Garden And Orchard Tractors Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

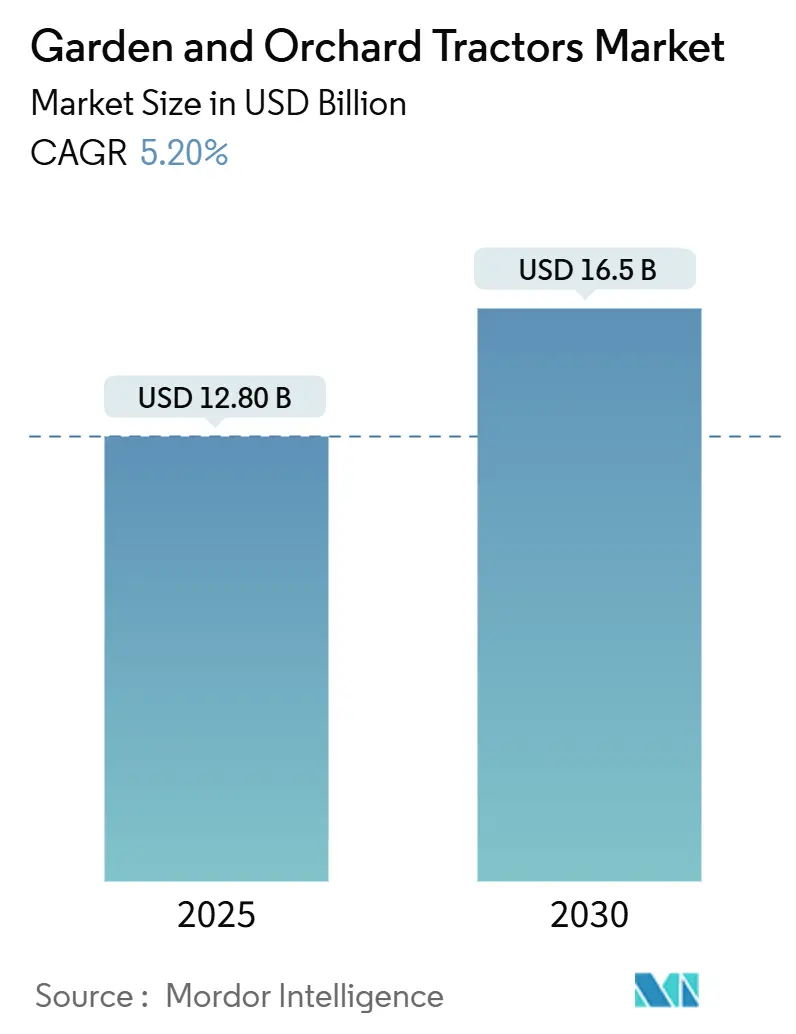

| Market Size (2025) | USD 12.80 Billion |

| Market Size (2030) | USD 16.5 Billion |

| Growth Rate (2025 - 2030) | 5.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

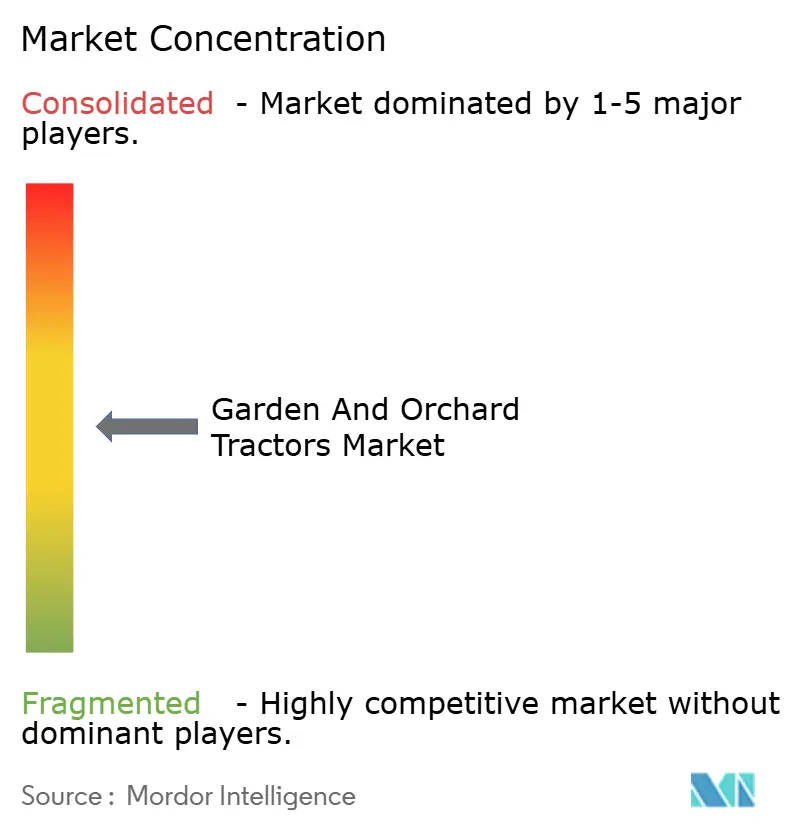

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Garden And Orchard Tractors Market Analysis by Mordor Intelligence

The garden and orchard tractors market size stands at USD 12.8 billion in 2025 and is forecast to reach USD 16.5 billion by 2030, reflecting a 5.2% CAGR through 2030. Growth rests on the convergence of fragmented landholdings, suburban landscaping activity, and the shift toward high-value specialty crops, all of which favor sub-60-horsepower platforms over traditional row-crop tractors. Compact diesel models still dominate unit shipments, yet zero-emission regulations in California and the European Union are accelerating the commercialization of electric and hybrid alternatives, which now close the total-cost-of-ownership gap after accounting for subsidies. Precision agriculture retrofits, from GNSS (Global Navigation Satellite System) section control to LiDAR-guided sprayers, are extending equipment life and generating recurring software revenue, while Original Equipment Manufacturer (OEM) embedded finance programs unlock pent-up demand among smallholders who typically lack hard collateral.

Key Report Takeaways

- By type, garden type tractors captured 61.0% of the garden and orchard type tractors market share in 2024, while orchard tractors are projected to expand at a 6.8% CAGR through 2030.

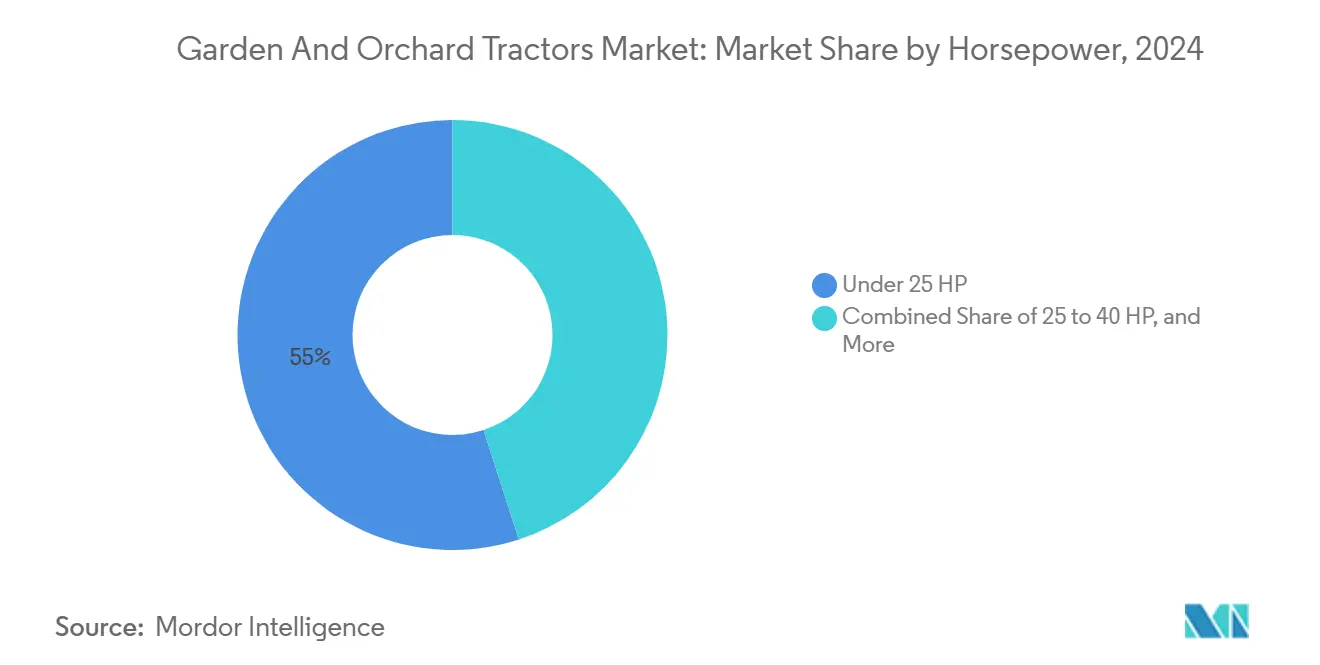

- By horsepower, the under 25-horsepower segment accounted for 55.0% of the garden and orchard tractors market size in 2024, while the 25 to 40-horsepower segment is forecast to grow at a 7.2% CAGR between 2025 and 2030.

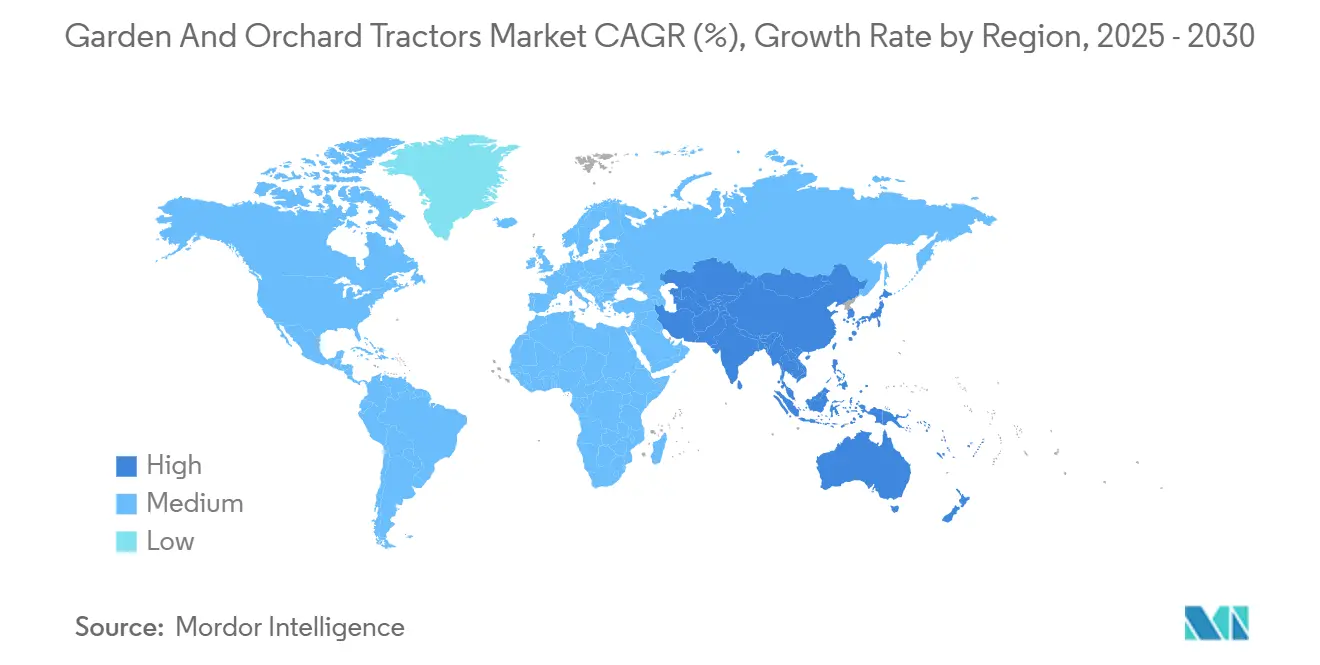

- By geography, North America accounted for roughly 37% of the global revenue in the garden and orchard tractors market in 2024. The Asia-Pacific region is anticipated to register a 6.8% CAGR through 2030, the fastest among all regions.

Global Garden And Orchard Tractors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government subsidies for compact mechanization | +1.2% | Asia-Pacific, Africa, South America, North America, Europe | Medium term (2-4 years) |

| Precision-farming retrofits for narrow-row crops | +0.9% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Rising lawn-and-garden care spending in suburbs | +0.7% | North America, Western Europe, Oceania | Short term (≤ 2 years) |

| Original Equipment Manufacturer (OEM) embedded-finance platforms for smallholders | +1.0% | Asia-Pacific, Africa, South America, Eastern Europe | Medium term (2-4 years) |

| Surge in electrified sub 40 HP tractor launches | +0.8% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Edge-AI safety packages for maneuvering in orchards | +0.5% | North America, Europe, Asia-Pacific premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Compact Mechanization

Fragmented landholdings in Asia-Pacific and Africa are driving national governments to prioritize compact tractor subsidies as a catalyst for food security and rural income growth. China's 2024 agricultural machinery purchase subsidy program allocated funds, with a significant percentage earmarked for tractors with a horsepower of under 40, directly benefiting manufacturers such as YTO Group and Lovol Heavy Industry [1]Source: Ministry of Agriculture China, “2024 Agricultural Machinery Purchase Subsidy Program,” moa.gov.cn. India's Sub-Mission on Agricultural Mechanization offers state-level rebates of 40-50% on compact tractors. In 2024, Maharashtra disbursed a major amount for power sprayers and narrow-row cultivators used in pomegranate and grape orchards. These fiscal interventions are expanding the addressable market for garden and orchard tractors annually, as they lower the payback period for mechanization investments in emerging economies.

Precision-Farming Retrofits for Narrow-Row Crops

Orchard and vineyard operators are retrofitting compact tractors with GPS-guided variable-rate application systems and ISOBUS-compatible implements to optimize input costs and comply with regulations that reduce pesticide use. Kubota's K-Monitor 2 terminal, launched in 2024, integrates section control and prescription mapping for tractors as small as 25 horsepower, enabling California walnut growers to reduce fungicide use by 22% while maintaining yield. TeeJet Technologies' Matrix 430VF display, certified for vineyard sprayers in 2024, utilizes canopy-sensing LiDAR to adjust nozzle flow rates in real-time, resulting in a modest percentage reduction in chemical waste in French Champagne vineyards.

Rising Lawn-and-Garden Care Spending in Suburbs

North American suburban expansion and home-improvement activity are sustaining demand for garden-type tractors in the 15 to 25 horsepower range, as residential lot sizes above 0.5 acres favor ride-on mowers with front-end loader attachments over walk-behind equipment. Professional landscaping services in the United States are upgrading to diesel-powered garden tractors with hydrostatic transmissions and quick-attach implements to service multiple properties per day, resulting in a 15 to 20% reduction in labor costs compared to walk-behind crews. This suburban demand contributes modest percentage points to annual growth, although it remains concentrated in North America and Western Europe, with limited spillover to the Asia-Pacific or Africa regions.

Original Equipment Manufacturer (OEM) Embedded-Finance Platforms for Smallholders

Manufacturers are deploying digital lending platforms that bypass traditional bank intermediaries, using telematics data and crop-yield proxies to underwrite tractor loans for farmers with limited credit histories. John Deere Financial's revolving credit plan, introduced in India in 2024, approves compact tractor loans within a shorter timeframe compared to traditional timelines, utilizing smartphone-based income verification to reduce documentation requirements and expand credit access to farmers with less than 2 hectares of land. CNH Industrial's Raven Finance platform, piloted in Kenya and Tanzania in 2024, utilizes satellite imagery of field conditions to adjust repayment schedules during drought years, resulting in a reduction of default rates compared to conventional microfinance loans.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tractor-rental marketplaces cannibalizing sales | −0.8% | Asia-Pacific, Africa, South America, Eastern Europe | Short term (≤ 2 years) |

| Uneven rural credit access in emerging markets | −1.1% | Africa, Asia-Pacific, South America | Medium term (2-4 years) |

| Dealer-service gaps for specialty narrow tractors | −0.6% | Africa, Middle East, South America, rural Asia-Pacific | Medium term (2-4 years) |

| Raw-material price volatility inflating MSRP (Manufacturer's Suggested Retail Price) | −0.7% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tractor-Rental Marketplaces Cannibalizing Sales

Digital platforms offering pay-per-use access to compact tractors are suppressing new-unit sales in price-sensitive markets, as smallholders with seasonal demand opt for rental sessions at USD 60 to USD 70 per four-hour block rather than purchasing equipment with payback periods of 8 to 10 years. Hello Tractor, operating in 18 African countries, facilitated tractor-rental transactions, with average session durations of 3.5 to 4.5 hours for plowing and harrowing. TAFE's JFarm Services platform, active in 12 Indian states, registered 295,000 users in 2024 and coordinated 680,000 rental sessions, with compact tractors under 30 horsepower accounting for a modest percentage of bookings. Brazil's EM3 AgriServices offers subscription-based access to garden tractors for smallholder vegetable growers, charging USD 160 to 240 per month for unlimited use.

Uneven Rural Credit Access in Emerging Markets

High interest rates, stringent collateral requirements, and limited branch networks in rural areas are constraining tractor purchases in Africa, South Asia, and South America, where credit-to-GDP ratios remain 30 to 50% points below OECD averages. Sub-Saharan Africa's credit-to-GDP ratio averaged 24 to 30% in 2024, with banks in Kenya, Nigeria, and Tanzania demanding collateral of 180 to 220% for agricultural equipment loans and imposing interest rates of 14 to 18%, effectively excluding smallholders with less than 5 hectares from formal credit markets [2]Source: World Bank, “Commodity Markets Outlook 2024,” worldbank.org . Indonesia's state-owned banks disbursed only 12% of agricultural credit for equipment purchases in 2024, with the remainder allocated to seeds, fertilizers, and working capital. This leaves tractor demand dependent on government subsidy programs that cover 30 to 40% of the purchase costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Garden Tractors Dominate Residential and Municipal Demand

Garden tractors held a 61.0% market share in 2024, reflecting their versatility for residential lawn care, municipal landscaping, and hobby farming applications. Garden tractors, typically equipped with mid-mount mowing decks, front-end loaders, and hydrostatic transmissions, serve North American suburban properties exceeding 0.5 acres and European municipal contracts requiring daily operation across multiple sites. Garden tractors are also gaining traction in the Asia-Pacific region, with Japan's residential construction boom and Australia's peri-urban expansion driving demand for sub-25-horsepower. Orchard tractors remain a niche market in the region due to limited vineyard acreage outside of South Australia and Victoria.

Orchard models are forecasted to grow at a 6.8% CAGR from 2025 to 2030 as specialty crop mechanization intensifies in Mediterranean and California production zones. Orchard-type tractors, characterized by narrow profiles (1.2 to 1.8 meters), low centers of gravity, and ROPS-certified cabs, are gaining traction in California's orchards and Spain's 967,000 hectares of vineyards, where row widths of 2.5 to 3.5 meters demand specialized chassis designs. Orchard models are benefiting from precision-agriculture retrofits, with TeeJet's Matrix 430VF display enabling variable-rate spraying that reduces chemical use in French Champagne vineyards. Meanwhile, garden tractors are seeing the adoption of electric drivetrains, with Fendt's e100 V Vario securing 320 pre-orders from German municipalities seeking to comply with urban noise ordinances.

By Horsepower: Sub 25 HP Leads, 25 to 40 HP Gains Momentum

The under-25-horsepower segment commanded a 55.0% market share in 2024, driven by its suitability for residential lawn care, smallholder vegetable cultivation, and inter-row mowing in vineyards. Sub 25-horsepower tractors, priced at USD 10,000 to 20,000, dominate India's compact tractor market, where the maximum percentage of landholdings is smaller than 2 hectares, and North America's residential segment, where lot sizes of 0.5 to 1.0 acres favor ride-on mowers with tractor-like capabilities [3]Source: Reserve Bank of India, “Financial Inclusion Report 2024,” rbi.org.in. Kubota's BX-Series, the best-selling sub-25-horsepower line in North America, shipped a significant number of units in 2024, with a major percentage purchased by homeowners and small-scale farmers.

The 25 to 40 horsepower band is projected to expand at a 7.2% CAGR through 2030 as orchard operators upgrade to cab-equipped platforms with ISOBUS compatibility. The 25 to 40 horsepower band is also seeing electric entrants, with Monarch's MK-V delivering 40 horsepower of continuous and 70 horsepower of peak output from a 110-kilowatt-hour battery. This model targets California almond and walnut growers who benefit from the United States Department of Agriculture Environmental Quality Incentives Program (USDA's EQIP) subsidies, which cover 50 to 60% of the purchase costs.

Geography Analysis

North America held the largest market share, at 37%, in 2024, driven by demand for suburban lawn care, professional landscaping activities, and the adoption of precision agriculture in California's specialty crop belt. The Outdoor Power Equipment Institute reported that lawn and garden equipment sales in the United States experienced significant growth, with compact tractors and zero-turn mowers contributing a notable share of the revenue. This growth is linked to residential lot sizes that favor ride-on platforms over walk-behind equipment. In Canada, residential construction activity remained strong, with single-family homes in Ontario and British Columbia having larger lot sizes, driving a replacement cycle for garden tractors over time.

The Asia-Pacific region is forecast to expand at a 6.8% CAGR from 2025 to 2030, the fastest among all regions, as government subsidies, smallholder mechanization programs, and rising labor costs converge to drive compact tractor adoption in India, China, and Southeast Asia. China has allocated funds for agricultural machinery purchases in 2024, with a significant portion designated for tractors under 40 horsepower. This allocation is anticipated to benefit domestic manufacturers, including YTO Group and Lovol Heavy Industry. Meanwhile, India's Sub-Mission on Agricultural Mechanization has provided state-level rebates on compact tractors. For instance, Maharashtra has allocated resources specifically for power sprayers and narrow-row cultivators.

The European garden and orchard tractor market is growing at a slow rate among major regions, as mature markets in Germany, France, and the United Kingdom face saturation of the replacement cycle, offset by the adoption of orchard mechanization in Mediterranean countries and the introduction of electric tractors driven by Stage V emissions compliance.

Competitive Landscape

The garden and orchard tractors market exhibits moderate concentration, with the top five players, including Deere & Company, CNH Industrial N.V., Kubota Corporation, AGCO Corporation, and Mahindra & Mahindra Ltd., holding a significant combined share in 2024. Embedded-finance platforms, electric-tractor startups, and pay-per-use rental marketplaces are fragmenting traditional dealer channels and compressing new-unit margins.

Opportunities are emerging in electric propulsion below 30 horsepower, where battery costs of USD 128 to 133 per kilowatt-hour in 2025 enable price parity with diesel models when subsidies cover 50 to 60% of upfront costs, and in autonomous orchard platforms, where ISO 18497 series standards updated in 2024 permit supervised autonomy in confined spaces with row widths as narrow as 1.5 meters. Monarch Tractor, Solectrac, and Bobcat's AT450X are disrupting the California specialty-crop segment, yet incumbents retain advantages in dealer networks, parts availability, and brand trust.

Strategy patterns include vertical integration into precision software (AGCO-Trimble PTx, Kubota-Agtonomy), embedded-finance platforms that bypass bank intermediaries (John Deere Financial, Kubota Credit), and electric-powertrain partnerships to share battery-development costs (CNH-Nikola, AGCO-Cummins). Technology is becoming the primary competitive catalyst, with edge-AI safety packages, telematics-enabled predictive maintenance, and ISOBUS-compatible implements differentiating premium models from commodity offerings, yet price sensitivity in emerging markets sustains demand for basic diesel platforms.

Garden And Orchard Tractors Industry Leaders

Deere & Company

CNH Industrial N.V.

Kubota Corporation

AGCO Corporation

Mahindra & Mahindra Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Kubota Corporation announced a partnership with Agtonomy to develop the M5N autonomous orchard tractor, targeting commercial availability in 2027 for Japanese apple and pear orchards. The collaboration integrates Agtonomy's edge-AI vision systems with Kubota's 30-horsepower diesel platform, enabling supervised autonomy for mowing, spraying, and inter-row cultivation in confined spaces with row widths as narrow as 1.5 meters.

- June 2024: Mahindra & Mahindra Ltd unveiled its strategy to broaden its global footprint, targeting Western Europe and ASEAN (The Association of Southeast Asian Nations) to strengthen its international standing for Orchard and other types of Tractors in its lineup. Mahindra Tractors is set to make its Asia-Pacific debut in Thailand in 2024, with plans to venture into Western Europe in 2025. The company has set an ambitious goal to double its international business within the next three years.

- February 2024: AGCO Corporation launched the Massey Ferguson 3 Series Specialty tractor in North America. Tailored for the distinct needs of vineyards and orchards, the MF 3 Series offers seven models, boasting horsepower between 75 and 115, ensuring reliable performance in a new market.

Global Garden And Orchard Tractors Market Report Scope

Garden and Orchard Tractors Market Report is Segmented by Type (Orchard Tractor and Garden Tractor), by Horsepower (Under 25 HP, 25 To 40 HP, 41 To 60 HP, and Above 60 HP), and by Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

| Orchard Tractor |

| Garden Tractor |

| Under 25 HP |

| 25 to 40 HP |

| 41 to 60 HP |

| Above 60 HP |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Turkey |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Type | Orchard Tractor | |

| Garden Tractor | ||

| By Horsepower | Under 25 HP | |

| 25 to 40 HP | ||

| 41 to 60 HP | ||

| Above 60 HP | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the garden and orchard tractors machinery market be by 2030?

The sector is forecast to reach USD 16.5 billion by 2030, rising from USD 12.8 billion in 2025.

Which tractor type is growing fastest?

Orchard-specific models are projected to advance at a 6.8% CAGR through 2030 as specialty-crop mechanization accelerates in Mediterranean and Californian regions.

Which companies dominate the competitive landscape?

Deere & Company, CNH Industrial N.V., Kubota Corporation, AGCO Corporation, and Mahindra & Mahindra Ltd.. controlled a significant share of 2024 shipments, underscoring a moderately concentrated competitive landscape.

Why is Asia-Pacific the most dynamic region?

Generous subsidies, rising labor costs, and fragmented landholdings propel a 6.8% regional CAGR, with China and India leading adoption.

Page last updated on: