Aerospace Parts Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.02 Trillion |

| Market Size (2030) | USD 1.39 Trillion |

| Growth Rate (2025 - 2030) | 6.39% CAGR |

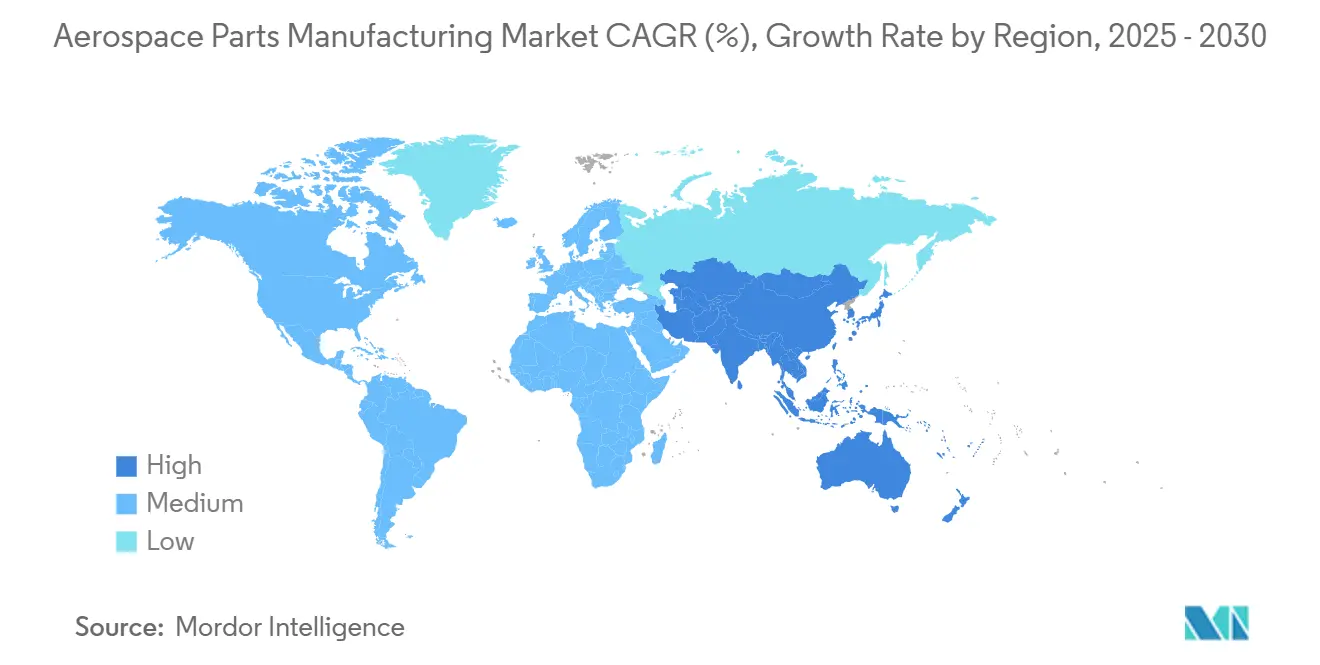

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aerospace Parts Manufacturing Market Analysis by Mordor Intelligence

The aerospace parts manufacturing market size stood at USD 1.02 trillion in 2025 and is projected to reach USD 1.39 trillion by 2030, translating into a 6.39% CAGR over the forecast period. Fleet modernization programs, surging passenger volumes, and defense procurement expansion sustain healthy order books while new segments such as Advanced Air Mobility (AAM) add incremental momentum. Engines remain the largest product category, capturing 36.52% of 2024 revenue, and metals and alloys dominate material usage at 46.23%. Commercial aviation contributes almost two-thirds of demand, backed by record backlogs that help buffer cyclical swings. Original Equipment Manufacturers (OEMs) account for more than 70% of 2024 sales, but the aftermarket is positioned for resilient growth as aircraft utilization intensifies. Regionally, North America leads by value while Asia-Pacific is the fastest-growing geography, reflecting the dual pull of mature supply chains and emerging capacity build-outs.

Key Report Takeaways

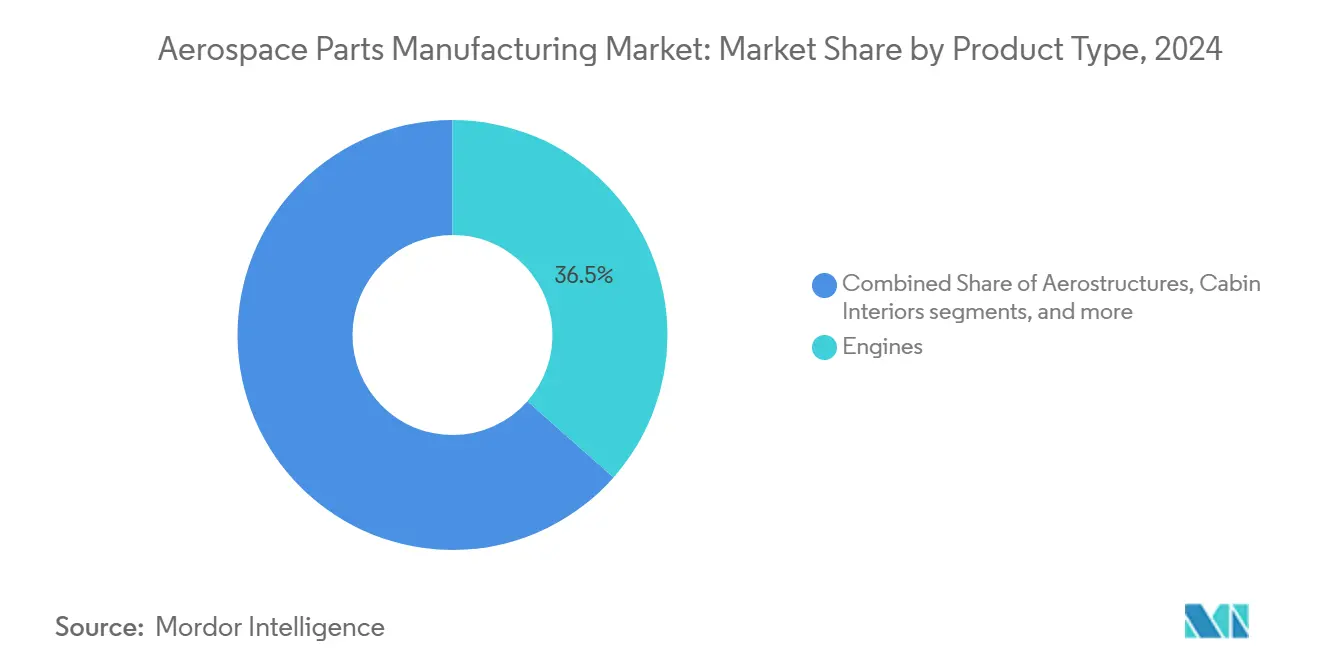

- By product type, engines held 36.52% of the aerospace parts manufacturing market share in 2024, while insulation components are forecasted to outpace all other categories at a 7.94% CAGR through 2030.

- By material, metals and alloys commanded 46.23% of the aerospace parts manufacturing market size in 2024, whereas advanced ceramics and ceramic matrix composites are set to expand at a 7.75% CAGR during 2025–2030.

- By aircraft type, commercial aviation generated 63.24% of 2024 revenue; Advanced Air Mobility is projected to rise at a 9.57% CAGR to 2030.

- By end user, OEMs controlled 70.11% of 2024 sales, and show a 6.76% CAGR outlook through 2030.

- By geography, North America contributed 36.54% of the 2024 value, while Asia-Pacific is forecasted to deliver the fastest regional CAGR of 7.01% over the next five years.

Global Aerospace Parts Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in worldwide air passenger traffic | +1.2% | Global, strongest impact in Asia-Pacific and Middle East | Medium term (2–4 years) |

| Fleet modernization efforts to enhance fuel efficiency | +1.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of global defense procurement programs | +0.9% | North America, Europe, Asia-Pacific defense corridors | Medium term (2–4 years) |

| Rising adoption of lightweight and advanced materials | +1.1% | Global manufacturing hubs, concentrated in developed markets | Long term (≥ 4 years) |

| Establishment of additive manufacturing hubs across aerospace supply chains | +0.7% | North America, Germany, Singapore, emerging in India | Medium term (2–4 years) |

| Nearshoring incentives for critical alloys | +0.4% | USMCA region, EU-adjacent suppliers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Worldwide Air Passenger Traffic

Passenger traffic rebounded sharply in 2024 and continues climbing in 2025, forcing airlines to add capacity and upgrade fleets. Airbus shipped 766 aircraft in 2024 and still holds a EUR 629 billion (USD 746.15 billion) backlog, underscoring long-dated demand visibility. Meanwhile, the B737 MAX line is stabilizing at 25 units per month, with further upside planned as supply bottlenecks clear. Asia-Pacific remains the pivot for incremental growth, as China alone is expected to triple its active fleet by 2042—an expansion that cascades across engines, aerostructures, and cabin systems. High utilization also lifts the aftermarket because more cycles translate into heavier maintenance, repair, and overhaul workloads.

Fleet Modernization Efforts to Enhance Fuel Efficiency

Airlines are retiring older airframes in favor of next-generation models equipped with high-bypass engines, advanced composites, and more-electric architectures. Ceramic matrix composites in hot sections elevate allowable temperatures and trim weight, enabling double-digit efficiency gains over legacy platforms.[1]GE Aerospace Commentary, “Ceramic Matrix Composite Advances,” financialmodelingprep.com Lightweight materials, including advanced ceramics, are registering a 7.75% CAGR growth—outpacing the broader aerospace parts manufacturing market as operators strive to lower cost per available seat-mile. Around three-quarters of commercial fleets will require interior refits every six to seven years, creating sustained pull for cabin components even as new deliveries rise. Environmental regulations further accelerate replacement cycles as carriers look to cut carbon intensity per passenger.

Expansion of Global Defense Procurement Programs

Rising geopolitical tensions have prompted NATO members and several Asia-Pacific governments to elevate defense outlays. CPI Aerostructures’ order backlog swelled to USD 510 million, while Astronics reported 41.60% quarterly growth in its military-oriented avionics line. Programs spanning next-generation fighters and unmanned aerial systems drive demand for complex structures, advanced electronic warfare modules, and thermal-resistant materials. The defense channel acts as a countercyclical buffer, partly insulating the aerospace parts manufacturing market from commercial downswings. It often requires high-margin specialized components with lengthy lifecycles.

Rising Adoption of Lightweight and Advanced Materials

Suppliers push composite fabrication, additive manufacturing, and ceramic matrix technologies deeper into serial production. New insulation materials address stricter thermal and acoustic requirements in AAM vehicles and more-electric airframes. TIGHITCO and InsulTech are rolling out battery-friendly liners that withstand higher heat loads without weight penalties. OEMs also experimented with bio-based polymers and recyclability schemes to align with emerging circular economy mandates. Such transitions increase value per shipset and diversify revenue streams away from traditional metallic content.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating certification and compliance costs across international programs | -0.8% | Global, highest burden in multi-jurisdictional programs | Medium term (2–4 years) |

| Global shortages of skilled labor and associated capital investment burdens | -1.1% | North America and Europe primarily, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Volatility in worldwide supply of critical minerals | -0.9% | Global supply chains, concentrated impact in titanium and rare earth dependent regions | Short term (≤ 2 years) |

| Long-term reduction in parts demand due to aircraft electrification trends | -0.3% | Global, with early impact in Advanced Air Mobility and regional aircraft segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Certification and Compliance Costs Across International Programs

The path to FAA, EASA, and other regulatory approvals is becoming longer and costlier. Achieving FAA Part 21 clearance on a complex assembly can exceed USD 1 million, while parallel EASA and Transport Canada submissions multiply documentation and testing requirements. Greater scrutiny after recent safety incidents has added several months to typical approval cycles, a delay that strains smaller suppliers’ cash flows. Compliance costs also weigh on innovation because new designs face an increasingly expensive validation hurdle, potentially stalling time-to-market for promising technologies.

Global Shortages of Skilled Labor and Associated Capital Investment Burdens

Precision machining, composite lay-up, and inspection roles remain chronically understaffed. Companies are investing in automation—CNC machining centers priced between USD 2 million and USD 5 million—to compensate, but such outlays raise fixed-cost structures and lengthen payback periods. Demographic shifts exacerbate the problem as veteran technicians retire faster than technical colleges can replenish the pipeline, causing a structural constraint on the aerospace parts manufacturing industry’s growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engines Anchor Revenue While Insulation Components Accelerate

Engines generated the largest slice of the aerospace parts manufacturing market size, delivering 36.52% of 2024 sales as airlines and defense forces prioritized propulsion efficiency and reliability. High shop-visit volumes and rate hikes on single-aisle programs support a steady spare-parts stream, while next-generation geared turbofan and open-fan concepts promise richer bill-of-materials per unit. The segment benefits from multi-decade service agreements that lock in recurring revenue and shield suppliers from short-term traffic shocks.

Though much smaller in absolute value, insulation components are on track for a 7.94% CAGR—well ahead of industry growth. Demand stems from more-electric architectures that generate localized heat and urban air-mobility designs requiring tight acoustic footprints. Specialized players like TIGHITCO have introduced lightweight, fire-resistant blankets for battery compartments and avionics bays. As regulatory bodies tighten cabin noise and thermal performance rules, the aerospace parts manufacturing market share captured by insulation providers will likely increase.

By Material: Metals Retain Dominance as Advanced Ceramics Surge

Metallic content accounted for 46.23% of 2024 revenue, reflecting titanium’s ubiquity in engines, aluminum’s prevalence in primary structures, and high-strength steels in landing gear. Howmet Aerospace reported USD 3.735 billion in 2024 engine-product sales, exemplifying the scale in forged and precision-cast alloys.[2]Howmet Aerospace Investor Relations, “2024 Form 10-K Highlights,” howmetaerospace.com While metals are indispensable, suppliers grapple with titanium bottlenecks and price volatility, sparking interest in regional processing and recycling initiatives.

Advanced ceramics and ceramic matrix composites exhibit the fastest expansion at a 7.75% CAGR, leveraged by GE Aerospace’s serial production of CMC turbine shrouds and nozzles that permit hotter operating temperatures. The aerospace parts manufacturing market size attributed to these materials is still modest but rising swiftly as design teams chase higher thrust-to-weight ratios.

By Aircraft Type: Commercial Dominates, AAM Gains Altitude

Commercial aviation delivered 63.24% of the 2024 aerospace parts manufacturing market revenue as carriers restored capacity and pursued fuel burn reductions. Airbus targets 75 A320-family units per month by 2027, while the B737 MAX assembly line approaches its pre-crisis cadence, reinforcing visibility for Tier-1 and Tier-2 suppliers. Although smaller in unit terms, widebody programs contribute higher value per frame through complex structures and premium systems content.

AAM posts the highest growth at a 9.57% CAGR, reflecting aggressive investment in electric vertical take-off and landing (eVTOL) prototypes, regional hybrid aircraft, and cargo drones. Though volumes are embryonic, the nascent ecosystem demands bespoke propulsion, lightweight structures, and rapid-certification pathways—areas where nimble suppliers can secure early mover advantages. Over time, AAM’s share of the aerospace parts manufacturing market is poised to climb as certification milestones and infrastructure build-outs converge.

By End User: OEMs Command Scale as Aftermarket Ensures Resilience

OEMs accounted for 70.11% of the market revenue in 2024 and are expected to grow at a CAGR of 6.76% during the forecast period, buoyed by firm delivery schedules and rate increases on flagship platforms. Long-term purchase agreements, risk-sharing production models, and substantial capital barriers solidify their position at the top of the aerospace parts manufacturing market. Consolidation—epitomized by Boeing’s pending Spirit AeroSystems acquisition—furthers vertical integration, enabling tighter cost and quality oversight.

While smaller, the aftermarket is a profit stabilizer, with lifetime value often exceeding original sale proceeds. As global flight hours climb, airlines allocate larger budgets toward maintenance, repair, and overhaul. Providers secure Parts Manufacturer Approval (PMA) to enter competitive niches previously locked down by OEM-mandated proprietary parts.

Geography Analysis

North America accounted for 36.54% of 2024 revenue, underpinned by Boeing, Lockheed Martin, and a dense network of systems integrators clustered in Washington, California, and the Southeast.[3]PitchBook Data, “Boeing Company Profile 2025,” pitchbook.comMexico’s emergence as a cost-competitive nearshoring hub deepens regional self-sufficiency, complementing USMCA trade benefits and shortening logistics loops. Capital spending remains robust, exemplified by Howmet Aerospace’s USD 321 million program to expand high-temperature alloy production. FAA certification frameworks and ITAR regulations shape workflow complexity and nurture a mature quality-assurance culture that sustains export competitiveness.

Asia-Pacific is the fastest-growing region at 7.01% CAGR, anchored by China’s ambition to triple its fleet by 2042 and India’s policy push to localize aerospace manufacturing. Singapore’s high-value MRO ecosystem and South Korea’s component expertise add depth, while Southeast Asian nations court Tier-3 suppliers with tax incentives. Domestic champions such as AVIC and Hindustan Aeronautics absorb technology transfers and replicate best-in-class processes, gradually boosting regional content in global supply chains. Talent shortages and evolving regulatory alignments remain execution hurdles.

Europe maintains significant weight through Airbus and an array of specialty houses—Safran in engines, Rolls-Royce in propulsion, and Diehl in interiors. Airbus alone delivered EUR 69.2 billion (USD 82.10 billion) in 2024 revenue and is scaling A320 output to 75 units monthly. EASA environmental mandates spur material innovation and life-cycle analyses, while Brexit reshapes trade protocols between the UK and continental suppliers. The Middle East and Africa show selective strength, most notably in Gulf carrier fleet additions and associated MRO ventures, yet political and fiscal uncertainties temper broader uptake.

Competitive Landscape

Competitive intensity in the aerospace parts manufacturing market is fragmented and rising due to consolidation at the top and specialization among smaller players. RTX Corporation, Safran, and GE Aerospace continue to invest heavily in ceramic matrix composites, additive manufacturing, and digital thread initiatives to defend technological moats.

Tier-1 suppliers leverage size to negotiate long-term agreements, while Tier-2 and Tier-3 firms differentiate through niche capabilities such as high-temperature coatings or complex machining. Howmet Aerospace booked USD 975 million in 2024 capital deployment, funding bolt-on automation projects and share repurchases that reinforce its balance-sheet flexibility. At the same time, white-space entrants focus on AAM, hydrogen propulsion, and recyclable composites, aiming to disrupt incumbents with agile development cycles.

Certification hurdles act as barriers to entry, favoring organizations possessing established quality systems and financial stamina. Digitalization is another battleground; data-rich suppliers offering predictive maintenance insights or integrated design-for-manufacturability services often secure preferred-supplier status. Regionalization trends further shape the competitive map, as OEMs encourage local content to mitigate trade and logistics risk, opening doors for indigenous champions in Asia-Pacific and South America.

Aerospace Parts Manufacturing Industry Leaders

RTX Corporation

Honeywell International Inc.

Rolls-Royce Holdings plc

GE Aerospace (General Electric Company)

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Dassault Aviation and Tata Advanced Systems Limited signed four Production Transfer Agreements for manufacturing Rafale fighter aircraft fuselages in India. This agreement strengthens India's aerospace manufacturing capabilities and enhances its position in global supply chains.

- April 2025: Cyient DLM expanded its strategic partnership with Deutsche Aircraft to design, develop, and manufacture the Cabin Management System (CMS) for the D328eco, a 40-seater regional turboprop aircraft.

- March 2025: The US Air Force awarded GE Aerospace an indefinite delivery/indefinite quantity (IDIQ) contract worth USD 5 billion to support foreign military sales (FMS) of F110-GE-129 engines for F-15 and F-16 aircraft operated by allied nations globally.

Global Aerospace Parts Manufacturing Market Report Scope

| Engines |

| Aerostructures |

| Cabin Interiors |

| Support Equipment |

| Avionics |

| Insulation Components |

| Metals and Alloys |

| Composites |

| Plastics and Polymers |

| Advanced Ceramics and Ceramic Matrix Composites (CMCs) |

| Commercial Aviation |

| Military Aviation |

| General Aviation |

| Unmanned Aerial Systems (UAS) |

| Advanced Air Mobility (AAM) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Product Type | Engines | ||

| Aerostructures | |||

| Cabin Interiors | |||

| Support Equipment | |||

| Avionics | |||

| Insulation Components | |||

| By Material | Metals and Alloys | ||

| Composites | |||

| Plastics and Polymers | |||

| Advanced Ceramics and Ceramic Matrix Composites (CMCs) | |||

| By Aircraft Type | Commercial Aviation | ||

| Military Aviation | |||

| General Aviation | |||

| Unmanned Aerial Systems (UAS) | |||

| Advanced Air Mobility (AAM) | |||

| By End User | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aerospace parts manufacturing market in 2025?

The aerospace parts manufacturing market size is USD 1.02 trillion in 2025 and is projected to reach USD 1.39 trillion by 2030, translating into a 6.39% CAGR over the forecast period.

Which product category generates the most revenue?

Engines lead with 36.52% of 2024 sales, benefiting from both new-build and aftermarket demand.

What region is growing the fastest?

Asia-Pacific exhibits a 7.01% CAGR outlook, driven by China’s and India’s expanding fleets and rising local manufacturing.

Which material segment is expanding the quickest?

Advanced ceramics and ceramic matrix composites are projected to rise at a 7.75% CAGR as OEMs seek higher temperature capability and weight savings.

How is consolidation affecting suppliers?

Strategic acquisitions such as Boeing’s purchase of Spirit AeroSystems signal deeper vertical integration, raising the competitive bar for smaller firms.

What is the biggest restraint on market growth?

Skilled labor shortages, combined with escalating certification costs, are the primary headwinds limiting capacity expansion.

Page last updated on: