AI In Drug Screening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

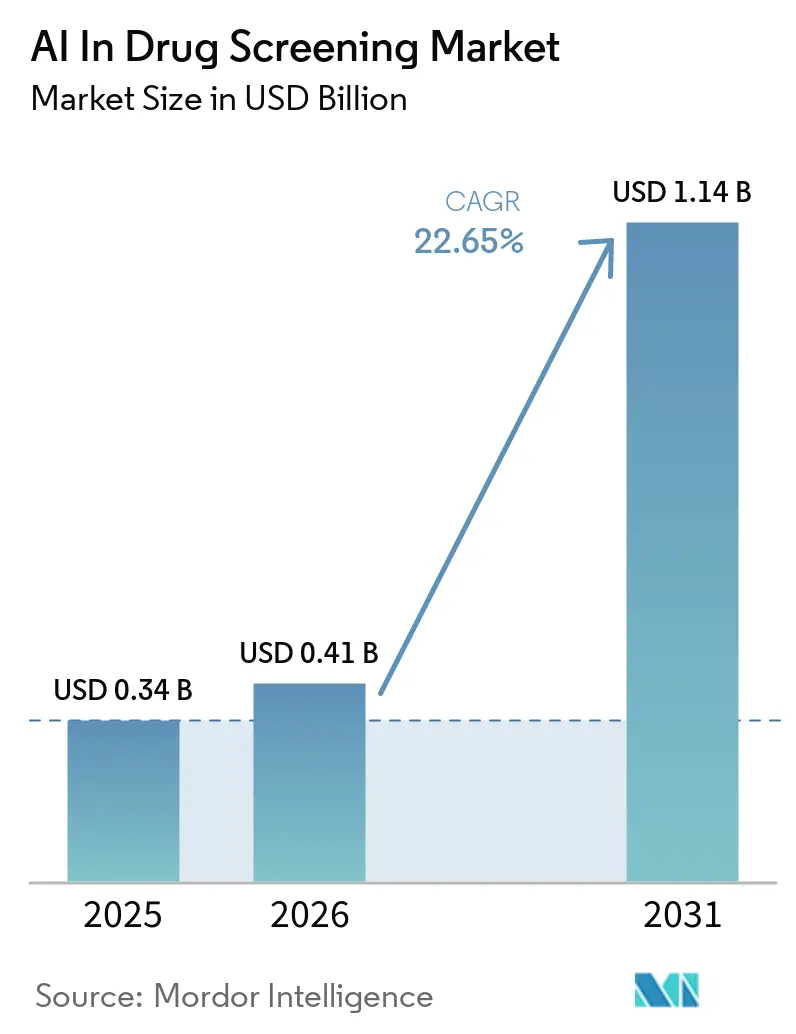

| Market Size (2026) | USD 0.41 Billion |

| Market Size (2031) | USD 1.14 Billion |

| Growth Rate (2026 - 2031) | 22.65% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Drug Screening Market Analysis by Mordor Intelligence

The AI In Drug Screening Market size is expected to grow from USD 0.34 billion in 2025 to USD 0.41 billion in 2026 and is forecast to reach USD 1.14 billion by 2031 at 22.65% CAGR over 2026-2031.

The Artificial Intelligence (AI) in drug screening market is moving from pilot use toward core discovery infrastructure as pharmaceutical R&D teams treat AI as a working part of target discovery, screening, and optimization rather than as an experimental add-on. Traditional drug development still carries an average cost of USD 2.6 billion per approved molecule, timelines of 10 to 15 years, and a 90% clinical failure rate, which keeps the cost-efficiency case for adoption front and center. AI-enabled pipelines have already reduced some preclinical phases to 12 to 18 months and delivered cost reductions of up to 40%, which makes return on investment easier for both large pharmaceutical companies and emerging biotech platforms to justify. Growth is also being reinforced by larger multi-omics datasets, stronger foundation models, more platform licensing activity, and rising institutional funding for AI-native drug design engines, even as model transfer, explainability, and documentation standards remain active constraints. The AI in drug screening market therefore continues to show strong expansion potential because efficiency gains, better target enablement, and tighter pharma-tech collaboration are advancing faster than the main structural bottlenecks.

Key Report Takeaways

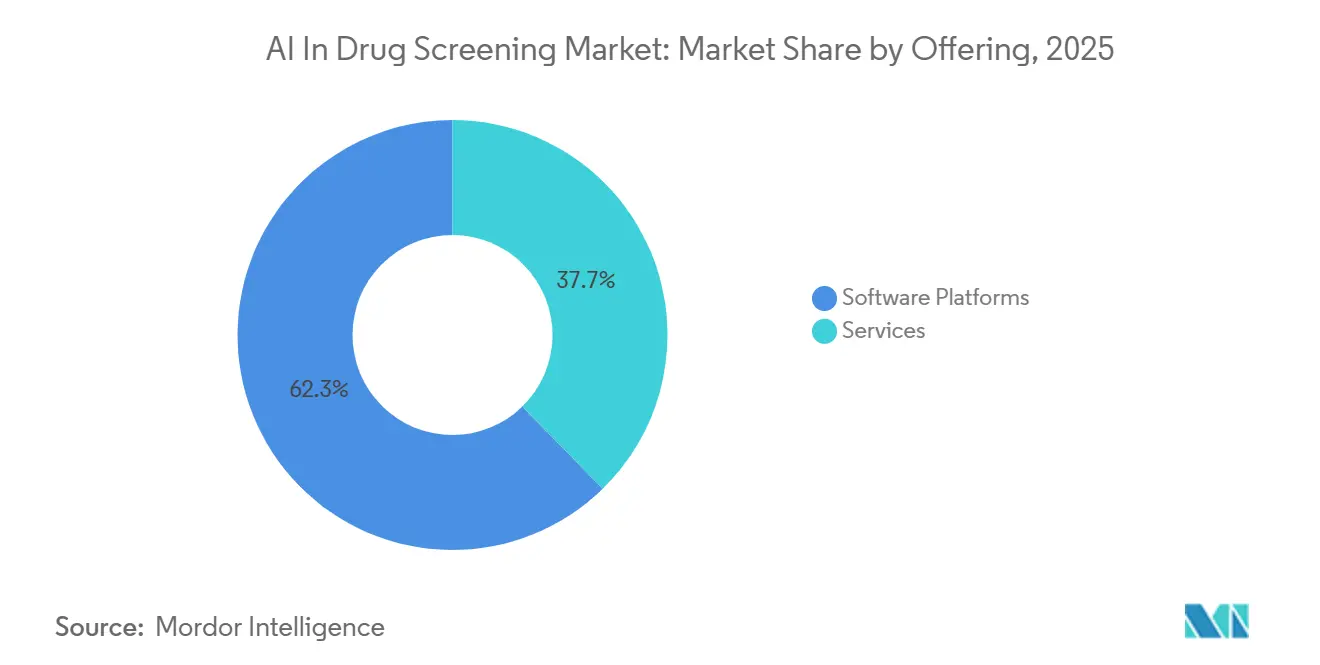

- By offering, software platforms held 62.31% of the market in 2025, while services are projected to expand at a 27.38% CAGR through 2031.

- By technology, machine learning accounted for 46.24% of the market in 2025, while deep learning and generative AI are expected to have the highest CAGR at 28.52% through 2031.

- By application, target identification and validation captured 28.52% of the market in 2025, while hit identification and virtual screening are forecast to record a 29.25% CAGR through 2031.

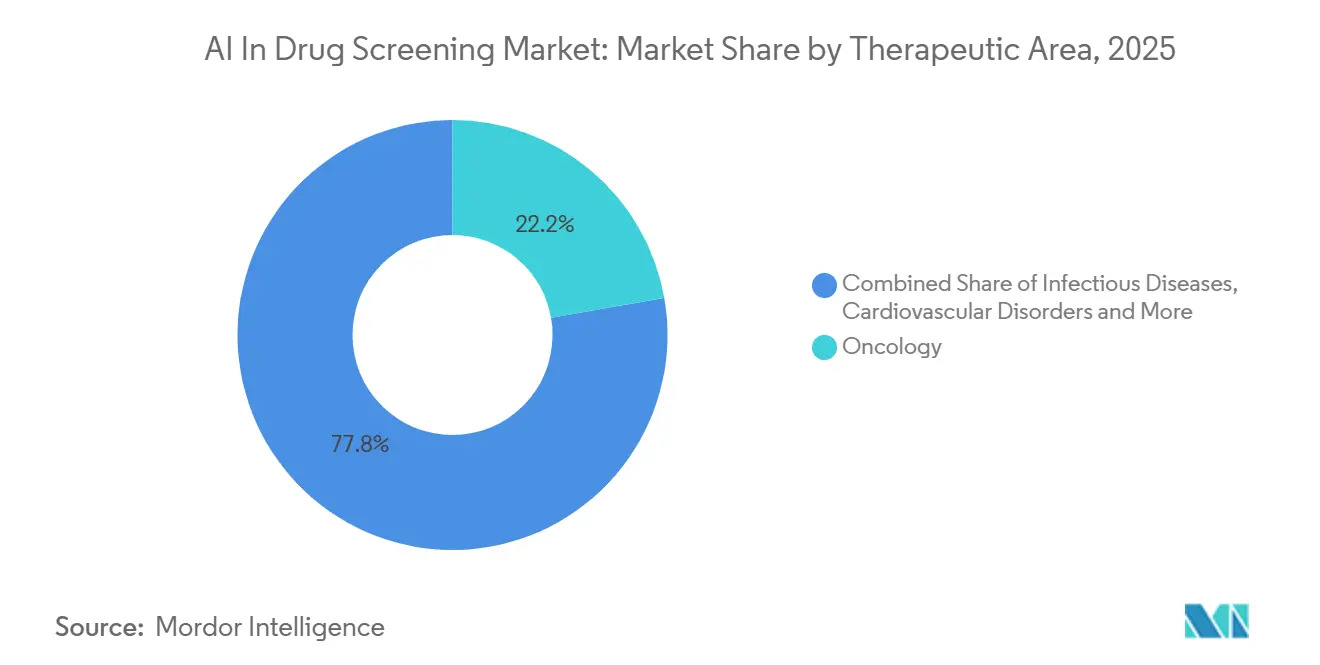

- By therapeutic area, oncology led with 22.24% of the market in 2025, while infectious diseases are expected to advance at a 30.83% CAGR through 2031.

- By end user, pharmaceutical and biotechnology companies represented 65.52% of the market in 2025, while CROs and CDMOs are projected to have a 28.35% CAGR through 2031.

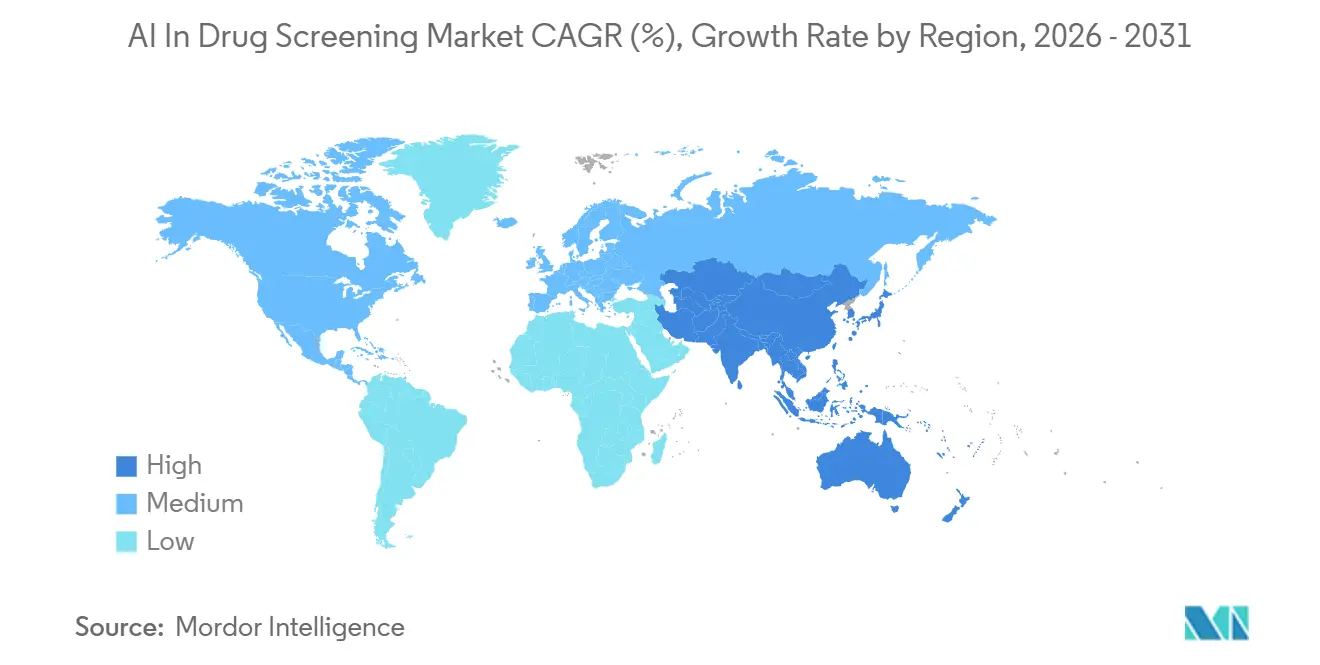

- By geography, North America held 43.24% of AI in the drug screening market share in 2025, while Asia-Pacific is expected to have a 26.53% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Drug Screening Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pressure To Cut Discovery Cost And Cycle Time | +4.0% | Global | Short term (≤ 2 years) |

| Expanding Multi-Omics And Clinical Training Datasets | +2.8% | North America & Asia-Pacific | Medium term (2-4 years) |

| Rising Pharma-Tech Partnerships And Licensing Activity | +3.2% | North America & Europe | Medium term (2-4 years) |

| Better Generative AI And Molecular Design Models | +4.5% | Global | Medium term (2-4 years) |

| AlphaFold-Scale Structure Maps Improving Target Enablement | +3.0% | Global | Short term (≤ 2 years) |

| Benchmark-Grade ADMET And Protein-Ligand Datasets Improving Model Reliability | +2.2% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pressure to Cut Discovery Cost and Cycle Time

Pharmaceutical pipelines continue to face a structural efficiency problem because average drug development cost still approaches USD 2.6 billion, timelines often exceed 10 years, and 90% of clinical candidates fail before approval. The AI in drug screening market is benefiting directly from this pressure because buyers now evaluate AI against a clear cost and time benchmark rather than against experimental novelty. Some AI-driven workflows have already reduced selected discovery stages to 12 to 18 months and delivered cost reductions of up to 40% against traditional methods. That compression is changing how early research budgets are assigned, with more capital moving toward platform subscriptions, model access, and compute infrastructure instead of only physical compound library expansion. The result is a stronger commercial case for platforms that can surface safety, efficacy, and screening signals earlier in the discovery cycle.

Better Generative AI and Molecular Design Models

The AI in drug screening market is also being lifted by a step change in model capability, especially in early lead generation where generative systems now produce outputs that can compete with parts of physical screening. Chai Discovery reported that its Chai-2 model achieved a near-20% experimental hit rate in de novo antibody design, a major increase over the prior 0.1% computational benchmark. VantAI launched Neo-1 in March 2025 as an atomistic foundation model that combines de novo molecular generation with multimodal structure prediction in one architecture, which broadens the range of tractable targets for platform users. Schrödinger has also positioned its Bunsen agentic AI co-scientist for early access in summer 2026, showing how platform vendors are moving from single-task models toward systems that can execute larger parts of discovery workflows. As these tools improve faster than wet-lab synthesis capacity, the next investment cycle is shifting toward automated chemistry and validation infrastructure, a pattern reinforced by Profluent’s USD 2.25 billion collaboration with Eli Lilly for AI-designed recombinases.

AlphaFold-Scale Structure Maps Improving Target Enablement

AlphaFold-scale structure prediction is widening the target universe that the AI in drug screening market can address because structural coverage now extends beyond simpler protein models into more complex interaction settings. AlphaFold 3 expanded prediction to protein-drug, protein-DNA, and protein-RNA interactions, which materially improves early target assessment for programs that previously lacked usable structural context. The EMBL-EBI and DeepMind collaboration has already added predictions for 30 million protein complexes to the AlphaFold Database, including 1.7 million high-confidence homodimer predictions[1]EMBL, “Millions of Protein Complexes Added to AlphaFold Database Shed Light on How Proteins Interact,” EMBL, embl.org. AF2BIND, published in Nature Methods in 2026, used pretrained AlphaFold features to identify de novo binding sites across the human proteome and generated a database of previously unknown sites in disease-relevant proteins. This is shortening target enablement cycles from years toward months in some workflows and is increasing the amount of screening work that AI platforms can realistically take on.

Rising Pharma-Tech Partnerships and Licensing Activity

The AI in drug screening market is seeing a clear shift from exploratory pilots toward larger licensing and collaboration structures that treat AI outputs as commercial assets rather than experimental support tools. XtalPi and DoveTree Medicines announced a collaboration valued at up to USD 5.99 billion in August 2025, including USD 51 million upfront and USD 49 million in additional near-term payments, which shows the scale of capital now being committed to AI and robotics-driven pharmaceutical R&D. Profluent’s April 2026 partnership with Eli Lilly for AI-designed recombinases added another large example, with the agreement valued at USD 2.25 billion. Owkin’s April 2026 three-year K Pro license agreement with AstraZeneca shows that enterprise customers are also buying higher-level AI scientist environments that support multi-step decision making across drug development teams. These structures deepen data exchange between pharmaceutical companies and platform vendors, which strengthens the training advantage of firms that already control broad proprietary assay and workflow datasets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Siloed Data, Privacy Constraints, And Poor Interoperability | -2.1% | Global | Short term (≤ 2 years) |

| Limited Explainability And Wet-Lab Translation Confidence | -1.8% | Global | Medium term (2-4 years) |

| Rising FDA And EMA Documentation Expectations For AI-Enabled Evidence | -1.2% | North America & Europe | Medium term (2-4 years) |

| Noisy Public Datasets And Weak Scaffold Transfer In Real-World Screening | -0.9% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Siloed Data, Privacy Constraints, and Poor Interoperability

The AI in drug screening market still faces a core data problem because many public ADMET datasets are assembled from 20 to 50 separate papers that use different experimental conditions and show weak reproducibility across studies. Collaborative Drug Discovery reported that ADMET models can reach R² near 0.9 on internal test sets but fall to around 0.75 on external benchmarks when assay methods differ, which shows that transfer across organizations is still limited[2]Collaborative Drug Discovery, “Applying Real-World Drug Discovery Experience in the OpenADMET ExpansionRx Blind Challenge,” Collaborative Drug Discovery, collaborativedrug.com. Multi-omics integration adds another layer of friction because genomic, transcriptomic, and proteomic data often sit in separate institutional silos with incompatible metadata and require manual harmonization before cross-study training can begin. This slows model development and also gives a lasting advantage to firms that have already federated large proprietary data assets into usable training environments. As a result, data governance in the AI in drug screening market is becoming just as important as model design for long-term competitive positioning.

Limited Explainability and Wet-Lab Translation Confidence

The AI in drug screening market also remains constrained by the gap between strong in silico predictions and the level of mechanistic explanation that medicinal chemists need before making lead progression decisions. A 2026 benchmark study across five toxicity endpoints found that no single AI tool delivered uniform reliability across all independent datasets, with BBB permeability and nephrotoxicity standing out as difficult areas. That inconsistency keeps confirmatory wet-lab testing in place even for candidates that score well in computational ranking, which reduces part of the cycle-time advantage that supports adoption. Structural issues such as model opacity, sparse data in niche chemical scaffolds, and validation challenges in druggability prediction still affect both target identification and lead optimization workflows. The FDA and EMA reinforced this point in January 2026 when they published 10 guiding principles for AI in medicine development that placed explainability, governance, and human oversight at the center of acceptable practice.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platforms Define Current Revenue Base

Software platforms captured 62.31% of AI in drug screening market size in 2025, which confirms that scalable model access still represents the main commercial format for buyers. The current revenue base favors software because cloud deployment lets drug discovery teams screen very large virtual libraries without a matching increase in laboratory cost. One platform subscription can support multiple programs at the same time, which gives internal R&D groups a more predictable cost structure than project-based service engagements. This model has kept software at the center of the AI in drug screening market while platform buyers continue to test different workflow combinations across target discovery and screening.

Services are the fastest-growing offering segment, with a projected CAGR of 27.38% from 2026 to 2031. This rise reflects stronger outsourcing demand from mid-size biotech firms that do not yet have the internal data, compute, or specialist teams needed to operate full discovery platforms on their own. CROs and CDMOs are responding by adding AI-enabled screening, data interpretation, and bespoke model training into their discovery packages. Over time, the balance in the AI in drug screening market is likely to move toward more service-led value capture as software functionality becomes easier to replicate and differentiation shifts toward integrated workflow execution on client-owned data.

By Technology: Machine Learning Incumbent, Generative AI Gaining Fast

Machine learning held 46.24% of the technology segment in 2025, which reflects its established role across ADMET prediction, property scoring, and quantitative structure-activity relationship modeling in production discovery workflows. In the AI in drug screening market, this installed base matters because machine learning methods are already embedded in day-to-day screening tasks and remain trusted for repeatable scoring functions. They also fit well into existing R&D systems, which lowers switching friction for buyers that want practical gains without rebuilding entire discovery stacks. That installed position explains why machine learning still anchors the current technology mix even as newer model classes gain attention.

Deep learning and generative AI is the fastest-growing technology segment, with a CAGR of 28.52% from 2026 to 2031. Chai Discovery’s Chai-2 model showed a near-20% experimental hit rate in de novo antibody design, which signals that generative systems are becoming viable first-pass screening tools rather than optional design aids. Receptor.AI also reported first-place ranking on 10 of 16 TDC benchmark tasks in 2025 for its ADMET model family, including strong results on DILI, hERG, and CYP450 endpoints. Natural language processing and graph-based methods continue to serve as enabling layers for literature mining and protein-ligand modeling, but the AI in drug screening industry is moving toward multimodal architectures that blur old segment boundaries and push vendors toward full workflow competition.

By Application: Target Identification Anchors Market, Virtual Screening Accelerates

Target identification and validation held 28.52% of the application segment in 2025, making it the largest entry point for commercial deployment. The AI in drug screening market gained early traction here because structure prediction and multi-omics integration improve the first screening decision, where traditional approaches are slow and expensive. Buyers also see high marginal value at this stage because better target selection can prevent weaker programs from moving deeper into the pipeline. That makes target identification a durable anchor application even as downstream use cases scale.

Hit identification and virtual screening is the fastest-growing application area, with a CAGR of 29.25% from 2026 to 2031. AF2BIND expanded the available starting point for screening by identifying previously unknown binding sites across disease-relevant proteins, which directly increases the searchable landscape for platform users. Lead generation and optimization are also benefiting because generative systems can reduce iterative design loops from months to weeks in selected workflows. Drug repurposing, preclinical candidate selection, toxicity prediction, and biomarker-linked companion work are all gaining relevance as the AI in drug screening market expands from single-task deployment toward broader decision support across the full discovery process.

By Therapeutic Area: Oncology Leads, Infectious Diseases Surge on AMR Urgency

Oncology accounted for 22.24% of the therapeutic area segment in 2025, giving it the leading position in current demand. The AI in drug screening market continues to favor oncology because cancer biology has the largest base of annotated clinical and molecular data, well-characterized targets, and an active population of precision-focused discovery programs. Nature Scientific Data published the MLOmics cancer multi-omics database in May 2025, which illustrates the level of benchmarking and data standardization now supporting oncology workflows. This depth of structured evidence helps oncology remain the most commercially mature therapeutic setting for AI-enabled screening.

Infectious diseases is the fastest-growing therapeutic area, with a CAGR of 30.83% from 2026 to 2031. Demand is rising because antimicrobial resistance creates urgent need for faster screening of new peptide and small-molecule candidates against difficult pathogen targets. Nature Machine Intelligence reported in 2026 that the ApexGO framework generated optimized antimicrobial peptides with strong activity against multidrug-resistant A. baumannii in preclinical mouse models. Neurology, psychiatric disorders, cardiovascular disease, metabolic disorders, and immunology remain important mid-tier opportunities, but the AI in drug screening market is seeing the strongest therapeutic momentum where dataset depth and unmet need move together.

By End User: Pharma and Biotech Dominate, CROs Diversify Service Offerings

Pharmaceutical and biotechnology companies accounted for 65.52% of end-user demand in 2025, which confirms that large drug developers still provide the main commercial base. These buyers have the strongest budgets, the widest discovery portfolios, and the clearest incentive to use AI across multiple programs at once. Many are building internal capability while also licensing external platforms, which allows them to combine proprietary datasets with outside model expertise. That combination has made pharmaceutical and biotechnology companies the central demand engine for the AI in drug screening market.

CROs and CDMOs are the fastest-growing end-user segment, with a CAGR of 28.35% from 2026 to 2031. Mid-size biotech firms are pushing this growth because many want AI-enabled discovery support without the fixed cost of building a full internal platform. Service providers are responding by expanding AI-assisted chemistry, screening, and data interpretation as a practical differentiator in outsourced discovery work. Academic institutes and research hospitals remain smaller commercial buyers, but they contribute strongly to open benchmark datasets, new model ideas, and translational workflows that continue to widen the operating scope of the AI in drug screening market.

Geography Analysis

North America held 43.24% of AI in drug screening market share in 2025, which kept it as the largest regional base. The region benefits from the highest concentration of AI-native drug discovery firms, deep venture funding, and close ties between biotech platforms, major pharmaceutical companies, and research institutions. In April 2026, the FDA launched an AI pilot program for drug development that supports real-time trial monitoring and reflects a broader move toward AI-enabled regulatory workflows. The NIH Complement-ARIE program also committed USD 150 million to AI-driven predictive systems that can act as alternatives to animal models, which lowers adoption risk for vendors that need credible validation pathways[3]Federal Register, “FDA AI Pilot Program for Drug Development,” Federal Register, govinfo.gov. Canada and Mexico add useful academic, biotech, and manufacturing links, but the region remains centered on U.S.-based platforms and capital formation.

Europe remains an important center of the AI in drug screening market, with activity increasingly concentrated around the UK, Germany, and Switzerland. The UK stands out in AI-first biotech, and Isomorphic Labs’ USD 2.1 billion Series B in May 2026 showed that very large pools of institutional capital are now backing long-horizon AI drug design platforms. The FDA and EMA jointly issued 10 guiding principles for AI in medicine development in January 2026, which gave European developers a clearer governance framework for explainability, oversight, and data handling EMA. Germany and France provide strong CRO and academic medical center capacity, while Spain and Italy are building momentum through growing biotech clusters and earlier adoption of AI-enabled drug development tools.

Asia-Pacific is the fastest-growing regional segment in the AI in drug screening market, with a CAGR of 26.53% from 2026 to 2031. China and India are the main growth engines because discovery outsourcing capacity, AI adoption in R&D, and platform integration are improving across regional ecosystems. Japan and South Korea add depth through pharmaceutical digitalization efforts and government-backed AI biotech initiatives that strengthen the broader innovation base. Middle East and Africa, supported in part by GCC capital participation in large AI drug design financings, and South America, led by Brazil’s developing CRO network, remain smaller today but still matter for long-term expansion of the AI in drug screening market.

Competitive Landscape

The AI in drug screening market is moderately fragmented, with competition spread across AI-native biotechs, computational chemistry firms, life sciences informatics specialists, and newer agentic platform vendors. No single company defines the category, and differentiation is increasingly tied to the breadth, cleanliness, and exclusivity of proprietary training data rather than to model architecture alone. Capital allocation is signaling a more competitive phase because large financings now favor platforms that can support long development cycles and build defensible data positions. Isomorphic Labs’ USD 2.1 billion Series B in May 2026 is a strong example of this trend because the round backed a full AI drug design engine rather than a narrow point solution. The AI in drug screening market is therefore moving toward consolidation around a smaller group of firms that can combine scale, capital, data access, and platform breadth.

Platform convergence is becoming a defining strategic pattern. Schrödinger’s Bunsen agentic AI co-scientist, expected for early access in summer 2026, shows how vendors are shifting from individual screening tools toward systems that can execute more of the full discovery workflow. Owkin’s three-year K Pro licensing agreement with AstraZeneca adds another example, with enterprise AI scientist tools moving into large commercial development environments rather than staying limited to experimental teams. These moves are widening the customer base beyond highly specialized computational users and are making workflow orchestration a more important source of competitive advantage.

Smaller vendors still have room to challenge incumbents when they solve specific bottlenecks more effectively. Insilico Medicine’s 13th IND clearance in April 2026 for Rentosertib’s inhalation formulation showed repeatable end-to-end execution and gave the company evidence that extends beyond a single proof point. QIAGEN’s 2026 integration of NVIDIA accelerated computing and the BioNeMo platform into its bioinformatics business illustrates how established informatics vendors are protecting installed customer relationships by adding stronger AI capability. The clearest open space remains with CRO-native and workflow-level solutions, where buyers want practical integration, pricing flexibility, and stronger translation from model output to laboratory execution across the AI in drug screening market.

AI In Drug Screening Industry Leaders

Recursion Pharmaceuticals

Schrödinger

Insilico Medicine

BenevolentAI

Atomwise

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: QIAGEN announced at the 2026 BIO-IT World Conference & Expo in Boston that the QIAGEN Digital Insights bioinformatics business and its curated knowledge bases and bioinformatics expertise are integrating NVIDIA accelerated computing and the NVIDIA BioNeMo platform to help researchers use AI more effectively in drug discovery.

- April 2026: Owkin signed a three-year K Pro license agreement with AstraZeneca to develop biopharma AI agents for decision support across drug discovery and competitive intelligence workflows. The agreement integrates Owkin's K Pro multimodal AI Scientist platform within AstraZeneca's IT infrastructure.

Global AI In Drug Screening Market Report Scope

As per the scope of the report, AI in drug screening refers to the use of artificial intelligence technologies to identify and evaluate potential drug candidates efficiently. This involves leveraging machine learning algorithms, data analysis, and predictive modeling to analyze biological, chemical, and pharmacological data.

The segmentation of the AI in drug screening market is categorized by offering, technology, application, therapeutic area, end user, and geography. By offering, the market is divided into software platforms and services. By technology, it includes machine learning, deep learning and generative AI, natural language processing, and other technologies. By application, it covers target identification and validation, hit identification and virtual screening, lead generation and optimization, drug repurposing, preclinical candidate selection and toxicity prediction, and biomarker discovery and companion insights. By therapeutic area, the market is segmented into oncology, infectious diseases, neurology and psychiatric disorders, cardiovascular disorders, metabolic and endocrine disorders, immunology and inflammatory disorders, and other therapeutic areas. By end user, it includes pharmaceutical and biotechnology companies, CROs and CDMOs, academic and research institutes, and hospitals and clinical research networks. By geography, the market is analyzed across North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Software Platforms |

| Services |

| Machine Learning |

| Deep Learning and Generative AI |

| Natural Language Processing |

| Other Technologies |

| Target Identification and Validation |

| Hit Identification and Virtual Screening |

| Lead Generation and Optimization |

| Drug Repurposing |

| Preclinical Candidate Selection and Toxicity Prediction |

| Biomarker Discovery and Companion Insights |

| Oncology |

| Infectious Diseases |

| Neurology and Psychiatric Disorders |

| Cardiovascular Disorders |

| Metabolic and Endocrine Disorders |

| Immunology and Inflammatory Disorders |

| Other Therapeutic Areas |

| Pharmaceutical and Biotechnology Companies |

| CROs and CDMOs |

| Academic and Research Institutes |

| Hospitals and Clinical Research Networks |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software Platforms | |

| Services | ||

| By Technology | Machine Learning | |

| Deep Learning and Generative AI | ||

| Natural Language Processing | ||

| Other Technologies | ||

| By Application | Target Identification and Validation | |

| Hit Identification and Virtual Screening | ||

| Lead Generation and Optimization | ||

| Drug Repurposing | ||

| Preclinical Candidate Selection and Toxicity Prediction | ||

| Biomarker Discovery and Companion Insights | ||

| By Therapeutic Area | Oncology | |

| Infectious Diseases | ||

| Neurology and Psychiatric Disorders | ||

| Cardiovascular Disorders | ||

| Metabolic and Endocrine Disorders | ||

| Immunology and Inflammatory Disorders | ||

| Other Therapeutic Areas | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| CROs and CDMOs | ||

| Academic and Research Institutes | ||

| Hospitals and Clinical Research Networks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of AI in drug screening?

The AI in drug screening market stands at USD 0.41 billion in 2026 and is projected to reach USD 1.14 billion by 2031 at a CAGR of 22.65%.

Why are pharmaceutical companies adopting AI for screening and discovery?

The main reason is efficiency. Traditional drug development can cost USD 2.6 billion per approved molecule, take 10 to 15 years, and still face a 90% clinical failure rate, while selected AI-enabled phases have been reduced to 12 to 18 months with cost reductions of up to 40%.

Which region leads global demand for AI-enabled drug screening tools?

North America led with 43.24% share in 2025, supported by strong biotech density, venture funding, and FDA-backed AI initiatives in drug development.

Which technology is growing the fastest in this field?

Deep learning and generative AI is the fastest-growing technology segment, with a CAGR of 28.52% from 2026 to 2031, as model performance improves in lead design and virtual screening.

Which therapeutic area is creating the strongest growth opportunity?

Infectious diseases is the fastest-growing therapeutic area at a 30.83% CAGR through 2031, while oncology remains the largest current segment with 22.24% share in 2025 because it has deeper datasets and more validated targets.

What is the biggest operational challenge for platform vendors and buyers?

Data interoperability remains the most persistent issue because model performance often weakens when internal training conditions do not match external assay settings, and regulators are also tightening expectations around explainability and governance.

Page last updated on: