Asia-Pacific Aircraft Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

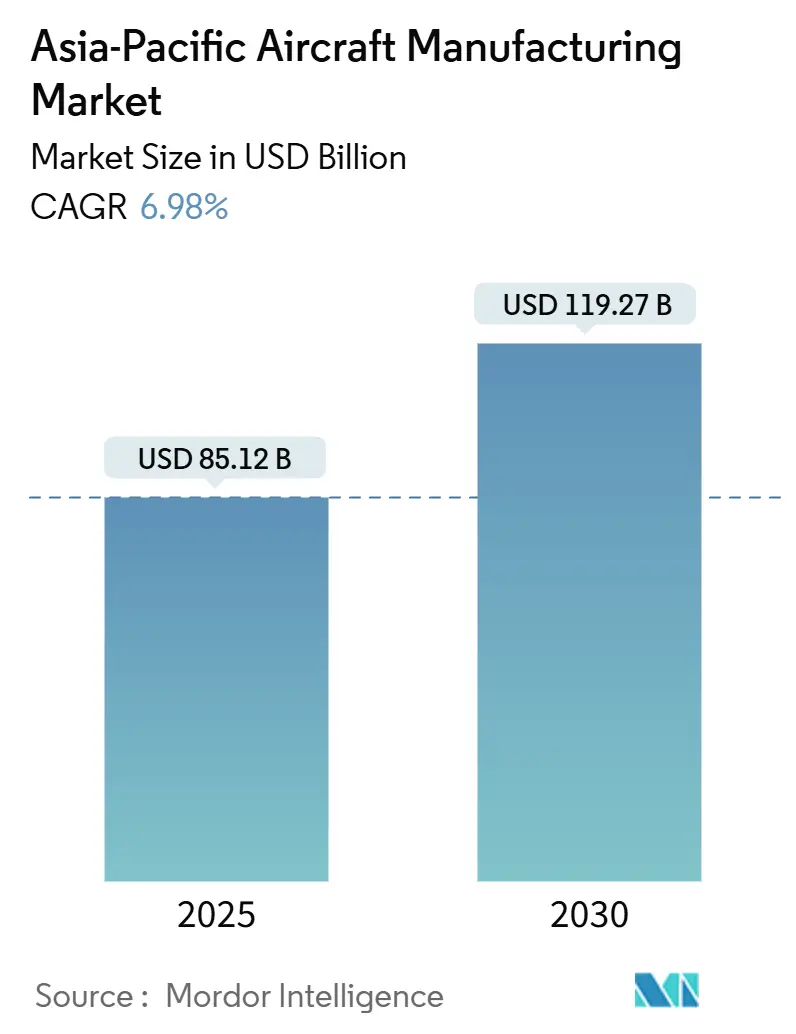

| Market Size (2025) | USD 85.12 Billion |

| Market Size (2030) | USD 119.27 Billion |

| Growth Rate (2025 - 2030) | 6.98% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Aircraft Manufacturing Market Analysis by Mordor Intelligence

The Asia-Pacific aircraft manufacturing market size equals USD 85.12 billion in 2025 and is forecast to reach USD 119.27 billion by 2030, reflecting a 6.98% CAGR. Expansion rests on surging domestic passenger volumes, accelerated fleet renewal by low-cost carriers (LCCs), and multibillion-dollar defense modernization programs. Supply-chain localization incentives across China, India, Japan, and South Korea cut reliance on imported sub-assemblies and encourage indigenous capability development. Strong demand for narrowbody jets and helicopters, coupled with early commitments to hydrogen propulsion, unlocks fresh production contracts. OEMs keep lead times competitive by co-locating final-assembly and MRO facilities near future growth nodes, cushioning the Asia-Pacific aircraft manufacturing market against external supply shocks.

Key Report Takeaways

- By aircraft type, narrowbodies led with 56.46% of the Asia-Pacific aircraft manufacturing market share in 2024, while helicopters delivered the fastest growth at an 8.65% CAGR through 2030.

- By application, commercial passenger platforms accounted for 59.36% of the Asia-Pacific aircraft manufacturing market size in 2024; military and defense solutions record a 7.32% CAGR to 2030.

- By propulsion technology, conventional jet-fuel and SAF-ready aircraft held 64.58% of the Asia-Pacific aircraft manufacturing market in 2024, whereas hydrogen-propelled models post an 8.58% CAGR forecast.

- By geography, China controlled 39.55% of the Asia-Pacific aircraft manufacturing market share in 2024, and India registered the steepest 7.21% CAGR through 2030.

Asia contributes to a system defined not by any single geography but by the interaction of many. The global aircraft manufacturing market data by Mordor Intelligence represents that combined structure.

Asia-Pacific Aircraft Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Description | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in domestic passenger traffic | +1.00% | China; India; Southeast Asia core markets | Medium term (2-4 years) |

| Fleet-renewal programs by LCC | +0.80% | India; Indonesia; Philippines | Short term (≤2 years) |

| Military modernization and indigenous fighter programs | +0.70% | China; India; South Korea; Japan; Australia | Long term (≥4 years) |

| Domestic supply-chain localization incentives | +0.60% | China; India; Japan; South Korea manufacturing hubs | Medium term (2-4 years) |

| Stricter regional carbon-tax frameworks accelerating next-gen production | +0.40% | China; Singapore; Japan | Long term (≥4 years) |

| Development of Asia-Pacific mega-hub airports driving widebody demand | +0.30% | Singapore; China; Thailand; Vietnam major hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth in Domestic Passenger Traffic

Domestic passenger volumes continue breaking records in China, India, and key Southeast Asian states. Every month, regional airlines unveil new point-to-point connections that stimulate first-time flyers and redirect demand from congested rail corridors. Airports in Tier-2 and Tier-3 cities are expanding runways and terminal capacity, allowing carriers to up-gauge fleets from turboprops to narrowbodies. Leasing companies funnel additional A320neo and B737-MAX variants into the pool, confident that high load factors will sustain lease yields.[1]Asian Aviation Staff, “Cathay Pacific orders 14 Boeing 777-9s,” Asian Aviation, asianaviation.com Manufacturers benefit through firm multi-year order books and the pull-through of related component contracts. Supply-chain actors downstream gain dependable volume that justifies investment in local machining centers and avionics integration lines.

Fleet-Renewal Programs by Low-Cost Carriers

Asia-Pacific LCCs wage a cost-per-seat battle on fuel efficiency and dispatch reliability. Operators such as Vietjet, AirAsia, and IndiGo have lined up bulk deliveries over the rest of the decade, locking in favorable pricing and escalation clauses. The resulting production tempo secures hundreds of supplier jobs, while flexibility clauses let airlines swap models to meet seasonal demand shocks. Regional factories see predictable slot visibility, enabling better capacity utilization of autoclave, wing box, and fuselage sections. Leasing syndicates underwrite many of these deals, spreading residual risk across global investor bases. Aggregate output scales further as secondary market aircraft head to freighter conversion lines rather than early retirement.

Military Modernization and Indigenous Fighter Programs

Defense budgets keep rising as regional governments respond to territorial disputes and maritime security gaps. South Korea’s KF-21 advances flight-test milestones on schedule, drawing dozens of Korean SMEs into the qualified supplier list. China fields additional J-20 production lots at Chengdu, while India’s HAL accelerates Tejas Mk-II assembly. Helicopter modernization mirrors fighter investments; the Philippines is set to operate 47 S-70i Black Hawks by 2026.[2]Lockheed Martin Corporation, “Lockheed Martin Delivers S-70i Black Hawk Helicopters to the Philippines,” lockheedmartin.com Each contract seeds long-term spares and training demand. Knowledge transfers in composite structures, fly-by-wire systems, and low-observable coatings spill into civil programs, narrowing the technology gap with Western OEMs.

Domestic Supply-Chain Localization Incentives

Governments layer tax rebates, land grants, and offset credits onto aerospace investment packages. India approves 100% foreign direct investment in MRO while stipulating minimum local content thresholds. China offers accelerated depreciation on new five-axis machine tools, making it economical for suppliers to copy-exact their European lines. Japan funds R&D for high-temperature alloys and additive manufacturing pilots to capture engine hot-section work shares. These incentives steadily build a tiered supplier ecosystem that lifts regional resilience and reduces import bill exposure.

Restraints Impact Analysis*

| Description | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and long pay-back period | -1.30% | Global (especially new entrants and smaller players) | Long term (≥4 years) |

| Certification and export-control complexity | -1.00% | China; India; emerging manufacturers | Medium term (2-4 years) |

| Chronic aero-engine supply bottlenecks | -0.80% | Global supply chain | Short term (≤2 years) |

| Shortage of experienced aerospace manufacturing engineers | -0.60% | Australia; Singapore; emerging manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex and Long Pay-Back Period

Establishing a clean-sheet aircraft program can require well above USD 10 billion over a decade before positive cash flow starts. Even retrofit lines for popular widebodies call for nine-figure investments in jigs, tooling, and flight-test instrumentation. Smaller entrants struggle to finance such sums without sovereign backing or anchor customer guarantees. Interest-rate volatility forces developers to hedge exposure, adding cost layers. Therefore, the Asia-Pacific aircraft manufacturing market leans toward risk-sharing partnerships where multiple stakeholders absorb capital outlays in return for future royalties or guaranteed production slots.

Certification and Export-Control Complexity

Securing simultaneous validation from FAA, EASA, and CAAC introduces duplicative test campaigns that can stretch timelines by several years. COMAC’s C919 still awaits full European type certification, limiting sales beyond domestic carriers. Export-control regimes such as ITAR add paperwork layers for avionics or military-grade sensors, compelling suppliers to segregate production lines to protect controlled technologies. These administrative hurdles raise overhead and deter agile product iterations, slowing down cumulative delivery totals in the Asia-Pacific aircraft manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbodies Drive Volume, Helicopters Accelerate Growth

Narrowbody platforms anchored 56.46% of the Asia-Pacific aircraft manufacturing market share in 2024, equal to over 520 rolled-out units and slot commitments. Their dominance reflects airline economics that reward short-sector fuel efficiency, lower crew costs, and high utilization rates. Production sequencing across Tianjin, Nagpur, and Kuala Lumpur final-assembly lines keeps shipping costs minimal while bringing aftermarket support closer to operators. Helicopter programs enjoy the highest 8.65% CAGR, propelled by defense re-capitalization, offshore wind-farm logistics, and heightened demand for emergency medical services.[3]Leonardo S.p.A., “Leonardo and Weststar launch major government rotorcraft expansion,” leonardo.com

Strategically, OEMs co-develop modular avionics suites that migrate across rotorcraft, trainer, and light-transport variants, reducing non-recurring engineering costs. Framework agreements such as Leonardo’s 28-helicopter lease program in Malaysia illustrate how structured financing unlocks civil-government demand clusters while embedding future upgrade work. The Asia-Pacific aircraft manufacturing market size assigned to rotorcraft is forecasted to surpass USD 14 billion by 2030, enriching local Tier-2 metal-bond and composite lay-up shops. Narrowbody assembly, meanwhile, integrates quick-change freighter kits and future hydrogen-compatible wing boxes, ensuring product longevity across multiple mission profiles.

By Application: Commercial Leads, Defense Accelerates

Commercial passenger jets captured 59.36% of the Asia-Pacific aircraft manufacturing market in 2024, as rising middle-class incomes prioritize air travel convenience. Airlines bulk-purchased 240-plus single-aisles last year to replace aging A320ceo and B737NG fleets. Defense allocations are catching up, advancing at a 7.32% CAGR. Government planners finance multirole fighters, surveillance planes, and tactical lift helicopters that share production tooling with civil counterparts, smoothing learning curves for welders and composite technicians.

Cargo conversions remain another growth pocket. Retired passenger narrowbodies re-enter service as freighters amid booming e-commerce fulfillment volumes. Engineering centers in Singapore and Penang execute freighter door cut-outs and floor reinforcement, extending airframe life cycles by 15 years. Business aviation stays a niche but lucrative domain, with island nations ordering amphibious twins for tourism and medical evacuation. The overall mix helps the Asia-Pacific aircraft manufacturing market remain resilient against sector-specific downturns.

By Propulsion Technology: Conventional Dominates, Hydrogen Emerges

Conventional and SAF-compatible turbines will retain 64.58% of the Asia-Pacific aircraft manufacturing market size in 2024. OEM line stations produce higher-pressure-ratio cores and fan cases to meet ICAO Stage 5 emissions limits without radical airframe redesign. Yet hydrogen propulsion records the loftiest 8.58% CAGR as regional governments pledge net-zero frameworks. ITOCHU’s stake in ZeroAvia grants exclusive engine support rights across Japan, linking potential sales to airports committing to cryogenic refueling.[4]ITOCHU Corporation, “Investment in Hydrogen-Electric Engine Manufacturer ZeroAvia,” itochu.co.jp

Hybrid-electric demonstrators bridge the gap; Malaysia’s VoltAero partnership will serial-produce Cassio family aircraft, anchoring supply contracts for high-energy-density batteries and distributed-drive propulsors. Airbus and Toshiba explore superconducting motors cooled by liquid hydrogen to boost power-to-weight ratios, signaling cross-industry collaborations that redefine the propulsion value chain. The Asia-Pacific aircraft manufacturing market incubates these prototypes through public-private grants, ensuring local engineers master cryogenic sealing, thermal insulation, and high-frequency inverter technologies.

Geography Analysis

China’s manufacturing campuses stretch from Xi’an to Chengdu, each optimized for distinct work packages ranging from fuselage barrel spinning to carbon fiber prepreg lay-up. Government procurement quotas ensure predictable forward loads, allowing suppliers to amortize tooling quickly even as they re-qualify domestic alloys for critical usage. Export ambitions motivate dual-release certification processes, with joint FAA-CAAC audits embedded early to hasten foreign-sales compliance.

India’s cluster strategy centers on Bengaluru, Hyderabad, and Nagpur, where aerospace parks co-locate machining, surface treatment, and testing labs. Academic partnerships with IITs widen the engineering talent funnel, offsetting a regional skills shortage. Offset agreements linked to recent widebody orders mandate knowledge transfer on advanced assembly jigs, enlarged autoclaves, and robotic drilling cells. These steps ensure local readiness for direct workshare on future single-aisle and regional jet programs.

Japan and South Korea command high-value systems integration, focusing on flight-control computers, satellite-based navigation antennas, and de-icing systems. Their respective defense ministries bankroll R&D budgets that spin off civil applications, creating virtuous cycles of technology maturation. Australia underwrites a sovereign industrial base across avionics testing and engine MRO in Brisbane and Melbourne. At the same time, Singapore positions Seletar Aerospace Park as a bonded hub that slices customs delays for imported components. Emerging Southeast Asian economies channel infrastructure loans into runway extensions and hangar bays, wooing tier-three metal-forming firms looking to spread geopolitical risk.

The aircraft manufacturing market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for North America and Europe.

Competitive Landscape

The competitive field blends established Western OEM influence with rising Asian champions. Boeing and Airbus still provide design leadership, global leasing support, and aftermarket integration. Their strategic decision to assign a growing share of work packages to Asia-Pacific factories cements regional stickiness and creates win-win technology transfers. COMAC steps beyond domestic delivery quotas by marketing the C919 to African and Latin American carriers, aiming for a ten-year break-even on non-recurring costs.

AVIC and HAL invest in subsystem autonomy, recognizing that engine hot-sections and flight-control law software drive long-term economic moat. Korea Aerospace Industries leverages KF-21 learnings to pitch next-generation advanced trainers to ASEAN buyers, bundling commitment with comprehensive industrial participation schemes. Kawasaki Heavy Industries offers composite center wing boxes for the B787 and investigates hydrogen cryogenic tank manufacturing, enhancing specialization depth.

Joint ventures proliferate: Airbus-MTU hydrogen partnerships, AAR-Air France-KLM MRO expansion, and HAECO-COMAC service contracts underscore the trend toward risk-sharing rather than pure competition. Suppliers diversify customer portfolios, mitigating dependency by adopting common digital-thread standards that facilitate design-for-manufacture handoffs across OEM lines. Therefore, the Asia-Pacific aircraft manufacturing market transitions from contractor-subcontractor binaries to interlinked networks where intellectual property, tooling assets, and aftermarket royalties circulate fluidly.

Asia-Pacific Aircraft Manufacturing Industry Leaders

The Boeing Company

Airbus SE

Commercial Aircraft Corporation of China, Ltd. (COMAC)

Hindustan Aeronautics Limited (HAL)

Korea Aerospace Industries, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Qantas accepted the first A321XLR in Asia Pacific, inaugurating extended-range narrowbody services.

- August 2025: Cathay Pacific ordered 14 B777-9s to reinforce long-haul fleet depth.

- May 2025: Leonardo and Weststar launched a 28-helicopter Malaysian government program for multisector missions.

- January 2025: Tata and Airbus confirmed H125 production, creating India’s first private helicopter line.

Asia-Pacific Aircraft Manufacturing Market Report Scope

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

| Turboprop Aircraft |

| Business Jets |

| Helicopters |

| Amphibious Aircraft |

| Commercial Passenger |

| Cargo/Freight |

| Military and Defense |

| Business/Private Aviation |

| Special Mission (Surveillance, Emergency) |

| Conventional Jet-Fuel Aircraft/SAF-Ready Aircraft |

| Hybrid-Electric Aircraft |

| Hydrogen-Propulsion Aircraft |

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Indonesia |

| Singapore |

| Rest of Asia-Pacific |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| Turboprop Aircraft | |

| Business Jets | |

| Helicopters | |

| Amphibious Aircraft | |

| By Application | Commercial Passenger |

| Cargo/Freight | |

| Military and Defense | |

| Business/Private Aviation | |

| Special Mission (Surveillance, Emergency) | |

| By Propulsion Technology | Conventional Jet-Fuel Aircraft/SAF-Ready Aircraft |

| Hybrid-Electric Aircraft | |

| Hydrogen-Propulsion Aircraft | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Singapore | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the Asia-Pacific aircraft manufacturing market size in 2025 and its projected CAGR through 2030?

The sector is valued at USD 85.12 billion in 2025 and is expected to grow at a 6.98% CAGR to reach USD 119.27 billion by 2030.

Which aircraft category currently dominates regional production?

Narrowbody jets lead with 56.46% share of total deliveries in 2024, reflecting airlines’ focus on high-frequency point-to-point routes.

Which aircraft type is expanding the fastest over the forecast period?

Helicopter output shows the steepest momentum, advancing at an 8.65% CAGR on the back of defense modernization and utility demand.

Which country commands the largest share of Asia-Pacific aircraft output today?

China holds 39.55% of regional production, supported by state-backed programs such as COMAC’s C919 narrowbody.

Which geography is projected to log the fastest production growth?

India records the highest 7.21% CAGR to 2030, driven by competitive manufacturing costs and large-scale OEM partnerships.

What propulsion technology is expected to gain share most rapidly?

Hydrogen-powered platforms post an 8.58% CAGR as governments push net-zero targets and OEMs validate fuel-cell and cryogenic designs.

What is the single biggest driver behind near-term production growth?

Surging domestic passenger traffic across China, India, and Southeast Asia is prompting airlines to lock in large narrowbody orders, sustaining factory backlogs.

What key restraint could slow near-term delivery schedules?

Global shortages of modern aero-engines are creating production bottlenecks that could trim output in the next one to two years.

Page last updated on: