Aircraft Spare Parts Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

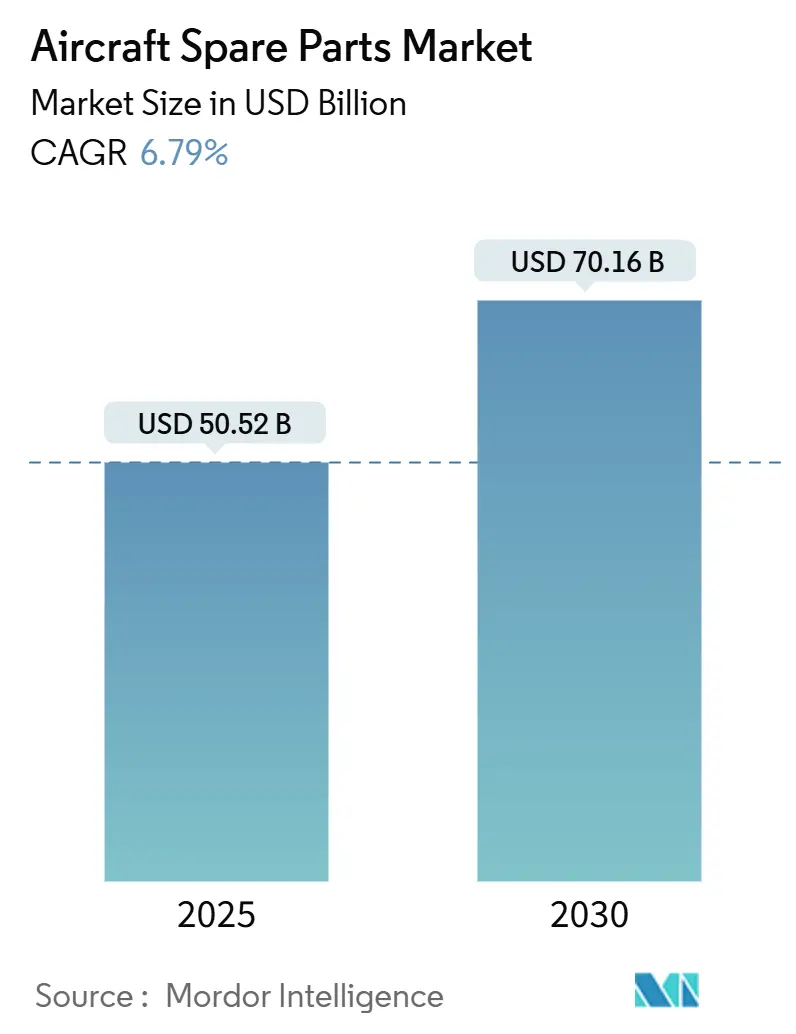

| Market Size (2025) | USD 50.52 Billion |

| Market Size (2030) | USD 70.16 Billion |

| Growth Rate (2025 - 2030) | 6.79% CAGR |

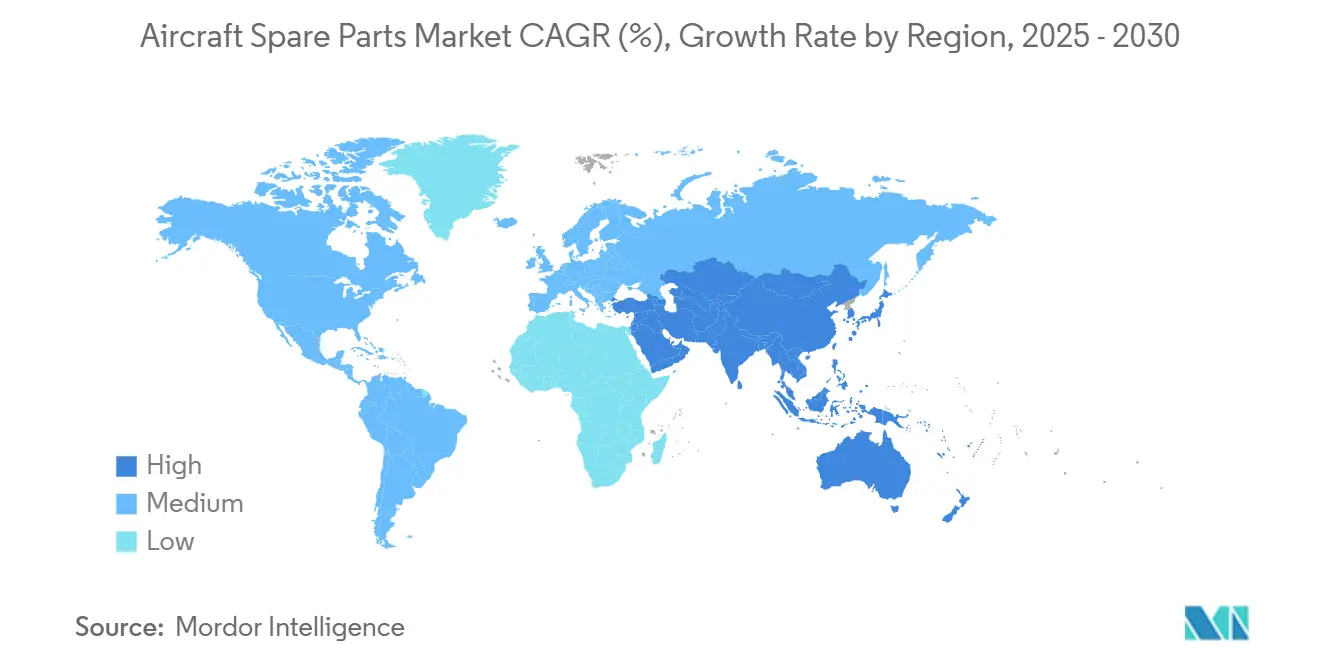

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

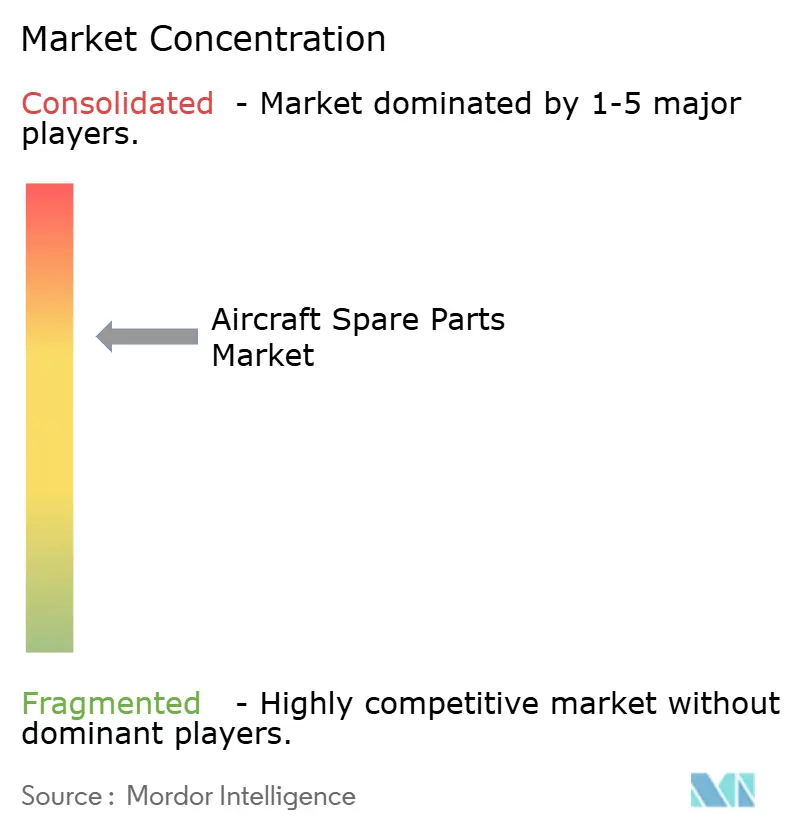

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aircraft Spare Parts Market Analysis by Mordor Intelligence

The aircraft spare parts market size stood at USD 50.52 billion in 2025 and is forecasted to reach USD 70.16 billion by 2030, translating to a 6.79% CAGR. Growth is propelled by simultaneous fleet expansion and aging, production backlogs that lengthen in-service lives, and airline strategies favoring cost-efficient Parts Manufacturer Approval (PMA) and Used Serviceable Material (USM) components over costlier original equipment. Airlines’ pivot toward independent maintenance, repair, and overhaul (MRO) partners has accelerated as PMA components generate 20-40% savings while retaining regulatory compliance. Titanium-intensive engine upgrades, heightened narrowbody utilization, and blockchain-enabled e-commerce channels further widen demand for traceable, competitively priced parts. Meanwhile, consolidation among tier-1 suppliers and OEM efforts to protect intellectual property shape a competitive landscape in which digital capabilities and inventory agility offer decisive advantages.

Key Report Takeaways

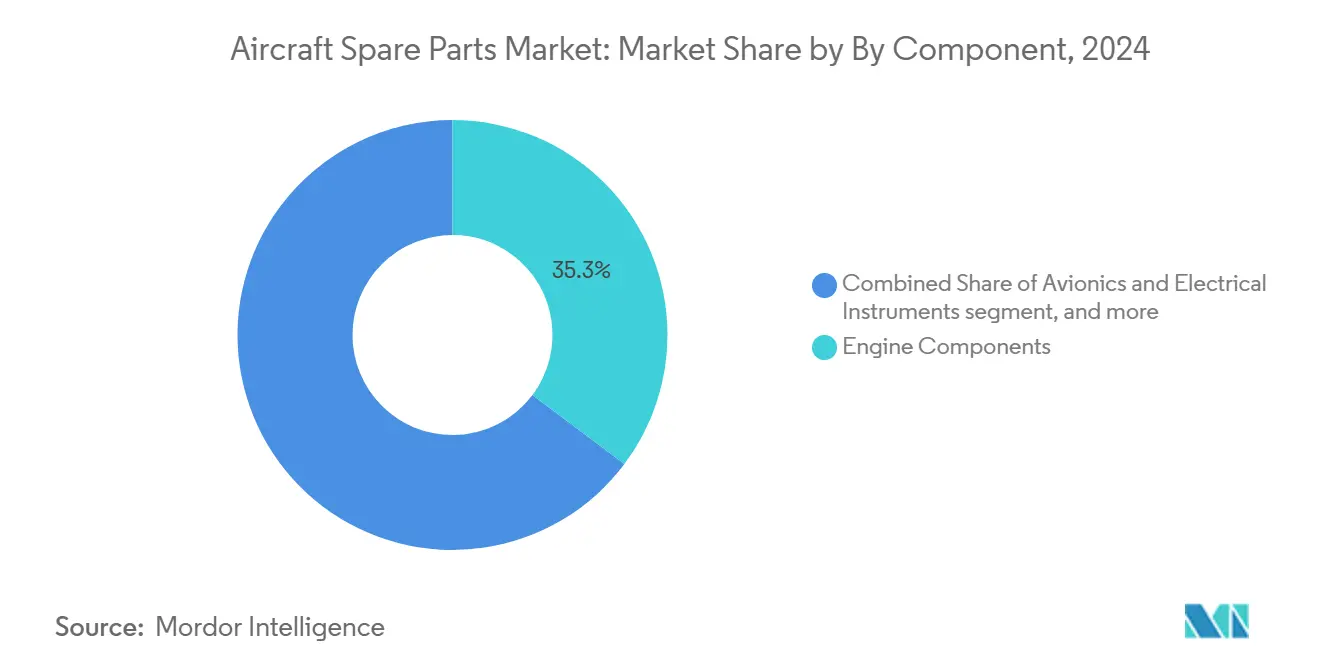

- By component type, engine components commanded 35.25% of the aircraft spare parts market share in 2024.

- By aircraft platform, widebody aircraft captured 42.75% revenue in 2024; narrowbody aircraft are projected to post an 8.83% CAGR through 2030.

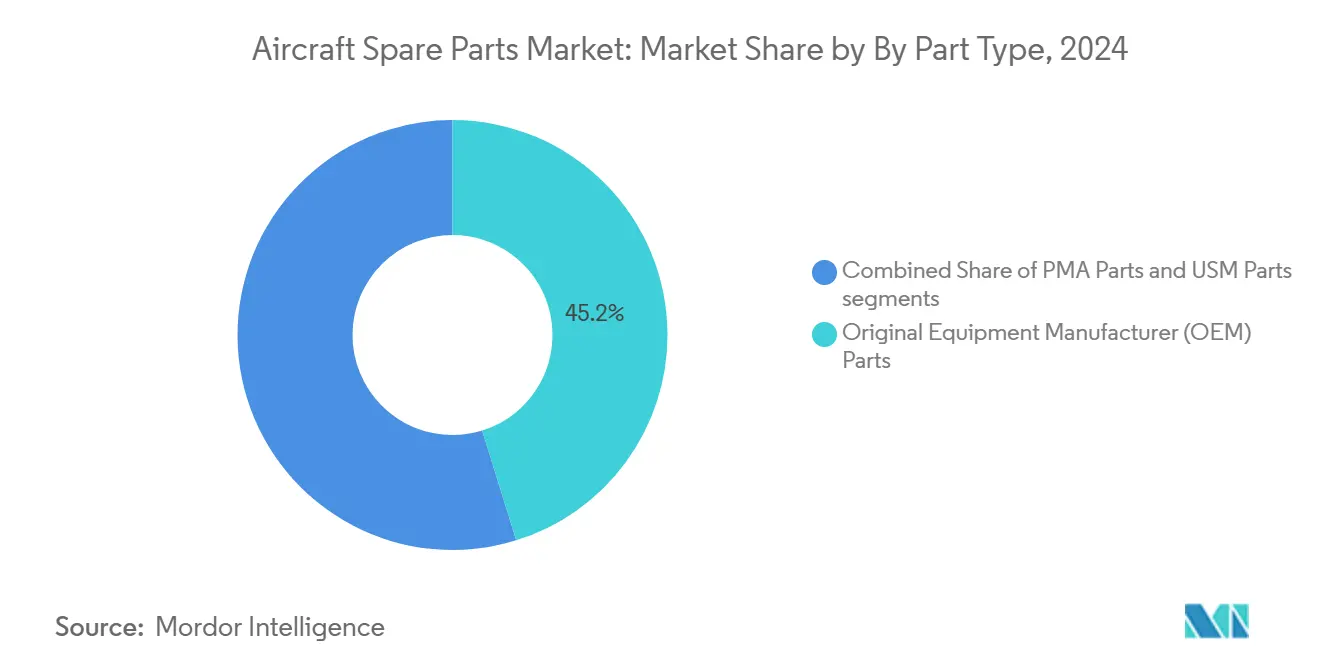

- By part type, Original Equipment Manufacturer (OEM) parts commanded 45.21% market share, while Parts Manufacturer Approval (PMA) components are projected to grow at a 7.80% CAGR between 2025 and 2030.

- By end user, OEM channels held 55.32% of the aircraft spare parts market size in 2024, while independent MROs are expanding at a 7.91% CAGR to 2030.

- By geography, North America accounted for 38.22% of global spending in 2024; Asia-Pacific is advancing at a 7.23% CAGR through 2030

Global Aircraft Spare Parts Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet expansion and ageing aircraft boosting MRO demand | +2.1% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| OEM production backlogs extend aircraft service lives | +1.8% | Global; Asia-Pacific and North America most exposed | Short term (≤2 years) |

| Growth in global passenger traffic and utilization | +1.5% | Asia-Pacific core; spill-over to MEA and Latin America | Long term (≥4 years) |

| Rising adoption of PMA and USM parts for cost savings | +1.2% | North America and EU; expanding in Asia-Pacific | Medium term (2-4 years) |

| Blockchain-enabled e-commerce marketplaces and traceability | +0.9% | Global; early uptake in North America and Europe | Short term (≤2 years) |

| Titanium demand surge from engine durability upgrades | +0.7% | Global supply diversification in US and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fleet expansion and ageing aircraft boosting MRO demand

The aircraft spare parts market is witnessing robust growth as global fleet expansion coincides with the ageing of existing aircraft. Airlines are rapidly adding new aircraft to accommodate rising passenger traffic, yet a substantial portion of the current fleet is reaching maturity, requiring frequent inspections, repairs, and replacements. Record backlogs—Boeing logged 5,943 aircraft on order in 2025—force carriers to fly older jets longer, lifting maintenance frequency and spare-parts budgets by 15-20% among Asia-Pacific regionals.[1]Boeing Logs 606 Net Orders in 2025,” Mexico Business, mexicobusiness.news Airlines postpone retirements, notably narrowbody fleets, to offset delivery delays, resulting in heavier engine shop visits and greater consumption of hard-to-source life-limited parts. FAA and EASA enhanced-airworthiness programs enable the practice, yet mandate rigorous traceability. These factors translate directly into higher demand for certified components across engines, landing-gear assemblies, and cabin interiors. This dual scenario significantly boosts the demand for MRO services. Ageing aircraft, in particular, drive recurring spare parts requirements, while fleet expansion ensures sustained long-term demand. Together, these factors create a steady market cycle, positioning MRO as a critical growth driver for the aircraft spare parts industry.

OEM production backlogs extend aircraft service lives

The persistent production backlogs faced by original equipment manufacturers (OEMs) are compelling airlines to extend the operational life of their existing aircraft fleets. With new aircraft deliveries delayed, carriers increasingly rely on older aircraft, which demand higher MRO activities. Production caps Boeing’s current 38-unit monthly rate, and supply constraints at Airbus compel operators to intensify utilization of existing aircraft, accelerating wear on titanium fan blades, compressor disks, and exhaust components.[2]Titanium Demand Surges on Aircraft Engine Growth,” Argus Media, argusmedia.com Engine MRO specialists report 25-30% spikes in unscheduled removals, opening space for PMA suppliers who respond faster than OEMs tethered to new-build priorities. Service difficulty reporting tightens oversight, but independent suppliers leverage quicker lead times to capture share. This directly increases spare parts consumption to ensure safety, compliance, and operational efficiency. Extended service lives of aircraft create recurring replacement cycles, fueling sustained aftermarket demand. Consequently, OEM bottlenecks not only affect fleet renewal strategies but also strengthen the role of spare parts and MRO providers in maintaining global airline operations.

Growth in global passenger traffic and utilization

The steady rise in global passenger traffic significantly increases aircraft utilization, driving demand for spare parts and maintenance services. Airlines are operating fleets at higher frequencies to meet the surge in travel demand, leading to accelerated wear and tear of critical components. Passenger traffic exceeded pre-pandemic levels by 2025, led by 8%-plus gains in China and India.[3]India Aviation Market to Be Worth $40 Billion by 2027,” Economic Times, economictimes.indiatimes.com Airlines operate aircraft 10-15% above historical utilization, stressing landing-gear, auxiliary-power units, and pressurization systems whose life limits correlate with flight cycles, not calendar time. Turboprop and regional jet segments feel acute pressure because short-haul frequency accelerates cycle-driven fatigue. Robust ICAO forecasts suggest durable growth that underpins the long-term outlook for the aircraft spare parts market. This heightened utilisation shortens replacement cycles and amplifies the need for reliable MRO support. As international and domestic travel rebounds strongly, the consistent pressure on airlines to maintain operational efficiency and safety ensures a growing market for spare parts, underpinning long-term industry expansion.

Rising adoption of PMA and USM parts for cost savings

Airlines and MRO providers are increasingly adopting Parts Manufacturer Approval (PMA) and Used Serviceable Material (USM) components to optimize maintenance costs and improve operational efficiency. With rising fuel prices and cost pressures, carriers seek affordable alternatives to OEM spare parts without compromising safety or reliability. Persistent margin pressure drives airlines to PMA components that cost 20-40% less than OEM equivalents while meeting FAA-EASA certification.[4]PMA Parts Update: The Industry Is Still Booming,” Aviation Maintenance Magazine, avm-mag.com USM uptake accelerates as teardowns of A320ceo and B737-NG families create inventory funnels. Although some lessors and flagship carriers restrict PMA use on core assets, streamlined FAA approval cuts lead times, and blockchain traceability removes authenticity doubts, encouraging broader deployment. PMA parts provide certified quality at lower prices, while USM offers sustainable value by extending part life cycles. This shift toward cost-effective solutions transforms procurement strategies across the aviation industry, accelerating demand for non-OEM spare parts and reinforcing their role as a critical growth driver in the global aircraft spare parts market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain disruptions and raw-material shortages | -0.8% | Global; acute in Asia-Pacific hubs | Short term (≤2 years) |

| Skilled labor shortages in certified technicians | -0.6% | North America and EU; emerging in Asia-Pacific | Long term (≥4 years) |

| Counterfeit-part proliferation raising certification costs | -0.5% | Global; felt most by US and European OEMs | Short term (≤2 years) |

| Regulatory limits on additive-manufactured critical parts | -0.4% | Global; stricter among tier-1 carriers and lessors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-chain disruptions and raw-material shortages

The aircraft spare parts market faces significant challenges due to ongoing supply-chain disruptions and shortages of critical raw materials. Global supply networks have been under pressure from geopolitical tensions, trade restrictions, and logistical bottlenecks, which have slowed the availability of essential components such as engines, avionics, and structural materials. At the same time, shortages of key raw materials like titanium, aluminum, and composites widely used in aircraft manufacturing have further escalated production costs and lead times. These constraints hinder the ability of both OEMs and aftermarket suppliers to meet rising demand from airlines and MRO providers. For operators, longer delivery schedules and inflated procurement costs disrupt planned maintenance cycles, forcing airlines to keep older aircraft in service for extended periods or source alternative components. This increases operational risks and pressures profitability, particularly for cost-sensitive carriers. While some manufacturers and suppliers are diversifying sourcing strategies and building localized inventories, recovery remains gradual. Persistent disruptions threaten the timely supply of high-quality spare parts, potentially limiting overall market growth. As a result, supply-chain instability and raw-material scarcity stand out as critical restraints, shaping both short-term performance and long-term planning in the aircraft spare parts industry.

Skilled labor shortages in certified technicians

The aircraft spare parts market is increasingly constrained by the shortage of skilled and certified aviation technicians, particularly in MRO operations. As fleets expand and ageing aircraft require more frequent servicing, the demand for qualified personnel to install, inspect, and certify spare parts has surged. However, the industry faces a growing talent gap due to an ageing workforce, limited new entrants, and the long training cycles required to meet international aviation standards. This shortage directly affects turnaround times for aircraft maintenance, often leading to longer groundings and higher operating costs for airlines. Delays in part installation and certification can disrupt maintenance schedules, causing inefficiencies across global supply chains. Smaller airlines and independent MRO providers are especially vulnerable, as they struggle to compete with larger players offering higher wages and better incentives to retain talent. Moreover, as new technologies such as advanced avionics and composite materials become more widespread, the skills gap widens, demanding more specialized training. Without adequate technical expertise, the availability of spare parts alone cannot ensure smooth operations. Thus, the shortage of certified technicians poses a severe restraint, limiting the effective utilization of spare parts and constraining overall market growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component Type: Engine Components anchor revenue leadership

Engine components contributed 35.25% to the aircraft spare parts market size in 2024. Titanium-rich fan blades and compressor parts dominate spending because durability upgrades lengthen the time on the wing, but raise replacement costs when limits are reached. Over 2025-2030, avionics and electrical instruments are set for the quickest 7.22% CAGR as semiconductor content in fly-by-wire and satellite-communication suites expands amid cabin-connectivity upgrades.

Engine components represent the largest revenue-generating segment in the aircraft spare parts market, owing to their critical role in ensuring safety, performance, and regulatory compliance. Engines are highly complex systems with the highest frequency of maintenance and replacement cycles, driving consistent demand for spare parts. Due to their cost intensity and operational importance, airlines and MRO providers prioritize investment in engine-related components such as turbines, compressors, and fuel systems. With increasing fleet utilisation and ageing aircraft, the engine components segment continues to anchor market growth, reinforcing its position as the dominant revenue contributor.

By Aircraft Platform: Widebodies lead value; narrowbodies accelerate growth

Widebody aircraft held 42.75% of 2024 revenue as complex long-haul systems require pricier engines, avionics, and structural assemblies. Yet narrowbody platforms will grow fastest at 8.83% CAGR because airlines stretch existing A320 and B737 fleets to absorb travel recovery, magnifying engine demand, landing gear, and cabin retrofits. Widebody aircraft account for the most considerable market value in spare parts demand, driven by their long-haul operations, larger component size, and higher maintenance complexity. These platforms require significant engine investments, landing gear, and structural parts, anchoring revenue leadership.

However, narrowbody aircraft are experiencing faster growth, supported by rising short-to-medium haul travel, fleet expansion, and low-cost carrier (LCC) penetration. Their higher flight frequencies lead to accelerated wear and tear, boosting demand for parts replacement and MRO services. Wide and narrowbody platforms create complementary growth dynamics in the global aircraft spare parts market. Regional jets and turboprops carve distinct requirements—propeller systems, short-field brakes, and lower-pressure cabin parts, particularly in emerging markets that expand secondary routes. ICAO forecasts support a diversified fleet composition, ensuring each platform maintains specialized parts pipelines through 2030.

By Part Type: OEM anchors market leadership with certified reliability

Original Equipment Manufacturer (OEM) parts commanded the largest 2024 share at 45.21%, underscoring their central role in the aircraft spare parts market. Airlines and MRO providers prioritize OEM components for their unmatched regulatory compliance, integration compatibility, and warranty-backed reliability across engines, avionics, and structural assemblies. OEM dominance is reinforced by exclusive supplier agreements, bundled service contracts, and strong aftermarket support networks, ensuring long-term revenue stability. High-value parts such as landing gear, turbines, and flight-control systems remain OEM-driven due to stringent safety protocols. This entrenched reliance positions OEMs as the backbone of aviation maintenance, even as operators explore cost-efficient alternatives.

Parts Manufacturer Approval (PMA) components are expected to expand rapidly, projected to grow at a 7.80% CAGR between 2025 and 2030. Airlines and independent MROs increasingly adopt PMA parts to offset high maintenance costs and reduce reliance on OEM supply chains. Their FAA-certified quality and proven performance in non-critical systems such as cabin interiors, lighting, and specific engine accessories are strengthening market acceptance. Cost efficiency, faster availability, and supply resilience position PMA as a compelling aftermarket solution, particularly as global fleets expand. Growing confidence in PMA reliability ensures its role as the spare parts market’s fastest-rising sub-segment.

By End User: OEM dominance faces agile independent challenge

Original Equipment Manufacturers (OEMs) dominate the aircraft spare parts market due to their brand credibility, regulatory approvals, and ability to provide high-quality certified components. Their strong integration with aircraft production and long-standing airline contracts further reinforces leadership. OEM distribution channels accounted for 55.32% of 2024 revenue, strengthened by proprietary manuals, warranty leverage, and exclusive engineering data.

Independent MROs, however, are pacing a 7.91% CAGR through 2030, propelled by PMA and USM cost advantages that appeal to cash-constrained airlines. Airlines juggle OEM reliability against rising costs, increasingly adopting a dual-sourcing policy in which non-critical components shift to independents. At the same time, power-by-the-hour contracts cover engines and avionics. Blockchain marketplaces lower search and authentication friction, tipping bargaining power toward buyers able to compare suppliers in real time.[5]Honeywell GoDirect Trade Surpasses $2 Billion,” Honeywell, honeywell.com However, independent distributors and MRO providers are increasingly challenging this dominance by offering faster turnaround times, cost-effective alternatives such as PMA and USM parts, and greater flexibility in sourcing. This agile approach appeals to airlines seeking efficiency and cost savings, gradually reshaping competitive dynamics in the aftermarket. As demand intensifies, OEM and independent players continue to redefine market balance.

Geography Analysis

North America retained the largest 38.22% slice of the aircraft spare parts market in 2024, buoyed by the world’s biggest commercial fleet, high utilization, and dense MRO infrastructure stretching from Seattle to Miami.[6]US Imports from Germany 2017-2024,” GTAIC, gtaic.ai Proximity to Boeing and a rich tier-1 supplier base compresses lead times and freight costs, reinforcing the region’s import heft, USD 163 billion from Germany in 2024 alone. FAA standards often set the compliance baseline globally, funneling demand for traceable, overhauled parts.

Asia-Pacific is the fastest-growing region at a 7.23% CAGR, fueled by double-digit traffic in China and India, rising LCCs, and fresh MRO capacity in Singapore, Indonesia, and China’s Greater Bay Area. Localized overhaul capability and resumed Boeing deliveries to Chinese airlines amplify the demand for narrowbody engine pieces, avionics modules, and cabin spares.

Europe, the Middle East, and Africa combine mature fleets with hub-focused utilization, elevating widebody spare-parts intensity. European carriers gain from Airbus proximity, while Middle Eastern hubs sustain 16-plus-hour flight legs that accelerate engine overhaul cycles. Over time, Asia-Pacific’s acceleration narrows the gap, yet North American maturity continues to anchor global demand through stable replacement cycles.

Competitive Landscape

Moderate consolidation defines the aircraft spare parts industry. Parker-Hannifin’s USD 7.2 billion Meggitt buyout enlarged aftermarket access across actuation and fluid-control product lines, highlighting supplier pursuit of higher-margin service revenues. OEMs guard data rights to preserve market command but face mounting share erosion as PMA-ready independents and teardown specialists monetize alternative channels. Digital disruption intensifies rivalry. Honeywell’s GoDirect Trade eclipsed USD 2 billion in transactions by 2025, signalling broad acceptance of blockchain-verified marketplaces that bypass legacy distributors. Predictive-maintenance platforms that couple sensor telemetry with AI parts forecasting create fresh battlegrounds, rewarding firms capable of blending hardware heritage with software insight. Barriers remain steep, FAA Parts Manufacturer Approval and EASA Part-21 rules shape certification timelines, but nimble entrants exploit inventory agility and price flexibility. Combined with airlines’ cost-down imperatives, these forces nurture a competitive equilibrium where neither OEMs nor independents achieve unassailable dominance.

Aircraft Spare Parts Industry Leaders

Honeywell International Inc.

The Boeing Company

TransDigm Group Incorporated

Safran SA

Liebherr Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Parker-Hannifin Corporation completed the acquisition of Meggitt, integrating its aerospace components and sensors business. This move is expected to boost Parker’s combined aerospace systems revenue above USD 4.3 billion and strengthen its global distribution reach.

- September 2025: Safran announced its intention to divest its aircraft interiors business, including overhead bins and galleys, to focus more on core high-margin areas like engines and avionics.

- August 2025: Montana Aerospace acquired Asco Industries, consolidating its structural parts manufacturing footprint across Europe and North America.

- August 2025: Spirit AeroSystems expanded in the aftermarket segment by acquiring Bombardier’s aerostructures business, increasing its spare parts and component capabilities.

- August 2025: Hanwha Aerospace expanded via acquisitions in avionics and hydraulics, strengthening its parts and systems capabilities for aerospace applications.

Global Aircraft Spare Parts Market Report Scope

| Engine Components |

| Avionics and Electrical instruments |

| Airframe Structures and Control-Surface Parts |

| Landing Gear |

| Wheels and Brakes |

| Auxiliary Power Units (APUs) |

| Hydraulic and Pneumatics Systems |

| Cabin and Interior Systems |

| Others |

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Aircraft |

| Turboprops |

| Original Equipment Manufacturer (OEM) Parts |

| Parts Manufacturer Approval (PMA) Parts |

| Used Serviceable Material (USM) Parts |

| Airlines |

| MROs |

| OEMs |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component Type | Engine Components | ||

| Avionics and Electrical instruments | |||

| Airframe Structures and Control-Surface Parts | |||

| Landing Gear | |||

| Wheels and Brakes | |||

| Auxiliary Power Units (APUs) | |||

| Hydraulic and Pneumatics Systems | |||

| Cabin and Interior Systems | |||

| Others | |||

| By Aircraft Platform | Narrowbody Aircraft | ||

| Widebody Aircraft | |||

| Regional Aircraft | |||

| Turboprops | |||

| By Part Type | Original Equipment Manufacturer (OEM) Parts | ||

| Parts Manufacturer Approval (PMA) Parts | |||

| Used Serviceable Material (USM) Parts | |||

| By End User | Airlines | ||

| MROs | |||

| OEMs | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the aircraft spare parts market in 2025?

The aircraft spare parts market size reached USD 50.52 billion in 2025.

What CAGR is forecast for aircraft spare parts through 2030?

A 6.79% CAGR is projected for 2025-2030, lifting value to USD 70.16 billion.

Which component category drives the most revenue?

Engine components led with 35.25% of 2024 revenue due to high unit cost and replacement frequency.

Which aircraft platform will grow fastest?

Narrowbody aircraft spare parts spending is set to expand at an 8.83% CAGR through 2030.

Which region offers the strongest growth prospects?

Asia-Pacific is expected to record a 7.23% CAGR, outpacing all other regions.

How are airlines cutting spare-parts costs?

Carriers increasingly deploy PMA and USM alternatives that deliver 20-40% savings while meeting FAA-EASA certification.

Page last updated on: