AI In Clinical Workflow Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.39 Billion |

| Market Size (2031) | USD 11.60 Billion |

| Growth Rate (2026 - 2031) | 27.90% CAGR |

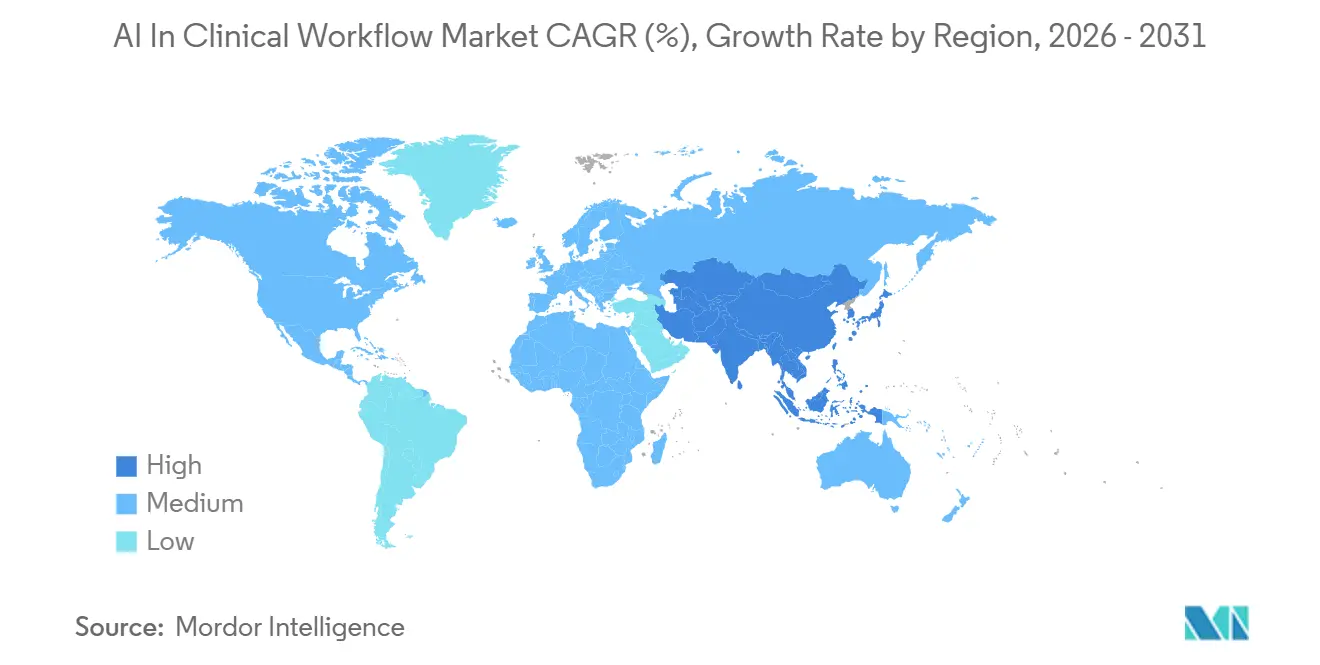

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

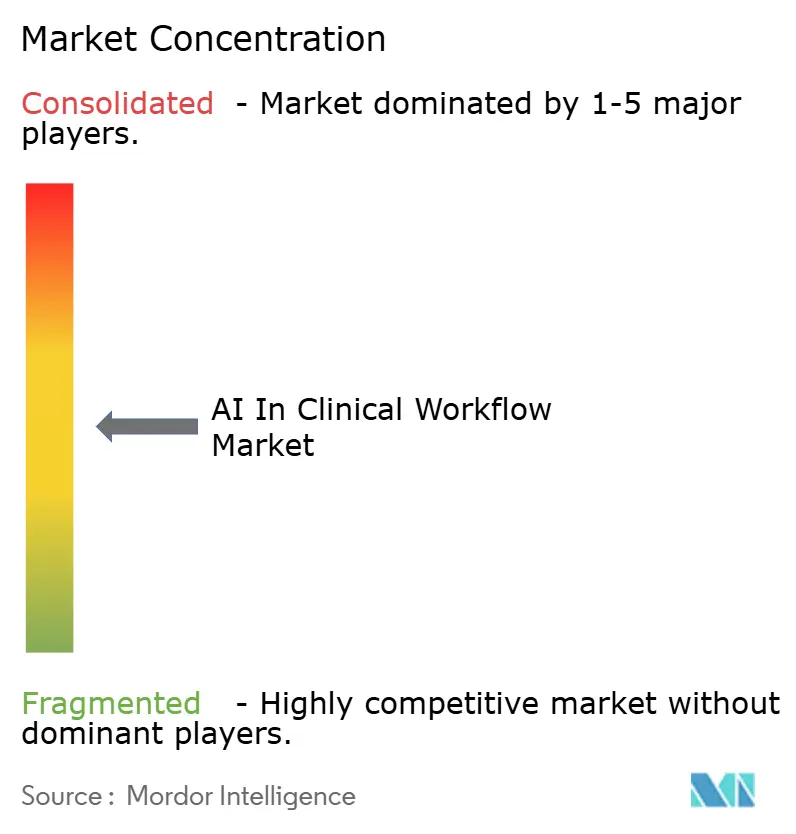

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Clinical Workflow Market Analysis by Mordor Intelligence

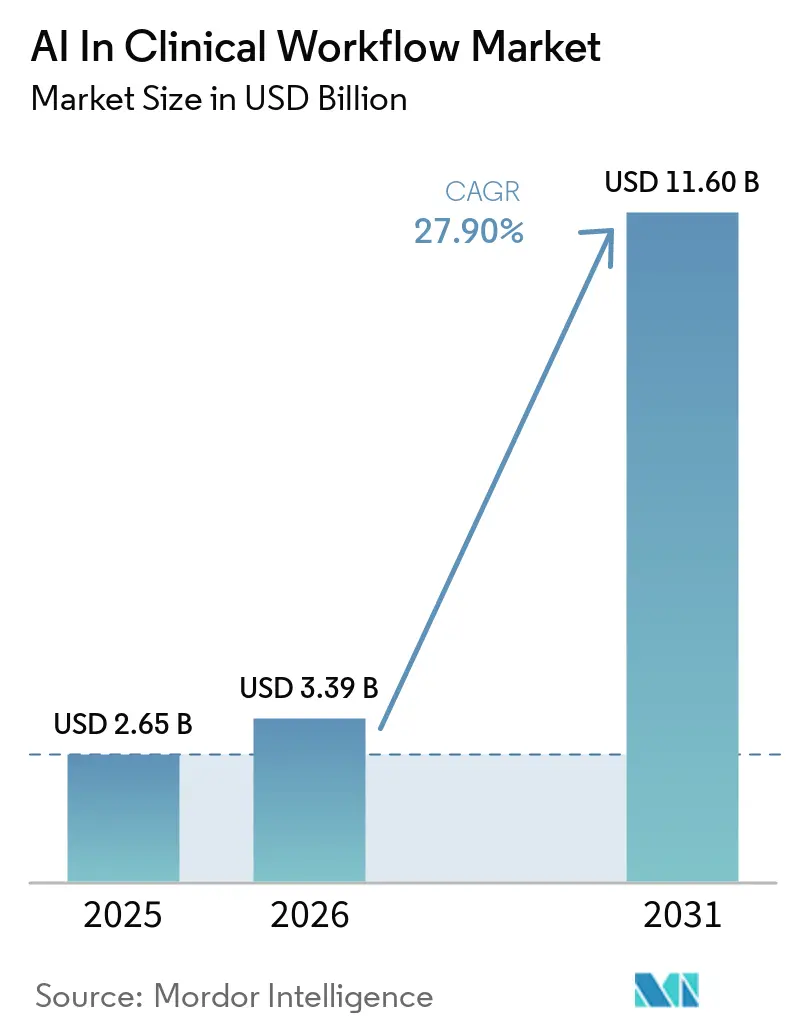

The AI In Clinical Workflow Market size is expected to grow from USD 2.65 billion in 2025 to USD 3.39 billion in 2026 and is forecast to reach USD 11.60 billion by 2031 at 27.90% CAGR over 2026-2031.

Persistent labor shortages, mandatory value-based reimbursement rules, and the integration of native generative AI by electronic health record (EHR) vendors have propelled the AI in Clinical Workflow market from pilot initiatives to a critical component of hospital infrastructure. Software continues to dominate the market due to the minimal replication costs once models are trained. However, services are expanding at a faster pace as healthcare providers prioritize validation, bias audits, and workforce upskilling. Cloud deployment now accounts for more than three-quarters of market spending, driven by its ability to streamline hardware procurement cycles and shift compliance management to vendors. Diagnostic imaging triage remains the largest use case, while virtual nursing assistants are experiencing the fastest growth as health systems seek scalable solutions to address chronic staffing shortages.

Key Report Takeaways

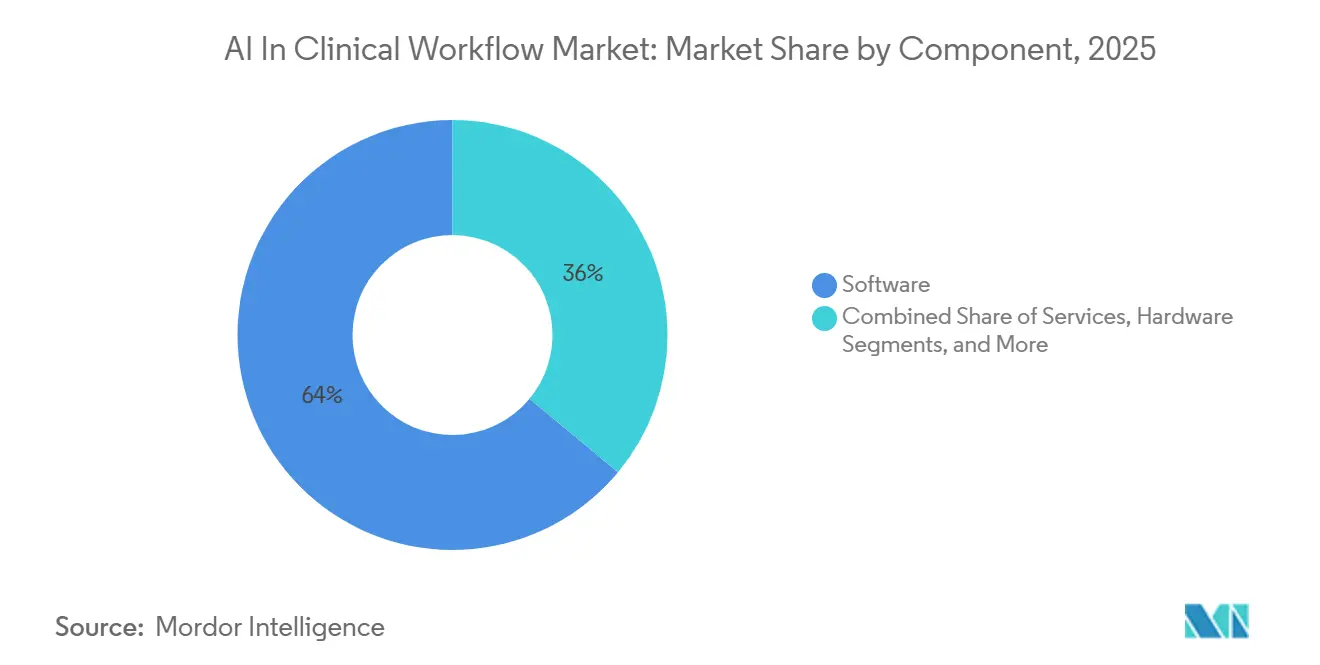

- By component, software held 63.98% of AI in the clinical workflow market share in 2025; services are projected to expand at a 28.77% CAGR through 2031.

- By deployment, cloud-based led with 75.66% revenue share in 2025; cloud-based is projected to grow at a 28.16% CAGR to 2031.

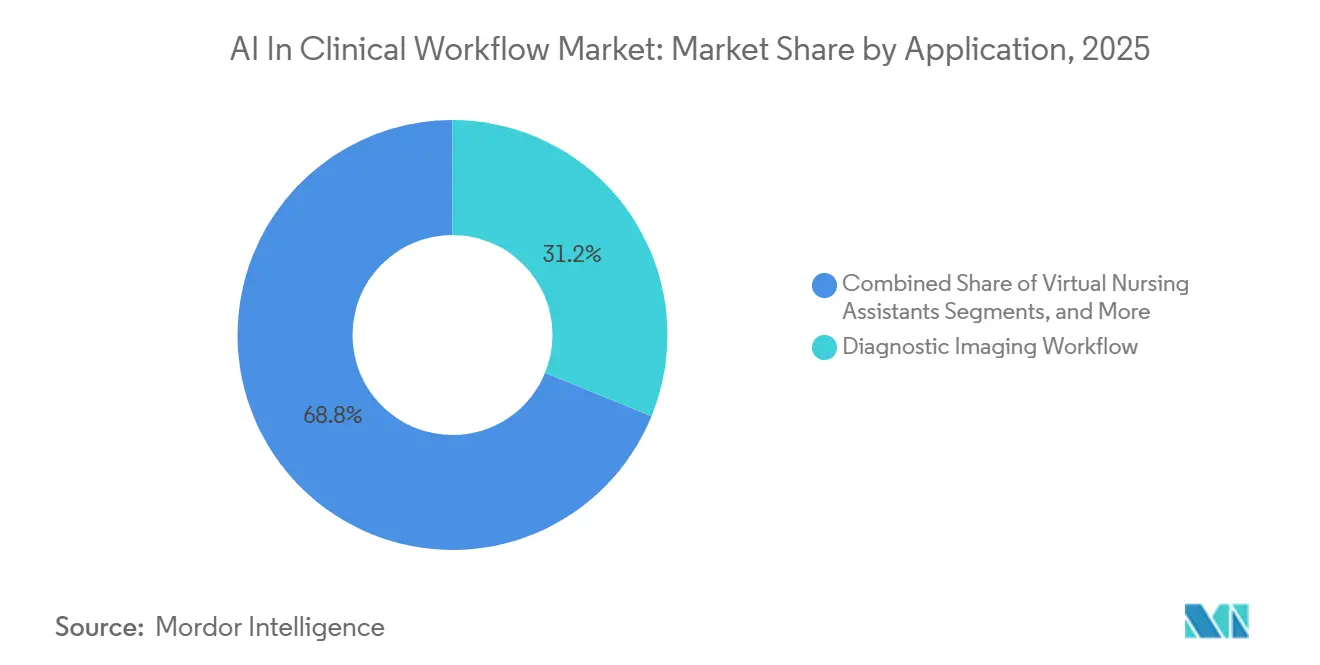

- By application, diagnostic imaging workflow led with 31.17% revenue share in 2025; virtual nursing assistants are expected to grow at a 28.33% CAGR to 2031.

- By end user, hospitals & health systems commanded 42.18% of the AI in clinical workflow market size in 2025.

- By geography, the United States led with 45.12% revenue share in 2025; the Asia-Pacific region is expected to grow at a 28.42% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Clinical Workflow Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accelerated EHR-AI integration by top EMR vendors | +6.8% | Global, early North America leadership | Medium term (2-4 years) |

| Shift to value-based care driving workflow automation | +5.2% | North America core, spill-over to EU and APAC | Long term (≥ 4 years) |

| Chronic-disease patient load boosting virtual nursing assistants | +4.9% | Global | Medium term (2-4 years) |

| FDA’s TAP fast-track for workflow AI tools | +3.1% | United States | Short term (≤ 2 years) |

| Rise of ambient clinical documentation for rural hospitals | +4.3% | North America, APAC rural regions | Medium term (2-4 years) |

| Gen-AI copilots embedded in RIS/PACS upgrade cycles | +3.7% | Mature imaging markets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated EHR-AI Integration by Top EMR Vendors

Leading EHR systems now incorporate native AI functionalities. Epic’s Art for Clinicians generates progress notes from in-room conversations, queues medication orders, and condenses discharge summaries, reducing administrative workloads by nearly one-third at early adopter sites. Oracle Health’s Clinical AI Agent, integrated into emergency departments, has recorded encounters and saved physicians approximately 200,000 hours.[1]Oracle Newsroom Staff, “Oracle Health Clinical AI Agent Helps Emergency and Inpatient Doctors Spend More Time on Patient Care,” Oracle, oracle.com Embedding AI directly at the point of care eliminates log-in delays, accelerates system-wide implementation, and establishes a competitive standard.

Shift to Value-Based Care Driving Workflow Automation

With over half of U.S. reimbursements tied to value-based contracts, healthcare providers are increasingly required to predict risks, address documentation gaps, and demonstrate outcomes. AI platforms streamline these processes by consolidating claims, lab results, and social-determinant data, then automating outreach and care-gap tasks. Providers and payers have reported up to an 80% reduction in prior-authorization turnaround times and significant increases in revenue from Hierarchical Condition Category (HCC) codes flagged by AI. These financial benefits have transitioned AI from an experimental tool to a budgeted necessity.

Chronic Disease Burden and Aging Populations Drive Virtual Nursing Assistant Adoption

The growing prevalence of chronic diseases and aging populations is placing significant pressure on nursing resources. AI-powered virtual nursing assistants (VNAs) are addressing this challenge by handling medication inquiries, scheduling follow-ups, and monitoring vital signs, enabling bedside nurses to focus on higher-priority tasks. University Hospitals implemented a VNA across 50 sites within four months, achieving improved patient satisfaction and faster discharge readiness. Similarly, WVU Medicine has expanded ambient-AI documentation to 25 hospitals and is piloting nursing modules. The potential for reduced readmissions and lower overtime costs is accelerating the adoption of VNAs.[2]Editorial Team, “New HIPAA Security Rule Proposal Expands AI Oversight,” Vorlon, vorlon.ai

FDA Regulatory Pathways Accelerate AI Workflow-Tool Market Entry

The FDA’s TEMPO pilot program allows selected AI workflow tools to bypass traditional premarket clearance processes while collecting real-world evidence under the CMS ACCESS payment model.[3]U.S. Food and Drug Administration, “Technology-Enabled Meaningful Patient Outcomes (TEMPO) for Digital Health Devices Pilot,” Federal Register, federalregister.gov Companies that demonstrate strong outcomes data during the pilot phase can leverage this evidence for future submissions, reducing commercialization timelines and attracting investment.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Interoperability gaps among legacy hospital IT stacks | -4.6% | Fragmented U.S. market most affected | Medium term (2-4 years) |

| Data-privacy compliance costs (HIPAA, GDPR, LGPD) | -2.8% | Global with regional peaks | Long term (≥ 4 years) |

| GPU allocation shortages inside hospital private clouds | -2.1% | Resource-constrained regions | Short term (≤ 2 years) |

| Physician resistance to fully autonomous triage | -3.4% | Mature healthcare markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interoperability Gaps Among Legacy Hospital IT Stacks

Many community hospitals continue to operate decade-old EHR modules that lack modern application-programming interfaces. Integrating AI requires either custom interfaces or expensive middleware, which delays implementation and increases the total cost of ownership. Vendors have introduced orchestration layers to standardize image routing and results delivery using HL7 and DICOM; however, significant gaps remain, particularly in settings where multiple best-of-breed systems coexist. These slower deployments reduce operational efficiency and limit short-term growth potential.

Data-Privacy Compliance Costs

Proposed updates to HIPAA Security rules in 2025 will require maintaining inventories of all AI tools that interact with protected health information. Additionally, compliance with region-specific regulations, such as the European General Data Protection Regulation (GDPR) and Brazil’s LGPD, adds further audit requirements and increases legal costs. A 2026 survey indicated that only 27% of healthcare chief information-security officers reported full compliance, prompting many providers to delay AI deployments until governance frameworks are fully developed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Governance Needs Fuel Service Growth

In 2025, software accounted for 63.98% of the revenue in the AI in Clinical Workflow market, showcasing the scalability of cloud subscriptions and the minimal costs incurred post-algorithm training. Leading platforms such as Abridge, Viz.ai, and Oracle Health Clinical AI Agent, when integrated into existing EHR workflows, offer near-instant functionality, ensuring a swift return on investment. Conversely, services are witnessing a robust growth rate of 28.77% CAGR, driven by hospitals' needs for implementation expertise, model-performance audits, and bias monitoring. Highlighting the importance of trustworthy AI, third-party assessors now provide continuous-validation dashboards that are presented to board-level risk committees. This underscores the necessity of ongoing human oversight in AI applications.

Service vendors play a pivotal role in workforce training. Given that only a fraction of clinical staff possess formal data-science skills, hospitals are turning to packaged boot camps and on-call AI “help desk” support. These services are not just add-ons; they are reshaping post-go-live maintenance from a once-internal challenge to a streamlined, predictable subscription model, aligning seamlessly with health systems' shift towards operating-expense frameworks.

By Deployment Model: Cloud-First Becomes Default

In 2025, cloud solutions dominated the spending landscape, capturing 75.66% of the market share. With providers increasingly valuing elasticity and vendor-managed compliance, cloud solutions are projected to grow at a robust 28.16% CAGR. Typically, a cloud rollout can be initiated within weeks, often starting with a pilot in a single nursing unit before expanding enterprise-wide. Providers are charged per clinician, with fees ranging from USD 100 to 300 monthly, a model that CFOs favor over hefty multi-million-dollar capital investments.

On-premise installations remain vital in scenarios where latency is critical, such as in acute stroke or pulmonary embolism triage. Data-localization mandates in regions like China and select EU states necessitate localized GPU clusters. Yet, vendors are increasingly offering cloud-style automated updates and monitoring packages, blurring the distinctions between deployment types and ensuring on-premise growth aligns with the broader AI in Clinical Workflow market trajectory.

By Application: Imaging Dominates, Nursing Assistants Surge

In 2025, the Diagnostic Imaging Workflow commanded 31.17% of the market revenue, underscoring its importance, especially since timely triage can significantly influence patient outcomes. Mercy's implementation of Aidoc's aiOS flagged close to 250,000 actionable studies, slashing the time for outpatient critical-finding diagnoses by an impressive 90%. This highlights the tangible clinical benefits of imaging AI. Other areas attracting investment include clinical-decision-support sub-segments such as sepsis alerts, readmission predictions, and guideline-compliance checks.

Meanwhile, Virtual Nursing Assistants (VNAs) are witnessing the most rapid growth, boasting a 28.33% CAGR. Reports indicate that AI-driven nursing follow-ups can reduce hospital utilization by 75% and enhance medication adherence by over 100%. Such quantifiable benefits position VNAs as a focal point for chief nursing officers, especially in light of prevailing vacancy challenges.

By End User: Hospitals Remain Core Buyers, Telehealth Scales

In 2025, Hospitals & Health Systems accounted for a substantial 42.18% of the market revenue, solidifying their status as primary stakeholders in the AI in Clinical Workflow arena. This dominance is largely due to the comprehensive nature of inpatient workflows, which encompass imaging, documentation, and billing, all under a unified contract. A testament to this scale is Kaiser Permanente's initiative to integrate ambient-AI scribes for over 25,000 clinicians. The commitment is further underscored by documented benefits, with faster note completion and increased patient encounters contributing to reduced clinician burnout.

Telehealth Providers are on an upward trajectory, expanding at a rate of 29.15% CAGR. To ensure safety and replicate in-clinic standards, video-first platforms are integrating AI for triage, auto-coding, and real-time drug-interaction checks. Many platforms are also incorporating remote-patient-monitoring devices, which relay continuous vital signs to AI models, flagging any anomalies for virtual nurse attention. With payers promoting hybrid-care incentives, the adoption of AI in telehealth is gaining momentum, particularly in rural areas where specialist access is limited.

Geography Analysis

In 2025, North America accounted for 45.12% of total revenue, with over 27% of U.S. health systems investing in commercial AI licenses, which is three times the average for enterprise software. Federal grants, along with clear FDA pathways for Software as a Medical Device, accelerate pilot programs and reduce risks associated with vendor selection. Canadian provinces are collaborating with national AI institutes to develop open-source clinical decision-support models, ensuring broader access beyond major urban areas.

Europe, while demonstrating strong EHR penetration, enforces stringent governance measures. The upcoming EU AI Act categorizes diagnostic algorithms as high-risk, requiring conformity assessments and continuous oversight. Providers are accepting these costs as AI agents assist in achieving sustainability and staffing objectives. In 2026, leading German networks implemented radiology triage across multiple trusts after completing cross-border data protection impact assessments.

Asia-Pacific is experiencing the fastest growth, driven by government-supported "AI-first" digital health strategies. China's "Healthy China 2030" and Japan's "Healthcare DX" initiatives are allocating funds to public-cloud AI for rural imaging and chronic disease management. Local vendors are partnering with global firms to develop language-specific natural language processing models. Additionally, state payers are reimbursing virtual nursing services in both high-density metropolitan areas and remote counties.

Competitive Landscape

Competition is intensifying between EHR-native giants and specialist pure-plays. Epic Systems, Oracle Health, and Microsoft, through Nuance Dragon Copilot, are integrating AI features directly into clinical charts. Their strategy, focused on ease of deployment and unified governance, has enabled them to secure significant enterprise deals. Meanwhile, specialists such as Abridge, Suki AI, Viz.ai, and RapidAI are differentiating themselves by demonstrating higher adoption rates or advanced analytics within specific domains.

EHR vendors simplify the purchasing process by eliminating the need for additional business associate agreements and bundling features like ambient documentation, billing code suggestions, and patient-experience chatbots into a single renewal. However, hospitals remain concerned about potential vendor lock-in and slower innovation cycles. Specialist vendors address these concerns by providing peer-reviewed outcome data and often entering into risk-sharing contracts, where fees are tied to documented time savings or improved coding accuracy.

Strategic activity in the market remains robust. Tempus AI's acquisition of Ambry Genetics aims to combine genomic insights with clinical data. Similarly, GE HealthCare is enhancing its imaging hardware with agentic AI modules. Microsoft is expanding the reach of its Dragon Copilot by making it available to third-party applications through its marketplace, allowing niche vendors to leverage its distribution network. Competitive differentiation now hinges on factors such as FDA clearances, transparent bias audits, and evidence of long-term performance.

AI In Clinical Workflow Industry Leaders

Epic Systems

GE HealthCare

Siemens Healthineers AG

Oracle Health

Koninklijke Philips N.V

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Microsoft unveiled a major Dragon Copilot upgrade at HIMSS 2026, adding Microsoft 365 context and a third-party marketplace.

- March 2026: Epic Systems launched Agent Factory, a low-code builder for customized AI agents across clinical and operational workflows.

- March 2026: Philips received FDA 510(k) clearance for SmartHeart, automating 14 cardiac-MR views in less than 30 seconds.

- September 2025: Tempus AI and Northwestern Medicine integrated a gen-AI co-pilot into the health system’s EHR and expanded precision-oncology genomic testing.

Global AI In Clinical Workflow Market Report Scope

As per the scope of the report, AI in clinical workflow refers to the integration of artificial intelligence technologies such as machine learning (ML), natural language processing (NLP), and computer vision into the daily processes, administrative tasks, and patient care activities of healthcare providers. It serves as a tool to automate routine tasks, analyze medical data, and augment clinician decision-making, aiming to improve efficiency, accuracy, and patient outcomes.

The AI in clinical workflow market is segmented by component, deployment model, application, end-user, and geography. By component, the market includes software, services, and hardware. By deployment model, the market is segmented into cloud-based and on-premise. By application, the market is categorized into patient scheduling & throughput, clinical decision support, diagnostic imaging workflow, medication management, virtual nursing assistants, and others. By end-user, the market is segmented into hospitals & health systems, ambulatory surgical centers, diagnostic imaging centers, telehealth providers, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software |

| Services |

| Hardware |

| Cloud-based |

| On-premise |

| Patient Scheduling & Throughput |

| Clinical Decision Support |

| Diagnostic Imaging Workflow |

| Medication Management |

| Virtual Nursing Assistants |

| Others |

| Hospitals & Health Systems |

| Ambulatory Surgical Centers |

| Diagnostic Imaging Centers |

| Telehealth Providers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Hardware | ||

| By Deployment Model | Cloud-based | |

| On-premise | ||

| By Application | Patient Scheduling & Throughput | |

| Clinical Decision Support | ||

| Diagnostic Imaging Workflow | ||

| Medication Management | ||

| Virtual Nursing Assistants | ||

| Others | ||

| By End User | Hospitals & Health Systems | |

| Ambulatory Surgical Centers | ||

| Diagnostic Imaging Centers | ||

| Telehealth Providers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will AI in Clinical Workflow be by 2031?

The AI in Clinical Workflow market size is projected to reach USD 11.60 billion by 2031, expanding at 27.90% CAGR from 2026 to 2031.

Which application is expanding fastest?

Virtual Nursing Assistants record the highest 28.33% CAGR because they relieve chronic staff shortages and improve medication adherence.

What share do cloud deployments hold today?

Cloud platforms captured 75.66% of 2025 revenue as hospitals favored rapid, vendor-managed rollouts.

Why are Services growing quicker than Software?

Providers lack in-house machine-learning auditors, so they purchase validation and governance subscriptions that grow at 28.77% CAGR.

Which region leads in spending?

North America held 45.12% of 2025 revenue thanks to mature EHR infrastructure and clear FDA pathways.

What factor most restrains adoption?

Interoperability gaps among legacy hospital IT systems subtract an estimated 4.6 percentage points from forecast CAGR by delaying deployments.

Page last updated on: