Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

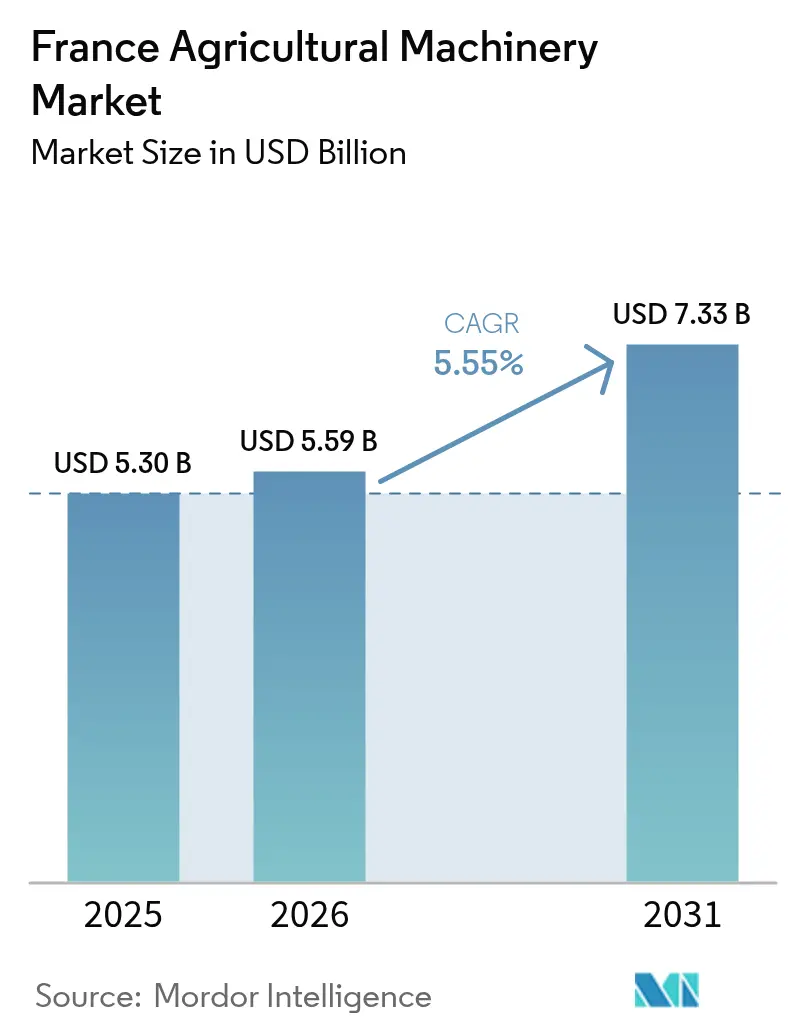

| Base Year Market Size (2025) | USD 5.30 Billion |

| Market Size (2026) | USD 5.59 Billion |

| Market Size (2031) | USD 7.33 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Agricultural Machinery Market Analysis by Mordor Intelligence

The agricultural machinery market size in France was valued at USD 5.30 billion in 2025 and estimated to grow from USD 5.59 billion in 2026 to reach USD 7.33 billion by 2031, at a CAGR of 5.55% during the forecast period (2026-2031). Robust mechanization demand stems from a shrinking farm labor pool, mounting climate-resilience needs, and subsidy-backed precision-farming programs that reward smart equipment adoption. High-horsepower tractor purchases indicate a pivot toward fewer but more capable assets, while water-efficient irrigation systems gain traction as aquifer stress intensifies. International manufacturers continue localizing parts distribution and service networks, and emerging contractor fleets are channeling equipment-as-a-service models to smaller holdings. Together these forces create a dynamic yet policy-steered growth pathway for the agricultural machinery market.

Key Report Takeaways

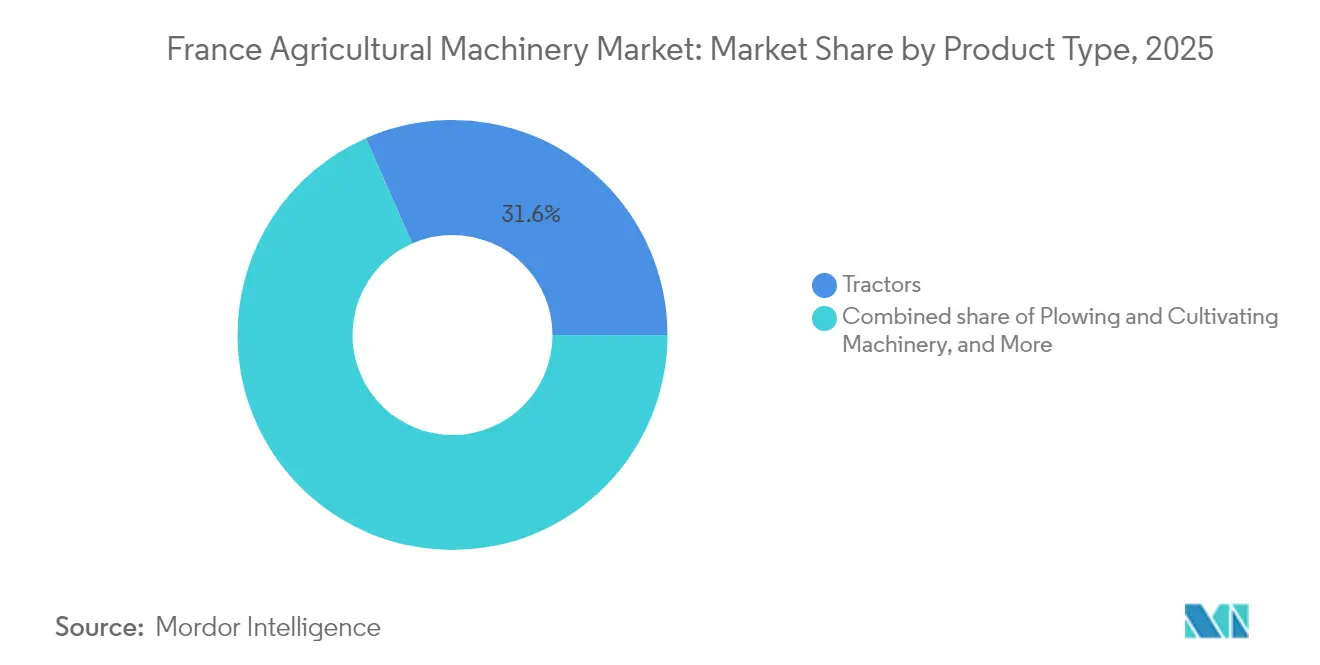

- By product type, tractors led with a 31.60% of france agricultural machinery market share in 2025. Irrigation machinery is forecast to expand at a 23.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing shortage of agricultural labor | +1.2% | National, with acute impact in Île-de-France, and Normandy | Short term (≤ 2 years) |

| Growing demand for high-horsepower tractors in large farms | +0.8% | National, concentrated in Beauce, and Champagne regions | Medium term (2-4 years) |

| Government subsidies for precision farming equipment | +1.5% | National, enhanced in rural development zones | Short term (≤ 2 years) |

| Rising need for climate-smart machinery | +0.9% | National, priority in drought-prone southern regions | Medium term (2-4 years) |

| Adoption of autonomous field robots by contractor fleets | +0.7% | National, early adoption in Picardy, and Centre-Val de Loire | Long term (≥ 4 years) |

| Growth of equipment-as-a-service financing models | +0.4% | National, accelerated in high-debt farming regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Shortage of Agricultural Labor

The Ministry of Agriculture's permanent scheme for seasonal agricultural worker assistance, introduced in the 2025 budget, exempts employers from contributions for hires under specific salary thresholds, yet fails to address the structural decline in available workers[1]Source: Direction de l’Information Légale et Administrative, “2025 Budget: What Measures for Agriculture?” service-public.fr. This labor scarcity is driving unprecedented adoption of autonomous weeding robots, with companies like Naïo Technologies reporting 100% electric robots achieving work rates up to 1,000 square meters per hour, effectively replacing manual labor in organic farming operations where chemical alternatives are prohibited. The contractor fleet model is emerging as a critical solution, allowing smaller farms to access sophisticated automation without capital investment, while contractors achieve economies of scale across multiple operations.

Growing Demand for High-Horsepower Tractors in Large Farms

The consolidation of French agriculture into larger operational units is driving a fundamental shift in power requirements, with tractors exceeding 300 horsepower experiencing high registration growth in 2024 despite overall market contraction. This trend reflects the economic reality that large-scale operations in regions like Beauce and Champagne require equipment capable of handling wider implements and faster field operations to maintain profitability margins compressed by input cost inflation. French farms averaging over 200 hectares increasingly view high-horsepower tractors as productivity multipliers rather than mere field implements, justifying premium pricing through reduced labor requirements and enhanced operational flexibility.

Government Subsidies for Precision Farming Equipment

With a budget of USD 432 million, the France 2030 initiative stands as the most pivotal policy move in agricultural mechanization. The initiative offers subsidies of 20-40% on the purchase of innovative equipment. Targeted technologies include drones for monitoring natural resources, connected sensors, autonomous weeding robots, and systems that treat livestock waste to produce organic fertilizers. By emphasizing a reduction in chemical inputs, the program not only aligns with regulatory trends but also frames these subsidized purchases as essential investments in compliance rather than mere upgrades. This initiative is projected to significantly boost the agricultural machinery market in France by driving demand for advanced precision agriculture technologies and fostering innovation among equipment manufacturers to meet the program's requirements.

Rising Need for Climate-Smart Machinery

Water resource constraints have reached critical levels in France, with more than half share of aquifers experiencing drainage conditions and four departments under water use restrictions as of May 2025, creating urgent demand for irrigation efficiency technologies. Smart micro-irrigation systems that optimize water use through IoT sensors and data analytics are becoming essential infrastructure rather than optional upgrades, particularly in southern regions where traditional rainfall patterns have become unreliable. The integration of weather monitoring and soil moisture sensors with irrigation machinery enables farmers to maintain productivity while reducing water consumption by up to 30%, creating both environmental compliance and operational cost benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and maintenance cost | -1.1% | National, acute in small farm regions | Short term (≤ 2 years) |

| Data ownership and cyber-security concerns | -0.6% | National, heightened under GDPR compliance | Medium term (2-4 years) |

| Grid capacity limits for electrified machinery charging | -0.4% | Rural areas, remote farming regions | Long term (≥ 4 years) |

| Fragmented digital standards inhibiting interoperability | -0.3% | National, affecting precision agriculture adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Maintenance Cost

The average price of precision-enabled tractors has increased 15-20% over conventional alternatives, while maintenance costs for GPS guidance and autonomous systems require specialized technician expertise that commands premium service rates. Equipment-as-a-service models are emerging as a partial solution, allowing farmers to access advanced machinery through operational expense structures rather than capital investments, though adoption remains limited by contractor availability in remote regions.

Data Ownership and Cyber-Security Concerns

The Fédération nationale des syndicats d'exploitants agricoles's (FNSEA) Data Agri charter mandates explicit consent for equipment-generated data use, and compliance raises software costs while making farmers wary of cloud-stored agronomic maps. The certification process for Data Agri compliance, verified by independent experts, creates an additional layer of operational complexity that may slow technology adoption among risk-averse farming operations concerned about data security breaches or competitive intelligence leakage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tractors Anchor Revenue Growth and Irrigation Machinery Delivers Fastest Expansion

Tractors contributed 31.60% agricultural machinery market share in 2025, cementing their role as the power and data hub for modern French farms. Demand clusters at ≥ 150 horsepower where advanced hydraulics support variable-rate seeders and smart sprayers. Below 50 horsepower, specialty vineyard units face pressure from muted wine margins. Registrations fell to 2,531 units in 2024. The agricultural machinery market size for the high-horsepower subclass is forecast to outpace overall equipment spending between 2026 and 2031 as large holdings in Beauce consolidate land and pursue fewer passes per hectare. Digital retrofits, such as Global Navigation Satellite System (GNSS) antennas and ISOBUS UT displays, push resale values higher, extending trade-in cycles while raising lifetime service revenues for dealers. Combined with subsidy-driven demand for auto-guidance, tractor Original Equipment Manufacturer (OEMs) are layering subscription telematics and over-the-air updates to lock in post-sale recurring income opportunities.

Irrigation equipment registers a 23.1% CAGR, the highest among product lines, as farms seek drought resilience amid tightened abstraction quotas. Drip systems dominate high-value fruit and vegetable acres, whereas center-pivot retrofits with variable-rate sprinklers are more suitable for broad-acre cereals. The agricultural machinery market size for connected micro-irrigation kits is poised to grow by 2031, enabled by France 2030 grants covering soil-sensor-linked pumps. Cloud dashboards cluster multiple pivots, weather stations, and fertigation injectors, allowing contractors to oversee dispersed clients. OEMs are integrating 4G/LTE gateways factory-side to simplify edge-to-cloud connectivity under General Data Protection Regulation (GDPR) consent protocols.

Geography Analysis

Northern France’s large-scale cereal farms exhibit the highest mechanization intensity, with the Paris Basin alone accounting for nearly 30% of the country's national tractor power sales. The agricultural machinery market size in the Île-de-France, Picardy, and Centre-Val de Loire corridor is forecast to expand as consolidation drives high-horsepower upgrades.

In contrast, Mediterranean departments allocate their equipment budgets chiefly to irrigation machinery and climate-smart sprayers, reflecting the vulnerability of specialty crops to water scarcity. Drip-line subsidies under the extended drought-protection program cover up to 40% of investment, accelerating adoption of sensor-led micro-irrigation systems that integrate with field-server platforms.

Western livestock regions such as Brittany and Pays de la Loire sustain stable demand for forage harvesters, balers, and manure spreaders. OEMs see an opportunity to upsell slurry injectors linked to nutrient-mapping software that supports CAP nutrient-runoff compliance. Dealer density in these dairy hubs outpaces other areas, reducing downtime and reinforcing brand loyalty. Together, these diverse regional drivers create a balanced national sales profile for the agricultural machinery market.

Regulatory Landscape

Agricultural machinery placed on the French market must comply with EU harmonized machinery safety rules, along with French obligations under the Labor Code, including employer duties on the safe use of equipment. Typical compliance steps include a documented risk assessment, a technical file, user instructions in French, and CE marking under the EU machinery framework (Directive 2006/42/EC). The Machinery Regulation (EU) 2023/1230 is scheduled to apply from January 2027, which is pushing OEMs and importers to update conformity documentation and safety-by-design processes ahead of that date.

For agricultural and forestry vehicles used on public roads, the EU type-approval framework under Regulation (EU) No 167/2013 applies, alongside national road-use requirements under the French Highway Code and the December 19, 2016 order referenced for agricultural vehicle road approval. On technical standards, safety design and guarding practices reference NF EN ISO 4254-1 (including its 2021 amendment), plus product-family standards such as NF EN ISO 4254-20 (2025) for harvesting machinery. France 2030 support administered through FranceAgriMer also steers compliance-linked purchases for innovative irrigation and other smart equipment.

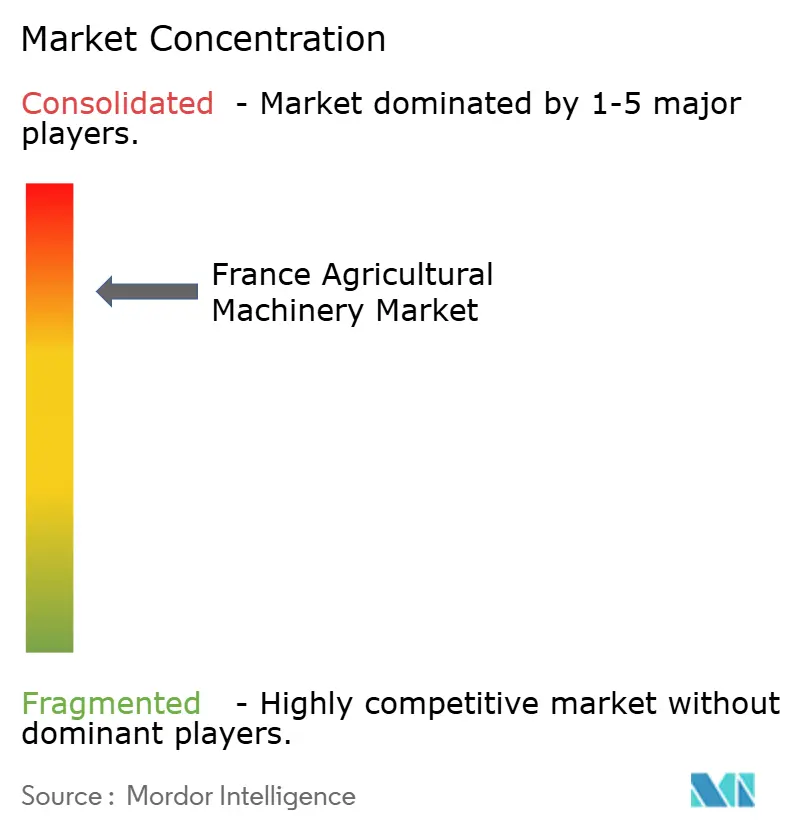

Competitive Landscape

Global majors CNH Industrial N.V., AGCO Corporation, Deere & Company, Claas KGaA mbH, and Kubota Corporation hold technological and financing scale that smaller rivals cannot match, yet regional brands thrive in niche segments like vineyard tractors and specialty harvesters. Manufacturers’ top-five combined agricultural machinery market share is estimated to be more than half, indicating moderate concentration.

AGCO’s EUR 87 million (USD 94 million) parts distribution center in Amnéville consolidates five depots, slashing delivery lead times from 72 hours to 24 hours for 11,000 French dealers and workshops in January 2025[4]Source: AGCO Corporation, “AGCO Announces New European Parts Distribution Centre in France,” agcocorp.com. CNH Industrial N.V.’s strategic plan in 2025 aims for 16-17% EBIT margins by 2030 through USD 550 million in operational savings and a tripling of Precision Tech revenue share.

Technology partnerships differentiate offerings. New Holland’s alliance with Bluewhite embeds autonomous navigation in orchard tractors, targeting 85% operating-cost savings and reinforcing brand credibility in the specialty-crop belt. Meanwhile, SDF Group positions SAME vineyard tractors as historically rooted yet digitally upgraded, appealing to terroir-focused estates wary of multinational suppliers. Hybrid models of pay-per-acre equipment services are emerging, with dealer-owned fleets providing on-demand access to robotic weeders, trimming both capex and skill barriers for smallholders.

France Agricultural Machinery Industry Leaders

AGCO Corporation

Kubota Corporation

Deere & Company

Claas KGaA mbH

CNH Industrial N.V.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-backed modernization and localization programs are creating near-term opportunities for OEMs, suppliers, and service partners that can bundle equipment, software, and compliance-ready documentation into subsidy-eligible offers. France 2030 funding targets sustainable and intelligent agricultural equipment, with around EUR 200 million in credits cited for localization and industrialization of equipment innovations, and a EUR 65 million France 2030 research program focused on the agroecology and digital interface. This supports a pipeline for robotics, sensing, and decision-support integration, which can raise attach rates for guidance, telematics, and retrofit kits.

Demand-side opportunities are most concentrated where regulation, labor constraints, and climate stress translate into buying triggers. Water-use restrictions in multiple departments as of May 2025 increase the business case for connected micro-irrigation, sensor-linked pumping, and variable-rate irrigation retrofits. Meanwhile, farm data governance and interoperability concerns favor vendors whose product design and contracting align with FNSEA-associated Data Agri charter practices and GDPR consent handling. On collaboration, the Ministry of Agriculture approved 19 Mixed Technological Networks (RMT) starting January 1, 2026 for five years, including themes such as agricultural robotics and labor renewal, which should provide a channel for pilots, field validation, and pre-commercial scaling with French farms, contractors, and research partners.

Recent Industry Developments

- June 2026: CLAAS announced a EUR 50 million investment plan for its French industrial sites, including the Woippy facility, under the Choose France 2026 initiative. The program supports modernization and industrial capability in France, reinforcing local production footprints and supplier linkages for key haying and forage equipment lines sold into the French market.

- May 2026: CLAAS began serial production of the ARION 6.190 CMATIC tractor at its Le Mans facility. Bringing a new tractor variant into series output supports domestic availability and can tighten lead times for dealers serving high-utilization segments that prioritize power, automation, and service continuity.

- April 2024: AGCO acquired an 85% stake in PTx Trimble, expanding its precision agriculture technology portfolio across guidance, autonomy, precision spraying, connected farming, and data management. The deal strengthens AGCO-aligned offerings available through French dealer networks, supporting higher-value technology bundling on tractors and mixed-fleet precision retrofits.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the France agricultural machinery market is defined as the value of farm machinery and implements sold for agricultural field operations in France, tracked in current USD across the study period.

Scope exclusions: Used equipment resale between farms, pure forestry-only machinery, and after-sales service labor are not counted unless bundled in a new equipment transaction.

Segmentation Overview

- By Product Type

- Tractors

- Below 50 HP

- 50 - 99 HP

- 100 - 149 HP

- 150 HP and Above

- Plowing and Cultivating Machinery

- Plows

- Harrows

- Rotovators and Cultivators

- Other Equipment

- Planting Machinery

- Seed Drills

- Planters

- Spreaders

- Other Planting Machinery

- Sprayers

- Irrigation Machinery

- Drip Irrigation Systems

- Sprinkler Irrigation Systems

- Other Irrigation Machinery

- Harvesting Machinery

- Combine Harvesters

- Other Harvesting Machinery

- Haying and Forage Machinery

- Mowers and Conditioners

- Balers

- Other Haying and Forage Machinery

- Other Types

- Tractors

Data Sources, Market Sizing, and Validation

Desk Research

We start by building the fact base around French farm activity, equipment demand signals, and policy context, then we translate it into a set of sizing inputs.

Public sources we use include statistics and releases from bodies such as INSEE, the French Ministry of Agriculture and Food Sovereignty, Eurostat, and FAOSTAT, to understand farm structure, cropping patterns, and machinery-relevant indicators.

To keep pricing and unit assumptions realistic, we also review manufacturer annual reports, investor presentations, and reputable press coverage on product launches and dealer network moves. Patent databases are used as a directional check on technology push areas (such as precision features) that can affect mix and average selling prices. Where available, we use paid subscriptions for company financials and an import export shipment-level database to cross-check trade flows and company exposure before finalizing assumptions.

The desk sources listed above are illustrative only, and additional public and paid sources are used for data collection, validation, and clarification.

Primary Interviews and Surveys

Next, we validate the desk assumptions through expert interviews and structured surveys across the value chain, including equipment makers, dealer networks, rental and service businesses, and large farm operators and cooperatives. Since this is a country market, the fieldwork is concentrated in France, and the focus is on clarifying pricing movements, replacement cycles, and how subsidy and compliance needs shift buying timing and product mix.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | |

| Mid tier: 57% | Functional/Unit leaders: 30% | |

| Smaller Players: 17% | Managers: 58% |

Market-Sizing & Forecasting

The core model uses a top-down build that starts from France equipment demand pools. We convert farm area, crop mix, mechanization intensity, and replacement cycles into annual unit needs, then value these using average selling price bands by machinery category.

To keep totals grounded, we run selective bottom-up checks using supplier revenue exposure to France, dealer channel checks, and sampled ASP multiplied by estimated volumes for a few high-weight product groups.

Key inputs for this market include tractor and harvester replacement timing, utilization levels for contracting and rental fleets, shifts in mix toward higher-horsepower or feature-rich equipment, and the pace of precision attachments being added to standard equipment. We also track agricultural production signals and farm income sentiment indicators because they often influence when large-ticket purchases move from planning to contracting.

Forecasting is done with scenario analysis. The base case reflects expert views on subsidy continuity, financing availability, and expected price progression, and stress cases test sensitivity around demand delays or faster technology adoption. When a bottom-up proxy is incomplete for smaller private players, gap handling is done through channel share assumptions that are checked against interview feedback and reconciled back to the top-level demand pool.

Data Validation & Update Cycle

Outputs are checked in more than one way so the final figures do not depend on a single assumption. We compare model totals against independent signals such as import patterns, manufacturer commentary on France performance, and observed pricing direction in dealer quotes. When we see outliers, we review and correct them if the driver does not align with practical replacement behavior or price movement.

Before sign-off, the model and assumptions go through multi-step internal reviews, and respondents are re-contacted when a large variance shows up in a key variable like replacement cycle, ASP movement, or category mix. The report is refreshed annually, and interim updates are made when material events occur, such as a policy change or a sharp pricing swing. Right before delivery, we complete a final validation pass so clients get the latest updated view.

Mordor Intelligence's France Agricultural Machinery Market Sizing Compared With Other Published Estimates

Published market numbers for France agricultural machinery can look far apart, even when they appear to cover a similar equipment set. The differences usually come from what is counted as the market boundary, the year and currency timing used, and how pricing and replacement demand are translated into a value total.

Import patterns, dealer-level pricing direction, and replacement cycle checks are the evidence points that anchor Mordor Intelligence's estimate to the new equipment demand visible in France, rather than mixing in broader manufacturing output or service-heavy revenues. Differences also show up when some publications fold forestry machinery into the same bucket, or when they report a manufacturing industry turnover number that includes exports, which can raise the headline size versus a France demand-side spend view.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.30 B (2025) | |

| Industry Publisher A | USD 5.80 B (2024) | Uses an earlier base year and a broader inclusion set that explicitly emphasizes digital and automation-related technology content, which can shift mix and pricing without clearly isolating France new-equipment transaction value. |

| Industry Database B | USD 10.64 B (2026) | Represents a manufacturing industry value that is reported in EUR and then converted, and it can capture production turnover and exports alongside domestic sales, which does not match a France demand-side spending scope. |

The comparison shows that most of the spread is explained by scope and accounting boundaries, not a true disagreement on equipment activity. By keeping the market tied to observable France buying drivers (units, replacement behavior, and price bands) and then cross-checking against trade and channel signals, the final number stays traceable and repeatable for planning use.

Key Questions Answered in the Report

How large is the agricultural machinery market in France in 2026?

It is valued at USD 5.59 billion and is projected to reach USD 7.33 billion by 2031.

What is the expected CAGR for French farm equipment spending through 2031?

The overall market is forecast to grow at 5.55% annually between 2026 and 2031.

Which product category leads sales in France?

Tractors hold a 31.60% market share, making them the top revenue contributor in 2025.

Which segment is growing fastest?

Irrigation machinery shows a 23.1% CAGR as farms invest in water-efficient systems.

How are government subsidies influencing machinery adoption?

France 2030 grants covering 20-40% of eligible equipment costs accelerate purchases of precision farming and climate-smart technologies.

What role do contractor fleets play in equipment access?

Contractors lease high-tech machinery to small farms, spreading ownership costs and easing labor constraints while boosting equipment utilization.

Page last updated on: