Adaptive Learning Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

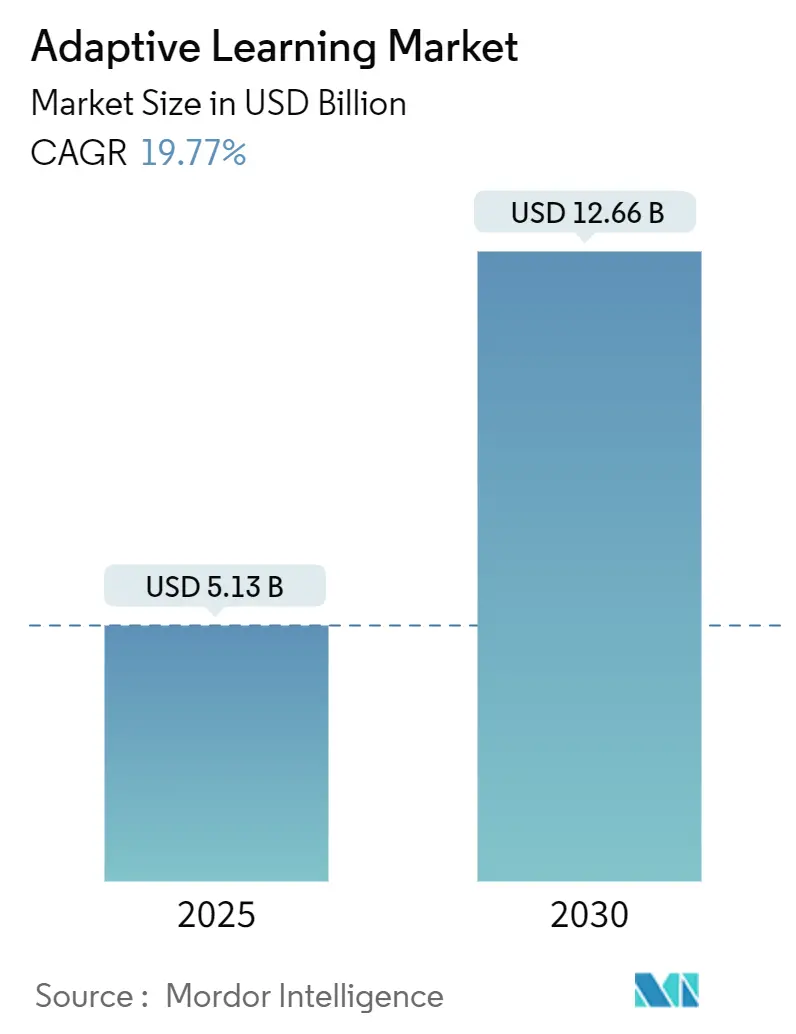

| Market Size (2025) | USD 5.13 Billion |

| Market Size (2030) | USD 12.66 Billion |

| Growth Rate (2025 - 2030) | 19.77% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adaptive Learning Market Analysis by Mordor Intelligence

The adaptive learning market size stood at USD 5.13 billion in 2025 and is forecast to reach USD 12.66 billion in 2030, expanding at a 19.77% CAGR. Growth reflects a global pivot from one-size-fits-all instruction toward AI-driven personalization that calibrates content difficulty and pacing to each learner. Post-pandemic technology investments, expanding cloud bandwidth, and favourable public-sector funding continue to accelerate adoption. Platform and software vendors defend share through algorithm innovation, while services providers capture value by solving integration and teacher-training pain points. Data-privacy mandates and legacy-system complexity temper near-term uptake, yet demonstrated learning-outcome gains sustain long-term demand for adaptive solutions.

Key Report Takeaways

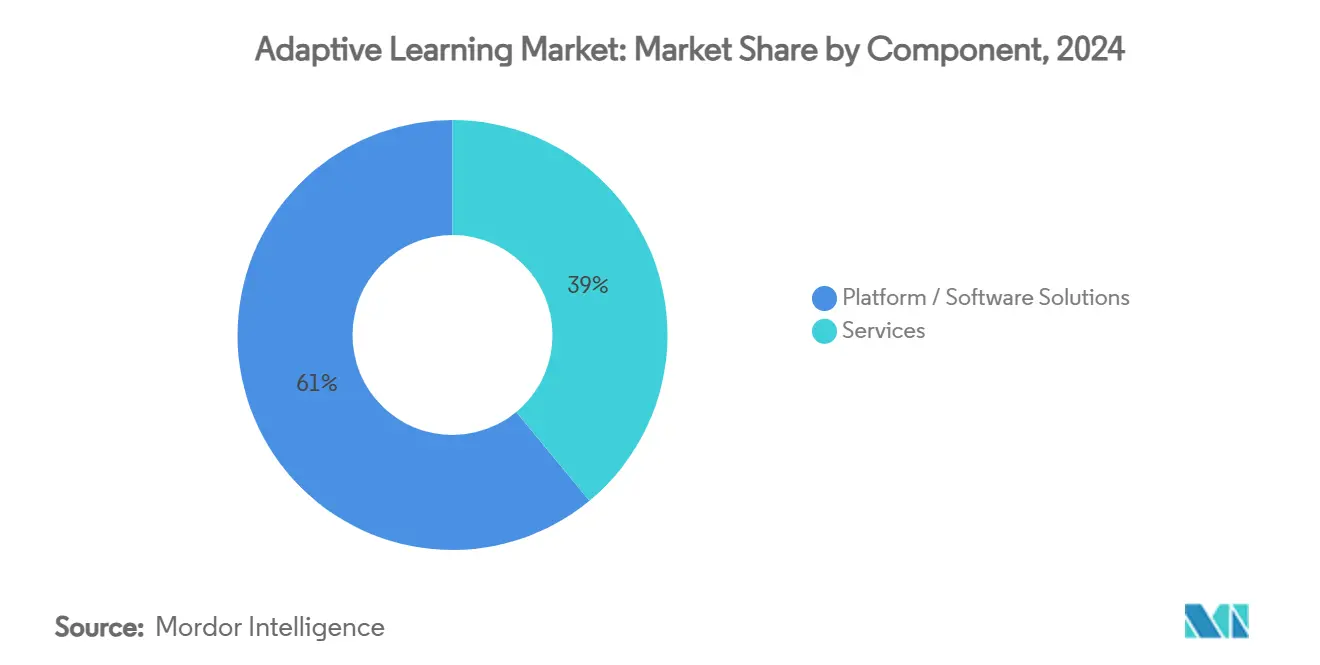

- By component, platform and software solutions led with 61.0% of adaptive learning market share in 2024; professional services are projected to post the fastest 19.87% CAGR through 2030.

- By deployment mode, cloud deployment accounted for 71.3% share of the adaptive learning market size in 2024 and is advancing at a 19.9% CAGR through 2030.

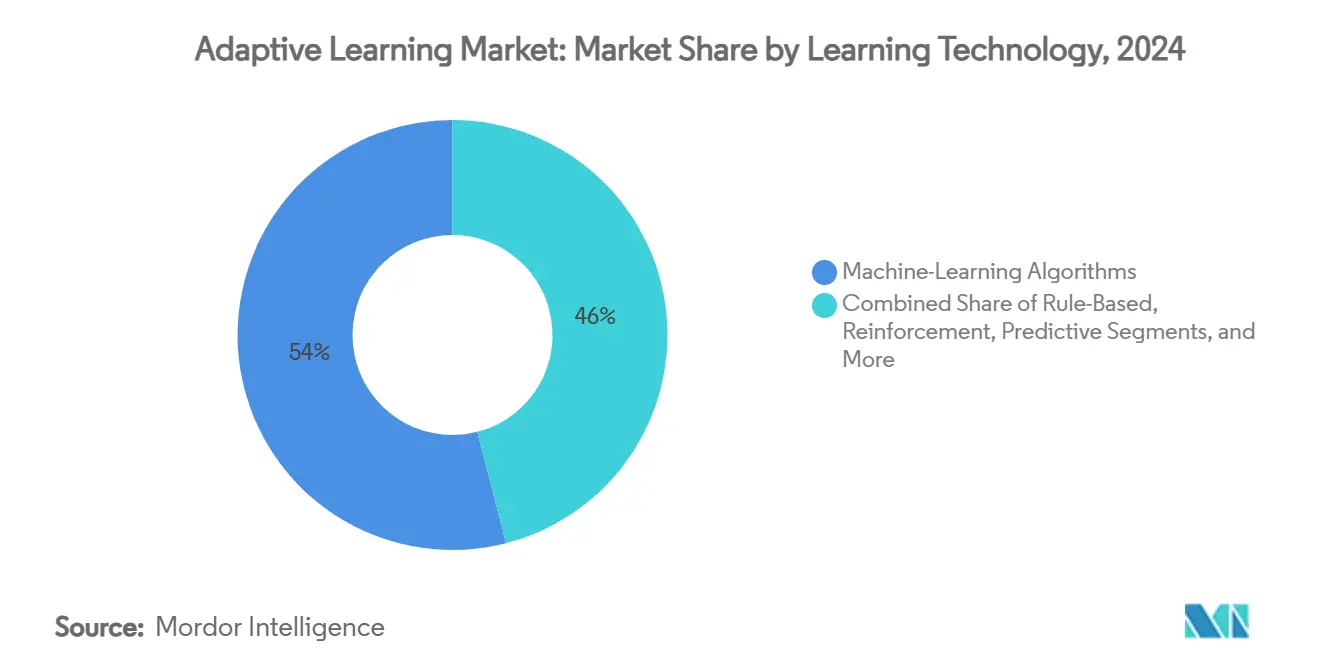

- By learning technology, machine-learning algorithms held 54.0% share in 2024, whereas reinforcement-learning agents are forecast to grow at a 20.2% CAGR to 2030.

- By end user, K-12 schools commanded 42.5% of adaptive learning market share in 2024; corporate and enterprise users record the highest projected 20.7% CAGR to 2030.

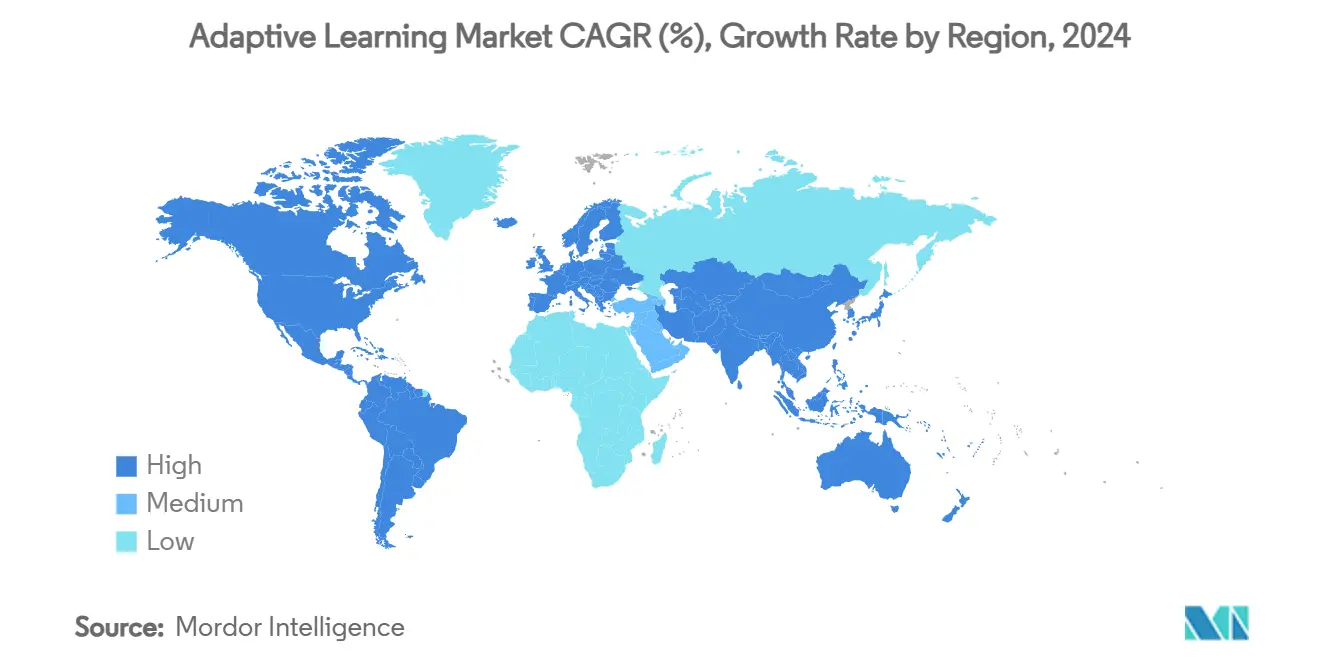

- By geography, North America contributed 44.6% revenue share in 2024, while APAC is set to expand at a 20.5% CAGR to 2030.

Global Adaptive Learning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid digitization of K-12 curricula post-COVID mandates | | +4.2% | Global (North America & Europe lead) | Medium term (2-4 years) |

| Corporate L and D budgets shifting toward data-driven upskilling platforms | +3.8% | North America & EU, rising in APAC | Long term (≥ 4 years) |

| Cloud-native authoring tools lowering total cost of ownership | +2.9% | Global | Short term (≤ 2 years) |

| National AI strategies funding adaptive tutoring pilots | +2.1% | EU, China, Singapore, emerging markets | Long term (≥ 4 years) |

| Edge-AI silicon enabling offline adaptive learning | +1.8% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Neuro-adaptive UX boosting learning efficacy KPIs | +1.4% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid digitization of K-12 curricula post-COVID mandates

School systems accelerated technology roll-outs by three to five years during pandemic lockdowns, creating sunk investments that now require demonstrable instructional returns. Districts that began with standard LMS tools are migrating to adaptive platforms to lift test scores and justify funding. Montana, for example, selected DreamBox Learning for nearly 30,000 students, signalling statewide momentum. [1]Montana Office of Public Instruction, “Montana Office of Public Instruction Selects Discovery Education's DreamBox Learning to Increase Learning Achievement for Montana Students,” mt.gov Platform vendors capable of evidencing outcome gains find receptive buyers, while professional-services demand rises for deployment and teacher coaching. Rural districts, however, still face bandwidth and staffing constraints that slow scale-up.

Corporate L&D budgets shifting toward data-driven upskilling platforms

Enterprises are reallocating learning budgets toward systems that surface skills gaps and prescribe personalised pathways. AT&T’s USD 1 billion reskilling agenda and Uplimit’s AI agents training 1,000 employees at once exemplify corporate appetite for scalable precision learning . Providers such as Workera integrate adaptive diagnostics with HR data to link training spend to productivity metrics. Momentum underpins the segment’s 21.7% CAGR and intensifies competition for enterprise IT integration partnerships.

Cloud-native authoring tools lowering total cost of ownership

Micro-services architectures allow institutions to scale compute resources on demand, trimming infrastructure overhead by up to 40% relative to on-premises estates. [2]Aman K. Singh, “Cloud-Native eLearning Platforms: A Guide To Scalability And Security,” elearningindustry.com. Vendors such as dominKnow streamline collaborative authoring and automated updates, reducing content-development cycles and expanding access for smaller schools. [3]dominKnow, “Cloud Based eLearning Authoring Tools – dominKnow,” dominknow.com. Lower cost of ownership propels cloud’s leading 24.8% CAGR, yet also raises expectations for continuous feature delivery and iron-clad security protocols.

National AI strategies funding adaptive tutoring pilots (e.g., EU Digital Education Action Plan 2027)

Public-sector programmes inject sizable grants into AI-enabled education. The EU earmarked EUR 108 million (USD 121.0 million) for virtual-world and edge-computing curricula. Singapore committed SGD 1 billion (USD 740 million) to national AI roll-outs, while US federal directives promote K-12 AI literacy. Government endorsement legitimises adaptive learning solutions, reduces adoption risk, and catalyses co-investment from private stakeholders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy regulations complicate learner-data collection | −2.8% | EU, North America, global spillover | Short term (≤ 2 years) |

| High integration complexity with legacy SIS/LMS stacks | −2.1% | Global | Medium term (2-4 years) |

| Teacher reskilling gap slows classroom adoption | −2.4% | Global, under-resourced areas | Medium term (2-4 years) |

| Algorithmic bias concerns triggering stricter vendor vetting | −1.9% | EU, North America, expanding to APAC & LatAm | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-privacy regulations complicate learner-data collection

GDPR, FERPA, and the imminent EU AI Act classify educational AI as high-risk, compelling robust consent, transparency, and bias-mitigation controls that add 15-25% to project budgets and extend roll-outs by up to six months. [4]Nhi Nguyen, “What is the EU AI Act? A comprehensive overview,” feedbackfruits.com. Smaller vendors struggle to resource compliance, potentially consolidating market power among capital-rich incumbents. Institutions weigh data-sovereignty clauses and encryption standards before contract award, elongating sales cycles.

High integration complexity with legacy SIS/LMS stacks

Universities and districts often run decades-old student-information and grading systems lacking modern APIs. Projects such as the Unizin–D2L data pipeline required extensive ETL work to compress nightly processing from 12 hours to 2 hours. Custom interfaces raise cost by as much as 50% and necessitate ongoing professional-services support, a chief reason services grow faster than the overall adaptive learning market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Propel Implementation Success

Professional services expanded at a 19.87% CAGR, outpacing the 19.77% headline adaptive learning market growth as institutions sought integration, change-management, and analytics guidance. Platforms retained 61.0% revenue in 2024 but increasingly rely on services partners to drive user adoption. Many districts bundle multi-year managed-services contracts covering data migration, instructional design, and continuous optimisation. The linkage between outcome guarantees and professional expertise reinforces vendor lock-in, yet also increases total cost of ownership. For smaller clients, consortium purchasing and shared-service models are emerging to alleviate budget strain. Competitive differentiation now tilts toward domain consultants that translate dashboard insights into classroom practice while respecting local curricula requirements.

The adaptive learning market size for professional services is projected to climb alongside platform roll-outs, capturing a larger slice of value as deployments scale district-wide. Conversely, standalone software margins compress amid open-source analytics and low-cost entrants, pushing providers to bundle advisory offerings. Investment funds target firms with hybrid tech-service portfolios, anticipating consolidation waves as schools prefer one-stop solutions.

By Deployment Mode: Cloud Infrastructure Underpins Scalability

Cloud deployments accounted for 71.3% of adaptive learning market share in 2024, reflecting institutions’ preference for elastic compute to run AI inference and continuous data-collection loops. With 19.9% CAGR, cloud outpaces on-premises and hybrid models, driven by bundled security, auto-scaling, and consumption-based pricing. Education IT teams leverage vendor-managed micro-services to roll out updates without service windows, minimising classroom disruption.

On-premises retains relevance for universities with sunk investment in private data centres and specialised research computing. Hybrid configurations bridge local SIS repositories with public-cloud analytics, though they require sophisticated orchestration. As edge-AI chipsets mature, an emerging “cloud-edge continuum” positions device-side processing for offline scenarios while syncing summaries to central models, blending benefits of both worlds. Vendors differentiate through FedRAMP, ISO 27001, and GDPR compliance attestations, which have become table stakes in procurement.

By Learning Technology: Reinforcement Learning Gains Traction

Machine-learning engines remained the backbone of 54.0% of platforms in 2024, delivering content sequencing and mastery prediction. Reinforcement-learning (RL) agents, however, log a robust 20.2% CAGR as research evidences superior support for lower-performing students, elementary maths trials showed significant score lifts using RL tutors versus control groups. RL algorithms iteratively optimise teaching strategies via reward signals linked to learner progress, requiring vast interaction data and careful exploration-exploitation balancing. Early adopters integrate guardrails for explainability to assuage educator concerns about “black-box” decision making.

Rule-based engines persist in tightly regulated curricula with deterministic pathways, while predictive-analytics engines inform institutional interventions rather than real-time content adjustment. Competitive edge increasingly hinges on meta-learning frameworks that accelerate RL convergence across subjects, reducing cold-start issues. Patent filings around neuro-adaptive inputs suggest future engines may fuse biosignals with RL to refine personalisation further.

By End User: Enterprises Prioritise Skills Transformation

K-12 districts led 42.5% of revenue in 2024, buoyed by federal grants and public pressure to recover learning losses. Yet, corporate buyers exhibit the fastest 20.7% CAGR, propelled by automation-induced skills churn. Firms deploy adaptive platforms to map employee competency gaps, recommending micro-courses tied to business KPIs. Large upskilling programmes, such as AT&T’s billion-dollar reskilling push, validate the enterprise use case. Integration with HRIS and performance-management suites establishes closed-loop measurement of learning ROI, a critical board-level metric.

Higher-education adoption steadies as universities embed adaptive courseware into gateway subjects to lift retention. Government agencies explore adaptive training for public-sector workforce development, albeit with stringent data-security requirements. Success stories like a Texas school moving into the top 2% nationwide after two daily hours with an AI tutor amplify public acceptance. As efficacy evidence mounts, cross-sector adoption accelerates, positioning adaptive learning as foundational infrastructure for lifelong education.

Geography Analysis

North America generated the largest regional revenue in 2024, capturing 44.6% of the adaptive learning market. Early EdTech investment, broad broadband access, and state-level procurement frameworks accelerated implementation, though compliance with FERPA and diverse district requirements prolong sales cycles. Platform providers differentiate on evidence of learning gains and turnkey teacher-training programmes to win multi-year district contracts.

APAC, in contrast, leads growth momentum with a 20.5% CAGR through 2030. China, India, and Indonesia channel public and private capital toward AI-driven education to expand access and elevate quality. National AI plans subsidise pilot programmes, thus lowering entry costs for schools. Vendors succeed by localising content to national curricula and incorporating offline modes for rural zones. Macro-economic expansion and a cultural premium on education underpin sustained demand.

Europe balances ethical AI imperatives with innovation. Funding via the Digital Europe Programme spurs R&D in edge-computing and virtual-learning environments, while the EU AI Act imposes stringent governance on educational algorithms. Providers investing in transparency tooling and local data hosting gain an advantage. Over the forecast period, regional partnerships between publishers and AI specialists are expected to deepen to meet localisation and compliance expectations.

Competitive Landscape

The adaptive learning market is moderately fragmented. Legacy publishers such as McGraw Hill and Houghton Mifflin Harcourt integrate AI engines into extensive content libraries, while start-ups like SchoolAI and DreamBox specialise in algorithmic personalisation. McGraw Hill’s USD 537 million IPO underscores investor confidence in incumbent transformation strategies. Partnerships, exemplified by McGraw Hill and Pearson linking assessment and curriculum assets, signal ecosystem consolidation.

AI-native challengers raise sizeable venture rounds: SchoolAI secured USD 25 million to extend its district footprint, while Brisk Teaching collected USD 15 million to enhance AI teaching assistants. Technology giants experiment with foundation-model integration; Sunlands wove the DeepSeek model into adult-learning content to scale personalised feedback loops.

Competitive advantage increasingly derives from algorithm transparency, bias-mitigation features, and seamless interoperability with SIS, HRIS, and analytics stacks. Patent activity in neuro-adaptive interventions hints at future disruption paths. Providers targeting offline and low-bandwidth scenarios via edge-AI have an opening in emerging markets where incumbents lack infrastructure-light offerings. Strategic M&A is expected to continue as publishers acquire AI talent and start-ups seek distribution scale.

Adaptive Learning Industry Leaders

DreamBox Learning, Inc.

McGraw-Hill LLC (ALEKS Corporation)

Knewton, Inc.

Area9 Lyceum ApS

Adaptemy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: McGraw Hill completed a USD 537 million IPO to fund further AI-platform expansion and international growth strategies

- June 2025: Discovery Education, known for its vital PreK-12 learning solutions adopted worldwide, has unveiled major upgrades to its online adaptive literacy platform, DreamBox Reading. These enhancements extend DreamBox Reading's reach to encompass all PreK-5 students, empowering educators to bolster students' foundational reading skills and confidence through tailored instruction.

- April 2025: SchoolAI raised USD 25 million and Brisk Teaching USD 15 million to accelerate AI-tutor feature roadmaps and district onboarding, highlighting venture appetite for K-12 personalisation tools

- February 2025: Sunlands Technology integrated DeepSeek AI to personalise adult-learning content, aligning with China’s lifelong-learning push and differentiating via large-language-model capabilities

Global Adaptive Learning Market Report Scope

| Platform / Software Solutions | |

| Services | Professional Services |

| Managed Services |

| Cloud |

| On-Premises |

| Hybrid |

| Rule-Based Adaptive Engines |

| Machine-Learning Algorithms |

| Reinforcement-Learning Agents |

| Predictive-Analytics Engines |

| Other Learning Technologies |

| K-12 Schools |

| Higher Education Institutions |

| Corporate / Enterprise |

| Government and Other End Users |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Component | Platform / Software Solutions | ||

| Services | Professional Services | ||

| Managed Services | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Learning Technology | Rule-Based Adaptive Engines | ||

| Machine-Learning Algorithms | |||

| Reinforcement-Learning Agents | |||

| Predictive-Analytics Engines | |||

| Other Learning Technologies | |||

| By End User | K-12 Schools | ||

| Higher Education Institutions | |||

| Corporate / Enterprise | |||

| Government and Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the adaptive learning market in 2025?

The adaptive learning market size is projected to reach about USD 5.2 billion in 2025, tracking the 19.77% CAGR established between 2024 and 2030.

Which component of adaptive learning grows fastest?

Professional services, including integration and teacher training, are forecast to grow at 19.87% CAGR as institutions seek expertise to implement and optimise platforms.

Why is cloud deployment dominant in adaptive learning?

Cloud infrastructure offers elastic compute for real-time AI processing, lowers ownership costs, and simplifies updates, giving it 71.3% market share in 2024.

What drives corporate adoption of adaptive learning?

Enterprises prioritise measurable skills transformation, using AI analytics to identify gaps and personalize pathways, resulting in a 20.7% CAGR for the corporate segment.

Page last updated on: