Immersive Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

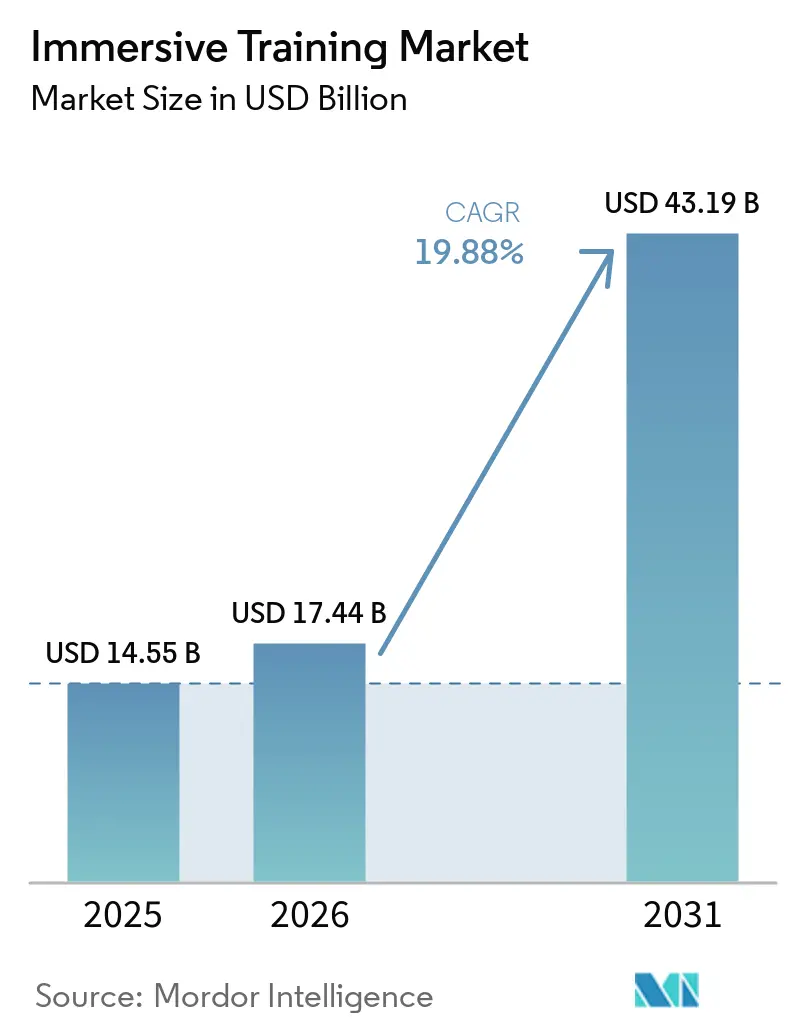

| Market Size (2026) | USD 17.44 Billion |

| Market Size (2031) | USD 43.19 Billion |

| Growth Rate (2026 - 2031) | 19.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Immersive Training Market Analysis by Mordor Intelligence

Immersive training market size in 2026 is estimated at USD 17.44 billion, growing from 2025 value of USD 14.55 billion with 2031 projections showing USD 43.19 billion, growing at 19.88% CAGR over 2026-2031. Rapid enterprise uptake stems from the need to reduce operational risk and improve learning outcomes in high-stakes environments. Cloud-native XR streaming combined with bring-your-own-device access is reshaping total cost of ownership, letting organizations launch programs without large hardware outlays. Hardware continues to anchor the immersive training market, yet services rise fastest as firms value content quality and platform integration above device counts. Healthcare, defense, and manufacturing drive near-term demand, but retail, e-commerce, and corporate soft skills programs expand addressable user bases. Convergence of VR, AR, and mixed reality into extended reality platforms unlocks unified deployments, while regional momentum shifts toward Asia-Pacific on the back of manufacturing digitization.

Key Report Takeaways

- By component, hardware held 51.68% of the immersive training market share in 2025, whereas services post the highest projected CAGR at 21.75% through 2031.

- By technology, virtual reality led with 37.74% revenue share in 2025, while extended reality experiences advance at a 20.54% CAGR to 2031.

- By industry vertical, healthcare accounted for 26.33% share of the immersive training market size in 2025 and retail and e-commerce are forecast to expand at 23.61% CAGR between 2026-2031.

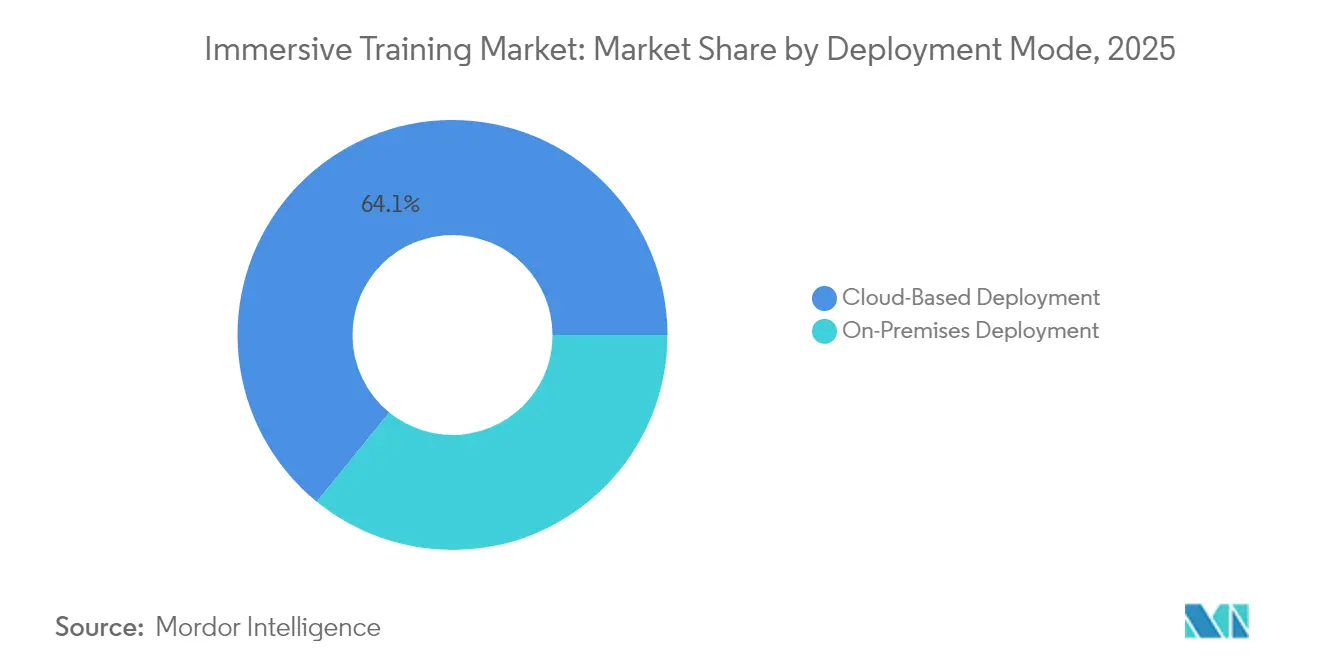

- By deployment mode, cloud-based platforms commanded 64.12% of the immersive training market share in 2025 and are poised to grow at 21.96% CAGR through 2031.

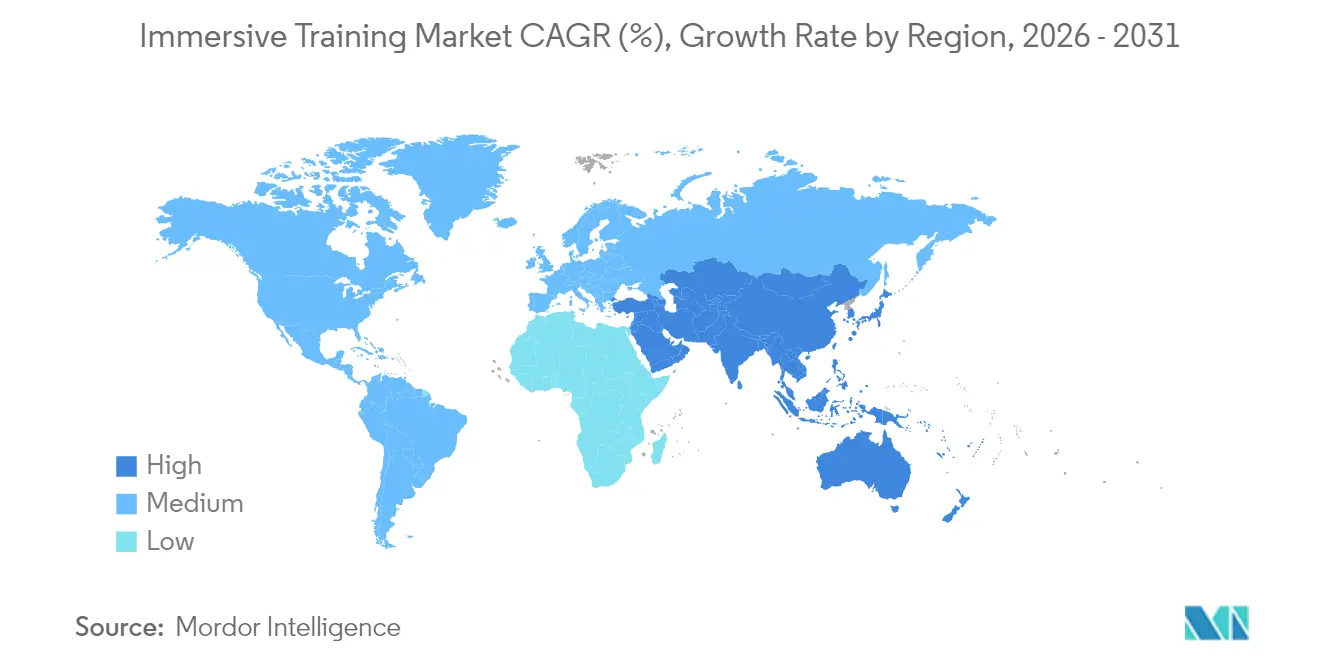

- By geography, North America contributed 38.62% of 2025 revenues, yet Asia-Pacific records the quickest regional CAGR at 21.12% for the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Immersive Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise adoption of XR-based remote workforce upskilling | +4.20% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Cost reduction through digital-twin simulated training | +3.80% | Manufacturing hubs in Asia-Pacific, North America, and Germany | Long term (≥ 4 years) |

| Regulatory push for surgical competence validation via VR | +3.10% | North America, Europe, with expansion to Asia-Pacific | Medium term (2-4 years) |

| Rise of defense metaverse funding pipelines | +2.90% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Cloud streaming of immersive content enabling BYOD training | +3.50% | Global, accelerated in regions with robust cloud infrastructure | Short term (≤ 2 years) |

| Neuroadaptive feedback enhancing learning retention metrics | +2.80% | Advanced markets in North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Adoption of XR-Based Remote Workforce Upskilling

Enterprises embed XR modules into learning management systems to give dispersed staff hands-on practice without travel or classroom setup. Large employers report up to 40% reductions in per-employee training expense versus instructor-led models. Hybrid work policies accelerate program scale because immersive sessions run on consumer-grade headsets, laptops, or mobiles, lifting adoption barriers. Standardized digital content keeps skill quality uniform across sites, and analytics dashboards let managers track competence in real time. These benefits push the immersive training market toward mainstream use within routine workforce development budgets.

Cost Reduction Through Digital-Twin Simulated Training

Digital twins recreate complex equipment and hazardous environments, so staff learn without shutting down production lines. Automotive and electronics factories record 60% fewer machine stoppages during onboarding cycles when simulations replace real-world practice.[1]Siemens AG, “Siemens and NVIDIA Partner for Industrial Metaverse,” Siemens.com Repetition in virtual space eliminates consumable materials costs and mitigates worker injury risk. Integrating live sensor data ensures scenarios mirror current operating conditions, keeping instruction relevant. Enterprises typically realize payback inside 18 months, feeding sustained growth in the immersive training market.

Regulatory Push for Surgical Competence Validation via VR

The United States FDA issued 2024 guidance that formalizes approval pathways for immersive medical training platforms, giving hospitals legal clarity to certify surgeons through VR modules.[2]Food and Drug Administration, “Digital Health Software Precertification (Pre-Cert) Program,” FDA.gov Performance metrics such as motion-tracking accuracy enable objective assessment, satisfying regulators that procedures meet safety benchmarks. Similar frameworks emerge in Europe and are under draft review in Asia-Pacific. Hospitals allocating budget for compliance turn to validated XR suites, reinforcing healthcare dominance in the immersive training market.

Cloud Streaming of Immersive Content Enabling BYOD Training

High-fidelity XR streaming shifts compute workloads to the cloud, letting users access complex simulations on thin clients. Services like NVIDIA CloudXR deliver 90-frames-per-second visuals with minimal latency, eliminating specialized workstations.[3]NVIDIA Corporation, “NVIDIA Omniverse Cloud,” NVIDIA.com This model converts capital expense into pay-per-use operating cost, easing adoption for budget-constrained firms. Central cloud repositories also simplify content updates, ensuring consistent experiences across multiple sites and devices. The resulting flexibility fuels quick gains in the immersive training market, especially for seasonal or high-turnover workforce segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront hardware CapEx for multi-user installations | -2.10% | Global, particularly affecting small-to-medium enterprises | Short term (≤ 2 years) |

| Persistent motion sickness and user comfort issues | -1.80% | Global, with higher impact in regions with limited XR exposure | Medium term (2-4 years) |

| Data privacy concerns in biometric telemetry capture | -1.50% | Europe and North America due to GDPR and privacy regulations | Medium term (2-4 years) |

| Lack of instructional design standards for immersive assessments | -1.30% | Global, with particular impact on regulated industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware CapEx for Multi-User Installations

Complete room-scale training suites cost between USD 50,000 and USD 500,000, straining budgets of small enterprises. Hardware refresh cycles every three years add repeat expense, while facility retrofits such as tracking rigs increase complexity.[4]HTC Corporation, “HTC Vive Pro 2 Enterprise Solutions,” HTC.com Cloud streaming mitigates some capital load, yet network latency and bandwidth limits in certain regions still necessitate on-premises gear, slowing the immersive training market rollout among cost-sensitive buyers.

Persistent Motion Sickness and User Comfort Issues

Twenty-five to thirty percent of first-time users report discomfort within 45-minute VR sessions, prompting organizations to shorten modules or provide alternative formats. User fatigue undermines lesson depth and lowers engagement metrics. Although display refresh rates, field-of-view optimization, and foveated rendering alleviate symptoms, complete resolution remains years away. This physiological barrier tempers adoption speed in sectors that require extended training durations, limiting short-term growth of the immersive training market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Emerge as Growth Catalyst

Services revenue grows at 21.75% CAGR, outpacing hardware and software as enterprises realize that expert content and integration drive training impact. In 2025, hardware still controlled 51.68% of immersive training market share, but enterprises redirect budgets toward scenario design, deployment consulting, and ongoing support. Custom modules range from USD 100,000 to USD 1 million depending on fidelity, complexity, and regulatory requirements. The immersive training market size attributable to services is projected to overtake hardware after 2028, given recurring maintenance and content refresh fees.

Content creation studios benefit from long-tail demand for vertical-specific scenarios such as clean-room semiconductor procedures or emergency response drills. Managed services for analytics and performance dashboards add incremental revenue streams. Software retains steady demand because enterprises still require authoring tools and learning management connectors, yet its relative share declines as platform commoditization sets in. Overall, the immersive training market continues a pivot from device procurement toward holistic outcome-oriented service engagements.

By Technology: Extended Reality Drives Convergence

Extended reality platforms grow at 20.54% CAGR as enterprises seek single toolchains that handle VR, AR, and mixed reality functions. Virtual reality owns 37.74% of the immersive training market size in 2025 owing to high-immersion requirements in surgery and aviation. However, AR overlays gain popularity for on-the-job guidance, while mixed reality provides spatially precise holograms for complex maintenance tasks. Unified XR engines reduce integration overhead, cutting total deployment cost by up to 25% when compared with discrete stacks.

360-degree video remains a gateway for organizations hesitant about interactable simulations, offering lower development overhead at the expense of interactivity. AI-driven adaptive content begins to surface, tailoring difficulty based on biometric feedback. As headset capabilities converge and licensing models simplify, the immersive training market aligns around agnostic XR runtimes that can flex between use cases without hardware lock-in.

By Industry Verticals: Healthcare Leads, Retail Accelerates

Healthcare held 26.33% of immersive training market share in 2025, fuelled by regulatory mandates and the need for repeatable, measurable competency checks. Clinical programs leverage haptic devices to mimic tissue response, and hospitals value objective scoring systems for accreditation audits. Retail and e-commerce represent the quickest-growing vertical at 23.61% CAGR, using VR role-play to teach customer engagement and shelf stocking across dispersed outlets.

Aerospace and defense maintain deep simulation histories, yet modern XR adds cyber and space operations layers impossible in legacy dome simulators. Manufacturing expands adoption for line-changeover rehearsals and safety drills, trimming incident rates. Education institutions integrate immersive capstone projects to bridge theory and practice, while corporate soft-skills modules diversify demand. As these verticals mature, the immersive training industry crosses from early adopter pockets into enterprise-wide learning ecosystems.

By Deployment Mode: Cloud-Based Solutions Dominate

Cloud delivery held 64.12% market share in 2025 and rises at 21.96% CAGR, reinforcing an operational spending preference. Enterprises appreciate instant scale for seasonal onboarding and disaster response rehearsal without adding on-premises graphics servers. Edge compute nodes inside regional data centers lower latency to under 20 milliseconds, meeting comfort thresholds for most users.

Hybrid stacks persist where data sovereignty laws or connectivity gaps prevail. Yet even heavily regulated sectors pilot secure cloud sandboxes, signalling longer-term migration. Automated update pipelines mean security patches and feature rollouts propagate instantly, reducing IT headcount requirements. This deployment shift reinforces the immersive training market trend toward subscription revenue, smoothing supplier cash flows and broadening customer entry options.

By Application: Simulation-Based Learning Leads Market

Simulation-based learning retained 32.85% share in 2025, addressing high-risk tasks like refinery shutdowns and surgical procedures. Immersive soft-skills programs, however, grow at a 20.92% CAGR, illustrating widening acceptance of VR for leadership, negotiation, and conflict resolution drills. Interactive learning combines instructor avatars with real-time coaching, while gamified leaderboards enhance engagement.

Virtual instructor-led training blends synchronous classroom interaction with 3D content, enabling geographically scattered cohorts to collaborate. Technical skills modules remain vital in heavy industry, but compliance content gains ground as regulators endorse immersive audits. Overall diversification of use cases sustains double-digit expansion of the immersive training market and showcases XR versatility across cognitive and motor skill development.

Geography Analysis

North America generated 38.62% of 2025 revenues thanks to early adopters, mature cloud infrastructure, and government budget allocations such as the U.S. Department of Defense USD 1.2 billion immersive initiative. High broadband penetration lets enterprises stream multi-user sessions with minimal latency. Canada mandates VR surgical validation in select provinces, while Mexico’s automotive plants use XR for assembly training. Integration with established enterprise software ecosystems lowers friction for large buyers, keeping North America at the forefront of the immersive training market.

Asia-Pacific records the fastest CAGR at 21.12% through 2031. Chinese manufacturers, supported by state digitization subsidies, deploy digital twins to cut downtime and quality defects. Japanese automakers integrate mixed reality into precision torque procedures, and South Korean semiconductor fabs rely on AR overlays during sub-micron lithography maintenance. India’s IT services sector supplies cost-effective immersive content to global clients, leveraging low-cost development talent. Rapid 5G rollout and cross-border cloud expansions remove historical connectivity hurdles, enabling broader uptake of immersive training market solutions.

Europe experiences steady progress, driven by stringent safety and data privacy regulations that push organizations toward standardized competency validation. Germany’s Industry 4.0 agenda merges XR with real-time production data, while the United Kingdom NHS experiments with VR duty-of-care programs. France’s aerospace cluster adopts haptic flight deck simulators to shorten pilot conversion times. GDPR influences platform design to prioritize on-device encryption and anonymized analytics, and this compliance focus positions European vendors for premium contracts in privacy-sensitive domains. Collectively, regional dynamics create a balanced global outlook for the immersive training market.

Competitive Landscape

The supplier field remains moderately fragmented but is trending toward consolidation. Technology majors such as Microsoft and Meta bundle cloud, device, and collaboration services, offering one-stop procurement paths. Specialized content leaders like CAE, Boeing, and VirtaMed leverage vertical expertise to sell high-margin scenario libraries. Hardware innovators race to add features such as pancake lenses and haptic gloves that extend session comfort.

Competitive edge is shifting from raw hardware specifications to measurable learning outcomes. Vendors highlight reductions in time-to-competency and improvements in safety metrics to secure enterprise renewals. Intellectual property filings concentrate on neuroadaptive feedback loops that tailor difficulty on the fly, aiming to raise skill retention rates. Partnerships between chipmakers and content studios indicate a push toward integrated offerings that can capture a larger slice of the immersive training market size.

Price competition persists at the entry level, yet mid-tier and regulated sectors favour vendors that provide validation evidence and regulatory documentation. Consequently, strategic alliances and acquisitions intensify. Notable moves include Microsoft integrating acquisition talent into its Mesh platform and Meta targeting Quest 3S enterprise bundles. Long-term, the immersive training industry may see a small cadre of full-stack suppliers dominating complex deals while boutique specialists service niche scenarios.

Immersive Training Industry Leaders

Microsoft Corporation

Meta Platforms, Inc.

Alphabet Inc.

HTC Corporation

Unity Software Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Meta Platforms expanded its Quest for Business program with enhanced enterprise management tools and multi-user licensing options, enabling organizations to deploy immersive training at scale with centralized content distribution and user analytics capabilities that reduce administrative overhead by approximately 35%.

- September 2025: Boeing secured a USD 280 million contract from the U.S. Navy for advanced immersive pilot training systems integrating artificial intelligence-driven scenario generation, enabling dynamic mission planning exercises that adapt to individual trainee performance and operational requirements.

- August 2025: Siemens launched its Industrial Metaverse Training Suite, combining digital twin technology with immersive VR platforms to provide manufacturers with standardized training content for complex equipment operations, targeting USD 150 million in first-year revenue from automotive and electronics sector clients.

- July 2025: Microsoft announced the integration of Copilot AI capabilities into Mesh for immersive training applications, enabling real-time language translation and automated training content generation that reduces content development time by up to 50% for enterprise clients.

Global Immersive Training Market Report Scope

The Immersive Training Market Report is Segmented by Component (Hardware, Software, Services), Technology (VR, AR, MR, XR, 360-Degree Video), Industry Verticals (Healthcare, Aerospace and Defense, Manufacturing, Automotive, Education, Corporate Training), Deployment Mode (On-Premises, Cloud-Based), Application (Simulation-Based Learning, Interactive Learning, VILT, Gamification), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | VR Headsets |

| AR Glasses | |

| Haptic Feedback Devices | |

| Motion Sensors and Trackers | |

| Wearables and Accessories | |

| Software | Learning Management Systems (LMS) |

| Simulation Software | |

| Content Management Systems | |

| Customized Training Content | |

| Services | Content Development |

| Integration and Deployment | |

| Support and Maintenance | |

| Consulting and Training Services |

| Virtual Reality (VR) |

| Augmented Reality (AR) |

| Mixed Reality (MR) |

| Extended Reality (XR) |

| 360-Degree Video Training |

| Others Technology (AI-Enabled Immersive Platforms, Haptic Simulations) |

| Healthcare | Surgical Training |

| Patient Care Simulations | |

| Aerospace and Defense | Combat Simulations |

| Mission Planning | |

| Manufacturing | Equipment Training |

| Safety Drills | |

| Automotive | |

| Education and Academia | |

| Media and Entertainment | |

| Retail and E-commerce | |

| Corporate / Enterprise Training | |

| Other Automotive Uses (Energy, Construction, Logistics) |

| On-Premises Deployment |

| Cloud-Based Deployment |

| Simulation-Based Learning |

| Interactive Learning |

| Virtual Instructor-Led Training (VILT) |

| Gamification |

| Soft Skills Training |

| Technical Skills Training |

| Compliance Training |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | VR Headsets |

| AR Glasses | ||

| Haptic Feedback Devices | ||

| Motion Sensors and Trackers | ||

| Wearables and Accessories | ||

| Software | Learning Management Systems (LMS) | |

| Simulation Software | ||

| Content Management Systems | ||

| Customized Training Content | ||

| Services | Content Development | |

| Integration and Deployment | ||

| Support and Maintenance | ||

| Consulting and Training Services | ||

| By Technology | Virtual Reality (VR) | |

| Augmented Reality (AR) | ||

| Mixed Reality (MR) | ||

| Extended Reality (XR) | ||

| 360-Degree Video Training | ||

| Others Technology (AI-Enabled Immersive Platforms, Haptic Simulations) | ||

| By Industry Vertical Use | Healthcare | Surgical Training |

| Patient Care Simulations | ||

| Aerospace and Defense | Combat Simulations | |

| Mission Planning | ||

| Manufacturing | Equipment Training | |

| Safety Drills | ||

| Automotive | ||

| Education and Academia | ||

| Media and Entertainment | ||

| Retail and E-commerce | ||

| Corporate / Enterprise Training | ||

| Other Automotive Uses (Energy, Construction, Logistics) | ||

| By Deployment Mode | On-Premises Deployment | |

| Cloud-Based Deployment | ||

| By Application | Simulation-Based Learning | |

| Interactive Learning | ||

| Virtual Instructor-Led Training (VILT) | ||

| Gamification | ||

| Soft Skills Training | ||

| Technical Skills Training | ||

| Compliance Training | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the immersive training market?

The immersive training market size is USD 17.44 billion in 2026.

How fast is global demand for immersive training growing?

Market revenues are forecast to rise at a 19.88% CAGR through 2031.

Which component category shows the fastest revenue expansion?

Services grow most quickly at 21.75% CAGR as firms prioritize content and integration expertise.

Why is Asia-Pacific considered the most attractive growth region?

Manufacturing digitization programs and supportive government upskilling policies drive a 21.12% regional CAGR.

How does cloud deployment influence adoption?

Cloud streaming cuts capital expense, offers rapid scaling, and holds a 64.12% share, making it the dominant deployment mode.

Which industry vertical leads in immersive training use today?

Healthcare commands 26.33% of 2025 revenue due to regulatory demands for validated surgical competence.

Page last updated on: