Asia-Pacific Agricultural Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

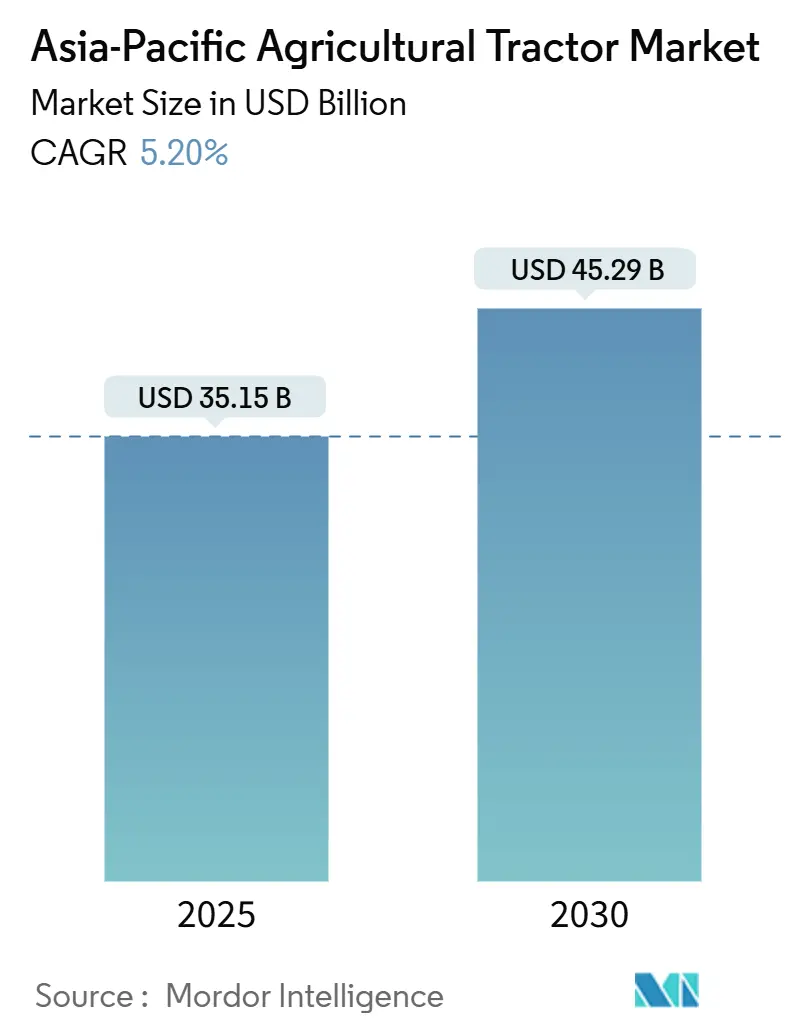

| Market Size (2025) | USD 35.15 Billion |

| Market Size (2030) | USD 45.29 Billion |

| Growth Rate (2025 - 2030) | 5.20% CAGR |

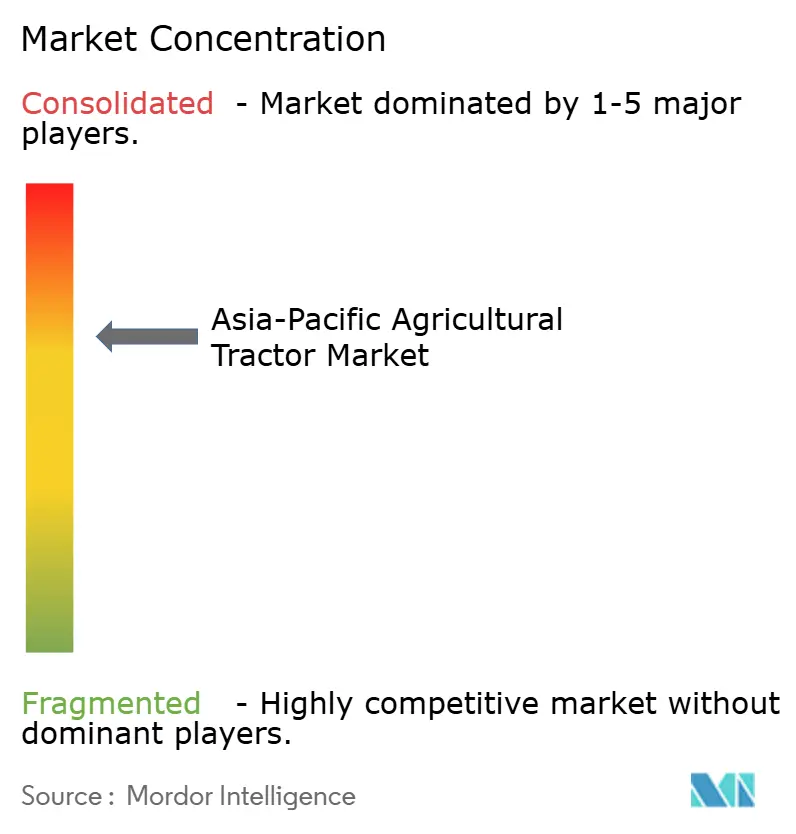

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Agricultural Tractor Market Analysis by Mordor Intelligence

The Asia-Pacific agricultural tractor market size was valued at USD 35.15 billion in 2025 and is projected to reach USD 45.29 billion by 2030, registering a 5.2% CAGR over the forecast period, underscoring a solid expansion trajectory anchored in mechanization demand across diverse farm structures. Labor shortages, generous equipment subsidies, and rapid uptake of precision agriculture tools continue to stimulate purchasing activity, while emerging pay-per-use models widen access for smallholder farmers. Diesel remains the dominant propulsion choice, yet electric and hybrid alternatives are gaining traction as regional governments link carbon-credit incentives to equipment upgrades. Competitive intensity is moderate, but pockets of fragmentation offer headroom for mergers, partnerships, and localized assembly ventures. Investments in autonomous platforms and mid-range horsepower tractors illustrate how suppliers balance affordability and performance to satisfy the core demand profile of rice- and grain-centric production systems.

Key Report Takeaways

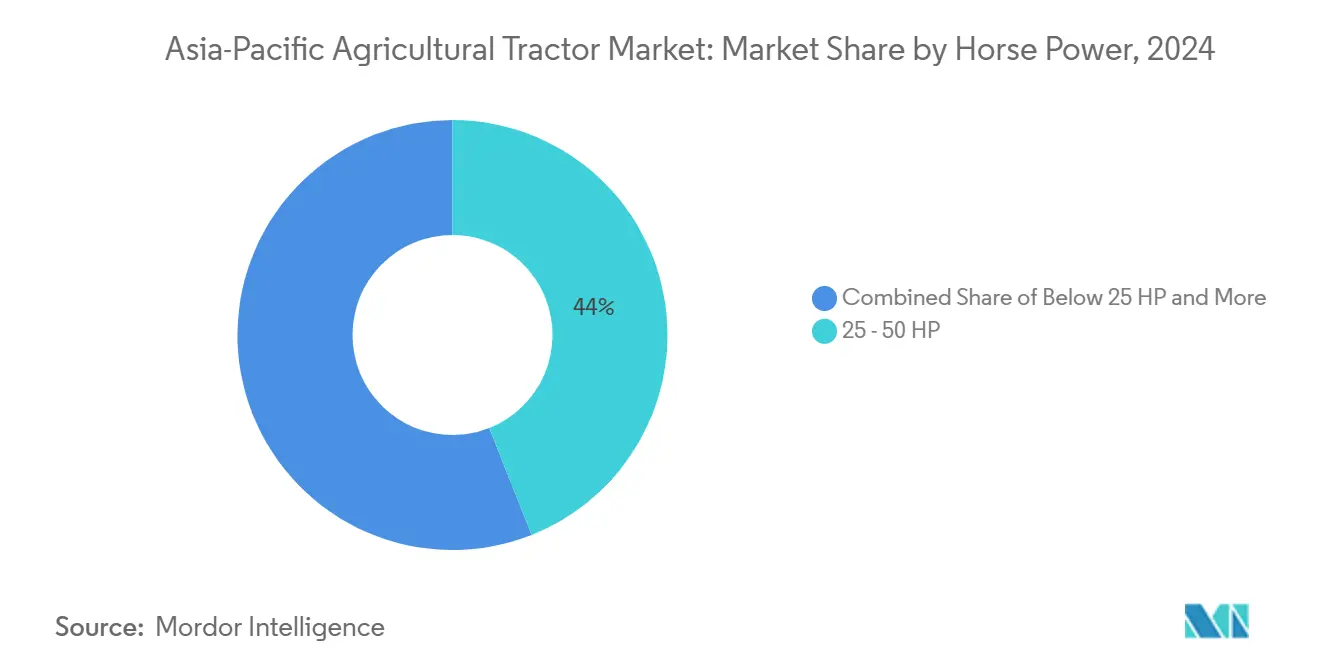

- By engine power, 25-50 HP units accounted for 44% of the Asia-Pacific agricultural tractor market share in 2024, while models above 150 HP are projected to expand at an 8.8% CAGR to 2030.

- By drive type, two-wheel-drive tractors dominated at 77% of 2024 revenue, and four-wheel-drive units are advancing at an 11.4% CAGR through 2030.

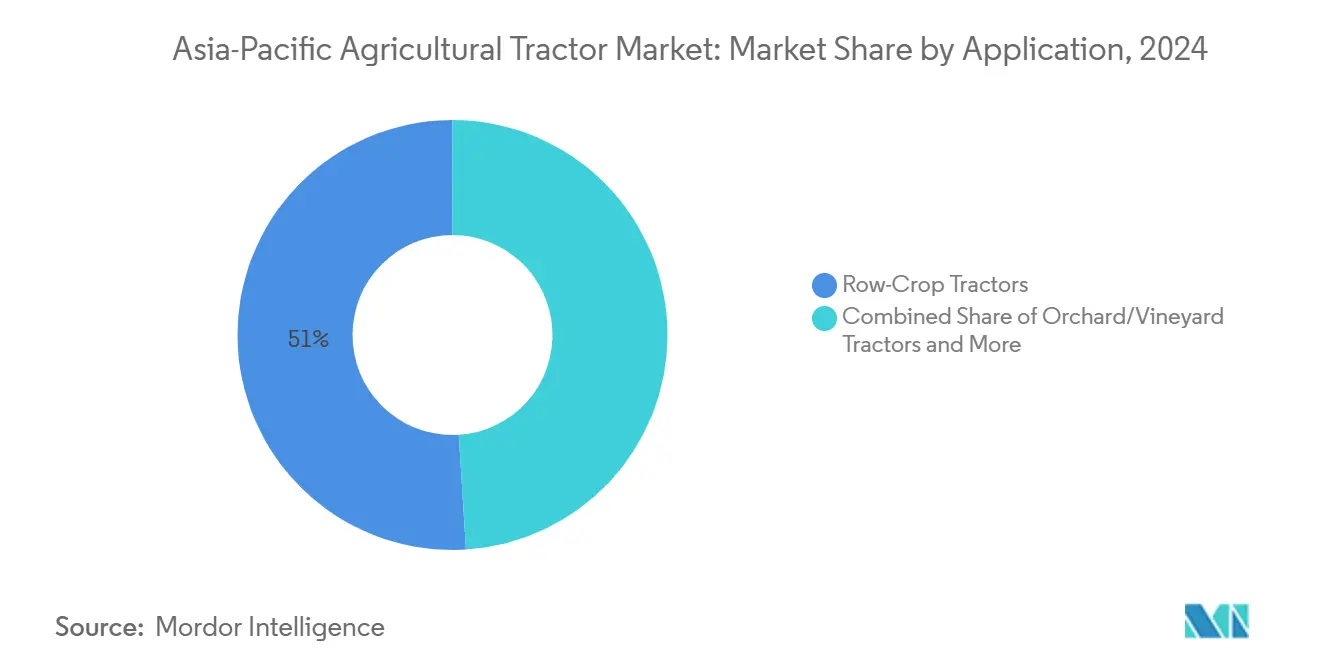

- By application, row-crop models led with 51% of the Asia-Pacific agricultural tractor market size in 2024, while crawler/track tractors are forecast to rise at a 13.2% CAGR through 2030.

- By geography, China commanded 39% of the 2024 value, while Vietnam is projected to post the fastest 6.5% CAGR through 2030.

Asia-Pacific Agricultural Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing farm mechanization rates | +1.8% | China, India, and Vietnam | Medium term (2-4 years) |

| Government subsidies and low-interest credit lines | +1.2% | China, India, Thailand, and Indonesia | Short term (≤ 2 years) |

| Rising labor costs and rural-to-urban migration | +0.9% | Japan, South Korea, and Australia | Long term (≥ 4 years) |

| Adoption of precision agriculture platforms | +0.7% | Australia, Japan, and South Korea | Medium term (2-4 years) |

| Pay-per-use tractor-as-a-service business models | +0.4% | India, Thailand, and Indonesia | Medium term (2-4 years) |

| Carbon-credit incentives for electric tractors | +0.2% | China, Japan, and Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Farm Mechanization Rates

Regional governments view mechanization as a pillar of food-security policy. Vietnam aims to increase its mechanization coverage in crop cultivation over the coming years. China maintains a higher mechanization density compared to other Southeast Asian countries like Vietnam and Thailand, highlighting substantial convergence potential for emerging markets. The World Bank extended a substantial loan in 2025 to boost eco-friendly equipment adoption in China, reinforcing fiscal backing for machinery upgrades. Japanese manufacturers are relocating capacity to Indonesia to answer rapidly rising regional demand. Such production shifts indicate that supply chains are evolving to align with the growth centers of the Asia-Pacific agricultural tractor market.

Rising Labor Costs and Rural-to-Urban Migration

Demographic changes are pushing wage levels higher, tightening the farm labor pool. Japan’s core farm-worker base halved over two decades, prompting local makers such as Kubota to divert capacity to lower-cost Asian plants while accelerating autonomous product pipelines[1]Source: Vietnam News Agency, "Japanese farm equipment maker plans to relocate capacity in Indonesia," theinvestor.vn. South Korea exhibits comparable pressure. Daedong Corporation plans to commercialize Level-4 autonomous tractors by the end of 2025 to address operator scarcity. Thailand’s agriculture gross domestic product is forecast to rebound moderately in the coming years, with Siam Kubota emphasizing smart-farming packages to offset labor deficits. Taiwan’s machinery-sharing programs featuring dry and wet leases illustrate regional strategies to raise equipment utilization rates under a shrinking labor supply.

Pay-per-Use Tractor-as-a-Service Business Models

Rental services soften capital-expenditure hurdles for smallholders who dominate regional farm structures. Mahindra & Mahindra Ltd.'s Trringo platform in Karnataka serves state-level tractor rental demand through a network of over 100 hubs supported by government funding. Similar pay-per-use ecosystems are emerging in Thailand and Indonesia, allowing owners to recover costs faster and renters to access specialized tools only when needed. The alignment of rental apps with telematics ensures real-time equipment health reporting, reducing downtime for both parties. Financiers increasingly bundle usage-based insurance into rental packages, further lowering risk exposure. This usage model creates secondary demand for mid-life refurbishment services, expanding aftermarket revenue streams for manufacturers and dealers.

Adoption of Precision Agriculture Platforms

Digitalization is redefining mechanization. Kubota’s smart-farming toolkit in Thailand boosted task efficiency through live soil-condition monitoring. Yanmar completed field trials in Thailand that integrated centimeter-grade positioning to run simultaneous tillage and seeding, financed in part by the Japan International Cooperation Agency[2]Source: Yanmar, "Yanmar Demonstrates Autonomous Agricultural Machinery at Joint Thailand-Japan Project," yanmar.com. South Korea’s LS Mtron launched a cloud-linked tractor data suite and unveiled the country’s largest autonomous-tractor experience hub to speed farmer training. The convergence of GPS, 5G, and artificial intelligence is steering the Asia-Pacific agricultural tractor market toward data-centric service models that lift yields while trimming resource use.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront purchase cost | −1.1% | India, Indonesia, Vietnam, and Philippines | Short term (≤ 2 years) |

| Limited farmer awareness and operator skills | −0.8% | Vietnam, Indonesia, Myanmar, and Cambodia | Medium term (2-4 years) |

| Fragmented landholdings limiting scale efficiencies | −0.6% | India, China, Thailand, and Philippines | Long term (≥ 4 years) |

| Import tariffs on high-power engines in selected nations in the region | −0.3% | Indonesia, Thailand, and Malaysia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Purchase Cost

Capital intensity restricts tractor penetration in lower-income rural pockets. Pakistan, where 64% of farms occupy fewer than 5 acres, posted only 35% mechanization, versus 70% in many European markets, illustrating affordability gaps. Banks often treat tractors as non-productive assets, quoting higher interest rates relative to crop loans, which inflates ownership cost. Manufacturers partially alleviate sticker shock through deferred-payment and bundled-service plans, though penetration remains skewed toward farmers with superior collateral. Rising used-equipment imports from Japan and South Korea offer a stopgap but raise maintenance complexity due to parts availability.

Limited Farmer Awareness and Operator Skills

Skill deficits lower utilization returns on sophisticated machinery. Vietnam satisfies only 32% of domestic equipment needs through local production, leaving a gap for imported models that require advanced operation and maintenance know-how. Training centers lag population needs, creating mismatches between equipment capabilities and field practices. South Korea leverages quality standards such as the Korean Standard Quality Excellence Index to promote intuitive tractor interfaces, with Daedong ranked first for tractors in 2024, reflecting deliberate design to reduce learning curves. Digitized dashboards with icon-based prompts and multilingual prompts improve accessibility but depend on robust rural connectivity infrastructure that remains uneven outside of advanced economies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Power: Mid-Range Versatility Spurs Volume Growth

The 25-50 HP band captured 44% of the Asia-Pacific agricultural tractor market in 2024 as small and medium paddies dominate rice-growing economies such as India and Vietnam. This horsepower range balances purchase cost with multi-crop versatility, encouraging repeat buys and fostering an expansive dealer-service network. Subsidy formulas in China and Thailand frequently use 50 HP as a rebate threshold, further steering demand into this bracket. Above 150 HP units, though accounting for a smaller installed base, are recording an 8.8% CAGR because commercial farms in Australia and consolidated Chinese holdings seek higher drawbar power for deep tillage and high-capacity planters.

The 101-150 HP band is evolving as an incremental upgrade path for medium farms that outgrow mid-range equipment yet cannot justify flagship models. In 2025, China revised policies to raise subsidies for high-horsepower tracked tractors and to introduce grants for intelligent control systems, signaling a push toward digital efficiency. South Korea is evaluating similar incentives within its Smart Farm Expansion Roadmap. As connectivity becomes integral, horsepower segmentation is blending with tech-readiness levels, compelling manufacturers to bundle sensors, guidance modules, and remote diagnostics even into lower-power offerings to retain buyer interest.

By Application: Row-Crop Preeminence and Autonomous Momentum

Row-crop tractors fulfilled 51% of 2024 deliveries, mirroring the predominance of cereal cultivation across China, India, and Southeast Asia. Their adjustable track width and PTO (power take-off) flexibility suit diverse row spacings, making them the default mechanization choice. Utility tractors trail closely, serving livestock and haulage roles on mixed farms.

Crawler/track tractors are forecast to rise at a 13.2% CAGR through 2030. Crawler/track tractors remain niche, favored in the Mekong Delta and Japanese paddy fields where low soil compaction is critical. Orchard and vineyard tractors cater to Australia’s expanding wine sector and China’s high-value fruit belts, underlining the geographic heterogeneity within the Asia-Pacific agricultural tractor market. YTO’s LF2204 cableless autonomous prototype incorporates 5G links, global positioning system guidance, and millimeter-wave radar to traverse fields without human supervision and is slated for commercial launch within five years. As autonomous functionality migrates into mainstream segments, traditional tractor-type boundaries may dissolve, replaced by modular chassis that accept swappable power and guidance units.

By Drive Type: Two-Wheel Simplicity Meets Four-Wheel Traction

Two-wheel-drive (2WD) tractors held 77% market share in 2024 because their lower acquisition cost aligns with the smallholder-dominated purchase profile across South and Southeast Asia. Four-wheel-drive (4WD) models are gaining at an 11.4% CAGR to 2030 as farms consolidate and cultivation shifts toward upland crops needing higher traction. In the Mekong Delta, government subsidy programs for waterlogged areas reimburse part of the cost of four-wheel-drive tractors, accelerating the shift from two-wheel-drive models.

Autonomous drive systems presently command a negligible share but are primed for an exponential upswing once regulatory trials graduate to commercial approval. South Korea completed national Level-3 autonomous trials in 2024, paving the way for Level-4 releases planned by Daedong at the close of 2025. The operational savings from driverless field passes may offset initial premiums within four seasons, according to pilot users in Japan. With telematics enabling over-the-air software updates, drive type may become a software-defined attribute rather than a hardware constraint, widening design flexibility for original-equipment manufacturers.

Geography Analysis

China remained the anchor, holding 39% of value in 2024, propelled by equipment upgrades and expanded subsidy categories, and lifted per-unit support for large tractors. YTO, a domestic manufacturer, increased its tractor production, supported by higher exports to Central Asia. International manufacturers are expanding their local presence, with Kubota planning to establish a tractor manufacturing facility in India.

Vietnam stands out with a projected 6.5% CAGR to 2030 as it pursues mechanization densities closer to regional peers. Domestic assembly meets only one-third of demand, ensuring sustained import reliance. Mekong Delta subsidy schemes for 4WD units and rice-harvest automation fuel above-trend growth. Rising penetration of pay-per-use services further accelerates uptake among fragmented landholdings.

India, Japan, Australia, South Korea, and Thailand display varied growth arcs. Australia experienced a cyclical dip in unit sales during the past year, yet retains a significant growth rate as commodity prices stabilize. South Korea channels strategic focus into autonomous technology exports, while Thailand leverages EV tax holidays to nurture electric tractor assembly. Together, these markets frame a mosaic where policy nuance and agronomic needs shape localized demand profiles.

Competitive Landscape

The Asia-Pacific agricultural tractor market hosts a moderately consolidated competitive field. Mahindra & Mahindra Ltd., Deere & Company, Kubota Corporation, CNH Industrial N.V., and Tractors and Farm Equipment Limited collectively commanded the majority share of revenue in 2024. Mahindra & Mahindra Ltd. leverages domestic scale to fund international forays and has expanded capacity across India to serve South American and African exports. Deere & Company invests in precision-ag stack integration, acquiring software start-ups that enable cloud-based agronomic insights for its 5E and 6B series. Kubota Corporation applies a dual-hub model, with Japanese factories reserved for premium segments and its forthcoming Indian facility focused on cost-optimized global mid-range models.

Daedong terminated a two-decade link with Deere & Company to accelerate proprietary platform development, including HX large tractors aimed at Level-4 autonomy by late 2025. The company simultaneously secured a substantial supply contract with Doosan Bobcat’s United States affiliate to broaden North American reach. AGCO Corporation partnered with SDF to co-develop sub-85 HP utility models, filling a product gap that accounts for a significant share of worldwide tractor demand [3]Source: AGCO Corporation, "AGCO and SDF Enter New Partnership to Strengthen Global Position in Low-Mid Horsepower Tractor Segment," agcocorp.com.

Strategic priorities converge on autonomy, electrification, and service monetization. Mahindra & Mahindra Ltd.’s Trringo rental platform exemplifies service innovation by generating recurring fees while seeding brand exposure among new-to-tractor farmers. Kubota Corporation and Yanmar Holdings Co., Ltd. invest in hydrogen-ready powertrains as insurance against battery-supply volatility. CNH Industrial N.V.’s New Holland brand pilots battery-swap field stations in Australia, testing uptime advantages. Such moves indicate that competitive differentiation is migrating from horsepower specifications to integrated solutions that blend hardware, software, and financing.

Asia-Pacific Agricultural Tractor Industry Leaders

-

Mahindra & Mahindra Ltd.

-

Deere & Company

-

Kubota Corporation

-

CNH Industrial N.V.

-

Tractors and Farm Equipment Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tractors and Farm Equipment Limited and AGCO Corporation have concluded a USD 260 million agreement, transferring complete ownership and exclusive rights of the Massey Ferguson brand to TAFE for India, Nepal, and Bhutan markets. This settlement terminates previous commercial arrangements between the companies and alters the competitive landscape in the Asia-Pacific agricultural tractor market.

- October 2024: At the 2024 China International Agricultural Machinery Exhibition, Zoomlion Agriculture Machinery Co., Ltd. displayed its DV3804 hybrid tractor (380 HP) and HEV500 hybrid powertrain. The company is expanding into high-performance and smart tractor segments. Zoomlion Agriculture Machinery Co., Ltd. is increasing its presence in Southeast Asia through artificial intelligence integration, digital solutions, and region-specific tractor models.

Asia-Pacific Agricultural Tractor Market Report Scope

A tractor is an industrial vehicle with one or two small wheels in front and two large wheels at the back for agricultural and other functions. It is used to move the attached implement that plows the field or performs different activities. For this report, tractors used in agricultural operations have been considered. The report does not cover other farm machinery and attachments to tractors. Tractors used for industrial and construction purposes are also excluded from the study.

Asia-Pacific agricultural tractor market is segmented by horsepower (less than 25 HP, 25-100 HP, and above 100 HP), type (orchard tractors, row crop tractors, and other types), and Geography ( China, India, Japan, Australia, and rest of Asia-Pacific). The report offers market size and forecasts for all the above segments in terms of value (USD).

| Below 25 HP |

| 25-50 HP |

| 51-100 HP |

| 101-150 HP |

| Above 150 HP |

| Row-Crop Tractors |

| Orchard/Vineyard tractors |

| Crawler/track tractors |

| Other Applications |

| Two-wheel drive (2WD) |

| Four-wheel drive (4WD) |

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Indonesia |

| Thailand |

| Vietnam |

| Rest of Asia-Pacific |

| By Engine Power | Below 25 HP |

| 25-50 HP | |

| 51-100 HP | |

| 101-150 HP | |

| Above 150 HP | |

| By Application | Row-Crop Tractors |

| Orchard/Vineyard tractors | |

| Crawler/track tractors | |

| Other Applications | |

| By Drive Type | Two-wheel drive (2WD) |

| Four-wheel drive (4WD) | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the 2025 value of the Asia-Pacific agricultural tractor market?

The market is valued at USD 35.15 billion in 2025.

How fast is the market projected to grow over 2025-2030?

A 5.2% compound annual growth rate is projected, lifting value to USD 45.29 billion by 2030.

Which tractor segment recorded the highest share in 2024?

Row-crop tractors led with 51% revenue share in 2024.

How dominant are diesel engines today?

By propulsion, diesel systems held a 90% share in 2024.

Page last updated on: