Europe Aviation Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

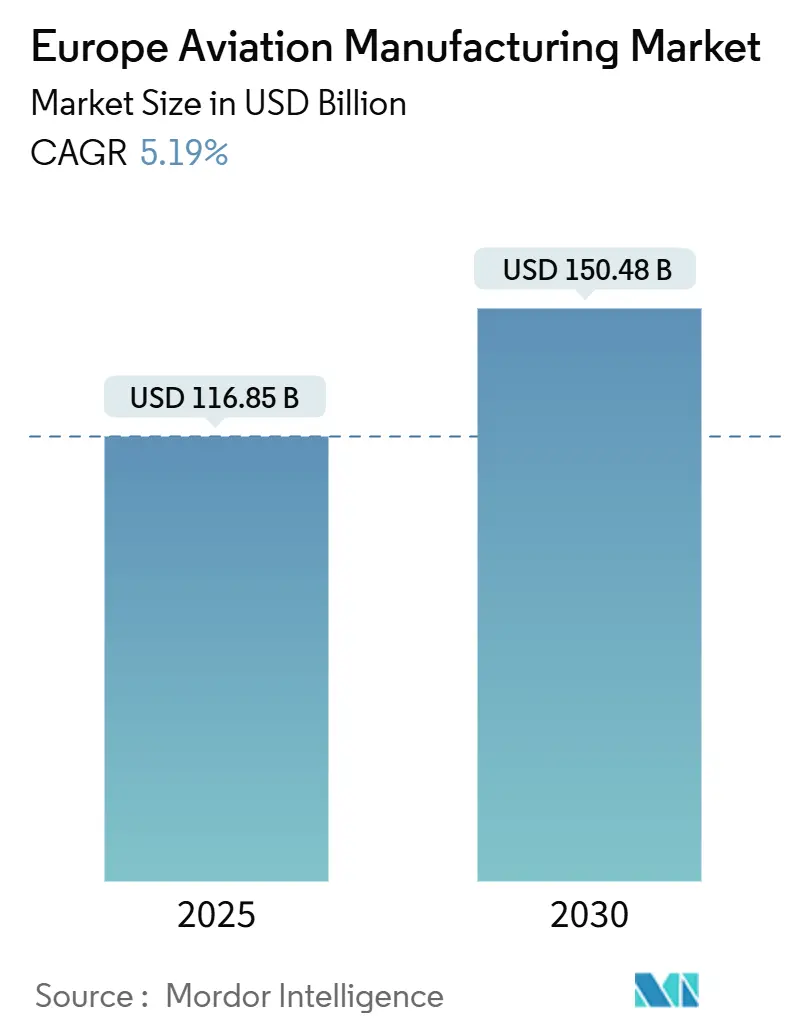

| Market Size (2025) | USD 116.85 Billion |

| Market Size (2030) | USD 150.48 Billion |

| Growth Rate (2025 - 2030) | 5.19% CAGR |

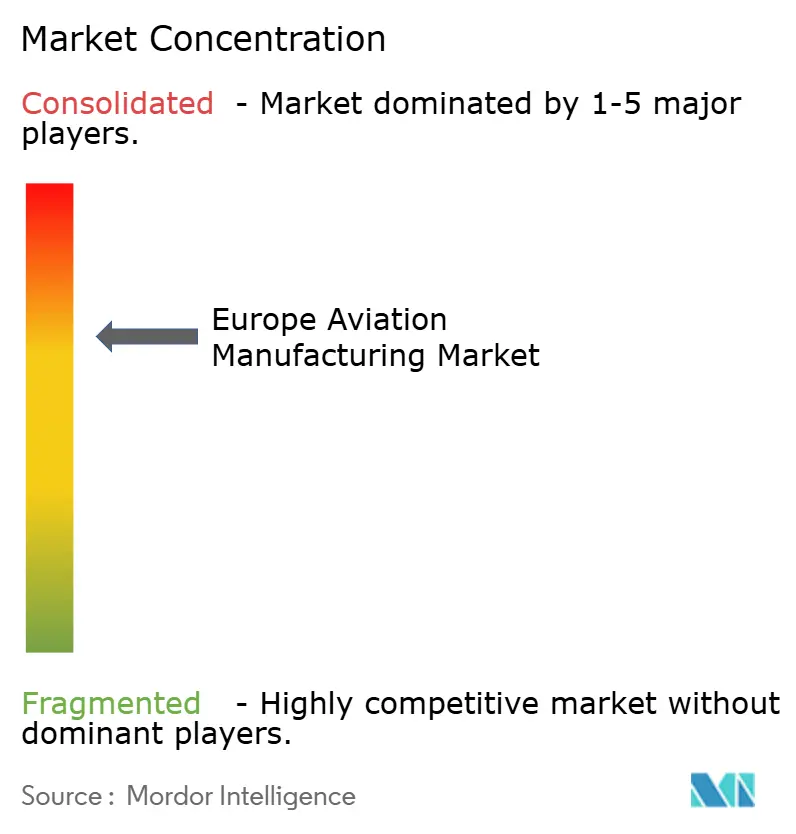

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Aviation Manufacturing Market Analysis by Mordor Intelligence

The Europe aviation manufacturing market size stood at USD 116.85 billion in 2025 and is forecasted to reach USD 150.48 billion by 2030, advancing at a 5.19% CAGR. Europe’s integrated value chain—spanning airframes, propulsion, and advanced materials—anchors this momentum while regulatory frameworks preserve the balance between innovation and safety. Sovereign defense budgets, a resurgent single-aisle backlog, and accelerating urban-air-mobility (UAM) programs jointly reinforce demand visibility across the Europe aviation manufacturing market. Supply-chain resilience initiatives, including titanium recycling and green-aluminum adoption, help companies hedge raw-material volatility and align with EU Taxonomy norms. Simultaneously, workforce-development alliances with technical universities aim to narrow looming skills gaps as veteran engineers retire across Germany, France, and the United Kingdom.

Key Report Takeaways

- By aircraft type, commercial aviation led with 58.98% of the European aviation manufacturing market share in 2024, while military aviation is projected to expand at a 6.93% CAGR through 2030.

- By component, propulsion systems accounted for 41.28% of the European aviation manufacturing market size in 2024, whereas landing gear and actuators are climbing fastest at a 6.48% CAGR.

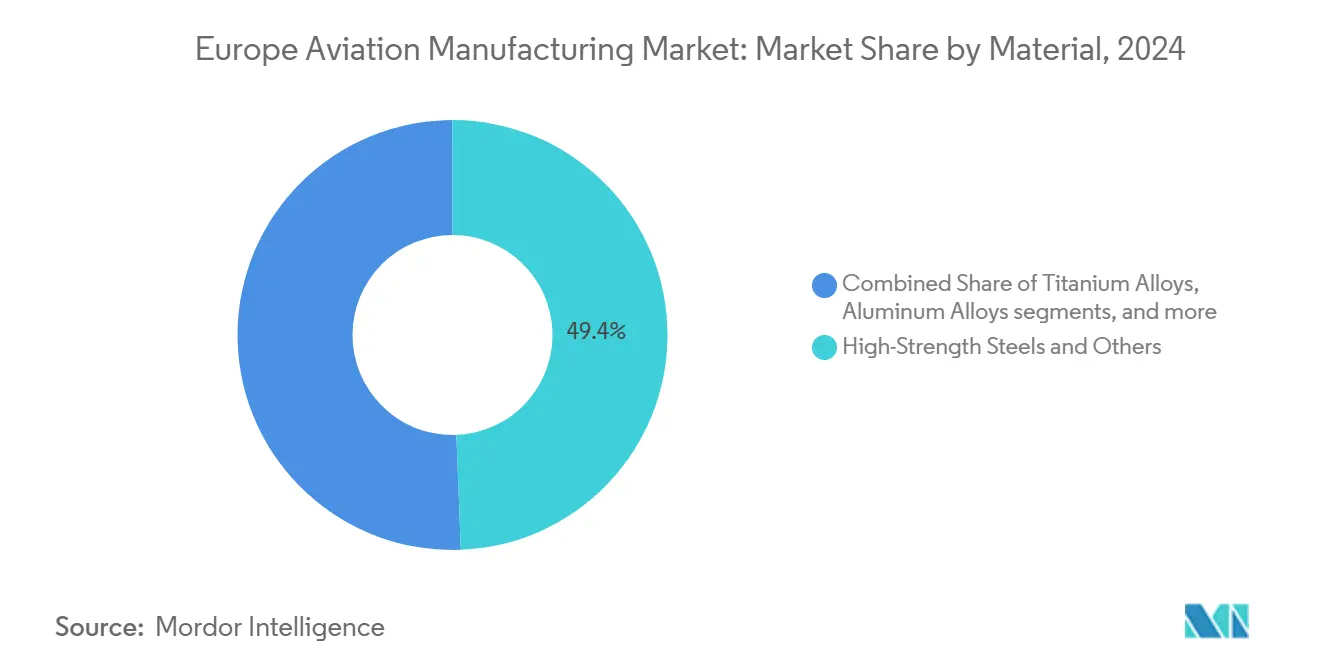

- By material, the high-strength steels and others segment retained a 49.38% share of the European aviation manufacturing market in 2024; carbon-fiber composites are pacing at a 7.18% CAGR to 2030.

- By geography, the United Kingdom commanded 39.49% of the European aviation manufacturing market share in 2024, whereas Germany is projected to register the quickest 7.82% CAGR through 2030.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on aviation manufacturing market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Aviation Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( %) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid ramp-up of single-aisle production rates | +1.60% | Germany, France, United Kingdom | Medium term (2-4 years) |

| Eurozone defense budgets redirecting capacity to military jets | +1.20% | EU core plus United Kingdom and Nordics | Short term (≤ 2 years) |

| Growing demand for narrowbody fleet replacement | +0.80% | European carriers with global fleets | Medium term (2-4 years) |

| Sustained MRO backlog supporting parts manufacturing | +0.90% | Germany, France, United Kingdom MRO hubs | Long term (≥ 4 years) |

| Use-case surge for eVTOL air-taxis ahead of 2030 urban mobility launches | +0.70% | Hamburg, Paris, Milan; EASA jurisdiction | Long term (≥ 4 years) |

| EU Taxonomy pressure accelerating green‐aluminum adoption | +0.6% | EU member states; Nordic aluminum suppliers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Ramp-Up of Single-Aisle Production Rates

Rising replacement cycles push Airbus to lift A320neo output despite supply bottlenecks in engines and titanium forgings.[1]Tamm Heike, “Airbus Secures Key Spirit AeroSystems Assets to Strengthen Aircraft Production,” avitrader.com Safran’s EUR 1 billion (USD 1.17 billion) global MRO expansion targets 1,200 LEAP shop visits annually by 2028, anchoring aftermarket certainty for the European aviation manufacturing market. Tier-1 suppliers adopt risk-sharing production models to synchronize schedules and buffer working-capital swings. While capacity growth unlocks revenue, it also magnifies exposure to component shortages that could stall final-assembly lines. Increased digital-twin deployment across German and French facilities helps predict part-shortfall scenarios and maintain on-time delivery commitments.

Eurozone Defense Budgets Redirecting Capacity to Military Jets

Defense outlays climbed to EUR 343 billion (USD 401.96 billion) in 2024, reallocating plant slots toward fighters such as Tempest/GCAP and Rafale lines.[2]European Defence Agency, “Defence Data Portal,” eda.europa.eu Dassault delivered 21 Rafales in 2024 and booked 30 more, pulling high-temperature composite production away from commercial tasks. Leonardo’s UAV venture with Baykar exemplifies joint programs that let mid-tier suppliers tap new military revenues without abandoning core civil contracts. This dual-track strategy stabilizes order books but strains specialist labor pools, intensifying competition for security-cleared technicians. Smaller subcontractors see entry points through industrial-cooperation clauses attached to multi-national fighter projects.

Growing Demand for Narrowbody Fleet Replacement

European carriers accelerate fleet renewal to meet carbon-intensity targets and noise-abatement regulations, spotlighting the European aviation manufacturing market in sustainability dialogues. Orders for A320neo variants by Eurowings and Brussels Airlines underscore priority on fuel burn and digital cockpit integration, while Vueling’s evaluation of B737 MAX options highlights pragmatic sourcing over historic allegiance. Retrofit programs for legacy cabins and avionics grant component makers incremental revenue as airlines synchronize replacement with maintenance intervals. Lifecycle-cost analytics, embedded in OEM service contracts, increasingly dictate configuration choices over list-price considerations.

Sustained MRO Backlog Supporting Parts Manufacturing

Safran’s worldwide repair-station network broadens reach to Brussels, Hyderabad, and Casablanca, reflecting 40% operating-profit growth at MTU Aero Engines in Q2 2025, mainly from MRO volume. Extended engine time-on-wing pushes deferred-maintenance peaks into 2026-2028, preserving shop-visit visibility that underpins capital-expenditure decisions across the European aviation manufacturing market. Landing-gear, avionics, and structural-component specialists see parallel advantages as airlines prioritize predictive-maintenance suites to avoid unscheduled downtime. Stable aftermarket cash flows enable suppliers to invest in additive-manufacturing cells and digital-thread architectures, improving turnaround times and cost profiles.

Restraints Impact Analysis*

| Restraint | ( %) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy workforce retirements causing skills gap | −0.8% | Germany, United Kingdom, France | Short term (≤ 2 years) |

| Titanium supply-chain vulnerability from Russia–Ukraine conflict | −0.9% | Europe with global upstream exposure | Medium term (2-4 years) |

| Sluggish widebody demand limiting composite wing capex | −0.5% | Europe-wide composite suppliers | Long term (≥ 4 years) |

| Persistent certification delays for next-gen propulsion | −0.5% | EASA jurisdiction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Workforce Retirements Causing Skills Gap

BDLI notes aerospace employment reached 120,000 in 2024, yet retirements outpace new-hire absorption in composite lay-up, precision machining, and systems-integration roles.[3]German Aerospace Industries Association, “Frontpage | BDLI,” bdli.de Higher defense workloads further siphon experienced staff, inflating wage levels and threatening delivery milestones for the European aviation manufacturing market. OEMs co-fund apprenticeship schemes with technical universities, but multi-year learning curves delay proficiency gains. Automation mitigates repetitive-task vacancies; however, tacit know-how in complex assembly still hinges on human expertise. Smaller suppliers lacking robust training budgets face consolidation risks as primes demand assured labor continuity.

Titanium Supply-Chain Vulnerability from Russia–Ukraine Conflict

The conflict curtailed traditional Russian feedstock, prompting substitution efforts via Japanese and Kazakh mills and aggressive in-house recycling investments such as IMET Alloys’ EUR 15 million (USD 17.58 million) program in France. Limited scrap availability means recycled volumes cannot quickly offset aerospace-grade billet shortfalls, elevating raw-material costs and elongating lead times for the European aviation manufacturing market. Strategic stockpiling consumes working capital, while long-term contracts with alternative smelters lock suppliers into elevated price floors. Design-to-cost engineering now emphasizes titanium-sparing architectures and hybrid-material joints to cushion price volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Military Surge Drives Growth

Military aviation is projected to compound at a 6.93% CAGR between 2025-2030 as Eurofighter upgrades, Tempest/GCAP development, and UAV acquisitions widen order backlogs. The European aviation manufacturing market benefits because fighter programs demand high-value composites, radar-absorbing structures, and mission-systems integration that outstrip margins available on civil narrow-bodies. Investment in non-combat platforms—transporters, tankers, and maritime-patrol aircraft—also channels fresh demand to German and French airframe plants.

Commercial aviation nevertheless preserves a 55.38% share of the European aviation manufacturing market size in 2024, owing to entrenched A320neo and A350 lines. Production tempo, however, hinges on engine-core availability and avionics-chip supply stabilization. Regional jets witness subdued prospects as airlines streamline networks, yet turboprop demand shows resilience for thin routes under 500 nm. General aviation segments hold niche relevance: business jet refurbishments generate cabin-interior work, while piston trainers remain vital for pilot pipeline continuity.

By Component: Propulsion Leadership Faces Actuation Challenge

Propulsion systems retained a 43.58% share of the European aviation manufacturing market in 2024, supported by LEAP, Trent, and PW1100G programs and lucrative service contracts. The aftermarket intensity of these engines underwrites R&D into open-fan and hybrid-electric demonstrators targeting 2030s entry-into-service.

Landing gear and actuation product lines post the fastest 6.48% CAGR as airlines retrofit electro-mechanical units that cut hydraulic-fluid weight while easing maintenance. European suppliers leverage modular architectures usable across fixed-wing and rotorcraft to diversify revenue within the European aviation manufacturing market. Meanwhile, avionics suites migrate toward integrated flight-management computers, enabling single-pilot operations on future regional aircraft, creating pull-through for sensor and software firms. Cabin-and-interior modules confront margin pressure from low-cost-carrier austerity but still earn a premium on long-haul comfort upgrades.

By Material: Composites Challenge Steel Dominance

The high-strength steels and others segment held a 42.87% share in 2024 as mature forging networks in France and Italy sustained low-cost volume. Yet environmental levies on energy-intensive blast furnace routes spur manufacturers to adopt green steel variants with renewable power inputs.

Carbon-fiber composites, growing at a 7.18% CAGR, feed wing-box, fuselage-panel, and nacelle contracts that lighten aircraft and shrink fuel burn. Thermoplastic tape-laying lines in Germany reduce autoclave cycles, driving unit-cost parity with aluminum. EU funding channels also back composite recycling, which is crucial for cradle-to-grave sustainability across the European aviation manufacturing market. Aluminum alloys remain relevant via green-aluminum initiatives like Norsk Hydro’s CIRCAL series, which achieves up to 75% lower carbon footprint than primary ingot production.[4]Norsk Hydro, “CIRCAL Low-Carbon Aluminum,” hydro.com Titanium alloys, though supply-constrained, stay indispensable for hot-section and landing-gear applications.

Geography Analysis

The United Kingdom owned 40.82% of the European aviation manufacturing market share in 2024, thanks to Rolls-Royce’s rebound—its valuation topping GBP 100 billion (USD 134.25 billion) on civil-engine aftermarket strength—and sustained BAE Systems defense output. Government backing through the Aerospace Technology Institute’s GBP 975 million (USD 1.31 billion) tranche continues until 2030, underwriting digital-manufacturing demonstrators in Derby and Bristol.

Germany is advancing at a 7.82% CAGR on MTU Aero Engines’ 40% year-on-year operating profit jump and Bavaria’s EUR 11 billion (USD 12.89 billion) aerospace-cluster revenues. Federal hydrogen-propulsion grants and Industry 4.0 retrofits help medium-sized suppliers scale capacity without eroding cost competitiveness in the European aviation manufacturing market.

France preserves Airbus’s Toulouse core and Safran’s multi-continental footprint, generating EUR 70.2 billion (USD 82.27 billion) in 2023 aerospace turnover and employing more than 210,000 people. Italy leverages Leonardo’s helicopter and fighter lines alongside a new UAV joint venture, Spain concentrates on Airbus wing work, while Sweden remains niche through Saab’s Gripen upgrades. Poland attracts tier-2 structures work as cost-sensitive primes rebalance eastward.

Competitive Landscape

The European aviation manufacturing industry displays moderate consolidation: Top primes—Airbus SE, Leonardo S.p.A., Rolls-Royce Holdings plc, BAE Systems plc, and Safran SA—shape platform roadmaps, but hundreds of specialist SMEs anchor niche capabilities. Strategic partnerships are proliferating; Diehl Aviation’s Romanian plant trims cost curves, whereas Airbus’s Spirit AeroSystems asset purchase secures composite-fuselage know-how. Cross-border joint ventures, typified by Leonardo-Baykar UAV cooperation, allow risk-sharing on capital-heavy prototypes while safeguarding intellectual property inside the European aviation manufacturing market.

Technology adoption dictates a competitive tempo. Digital twins, predictive maintenance analytics, and additive manufacturing of engine hardware differentiate MTU and Safran in bidding for open-fan demonstrators. Sustainability themes foster new entrants—Helsing’s CA-1 Europa autonomous fighter and AURA AERO’s hybrid-electric commuter program—each cultivated under EU emissions mandates. Established players respond by co-investing in hydrogen combustion tests to defend relevance against disruptive propulsion architectures.

White-space prospects include eVTOL final assembly, green aluminum rolling, and aircraft battery modules. However, EASA certification and EU Taxonomy compliance raise entry barriers, fortifying incumbents who already possess safety-assurance ecosystems. Top-tier OEMs increasingly vertically integrate high-margin sections, evident in Airbus reabsorbing Spirit facilities and nudging specialized suppliers toward service-heavy offerings to maintain their share within the European aviation manufacturing market.

Europe Aviation Manufacturing Industry Leaders

Airbus SE

Safran SA

BAE Systems plc

Rolls-Royce Holdings plc

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Diehl Aviation broke ground on a component facility in Craiova, Romania, which will employ 500 medium-term workers and supply commercial aircraft cabins.

- April 2025: Airbus secured key Spirit AeroSystems assets to bolster airframe production resilience against composite-supply disruptions.

- October 2024: Safran announced a EUR 1 billion (USD 1.17 billion) plan to enlarge its global LEAP-engine MRO network, targeting 1,200 annual shop visits by 2028.

Europe Aviation Manufacturing Market Report Scope

| Commercial Aviation | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Aircraft | |

| Military Aviation | Combat Aircraft |

| Non-Combat Aircraft | |

| Helicopters | |

| General Aviation | Business Jets |

| Turboprop Aircraft | |

| Piston Aircraft | |

| Helicopters |

| Airframe Structures |

| Propulsion Systems |

| Avionics and Flight-Control Systems |

| Cabin and Interior Modules |

| Landing Gear and Actuation |

| Other Components |

| Aluminum Alloys |

| Carbon-Fiber Composites |

| Titanium Alloys |

| High-Strength Steels and Others |

| Other Materials |

| United Kingdom |

| France |

| Germany |

| Italy |

| Spain |

| Russia |

| Sweden |

| Poland |

| Rest of Europe |

| By Aircraft Type | Commercial Aviation | Narrowbody Aircraft |

| Widebody Aircraft | ||

| Regional Aircraft | ||

| Military Aviation | Combat Aircraft | |

| Non-Combat Aircraft | ||

| Helicopters | ||

| General Aviation | Business Jets | |

| Turboprop Aircraft | ||

| Piston Aircraft | ||

| Helicopters | ||

| By Component | Airframe Structures | |

| Propulsion Systems | ||

| Avionics and Flight-Control Systems | ||

| Cabin and Interior Modules | ||

| Landing Gear and Actuation | ||

| Other Components | ||

| By Material | Aluminum Alloys | |

| Carbon-Fiber Composites | ||

| Titanium Alloys | ||

| High-Strength Steels and Others | ||

| Other Materials | ||

| By Geography | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Poland | ||

| Rest of Europe | ||

Key Questions Answered in the Report

How large will the Europe aviation manufacturing market be by 2030?

The Europe aviation manufacturing market is projected to reach USD 150.48 billion by 2030, growing at a 5.19% CAGR.

Which aircraft segment is expanding fastest?

Military aviation is expected to grow at a 6.93% CAGR between 2025-2030.

What materials are gaining share in European aircraft production?

Carbon-fiber composites are increasing at a 7.18% CAGR as manufacturers prioritize weight savings and sustainability.

Which country currently holds the largest share of European aviation output?

The United Kingdom leads with 40.82% of regional output, anchored by Rolls-Royce Holdings plc and BAE Systems plc.

How are labor shortages being addressed?

OEMs collaborate with technical universities and invest in automation to mitigate skills gaps from retiring engineers.

Why is MRO activity important to market growth?

A sustained engine-repair backlog provides stable cash flow and funds R&D, bolstering overall market resilience through 2028.

Page last updated on: