Cognitive Assessment And Training Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

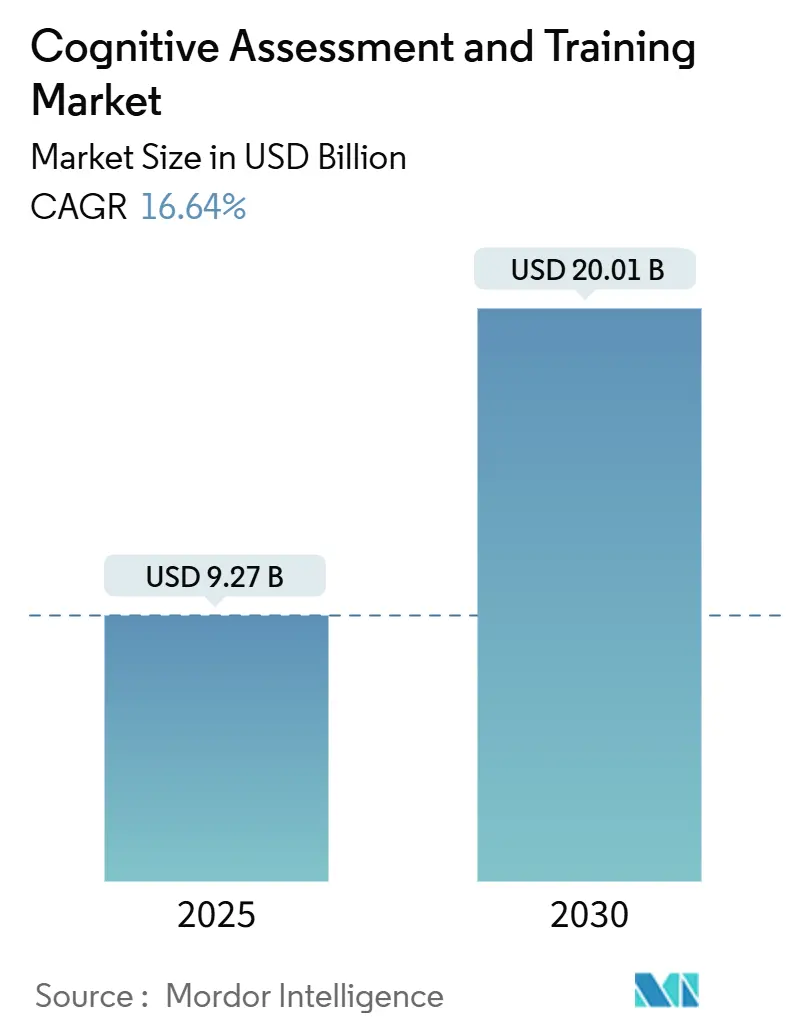

| Market Size (2025) | USD 9.27 Billion |

| Market Size (2030) | USD 20.01 Billion |

| Growth Rate (2025 - 2030) | 16.64% CAGR |

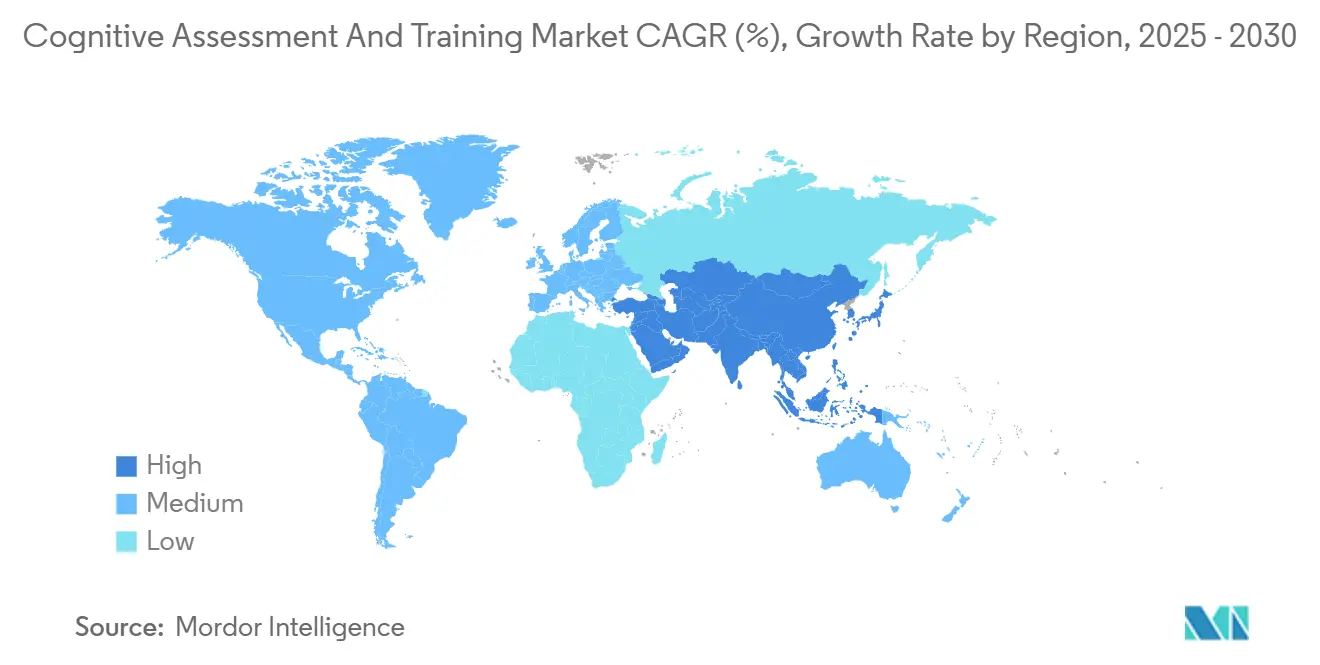

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

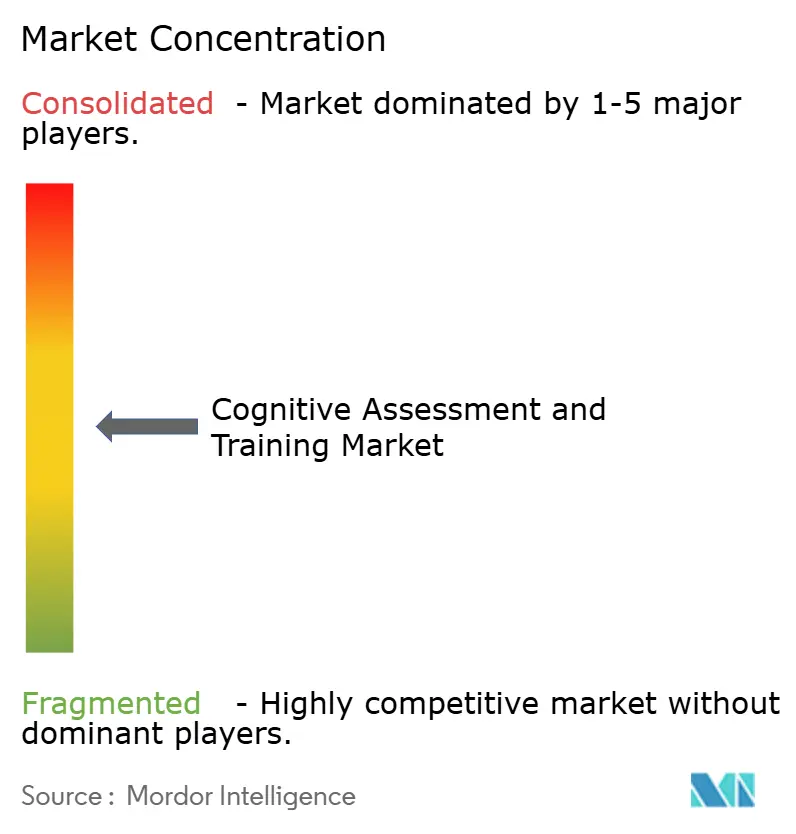

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cognitive Assessment And Training Market Analysis by Mordor Intelligence

The cognitive assessment and training market size stands at USD 9.27 billion in 2025 and is forecast to reach USD 20.01 billion by 2030, supported by a 16.64% compound annual growth rate (CAGR). This rapid scale-up roots itself in growing life expectancy, a widening prevalence of dementia and mild cognitive impairment, and steady integration of AI-enabled screening tools into routine clinical and corporate workflows. Health systems are adopting computer-based tests as first-line triage instruments, while employers fold evidence-backed brain-fitness modules into wellness strategies to curb productivity losses. Regulatory acceptance of Class II computerized cognitive assessment aids and the emergence of specific reimbursement codes are lowering adoption barriers, and venture funding continues to back specialized start-ups that target speech analytics or EEG-based biomarkers. At the same time, data-privacy mandates and algorithmic-bias debates are pushing providers to embed encryption, consent management, and inclusive validation protocols from day one.

Key Report Takeaways

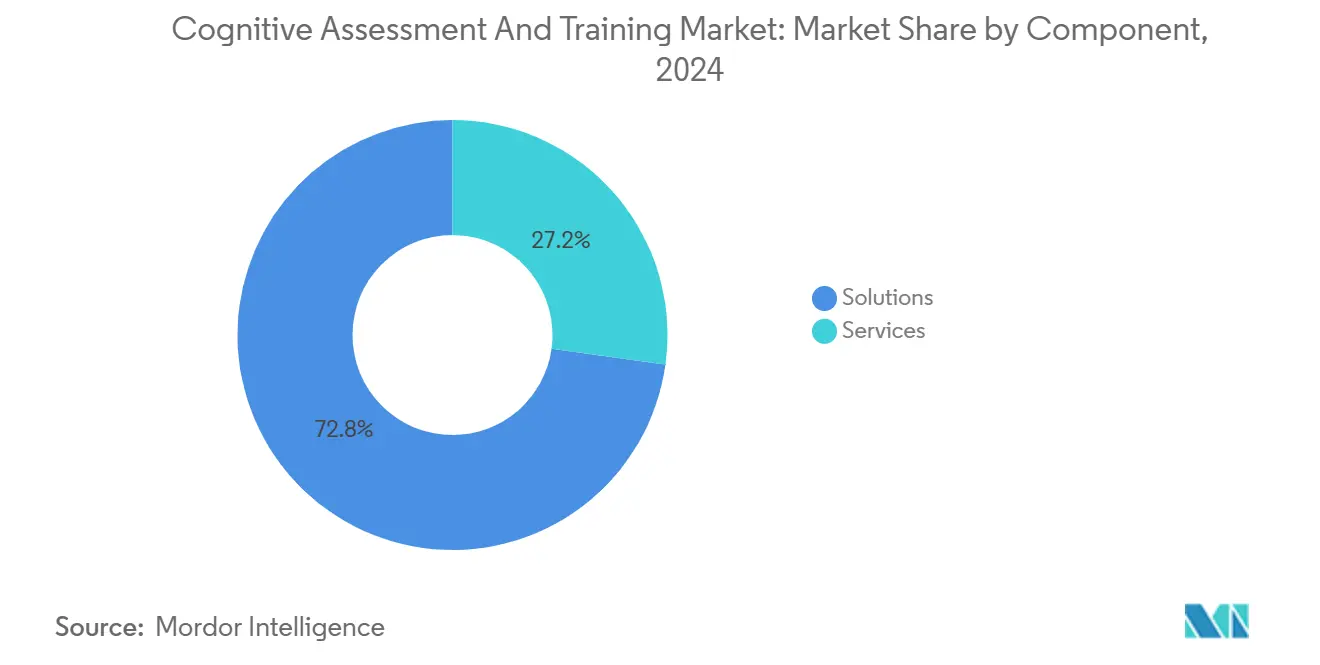

- By component, solutions held 72.8% of the cognitive assessment and training market share in 2024, whereas services are projected to grow at an 18.12% CAGR through 2030.

- By application, clinical trials accounted for 34.2% of the cognitive assessment and training market size in 2024, while corporate workforce training is advancing at a 19.36% CAGR to 2030.

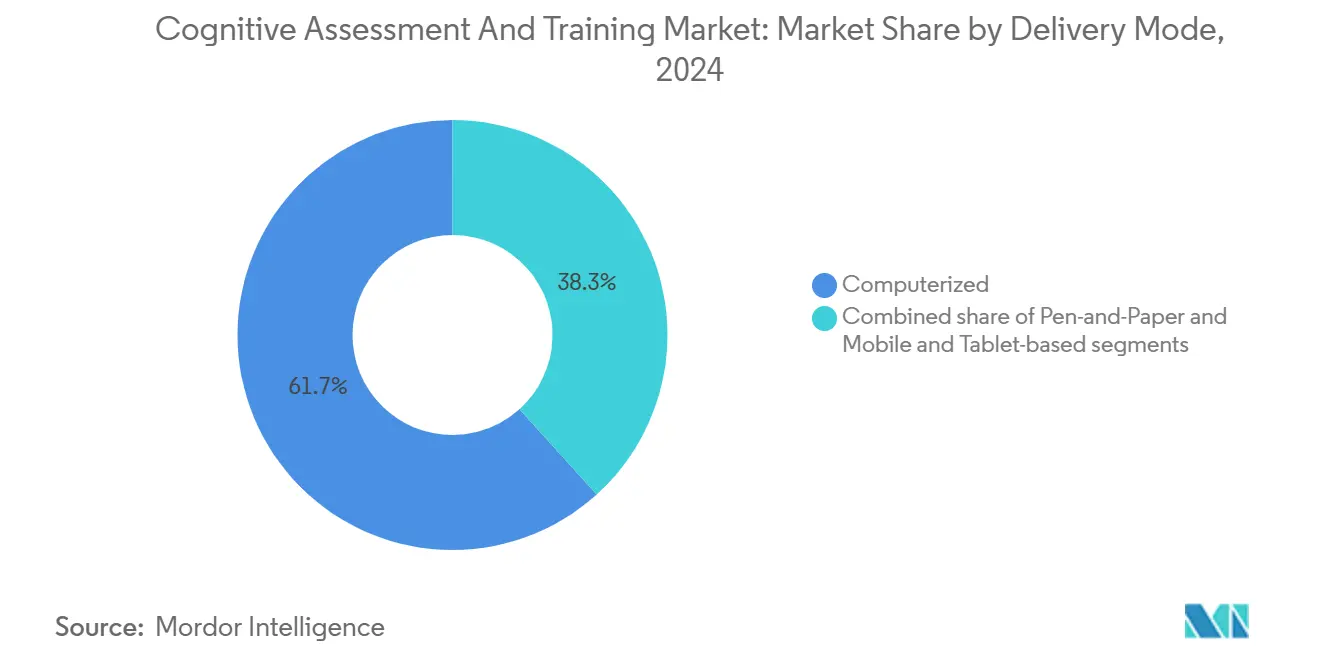

- By delivery mode, computerized platforms captured 61.7% revenue share in 2024; mobile and tablet-based delivery is forecast to expand at a 17.92% CAGR between 2025-2030.

- By end-user, healthcare and pharmaceutical entities held 44.7% of the cognitive assessment and training market size in 2024, yet corporate users exhibit the highest CAGR at 18.86% over the projection window.

- By geography, North America led with 42.5% market share in 2024, while Asia-Pacific is set to record the fastest 18.47% CAGR through 2030.

Global Cognitive Assessment And Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of neurocognitive disorders | +3.2% | Global; strongest in aging economies of North America, Europe, Japan | Long term (≥ 4 years) |

| Growing adoption of digital health & tele-medicine integrations | +2.8% | Global; early scale-up in North America and Europe | Medium term (2-4 years) |

| Heightened corporate wellness spending on cognitive programs | +2.1% | North America and Europe; accelerating in Asia-Pacific | Medium term (2-4 years) |

| Increased use of computerized tests in CNS clinical trials | +1.9% | Global; led by US, EU, Japan | Short term (≤ 2 years) |

| AI-driven speech analytics for passive home-based assessment | +1.7% | North America, Europe; pilot rollouts in urban APAC | Medium term (2-4 years) |

| Gamified training aimed at aging populations in emerging markets | +1.5% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Neurocognitive Disorders

The global dementia population is expected to triple by 2050, prompting governments and health insurers to favor proactive screening over costly late-stage care, an outlook that directly fuels the cognitive assessment and training market[1]World Health Organization, “Dementia Fact Sheet,” who.int. Pharmaceutical sponsors are embedding digital cognitive endpoints in neurology pipelines to accelerate go-no-go decisions, evidenced by a seven-country trial evaluating ketogenic nutrition for mild cognitive impairment that relies on tablet-based test batteries. Clinical demand is mirrored in emerging markets where incidence curves now match Western trends, widening the addressable user base. Payers recognize that every year of undetected impairment escalates lifetime treatment outlays, nudging policy toward routine cognitive check-ups. This epidemiological swell therefore anchors long-range growth.

Growing Adoption of Digital Health & Tele-Medicine Integrations

Pandemic-era tele-care has normalized remote neurocognitive screening, and cross-platform tools now plug directly into EHRs, giving providers real-time dashboards. Linus Health’s FDA-listed Anywhere for Health Systems™ illustrates the shift, enabling 91% sensitivity for mild cognitive impairment via an iPad camera test that physicians can prescribe asynchronously. The US Centers for Medicare & Medicaid Services has published HCPCS codes GMBT1-3 to reimburse digital mental-health treatment, improving billing clarity. Comparable frameworks are surfacing in Europe’s DiGA catalog and Japan’s digital-device sandbox, shortening sales cycles. These policies materially lift near-term uptake.

Heightened Corporate Wellness Spending on Cognitive Programs

Productivity losses tied to cognitive lapses cost enterprises billions each year; firms therefore allocate wellness budgets toward validated brain-fitness modules. Since its October 2024 launch, the Business Collaborative for Brain Health has enrolled over 420 companies that benchmark employees on a Brain Health Best Practice Score[2]Centers for Disease Control and Prevention, “Promising Practice: Business Collaborative for Brain Health,” cdc.gov. Training vendors reply with SaaS dashboards tracking memory span, decision speed, and stress physiology, packaging outcome data for HR reporting. Gamified programs such as NeeuroFIT have expanded from pilot workshops to full-scale rollouts for finance and tech employers. Evidence that targeted exercises raise executive function and lower burnout cements corporate demand, positioning workplace channels as the fastest-growing revenue lane for the cognitive assessment and training market.

Increased Use of Computerized Tests in CNS Clinical Trials

Regulators now treat digital cognitive endpoints as reliable surrogates for early-stage neurological drugs, reducing site burden and sample-size requirements. Cambridge Cognition’s contract for Actinogen’s XanaMIA Alzheimer’s trial bundles eCOA, high-frequency assessments, and automated quality checks into a single platform. The US FDA has codified these modules under 21 CFR 882.1470, giving sponsors a clear predicate device class. In parallel, blockchain-secured audit trails strengthen data integrity for decentralized trial designs. Clinical-development teams consequently view computerized batteries as the new gold standard, sustaining double-digit demand growth.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement for cognitive assessment solutions | -2.4% | Global; acute in emerging markets and private systems | Medium term (2-4 years) |

| Data-privacy & cybersecurity concerns over sensitive results | -1.8% | Global; pronounced in GDPR jurisdictions, growing in Asia | Short term (≤ 2 years) |

| Algorithmic bias reducing validity across demographic groups | -1.5% | Global; larger effect in diverse populations | Medium term (2-4 years) |

| Long-term user engagement drop-offs in training programs | -1.3% | Global; notable in consumer and corporate apps | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement for Cognitive Assessment Solutions

Despite clinical utility, insurers still classify many digital assessments as wellness rather than medical devices, curbing coverage breadth. Qualitative interviews with US payers confirm that proof thresholds mirror pharmaceutical trials, with randomized-controlled data often demanded before payment approval[3]Ainhoa Gomez Lumbreras et al., “Insurance Coverage for Digital Therapeutics: A Qualitative Study of US Payer Perspectives,” jmcp.org. Commercial plans like UnitedHealthcare and Cigna reimburse cognitive rehabilitation only for stroke or severe TBI, excluding mild impairment and general brain-fitness modules, thereby slowing rollouts. CMS’s new digital-therapy codes are a positive signal yet remain tied to formal FDA clearance, meaning many consumer-oriented tools still face out-of-pocket hurdles.

Data-Privacy and Cybersecurity Concerns Over Sensitive Results

Neurological scores, speech files, and EEG traces are classified as highly sensitive health data that require stringent protection measures. Recent data breaches affecting 31 million US patients have increased public concerns about data security and privacy vulnerabilities in healthcare systems. Research indicates that 70% of adults oppose the reuse of cognitive data without explicit consent, highlighting growing awareness of data privacy rights. Countries including India and Sri Lanka have implemented strict regulations with substantial financial penalties for non-compliance, which has increased vendor compliance costs and operational complexity. Although advanced security measures like encryption and zero-knowledge proofs provide robust data protection, persistent concerns about potential data misuse continue to limit adoption among privacy-conscious consumers, particularly in healthcare and research applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Remain Core While Services Accelerate

In 2024, solutions dominated the cognitive assessment and training market, accounting for 72.8% of the revenue. It highlights the importance of validated test batteries, analytics engines, and compliance repositories. These solutions are integral to ensuring accurate assessments and streamlined operations, particularly in the healthcare and pharmaceutical sectors. Typically, hospitals and pharmaceutical sponsors begin by acquiring assessment modules, which form the foundation of their cognitive evaluation processes. They then enhance these capabilities by adding consultancy or integration packages to address specific operational needs. The market size for these solutions reached USD 6.76 billion in 2024, with projections indicating steady growth. This growth is fueled by advancements in AI algorithms, which enhance the precision and efficiency of assessments, and the increasing adoption of multi-modal data fusion, which enables comprehensive and holistic evaluations.

While currently smaller, the services segment is poised for rapid growth, projected at an 18.12% CAGR. Providers are increasingly being approached for specialized needs like workflow mapping, linguistic localization, and clinical-trial study design areas that demand domain expertise over mere product licenses. These services cater to the growing complexity of cognitive assessment requirements, ensuring tailored solutions for diverse applications. Furthermore, as national data-protection acts proliferate, there is a heightened demand for security audits and compliance attestations. This demand is driven by the need to safeguard sensitive data and adhere to stringent regulatory standards, further propelling the growth of the services segment. The combination of these factors positions the services segment as a critical growth driver within the cognitive assessment and training market.

By Application: Clinical Trials Lead; Corporate Training Accelerates

In 2024, clinical trials secured a 34.2% share of the cognitive assessment and training market, as sponsors shifted from subjective rating scales to high-frequency computerized endpoints. This transition reflects the growing demand for objective and reliable data in clinical research. With a robust pipeline for Alzheimer’s and Parkinson’s compounds, test volumes are set to grow steadily, driven by the increasing prevalence of neurodegenerative diseases and the need for innovative treatments. Due to decentralized study models, which enhance patient participation and streamline data collection, the market size for cognitive assessments tied to trials is forecasted to see low-double-digit growth rates over the coming years.

On the other hand, corporate training is surging at a 19.36% CAGR. Executives increasingly recognize that enhanced cognition accelerates decision-making and fosters innovation, making cognitive training a strategic investment. HR budgets are now prioritizing modules that assess working memory, cognitive flexibility, and stress resilience, frequently incorporating these scores into annual performance reviews to align individual development with organizational goals. Successful trials at professional services firms have led to widespread adoption across the sector, with tangible ROI evidence, like reduced error rates and improved productivity, ensuring continued funding. Additionally, the integration of cognitive training into corporate wellness programs highlights its growing importance in fostering a resilient and high-performing workforce.

By Delivery Mode: Computerized Dominance Faces Mobile Surge

In 2024, desktop-based, clinic-controlled environments commanded a dominant 61.7% share of total revenues. Neuropsychologists prioritize calibrated screens, stable latency, and secure hospital networks for baseline assessments. These environments provide the reliability and precision required for accurate diagnostics, making them the preferred choice for many clinical professionals. The controlled settings of clinics ensure consistency in testing conditions, which is critical for obtaining reliable results. However, the growing demand for convenience and accessibility is gradually shifting patient preferences toward mobile solutions. This shift is driven by the increasing adoption of digital technologies and the need for more flexible assessment options.

As smartphone penetration surpasses 80% in numerous economies, mobile and tablet deployments are projected to grow at a robust 17.92% CAGR. These devices offer portability and ease of use, making them an attractive alternative for both patients and clinicians. A recent study highlighted that an Android n-back game identified mild impairments with over 80% specificity, bolstering clinical trust in handheld assessments. It demonstrates the potential of mobile platforms to deliver reliable results comparable to traditional methods. While pen-and-paper methods remain in use at low-resource clinics and during insurance audits, their market share is expected to decline annually as digital solutions continue to gain traction. The transition to digital tools reflects the broader trend of technological integration within the healthcare sector.

By End-User Industry: Healthcare Anchors; Corporate Demand Blossoms

In 2024, healthcare and pharmaceutical clients accounted for 44.7% of revenues, leveraging computerized cognition indices for disorder diagnosis, treatment monitoring, and clinical-trial cohort stratification. These tools have become integral in improving patient outcomes and streamlining clinical processes. Additionally, payer reforms that now reimburse FDA-approved digital therapeutics, such as Rejoyn, have significantly influenced budget allocations, further driving the adoption of these advanced solutions within the healthcare and pharmaceutical sectors.

Corporates have emerged as the most dynamic buyer segment, achieving an impressive 18.86% CAGR. Industries like banking, aviation, and technology are increasingly implementing quarterly brain-health assessments to mitigate human-error risks and enhance managerial efficiency. Education ministries and universities are also adopting similar tools to facilitate the early detection of learning disabilities, ensuring timely interventions. Meanwhile, defense agencies are piloting vestibular-balance games to improve soldier readiness, showcasing the diverse applications of these technologies across various sectors.

Geography Analysis

North America retains its prime position, buoyed by Medicare’s draft payment schedule for digital mental-health devices and successive FDA nods for AI-enabled therapeutics such as DaylightRX for generalized anxiety disorder. Large employers, exemplified by the 420-member Business Collaborative for Brain Health, institutionalize brain-fitness check-ups as part of annual wellness benefits, guaranteeing volume streams. Yet forward growth moderates to the low teens as the early-adopter pool approaches saturation in hospital networks and Fortune 500 firms.

Asia-Pacific leads with an impressive 18.47% CAGR, fueled by an aging demographic in China and Japan, alongside new state investments in digital care. Regulatory bodies, from Singapore's HSA to Australia's TGA, are streamlining software-as-a-medical-device approvals by aligning with IMDRF standards, which have significantly reduced approval timelines. Vendors, eager to secure contracts with public insurers, are making localization investments, incorporating Mandarin speech corpora, Hindi interface text, and culturally relevant game narratives. These efforts enhance user engagement and address the diverse linguistic and cultural needs of the region, giving vendors a competitive edge.

Europe takes a more measured approach. Germany's DiGA program supports nationwide rollouts, providing a structured framework for digital health applications to gain reimbursement. Meanwhile, France and Belgium are piloting similar fast-track reimbursement catalogs to evaluate their feasibility and impact. The European Health Data Space initiative promotes cross-border data sharing, potentially paving the way for unified cognitive score benchmarks across the EU. This initiative aims to enhance collaboration and standardization in healthcare data usage across member states. While GDPR mandates a privacy-centric design, startups utilizing advanced technologies like homomorphic encryption find themselves in a favorable position. These startups meet stringent compliance requirements and qualify for hospital tenders, achieving a balance between regulatory adherence and scalability, which is crucial for long-term growth in the market.

Competitive Landscape

Industry structure is moderately fragmented: the top five companies collectively control a significant share of 2024 revenue, with the remainder split among over 150 niche suppliers. Consolidation is brisk; NeuroFlow’s acquisition of Owl produced a 17-million-life measurement platform, showcasing a vertical-integration play that marries assessment, analytics, and engagement. Linus Health followed by purchasing Together Senior Health, adding a movement-based intervention layer to its diagnostic engine. Larger incumbents prize FDA clearance speed and data-lake depth, often absorbing AI boutiques to fortify those assets.

White-space still abounds in culturally inclusive datasets and passive monitoring verticals. Firefly Neuroscience’s EEG-derived brain-age biomarker exemplifies frontier R&D that could redefine baselining norms. Speech analytics specialists harness transformer models fine-tuned on multilingual corpora to sidestep bias pitfalls. Competitive levers, therefore, encompass regulatory track record, accuracy validated in peer-reviewed studies, and breadth of cloud APIs enabling third-party integrations.

Strategic alliances are equally common: Thread and Cogstate co-developed no-code eCOA templates to capture CNS endpoints, cutting trial set-up times for biotech clients. Tech giants eye adjacent value; Verint’s purchase of Cogito aims to infuse live call-center analytics with cognitive scoring, hinting at cross-industry diffusion beyond healthcare. With several SPAC-funded digital therapeutics firms re-evaluating burn rates, further mergers appear imminent.

Cognitive Assessment And Training Industry Leaders

Cambridge Cognition Holdings Plc

Cogstate Ltd

Pearson Plc

Lumos Labs Inc (Lumosity)

Posit Science Corp (BrainHQ)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Linus Health launched Anywhere for Health Systems™, an FDA-listed remote cognitive assessment that integrates across leading EHRs.

- March 2025: April Health and Wysa have merged, forming a unified AI-centric platform for mental health. This merger aims to integrate advanced artificial intelligence capabilities with mental health solutions, enhancing accessibility and personalized care for users

- January 2025: Firefly Neuroscience, leveraging its FDA-approved BNA™ EEG platform, has introduced a novel brain-age biomarker. This innovation is designed to provide deeper insights into brain health and aging, offering potential applications in both clinical and research settings.

- January 2025: Cambridge Cognition broadened its collaboration with Actinogen, focusing on the Phase 2b/3 XanaMIA trial for Alzheimer's. This expanded partnership seeks to advance the development of cognitive assessment tools and support the evaluation of Actinogen's therapeutic interventions for Alzheimer's disease.

Global Cognitive Assessment And Training Market Report Scope

| Solutions | Assessment Tools & Modules |

| Data Analysis & Reporting | |

| Data Storage & Compliance | |

| Others | |

| Services | Training & Technical Support |

| Strategic Consulting & Study Design |

| Clinical Trials |

| Corporate/Workforce Training |

| Academic Research |

| Others |

| Pen-and-Paper |

| Computerized |

| Mobile & Tablet-based |

| Healthcare and Pharmaceutical |

| Education |

| Corporate |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Component | Solutions | Assessment Tools & Modules |

| Data Analysis & Reporting | ||

| Data Storage & Compliance | ||

| Others | ||

| Services | Training & Technical Support | |

| Strategic Consulting & Study Design | ||

| By Application | Clinical Trials | |

| Corporate/Workforce Training | ||

| Academic Research | ||

| Others | ||

| By Delivery Mode | Pen-and-Paper | |

| Computerized | ||

| Mobile & Tablet-based | ||

| By End-User Industry | Healthcare and Pharmaceutical | |

| Education | ||

| Corporate | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current revenue value of the cognitive assessment and training market?

The market generate USD 9.27 billion in 2025 and is projected to reach USD 20.01 billion by 2030.

Which application generates the largest spending?

Clinical trials account for 34.2% of 2024 revenue, driven by the widespread use of computerized cognitive endpoints.

Which delivery mode is expanding fastest?

Mobile and tablet-based platforms are growing at a 17.92% CAGR as patients prefer on-the-go testing.

Why are employers investing in brain-health programs?

Evidence links improved cognition with higher productivity and lower error rates, motivating companies to fund structured training.

Which region will add the most new users by 2030?

Asia-Pacific, propelled by demographic aging and supportive digital-health policies, is forecast to log an 18.47% CAGR.

What hinders wider reimbursement?

Many payers still classify digital assessments as wellness tools, requiring robust clinical evidence before coverage is approved.

Page last updated on: