AI In Point-of-Care Hematology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

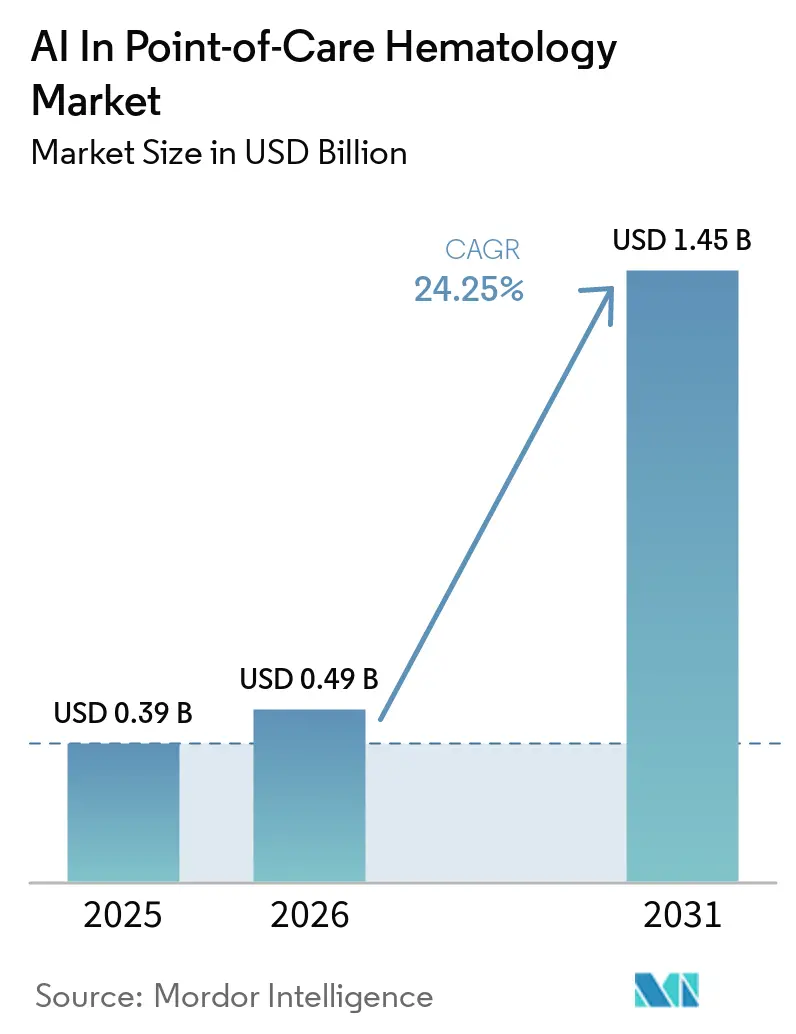

| Market Size (2026) | USD 0.49 Billion |

| Market Size (2031) | USD 1.45 Billion |

| Growth Rate (2026 - 2031) | 24.25% CAGR |

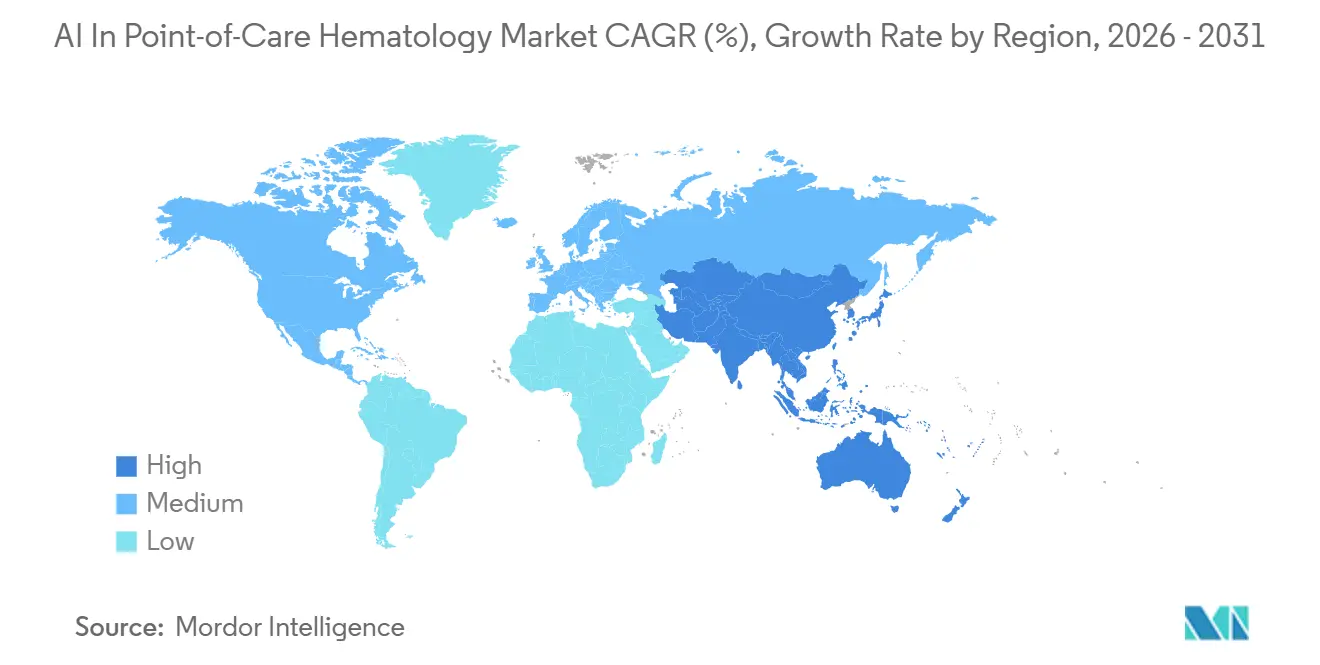

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Point-of-Care Hematology Market Analysis by Mordor Intelligence

The AI In Point-of-Care Hematology Market size is projected to expand from USD 0.39 billion in 2025 and USD 0.49 billion in 2026 to USD 1.45 billion by 2031, registering a CAGR of 24.25% between 2026 to 2031.

The AI in point-of-care hematology market is growing due to increasing demand for bedside complete blood counts in emergency, oncology, and ambulatory settings, where faster decision-making is critical compared to central laboratories. A shortage of skilled personnel for large-scale blood morphology reviews further drives the adoption of AI-powered solutions that streamline routine interpretations and prioritize exceptions. Compact, cartridge-based systems are reducing operator workload, enabling hematology testing in decentralized locations like clinics and community sites. Regulatory approvals, such as the clearance of AI-powered analyzers, are accelerating adoption, positioning the market to transition from niche innovation to a broader diagnostic model with faster testing, simplified workflows, and expanded access to hematology services.

Key Report Takeaways

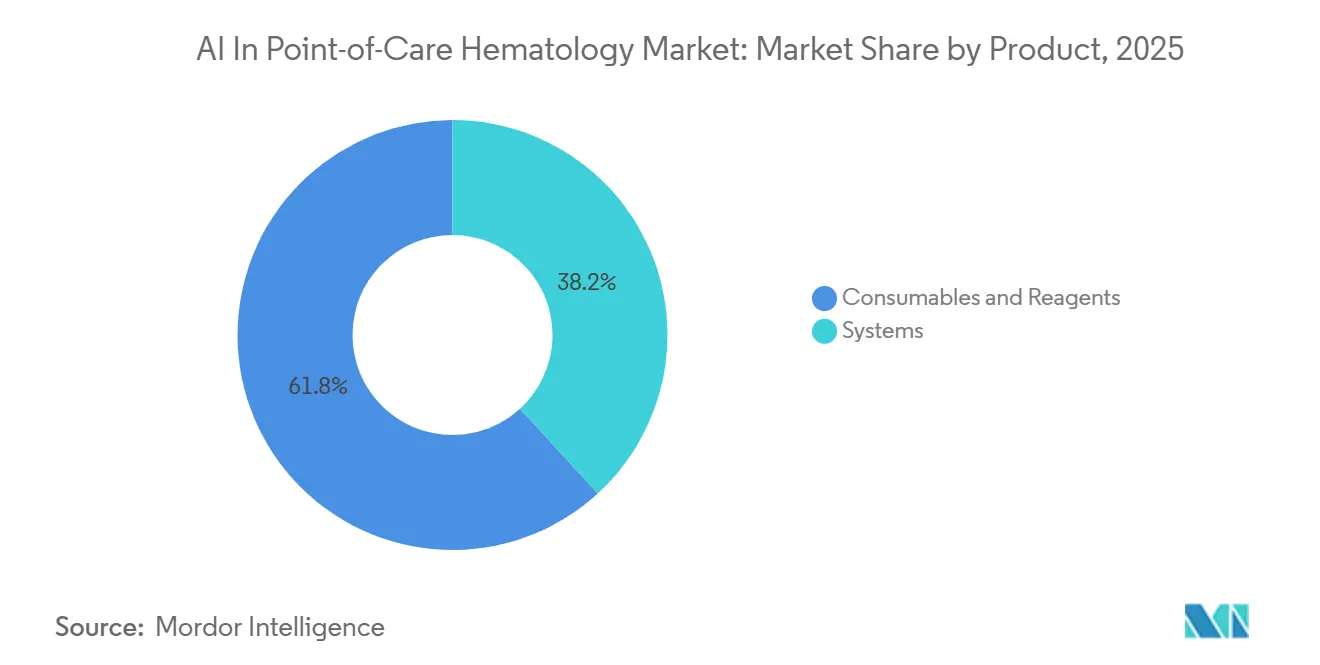

- By product, systems held 38.2% of revenue in 2025, while consumables and reagents are projected to grow at 25.05% CAGR through 2031.

- By test type, complete blood count testing accounted for 39.78% of revenue in 2025, while hemoglobin and hematocrit testing is expected to expand at 25.76% CAGR through 2031.

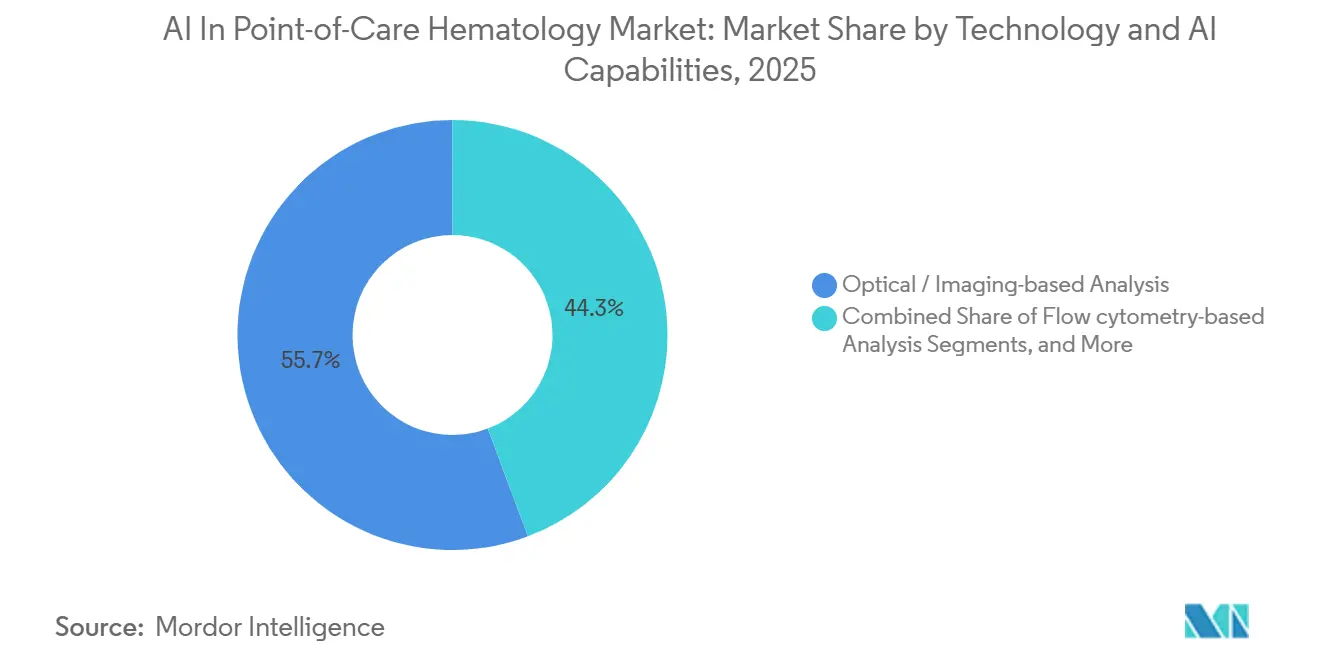

- By technology and AI capability, optical and imaging-based analysis captured 55.72% of revenue in 2025, while flow cytometry-based analysis is projected to grow at 26.15% CAGR through 2031.

- By end user, hospitals held 46.1% of revenue in 2025, while diagnostic laboratories are projected to record the fastest growth at 26.75% CAGR through 2031.

- By geography, North America accounted for 44.32% of revenue in 2025, while Asia-Pacific is projected to grow at 27.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Point-of-Care Hematology Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid bedside CBC demand in acute care | +4.2% | Global, with highest intensity in North America and Western Europe emergency departments | Short term (≤ 2 years) |

| Rising burden of anemia, infection, and hematologic disease | +3.8% | Global, with highest absolute burden in Asia-Pacific, Sub-Saharan Africa, and South America | Medium term (2-4 years) |

| Miniaturized cartridge and capillary sampling adoption | +3.5% | Global, with early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Expansion of decentralized diagnostics in Asia-Pacific and emerging markets | +3.8% | Asia-Pacific core, with spillover to Middle East and Africa and Latin America | Medium term (2-4 years) |

| Morphology workforce shortages favor AI-assisted review | +2.8% | North America, Europe, Japan, and Australia | Short term (≤ 2 years) |

| Remote telemedicine and digital collaboration enabling cloud-based hematology review | +2.5% | North America and Europe, with emerging use in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Bedside CBC Demand in Acute and Ambulatory Care

Rapid bedside hematology is becoming critical as emergency and ambulatory teams require immediate blood count results to make treatment decisions. The AI in point-of-care hematology market is benefiting from this demand, with advanced analyzers delivering multi-parameter blood counts from fingerstick or low-volume samples in minutes. This capability is particularly impactful in oncology follow-ups, monitoring immunosuppressed patients, and urgent triage, where delays can disrupt patient flow and increase repeat visits. The introduction of AI-supported testing devices for near-patient use highlights the shift toward decentralized diagnostics, enabling faster and more efficient decision-making. Providers are also leveraging this technology to transition routine blood monitoring to care sites previously reliant on central laboratories.

Rising Burden of Anemia, Infection, and Hematologic Disease

The growing prevalence of anemia, infections, oncology cases, and hematologic diseases is driving demand for AI in point-of-care hematology. Clinical validation of AI-supported analyzers in pediatric oncology demonstrated over 98.9% classification accuracy and Cohen’s kappa values above 0.95, proving their reliability in high-frequency testing. These systems also offer cost advantages, making them suitable for clinics and resource-limited settings. Additionally, AI devices for sepsis triage have shown superior performance compared to traditional markers, achieving a bacterial infection AUROC of 0.83 and enhanced sensitivity for ICU-level care. These advancements are building trust in AI tools for both routine and critical care applications.

Miniaturized Cartridge and Capillary Sampling Adoption

Miniaturization is a key driver in the AI in point-of-care hematology market, simplifying workflows and reducing dependency on bulky instruments. Cartridge-based and low-volume sampling designs enable easy deployment in decentralized settings, allowing non-specialist staff to operate the systems efficiently. For example, advanced devices now deliver a 5-part differential complete blood count from a single drop of blood in about 5 minutes. Certification processes that streamline compliance across multiple markets further enhance scalability, enabling faster international rollouts. These innovations align product designs with the operational needs of smaller care sites, making the technology more accessible and practical.

Expansion of Decentralized Diagnostics in APAC and Emerging Markets

The AI in point-of-care hematology market is expanding rapidly in Asia-Pacific, driven by high disease burdens, limited laboratory access, and efforts to bring diagnostics closer to patients. In Japan, the implementation of AI workflow solutions reduced over 7,600 work hours within four months, showcasing the efficiency gains from automation.[1]Yuki Matsuoka, “Current Status and Issues of AI Equipped SaMD Including Hematology Systems,” Journal of Medical Laboratory Technology, jstage.jst.go.jp This growth reflects a broader shift toward decentralized diagnostics, emphasizing workflow redesign and the ability to manage increasing test volumes with fewer manual steps. The market's momentum in emerging regions highlights a structural transformation rather than a simple replacement of existing systems in tertiary hospitals.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Accuracy validation gap versus central lab workflows | -2.5% | Global, most acute in North America and Europe where ISO 15189 laboratory accreditation requirements are enforced | Short term (≤ 2 years) |

| High instrument and per-test consumable costs in resource-constrained settings | -2.0% | Middle East and Africa, South America, and lower-income Asia-Pacific markets | Medium term (2-4 years) |

| Ai bias risk in rare-cell and low-prevalence diagnostic scenarios | -1.8% | Global, with higher risk in heterogeneous and underrepresented patient populations | Long term (≥ 4 years) |

| Lis interoperability and cybersecurity compliance burdens at decentralized sites | -1.5% | North America and Europe, with increasing relevance in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accuracy Validation Gap Versus Central Laboratory Workflows

A critical challenge in the AI-driven point-of-care hematology market is ensuring that capillary or point-of-care test results meet the reliability standards of high-throughput central laboratory systems. Despite strong concordance results, accredited reporting environments demand method comparisons, precision assessments, and consistent evidence across sites. Commercial adoption depends on validation against established laboratory quality benchmarks, and compliance with ISO 15189 adds complexity. Smaller companies face hurdles as they often lack the resources or infrastructure to support extensive validation programs, slowing their market entry.

LIS Interoperability and Cybersecurity Compliance at Decentralized Sites

Interoperability remains a significant barrier, as many hospitals still use laboratory information systems designed for older analyzers and outdated messaging protocols. Modern devices with cloud-based architectures or alternative data exchange methods require site-specific configurations, creating deployment challenges. Additionally, stricter cybersecurity requirements demand robust controls over patient data processing and AI model deployment. Success in this market increasingly depends on secure integration with hospital digital systems, highlighting the importance of aligning technological advancements with operational infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Consumables Revenue Poised to Challenge Instrument Dominance

In 2025, systems dominated the product structure with 38.2% of revenue, reflecting capital spending trends and the demand for validated analyzer platforms in hospitals. The systems category benefits from hospital procurement cycles and service contracts, with instrument placement often determining consumables in workflows. Consumables and reagents are projected to grow at a robust 25.05% CAGR through 2031, driven by cartridge-based and closed-test designs that shift recurring spending to individual test events.

By Test Type: CBC Anchors Volume While Hemoglobin Testing Drives Incremental Growth

Complete blood count (CBC) testing contributed 39.78% of test-type revenue in 2025, maintaining its position as the volume anchor in the AI-driven point-of-care hematology market. CBC’s broad clinical applications, including infection assessment, anemia workup, oncology monitoring, and pre-surgical screening, sustain its market dominance. Hemoglobin and hematocrit testing, supported by demand from anemia screening and sickle-cell monitoring, is the fastest-growing test type, with a 25.76% CAGR forecast through 2031.

By Technology & AI Capability: Optical Leadership Remains Strong While Flow Cytometry Gains Speed

Optical and imaging-based analysis accounted for 55.72% of revenue in 2025, underscoring the dominance of AI-augmented image cytometry. These systems excel in morphology-heavy tasks, identifying features like blast cells and red blood cell shape variations. Flow cytometry-based analysis is expected to grow at 26.15% CAGR through 2031, driven by advancements in miniaturized fluidics that enable sophisticated methods in compact devices.

By End User: Hospitals Lead While Diagnostic Laboratories Expand Faster

Hospitals represented 46.1% of revenue in 2025, driven by the need for rapid blood count data in emergency departments, oncology units, and outpatient clinics. Diagnostic laboratories are forecast to grow at 26.75% CAGR through 2031, reflecting a shift toward same-day service models and faster turnaround times. Laboratory networks increasingly prioritize connected workflows and data-driven insights alongside analytical performance.

Geography Analysis

In 2025, North America commanded a dominant 44.32% share of the revenue in the AI-driven point-of-care hematology market. This leadership is supported by a strong regulatory framework, enhanced reimbursement for near-patient testing, and significant investments in hospital and outpatient care. The February 2026 clearance of Athelas Home under a CLIA-waived pathway further strengthened the region's position by enabling AI-powered testing in decentralized care settings. North America's focus on faster patient routing and quicker monitoring continues to make it a key launch market for innovations in this sector.

While Europe plays a crucial role in adoption, the pace varies across nations and healthcare settings. Western European markets are advancing in AI-supported digital morphology and workflow modernization, while other regions remain in early stages of integration. The February 2026 certification of Scopio Labs' AI-powered platforms under EU IVDR regulations expanded access across the EU. Europe's growth in this market depends on how quickly hospitals and laboratories transition from pilot programs to routine workflows.

Asia-Pacific is on track to witness a robust 27.25% CAGR growth rate through 2031, making it the fastest-growing region in the AI-driven point-of-care hematology market. Growth is driven by healthcare decentralization, rising demand for community diagnostics, and local manufacturers catering to regional needs. Operational changes in Japan highlight this trend, with significant efficiency gains reported after deploying AI solutions in laboratory operations. Simpler point-of-care platforms also address service gaps in areas with limited laboratory access, while community clinics and primary care networks serve as key entry points for adoption in emerging regions.

Competitive Landscape

The AI in point-of-care hematology market includes two main groups of competitors. The first group consists of large in vitro diagnostics companies with established service networks and extensive experience in hematology workflows. The second group comprises smaller, point-of-care-focused firms emphasizing compact instruments, cartridge formats, and AI-driven interpretations. This competitive structure ensures the market remains dynamic, with established players offering scale and trust, while newer entrants bring speed, simplicity, and targeted use-case solutions.

Large players hold an advantage where buyers prioritize comprehensive workflow integration, validated service support, and access to regulated hospital environments. Companies like Sysmex, Mindray, and Siemens Healthineers leverage their existing relationships and integrate AI tools into broader diagnostic portfolios. Smaller challengers are driving innovation in digital morphology and decentralized testing, with examples like Scopio Labs advancing AI-powered red blood cell and platelet capabilities and PixCell Medical focusing on microfluidics and AI machine vision for decentralized care.

Strategic moves across the AI in point-of-care hematology market show that companies are competing through regulation, workflow, and deployment models rather than hardware alone. Athelas has advanced ambulatory and near-patient testing with FDA CLIA-waived clearance for fingerstick-based AI-powered testing. Mindray has enhanced AI functionality by linking large-scale blood cell data with faster platelet analysis, while Sysmex has emphasized secure on-premises AI architecture to address data governance demands. Success in this market will depend on combining analytical performance, regulatory readiness, digital integration, and alignment with decentralized care delivery.

AI In Point-of-Care Hematology Industry Leaders

Siemens Healthineers AG

Sysmex Corporation

Abbott

F. Hoffmann-La Roche Ltd

Bio-Rad Laboratories, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mindray introduced its AI "Clinical Inspection Intelligent Agent" at ISLH 2026 in Edinburgh. The AI model generates three-level diagnostic hematology reports using over one million real blood cell data points. The company also launched PLT-Pro 2.0, achieving 96.5% platelet identification precision with the YOLO-PLT deep learning model.

- February 2026: The FDA granted CLIA-waived 510(k) clearance to Athelas Home for its AI-powered point-of-care WBC and neutrophil percentage testing from fingerstick samples. This enables ambulatory oncology and clozapine monitoring without reliance on central laboratories.

- February 2026: Scopio Labs secured EU IVDR certification for its AI-powered Full-Field Digital Morphology Platforms. This expands market access across the European Union, complementing their existing FDA clearances for the U.S. market.

Global AI In Point-of-Care Hematology Market Report Scope

As per the scope opf the report, Artificial Intelligence (AI) in point-of-care (POC) hematology refers to the use of machine learning and smart algorithms to analyze blood samples directly at the patient's bedside or in near-patient clinics. It eliminates the delay of sending samples to central labs, delivering fast, specialized blood analysis and cell interpretation in minutes.

The AI in point-of-care (POC) hematology market is segmented by product, test type, technology & AI capability, end-user, and geography. By product, the market includes systems and consumables & reagents. By test type, the market is segmented into complete blood count (CBC), white blood cell count/differential, hemoglobin/hematocrit testing, anemia screening & triage, ESR/CRP-enabled hematology, and digital morphology/peripheral smear review. By technology & AI capability, the market is segmented into impedance-based analysis, optical/imaging-based analysis, flow cytometry-based analysis, microfluidic/lab-on-cartridge analysis, AI-assisted cell classification, and others. By end-user, the market is segmented into hospitals, emergency departments, diagnostic laboratories, blood banks & transfusion centers, ambulatory/urgent care centers, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Systems |

| Consumables & Reagents |

| Complete Blood Count (CBC) |

| White Blood Cell Count / Differential |

| Hemoglobin / Hematocrit Testing |

| Anemia Screening & Triage |

| ESR / CRP-enabled Hematology |

| Digital Morphology / Peripheral Smear Review |

| Impedance-based Analysis |

| Optical / Imaging-based Analysis |

| Flow cytometry-based Analysis |

| Microfluidic / Lab-on-Cartridge Analysis |

| AI-assisted Cell Classification |

| Others |

| Hospitals |

| Emergency Departments |

| Diagnostic Laboratories |

| Blood Banks & Transfusion Centers |

| Ambulatory / Urgent Care Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Systems | |

| Consumables & Reagents | ||

| By Test Type | Complete Blood Count (CBC) | |

| White Blood Cell Count / Differential | ||

| Hemoglobin / Hematocrit Testing | ||

| Anemia Screening & Triage | ||

| ESR / CRP-enabled Hematology | ||

| Digital Morphology / Peripheral Smear Review | ||

| By Technology & AI Capability | Impedance-based Analysis | |

| Optical / Imaging-based Analysis | ||

| Flow cytometry-based Analysis | ||

| Microfluidic / Lab-on-Cartridge Analysis | ||

| AI-assisted Cell Classification | ||

| Others | ||

| By End User | Hospitals | |

| Emergency Departments | ||

| Diagnostic Laboratories | ||

| Blood Banks & Transfusion Centers | ||

| Ambulatory / Urgent Care Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of AI in point-of-care hematology?

The AI in point-of-care hematology market size stands at USD 0.49 billion in 2026 and is forecast to reach USD 1.45 billion by 2031 at a 24.25% CAGR.

What is driving adoption of AI-enabled point-of-care hematology systems?

Adoption is being supported by rising bedside CBC demand, staff shortages in morphology review, and compact cartridge-based devices that make testing easier outside central laboratories.

Which product segment is growing fastest in this space?

Consumables and reagents are the fastest-growing product group, with a projected 25.05% CAGR through 2031, while systems remained the largest product segment in 2025.

Which test type remains most important for revenue?

Complete blood count testing held 39.78% of test-type revenue in 2025 because it supports infection triage, oncology monitoring, anemia assessment, and routine screening.

Which region leads AI in point-of-care hematology adoption?

North America led with a 44.32% revenue share in 2025, supported by regulatory clearances, reimbursement support, and strong acute care investment.

Which region is expected to grow the fastest through 2031?

Asia-Pacific is forecast to grow at 27.25% CAGR through 2031 because healthcare systems are expanding decentralized diagnostics and local companies are increasing regional supply.

Page last updated on: