Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.48 Billion |

| Market Size (2026) | USD 15.02 Billion |

| Market Size (2031) | USD 18.05 Billion |

| Growth Rate (2026 - 2031) | 3.74% CAGR |

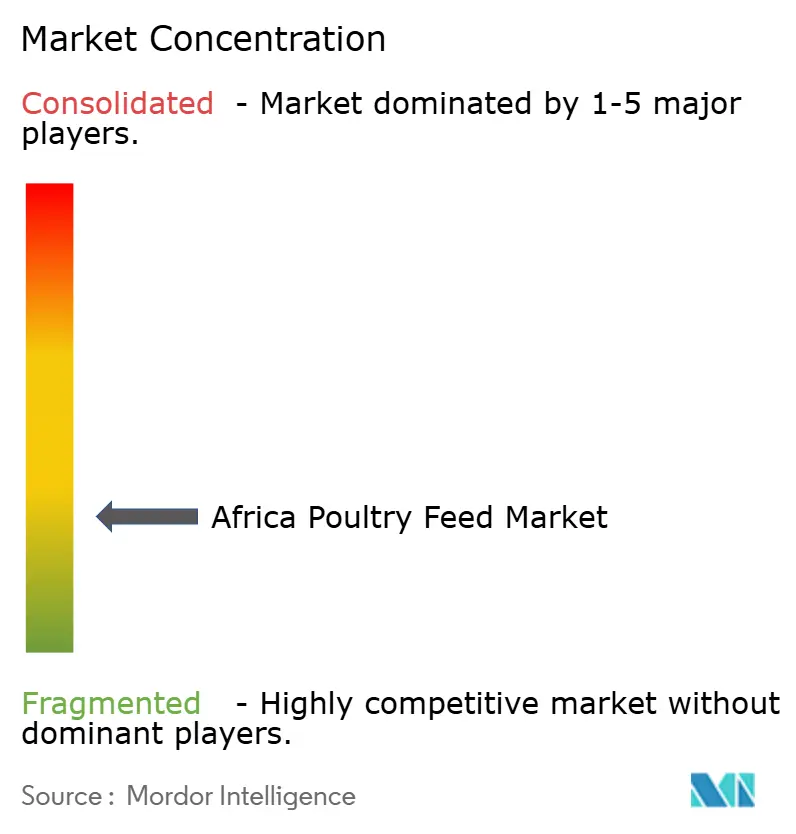

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Poultry Feed Market Analysis by Mordor Intelligence

The Africa poultry feed market size was valued at USD 14.48 billion in 2025 and estimated to grow from USD 15.02 billion in 2026 to reach USD 18.05 billion by 2031, at a CAGR of 3.74% during the forecast period (2026-2031). Sustained urban growth, rising disposable incomes and protein intake, and regional policy coordination under the African Continental Free Trade Area (AFCFTA) underpin this outlook. Integrated producers are scaling feed operations to capture economies of scale, while quick-service restaurants (QSRs) demand traceable, high-quality broiler supply chains that, in turn, increase demand for nutritionally consistent feed. Government input subsidies and technology investments in precision nutrition further accelerate efficiencies, even as manufacturers continue to mitigate grain cost volatility through ingredient diversification and logistics optimization. Finally, cross-border feed corridors enabled by AFCFTA lower landed costs for soybean meal and maize, sharpening competitiveness of regional mills.

Key Report Takeaways

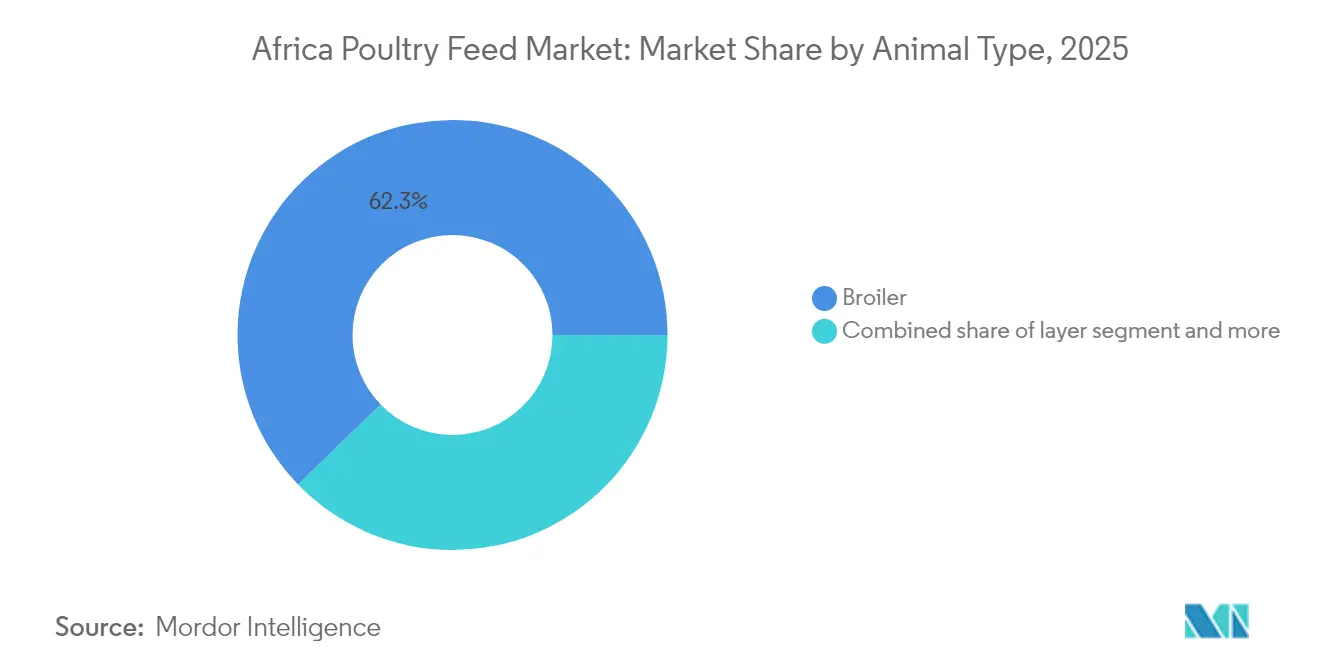

- By animal type, broiler feed held 62.25% of the Africa poultry feed market share in 2025, whereas turkey feed is forecast to post the fastest 7.30% CAGR through 2031.

- By ingredient type, cereals accounted for 54.05% of the Africa poultry feed market size in 2025, while molasses is projected to expand at an 18.35% CAGR to 2031.

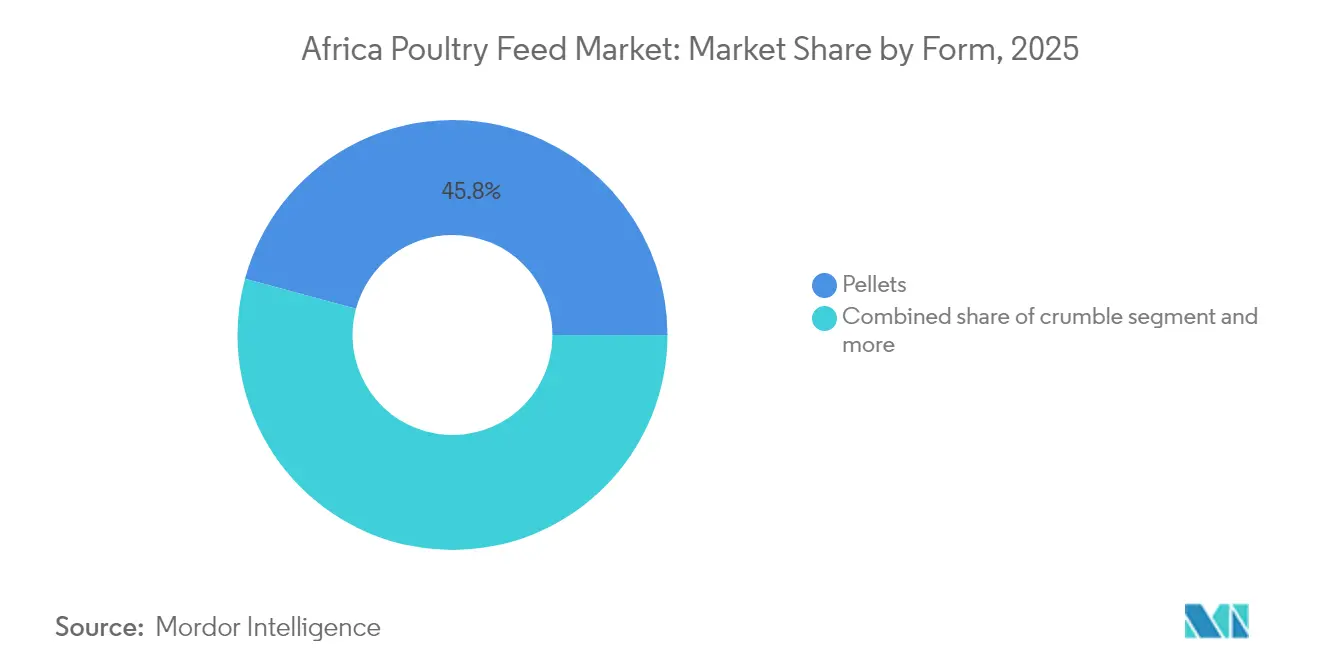

- By form, pellets led with 45.78% revenue share in 2025. The crumble feed shows a 7.15% CAGR through 2031.

- By geography, Nigeria captured 28.22% of the market in 2025. Ethiopia is anticipated to expand at a market-leading 7.64% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Poultry Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong demand from quick-service restaurant chicken chains | +0.8% | Nigeria, South Africa, Kenya, and Morocco | Medium term (2-4 years) |

| Growth of integrated poultry producers | +0.6% | South Africa, Algeria, Morocco, and Ethiopia | Long term (≥ 4 years) |

| Government subsidies for maize and soybean cultivation | +0.5% | Nigeria, Ghana, Senegal, Malawi, and Zambia | Short term (≤ 2 years) |

| Rising adoption of nutritionally balanced commercial feed | +0.7% | Global, with early gains in South Africa, Nigeria, and Kenya | Medium term (2-4 years) |

| Surge in insect-meal pilot projects for feed protein | +0.4% | Kenya, Rwanda, South Africa, Namibia, and Zimbabwe | Long term (≥ 4 years) |

| African Continental Free Trade Area (AFCFTA)-driven cross-border feed logistics efficiencies | +0.3% | Regional corridors: East Africa, SADC, and ECOWAS | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Demand from Quick-Service Restaurant Chicken Chains

Pan-African QSR expansion, led by KFC’s more than 1,000 outlets, requires standardized broiler supply programs that lock in feed quality and volume commitments. Contract farming models incentivize mills to formulate feeds that consistently meet weight and feed-conversion targets within six-week grow-outs. QSR procurement policies increasingly specify antibiotic-free protocols, accelerating uptake of phytogenic additives that carry premium margins. The resulting predictable demand stream enables capital investment in automated pelleting lines and regional distribution hubs. Together, these factors anchor a virtuous cycle of higher throughput, lower per-unit costs, and improved profitability across the Africa poultry feed market.

Growth of Integrated Poultry Producers

Companies such as Zalar Holding and Country Bird Holdings deepen vertical integration to shield against raw-material price swings, which account for 60-70% of cost of goods sold. In-house feed mills allow synchronized formulation changes that match flock age and performance targets, supporting phase-feeding programs that reduce waste. Integrated models shorten working-capital cycles, enhance quality control, and support rapid adoption of alternative proteins like insect meal. Over time, this alignment is projected to compress cost structures across major North and Southern African producers, bolstering competitiveness.

Government Subsidies for Maize and Soybean Cultivation

Input subsidy schemes help narrow the yield gap between African growers and global exporters, improving local raw-material availability. Lagos State’s 25% feed subsidy, launched in January 2025, directly lowered mill gate prices for poultry and aquaculture farmers[1]Source: MSME Africa Online, “Lagos Launches 25% Feed Subsidy,” msmeafricaonline.com. Senegal is committed to buying 5,000 metric tons of local maize at USD 0.37/kg, surpassing the USD 0.33/kg import price to spur domestic production. Such interventions partially insulate feed producers from foreign-exchange shocks and improve raw-material security, even though long-term fiscal sustainability remains a question.

Rising Adoption of Nutritionally Balanced Commercial Feed

Commercial feed adoption enables consistent nutrient delivery that optimizes growth performance and reduces production variability, particularly critical for broiler operations targeting specific market weights[2]Source: International Livestock Research Institute, “Local Production of Quality Affordable Poultry Feed,” ilri.org. Local technology packages that blend regionally sourced maize, soybean meal, and vitamin premixes trim delivered costs up to 60% versus imported formulations. Better flock uniformity and shorter grow-out cycles raise enterprise incomes, supporting reinvestment in improved housing and water systems. Feed mills respond by launching starter, grower, and finisher lines matched to local breed genetics, cementing loyalty and market share.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High volatility in grain import prices | -0.9% | Nigeria, Ghana, Egypt, and Morocco | Short term (≤ 2 years) |

| Disease outbreaks driving temporary demand slumps | -0.6% | South Africa, Nigeria, and Egypt | Short term (≤ 2 years) |

| Electricity shortages affecting feed-mill uptime | -0.4% | South Africa, Nigeria, Ghana, and Zimbabwe | Medium term (2-4 years) |

| Limited cold-chain for vitamin premix storage | -0.3% | Rural sub-Saharan markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Volatility in Grain Import Prices

Commodity price fluctuations create significant margin pressure for feed manufacturers, particularly in markets with limited domestic grain production capacity. In 2024, maize prices in Ghana jumped 80% in eight months, forcing mills to idle 30% of capacity and prompting calls for import-license waivers. Egypt’s sector likewise teetered under soaring corn and soybean costs that eroded producer margins. Currency devaluation compounds these challenges, as most African countries import significant portions of their feed ingredients in hard currencies while selling finished products in local markets.

Disease Outbreaks Driving Temporary Demand Slumps

Highly pathogenic avian influenza (HPAI) culled 10 million birds in South Africa, resulting in a loss of USD 515 million in value and a sudden reduction in feed demand in 2023. The Food and Agriculture Organization (FAO) 's surveillance programs in Côte d'Ivoire demonstrate the ongoing regional coordination efforts required to manage transboundary animal disease risks [3]Source: Food and Agriculture Organization, “FAO in Côte d'Ivoire,” fao.org. Producers redirect cash toward biosecurity rather than feed upgrades, causing sporadic order cancellations and inventory write-downs at mills. Regional governments are stepping up surveillance, yet recurring outbreaks sustain an environment of unpredictable demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Broiler Feed Dominates Commercial Production

Broiler formulations accounted for 62.25% of Africa poultry feed market share in 2025, reflecting the segment’s short grow-out cycles and standardized demand profiles. The Africa poultry feed market size for turkey diets is projected to grow at a 7.30% CAGR to 2031, propelled by premium positioning and higher per-bird consumption. Broiler feed leverages economies of scale in pelleting and bulk distribution, resulting in lower unit costs compared to layer diets. Integrators align nutrient density with fast live-weight targets, reinforcing demand for energy-dense maize-soy rations.

Turkey feed, although smaller in volume, commands higher price points due to extended 28- to 32-week fattening schedules and specialized amino acid profiles. Feed manufacturers utilize differentiated additives, such as probiotic blends, to manage gut health over extended grow-out periods. While layer feed remains steady among egg enterprises, niche markets for guinea fowl and ducks spur tailored micro-batch production, preserving margins for agile, regionally focused mills.

By Ingredient Type: Cereals Lead Despite Molasses Growth

Cereals made up 54.05% of total inclusion rates in 2025, relying largely on maize for metabolizable energy and wheat byproducts where available. The Africa poultry feed market tied to molasses inputs is forecast to expand at a 18.35% CAGR through 2031, as mills adopt the byproduct to enhance pellet durability and reduce dust. High metabolizable sugar content allows partial substitution for costly grains, delivering savings without compromising energy density.

Oilseed meals, chiefly soybean meal, remain primary protein contributors despite price volatility. Fishmeal faces sustainability and cost constraints, pushing formulators toward alternative proteins such as insect meal. Supplements, vitamins, minerals, and enzymes occupy a smaller tonnage share yet drive product differentiation and premium pricing. Over the forecast period, ingredient portfolios are likely to diversify further to buffer against import shocks and climate variability.

By Form: Pellets Preferred for Handling Efficiency

Pellets held a 45.78% share of finished-feed output in 2025, favored for superior feed-conversion ratios and ease of mechanized handling. The Africa poultry feed market linked to crumble formulations is projected to grow at a 7.15% CAGR, driven by starter and grower diets where smaller particle sizes boost digestibility. Pelleted diets enable automated on-farm feeding, cutting labor requirements and minimizing spillage.

Crumble feed, produced by breaking pellets, targets early-age birds with limited gizzard capacity. Despite additional processing costs, higher early-stage weight gain justifies premium pricing. Mash retains market share among cost-sensitive backyard producers, and liquid feed solutions occupy niche applications such as medicated water-soluble nutrients.

Geography Analysis

Nigeria captured 28.22% of the market in 2025, while Ethiopia is anticipated to expand at a market-leading 7.64% CAGR to 2031. South Africa anchors the Africa poultry feed market with the continent’s most advanced manufacturing base and consolidated supply chains. Major integrators like Astral Foods invest in precision dosing and energy-efficient pellet coolers, even as intermittent power shortages oblige diesel generator outlays. Domestic grain sourcing and established rail networks reduce landed raw-material costs compared with many peers.

Nigeria represents the largest incremental demand center, powered by demographic momentum, urban income growth, and robust QSR expansion. Yet currency depreciation and port congestion inflate costs for imported soybean meal and vitamin premixes, challenging mill margins. The government’s 25% feed subsidy offers partial respite but faces budgetary limits. Morocco serves as a logistical gateway for North and West African grain flows. It's free-trade agreement with the United States secures favorable corn import tariffs, benefiting domestic mills and enabling re-exports along ECOWAS corridors. Algeria leverages its Mediterranean proximity to access global grain markets, while its poultry expansion is reinforced by state-backed financing for feed mill upgrades.

Competitive Landscape

The Africa poultry feed market is low, with multinational corporations, regionals, and agile local mills vying for share. Multinationals such as Cargill and Nutreco leverage global R&D pipelines to localize precision nutrition products, while regionals like RCL Foods Limited (Remgro Limited) and Astral Foods Limited differentiate themselves through vertically integrated value chains. In March 2024, consolidation includes Olam Agri’s USD 18.4 million acquisition of Senegalese feed maker Avisen, which expands West African throughput capacity.

Companies are gaining competitive advantages through the adoption of technology. DSM-Firmenich established feed premix facilities in Egypt to reduce delivery times for customized feed blends. Nutreco expanded its feed enzyme and probiotic offerings through the acquisition of Animal Nutrition and Health in South Africa's feed market in 2024. In the emerging insect-protein segment, AgriProtein's Gauteng facility increased Black Soldier Fly production to commercial scale, indicating a transformation in protein-sourcing methods.

Local feed mills leverage their proximity to smallholder clusters as a key differentiator, offering microcredit and extension services to secure demand. Digital formulation platforms powered by cloud-based least-cost algorithms are emerging, lowering formulation errors and boosting margin capture. Nonetheless, fragmented distribution networks, limited cold-chain infrastructure, and uneven regulatory enforcement maintain significant entry barriers for new participants.

Africa Poultry Feed Industry Leaders

Cargill Inc.

Nutreco N.V. (Trouw Nutrition)

Alltech Inc.

Kemin Industries Inc.

Novus International, Inc. (Mitsui & Co., Ltd. and Nippon Soda Co., Ltd.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Lagos State government launched a 25% feed subsidy program for poultry and fish farmers, lowering input costs in Nigeria’s largest economic hub.

- April 2024: Nutreco opened a new poultry and animal feed production facility in Ibadan, Oyo State, Nigeria, through its subsidiaries Skretting and Trouw Nutrition. This USD 26.7 million facility spans 170,000 sq. meter and has an annual production capacity of 125,000 metric tons of poultry and animal feeds.

- March 2024: Olam Agri, a Singapore-based food and agribusiness company, purchased Avisen in Senegal for USD 18.6 million. This acquisition is part of Olam Agri's strategy to expand and improve its animal feed and protein production capabilities in the region, focusing on poultry feed.

Africa Poultry Feed Market Report Scope

The food for farm poultry, including chickens, ducks, geese, and other domestic birds, is referred to as poultry feed. Healthy poultry requires protein and carbohydrates, the necessary vitamins, dietary minerals, and an adequate supply of water supplied through the feed. For this report, only feed sold commercially has been considered. The homemade feed has been excluded from the scope.

The African poultry feed market is segmented by animal type (layer, broiler, turkey, and other animal types), ingredient type (cereal, oilseed meal, molasses, fish oil, and fish meal, supplements, and other ingredient types), and geography (South Africa, Algeria, Nigeria, Ethiopia, Morocco, and Rest of Africa). The report offers the market size and forecasts in terms of both value (USD) and volume (metric tons) for all the above segments.

By Animal Type

| Broiler |

| Layer |

| Turkey |

| Other Animal Types |

By Ingredient Type

| Cereals |

| Oilseed Meal |

| Molasses |

| Fish Oil and Fish Meal |

| Supplements |

| Other Ingredient Types |

By Form

| Pellets |

| Crumble |

| Mash |

| Other Forms |

By Geography

| South Africa |

| Algeria |

| Nigeria |

| Ethiopia |

| Morocco |

| Rest of Africa |

| By Animal Type | Broiler |

| Layer | |

| Turkey | |

| Other Animal Types | |

| By Ingredient Type | Cereals |

| Oilseed Meal | |

| Molasses | |

| Fish Oil and Fish Meal | |

| Supplements | |

| Other Ingredient Types | |

| By Form | Pellets |

| Crumble | |

| Mash | |

| Other Forms | |

| By Geography | South Africa |

| Algeria | |

| Nigeria | |

| Ethiopia | |

| Morocco | |

| Rest of Africa |

Key Questions Answered in the Report

How large is the Africa poultry feed market in 2026?

It stands at USD 15.02 billion and is projected to reach USD 18.05 billion by 2031.

What is the projected CAGR for poultry feed demand across Africa to 2031?

The compound annual growth rate is forecast at 3.74%.

Which animal type consumes the most feed across Africa?

Broiler feed dominates with 62.25% share of total volumes in 2025.

Which ingredient category is growing fastest in African feed formulations?

Molasses is expanding fastest at an 18.35% CAGR through 2031.

Page last updated on: