Europe Aircraft Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 60.20 Billion |

| Market Size (2030) | USD 78.03 Billion |

| Growth Rate (2025 - 2030) | 5.32% CAGR |

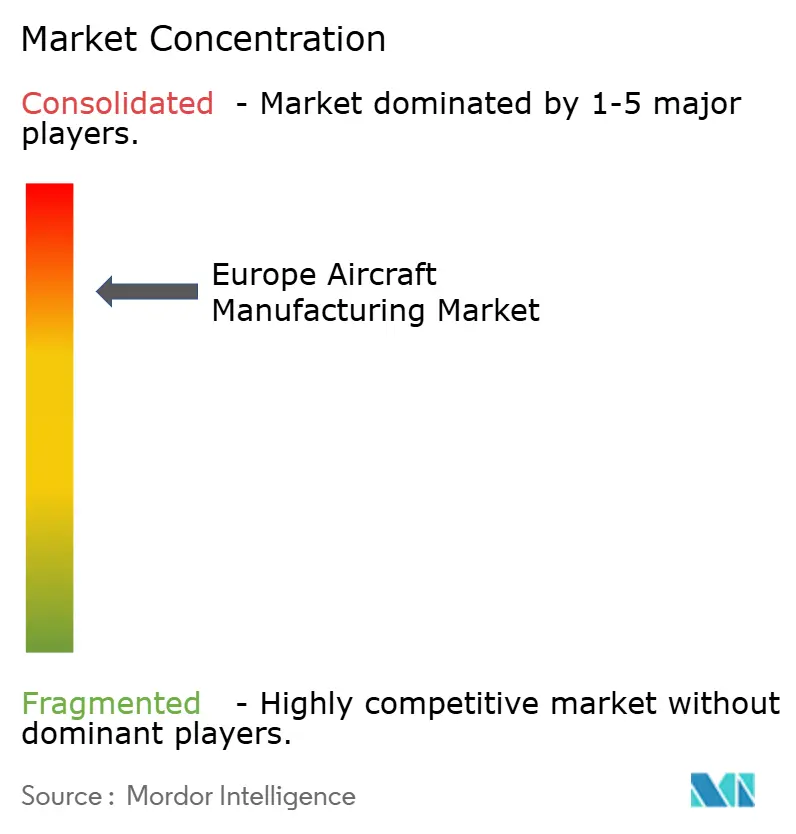

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Aircraft Manufacturing Market Analysis by Mordor Intelligence

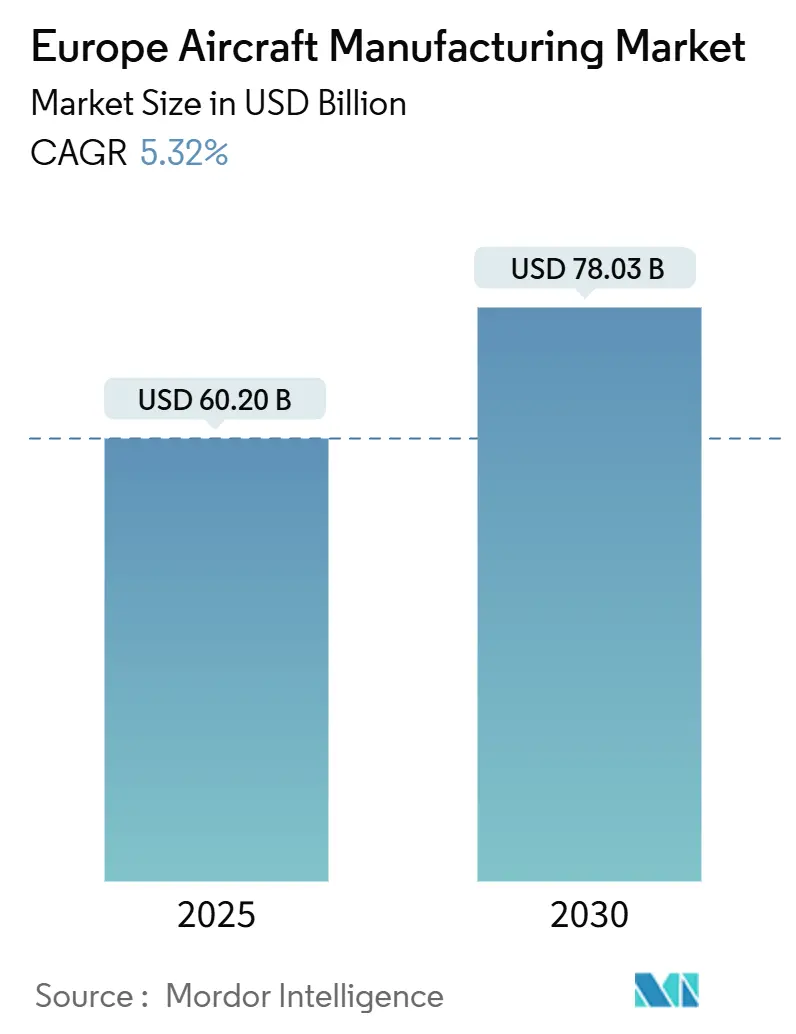

The Europe aircraft manufacturing market size reached USD 60.20 billion in 2025 and is projected to register USD 78.03 billion by 2030, advancing at a 5.32% CAGR. The region’s robust performance reflects a balanced recovery in commercial aviation and steadily rising defense procurement, underpinned by strategic investments in sustainable propulsion technologies. Fleet renewals among low-cost carriers (LCCs), expansion of hydrogen-propulsion demonstration programs, and government incentives for sustainable aviation fuel (SAF) collectively reinforce demand momentum. Concurrently, supply-chain vulnerabilities around aerospace-grade titanium and heightened certification costs temper near-term capacity ramps, compelling manufacturers to diversify sourcing and adopt digital-twin tools for faster prototype validation. Competitive intensity centers on technological leadership, with five dominant players prioritizing hydrogen readiness, advanced composites, and data-driven manufacturing to strengthen market positioning.

Key Report Takeaways

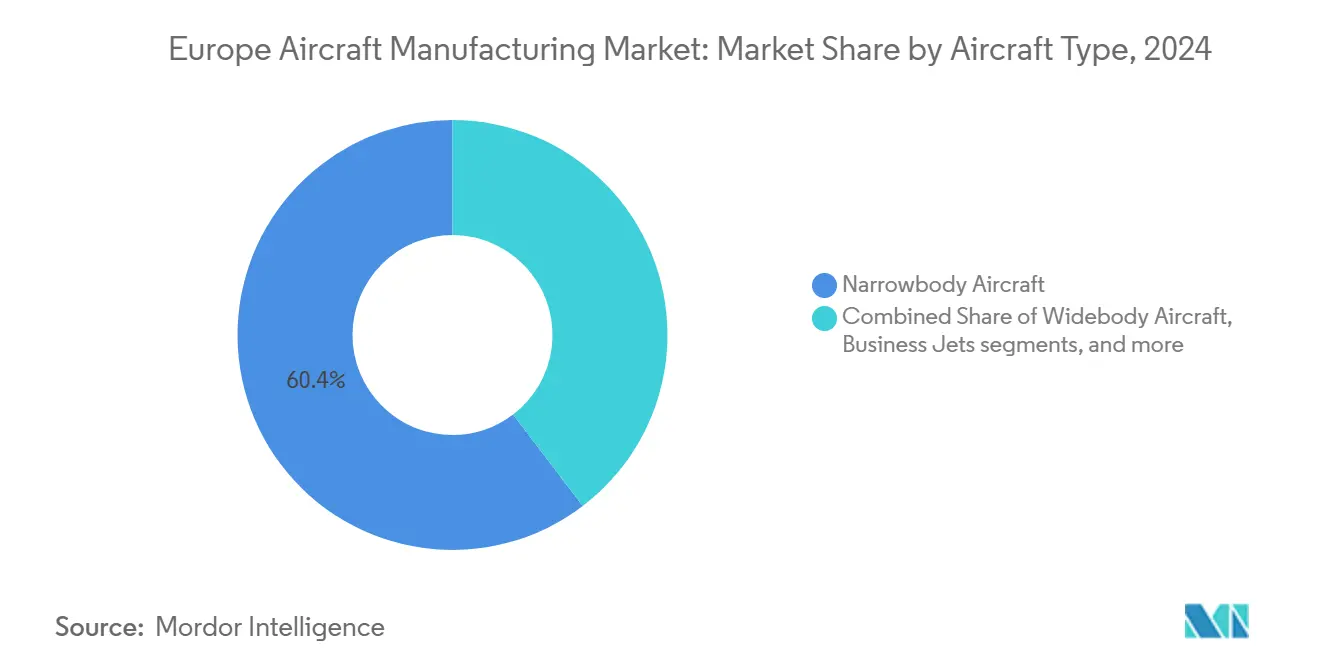

- By aircraft type, narrowbody platforms led with 60.36% of the European aircraft manufacturing market share in 2024, while business jets are forecasted to expand at a 6.37% CAGR through 2030.

- By application, commercial passenger transport commanded a 62.76% share of the European aircraft manufacturing market in 2024, whereas business/private aviation is advancing at a 7.47% CAGR to 2030.

- By propulsion technology, conventional jet-fuel and SAF-ready aircraft held 70.27% of the European aircraft manufacturing market share in 2024; hydrogen-propulsion airframes show the highest projected CAGR at 8.23% until 2030.

- By geography, the United Kingdom (UK) accounted for 39.41% of Europe's aircraft manufacturing market size in 2024, while Germany recorded the fastest expansion at a 6.91% CAGR through 2030.

Global valuation is built by aggregating outputs from multiple regions, with Europe forming one of the important contributors. Mordor Intelligence's global aircraft manufacturing market size report represents that cumulative total.

Europe Aircraft Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in commercial passenger traffic within Europe | +1.10% | Pan-European; Western Europe leadership | Short term (≤ 2 years) |

| EU Green Deal incentives for low-emission manufacturing | +0.90% | EU-wide; Nordic and German focus | Medium term (2-4 years) |

| Defense funding surge for next-gen fighter programs | +1.30% | UK, France, Italy, Germany, Spain | Long term (≥ 4 years) |

| Fleet renewal to fuel-efficient aircraft | +1.00% | UK, Germany, France | Medium term (2-4 years) |

| Horizontal supply-chain integration via digital twins | +0.80% | Germany, France, UK hubs | Short term (≤ 2 years) |

| Scaling Sustainable Aviation Fuel (SAF) production agreements | +0.70% | Netherlands, Germany, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Commercial Passenger Traffic Within Europe

European passenger volumes climbed 12% in 2024, returning to 95% of pre-pandemic levels as intra-European routes led the rebound. Low-cost carriers captured 42% of that growth, highlighted by Ryanair’s 300 B737 MAX-10 orders and easyJet’s expanding A321neo fleet, which amplifies demand for narrow-body output.[1]Reuters, “Ryanair orders 300 Boeing 737 MAX-10 jets worth USD 40 billion,” reuters.com Higher aircraft utilization accelerates replacement cycles, pushing OEM production lines toward maximum capacity. Component suppliers now report order backlogs stretching 18 months, underscoring tight supply conditions across the value chain. Airport operators are investing EUR 15 billion (USD 17.70 billion) in terminal and runway upgrades to accommodate traffic increases, further boosting ancillary demand for specialized short-haul variants.

EU Green Deal Incentives for Low-Emission Manufacturing

The EU committed EUR 8.2 billion (USD 9.68 billion) in 2024 to aerospace decarbonization, subsidizing hydrogen propulsion R&D, SAF infrastructure, and low-carbon manufacturing processes.[2]European Commission, “ReFuelEU Aviation: sustainable aviation fuels for Europe,” ec.europa.eu Germany leads with EUR 1.2 billion (USD 1.42 billion) in co-funding, while France offers EUR 800 million (USD 944.2 billion) tax breaks to adopters of carbon-neutral production lines. Carbon-border adjustments shield compliant European OEMs from competitors with weaker environmental standards, delivering an estimated 8-12% cost edge by 2027. Denmark and the Netherlands mandate 10% SAF blending by 2030, prompting rapid retrofits for fuel-system compatibility. Circular-economy clauses covering end-of-life recycling further differentiate European aircraft on sustainability grounds.

Defense Funding Surge for Next-Gen Fighter Programs

European defense outlays reached EUR 240 billion (USD 283.26 billion) in 2024, with aircraft procurement absorbing 18% of that spend as NATO states modernize fleets. The UK’s GBP 75 billion (USD 101.36 billion) GCAP/Tempest program, Italy’s EUR 7 billion (USD 8.26 billion) F-35 expansion, and France’s EUR 4.5 billion (USD 5.31 billion) Rafale upgrades headline multi-decade pipelines. Spain’s Eurofighter orders and Germany’s Tornado replacement bring cumulative aircraft-program value above EUR 150 billion (USD 177.04 billion) through 2040. These projects cultivate European sovereignty in advanced materials, AI-enabled mission systems, and directed-energy technologies. The GCAP initiative adds 25,000 skilled engineering jobs, reinforcing the talent base required for sixth-generation platforms.

Fleet Renewal to Fuel-Efficient Aircraft

Fuel costs represented 28% of airline operating expenses in 2024, intensifying the push toward jets offering 15-20% efficiency gains. Lufthansa’s EUR 12 billion (USD 14.16 billion) orders, Air France-KLM’s A350 expansion, and British Airways’ B787 deliveries exemplify Europe-wide adoption of new-generation models. Airlines increasingly assess the total cost of ownership, favoring airframes equipped with predictive-maintenance software and longer service intervals. OEMs with robust aftermarket networks secure a competitive advantage by minimizing downtime and lifecycle expense. Noise-abatement rules at slot-constrained hubs further elevate demand for quieter engines and refined aerodynamics.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain disruptions for critical raw materials | −0.7% | Global supply; EU production | Short term (≤ 2 years) |

| Certification delays due to EASA stringency | −0.5% | EU-wide compliance | Medium term (2-4 years) |

| Skilled-labor shortages in composite fabrication hubs | −0.6% | Germany, UK, France | Medium term (2-4 years) |

| Capital intensity and inflationary pressure on tooling and facilities | −0.4% | Pan-European sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Disruptions for Critical Raw Materials

Russian titanium exports fell 65% in 2024, forcing European OEMs to procure from Japan and the US at 45-60% higher prices. Simultaneously, Chinese carbon-fiber suppliers redirected 25% of output to domestic wind-energy projects, extending aircraft lead times to six months. Rare-earth shortages jeopardize avionics production, prompting strategic alliances with Australian and Canadian miners. Wide-body programs—where titanium constitutes 15% of structural weight—face the sharpest cost inflation. Manufacturers invest EUR 3.2 billion (USD 3.78 billion) in vertical integration, recycling, and alloy substitution strategies to mitigate risk.

Certification Delays Due to EASA Stringency

EASA’s enhanced oversight protocols lengthened average certification cycles by 18 months in 2024, with cybersecurity validation alone adding up to a year for software-rich platforms. Hybrid-electric and hydrogen concepts encounter additional scrutiny as the agency drafts new airworthiness codes, potentially postponing market entry. Compliance costs rose EUR 15-25 million (USD 17.7-29.51 million) per program, burdening smaller OEMs dependent on external consultants. Companies now earmark EUR 500 million (USD 590.13 million) annually for regulatory affairs infrastructure, including dedicated simulation labs. While delays constrain revenue timing, rigorous standards uphold global confidence in European air-safety leadership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Business Jets Drive Premium Growth

Narrowbody aircraft retained 60.36% share of the European aircraft manufacturing market in 2024, reflecting strong post-pandemic fleet renewals, yet business jets captured investor attention with a 6.37% CAGR, signaling premium-travel resilience. Shorter-haul mission profiles align with point-to-point corporate mobility, where cabin pressurization, Wi-Fi, and health-centric filtration boost perceived value. Fleet operators increasingly select SAF-ready engines to comply with corporate ESG mandates, supporting Dassault Aviation’s Falcon 6X, which achieved 95% acceptance among European charter firms.[3]Dassault Aviation, “Falcon 6X achieves EASA certification,” dassaultfalcon.com The shift elevates cabin-system suppliers who integrate biometric access, predictive maintenance, and real-time emissions tracking. Meanwhile, wide-body production lags as intercontinental travel normalizes gradually, directing engineering resources toward hydrogen-ready demonstrators. Turboprops enjoy demand from island and Arctic routes, but volume remains modest, underscoring the European aircraft manufacturing market’s pivot to flexible, mission-optimized airframes. OEMs expand after-sales packages, offering power-by-the-hour contracts to mitigate maintenance-cost uncertainties, further cementing brand loyalty.

By Application: Business Aviation Accelerates Beyond Commercial Recovery

Commercial passenger transport accounted for 62.76% of the European aircraft manufacturing market size in 2024, benefiting from restored leisure travel and route reopenings. Nonetheless, business/private aviation leads growth at 7.47% CAGR as corporations emphasize time efficiency and health security. Aircraft management companies report record fractional-ownership inquiries, signaling sustainable demand rather than pandemic-driven anomalies.

Cargo conversions gain traction as e-commerce volumes remain elevated, driving appetite for the B737 and A321 freighter programs. Special-mission versions, including maritime patrol and border-security aircraft, secure stable government funding. The regulatory environment tightens around noise and emissions, encouraging upgrades to quieter engines and lightweight interiors. Consequently, OEMs position flexible cabin-conversion kits to address seasonal demand swings, reinforcing the European aircraft manufacturing market’s adaptability across user segments.

By Propulsion Technology: Hydrogen Propulsion Leads Innovation Wave

Conventional jet-fuel and SAF-ready aircraft still command 70.27% of the European aircraft manufacturing market; however, hydrogen-propulsion designs register the fastest 8.23% CAGR through 2030. Hybrid-electric concepts serve as technological bridges, especially for sub-500 nm routes where battery density suffices for partial power. Amsterdam Schiphol and Munich airports pilot liquid-hydrogen supply chains, setting industry benchmarks for refueling-time parity with kerosene operations.

Regulators publish draft requirements covering leak detection and cryo-tank crashworthiness, offering clarity that unlocks private investment. Tier-1 suppliers co-develop modular fuel-cell stacks compatible with regional aircraft and future urban air mobility (UAM) platforms. Supply-chain realignment attracts automotive hydrogen specialists, blending new competencies into the European aircraft manufacturing industry, which gains a reputational first-mover edge on decarbonization.

Geography Analysis

The UK anchors regional leadership with a 39.41% market share, supported by BAE Systems' Typhoon production line, Rolls-Royce's propulsion innovations, and the GCAP/Tempest fighter roadmap that extends order visibility into the next decade. Employment surpassed 111,000 in 2024 and benefits from government grants targeting net-zero aviation research. Currency stability and robust export-credit backing further bolster UK competitiveness, even as Brexit necessitates customs-compliance overhead for EU deliveries.

Germany follows with the region's fastest CAGR at 6.91%, driven by strong public-private collaboration on hydrogen propulsion and battery-electric subsystems. MTU Aero Engines' hydrogen test facility and Lufthansa Technik's zero-emission maintenance capabilities exemplify Germany's strategic positioning. The country's automotive heritage facilitates cross-pollination in electronics, lightweighting, and scalable production, deepening supply-chain integration within the European aircraft manufacturing market.

France sustains pivotal influence through Airbus' final assembly in Toulouse, Dassault's Falcon series, and Thales avionics. Italy reinforces market breadth via Leonardo's AW139 and AW189 helicopters, while Spain specializes in composite wing structures for Airbus narrow-body programs. Smaller hubs in the Netherlands and Switzerland offer niche competencies in precision machining and system certification, underscoring Europe's aerospace ecosystem's distributed yet cohesive nature.

Coverage of the aircraft manufacturing market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for North America and Asia.

Competitive Landscape

Five principal manufacturers—Airbus SE, Dassault Aviation, Leonardo S.p.A., Avions de Transport Régional GIE (ATR), and United Aircraft Corporation (ROSTEC)—dominate output, enabling scale efficiencies and sustained R&D investments. Airbus leverages integrated supply chains to maintain narrow-body leadership, targeting 75 A320neo monthly deliveries by 2026. Dassault secures premium pricing through cabin customization and long-range performance, exemplified by its newly certified Falcon 6X. Leonardo capitalizes on helicopter demand across civil and parapublic missions, combining airframe production with mission-system integration.

Strategic collaborations proliferate as complexity rises; the GCAP partnership unites the UK, Italy, and Japan to share sixth-generation fighter R&D risk. Hydrogen propulsion accelerates alliance formation between aerospace OEMs and energy majors, pooling expertise in fuel infrastructure. Digital-twin ecosystems engage software firms and additive-manufacturing start-ups, compressing design cycles and enabling predictive maintenance.

Regulatory acumen forms a decisive barrier for non-European entrants. EASA's stringent cybersecurity and environmental standards favor incumbents familiar with procedural rigor. Nevertheless, white-space opportunities attract venture-backed disruptors in UAM and high-altitude drones, intensifying the European aircraft manufacturing market's innovation.

Europe Aircraft Manufacturing Industry Leaders

Airbus SE

Avions de Transport Régional GIE (ATR)

Leonardo S.p.A.

Dassault Aviation SA

United Aircraft Corporation (ROSTEC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Leonardo received a EUR 165 million (USD 193.78 million) contract extension from the British government to maintain the Royal Navy's fleet of 54 Merlin helicopters. This development reflects the UK's increased defense spending initiatives.

- June 2025: Saab and the French defense procurement agency signed a joint declaration of intent to acquire Saab's GlobalEye Early Warning and Control (AEW&C) aircraft, ground equipment, training, and support.

Europe Aircraft Manufacturing Market Report Scope

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Turboprop Aircraft |

| Business Jets |

| Helicopters |

| Amphibious Aircraft |

| Commercial Passenger |

| Cargo/Freight |

| Military and Defense |

| Business/Private Aviation |

| Special Mission (Surveillance, Emergency) |

| Conventional Jet-Fuel Aircraft/SAF-Ready Aircraft |

| Hybrid-Electric Aircraft |

| Hydrogen-Propulsion Aircraft |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Switzerland |

| Rest of Europe |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| Turboprop Aircraft | |

| Business Jets | |

| Helicopters | |

| Amphibious Aircraft | |

| By Application | Commercial Passenger |

| Cargo/Freight | |

| Military and Defense | |

| Business/Private Aviation | |

| Special Mission (Surveillance, Emergency) | |

| By Propulsion Technology | Conventional Jet-Fuel Aircraft/SAF-Ready Aircraft |

| Hybrid-Electric Aircraft | |

| Hydrogen-Propulsion Aircraft | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Switzerland | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe aircraft manufacturing market in 2025 and what is its projected CAGR through 2030?

The Europe aircraft manufacturing market stands at USD 60.20 billion in 2025 and is forecasted to reach USD 78.03 billion by 2030, reflecting a 5.32% CAGR.

Which aircraft type held the largest market share in 2024?

Narrowbody platforms led with 60.36% share, supported by fleet-renewal programs among the LCCs.

Which application segment is expanding the fastest?

Business/private aviation is advancing at a 7.47% CAGR as corporations favor point-to-point, time-efficient travel.

Which propulsion technology shows the highest growth rate?

Hydrogen-propulsion airframes register the fastest projected growth at an 8.23% CAGR, driven by Europe’s decarbonization goals.

Which country currently leads the market and which is growing the quickest?

The UK commanded 39.41% of regional output in 2024, while Germany records the fastest CAGR at 6.91% through 2030.

What are the main drivers behind market growth?

Fleet renewal for fuel efficiency, rising defense modernization budgets, and strong government incentives for sustainable aviation fuel and hydrogen technologies are key growth catalysts.

What major challenges could hinder production?

Supply-chain disruptions for aerospace-grade titanium, escalating EASA compliance costs, and skilled labor shortages in advanced composites remain significant headwinds.

Page last updated on: