AI In Medical Scheduling Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

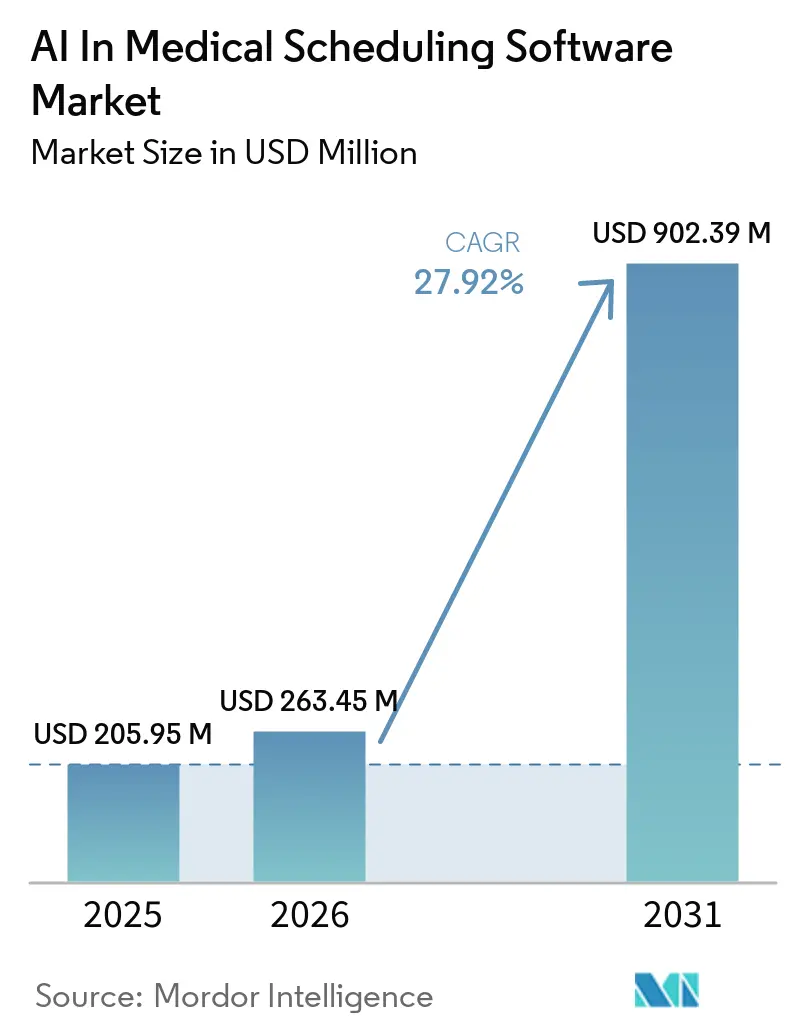

| Market Size (2026) | USD 263.45 Million |

| Market Size (2031) | USD 902.39 Million |

| Growth Rate (2026 - 2031) | 27.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Medical Scheduling Software Market Analysis by Mordor Intelligence

The AI In Medical Scheduling Software Market size was valued at USD 205.95 million in 2025 and is estimated to grow from USD 263.45 million in 2026 to reach USD 902.39 million by 2031, at a CAGR of 27.92% during the forecast period (2026-2031).

The pace of expansion shows that provider organizations now view appointment access, staff coordination, and patient communication as areas where automation can deliver faster financial returns than many other health IT projects. The AI in medical scheduling software market is also gaining support because scheduling tasks sit close to revenue capture, patient retention, and clinician productivity, so even small gains in attendance, slot utilization, and call handling can matter at scale. Staffing pressure remains a major push factor, as health systems continue to lose clinical time to administrative work and are placing more value on tools that reduce friction in routine workflows. Philips reported in 2025 that more than 75% of healthcare professionals lose clinical time to incomplete or inaccessible patient data, while a multicenter study in JAMA Network Open found clinician burnout fell after administrative work was reduced with ambient AI support. Competitive positioning in the AI in medical scheduling software market is moving toward deeper workflow integration, because providers increasingly reward vendors that can connect scheduling with EHR activity, patient messaging, and operational follow-up in a single system.

Key Report Takeaways

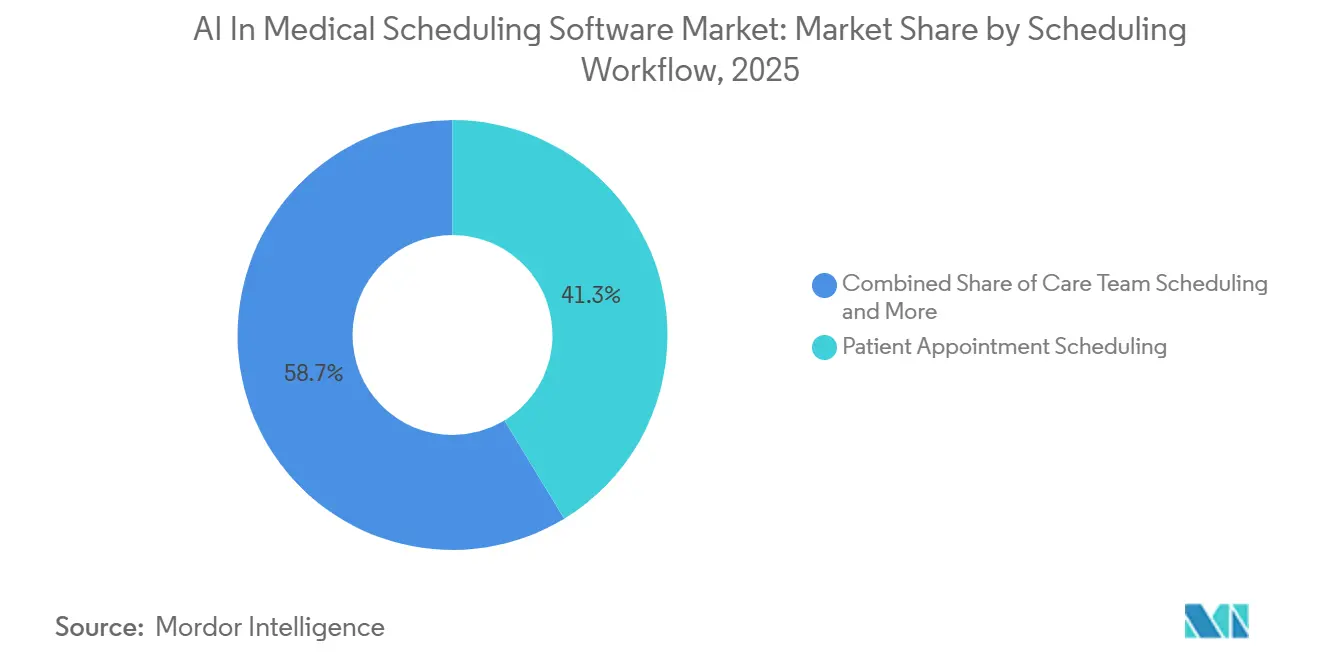

- By scheduling workflow, patient appointment scheduling held 41.31% share in 2025, while care team scheduling is forecast to expand at a 29.38% CAGR through 2031.

- By AI capability, predictive scheduling led with 38.24% share in 2025, while capacity optimization and waitlist automation is projected to grow at a 29.52% CAGR through 2031.

- By deployment model, cloud-based deployment accounted for 54.52% share in 2025, while on-premises deployment is expected to record a 29.25% CAGR through 2031.

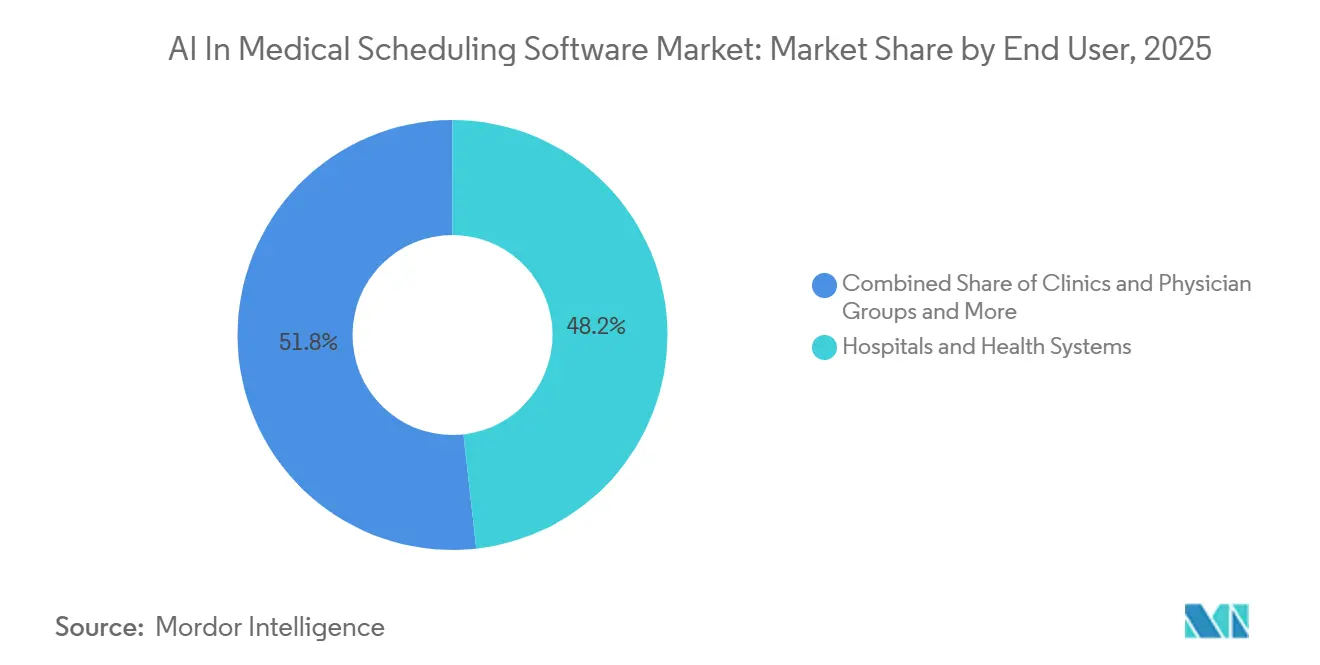

- By end user, hospitals and health systems held 48.24% share in 2025, while clinics and physician groups are projected to expand at a 29.83% CAGR through 2031.

- By specialty, primary care captured 61.52% share in 2025, while behavioral and mental health is forecast to grow at a 28.35% CAGR through 2031.

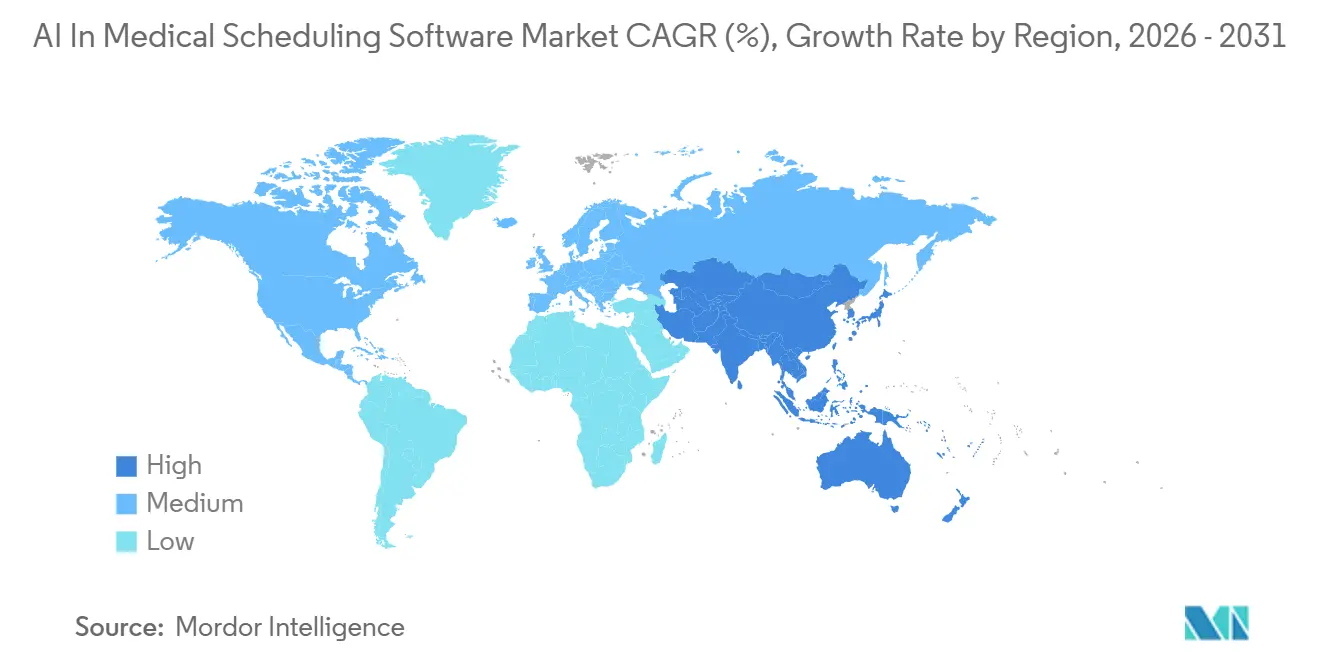

- By geography, North America held 47.24% share in 2025, while Asia-Pacific is projected to advance at a 30.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Medical Scheduling Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Led No-Show Prediction and Slot Recovery | +3.5% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| 24/7 Conversational Self-Scheduling Demand | +3.2% | Global, led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Provider Burnout and Staffing Shortages Driving Automation | +2.8% | Global, critical in North America, Western Europe, and ANZ | Medium term (2-4 years) |

| EHR-Connected Workflow Automation Adoption | +3.8% | North America dominant, growing in Western Europe and APAC | Medium term (2-4 years) |

| Prior-Authorization-Aware Booking Workflows | +2.5% | North America primary, EU and APAC adopting equivalent frameworks | Medium term (2-4 years) |

| Contact-Center Voice AI Economics | +2.9% | Global, especially high-volume North American and APAC health systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Led No-Show Prediction and Slot Recovery

The market is benefiting from the simple fact that missed appointments translate into lost revenue, idle clinician time, and more work for staff. Predictive models now use booking history, patient behavior, and care patterns to identify appointments with higher cancellation or no-show risk before the slot is lost. This matters because providers do not only want better reminders, they want a way to recover capacity before it goes unused. Luma Health stated in April 2026 that its platform had already helped health system clients save 2.5 million staff hours and manage more than 350,000 care-related next steps, which supports the commercial case for automated slot recovery and follow-up workflows. In the AI in medical scheduling software market, this feature set is especially valuable where high outpatient volumes make each unfilled slot more costly. It also creates a natural path for expansion because vendors that first prove value on attendance can later extend into waitlists, care gap closure, and broader access management.

24/7 Conversational Self-Scheduling Demand

The AI in medical scheduling software market is also being lifted by patient demand for round-the-clock digital access that does not depend on office hours or call queues. Voice and chat agents now let patients book, cancel, or reschedule in plain language, which reduces the load on front-desk teams and improves response time. Zocdoc launched Zo by Zocdoc in May 2025 to handle inbound scheduling calls autonomously, showing that conversational booking is being positioned as a mainstream access tool rather than a pilot feature. athenahealth pushed the same direction in February 2026 with agentic patient communication tools that included Waitlist Scheduling and Enhanced Patient Self-Scheduling across a provider network that serves 1 in 5 Americans. The same demand pattern is visible in Europe, where samedi offers AI features and a KI-Telefonassistent that connect directly to provider scheduling environments under local compliance expectations[1]samedi, “Künstliche Intelligenz von samedi,” samedi, samedi.com. As a result, the AI in medical scheduling software market is moving closer to an always-available access model where patient convenience and staff efficiency improve at the same time.

EHR-Connected Workflow Automation Adoption

The market is increasingly separating into high-value and low-value deployments based on how deeply the scheduling layer connects with the EHR. Hyro reported in December 2025 that 82% of organizations using configurable, bi-directional EHR integrations generated annual ROI above USD 500,000 from AI call-center agents, while only 18% of organizations relying on standard FHIR connections reached that level. That gap is important because providers want automation that can understand provider templates, patient context, and next-step workflows without forcing staff into manual correction. Oracle’s ONC-certified AI-powered EHR added clinical AI agents and voice navigation within workflow, which shows how larger platform vendors are building scheduling into wider operational orchestration. Epic has also been expanding AI development across charting, revenue cycle, and workforce tools, which supports the view that scheduling automation is becoming a native platform capability instead of a disconnected add-on. In the AI in medical scheduling software market, this trend favors vendors that can prove they fit naturally inside the clinical and operational systems providers already use every day.

Prior-Authorization-Aware Booking Workflows

The AI in medical scheduling software market is also being shaped by the need to connect booking decisions with payer approval logic before an appointment is finalized. This is most visible in imaging, procedures, and specialty referrals where an appointment without authorization can create rework, denials, and wasted capacity. Surescripts said in February 2025 that its Touchless Prior Authorization technology reduced appeals caused by missing clinical information by 88% and denials by 68%, with select approvals completed in under 30 seconds. Humata Health reported in April 2025 that its deployment with Allegheny Health Network reached 70% human-free approval within the first month for covered procedure codes, which shows that prior authorization automation is already moving into production workflows. As these functions move closer to the point of booking, scheduling platforms that cannot surface authorization requirements early will become less attractive to providers. That shift is giving the AI in medical scheduling software market a stronger workflow orientation, where value comes from preventing downstream friction rather than only arranging the initial appointment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patient Data Privacy and AI Governance Burden | -2.1% | Global, highest friction in North America, EU, and California | Medium term (2-4 years) |

| Fragmented EHR and Departmental Integration | -1.8% | Global, particularly acute in mid-market and multi-system US providers and APAC developing markets | Medium term (2-4 years) |

| Clinical Change-Management Resistance | -1.5% | Global, slower adoption in rural, academic, and single-specialty settings | Long term (≥ 4 years) |

| Real-Time Data Quality and Schedule-Rule Complexity | -1.2% | Global, most pronounced in multi-site health systems and complex procedural specialties | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Patient Data Privacy and AI Governance Burden

The market still faces slower adoption where providers believe the compliance burden is not yet matched by clear internal governance processes. Scheduling systems now handle appointment reasons, insurance information, communication history, and other data that can trigger strict privacy reviews when AI is involved. That creates hesitation in enterprise buying cycles, especially for mid-market vendors that need to prove oversight, documentation, and safe operating controls with limited legal resources. The effect is not that providers reject automation, but that they ask more questions about training data, human review, audit trails, and incident response before signing contracts. In the AI in medical scheduling software market, this tends to favor larger vendors and established platform partners that can present a fuller compliance package during procurement. It also lengthens sales cycles in settings where legal, security, and clinical teams all need to approve the same deployment.

Fragmented EHR and Departmental Integration

The market is also constrained by the uneven quality of scheduling data and the number of systems that must stay synchronized in real time. Provider organizations often run different workflows across clinics, departments, and service lines, which means a single scheduling engine has to account for different slot rules, provider qualifications, room dependencies, and payer checks. Even when data can technically move between systems, the meaning of that data does not always remain consistent across calendars, messaging tools, EHR workflows, and telehealth platforms. That raises implementation time, increases testing needs, and can reduce buyer confidence when providers worry about double booking, missed updates, or rule mismatches. The AI in medical scheduling software market therefore rewards vendors that can adapt to operational variation instead of assuming that one workflow model fits every service line. Until interoperability improves at the workflow level, integration work will remain a meaningful cost and timing drag on new deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Scheduling Workflow: Appointment Volume Anchors Revenue, Team Scheduling Accelerates

Patient appointment scheduling held 41.31% of the AI in medical scheduling software market share in 2025, making it the largest workflow segment because it sits at the front end of patient access and serves the broadest range of provider settings. This part of the AI in medical scheduling software market benefits from the widest vendor mix, including EHR-native modules, patient-facing booking tools, and contact-center automation platforms. Providers often begin here because the value is easier to see through fewer calls, better attendance, and faster booking completion. The segment also has a natural data advantage because appointment history, reminders, cancellations, and rebooking events create a steady record that AI models can use for optimization. That is why patient appointment scheduling remains the main revenue anchor even as the market expands into more specialized workflows.

Care team scheduling is projected to grow at a 29.38% CAGR through 2031, reflecting stronger demand for tools that align staff availability, credentials, and workload with patient demand. QGenda has framed this area as a workforce management problem as much as a scheduling problem, and a 2025 Forrester Total Economic Impact study commissioned by QGenda reported 430% ROI for health system clients using its unified care team scheduling platform[2]QGenda, “Hospitals and Health Systems Achieved 430% ROI with QGenda, According to New Forrester Total Economic Impact Study,” QGenda, qgenda.com. QGenda also introduced a certified integration with Workday HCM in May 2026, which strengthens the link between scheduling decisions and HR systems. Procedure and resource scheduling is also gaining traction as providers try to coordinate rooms, equipment, and staff across more complex service lines. LeanTaaS launched iQueue for Surgical Clinics in June 2025 as an end-to-end surgical coordination platform that extends optimization from clinic booking into operating room allocation and supports 4 million surgeries annually. Access-center and omnichannel scheduling adds another layer of growth because health systems want a single operating model across phone, portal, and digital outreach. In the AI in medical scheduling software industry, workflow expansion beyond simple appointment booking is a sign that vendors are moving closer to operational command-center roles.

By AI Capability: Predictive Scheduling Leads, Capacity Automation Grows Fastest

Predictive scheduling accounted for 38.24% of the 2025 market and led the AI in medical scheduling software market because its value is closely tied to revenue recovery and better use of existing appointment supply. Providers understand the model quickly because it helps identify likely no-shows, supports targeted outreach, and makes reminder efforts more efficient. This capability is often the first production use case because it requires less workflow redesign than broader orchestration tools. It also fits a wide range of specialties, from primary care to high-volume outpatient services, where missed appointments carry a clear cost. The leading position of predictive scheduling shows that buyers still prefer use cases with measurable operational outcomes at the start of adoption.

Capacity optimization and waitlist automation leads growth with a 29.52% CAGR through 2031, as the AI in medical scheduling software market shifts from predicting problems to automatically correcting them. That distinction matters because providers gain more value when cancellations are backfilled without manual calls or spreadsheet management. Luma Health’s Spring 2026 release expanded its Operational AI so the system could identify care gaps from incoming fax documents and trigger scheduling workflows without staff intervention. LeanTaaS was named Best in KLAS for Capacity Optimization Management for the second straight year in February 2026, which signals that buyer trust in this capability is consolidating around a smaller group of validated vendors. Conversational AI scheduling, rules-based recommendation engines, and triage-led tools remain important because they address different access points before the final booking happens. Together these functions are broadening the AI in medical scheduling software market from prediction alone into a fuller decision-and-action layer for patient access. The AI in medical scheduling software industry is therefore becoming more operational, not only more analytical.

By Deployment Model: Cloud Dominates, On-Premises Narrows the Gap

Cloud-based deployment held 54.52% of the 2025 market, giving it the largest share of the AI in medical scheduling software market size because SaaS delivery supports faster feature releases and lowers internal IT burden for many providers. This model is especially attractive for clinics and physician groups that want modern scheduling functions without heavy infrastructure spending. It also supports quicker updates to AI models, user workflows, and patient communication tools. The cloud model fits the commercial direction of the AI in medical scheduling software market, where vendors compete on speed of iteration and the ability to roll out enhancements across large customer bases. That keeps cloud in the lead even as provider requirements become more complex.

On-premises deployment is still the fastest-growing model at a 29.25% CAGR through 2031, which reflects demand from compliance-sensitive organizations that want tighter control over where data sits and how systems are managed. The segment is not growing because providers are moving backward, but because some large health systems, academic centers, and public-sector institutions still want deployment options that align with stricter governance preferences. Oracle has helped blur the line between cloud and on-premises by positioning its AI-powered EHR architecture so it can fit enterprise environments with more controlled hosting expectations. Hybrid deployment is also gaining ground in multi-site systems that combine older acute care infrastructure with newer ambulatory scheduling and engagement tools. This structure gives providers flexibility, but it also raises integration cost because data must be normalized across systems that were not designed together. Over time, that means the AI in medical scheduling software market is likely to support several deployment paths rather than a single dominant architecture. Buyers are choosing based on governance, installed systems, and workflow fit instead of using a simple cloud versus on-premises divide.

By End User: Hospitals Lead on Share, Clinics Drive Volume Growth

Hospitals and health systems held 48.24% of the 2025 market and led the AI in medical scheduling software market because they face the greatest scheduling complexity across specialties, departments, staff groups, and physical resources. Their size makes even modest productivity improvements meaningful, especially when missed appointments, idle capacity, and call-center load affect multiple locations at once. A LeanTaaS-commissioned survey released in April 2026 found that 72% of hospital CFOs reported margins of 2% or lower, which keeps attention focused on workflow tools that can recover revenue and reduce waste. That financial pressure explains why large systems continue to be important early adopters of access automation. It also helps explain why the AI in medical scheduling software market still draws substantial enterprise demand despite longer buying cycles.

Clinics and physician groups are forecast to grow at a 29.83% CAGR through 2031, which marks them as the fastest-growing end-user base in the AI in medical scheduling software market size. Growth here comes from lower-cost, easier-to-integrate tools that let independent practices adopt enterprise-style scheduling functions without large implementation budgets. NexHealth reinforced the strength of this demand pocket when it closed a USD 125 million Series C in July 2025 at a USD 1 billion valuation. Notable also showed the expanding role of AI-enabled access in provider transformation programs through its partnership with Inova Health in January 2026 and its deployment at Marshall Health Network in March 2026. Ambulatory surgical centers, imaging centers, and telehealth-focused providers add to demand because they depend on fast, accurate booking and fewer authorization errors. For these users, the AI in medical scheduling software market is attractive because automation can improve throughput without requiring a broad platform overhaul at the start. That is why growth is now spreading from large systems into smaller and more specialized care settings.

By Specialty: Primary Care Leads on Scale, Behavioral Health Leads on Urgency

Primary care held 61.52% of the 2025 market, which made it the largest specialty segment in the AI in medical scheduling software market because it has the highest outpatient volume and the broadest need for routine scheduling efficiency. It is also the most common starting point for AI deployment because recurring visits generate the historical booking data that predictive models need. The segment benefits from simpler visit types compared with more procedural specialties, which lowers the barrier to initial automation. At the same time, primary care still presents enough scale for no-show reduction, waitlist management, and self-scheduling features to produce visible operational gains. That combination of volume, data availability, and practical ROI keeps primary care at the center of current demand.

Behavioral and mental health is projected to expand at a 28.35% CAGR through 2031, making it the fastest-growing specialty in the AI in medical scheduling software market size because provider shortages and waitlist pressure are especially acute in this area. FAIR Health reported that mental health diagnoses accounted for 63% of telehealth claims nationally in April 2025, which supports the view that demand is high and increasingly digital. Qualifacts launched its iQ Agent for Scheduling in January 2026 for behavioral health workflows, showing that vendors are now tailoring scheduling automation to specialty-specific needs. CentralReach also reported in January 2025 that a deployment of CR ScheduleAI produced at least a 20% increase in appointments for ABA providers by automating language preference, provider preference, and cancellation management. Cardiology, orthopedics, and oncology each carry their own operational logic, but behavioral health stands out because scheduling friction there often reflects a structural mismatch between demand and provider supply. In the AI in medical scheduling software market, that makes automation feel less optional and more necessary for access management. The dental segment also remains active, helped by patient-driven self-scheduling expectations and repeat recall workflows that suit automation well.

Geography Analysis

North America held 47.24% of the AI in medical scheduling software market share in 2025, which made it the largest regional contributor because provider digitization, high administrative cost, and established vendor presence all support faster commercial adoption. The region benefits from a dense base of health systems, multi-site provider groups, EHR adoption, and patient access vendors that already sell into complex enterprise environments. It is also the geography where the business case for AI scheduling is often easiest to quantify, since call-center burden, appointment leakage, and operational labor costs are already closely tracked. The AI in medical scheduling software market in North America is therefore less about proving the category exists and more about proving which deployment model and integration depth can scale best. That mature demand base should keep the region central to vendor revenue even if its growth rate is lower than earlier-stage regions.

Europe presents a different adoption pattern because public health systems, privacy expectations, and procurement pathways shape rollout decisions more directly. Even so, the region is moving forward as regulatory clarity and interoperability efforts improve the environment for compliant deployment. France has taken a visible role in this shift, and the Ségur du numérique vague 2 LGC framework published in 2025 set interoperability requirements that make scheduling integrations easier to standardize[3]Agence du Numérique en Santé, “Ségur Vague 2, Publication de l'arrêté pour le dispositif LGC, Couloir Médecin de Ville,” esante.gouv.fr, esante.gouv.fr. Germany is also contributing through vendors such as samedi, which offers AI-enabled scheduling and telephone assistant capabilities that connect to provider workflows under local data expectations. The AI in medical scheduling software market in Europe is still more uneven than in North America, but the mix of public sector modernization and private practice digitization is widening the addressable opportunity. Adoption is likely to remain strongest where providers can connect compliance requirements with clear gains in referral handling, wait-time reduction, and outpatient coordination.

Asia-Pacific is the fastest-growing region with a 30.83% CAGR through 2031, showing that the AI in medical scheduling software market is expanding quickly where healthcare digitization is still catching up from a lower base. Large patient populations, uneven provider access, and government-backed digital health programs are creating room for tools that improve appointment flow and reduce manual bottlenecks. The region also has a growing base of local and international technology vendors targeting workflow automation in hospitals, clinics, and virtual care settings. That makes Asia-Pacific important not only for future revenue growth, but also for new deployment models that may be more mobile-first and cost-sensitive than those seen in North America. South America and the Middle East and Africa remain earlier-stage regions, yet they add long-term opportunity as hospital modernization and private provider digitization continue to spread.

Competitive Landscape

The AI in medical scheduling software market is moderately fragmented, with competition split between EHR-native vendors and specialists that focus on scheduling depth. Epic Systems, Oracle Health, and athenahealth are strengthening native capabilities inside broader clinical platforms, while Kyruus Health, LeanTaaS, Luma Health, Relatient, Zocdoc, and others compete on patient access, capacity management, and workflow specialization. This creates a market where product breadth matters, but measurable operational outcomes still carry significant weight in buying decisions. Oracle’s AI-powered EHR gained ONC certification in October 2025 and added clinical AI agents that reduced physician documentation time by 30%, which shows how large platform vendors are using workflow integration as a competitive lever. In the AI in medical scheduling software market, this means smaller vendors need stronger proof that they can integrate deeply, move fast, and deliver results in narrow but important use cases.

Recent strategic moves show that platform expansion and distribution partnerships are becoming more important. RevSpring announced the acquisition of Kyruus Health in September 2025, creating a broader connected care journey offering that linked search, scheduling, and payment touchpoints. Relatient was named athenahealth’s Preferred Solution Partner for intelligent scheduling in April 2026, extending its reach across a network that covers close to 50 million patient appointments annually. Notable expanded its position through health system partnerships, including Inova Health and Marshall Health Network in 2026. These moves suggest that the AI in medical scheduling software market is rewarding vendors that can secure trusted channels into provider workflows rather than rely only on standalone product merit.

Competitive pressure is also rising from adjacent technology players that see patient access as a valuable entry point into healthcare operations. Amazon Connect Health has entered healthcare contact-center automation with natural-language appointment booking and Epic integration, which signals that cloud and infrastructure leaders now view this space as commercially relevant. Voice AI and omnichannel access tools also lower barriers for smaller providers, because they let organizations automate common scheduling interactions without building large front-desk teams. Even so, the strongest moat still comes from configurable EHR integration, governance readiness, and demonstrated access outcomes. That is why the AI in medical scheduling software market is likely to keep favoring vendors that can combine workflow depth, enterprise trust, and a distribution model that scales across provider types.

AI In Medical Scheduling Software Industry Leaders

Epic Systems Corporation

Zocdoc

QGenda

Veradigm LLC

Relatient

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Luma Health released its Spring 2026 Operational AI update. The release introduced proactive care gap closure via automated fax intelligence, no-show rescheduling, and clinical results follow-up, building on 2.5 million hours of documented staff time savings across health systems in 2025.

- March 2026: Notable launched an online scheduling and registration platform at Marshall Health Network. The West Virginia-based academic health system is expanding the deployment to additional primary care clinics, marking Notable's continued push into regional health system digital transformation programs.

- February 2026: athenahealth launched agentic patient communication tools including Waitlist Scheduling, auto-filling cancelled slots via AI, and Enhanced Patient Self-Scheduling, plain-language appointment matching, deployed across a provider network serving 1 in 5 Americans.

Global AI In Medical Scheduling Software Market Report Scope

As per the scope of the report, AI in medical scheduling software refers to the use of artificial intelligence technologies to optimize and automate the process of scheduling appointments, staff shifts, and resource allocation within healthcare settings. It leverages machine learning algorithms, natural language processing, and data analytics to improve efficiency, reduce wait times, prevent scheduling conflicts, and enhance patient and staff satisfaction. AI-powered medical scheduling software can analyze patient needs, provider availability, and other factors to create dynamic, flexible schedules tailored to the specific demands of healthcare facilities.

The segmentation for AI in the medical scheduling software market is categorized by workflow type, AI functionality, deployment type, user type, medical specialty, and region. By workflow type, it includes scheduling patient appointments, coordinating care team schedules, scheduling procedures and resources, and omnichannel and access-center scheduling. By AI functionality, it covers predictive scheduling techniques, conversational AI for scheduling, rules-based and recommendation-driven scheduling, optimizing capacity and automating waitlists, and triage-led and intent-aware scheduling approaches. By deployment type, it is segmented into cloud solutions, on-premise installations, and hybrid models. By user type, it includes hospitals and health systems, clinics and physician groups, ambulatory surgical centers, diagnostic and imaging centers, and other users. By medical specialty, it is divided into primary care, behavioral and mental health, cardiology, orthopedics, oncology, dental services, and other specialties. By region, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Patient Appointment Scheduling |

| Care Team Scheduling |

| Procedure and Resource Scheduling |

| Access-Center and Omnichannel Scheduling |

| Predictive Scheduling |

| Conversational AI Scheduling |

| Rules-Based and Recommendation Scheduling |

| Capacity Optimization and Waitlist Automation |

| Triage-Led and Intent-Aware Scheduling |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Hospitals and Health Systems |

| Clinics and Physician Groups |

| Ambulatory Surgical Centers |

| Diagnostic and Imaging Centers |

| Other End Users |

| Primary Care |

| Behavioral and Mental Health |

| Cardiology |

| Orthopedics |

| Oncology |

| Dental |

| Other Specialities |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Scheduling Workflow | Patient Appointment Scheduling | |

| Care Team Scheduling | ||

| Procedure and Resource Scheduling | ||

| Access-Center and Omnichannel Scheduling | ||

| By AI Capability | Predictive Scheduling | |

| Conversational AI Scheduling | ||

| Rules-Based and Recommendation Scheduling | ||

| Capacity Optimization and Waitlist Automation | ||

| Triage-Led and Intent-Aware Scheduling | ||

| By Deployment Model | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End User | Hospitals and Health Systems | |

| Clinics and Physician Groups | ||

| Ambulatory Surgical Centers | ||

| Diagnostic and Imaging Centers | ||

| Other End Users | ||

| By Specialty | Primary Care | |

| Behavioral and Mental Health | ||

| Cardiology | ||

| Orthopedics | ||

| Oncology | ||

| Dental | ||

| Other Specialities | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving adoption of AI in medical scheduling software?

Growth is being driven by provider demand for better attendance, lower manual workload, stronger self-scheduling, and tighter workflow integration. The category is projected to rise from USD 263.45 million in 2026 to USD 902.39 million by 2031 at a 27.92% CAGR.

Which workflow segment currently leads revenue?

Patient appointment scheduling led with 41.31% share in 2025 because it is the most common entry point for automation and serves the broadest provider base.

Which capability is growing fastest through 2031?

Capacity optimization and waitlist automation is the fastest-growing capability with a 29.52% CAGR through 2031, reflecting provider demand to backfill cancelled slots and improve utilization automatically.

Why are clinics and physician groups adopting these tools faster?

Clinics and physician groups are forecast to grow at a 29.83% CAGR through 2031 because lower-cost, easier-to-deploy platforms now offer enterprise-style scheduling functions without large implementation budgets.

Which specialty shows the strongest growth outlook?

Behavioral and mental health is expected to grow at a 28.35% CAGR through 2031, supported by provider shortages, long waitlists, and the high role of telehealth in mental health access.

Which region is growing the fastest?

Asia-Pacific leads regional growth with a 30.83% CAGR through 2031, while North America remained the largest region in 2025 with a 47.24% share.

Page last updated on: