Adaptive AI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.51 Billion |

| Market Size (2031) | USD 18.77 Billion |

| Growth Rate (2026 - 2031) | 39.85% CAGR |

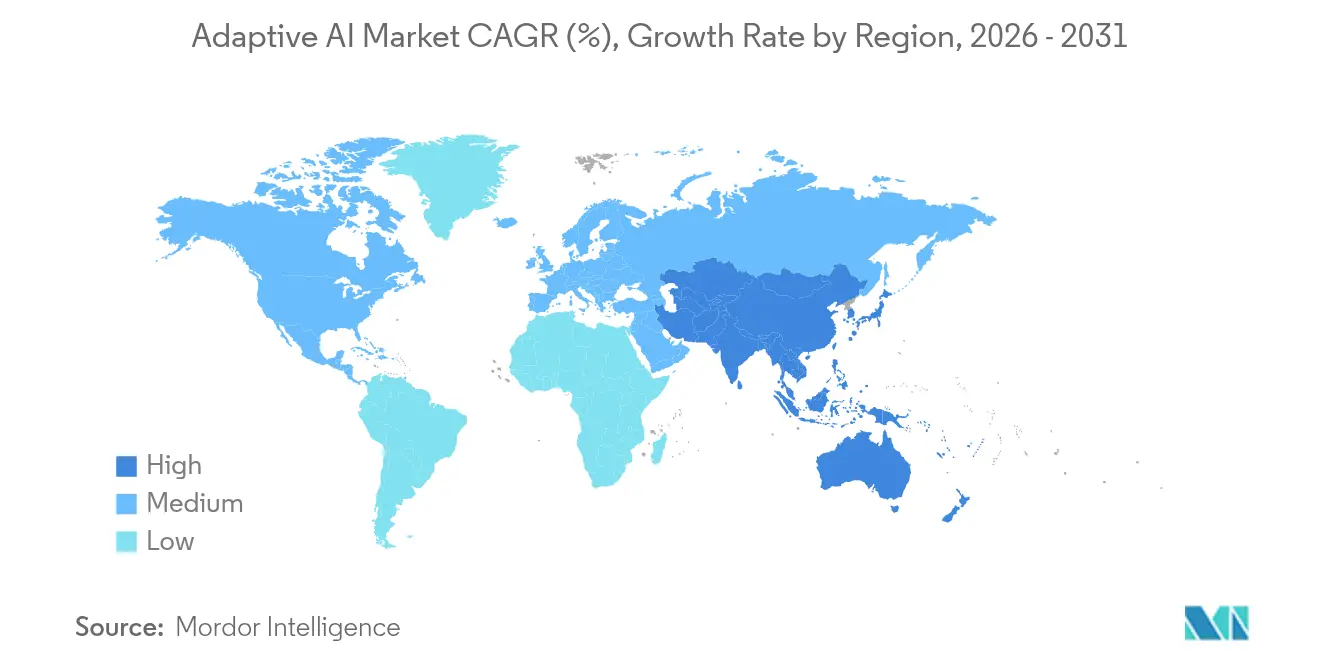

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

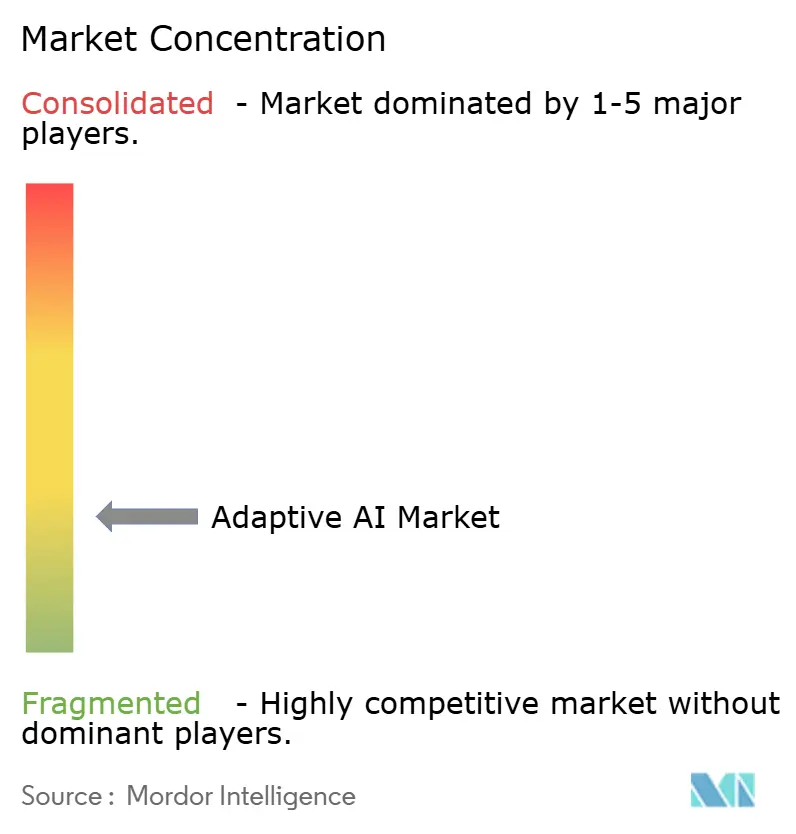

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adaptive AI Market Analysis by Mordor Intelligence

Adaptive AI market size in 2026 is estimated at USD 3.51 billion, growing from 2025 value of USD 2.51 billion with 2031 projections showing USD 18.77 billion, growing at 39.85% CAGR over 2026-2031. Rapid growth reflects enterprises’ pivot from static predictive tools to systems that learn continuously, self-correct, and operate with minimal human oversight. Strong capital commitments by leading vendors underpin this trend—Google earmarked USD 75 billion for AI infrastructure in 2025—while Microsoft pledged USD 80 billion for new AI-focused data-centers. At the application layer, fraud detection, real-time analytics, and autonomous decision loops demonstrate the clearest near-term returns, encouraging board-level sponsorship and driving cross-industry adoption. The shift toward multi-agent orchestration, in which specialized AI agents collaborate on complex workflows, is redefining software architectures and widening the addressable scope for adaptive AI platforms. Meanwhile, regulatory initiatives such as the EU AI Act are sharpening the market’s focus on explainability, data provenance, and region-specific model training, creating new opportunities for compliance-ready solutions.

Key Report Takeaways

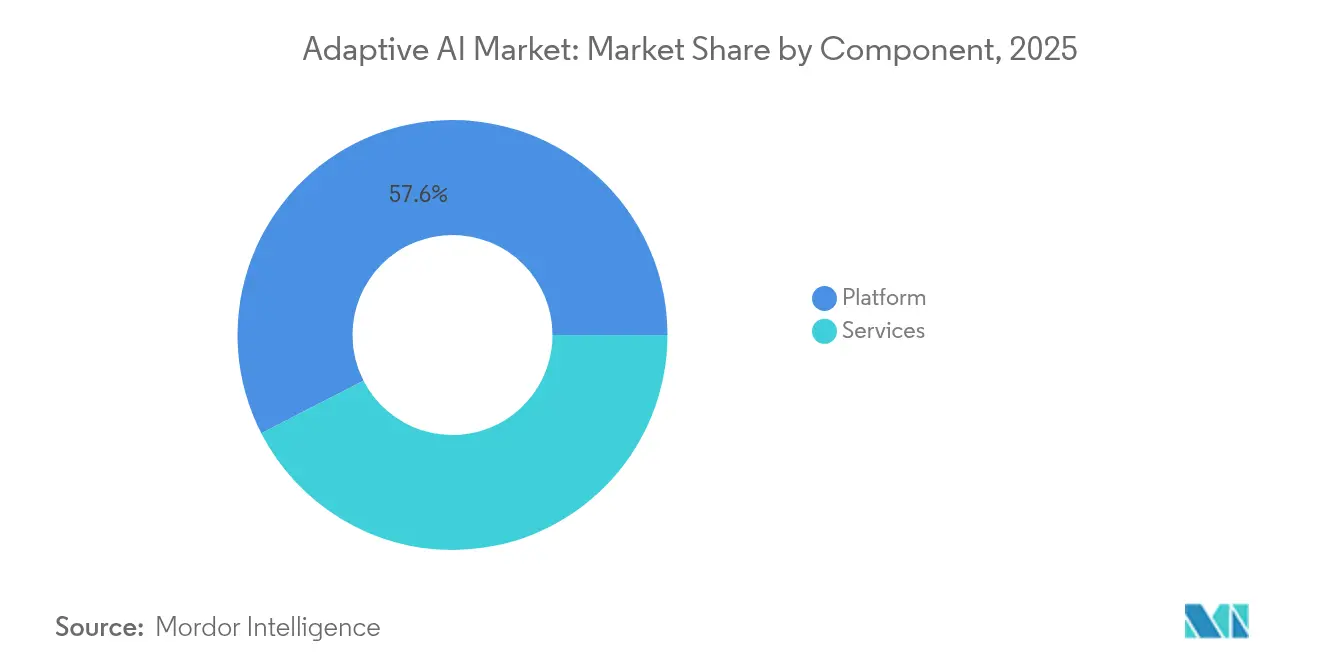

- By component, platform offerings led with 57.55% revenue share in 2025, whereas services are projected to register a 43.10% CAGR through 2031.

- By deployment model, the cloud segment held 70.65% of the adaptive AI market share in 2025, while hybrid solutions are expected to expand at a 49.90% CAGR to 2031.

- By end-user industry, BFSI captured 30.25% of the adaptive AI market size in 2025; healthcare and life sciences are forecast to post a 44.20% CAGR through 2031.

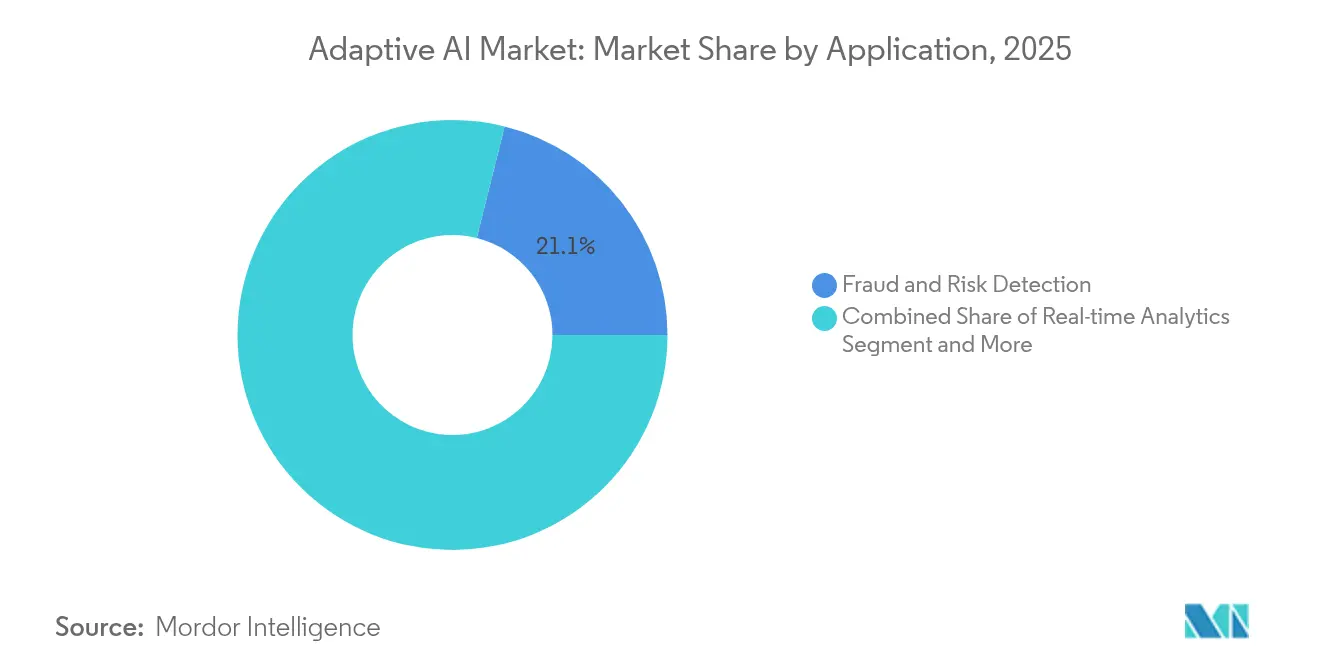

- By application, fraud and risk detection accounted for 21.10% of the adaptive AI market size in 2025, whereas autonomous systems are set to grow at a 51.80% CAGR through 2031.

- By technology, machine learning anchored 42.10% of 2025 revenue, but generative AI is projected to climb at a 52.30% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adaptive AI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for real-time analytics in dynamic data environments | +8.5% | Global, early gains in North America and Asia-Pacific financial hubs | Medium term (2-4 years) |

| Growing adoption of AI-as-a-Service platforms | +7.2% | Global, concentrated in North America and Europe | Short term (≤2 years) |

| Uptake in BFSI for fraud detection and hyper-personalisation | +6.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Shift to on-prem and hybrid deployments to curb cloud costs | +5.9% | Global, especially regulated industries | Short term (≤2 years) |

| Emergence of agentic AI frameworks for autonomous decision loops | +9.1% | Global, early in North America and Asia-Pacific | Long term (≥4 years) |

| Asia-Pacific localisation mandates for region-trained LLMs | +4.3% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Real-Time Analytics in Dynamic Data Environments

Three-quarters of enterprises now fund real-time analytics initiatives, and 80% report revenue uplift from live data-driven decisions. Adaptive AI streams incoming data, refines algorithms on the fly, and delivers instant insights that conventional batch analytics cannot match. Financial institutions use these capabilities to intercept fraudulent payments within milliseconds, updating risk models as new threats appear. Manufacturers feed sensor data to adaptive AI that autonomously fine-tunes line speeds, temperature settings, and supply schedules, yielding material savings and higher output quality. Across industries, executives cite faster insight-to-action cycles as a decisive competitive edge.

Growing Adoption of AI-as-a-Service Platforms

Cloud providers now bundle AutoML, vector databases, and pre-trained models into subscription-based services, lowering both cost and skill barriers. Microsoft’s Azure AI serves more than 53,000 organizations[1]“Azure AI Momentum Accelerates,” Microsoft, microsoft.com, while Google’s “AI Cloud Takeoff” program funds pilot projects across Southeast Asia. SMEs that previously lacked in-house data-science talent can deploy adaptive AI for customer support, demand planning, or warranty analytics without procuring specialist hardware. The pay-as-you-train pricing model accelerates experimentation, and integrated compliance toolkits ease regulatory audits.

Uptake in BFSI for Fraud Detection and Hyper-Personalisation

Banks and insurers allocate expanding budgets to adaptive AI engines that recast fraud prevention and client engagement. Real-time behavioral models achieve 99.2% detection accuracy and 60% fewer false positives, translating into lower charge-off rates and smoother customer journeys. Parallel personalization engines analyze each user’s transaction cadence, channel preference, and life-stage signals to surface bespoke products. Institutions that embed explainable AI scorecards meet stringent audit requirements while sustaining automated model retraining.

Emergence of Agentic AI Frameworks for Autonomous Decision Loops

Agentic AI systems construct goals, generate plans, and act with minimal human input, enabling end-to-end automation of complex tasks. Salesforce’s Agentforce links CRM records to specialized domain agents that orchestrate marketing, service, and sales workflows.[2]“Agentforce: The Next Evolution of CRM,” Salesforce, salesforce.com IBM’s watsonx Orchestrate taps over 1,500 enterprise applications to route tasks among procurement, finance, and HR bots.[3]“IBM watsonx: Orchestrating Enterprise Agents,” IBM, ibm.com The payoff lies in continuously improving processes: each agent assimilates outcomes, retrains its policy, and refines the collective strategy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy and cross-border governance hurdles | -4.2% | Global, strongest in EU and regulated markets | Long term (≥4 years) |

| Integration complexity with legacy data silos | -5.8% | Global, all mature enterprises | Medium term (2-4 years) |

| Hardware bottlenecks for on-device retraining | -3.1% | Global, resource-constrained sites | Short term (≤2 years) |

| Regulatory push for explainability slowing release cycles | -2.9% | EU, North America, regulated verticals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cross-Border Governance Hurdles

The EU AI Act, Colorado AI Law, and similar statutes compel detailed documentation, fairness audits, and human oversight. Firms operating across borders must localize data or deploy geo-fenced models, inflating project costs and complicating version control. China’s Interim AI Measures add security vetting and value-alignment clauses that restrict iterative retraining. Compliance expenses can consume 15% of an adaptive AI budget, prompting some enterprises to limit deployments to jurisdictionally simpler use cases.

Integration Complexity with Legacy Data Silos

Only a quarter of large-scale AI projects deliver anticipated returns, mainly due to fragmented data estates and incompatible schemas. Legacy core banking systems, ERP modules, and operational historians often lack real-time APIs, blocking the continuous data ingestion adaptive AI requires. Organizations must invest in data lakehouses, governance frameworks, and low-latency streaming pipelines before intelligent automation scales. Modernization outlays lengthen payback periods but remain prerequisite for production-grade adaptive AI.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform Centricity Fuels Enterprise Adoption

Platform offerings captured USD 1.44 billion and 57.55% of 2025 revenue, anchoring the adaptive AI market. These end-to-end suites let users collect data, craft features, train models, deploy agents, and monitor drift from a unified interface. Vendors bundle AutoML, reinforcement learning, and agent orchestration to mask algorithmic complexity, attracting business analysts alongside data scientists. The services segment grows fastest at a 43.10% CAGR because organizations still need integration, change management, and model-ops support. Consulting teams translate workflows into agentic blueprints, tune domain-specific models, and manage drift remediation under service level agreements.

Adaptive AI market size for services is projected to add nearly USD 3.1 billion by 2031 as companies pursue turnkey maintenance deals. Meanwhile, open-source accelerators plug into commercial platforms, enabling vendor-agnostic pipelines. This hybrid tooling lowers lock-in risk and encourages broader participation. Over the forecast horizon, platform providers that embed no-code process designers and pay-per-agent pricing models are poised to capture incremental share in mid-market accounts.

By Deployment Model: Cloud Dominance with Hybrid Momentum

In 2025 the cloud segment controlled 70.65% of adaptive AI market share thanks to elastic compute and managed accelerators. High-density GPU clusters cut training times for large language or vision models from weeks to hours, catalyzing experimentation. Yet the same consumption pricing inflates inference costs as workloads scale, pushing enterprises to repatriate stable workloads to on-prem racks or edge devices. Adaptive AI market size for hybrid architectures is projected to swell at a 49.90% CAGR, mirroring broader FinOps efforts to optimize total cost of ownership.

Regulatory mandates intensify the shift. Banks subject to data-residency rules host customer PII on-prem while tapping cloud GPUs for anonymized pretraining. Manufacturers stream plant telemetry to local inference boxes for sub-millisecond control while syncing anonymized snapshots to the cloud for fleet-wide model refinement. Vendors respond with “bring-your-own-key” encryption, hardware root of trust, and federated learning schemes that reconcile security with scale.

By End-User Industry: BFSI Maintains Lead as Healthcare Accelerates

The BFSI sector generated USD 0.76 billion and 30.25% of 2025 revenue, reflecting a mature appetite for fraud analytics and hyper-personalization engines. Banks layer adaptive AI atop payments, credit, and trading platforms to block emerging scams and tailor cross-sell offers. The sector’s conservative risk culture values the continuous explainability dashboards built into adaptive AI platforms.

Healthcare and life sciences advance fastest, with a 44.20% CAGR to 2031, driven by autonomous diagnostic tools and real-time treatment optimization. Adaptive AI models monitor vitals, interpret imaging scans, and adjust drug regimens without clinician intervention, pending oversight. Emerging regulations now permit algorithmic therapeutic recommendations if accompanied by provenance trails and override mechanisms, accelerating hospital adoption. Beyond these verticals, manufacturing exploits adaptive AI for predictive maintenance, while the public sector pilots citizen-service chatbots in multiple languages.

By Application: Fraud Detection Commands Spend; Autonomous Systems Surge

Fraud and risk detection represented USD 0.53 billion and 21.10% of the 2025 adaptive AI market size, underscoring the clear ROI of real-time anomaly spotting. Continuous learning models cut charge-backs, boost approval rates, and slash manual review queues. Yet autonomous systems, self-governing agent swarms handling logistics, IT operations, and customer care, are slated for a 51.80% CAGR. Early pilots show >40% cycle-time reductions in order fulfillment as agents coordinate suppliers, warehouses, and carriers.

Real-time analytics, recommendation engines, predictive maintenance, and conversational agents round out major segments. Enterprises increasingly bundle these use cases into composite agent networks, achieving network effects as knowledge propagates across tasks. Vendors that pre-package industry-specific skill libraries and guardrail policies are capturing the bulk of greenfield projects.

By Technology: Machine Learning Anchors; Generative AI Expands

Machine learning frameworks formed the backbone of 42.10% of 2025 revenue, supplying regression, classification, and reinforcement algorithms that underpin adaptive learning loops. Transfer learning and online gradient descent remain staples for resource-efficient retraining on streaming data. Generative AI, while smaller, is on a 52.30% CAGR trajectory as it imbues adaptive systems with the capacity to create content, craft code, or propose new process flows.

Reinforcement-learning-from-feedback algorithms refine agent strategies through continuous reward signals, while AutoML democratizes model selection and hyper-parameter tuning. Natural language processing lets agents converse, reason, and extract unstructured insights, closing the loop between textual data and downstream actions. Edge-optimized model compilers compress transformer weights for on-device inference, mitigating latency and privacy concerns.

Geography Analysis

North America accounted for 41.10% of 2025 revenue, buoyed by more than USD 300 billion in annual corporate AI outlays and a dense ecosystem of specialized chip, software, and cloud suppliers.Federal and state legislation supplies clear guardrails that de-risk production roll-outs, while abundant venture capital seeds a steady pipeline of adaptive AI startups. Workforce readiness programs from major vendors further accelerate adoption by upskilling IT staff in MLOps and agent orchestration.

Asia-Pacific is the fastest-growing theatre, sprinting at a 54.00% CAGR to 2031. Sovereign AI programs in China, Japan, and India subsidize local model training and open-source LLM repositories, spurring a wave of region-tuned adaptive AI solutions. Localization mandates that require in-country data processing propel demand for hybrid and edge deployments. Private-sector enthusiasm is equally strong: telecom operators deploy adaptive AI to optimize 5G roll-outs, and e-commerce leaders integrate real-time recommendation agents calibrated to cultural nuance.

Europe, valued near EUR 60 billion with a 13% CAGR, differentiates on ethics and privacy. The EU AI Act’s risk tiering encourages providers to embed explainability dashboards, bias audits, and override switches. Germany channels industrial AI funding into adaptive maintenance platforms for automotive plants, while France concentrates on health-data-safe AI sandboxes. Vendor strategies increasingly bundle compliance toolkits to win tenders in the region.

Competitive Landscape

The market remains moderately fragmented yet capital intensive, with hyperscale cloud providers, diversified software giants, and chip manufacturers setting the competitive tempo. Google, Microsoft, Amazon, IBM, and OpenAI leverage multi-billion-dollar RandD budgets and global data-center footprints to deliver full-stack adaptive AI ecosystems. Nvidia supplies an estimated 80% of AI accelerators, though challenger chip startups target inference cost reductions with domain-specific architectures.

Strategic maneuvers concentrate on vertical integration and talent capture. “Reverse acquihires” allow leading firms to absorb niche expertise—as when Amazon onboarded conversational-AI engineers from Adept AI—without the liabilities of full mergers. Partnerships between platform vendors and ERP providers embed adaptive agents directly into finance, HR, and supply-chain workflows, expanding addressable revenue and raising switching costs.

White-space opportunities lie in low-latency edge inference, industry-specific compliance overlays, and federated learning middleware that reconvenes insights across siloed data. Regional champions in Asia-Pacific develop localized agent frameworks attuned to vernacular languages and regulatory norms. Incumbent giants that open-source model weights under permissive licenses bolster community trust and stimulate third-party innovation.

Adaptive AI Industry Leaders

Microsoft

Google Cloud

Amazon Web Services

Nvidia

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: IBM and Oracle broadened their alliance to run watsonx multi-agent workflows on Oracle Cloud Infrastructure, unifying data, analytics, and AI pipelines.

- January 2025: Microsoft earmarked USD 80 billion for next-generation AI data centers to scale training and inference capacity worldwide.

- December 2024: OpenAI forecast 2025 revenue of USD 11.6 billion, citing surging demand for ChatGPT subscriptions and API calls.

- October 2024: IBM released Granite 3.0 models and expanded watsonx on AWS and Nvidia platforms under Apache 2.0 licensing.

Global Adaptive AI Market Report Scope

Adaptive AI is a form of AI that learns, adapts, and improves as it encounters changes, both in data and the environment. Adaptive AI uses evolutionary algorithms to optimize AI models, select features, and tune hyperparameters, enhancing the system's adaptability.

The adaptive AI market is segmented by component (platform, services), by deployment (cloud, on-premises), by end-users (BFSI, retail and e-commerce, healthcare, media and entertainment, manufacturing, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Platform |

| Services |

| Cloud |

| On-Premises |

| Hybrid / Edge |

| BFSI |

| Retail and E-commerce |

| Healthcare and Life Sciences |

| Manufacturing |

| Telecom and Media |

| Government and Defense |

| Others |

| Real-time Analytics |

| Personalised Recommendations |

| Fraud and Risk Detection |

| Autonomous Systems |

| Predictive Maintenance |

| Conversational Agents |

| Others |

| Machine Learning |

| Reinforcement Learning |

| Generative AI |

| Agentic AI |

| AutoML |

| Natural Language Processing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Platform | ||

| Services | |||

| By Deployment Model | Cloud | ||

| On-Premises | |||

| Hybrid / Edge | |||

| By End-user Industry | BFSI | ||

| Retail and E-commerce | |||

| Healthcare and Life Sciences | |||

| Manufacturing | |||

| Telecom and Media | |||

| Government and Defense | |||

| Others | |||

| By Application | Real-time Analytics | ||

| Personalised Recommendations | |||

| Fraud and Risk Detection | |||

| Autonomous Systems | |||

| Predictive Maintenance | |||

| Conversational Agents | |||

| Others | |||

| By Technology | Machine Learning | ||

| Reinforcement Learning | |||

| Generative AI | |||

| Agentic AI | |||

| AutoML | |||

| Natural Language Processing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the adaptive AI market?

The adaptive AI market is valued at USD 3.51 billion in 2026.

How fast will the adaptive AI market grow by 2031?

It is projected to register a 39.85% CAGR and reach USD 18.77 billion by 2031.

Which component segment dominates revenue today?

Platform offerings hold 57.55% of 2025 revenue, reflecting enterprises’ preference for integrated development and deployment suites.

Why are hybrid deployments gaining traction despite cloud dominance?

Hybrid models help control escalating cloud inference costs and satisfy data-sovereignty rules while still using cloud GPU clusters for heavy training workloads.

Which end-user vertical will grow fastest through 2031?

Healthcare and life sciences are expected to expand at a 44.20% CAGR, propelled by autonomous diagnostics and personalized treatment engines.

Page last updated on: