Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

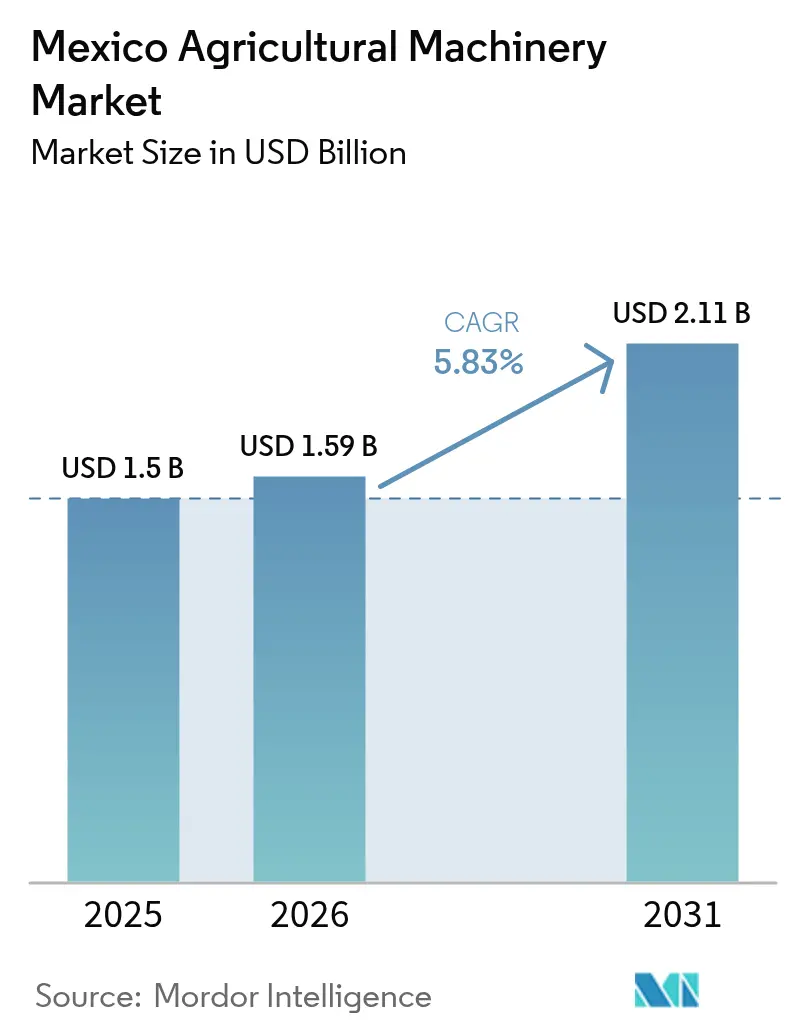

| Base Year Market Size (2025) | USD 1.5 Billion |

| Market Size (2026) | USD 1.59 Billion |

| Market Size (2031) | USD 2.11 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

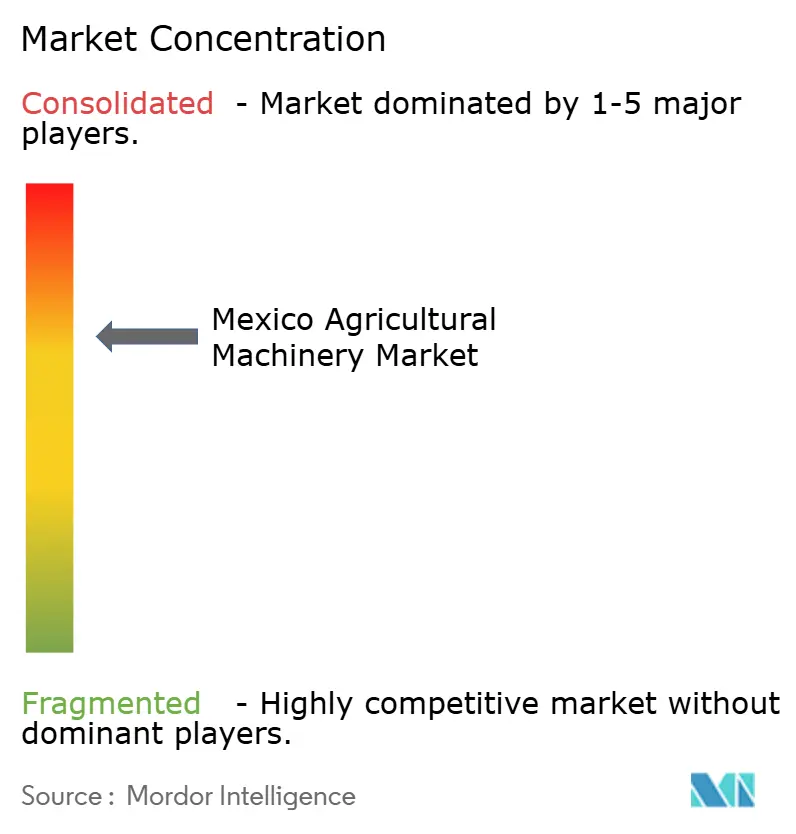

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mexico Agricultural Machinery Market Analysis by Mordor Intelligence

The Mexico agricultural machinery market size is expected to grow from USD 1.5 billion in 2025 to USD 1.59 billion in 2026 and is forecast to reach USD 2.11 billion by 2031 at 5.83% CAGR over 2026-2031. Farm consolidation, consistent public budget allocation, zero-tariff machinery imports, and increased adoption of precision irrigation systems drive the market growth. According to the United States Department of Agriculture, Mexico's domestic corn consumption increased from 44,000 metric tons to 45,700 metric tons from 2022 to 2023. This increase in consumption indicates rising food demand, which necessitates improved crop productivity through agricultural advancements, including agricultural machinery. The Mexican government increased its agricultural budget by 5% in 2024, demonstrating its support for sector modernization[1]Source: U.S. Department of Agriculture, “Mexico: Mexico’s 2024 Agricultural Budget Maintains Focus on Social Programs,” fas.usda.gov. Agricultural trade grew by 700% in 2024, creating significant demand for efficiency-enhancing equipment. Government financing programs focus primarily on medium-sized farms (5-20 hectares), while the growth in protected agriculture increases demand for water-efficient technologies. Global manufacturers are expanding their market presence through local manufacturing facilities and smart-leasing programs, improving equipment access for small-scale farmers.

Key Report Takeaways

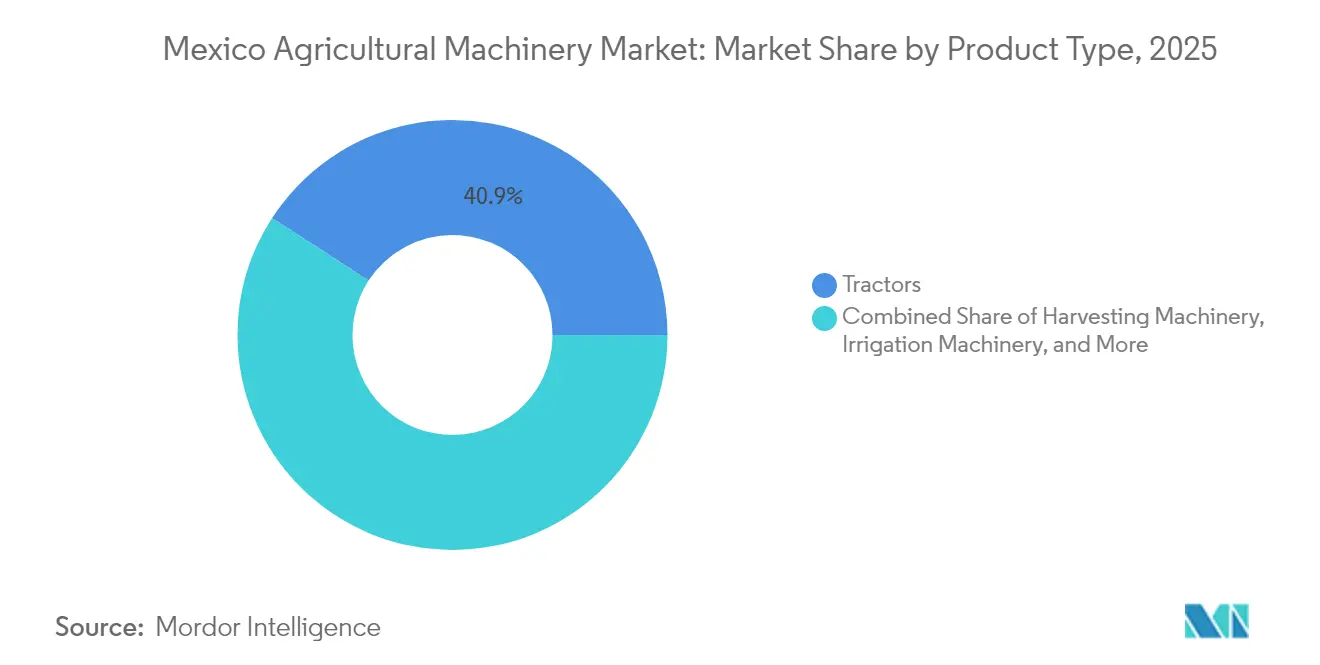

- By product type, tractors led the Mexico agricultural machinery market with a 40.85% share in 2025, while irrigation machinery is projected to grow at a 9.92% CAGR through 2031.

- By farm size, the medium (5–20 hectare) farm held 46.95% Mexico agricultural machinery market share in 2025, while small farms (less than 5 hectares) are projected to expand at a 7.08% CAGR to 2031.

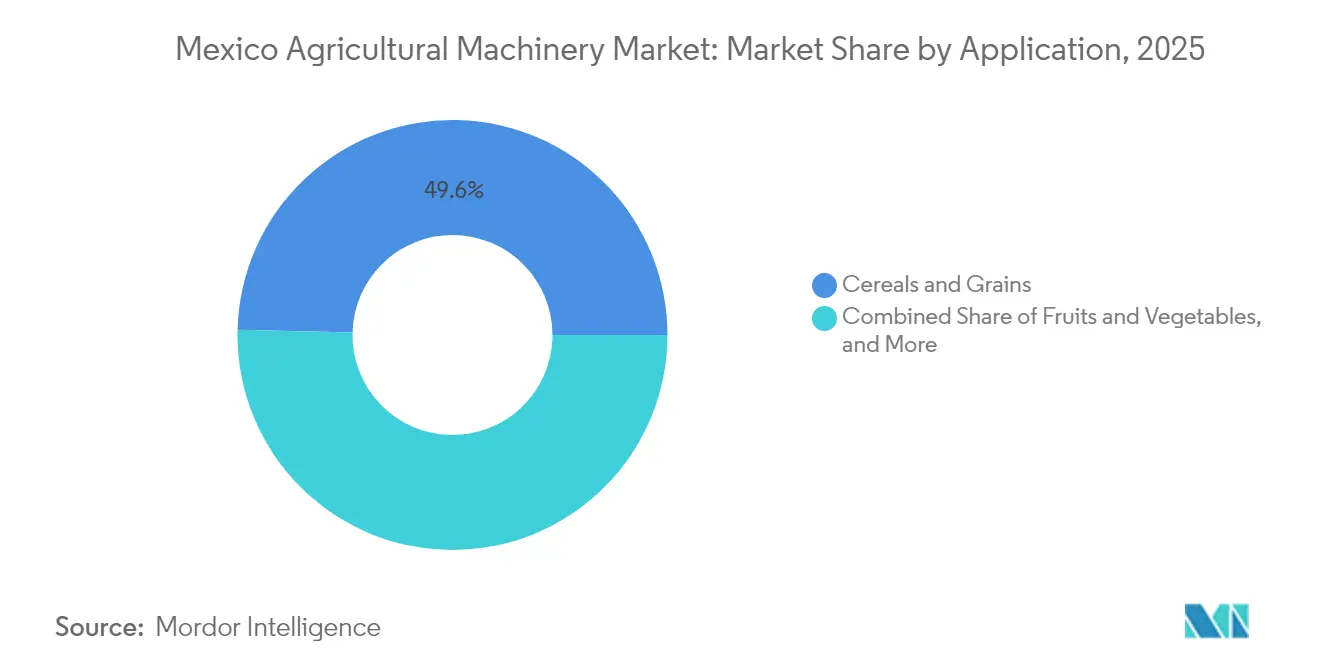

- By application, cereals and grains accounted for a 49.62% share of the Mexico agricultural machinery market size in 2025, while fruits and vegetables are projected to advance at a 9.42% CAGR through 2031.

- Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra Ltd. generated significant revenue in 2024, supported by ongoing capacity additions and captive financing arms.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Mexico Agricultural Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-hectare farm consolidation accelerates mechanization | +1.2% | National, concentrated in Sinaloa, Sonora, and Jalisco | Medium term (2-4 years) |

| Federal subsidies for agricultural machines | +1.0% | National, stronger in central and northern states | Short term (≤ 2 years) |

| Tariff-free machinery imports lowering acquisition cost | +0.7% | National, border states benefit most | Short term (≤ 2 years) |

| Rebound in protected-agriculture acreage | +1.1% | Northwest Mexico with Sinaloa leading | Medium term (2-4 years) |

| Dealer-financed credit expansion by Original Equipment Manufacturer (OEM) captive lenders | +0.6% | National, urban-adjacent farming regions | Medium term (2-4 years) |

| Emergence of smart-leasing platforms for seasonal equipment | +0.5% | National, technology-forward producers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sub-Hectare Farm Consolidation Accelerates Mechanization

Land policy reforms in Mexico enable farmers to consolidate small parcels for joint operations, leading to equipment-sharing arrangements. In Sinaloa and Sonora states, agricultural cooperatives reduce per-hectare operational costs through shared tractors and harvesters. A study in the Toluca Valley reveals a tractor-to-land ratio of 12.8 hectares per tractor, compared to the Food and Agriculture Organization's (FAO) recommended 50 hectares per tractor, indicating significant equipment underutilization. The consolidation of farmland addresses this inefficiency through shared ownership models. This arrangement facilitates the adoption of precision agriculture technologies, as advanced equipment can now service multiple adjacent plots[2]Source: Instituto Nacional de Investigaciones Forestales Agrícolas y Pecuarias, “Evaluación del nivel de mecanización tecno-agrícola en seis municipios del Valle de Toluca,” inifap.gob.mx. Communities with established cooperative practices demonstrate higher rates of participation in machinery sharing programs.

Federal Subsidies for Agricultural Machines

The Special Concurrent Program allocated USD 24.4 billion in January 2025 for irrigation and precision-agriculture equipment purchases. Foreign Inward Remittance Advice (FIRA) offices provide long-term credit, reducing acquisition barriers for mid-sized farms in the Mexico agricultural machinery market. The subsidy structure encourages locally assembled units, leading manufacturers to expand domestic production. Program adoption exceeds 70% in northern grain regions where established dealer networks facilitate enrollment. Dealers use federal incentives to offer integrated financing and after-sales service packages, driving increased demand[3]Source: U.S. Department of Agriculture, “USMCA, Canada, and Mexico – Mexico: Policy,” ers.usda.gov.

Tariff-Free Machinery Imports Lowering Acquisition Cost

The Presidential Anti-Inflation Decree maintains zero import duties on agricultural machinery through 2025. Dealers provide 10-15% discounts on precision planters and specialty harvesters not manufactured domestically, based on reduced landed costs. Border states experience expedited price reductions due to their proximity to import locations. Uncertainty regarding post-2025 tariffs has accelerated equipment purchases in the current cycle. The policy reduces greenhouse construction costs, facilitating investments in protected agriculture that require drip irrigation and climate-control systems.

Emergence of Smart-Leasing Platforms for Seasonal Equipment

Digital marketplaces now offer GPS-tracked equipment leasing pools for agricultural machinery, including planters, harvesters, and sprayers, which farmers utilize seasonally. Farmers who have implemented these platforms report cost reductions of 20-30% per hectare by paying for actual machine usage hours. The platforms establish consolidated maintenance agreements to maintain equipment uptime above 95% and utilize aggregated usage data to optimize lease rates. The initial implementation focused on regions with robust broadband coverage, with usage gradually expanding as rural mobile connectivity improves.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently high interest-rate environment | -1.4% | National, rural areas most affected | Short term (≤ 2 years) |

| Aging rural workforce reluctant to adopt new tech | -0.9% | National, concentrated in traditional farming regions | Long term (≥ 4 years) |

| Environmental and Regulatory Concerns | -0.6% | National, stricter enforcement in export-oriented regions | Medium term (2-4 years) |

| Security concerns in modern farming machinery | -0.5% | National, technology-intensive operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistently High Interest-Rate Environment

Rural loan interest rates are anticipated to remain 3-5% points higher than urban rates in 2025, even after anticipated rate reductions of 25-50 basis points. These elevated rates extend repayment periods for major equipment purchases. Mid-sized agricultural operations that do not qualify for government subsidies find precision farming equipment costs prohibitive compared to manual labor options. Financial institutions typically maintain higher risk premiums on rural loans due to the volatility of agricultural commodity prices and limited collateral options. Consequently, many farmers have switched from purchasing to leasing tractors or postponed equipment acquisitions, which has slowed market growth.

Security Concerns in Modern Farming Machinery

Agricultural producers express concerns about cloud-based telematics systems potentially exposing their operational data to competitors and regulatory bodies. GPS spoofing incidents and ransomware attacks on connected equipment in related agricultural sectors have increased these security concerns. As a result, some farmers disable data connectivity features, which affects the predictive maintenance capabilities essential to equipment manufacturers' service operations. This lack of trust impedes the adoption of autonomous tractors and remote software updates, particularly in high-value fruit and vegetable farming operations where equipment downtime can significantly impact production.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tractors Lead While Irrigation Gains Pace

Tractors account for 40.85% of Mexico's agricultural machinery market share in 2025, driven by their versatility in corn, wheat, and sorghum cultivation. Strategic manufacturing investments, such as John Deere's USD 55 million facility in Nuevo León in 2024, enhance after-sales support and customer retention. Harvesters maintain significance in sugarcane and cotton production regions but experience fluctuating demand based on commodity market conditions. Tillage equipment maintains a consistent market presence due to Mexico's extensive agricultural land area of 145 million hectares, requiring regular soil preparation.

The irrigation machinery segment grows at a 9.92% CAGR, addressing the agricultural sector's consumption of 76% of national water resources, despite 40% efficiency losses. Drip irrigation systems are prevalent in greenhouse operations, while center pivot systems expand in maize-growing regions with limited surface water access. Government initiatives promoting water efficiency provide subsidies for precision sprinkler systems, with dealers incorporating micro-nutrient injection systems for increased profitability. Manufacturers develop scalable pump systems to accommodate the expansion of protected cultivation areas.

By Farm Size: Medium Units Anchor Demand but Small Farms Accelerate

Medium farms spanning 5-20 hectares represented 46.95% of Mexico's agricultural machinery market share in 2025. These farms maintain the optimal balance between operational scale and management efficiency, positioning them as key beneficiaries of Foreign Inward Remittance Advice's (FIRA) agricultural credit programs. Through local equipment-sharing networks, these farms achieve over 1,000 annual operating hours for their primary tractors.

Small farms under 5 hectares are projected to grow at a 7.08% CAGR through 2031, supported by equipment rental services and digital leasing platforms. These farms predominantly utilize compact tractors below 70 HP due to field size constraints. While large farms require advanced equipment like high-capacity combines and GPS-enabled planters, their expansion remains restricted by land ownership regulations, limiting their overall machinery purchases.

By Application: Cereals Dominate, Fruits Accelerate

Cereal and grain operations account for 49.62% of Mexico's agricultural machinery market share in 2025. According to the Food and Agriculture Organization, maize cultivation, covering 64.3 million hectares in 2023, drives consistent demand for tractors, planters, and harvesters. Government price-support programs maintain equipment demand despite commodity price fluctuations.

The fruits and vegetables segment records a 9.42% CAGR, driven by expanding greenhouse operations in Sinaloa and Sonora for export production. Equipment requirements extend beyond traditional tillage machinery to include automated conveyors, climate-control fans, and high-pressure foggers. Protected agriculture facilities for tomatoes, peppers, and berries require specialized equipment for climate control, precision irrigation, and automated harvesting systems. Commercial crops, including cotton and sugarcane, remain significant in regional markets, particularly in northern states where large-scale operations support investments in advanced harvesting equipment. The application segmentation aligns with Mexico's agricultural export strategy, prioritizing mechanization investments and technology adoption for high-value crops.

Geography Analysis

The northern states of Mexico demonstrate advanced mechanization, particularly in Sinaloa, where protected-agriculture clusters utilize sophisticated irrigation systems and greenhouse tractors. The region's proximity to the United States' ports facilitates rapid freight transport and efficient spare parts delivery. The high concentration of equipment dealers in Culiacán and Hermosillo enables competitive financing options, driving increased mechanization in the Mexican agricultural machinery market.

In the central highland regions, including Mexico State and Puebla, mechanization adoption shows varied patterns. The Toluca Valley reports a tractor-to-land ratio of 12.81 hectares per tractor, indicating equipment underutilization. To address this, cooperative sharing initiatives maximize machine usage without requiring additional purchases. The government tests smart-leasing programs in these regions before implementing them nationwide.

Mechanization faces challenges in southern states such as Chiapas and Oaxaca due to land fragmentation and mountainous terrain. The agricultural sector adapts through the use of compact articulated tractors and walk-behind tillers, particularly in pineapple and coffee cultivation areas. Federal initiatives support mechanization by offering 50% subsidies on small-scale irrigation pumps, gradually increasing adoption despite geographical constraints.

Competitive Landscape

The Mexico agricultural machinery market exhibits moderate concentration, with the top five companies, Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Mahindra & Mahindra Ltd., holding the majority of market share in 2024. Deere & Company maintains market leadership through captive financing options, including 0% introductory rates for initial seasons. CNH Industrial N.V. ranks second, utilizing Case IH's Aguascalientes assembly facility to customize equipment for Mexican agricultural requirements. AGCO Corporation aims to double its precision technology revenue contribution to agricultural sales by 2030.

The industry competition now centers on data-driven services, with manufacturers integrating connectivity systems during production. These systems include fleet management platforms that enable fault detection and maintenance scheduling. New market entrants, particularly electric combine manufacturers, are promoting environmental sustainability, prompting established companies to develop alternative fuel technologies. Partnerships with agricultural financial technology platforms are expanding traditional leasing periods, increasing market accessibility.

After-sales service capabilities moderate price competition in the market. Companies with extensive rural service networks can maintain higher equipment prices due to farmers' need to minimize operational disruptions during critical harvest periods. Companies implementing local parts supply strategies reduce delivery times, strengthening customer relationships and expanding their market presence.

Mexico Agricultural Machinery Industry Leaders

Deere & Company

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

Mahindra & Mahindra Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Kubota North America formed a collaboration with Agtonomy, a developer of agricultural autonomy software, to implement autonomous operations for spraying and mowing on Kubota diesel tractors. This partnership aligns with Kubota's focus on developing solutions for specialty crop growers by providing technology that improves operational efficiency and productivity in North American countries, including Mexico.

- October 2024: Tractors and Farm Equipment Limited, one of the largest tractor manufacturers globally, established a subsidiary in Mexico to support its growing customer base. The expansion into the Mexican market represents a significant milestone following the company's successful introduction of its tractor range in Europe.

- June 2024: AGCO Mexico invested USD 45 million to expand its agricultural equipment manufacturing facilities in Corregidora, Queretaro. The investment highlights Queretaro's strategic importance as a manufacturing hub in Mexico's El Bajio region.

Mexico Agricultural Machinery Market Report Scope

Agricultural machinery refers to the agricultural devices and tools used in the agriculture process. These tools can be hand tools, power tools, and tractors used in farming or other agricultural processes.

The Mexican agricultural machinery market is segmented by tractors, equipment, irrigation machinery, harvesting machinery, and haying and forage machinery. The report offers the market size and forecasts in terms of value (USD) for all the above segments.

By Product Type

| Tractors | Engine Power | Less than 40 HP |

| 41 to 60 HP | ||

| 61 to 100 HP | ||

| 101 to 150 HP | ||

| More than 150 HP | ||

| Harvesting Machinery | Combine Harvesters | |

| Forage Harvesters | ||

| Other Harvesting Machinery (Sugarcane, Cotton, and Fruit and Vegetable Harvesters) | ||

| Irrigation Machinery | Drip Irrigation | |

| Sprinkler Irrigation | ||

| Other Irrigation Machinery (Boom Irrigation Machinery and Pivot Irrigation) | ||

| Haying and Forage Machinery | Mowers and Conditioners | |

| Balers | ||

| Other Haying and Forage Machinery (Windrowers and Tedders) | ||

| Tillage and Seed-bed Machinery | Plows | |

| Harrows | ||

| Rotovators and Cultivators | ||

| Other Equipment (Ridgers, Bed Shapers, etc.) |

By Farm Size

| Small (Less Than 5 ha) |

| Medium (5-20 ha) |

| Large (More Than 20 ha) |

By Application

| Cereals and Grains |

| Fruits and Vegetables |

| Oilseeds and Pulses |

| Commercial Crops |

| By Product Type | Tractors | Engine Power | Less than 40 HP |

| 41 to 60 HP | |||

| 61 to 100 HP | |||

| 101 to 150 HP | |||

| More than 150 HP | |||

| Harvesting Machinery | Combine Harvesters | ||

| Forage Harvesters | |||

| Other Harvesting Machinery (Sugarcane, Cotton, and Fruit and Vegetable Harvesters) | |||

| Irrigation Machinery | Drip Irrigation | ||

| Sprinkler Irrigation | |||

| Other Irrigation Machinery (Boom Irrigation Machinery and Pivot Irrigation) | |||

| Haying and Forage Machinery | Mowers and Conditioners | ||

| Balers | |||

| Other Haying and Forage Machinery (Windrowers and Tedders) | |||

| Tillage and Seed-bed Machinery | Plows | ||

| Harrows | |||

| Rotovators and Cultivators | |||

| Other Equipment (Ridgers, Bed Shapers, etc.) | |||

| By Farm Size | Small (Less Than 5 ha) | ||

| Medium (5-20 ha) | |||

| Large (More Than 20 ha) | |||

| By Application | Cereals and Grains | ||

| Fruits and Vegetables | |||

| Oilseeds and Pulses | |||

| Commercial Crops | |||

Key Questions Answered in the Report

What is the 2026 value of the Mexico agricultural machinery market?

The market stands at USD 1.59 billion in 2026.

How fast is the Mexico agricultural machinery market projected to grow through 2031?

It is projected to register a 5.83% CAGR, reaching USD 2.11 billion by 2031.

Which product category leads sales?

Tractors held 40.85% revenue share in 2025.

Why is irrigation machinery the fastest-growing segment?

Water scarcity and the expansion of protected agriculture push demand for precision irrigation, lifting the segment at a 9.92% CAGR.

Which farm-size bracket buys the most machinery?

Farms spanning 5–20 hectares captured 46.95% of purchases in 2025 because they balance scale and financing eligibility.

Page last updated on: