Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

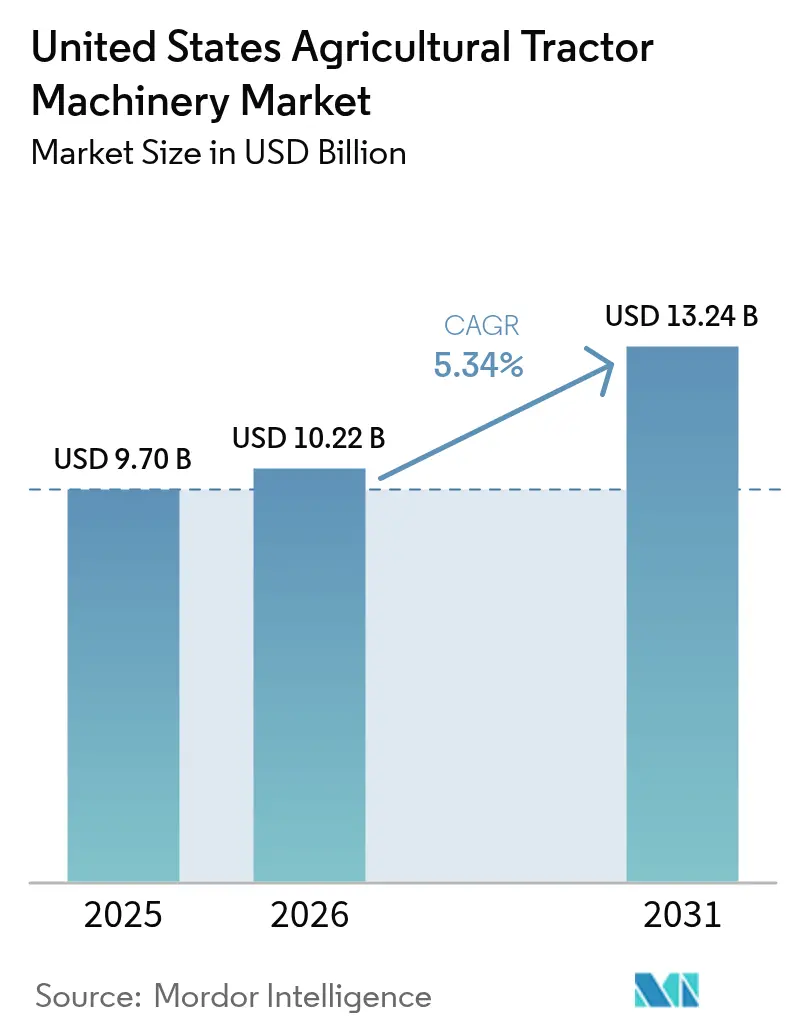

| Base Year Market Size (2025) | USD 9.7 Billion |

| Market Size (2026) | USD 10.22 Billion |

| Market Size (2031) | USD 13.24 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The United States agricultural tractor machinery market size was valued at USD 9.7 billion in 2025 and estimated to grow from USD 10.22 billion in 2026 to reach USD 13.24 billion by 2031, at a CAGR of 5.34% during the forecast period (2026-2031). The rising adoption of precision systems, the growing availability of electric attachments, and persistent labor cost inflation are driving a multi-year replacement cycle that extends beyond the usual fluctuations in farm income. Large farms are standardizing on sensor-rich implements that feed data into cloud software, which tightens brand lock-in and lifts aftermarket sales. Smaller specialty-crop operations are pivoting toward battery-electric units to comply with state emissions targets, while drought rules in the West are pushing investments in variable-rate irrigation-linked implements. At the same time, domestic sourcing prompted by Section 232 tariffs is reshaping supply chains and nudging prices upward. These cross-currents are fostering new dealer subscription models that spread capital outlays across seasons and convert sporadic equipment purchases into predictable service revenue.

Key Report Takeaways

- By product type, planting maching captured 30.62% of the United States agricultural tractor machinery market size in 2025, and sprayers are projected to expand at an 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Agricultural Tractor Machinery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Adoption of Precision Agriculture | +1.20% | Midwest, West, and Southeast | Medium term (2-4 years) |

| Rising in Electrification Incentives | +0.80% | West, Northeast, and Midwest | Long term (≥ 4 years) |

| Labor Cost Inflation on Large Farms | +1.00% | Midwest, West, and Southwest | Short term (≤ 2 years) |

| High Adoption of Dealer-Led Subscription Models | +0.60% | National, and early gains in Midwest | Medium term (2-4 years) |

| Section 232 Tariff-Driven Localization | +0.40% | National | Short term (≤ 2 years) |

| Carbon-Credit Revenue for Low-Emission Equipment | +0.30% | Iowa and Illinois are in the Midwest, and California is in West | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increase in Adoption of Precision Agriculture

Global Positioning System (GPS) guidance, variable-rate controllers, and section-control nozzles have become standard practices on farms exceeding 1,500 acres. In 2024, 75% of Midwest corn and soybean acres were planted using GPS-guided technology, up from 62% in 2020 [1]Source: USDA Economic Research Service, “Farm Production Expenditures,” ers.usda.gov. Farmers rely on automation because labor shortages make manual in-field adjustments unworkable. Telematics now feeds data to cloud platforms, which raises switching costs, so the competitive edge is tied to software interoperability rather than horsepower. As older implements reach the end of their life, upgrades automatically embed sensors and connectivity, increasing the technology content per unit in the United States agricultural tractor machinery market.

Rising in Electrification Incentives

Federal tax credits that cover up to 30% of electric or hybrid equipment cost and California rules that phase out small diesel engines are stimulating demand for lower-horsepower battery units [2]Source: U.S. Department of Energy, “Inflation Reduction Act Clean Energy Credits,” energy.gov. Monarch Tractor shipped more than 200 electric tractors with paired implements to California growers in 2024, marking a significant milestone in the commercial viability of the technology. Electric drives are not displacing the high-horsepower row-crop segment but are carving out a parallel lane for specialty farms under 500 acres. This bifurcation widens the product palette inside the United States agricultural tractor machinery market.

Labor Cost Inflation on Large Farms

Average hourly wages for equipment operators rose 12% between 2022 and 2024 [3]Source: U.S. Bureau of Labor Statistics, “Occupational Employment and Wage Statistics,” bls.gov. The jump has tightened margins on farms above 3,000 acres, which now install autonomous-ready implements that lower labor hours per acre by up to 30%. Deere & Company's exactShot planter uses robotics to place fertilizer precisely at the seed and delivers payback in under three years on large row-crop farms. Elevated wages are therefore accelerating the shift toward autonomy and data-enabled implements across the United States' agricultural tractor machinery market.

High Adoption of Dealer-Led Subscription Models

Deere & Company and CNH Industrial N.V. dealers are bundling tractor-mounted machinery, telematics, agronomic support, and seasonal equipment swaps into monthly subscription plans designed for the United States farms of about 800–1,500 acres. These models lower upfront costs for buyers facing higher interest rates, while providing dealers with more stable revenue. The continuous data generated through these bundled contracts also helps refine equipment design and keeps growers tied to the OEM (Original Equipment Manufacturers) ecosystem within the United States agricultural tractor machinery market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Equipment Capital Expenditure | -0.90% | National, acute in Southeast and Northeast | Short term (≤ 2 years) |

| Commodity-Price Volatility | -0.70% | Midwest, Southwest, and Southeast | Short term (≤ 2 years) |

| Advanced-Technology Maintenance Skill Gap | -0.50% | National, and severe in rural areas | Medium term (2-4 years) |

| Steel and Aluminum Tariff Cost Pass-Through | -0.40% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Advanced-Technology Maintenance Skill Gap

In 2024, 68% of equipment dealers reported technician shortages, with average hiring times exceeding 120 days for advanced-technology roles. Persistent rural broadband gaps affecting nearly 30% of the United States' farmland further limit the effectiveness of remote diagnostics, reducing the uptime benefits of precision tractor implements. As a result, OEMs (Original Equipment Manufacturers) with dense, well-resourced service networks gain a clear competitive edge, while smaller or newer market entrants struggle to maintain adequate support coverage across dispersed farming regions.

Steel and Aluminum Tariff Cost Pass-Through

In 2024, rising tariffs added an estimated USD 1,200 to USD 1,800 to the production cost of a typical 16-row planter, driving notable price pressure across tractor-powered machinery. Large OEMs (Original Equipment Manufacturers) partially absorbed these increases by localizing fabrication and leveraging scale in procurement, while short-line manufacturers faced sharper margin compression and reduced pricing flexibility. This cost imbalance is accelerating consolidation trends and reinforcing the dominance of major players within the United States agricultural tractor machinery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Planters Lead, Sprayers Accelerate

Planting machinery retained its position as the largest segment at 30.62% of the United States agricultural tractor machinery market size in 2025. Variable-rate seeding is nearing saturation on farms above 1,500 acres, making real-time seed spacing and downforce control standard rather than premium features. This normalization of precision technology has compressed hardware price spreads, pushing competition toward value-added services such as agronomic advice, data analytics, and integration with farm-management platforms. Farmers now prioritize not only the quality of seeding equipment but also software compatibility, dealer calibration support, and actionable insights that optimize yields and input efficiency, reinforcing the strategic importance of planting machinery in the United States agricultural tractor machinery market.

Sprayers are the fastest-growing segment with a projected 7.52% CAGR through 2031. Section-control nozzles and pulse-width-modulation systems have become standard for farms over 2,000 acres, turning precision application from an optional upgrade into an operational necessity. Pull-type boom designs are gradually giving way to self-propelled sprayers with integrated GPS and variable-rate controllers. Midwest row-crop growers justify the USD 300,000 to USD 500,000 premium through labor savings, reduced chemical overlap, and improved environmental compliance. Because these machines feed data directly into farm-management software, manufacturers with strong software ecosystems and dealer calibration support gain a significant competitive edge, highlighting the growing role of smart sprayer technologies in the United States agricultural tractor machinery market.

Geography Analysis

The Midwest generates the largest portion of revenue. Average farms in Iowa, Illinois, Indiana, and Nebraska invest around USD 1.5 million over five years and increasingly choose sensor-rich implements that feed data to farm-management software. Growth is moderate, as technology penetration is already high, yet each unit continues to include more advanced features. Labor pressures are driving wider adoption of autonomous-ready planters and sprayers.

The West is expanding rapidly. California specialty-crop farms utilize electric implements and variable-rate irrigation tools to comply with emissions and groundwater regulations. Monarch Tractor gains traction in vineyards and orchards with battery units, while large wheat and potato farms in Idaho and Washington largely remain diesel-oriented. This creates two distinct sub-markets within the region.

The Southeast is recovering with stable cotton and peanut prices. Sand-friendly planters and cultivators are seeing increasing demand, and conservation tillage is gaining support. The Southwest, supported by Texas dairy clusters, benefits from forage equipment upgrades that improve operations in confined animal setups. The Northeast remains the smallest market but shows niche adoption of compact electric cultivators on organic vegetable farms. These regional differences highlight the importance of configurable product families in the United States agricultural tractor machinery market.

Regulatory Landscape

United States agricultural tractor machinery suppliers operate under overlapping emissions, safety, and road-use compliance requirements. For powertrains, the US Environmental Protection Agency (EPA) regulates nonroad compression-ignition engines used in agricultural tractors under Tier 4 standards, with certification and compliance frameworks set out in 40 CFR Part 1039 and 40 CFR Part 1068. For higher-volume manufacturers, production-level testing obligations are addressed in federal provisions such as 40 CFR 1037.665, which ties engine-aftertreatment design, calibration updates, and ongoing conformity activities more closely.

Safety requirements in agricultural operations include roll-over protective structures (ROPS) and seatbelts for agricultural tractors manufactured after October 25, 1976, under 29 CFR 1928.51, shaping standard equipment specifications and retrofit practices in fleet replacement cycles. For equipment used on public roads, lighting and marking requirements reference federal transport rules such as 49 CFR Part 562 (including ANSI/ASAE standards). In February 2026, the EPA advanced farmers right-to-repair actions affecting nonroad equipment, adding momentum for broader access to diagnostic and repair capabilities and influencing OEM-dealer service policies.

Competitive Landscape

The United States agricultural tractor machinery market is dominated by Deere & Company, CNH Industrial N.V., and AGCO Corporation, which together hold the majority of industry revenue. Deere & Company leverages an integrated hardware-software ecosystem that creates customer stickiness through data lock-in, precision connectivity, and same-day parts service. CNH Industrial N.V. positions its Case IH and New Holland brands as flexible alternatives for diverse farm operations, strengthening its capabilities through partnerships, such as the collaboration with Raven Industries for autonomous guidance systems. AGCO Corporation differentiates its offerings with European-engineered precision under the Fendt and Massey Ferguson brands, emphasizing fuel efficiency and high-performance features tailored for large-scale farming.

Beyond the leading players, mid-tier manufacturers such as Kubota Corporation and Mahindra&Mahindra Ltd. are expanding their presence in the sub-100-horsepower segment, catering to specialty crop farms and livestock operations that require highly maneuverable equipment. This segment has also attracted emerging robotics and electric-vehicle firms, including Monarch Tractor, Blue White Robotics, and Autonomous Solutions Inc., which are piloting driverless attachments and battery-powered units. These innovators are targeting “white-space” opportunities in precision farming, creating pressure on traditional OEMs (Original Equipment Manufacturers) to maintain relevance.

Legacy manufacturers are actively defending their market positions through strategic acquisitions and tightened software controls. Deere & Company's 2024 acquisition of a machine-vision startup and CNH Industrial N.V.'s 2025 partnership with Raven Industries underscore this approach. However, evolving regulatory environments, such as right-to-repair legislation in Colorado and New York, could force OEMs to open their platforms, weakening traditional competitive moats and encouraging a more modular and interoperable landscape. These dynamics are reshaping the competitive framework and innovation pathways within the United States agricultural tractor machinery market.

United States Agricultural Tractor Machinery Industry Leaders

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

Mahindra&Mahindra Ltd.

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity area is third-party validation and de-risking of digital and AI-driven implement capabilities, supported by the USDA National Proving Grounds Network (NPG-Ag) launched in April 2026. Objective performance data for autonomy-adjacent features, including camera-based spraying, guidance, connectivity, and AI-enabled decision support, provides a more standardized evidence path for on-farm adoption. It also creates room for OEMs, short-line implement makers, and software providers to demonstrate measurable input and labor savings under test conditions.

The near-term equipment cycle also points to opportunities in affordability levers and lifecycle services as unit volumes soften. AEM reported US farm tractor sales of 16,815 units in May 2026 (down 21.6% year over year) and 18,186 units in June 2026 (down 18.4% year over year), which supports ongoing demand for dealer-led subscription models, retrofit precision upgrades, and uptime-focused service bundles that spread capex pressure across seasons. In parallel, US farm production expenditures show sustained budget allocation toward equipment, with USDA NASS reporting USD 18.9 billion spent on tractors and self-propelled machinery in 2024, keeping competition focused on sensor-rich implements, interoperability, and aftermarket parts availability, including domestic logistics investments such as Deere plans for a new parts distribution center in Hebron, Indiana.

Recent Industry Developments

- July 2026: Deere & Company entered an agreement with the US Federal Trade Commission and five states to provide farmers and independent technicians access to diagnostic and repair tools for its equipment. The agreement formalizes broader access to repair capabilities and reduces friction in mixed-brand fleets that rely on independent service networks. It also increases pressure on competing OEMs to align service-tool policies as right-to-repair momentum expands across nonroad equipment.

- June 2026: Deere & Company rolled out Model Year 2027 updates to its 6R and 6M tractor lineups, including the e19 powershift transmission and precision agriculture technology enhancements. The refresh reinforces the shift toward integrated connectivity and automation-ready capability as a standard buying criterion rather than a premium add-on. Updated mid-to-high horsepower platforms help Deere defend share during a period of tighter replacement spending.

- March 2025: Case IH launched SenseApply, a tractor-mounted sprayer and applicator system using multi-spectral cameras for spot-spraying and variable-rate applications. By marketing the technology without subscriptions or per-acre fees while targeting meaningful chemical-use reduction, the launch supports a broader push toward camera-guided, data-driven application in tractor-mounted crop protection. This increases competitive pressure on OEM and short-line sprayer ecosystems to pair hardware with practical, low-friction precision workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers the sales value of tractor-led farm machinery and implements used in US agriculture, where equipment demand is tied to crop and livestock operations and on-farm field activity.

Scope exclusions: We exclude standalone farm tractors sold as vehicles, and we also exclude irrigation systems and other non-tractor farm infrastructure.

Segmentation Overview

- By Product Type

- Plowing and Cultivating Machinery

- Plows

- Harrows

- Rotovators and Cultivators

- Other Plowing and Cultivating Machinery

- Planting Machinery

- Seed Drills

- Planters

- Spreaders

- Other Planting Machinery

- Sprayers

- Haying and Forage Machinery

- Mowers and Conditioners

- Balers

- Other Haying and Forage Machinery

- Other Types

- Plowing and Cultivating Machinery

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand context and the equipment replacement cycle for US farms, which keeps the model grounded in what operators can realistically buy. We mainly review public statistics and reference series such as USDA data releases, US Census Bureau economic and manufacturing datasets, USITC and Customs trade statistics for relevant equipment categories, and Bureau of Labor Statistics inflation series for price normalization.

To shape assumptions that public datasets do not fully explain, we also review company annual filings and investor decks, dealer and association websites, and reputable press coverage about planting, tillage, hay and forage, and spraying equipment. Where needed, we add checks using paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records, which helps verify product mix and the direction of pricing. These desk sources are illustrative and not exhaustive, and we used additional references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to test what the desk model cannot prove cleanly, especially equipment utilization, buying triggers, and the typical price ladder across implement classes. We spoke with a mix of manufacturers, dealers, farm operators, and service and attachment specialists across major US farming belts, then aligned assumptions to what was repeatedly confirmed across the value chain.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | |

| Mid tier: 55% | Functional/Unit leaders: 29% | |

| Smaller Players: 14% | Managers: 57% |

Market-Sizing & Forecasting

Sizing begins with a top-down reconstruction where US machinery demand is mapped to farm activity and replacement patterns, and then scaled using public indicators that move with equipment purchases. In practice, we tie the model to signals such as planted acreage and crop mix, farm income and cash receipts, equipment lending and interest-rate direction, dealer inventory tightness, and price inflation on machinery and parts. Because the market is implement-heavy, we also track seasonality linked to planting and harvest windows and the shift in adoption of precision-ready attachments that can lift average selling prices.

After the top-down totals are formed, selective bottom-up approximations are used to sanity check them, such as sampled ASP times estimated unit demand for key groups like tillage tools, planters and seeders, sprayers, and hay and forage machines, followed by channel checks with dealers to confirm mix. When direct volume indicators are patchy for a sub-category, gaps are handled by using adjacent equipment ratios and farm size distribution feedback from interviews, and then correcting the results back to the broader demand pool.

For forecasting, scenario analysis is used so the outlook can reflect realistic swings in farm income, financing conditions, and replacement delays, which shape the US equipment cycle. The final trajectory is reviewed with experts so the assumed price progression and adoption pace of newer attachments stays consistent with what buyers and dealers are expecting.

Data Validation & Update Cycle

Validation is done by triangulating the modeled market value against independent signals such as farm cash income direction, machinery trade flows, and inflation-adjusted equipment pricing movement, and then checking whether the implied unit demand feels plausible to interviewees. If any segment shows an abnormal jump, the drivers are re-checked, and we revisit assumptions like seasonality, product mix, and price normalization before sign-off.

Before release, at least one additional analyst review is completed so calculation logic, sources, and arithmetic are consistent across the time series. The report is refreshed annually, and interim updates are triggered when there are material events such as sharp rate moves, major subsidy or tariff changes, or a visible demand shock in key crop markets. Right before delivery, we do a fresh pass so clients receive the latest updated view available at that time.

Mordor Intelligence's United States Agricultural Tractor Machinery Market Size Versus Other Published Estimates

Published market values for US agricultural tractor machinery can vary even when the topic sounds the same, because sources do not always count the same equipment basket or apply the same price logic. Differences also come from the year used for the estimate, how inflation is treated, and whether a number is meant to represent implement machinery only or a broader equipment spend.

The main gap comes from whether tractors are included inside the total, where Mordor Intelligence counts tractor-linked implements and machinery such as tillage, planting, spraying, and hay and forage equipment, but leaves out standalone tractor vehicle sales that can inflate the headline value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.22 B (2026) | |

| Market Catalog A | USD 13.61 B (2024) | The estimate is stated for an earlier year and appears to use a broader machinery interpretation, which can blend tractor sales or adjacent equipment classes, and it may apply a different inflation or ASP progression method. |

| Industry Bulletin B | USD 20.73 B (2024) | This figure is positioned as an agricultural tractor market value, which is a different scope than tractor machinery and implements, so it typically captures tractor vehicle revenue and pushes the total higher than implement-focused sizing. |

The spread across sources is mostly explained by scope and timing, since a tractor-only market and a tractor machinery market are not directly comparable without adjusting what is being counted. By keeping the equipment basket tied to implement demand drivers and cross-checking price and replacement assumptions with dealers and operators, the total remains traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

How large is the United States agricultural tractor machinery market in 2026?

The market is valued at USD 10.22 billion in 2026 and is set to reach USD 13.24 billion by 2031.

Which product category leads current equipment demand?

Planting machinery hold the top position, accounting for 30.62% of product-type revenue in 2025.

What technology trend is most rapidly influencing buying decisions?

Precision agriculture systems that include GPS guidance and variable-rate controls are now standard on large farms and drive much of the upgrade cycle.

Why are electric tractors gaining attention?

Federal tax credits and state diesel phase-out rules cut purchase cost for small electric units, making them attractive to specialty-crop operations in states such as California.

Page last updated on: