 2026 to align with the Quality Management System Regulation, has made adoption easier in GxP software environments and has shortened validation cycles versus older Computer System Validation practices. At the same time, the gap between the broad value AI could create in life sciences and the small share of organizations that have achieved meaningful value at scale is leaving room for further software spending in the near term. The joint international principles on good AI practice in drug development are also raising the standard for model governance, which is pushing buyers to focus more on explainability, documentation, and human oversight before they scale deployments. These same governance demands are slowing some decisions, but they are also strengthening the long-term case for validated AI infrastructure across the AI in pharmaceutical quality management market.

Key Report Takeaways

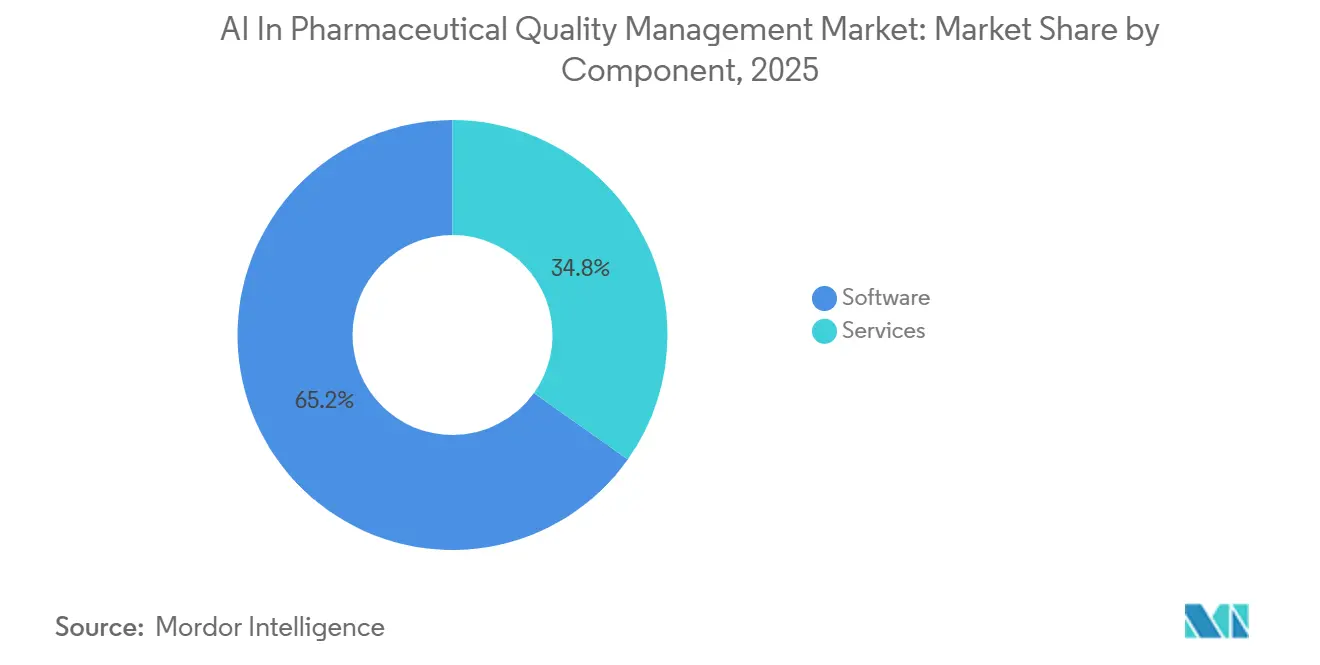

- By component, software held 65.2% of the AI in pharmaceutical quality management market size in 2025, while services grew faster than the overall market at 19.9% through 2031.

- By deployment model, cloud held the largest share in 2025, while on-premises recorded the fastest projected growth at 20.1% through 2031.

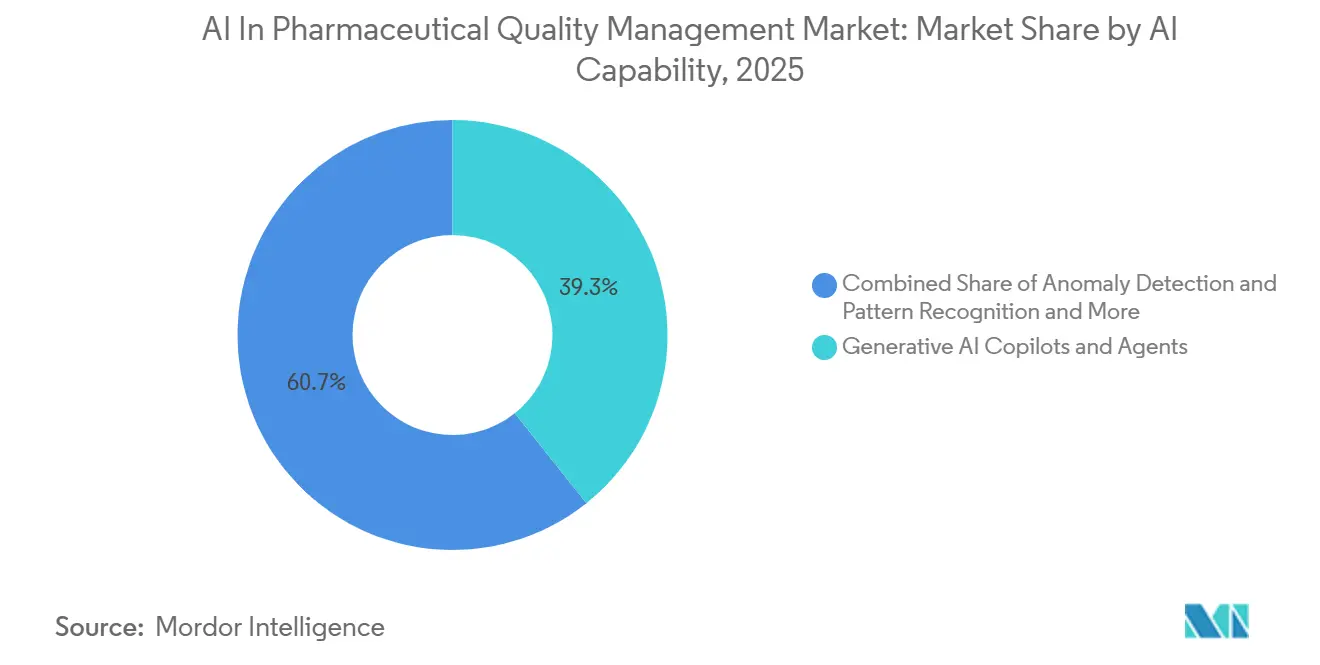

- By AI capability, generative AI copilots and agents led with 39.3% share in 2025, while anomaly detection and pattern recognition expanded at the fastest rate, though a segment CAGR was not stated in the draft.

- By end user, pharmaceutical companies accounted for the largest share in 2025, while CDMOs and CMOs posted the highest projected CAGR at 19.3% through 2031.

- By geography, North America held 38.2% of the AI in pharmaceutical quality management market share in 2025, while Asia-Pacific recorded the fastest projected CAGR at 19.4% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Pharmaceutical Quality Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Automation Of Deviation, CAPA, And Investigation Workflows | +5.2% | Global, with highest density in North America and Western Europe | Short term (≤ 2 years) |

| Rising Demand For Predictive Quality Risk Detection Across GMP Operations | +4.3% | Global, early adoption concentrated in North America, Germany, and Japan | Medium term (2-4 years) |

| Need To Reduce Batch Review, Release, And APQR Cycle Times | +3.5% | Global, with high urgency in India, China, and CDMO-heavy markets | Short term (≤ 2 years) |

| CSA-Led Acceptance Of AI-Enabled Validation Approaches In GxP Systems | +2.8% | North America and EU, with spillover to APAC and MEA | Medium term (2-4 years) |

| Multi-Site Quality Signal Mining Across QMS, MES, LIMS, And ERP Data | +2.1% | Global, with highest activity in multi-site pharma and CDMO operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Automation Of Deviation, CAPA, And Investigation Workflows

Managing deviations and CAPAs still absorbs 4% to 6% of total resources at a life science manufacturing site, and legacy workflows often extend investigations to 45 to 90 days. The AI in pharmaceutical quality management market is gaining momentum here because AI-assisted deviation classification, root-cause research, and draft preparation are cutting documentation time by 40% to 60% and improving triage speed by 15% to 30% in reported deployments[1]Hovsep Kirikian, “AI-Enabled QMS: How Deviation and CAPA Workflows Are Changing in 2026,” USDM, usdm.com. These gains matter beyond speed because more consistent CAPA records make it easier to compare quality signals across sites and detect recurring process failures that isolated site teams can miss. Astellas Pharma’s April 2026 deployment of a seven-agent AI setup for deviation processing across its network reported a 67% reduction in investigation workload and an estimated 980 monthly hours recovered at full rollout. Regulatory expectations under 21 CFR Part 11, ICH Q10, and GAMP 5 are keeping human review and audit trails central, which is shaping how these tools are configured and approved.

Rising Demand For Predictive Quality Risk Detection Across GMP Operations

Predictive quality risk detection is becoming one of the clearest reasons companies are investing in the AI in pharmaceutical quality management market, because it helps teams identify batch risk before conventional in-process testing reveals the problem. A 2025 study in Scientific Reports showed that deep learning models predicting critical quality attributes from process parameters achieved R² values above 0.9 and reduced out-of-specification batches by 18% over 3 production cycles. In sterile fill-finish settings, one deployment cited in the draft produced a 12% reduction in batch rejections and stronger audit traceability, which supports the case for using AI in high-control environments. The FDA’s internal Project Elsa, scaled agency-wide by January 2026, is reinforcing this shift because regulators can now scan electronic records rapidly to target high-risk inspections. A 2026 Journal of Pharmaceutical Innovation study that modeled FDA Form 483 data also found data integrity and CAPA effectiveness to be the strongest predictors of repeat regulatory exposure, which ties predictive quality investment directly to inspection risk.

Need To Reduce Batch Review, Release, And APQR Cycle Times

Batch review, batch release, and Annual Product Quality Review work remain some of the most visible time burdens in the AI in pharmaceutical quality management market. In one GMP-compliant deployment, automated batch record review reduced documentation time from 4 hours to 45 minutes per batch and helped prevent 9 potential batch losses in 6 months, saving EUR 340,000, or USD 375,000. For APQR, generative AI tools that gather information from LIMS, MES, and QMS are shortening work that once took 8 to 12 weeks into a matter of days. The Shionogi and Hitachi solution launched in February 2026 also showed a 50% reduction in clinical study report preparation time, which shows how faster document handling can improve broader product lifecycle decisions. This matters even more for CDMOs because faster release cycles improve throughput across multiple client schedules instead of only one internal pipeline.

CSA-Led Acceptance Of AI-Enabled Validation Approaches In GxP Systems

The FDA’s Computer Software Assurance framework changed the economics of validated AI deployment in the AI in pharmaceutical quality management market by replacing heavy documentation with a risk-based approach built on critical thinking. Traditional Computer System Validation often stretched AI rollouts to 6 to 8 months, while CSA-aligned organizations have reported validation timelines as short as 15 days for lower-risk functions. This shift favors companies with stronger data governance and clearer risk assessments, because they can move faster than organizations that still rely on older validation habits. A 2024 GAMP workshop poll cited in the draft found that only 14% of respondents had a strong understanding of CSA, which indicates that training, implementation, and validation services will remain in demand. MasterControl’s July 2025 ISO/IEC 42001 certification also shows that buyers are beginning to look beyond core software functions and ask vendors for formal AI management controls.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GxP Model Validation, Explainability, And Audit-Trail Requirements | -3.1% | Global, most acute in the EU and North America | Medium term (2-4 years) |

| Poor Data Readiness Across Legacy Quality Records And Disconnected Systems | -2.4% | Global, especially pronounced in India, Southeast Asia, and mid-size manufacturers | Long term (≥ 4 years) |

| QA User Trust, Adoption, And Human-In-The-Loop Governance Challenges | -1.8% | Global, with highest cultural friction in Japan and mature European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

GxP Model Validation, Explainability, And Audit-Trail Requirements

Model explainability still raises deployment cost in the AI in pharmaceutical quality management market because quality teams need traceability, documented controls, and credible human review before AI can be used at scale. The draft notes that EMA’s draft Annex 22 limits probabilistic and adaptive models in critical GMP use cases and keeps generative AI in supervised non-critical roles, which is splitting vendor roadmaps into compliant and non-compliant paths. The FDA’s April 2026 warning letter to Purolea Cosmetics Lab also showed that AI-generated manufacturing records cannot replace expert review that can identify missing regulatory elements. A 2026 analysis cited in the draft said that AI systems need thorough tracking with complete traceability inside the quality system, which adds model version control, input and output logging, and drift monitoring to the normal validation burden. These requirements are not temporary, so vendors that cannot demonstrate clear auditability will find it harder to compete across the AI in pharmaceutical quality management market.

Poor Data Readiness Across Legacy Quality Records And Disconnected Systems

Poor data readiness remains a structural barrier in the AI in pharmaceutical quality management market because older quality records are often fragmented across ERP, LIMS, MES, and scanned or handwritten archives. The draft notes that 47% of pharma digital transformation programs cite data quality as the main obstacle and that weak data quality carries large annual costs, which shows why software alone cannot solve the problem. Rare deviation events also create a training challenge because models built mainly on normal operating data can underperform on the unusual failures that matter most to quality teams[2]Jesper Madsen Wagner and Valentin Ioan Dascalescu, “Harnessing AI in GxP Environments: Innovation, Compliance, and Trust,” NIRAS, niras.com. The ALCOA+ requirement for traceable data lineage then raises the preparation burden further because training datasets must connect back to approved source records before they can support validated use.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominates but Services Scale Fastest

Software retained 65.2% of AI in pharmaceutical quality management market size in 2025, which reflects the strong position of enterprise eQMS, AI-enhanced LIMS, and deviation management platforms in large pharma accounts. The AI in pharmaceutical quality management market remains software-led because major manufacturers are embedding copilots for CAPA drafting, document summaries, and regulatory gap checks inside long-term platform contracts. These subscriptions are not only about automation, because buyers also want one validated environment that can connect deviation handling, training, document control, and investigation records. That makes software the foundation of daily digital quality work across the AI in pharmaceutical quality management market.

Services are growing faster than the overall market at 19.9% through 2031, because software alone does not solve CSA adoption, data preparation, retraining, or ongoing model governance. The AI in pharmaceutical quality management industry still has a wide knowledge gap around CSA, which supports demand for external implementation and validation help. Managed services are also expanding into drift monitoring, periodic re-validation, and audit-trail maintenance as buyers ask for support beyond the initial launch. This is especially relevant for companies moving from older CSV practices to risk-based assurance models that need new documentation habits and governance routines. As a result, service revenues are scaling alongside software deployments rather than trailing them.

By Deployment Model: Cloud Leads While On-Premises Captures Fastest Growth

Cloud-based deployment held the largest share in 2025, while on-premises was projected to expand at 20.1% through 2031. in pharmaceutical quality management market continues to rely on cloud infrastructure because vendors can provide compliance documentation and controlled environments that simplify qualification for many buyers. Hybrid deployment remains relevant for organizations that need to connect newer digital tools with legacy plants and older record architectures. Cloud therefore still anchors the mainstream deployment base even as the mix is shifting.

On-premises growth is faster at 20.1% through 2031 because data residency, validation control, and audit-trail ownership carry more weight in high-risk GxP settings. The draft links this shift to European and APAC demand for local inference, especially where GDPR, localized regulatory requirements, or plant-specific governance rules limit comfort with multi-tenant environments. This is creating a more balanced deployment pattern in the AI in pharmaceutical quality management market than a standard enterprise software category would normally show. Buyers are not rejecting cloud, but they are drawing a clearer line between lower-risk quality tasks and the highest-risk workflows that need tighter local control. That distinction is likely to keep hybrid and on-site models relevant for years.

By AI Capability: Generative AI Leads but Anomaly Detection Scales Sharpest

Generative AI copilots and agents held 39.3% of AI in pharmaceutical quality management market size in 2025, making them the largest capability segment in the draft. The AI in pharmaceutical quality management market adopted these tools early because they fit naturally into document-heavy work such as CAPA narratives, SOP support, APQR summaries, and regulatory content preparation. They also offer a faster path to value because they support QA teams without removing the human review that regulators still expect. Predictive analytics, risk scoring, and NLP remain important adjacent tiers, especially where companies are trying to automate review of large document sets or inspection patterns.

Anomaly detection and pattern recognition are scaling faster at 19.2% through 2031 because manufacturers want earlier visibility into process drift, batch deviation, and visual defect signals. A CNN-based visual inspection deployment cited in the draft improved defect detection from 94% to 99.7% and cut false rejects by 60%, which shows why inspection and process monitoring use cases are gaining traction. Körber’s B.R.AI.N platform and PAS-X K.AI integration also show that computer vision and MES-linked intelligence are advancing inside regulated production environments rather than staying in pilot mode. The AI in pharmaceutical quality management industry is therefore broadening from document assistance toward real-time operational monitoring. Over time, the balance between copilots and anomaly tools will depend on how quickly plants improve data quality and validation readiness.

By End User: Pharma Companies Anchor Revenue, CDMOs Drive Growth

Pharmaceutical companies accounted for the largest share of 2025 end-user revenue, while CDMOs and CMOs were projected to grow at 19.3% through 2031. The AI in pharmaceutical quality management market remains anchored by large pharma because multi-site operations, frequent inspections, and broad product portfolios create the biggest immediate need for scalable quality oversight. The draft also ties large-pharma demand to the need to reduce repeat FDA 483 exposure through better data integrity and CAPA effectiveness. Biotechnology companies form the next tier, with adoption rising in biologics inspection and batch disposition work that benefits from better document control and visual review.

CDMOs are growing faster at 19.3% through 2031 because a 483 or warning letter can affect several client programs at once, which turns quality software into a revenue protection tool as much as an efficiency tool. The AI in pharmaceutical quality management industry shows this dynamic clearly, because a contractor can spread one validated quality investment across multiple programs and sites. The February 2026 QMSR deadline also raised urgency for contractors that needed stronger lifecycle risk management and more reliable documentation workflows. This is why end-user growth is not just following company size, but also following the economic cost of shared compliance exposure. Other end users, including academic and specialty organizations, still represent a smaller part of the mix.

Geography Analysis

North America held 38.2% of AI in pharmaceutical quality management market share in 2025, which kept it in the leading regional position. The AI in pharmaceutical quality management market is strongest in this region because FDA activity is dense and manufacturers face a more visible enforcement and governance environment. The draft points to Project Elsa and the FDA’s broader digital inspection posture as signals that U.S. companies need stronger pre-inspection readiness across electronic records. The White House direction on strategic active pharmaceutical ingredient reserves also supports additional quality system spending by facilities expecting closer scrutiny and greater supply assurance obligations. Canada and Mexico add support through MDSAP-linked compliance demand and manufacturing expansion, but the core regional advantage still comes from the United States and its risk-based assurance framework.

Europe was the second-largest regional market, and its demand profile is being shaped by a more structured governance-first approach. The AI in pharmaceutical quality management market in Europe is being influenced by draft Annex 22, the revised Annex 11 discussion, and the EU AI Act, all of which raise the compliance threshold for deployable systems. Germany stands out through the Qua²ntum project led by Fraunhofer IPT with Sartorius, Groninger, and OCTUM, which is building QMS frameworks for AI in regulated settings. Spain, Italy, and France are also moving forward through generics clusters that compete heavily on operational quality performance.

Asia-Pacific was projected to expand at 19.4% through 2031, which made it the fastest-growing region in the draft. The AI in pharmaceutical quality management market is benefiting here from China’s April 2026 AI plus drug regulation roadmap, which set out targets for intelligent inspection, AI-assisted dossier review, and multi-source risk aggregation through 2030. India is also moving from reactive data integrity control toward predictive quality models under its Pharma 4.0 push, while Japan is building a credibility assessment framework for AI and is improving structured data availability through eCTD 4.0 adoption from 2026. South Korea’s move toward AI-based drug approval review in 2026 adds another regional tailwind, while MEA and South America remain earlier-stage markets led mainly by multinational standardization efforts and selective geographic expansion[3]Katrina Ortolan, “2026 Life Sciences Regulatory Updates: Asia,” PSC Software, pscsoftware.com.

Competitive Landscape

The AI in pharmaceutical quality management market is moderately fragmented, with large eQMS vendors and AI-native firms competing across enterprise, mid-market, and emerging biopharma accounts. Veeva Systems, IQVIA, MasterControl, ComplianceQuest, and Dassault Systèmes BIOVIA hold broad enterprise visibility, while Leucine, Dot Compliance, Qualio, and Scilife are competing more aggressively in focused or growing accounts. The central competitive shift is platform consolidation, because buyers want deviation management, document control, CAPA, and training on one data model rather than across separate tools. That preference is strengthening vendors that can embed AI directly into validated workflows instead of positioning it as a separate add-on. It is also raising the importance of explainability and governance, which means product design now carries as much weight as brand recognition across the AI in pharmaceutical quality management market.

Veeva’s release of AI agents across its applications, including quality event agents in Vault, is one of the clearest examples of an incumbent extending application-specific AI inside an already validated platform. MasterControl’s July 2025 ISO/IEC 42001 certification is another strategic move, because it gives the company a formal governance credential that buyers can use in vendor evaluation. Körber Pharma’s B.R.AI.N inspection platform and PAS-X K.AI integration show a different route, where shop-floor inspection and MES-linked intelligence are being combined into a broader regulated production stack. These moves show that competition is spreading across software depth, governance readiness, and production-level integration rather than price alone.

White space remains in multi-site quality signal aggregation, especially for CDMOs that must manage different client quality agreements on shared infrastructure. Leucine and Clinplex are early examples of firms trying to address that gap with compliance intelligence shaped around contractor workflows. Smaller providers that still treat validated AI as optional are more exposed, because buyers increasingly view governance capability as a baseline requirement. As this continues, the competitive field in the AI in pharmaceutical quality management market is likely to separate more clearly between full-platform vendors with strong governance and narrower tools with limited deployment scope.

AI In Pharmaceutical Quality Management Industry Leaders

MasterControl

Veeva Systems

Dassault Systèmes (BIOVIA)

AmpleLogic

Honeywell / Sparta Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: China's NMPA published its "Implementation Opinions on 'Artificial Intelligence + Drug Regulation,'" establishing a national AI roadmap for pharmaceutical supervision through 2030, encompassing intelligent inspection, AI-assisted dossier review, and multi-source quality risk signal aggregation for high-risk products including vaccines and biologics.

- April 2026: Astellas Pharma and Microsoft completed a proof-of-concept for a seven-agent AI system for deviation processing across 3 research institutes and 5 production sites, achieving a 67% reduction in investigation workload, approximately 980 hours per month at full global deployment.

- February 2026: Shionogi & Co. and Hitachi launched a generative AI solution for pharmaceutical regulatory document creation in Japan, reducing clinical study report drafting time by 50% and clinical trial protocol preparation by 20%, with the solution licensed by Shionogi to Hitachi for commercial distribution.

Global AI In Pharmaceutical Quality Management Market Report Scope

As per the scope of the report, AI in pharmaceutical quality management refers to the application of artificial intelligence technologies to enhance, optimize, and automate the processes involved in ensuring the quality, safety, and efficacy of pharmaceutical products.

The segmentation for the AI in pharmaceutical quality management market is categorized by component, deployment model, AI capability, end user, and geography. By component, the market is divided into software and services. By deployment model, it is segmented into cloud-based, on-premises, and hybrid. By AI capability, the categories include generative AI copilots and agents, predictive analytics and risk scoring, NLP/document intelligence, anomaly detection and pattern recognition, recommendation engines and root-cause guidance, and computer vision for quality inspection. By end user, the market is segmented into pharmaceutical companies, biotechnology companies, CDMOs/CMOs, and other end users. By geography, the segmentation includes North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Generative AI Copilots & Agents |

| Predictive Analytics & Risk Scoring |

| NLP / Document Intelligence |

| Anomaly Detection & Pattern Recognition |

| Recommendation Engines & Root-Cause Guidance |

| Computer Vision for Quality Inspection |

| Pharmaceutical Companies |

| Biotechnology Companies |

| CDMOs / CMOs |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By AI Capability | Generative AI Copilots & Agents | |

| Predictive Analytics & Risk Scoring | ||

| NLP / Document Intelligence | ||

| Anomaly Detection & Pattern Recognition | ||

| Recommendation Engines & Root-Cause Guidance | ||

| Computer Vision for Quality Inspection | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| CDMOs / CMOs | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving adoption of AI in pharmaceutical quality management?

The main push is the need to automate deviation handling, CAPA work, batch review, and predictive risk detection, while also meeting stronger regulatory expectations around digital quality systems.

How large could this space become by 2031?

The AI in pharmaceutical quality management market is forecast to reach USD 1.87 billion by 2031 from USD 0.79 billion in 2026, at an 18.85% CAGR over 2026-2031.

Which component category leads revenue today?

Software leads the mix, holding 65.2% share in 2025, because eQMS, AI-enhanced LIMS, and deviation management platforms are being embedded into long-term quality operations.

Why are CDMOs adopting these tools faster than some other users?

CDMOs and CMOs are projected to grow at 19.3% through 2031 because a single compliance issue can affect multiple client programs, so AI helps protect both revenue and operating continuity.

Which region is growing the fastest?

Asia-Pacific is the fastest-growing region, with a projected 19.4% CAGR through 2031, supported by regulatory and digital quality initiatives in China, India, Japan, and South Korea.

What is the biggest barrier to broader deployment?

Validation, explainability, audit-trail requirements, and weak data readiness remain the biggest barriers, because regulated AI needs traceable records, strong lineage, and credible human oversight.

Page last updated on: