North America Aircraft Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

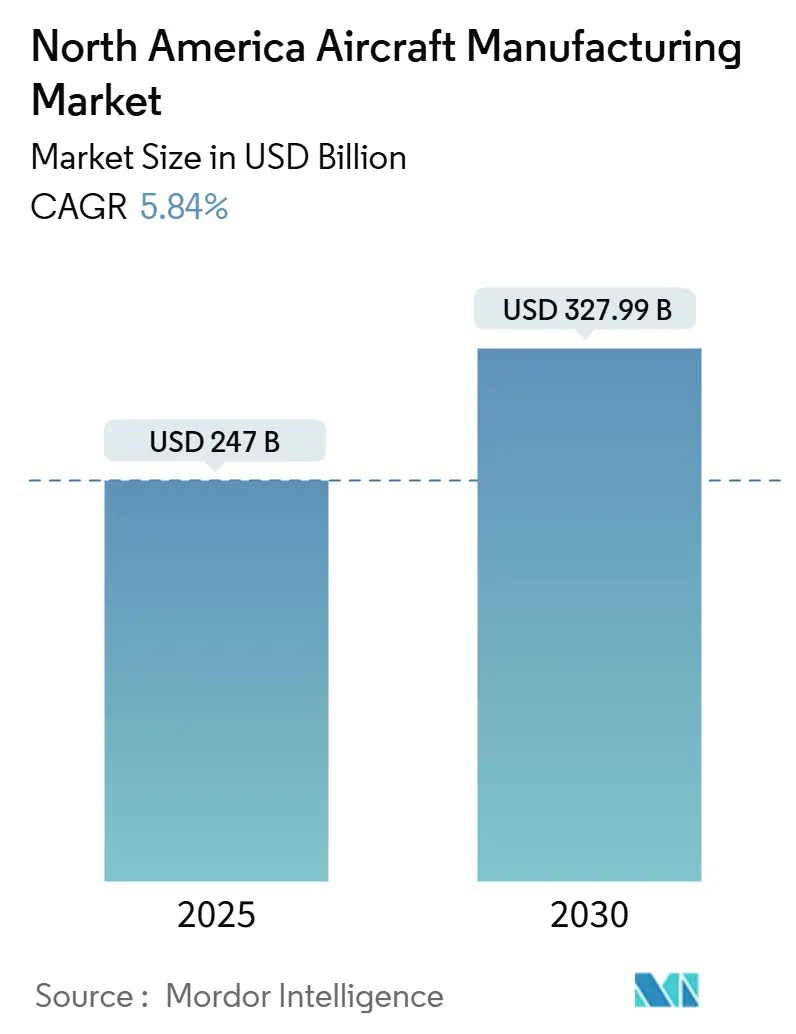

| Market Size (2025) | USD 247 Billion |

| Market Size (2030) | USD 327.99 Billion |

| Growth Rate (2025 - 2030) | 5.84% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Aircraft Manufacturing Market Analysis by Mordor Intelligence

The North America aircraft manufacturing market size stands at USD 247 billion in 2025 and is forecasted to reach USD 327.99 billion by 2030, expanding at a 5.84% CAGR. Defense-modernization programs, sustainable-propulsion investment, and digital-manufacturing adoption jointly propel the North America aircraft manufacturing market, even as supply-chain fragility and labor shortages temper output scalability. Boeing’s USD 18–20 billion NGAD F-47 contract shows how defense requirements reshape civil design philosophies, accelerating cross-platform technology transfer in fly-by-wire software, composite structures, and sensor fusion. Narrowbody fleet-renewal cycles that promise 15–20% fuel savings keep order books robust despite macroeconomic headwinds. At the same time, hydrogen-propulsion pilots and sustainable-aviation-fuel incentives push manufacturers toward emission-free architectures. Supply-chain reconfiguration around titanium, wiring harnesses, and semiconductors remains a critical risk, yet vertical integration and near-shoring strategies partially offset vulnerability. Competitive intensity tightens as the Boeing–Airbus duopoly deepens and defense primes expand through acquisitions to secure electronics, propulsion, and autonomy capabilities.

Key Report Takeaways

- By aircraft type, narrowbody platforms led with a 51.55% share of the North America aircraft manufacturing market in 2024, whereas business jets are forecasted to expand at a 6.75% CAGR through 2030.

- By application, commercial passenger aviation accounted for 61.86% of the North America aircraft manufacturing market size in 2024; military and defense is advancing at a 7.32% CAGR to 2030.

- By propulsion technology, conventional jet-fuel and SAF-ready aircraft retained 69.83% of the North America aircraft manufacturing market share in 2024, while hydrogen-propulsion platforms are projected to post a 6.98% CAGR to 2030.

- By geography, the US commanded 71.25% of the North America aircraft manufacturing market in 2024; Canada is forecasted to be the fastest-growing geography at a 5.32% CAGR, supported by Quebec’s cluster expansion.

Worldwide, activity is shaped by contributions from multiple regions, with North america representing one of the more structurally developed among them. The global report on aircraft manufacturing market by Mordor Intelligence reflects how these regional layers combine into a single system.

North America Aircraft Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commercial-fleet modernization and backlog digestion | +1.30% | North America and Global | Medium term (2-4 years) |

| Soaring defense outlays for next-gen air-platforms | +1.10% | United States and Canada | Long term (≥ 4 years) |

| Rapid adoption of advanced composites and additive manufacturing | +0.80% | North America and EU | Short term (≤ 2 years) |

| Digitized MRO/predictive analytics demand | +0.60% | Global, North America leadership | Medium term (2-4 years) |

| Reshoring and Mexico near-shoring incentives | +0.70% | United States and Mexico | Long term (≥ 4 years) |

| Tail-wind from e-commerce cargo conversions | +0.50% | North America, spillover to Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Commercial-Fleet Modernization and Backlog Digestion

A record order book underpins multi-year output visibility for the North America aircraft manufacturing market. Boeing’s backlog exceeds 5,900 aircraft, while Airbus delivered 263 jets during January–May 2024, highlighting sustained demand despite financing headwinds. Airlines replace aging fleets to secure 15–20% fuel-efficiency gains and lower maintenance burdens. United Airlines’ conditional purchase for up to 200 JetZero blended-wing aircraft illustrates how efficiency targets foster unconventional aerostructures.[1]“United Airlines Partners with JetZero for Blended Wing Aircraft,” United Airlines, united.com Production stability allows OEMs to invest in capacity expansions, yet FAA-mandated caps of 38 B737 MAX units per month constrain near-term throughput. Stable backlogs safeguard supplier payrolls and encourage tooling upgrades despite macroeconomic volatility.

Soaring Defense Outlays for Next-Gen Air-Platforms

US and Canadian defense budgets inject counter-cyclical momentum into the North America aircraft manufacturing market as Boeing’s USD 18–20 billion NGAD F-47 contract moves from concept to prototype.[2]Bo Sun, “Boeing Wins NGAD Contract for Next-Generation Fighter Development,” Reuters, reuters.com Canada’s CAD 19 billion (USD 13.74 billion) F-35 procurement embeds industrial-participation clauses that channel composite-structure work into regional suppliers. Program longevity stretches into the 2040s, anchoring skilled-labor demand and funding incremental sensor, avionics, and stealth-material breakthroughs. Lockheed Martin’s Vectis wingman drone underscores how manned-unmanned teaming spawns adjunct production lines. Defense programs mitigate commercial cyclicality and accelerate dual-use technology migration into civil cockpits and cabins.

Rapid Adoption of Advanced Composites and Additive Manufacturing

Advanced-composite wings, thermoplastic fuselage skins, and additive-manufactured brackets reduce structural weight by up to 15% while simplifying part counts. Boeing and Airbus each target 100-jet-per-month single-aisle rates using high-automation composite lay-up cells that curtail takt times. Digital-twin validation halves prototype iterations, cutting both lead time and scrap. On-demand 3-D-printed spares shrink inventory overhead, particularly for aging regional fleets. Uptake varies; early adopters focus on single sub-assemblies to capture quick wins. Firms that integrate design-for-AM practices lock in weight savings that translate to lower operating costs, reinforcing market competitiveness.

Digitized MRO/Predictive Analytics Demand

Operators deploy aircraft-health-monitoring suites (AHMS) that analyze real-time sensor feeds to predict component fatigue, reducing unplanned downtime. Engine OEMs package analytics subscriptions with spare-parts pools, creating recurring revenue streams that enlarge the North America aircraft manufacturing market beyond green-aircraft sales. Airlines value data-driven maintenance regimes that boost dispatch reliability above 99%. Digital-thread continuity from factory to field builds feedback loops that refine future design iterations. Adoption is most pronounced in North America, where ground-data offload bandwidth and regulatory frameworks enable seamless information flow. MRO digitization also supports remote inspections, lowering engineer travel costs and speeding return-to-service decisions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FAA quality-control clamp-downs post-2024 incidents | -0.80% | United States, global spillover | Medium term (2-4 years) |

| Raw-material (Ti, Al) geopolitical supply shocks | -0.90% | North America and Global | Short term (≤ 2 years) |

| Skilled-labor crunch across US and Canada plants | -0.70% | North America and EU regulatory focus | Long term (≥ 4 years) |

| Long certification cycles for novel propulsion | -0.60% | Global, North America leadership | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FAA Quality-Control Clamp-Downs Post-2024 Incidents

Intensified oversight after safety lapses caps B737 MAX monthly output at 38 units, trimming cash flow despite solid demand. The FAA’s proposed Part 25 cybersecurity rule expands design-assurance tasks, lengthening test campaigns and inflating engineering workloads.[3]“FAA Investigates Counterfeit Titanium in Aircraft,” FAA, faa.gov Counterfeit-titanium discoveries force rigorous supplier-traceability audits that elevate procurement costs. DO-326A security standards require avionics firms to harden systems against cyber threats, adding hardware redundancy and weight. Smaller airframers struggle to fund compliance staff, leading to schedule slips and potential market-share erosion.

Raw-Material (Ti, Al) Geopolitical Supply Shocks

Sanctions removed access to 40% of global aerospace-grade titanium, pushing North American lead times beyond 90 weeks. Collins Aerospace incurred USD 175 million in supplier-switching and requalification expenses.[4] “Collins Aerospace Addresses Titanium Supply-Chain Challenges,” Collins Aerospace, collinsaerospace.com Alternative Japanese mills ramp up output, yet capacity gaps persist, sustaining price volatility. Aluminum faces similar pressures as trade barriers reallocate billet flows. Recycling and closed-loop scrap capture gain traction but require multi-year capital outlays. Persistent material uncertainty forces OEMs to enlarge safety stocks, tying up working capital and complicating lean-manufacturing objectives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Business Jets Accelerate Despite Narrowbody Dominance

The narrowbody class retained a 51.55% share of the North America aircraft manufacturing market size in 2024 based on high-volume airline orders for B737 MAX and A321neo families. However, the business-jet segment is projected to post a 6.75% CAGR, buoyed by corporate travel appetite and fleet-renewal cycles prioritizing cabin flexibility and point-to-point speed. Honeywell forecasts 8,500 deliveries worth USD 280 billion over the next decade, with North America capturing 66% of that count.[5]“United Airlines Partners with JetZero for Blended Wing Aircraft,” United Airlines, united.com NBAA data indicate an 11% rise in 2025 business-aircraft deliveries valued at USD 25 billion, confirming sustained demand despite charter-rate normalization. Operators migrate toward super-mid and large-cabin models capable of intercontinental legs, embedding advanced avionics and cabin connectivity to replicate office environments aloft.

While narrowbody output remains the production-volume anchor, business jet programs deliver higher unit margins and diversified revenue through aftermarket services. Bombardier’s strategic pivot toward aftermarket income illustrates how OEMs balance cyclical airline exposure with stable service contracts. Regional-jet activity benefits from LCC route maps, yet faces competition from new turboprop concepts promising lower per-seat costs on sub-500-mile sectors. Widebody prospects lag given muted long-haul recovery, but freighter conversions inject partial demand. Helicopters and amphibious craft occupy niche roles in EMS, firefighting, and remote logistics, commanding premium pricing yet limited volumes.

By Application: Military Defense Spending Accelerates Growth

Commercial passenger use sustained a 61.86% share of the North America aircraft manufacturing market in 2024 as airlines restored capacity to near-pre-pandemic seat miles. Military and defense orders, however, are expected to advance at a 7.32% CAGR through 2030, reflecting multiyear procurement horizons and rising geopolitical tension. Boeing’s NGAD F-47 program assures a production ramp into the 2040s, while Canada’s CAD 19 billion (USD 13.74 billion) F-35 buy embeds industrial participation for domestic firms. Cargo operators capitalize on e-commerce growth and supply-chain regionalization demands, but face pilot availability constraints.

Business aviation gains from corporates valuing schedule flexibility and health security, turning private lift into a baseline travel tool rather than a discretionary perk. Special mission aircraft—ISR, firefighting, and border patrol—enjoy stable funding streams due to government-mandated responsibilities, further diversifying demand. The cross-pollination of technologies between defense and civil spheres expedites avionics, material, and propulsion advances, enhancing the overall competitiveness of the North American aircraft manufacturing market.

By Propulsion Technology: Hydrogen Innovation Challenges Conventional Dominance

Conventional jet-fuel designs, including SAF-ready variants, represented 69.83% of the North American aircraft manufacturing market share in 2024. Yet hydrogen-propelled concepts top the growth leaderboard at a 6.98% CAGR to 2030, underpinned by aggressive emission-reduction mandates. American Airlines’ order for 100 ZeroAvia engines to retrofit CRJ700s validates early commercial viability. Universal Hydrogen’s successful regional flight demo de-risked operational handling, while Airbus’s 2035 ZEROe target pushes architecture selection toward either fuel-cell electric or direct-burn combustion. Pratt & Whitney’s HySIITE explores liquid-hydrogen cycles compatible with geared turbofans, hinting at feasible single-aisle adoption.

Hybrid-electric solutions primarily target sub-600-mile missions where battery-weight premiums remain acceptable. Meanwhile, conventional airframe retrofits ensure fleet coverage resilience as airlines await infrastructure rollouts. The North American aircraft manufacturing market maintains dual-track propulsion strategies to hedge technological and regulatory uncertainties, blending incremental SAF adoption with leapfrog hydrogen R&D.

Geography Analysis

Canada posts the fastest regional growth at a 5.32% CAGR through 2030, anchored by Quebec’s aerospace cluster, which hosts 65% of Canada’s sector employment and specialized capabilities in composites, simulation, and regional aircraft assembly. Bombardier pivots its Montreal facilities toward high-margin Global and Challenger jet completions and aftermarket support, augmenting value-added services revenue. CAE scales pilot-training centers, leveraging simulator demand tied to pilot shortages and regulatory proficiency mandates. Federal offsets tied to F-35 procurement enhance supply-chain sophistication, injecting capital into SME fabrication shops.

The United States, while mature, retains 71.25% of the North America aircraft manufacturing market size thanks to entrenched OEM campuses in Washington, Alabama, Texas, and South Carolina. The Pentagon budgets support multibillion-dollar fighter, tanker, and rotorcraft programs that sustain engineering workforces and encourage suppliers to co-locate near assembly lines. Airbus’s second A320neo line in Mobile doubles its US capacity, signaling confidence in onshore production economics. Clustering of MRO, avionics, and interiors firms around Dallas–Fort Worth and Phoenix further deepens the ecosystem.

Mexico contributes 60,000 aerospace workers generating USD 8 billion in annual exports, specializing in wiring harnesses, landing-gear machining, and aero-engine cases. Safran’s USD 80 million Queretaro expansion highlights rising subsystem competence. Embraer’s evaluation of C-390 Millennium final assembly in Mexico underscores the country’s competitive labor cost and proximity to the US defense customer base. Tri-national supply-chain integration within USMCA fosters resilience by diversifying sourcing away from geopolitically risky nodes.

Mordor Intelligence provides coverage of the aircraft manufacturing market across other key regional markets, including Asia and Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

Boeing and Airbus remain the commercial center of gravity, yet both rely on strategic acquisitions to secure supply and technologies. Boeing’s USD 8.3 billion takeover of Spirit AeroSystems pulls critical fuselage and structural assemblies in-house, aiming to reduce quality lapses that plagued B737 MAX output. Airbus counters through organic capacity expansion, inaugurating its second A320neo line in Alabama to shorten lead times and strengthen its US market share.

Defense-prime consolidation reshapes subsystem portfolios. BAE Systems’ purchase of Ball Aerospace deepens electro-optical payload and space-system capabilities, aligning with the integrated-sensor demands of sixth-generation fighters.[6]“Sustainable Aviation Fuel Grand Challenge,” U.S. Department of Energy, energy.gov Lockheed Martin’s Vectis drone-wingman project advances manned-unmanned teaming, while Raytheon’s Pratt & Whitney progresses hydrogen-combustion demonstrators that may spill into civil programs. Vertical integration provides supply-chain visibility, regulatory leverage, and intellectual-property insulation.

White-space exploration accelerates. Boeing’s USD 70 million investment in Wisk Aero’s Canadian operations signals legacy OEM interest in autonomous air-taxi niches. Collaboration patterns reveal that established players increasingly partner with start-ups for software and battery expertise while contributing certification know-how and production scale. Aftermarket competition intensifies as OEMs expand parts distribution networks and predictive analytics platforms to lock in annuity revenues.

North America Aircraft Manufacturing Industry Leaders

The Boeing Company

Lockheed Martin Corporation

Bombardier Inc.

Textron Inc.

Airbus SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Airbus opened its second A320neo assembly line in Mobile, Alabama, a USD 300 million project adding 400 jobs.

- September 2025: Avelo Airlines placed a USD 4 billion order for 50 Embraer E-Jets, with options for 50 more.

- March 2025: The US DoD awarded the Engineering and Manufacturing Development (EMD) contract worth USD 18-20 billion to The Boeing Company for the NGAD F-47 combat aircraft.

North America Aircraft Manufacturing Market Report Scope

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Turboprop Aircraft |

| Business Jets |

| Helicopters |

| Amphibious Aircraft |

| Commercial Passenger |

| Cargo/Freight |

| Military and Defense |

| Business/Private Aviation |

| Special Mission (Surveillance, Emergency) |

| Conventional Jet-Fuel Aircraft/SAF-Ready Aircraft |

| Hybrid-Electric Aircraft |

| Hydrogen-Propulsion Aircraft |

| North America | United States |

| Canada | |

| Mexico |

| By Aircraft Type | Narrowbody Aircraft | |

| Widebody Aircraft | ||

| Regional Jets | ||

| Turboprop Aircraft | ||

| Business Jets | ||

| Helicopters | ||

| Amphibious Aircraft | ||

| By Application | Commercial Passenger | |

| Cargo/Freight | ||

| Military and Defense | ||

| Business/Private Aviation | ||

| Special Mission (Surveillance, Emergency) | ||

| By Propulsion Technology | Conventional Jet-Fuel Aircraft/SAF-Ready Aircraft | |

| Hybrid-Electric Aircraft | ||

| Hydrogen-Propulsion Aircraft | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the current value of the North America aircraft manufacturing market?

The North America aircraft manufacturing market is valued at USD 247 billion in 2025 and is projected to reach USD 327.99 billion by 2030, expanding at a 5.84% CAGR.

Which aircraft segment is growing the fastest in North America?

Business jets are expected to record the highest CAGR at 6.75% through 2030.

How big is the defense contribution to regional aircraft demand?

Military and defense applications are projected to grow at 7.32% CAGR, the fastest among all applications.

Why is hydrogen propulsion gaining traction?

Airline zero-emission commitments and successful flight demonstrations, such as ZeroAvia’s CRJ700 retrofit, are accelerating adoption prospects.

Which country in North America will grow quickest?

Canada is forecasted to post the fastest regional growth at 5.32% CAGR, driven by Quebec’s aerospace cluster and defense offsets.

How are supply-chain risks being managed?

OEMs pursue vertical integration, diversified sourcing, and recycling to mitigate titanium shortages and other material bottlenecks.

Page last updated on: