Australia Pet Nutraceuticals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

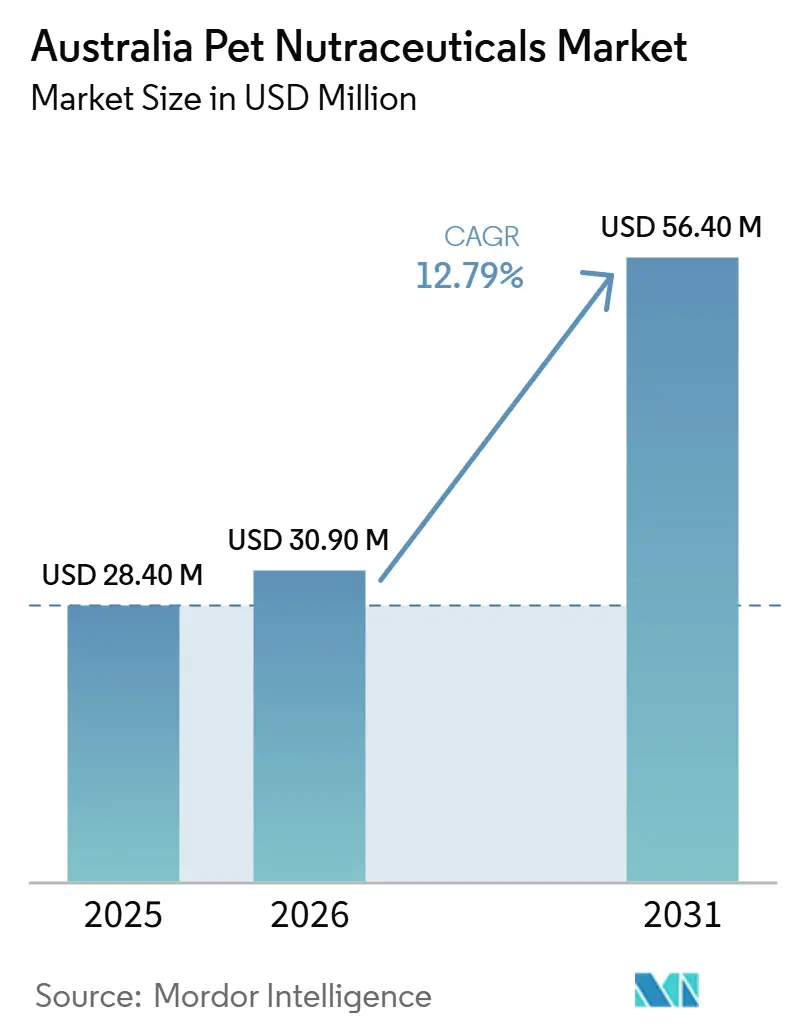

| Base Year Market Size (2025) | USD 28.40 Million |

| Market Size (2026) | USD 30.90 Million |

| Market Size (2031) | USD 56.40 Million |

| Growth Rate (2026 - 2031) | 12.79% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Pet Nutraceuticals Market Analysis by Mordor Intelligence

The Australia pet nutraceuticals market is anticipated to grow from USD 28.40 million in 2025 to USD 30.90 million in 2026 and is forecast to reach USD 56.40 million by 2031, with a CAGR of 12.79% during 2026-2031. Animal Medicines Australia reported that 73% of Australian households owned at least 1 pet in 2025, covering 31.6 million animals across 7.7 million homes, and that annual pet spending reached AUD 21.3 billion (USD 13.8 billion) in the 12 months to March 2025, supporting a broad base for daily wellness products[1]Source: Animal Medicines Australia, “Australia’s Most Comprehensive Pet Survey Shows Nearly Three Quarters of Australian Homes Now Have a Pet,” Animal Medicines Australia, animalmedicinesaustralia.org.au. The market is witnessing growing demand driven by a transition from reactive treatment to routine supplementation, as preventive care becomes an integral part of household pet spending. Furthermore, the fragmented supplier base presents opportunities for specialist brands, as no single group of companies dominates the category value. However, premium pricing remains a barrier to wider adoption, and stricter regulations on therapeutic claims require significant compliance efforts for brands seeking to differentiate on the basis of outcomes. The future trajectory of the Australia pet nutraceuticals market will depend not only on overall market growth but also on how effectively companies foster recurring customer engagement.

Key Report Takeaways

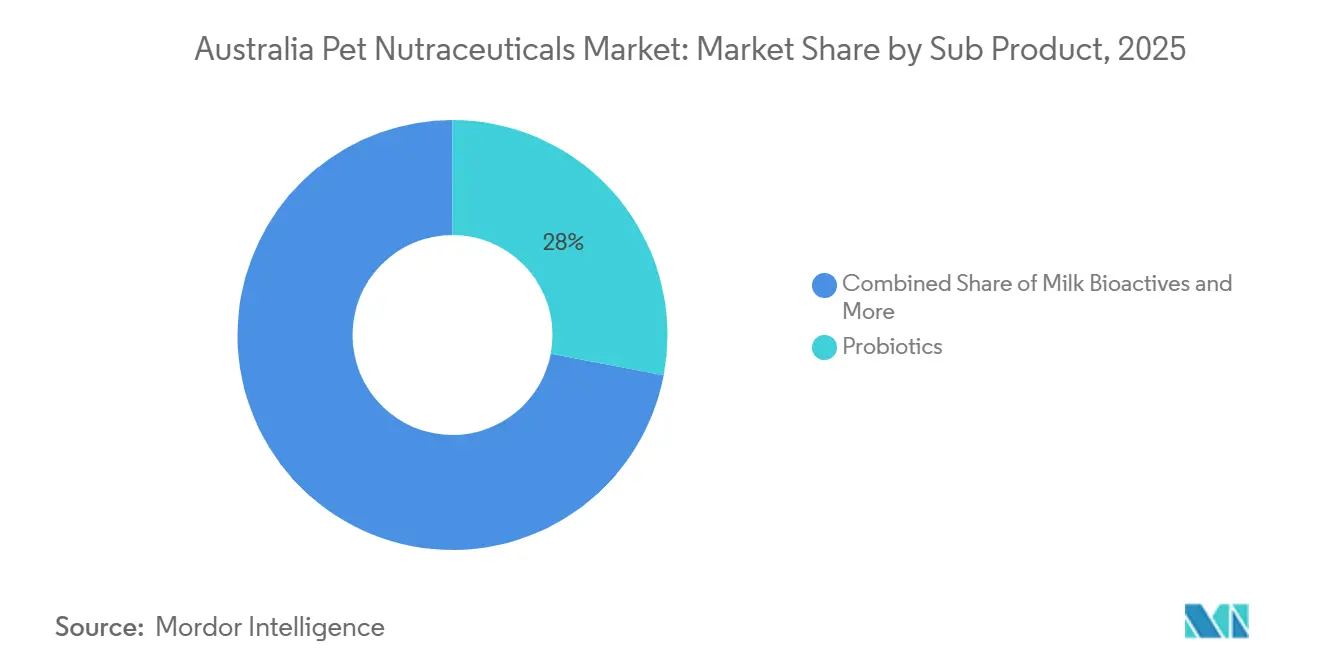

- By sub-product, probiotics led with 28.0% of the Australia pet nutraceuticals market in 2025, while milk bioactives is the fastest-growing, forecast to expand at an 15.3% CAGR through 2026 to 2031.

- By pet type, dogs held the largest pet type, 62.0% of the Australia pet nutraceuticals market size in 2025, while cats recorded the fastest-growing pet type, highest projected CAGR at 14.4% through 2026 to 2031.

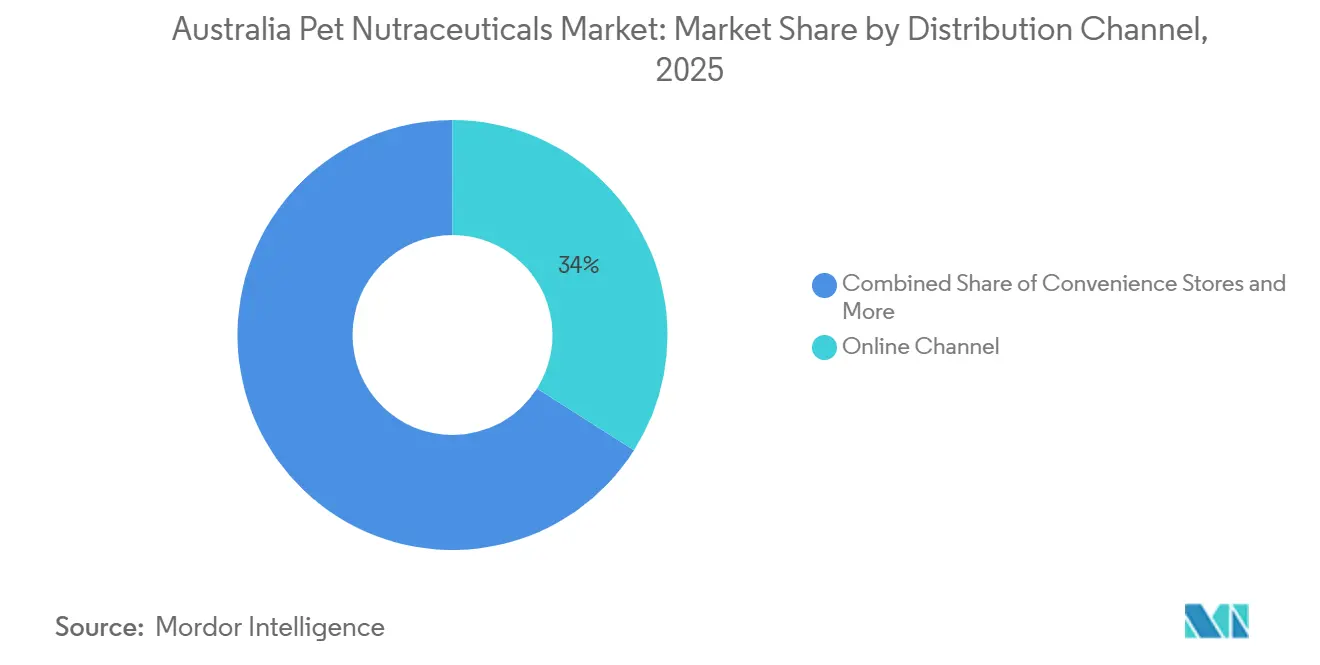

- By distribution channel, the online segment accounted for the largest share of 34.0% in the Australia pet nutraceuticals market in 2025. Additionally, it is the fastest-growing segment, with a projected CAGR of 15.5% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Pet Nutraceuticals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preventive Pet Healthcare Spending | +2.3% | National, with the strongest uplift in New South Wales (NSW) and Victoria | Short term (≤ 2 years) |

| Pet Humanization and Premium Wellness | +2.1% | National, led by urban metros in New South Wales (NSW), Victoria, and Queensland, | Medium term (2-4 years) |

| Veterinary Endorsement and Supplement Credibility | +1.8% | National, with veterinary channel depth in Queensland and Western Australia | Medium term (2-4 years) |

| Aging Pets and Mobility Needs | +1.9% | National, concentrated in densely pet-owned states | Long term (≥ 4 years) |

| E-Commerce Discovery and Replenishment | +2.0% | National, with Queensland and metro New South Wales (NSW), leading digital adoption | Short term (≤ 2 years) |

| Clean Label and Science-Backed Formulations | +1.5% | National, with a premium skew toward the urban East Coast | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Preventive Pet Healthcare Spending

Preventive supplementation has moved from an occasional purchase to a recurring spending line for many Australian households, and that shift is supporting the Australia pet nutraceuticals market. Animal Medicines Australia reported that dog-owning households spent AUD 2,520 (USD 1,634) per year on their pets in 2025, indicating the budget capacity for routine care rather than one-off treatment spending. This matters because supplements are being integrated into daily feeding habits rather than purchased only when a problem becomes visible. Once a product becomes part of an everyday routine, reorder cycles become steadier and brand retention improves. That change expands the addressable base for the Australia pet nutraceuticals market beyond households dealing with a current condition. It also supports better revenue visibility for brands that can secure repeat use with simple formats and clear wellness positioning.

Pet Humanization and Premium Wellness

The financial significance of pets in Australian households continues to grow, driving demand for higher-value products in the Australian pet nutraceutical market. According to Animal Medicines Australia, national pet spending reached AUD 21.3 billion (USD 13.8 billion) in 2025, up 35% from the revised 2022 total of AUD 15.7 billion (USD 10.2 billion). This trend indicates that pet care is evolving beyond basic maintenance, with consumers prioritizing tailored and wellness-focused products. As a result, premium formats are perceived less as a cost barrier and more as a sign of responsible pet ownership. In the Australian pet nutraceuticals market, brands that align products with life stage, breed-specific needs, and clear purposes are better positioned to sustain pricing and encourage repeat purchases. This dynamic has attracted both specialized supplement brands and larger animal health companies to the category.

Veterinary Endorsement and Supplement Credibility

Veterinary support remains one of the clearest trust signals in the Australia pet nutraceuticals market, especially for first-time supplement buyers. Products placed through veterinary clinics or supported by veterinarian-formulated messaging carry more weight because owners often want reassurance before adopting a daily health product. That trust then carries over into repeat purchasing behavior, even when the reorder occurs through digital channels rather than in the clinic. Elanco’s February 2025 launched of its Pet Protect supplement line for dogs and cats demonstrated how established animal health companies are leveraging veterinary credibility to deepen their presence in functional supplementation[2]Source: Elanco Animal Health, “Elanco Launches Pet Protect From the Makers of Advantage: Veterinarian-Formulated Supplements for Complete Pet Wellness,” PR Newswire, prnewswire.com. In the Australia pet nutraceuticals market, this gives an advantage to companies that can combine clinical language, trusted recommendations, and easy replenishment. It also raises the competitive bar for smaller brands that rely on broad wellness claims without comparable professional endorsement.

Aging Pets and Mobility Needs

Aging pets are creating a durable clinical need base for the Australia pet nutraceuticals market, particularly in mobility, digestive, and cognitive support. PetSure’s 2025 Pet Health Monitor showed that osteoarthritis was the leading condition for dogs aged 8 years and older in 2024 claims data, with an average treatment cost of AUD 831 (USD 539) per incident. The same monitor stated that canine cognitive dysfunction affected 28% of dogs aged 11 to 12 years and nearly 68% of dogs aged 15 to 16 years. As pets live longer and remain in households for more years, owners spend more time providing support, which increases lifetime supplement demand. This creates a self-reinforcing pattern in the Australia pet nutraceuticals market because better care supports longevity, and longer-lived pets often require more targeted daily support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Ambiguity Around Therapeutic Claims | -2.5% | National, with the highest compliance complexity for importer-distributors | Short term (≤ 2 years) |

| Premium Pricing Limits Mass-Market Conversion | -2.1% | National, more pronounced in regional and lower-income areas | Medium term (2-4 years) |

| Product Efficacy Skepticism Among First-Time Buyers | -1.4% | National, concentrated in non-veterinary purchase channels | Medium term (2-4 years) |

| Ingredient Sourcing Volatility for Specialized Actives | -1.6% | National, Asia-Pacific supply chain spill-over affecting Queensland importers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Ambiguity Around Therapeutic Claims

Regulatory uncertainty regarding therapeutic claims remains a significant challenge in the Australian pet nutraceuticals market. The Australian Pesticides and Veterinary Medicines Authority (APVMA) has clarified that using less definitive language, such as "may help," does not exempt therapeutic treatments from regulatory requirements, and authorization may still be necessary before including such claims in product materials. The APVMA then issued revised guidance effective May 1, 2025, clarifying that qualifying products under Excluded Nutritional or Digestive criteria would not need full registration as veterinary chemical products[3]Source: Australian Pesticides and Veterinary Medicines Authority, “Animal Feed Products,” Australian Pesticides and Veterinary Medicines Authority, apvma.gov.au. Even with that clarification, imported brands still face stricter claim discipline in Australia than in some other markets, which can slow launches and require label review or reformulation. This keeps compliance cost and timing risk high in the Australia pet nutraceuticals market for companies that want to market stronger functional outcomes.

Ingredient Sourcing Volatility for Specialized Actives

Volatility in ingredient sourcing poses a challenge for the Australia pet nutraceuticals market, particularly for brands dependent on specialized active ingredients or imported materials. Supply dependence becomes more visible when products require specific actives, premium marine inputs, or novel ingredients that lack a deep local sourcing base. This can affect lead times, landed cost, and final shelf pricing, which then feeds back into adoption pressure. The challenge is more noticeable for brands serving states farther from eastern distribution hubs because freight and availability issues can stack on top of ingredient tightness. In the Australia pet nutraceuticals market, this makes local manufacturing and Australian-made provenance more valuable because they reduce some exposure to external supply disruptions. It also explains why sourcing resilience is becoming part of competitive strategy rather than a back-end procurement issue alone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub Product: Probiotics Lead a Clinically Grounded Portfolio

Probiotics are projected to account for the largest share of the Australia pet nutraceuticals market in 2025, representing 28.0%. This positions them as the leading sub-product across both veterinary-led and direct-to-consumer segments. Vitamins and minerals remained the second major demand pillar because they fit a broad range of life stages and price points. Omega-3 fatty acids also held a growing position because they align with skin and allergy management, a concern that stays visible in routine care. This gives the Australia pet nutraceuticals market a sub-product mix where everyday digestive support leads, while broad wellness and skin support continue to anchor adjacent demand.

Milk bioactives is the fastest-growing segment, projected to grow at a 15.3% CAGR from 2026 to 2031. Although the market for milk bioactives is smaller, it is becoming increasingly significant in premium feline nutrition, where specialized positioning is more important than market size. Oversight by the Australian Pesticides and Veterinary Medicines Authority (APVMA) is particularly critical for sub-products marketed with strong health-related claims. As consumer demand increases, companies in the Australian pet nutraceuticals market must exercise caution in their claims. While proteins and peptides are gaining attention, there is a growing focus on providing targeted muscle and tissue support for senior and active dogs.

By Pet Type: Dogs Anchor Volume and Feline Supplementation Accelerates

Dogs accounted for the largest share, representing 62.0% of the Australia pet nutraceuticals market size in 2025, which kept them as the volume and revenue foundation of the category. In 2025, Animal Medicines Australia reported that 7.4 million dogs lived in 49% of Australian households, which explains why most established supplement lines still center on canine routines and conditions. The focus is shifting towards the growth potential within the lower-penetration feline segment, rather than diminishing the primary role of dogs in the market. Historically, supplement formats were primarily developed for dogs, leaving opportunities for cat-specific formulations to grow as advancements in palatability and dosing were made. This gap is now narrowing as more companies recognize feline support as a distinct market opportunity rather than an extension of dog-focused products.

Cats are projected to grow at a CAGR of 14.4% through 2031, indicating faster growth in the feline segment compared to the canine segment. According to PetSure’s 2024 data, feline obesity affected 17% to 53% of cats, depending on the age group, with the highest prevalence observed in the 7 to 8-year age cohort. Other pets, such as birds, reptiles, and small mammals, continue to represent a niche but stable portion of the Australian pet nutraceuticals market, driven by species-specific nutrition that sustains a specialized buyer base. This supports a broad category presence, even though the market remains concentrated in dogs, with the strongest growth observed in cats. Consequently, the Australian pet nutraceuticals market is projected to remain dog-dominated in terms of value while achieving a more balanced focus on product development and innovation.

By Distribution Channel: Online Channel Builds a Structural Lead

Online channels accounted for the largest share, at 34.0% of the Australia pet nutraceuticals market size in 2025, while online is the fastest-growing, advancing at a 15.5% CAGR through 2026 to 2031. Its lead is structural because digital platforms support product education, easy comparison, recurring orders, and broad access beyond the main metro store networks. Specialty stores and veterinary clinics still matter because they often serve as the trust gateway for first-time users who want a professional recommendation before adding a supplement.

Supermarkets and hypermarkets remain present, but they are more limited in their nutraceutical depth because shelf space and shopper behavior favor broader wellness items over targeted formats. Convenience stores play only a minor role because this category depends on repeat use, product explanation, and a stronger replenishment system than convenience formats usually provide. Physical trust and digital channels now complement each other. Buyers may try a supplement based on a clinic or specialty recommendation and later shift to online purchases once trust is established. This transition supports a recurring revenue model and helps the Australia pet nutraceuticals market reach households beyond specialty areas without high store expansion costs. As subscription offerings improve, the online channel is projected to grow further, while specialty outlets remain key for initial conversions. Omnichannel coordination is crucial, as each stage of the buyer journey serves a distinct role.

Geography Analysis

New South Wales benefits from a high population density, above-average household incomes, and a well-established network of veterinary and specialty retail outlets. Similarly, Victoria leverages Melbourne’s prominence in premium pet wellness retail and an urban owner base with strong preventive care habits. These factors contribute to the concentration of the Australia pet nutraceuticals market in the eastern states, even as growth begins to extend to other regions.

Queensland is notable for its rising demand, driven by a younger pet-owning demographic, robust digital purchasing behavior, and greater access to premium retail options. Western Australia and South Australia currently have lower market values, but improved e-commerce access is increasing product availability compared to previous years. In contrast, other regions in Australia are growing from a lower base of awareness and limited access to specialty products, which naturally moderates their short-term growth. However, the overall trend in the Australia pet nutraceuticals market is toward a broader geographic distribution rather than a concentration in a few metropolitan areas. This shift underscores the importance of digital fulfillment and brand reach in regions beyond the traditional core states. Companies that adapt their distribution strategies to cater to both densely populated and dispersed demand centers are likely to achieve more sustainable growth.

Western Australia is emerging as an increasingly significant contributor to the Australia pet nutraceuticals market. Improved access to premium pet health products through online channels and expanding retail networks is driving growth in the state. Despite its smaller and more geographically dispersed population compared to the eastern seaboard, strong pet ownership rates support demand for supplements targeting mobility, digestive health, and overall wellness. Regional areas are also benefiting from advancements in logistics and e-commerce fulfillment, which are addressing historical challenges in product availability. As awareness of preventive pet care continues to rise, Western Australia is projected to play a larger role in expanding the market's geographic reach and reducing dependence on the major eastern metropolitan centers.

Competitive Landscape

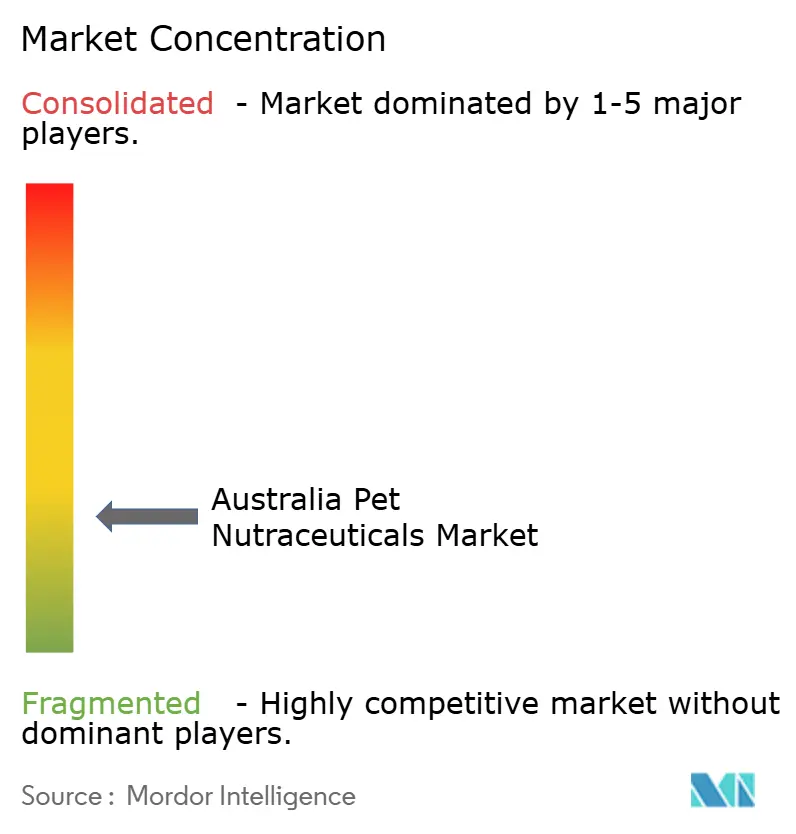

The Australian pet nutraceuticals market is fragmented, with the top five players in 2025 identified as Mars, Incorporated, Nestlé S.A., The Hill’s Pet Nutrition, Inc., H&H Group, and EBOS Group. This market structure creates opportunities for specialist brands, as no single company or group simultaneously dominates shelf presence, veterinary influence, and digital repeat demand. Mars Petcare benefits from its extensive brand reach, domestic manufacturing capabilities, and access to the Royal Canin veterinary channel. Nestlé Purina leverages its established retail and veterinary relationships, while EBOS Group plays a significant role through its extensive distribution network, which is as critical as direct brand ownership in this category.

Competitive strategies in the Australian pet nutraceuticals market emphasize linking trusted recommendations with recurring online reorder behavior. This underscores the importance of leveraging animal health expertise to build credibility in the nutraceuticals segment. Companies that combine scientific validation with targeted marketing efforts are better positioned to gain consumer trust. Additionally, integrating digital platforms to enable seamless reordering and customer engagement is essential to maintaining a competitive edge. The focus on clinically backed products and convenience-driven purchasing behavior is reshaping the competitive landscape, fostering innovation among both established players and new entrants.

Future competitive advantages in the Australian pet nutraceuticals market are expected to stem from sharper category focus rather than market size alone. Opportunities exist in areas such as breed-specific formulations, senior feline nutrition, and products emphasizing Australian ingredient provenance. Local innovators can differentiate themselves by offering credible formulations, clear use cases, and a straightforward digital reorder process. However, the fragmented market structure suggests that leadership will remain contested, with sustained market share gains relying more on effective execution than on brand recognition alone.

Australia Pet Nutraceuticals Industry Leaders

Mars, Incorporated

Nestlé S.A.

The Hill’s Pet Nutrition, Inc.

H&H Group

EBOS Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Virbac launched URSOLYX Soft Chews for Cats in Australia, the first feline-specific muscle support supplement in the company's global portfolio. The product follows the canine version launched in 2025, with early efficacy study results showing 82% improvement in mobility by week 8. The launch expands Virbac's nutraceutical presence across companion animals and strengthens its position in the Australian veterinary supplement channel.

- November 2025: Real Pet Food Company (RPF) launched Fresh(labs) in Australia, described as Asia-Pacific's first research and development initiative dedicated to fresh pet nutrition, including nutraceuticals. The multi-million-dollar investment aims to advance the science, education, and innovation of pet food.

- September 2025: Animal Medicines Australia published the 2025 Pets in Australia survey, documenting that 73% of Australian households own at least one pet and that annual national pet spending reached AUD 21.3 billion (USD 13.8 billion). The report confirmed an estimated 31.6 million pets living across 7.7 million Australian households, representing the highest recorded household pet ownership rate in the country's survey history.

Australia Pet Nutraceuticals Market Report Scope

Pet nutraceuticals are products administered to animals, including dogs, cats, birds, and horses, to offer health benefits that extend beyond basic nutrition. The Australia pet nutraceuticals market report is segmented by sub product (milk bioactives, omega-3 fatty acids, probiotics, proteins and peptides, vitamins and minerals, and other nutraceuticals), by pets (cats, dogs, and other pets), and by distribution channel (convenience stores, online channel, and more). The market forecasts are provided in terms of Value (USD) and Volume (Metric Tons).

| Vitamins and Minerals |

| Probiotics |

| Omega-3 Fatty Acids |

| Proteins and Peptides |

| Milk Bioactives |

| Other Nutraceuticals |

| Dogs |

| Cats |

| Other Pets |

| Convenience Stores |

| Online Channel |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Other Channels |

| By Sub Product | Vitamins and Minerals |

| Probiotics | |

| Omega-3 Fatty Acids | |

| Proteins and Peptides | |

| Milk Bioactives | |

| Other Nutraceuticals | |

| By Pet Type | Dogs |

| Cats | |

| Other Pets | |

| By Distribution Channel | Convenience Stores |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

Key Questions Answered in the Report

What is the 2026 value of the Australia pet nutraceuticals space?

The Australia pet nutraceuticals market is valued at USD 30.9 million in 2026.

Which product type leads revenue in Australia pet nutraceuticals?

Probiotics lead the category with 28.0% revenue share in 2025 because digestive support addresses a recurring clinical need across both dogs and cats.

Why are cats becoming more important for future growth?

Cats are projected to grow at 14.4% CAGR through 2031 as feline-specific formulations improve and awareness of obesity, digestive issues, and urinary conditions increases.

Which sales channel currently leads category distribution?

Online leads with 34.0% of category value in 2025 because it supports product education, repeat ordering, and wider access beyond dense specialty retail areas.

Page last updated on: