AI Tutors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

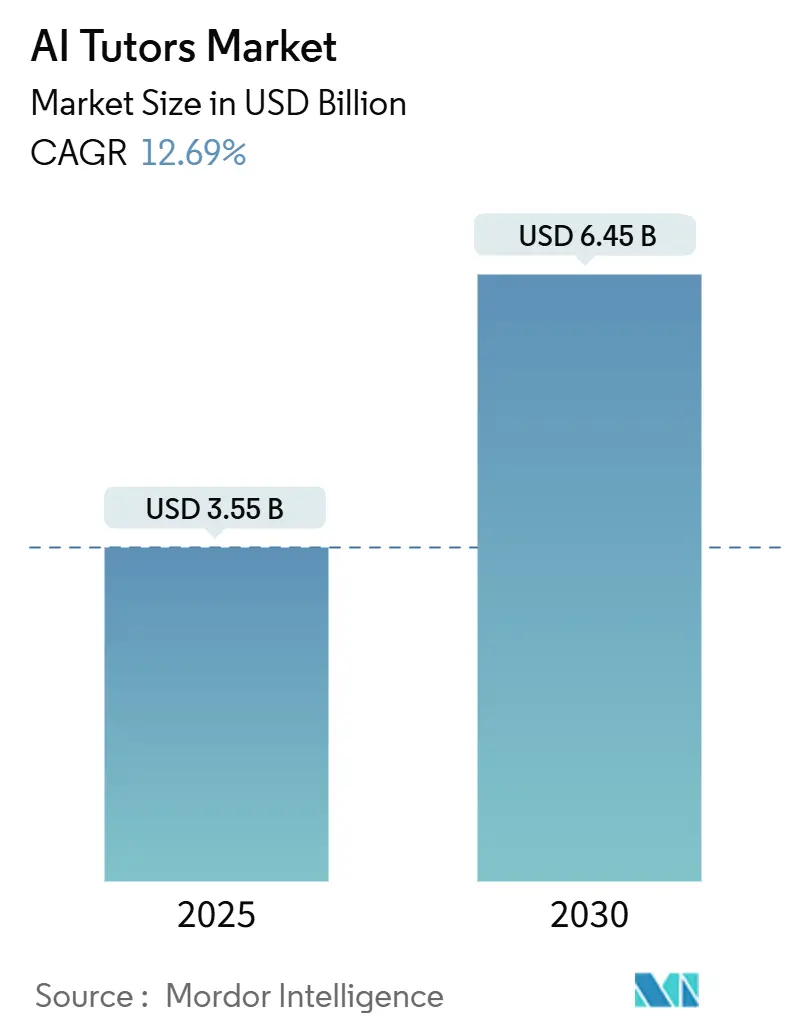

| Market Size (2025) | USD 3.55 Billion |

| Market Size (2030) | USD 6.45 Billion |

| Growth Rate (2025 - 2030) | 12.69% CAGR |

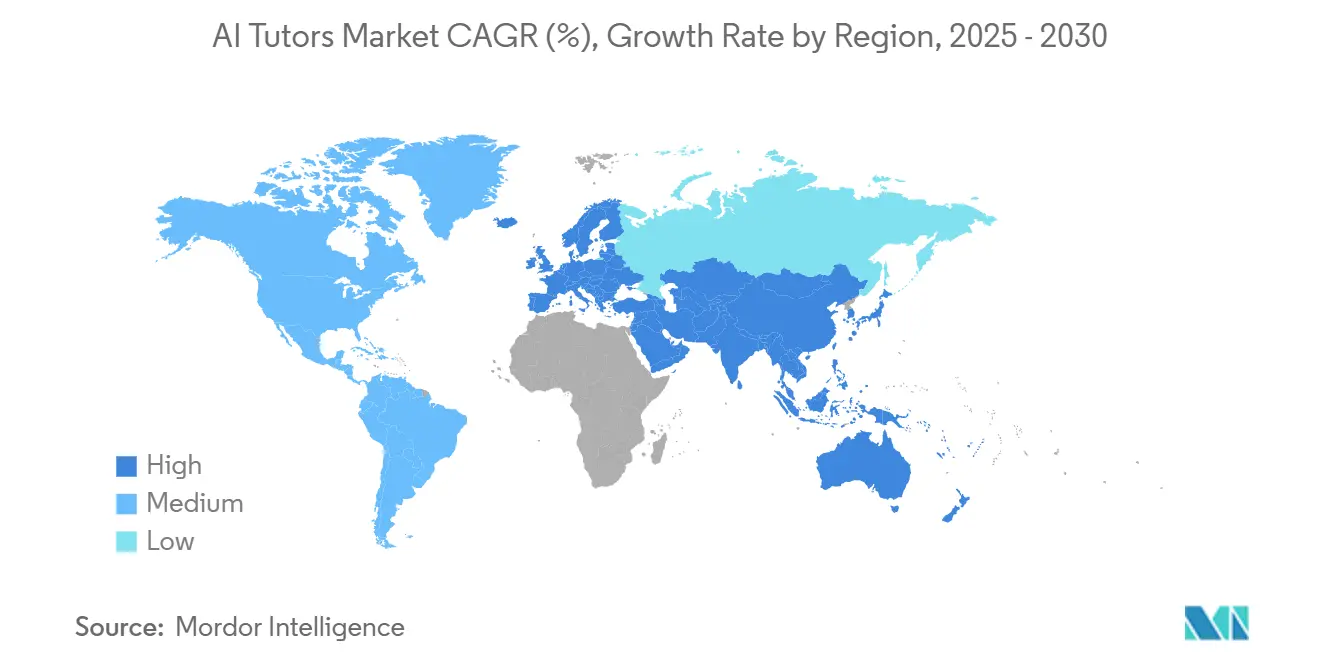

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Tutors Market Analysis by Mordor Intelligence

The AI Tutors Market size is estimated at USD 3.55 billion in 2025, and is expected to reach USD 6.45 billion by 2030, at a CAGR of 12.69% during the forecast period (2025-2030).

Rising demand for personalized learning, government-backed digital education initiatives, and corporate upskilling mandates collectively accelerate adoption. Rapid improvements in generative AI models have transformed AI tutors from basic question-answer software into context-aware instructional companions capable of sustaining dialogue that mirrors human tutoring sessions. Regulatory clarity in regions such as North America encourages institutional spending, while smartphone penetration above 85% in the Asia Pacific extends reach to first-time digital learners. Competitive intensity remains moderate as large education publishers partner with AI start-ups to secure content-algorithm synergies; however, data privacy compliance costs are eliminating small-scale suppliers. Alongside core academic applications, enterprises are piloting AI tutors for real-time professional reskilling tied to automation-driven job redesign.

Key Report Takeaways

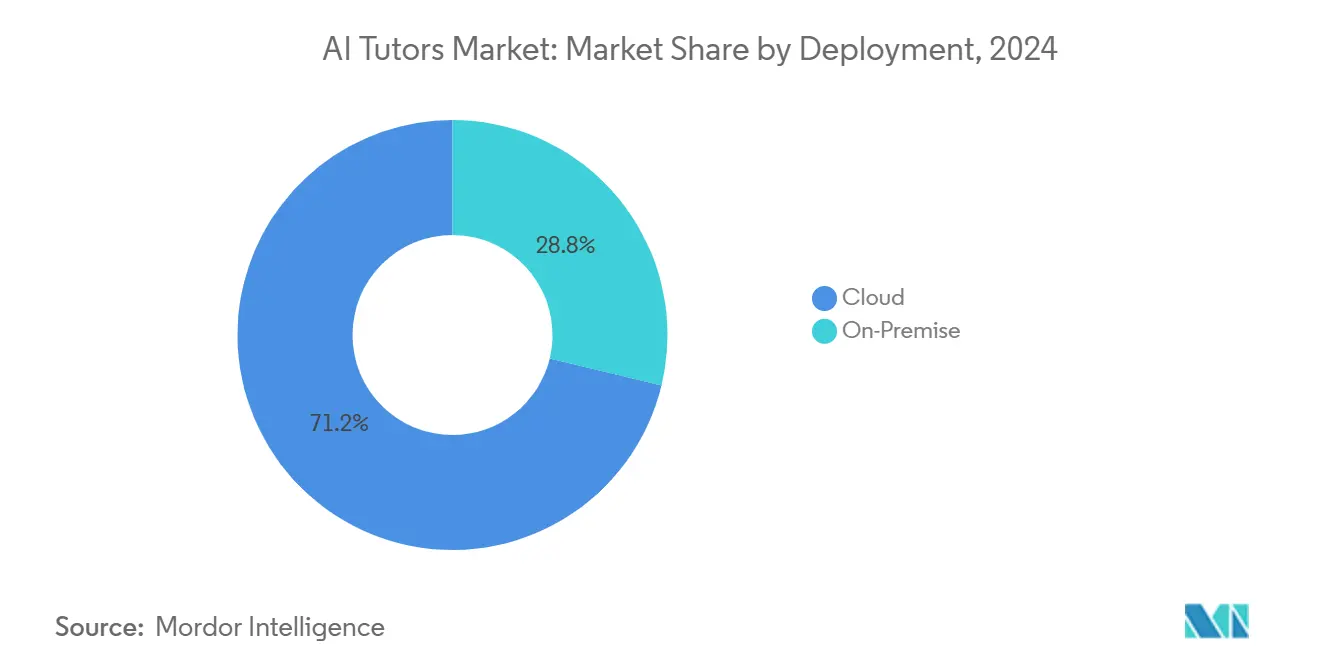

- By deployment, cloud solutions held 71.22% of the AI Tutor market share in 2024 and are forecasted to expand at a 11.3% CAGR through 2030.

- By end user, K-12 institutions accounted for 45.62% of the AI Tutors market size in 2024, while professional learning is projected to advance at a 14.65% CAGR through 2030.

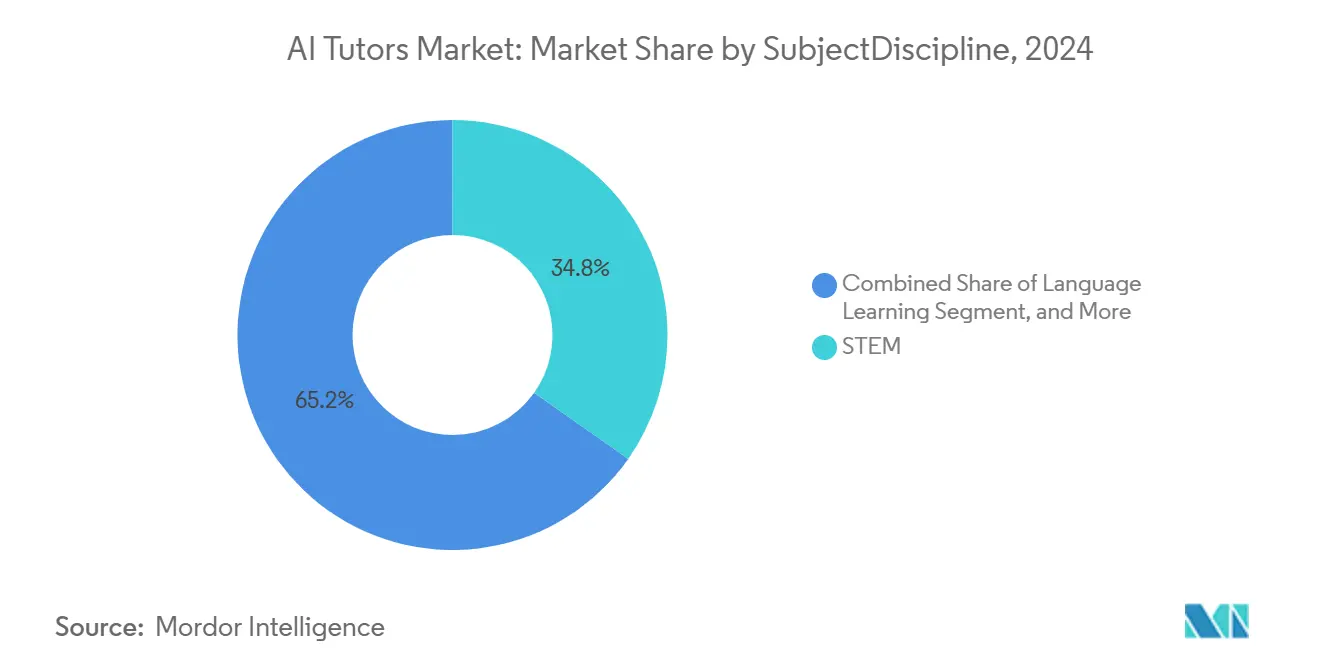

- By subject, STEM captured 34.78% of the AI Tutors market revenue in 2024; language learning is growing fastest at a 14.38% CAGR through 2030.

- By technology interface, chatbots led with 55.11% share of the AI Tutors market in 2024, whereas avatar-based tutors are set to rise at a 12.78% CAGR through 2030.

- By geography, North America accounted for 36.22% of the 2024 revenue in the AI Tutors market, while the Asia Pacific is projected to expand at a 14.88% CAGR between 2025 and 2030.

Global AI Tutors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Advancements in Generative AI Models Enabling Conversational Learning | +3.2% | Global, with early adoption in North America and APAC | Short term (≤ 2 years) |

| Increasing Demand for Personalized Learning Paths in K-12 Education | +2.8% | North America and Europe core, expanding to APAC | Medium term (2-4 years) |

| Government-Led Digital Education Initiatives and Funding Programs | +2.1% | APAC and Europe primary, selective North America programs | Medium term (2-4 years) |

| Corporate Upskilling Mandates in Response to Automation | +1.9% | Global, concentrated in developed economies | Short term (≤ 2 years) |

| Growing Smartphone and Internet Penetration in Emerging Economies | +1.6% | APAC, MEA, and Latin America focus | Long term (≥ 4 years) |

| Integration of AI Tutors with Learning Management Systems (LMS) | +1.3% | Global, institutional adoption priority | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Advancements in Generative AI

Cutting-edge language models now sustain subject-specific conversations that mirror Socratic tutoring, delivering 40% comprehension gains over legacy e-learning tools. OpenAI’s ChatGPT Edu offers curriculum-aligned prompt templates and institution-level safety controls, enabling real-time fact-checked responses and automated feedback loops that adapt to individual cognitive patterns. Vendors embedding retrieval-augmented generation reduce hallucination risk, which reassures administrators about academic integrity. Cost savings emerge as one teacher supervises multiple concurrent AI-supported study groups without compromising outcome metrics.

Increasing Demand for Personalized Learning Paths in K-12

School districts confront persistent achievement gaps and see adaptive AI as a non-stigmatizing means of differentiated instruction. Carnegie Learning’s MATHia engine dynamically adjusts problem difficulty, generating 25% faster mastery than textbook methods. AI tutors automate formative assessment, freeing teachers for project-based learning. Parents increasingly benchmark schools on measurable progress analytics, creating competitive pressure that favors AI deployments.

Government-Led Digital Education Initiatives

National funding pipelines such as Germany’s Digitalpakt 2.0 earmark EUR 6.5 billion (USD 7.3 billion) for AI-enabled classroom tools, while Canada’s CanCode program subsidizes intelligent tutoring for underserved learners.[1] Innovation, Science and Economic Development Canada, “CanCode Program Update 2024,” canada.ca India’s National Education Policy mandates AI integration by 2030, spawning a domestic market exceeding USD 2.8 billion. Procurement guidelines increasingly weight proven learning-gain data, compelling vendors to publish rigorous efficacy studies.

Corporate Upskilling Mandates in Response to Automation

McKinsey finds 87% of firms grappling with skill gaps as AI permeates workflows, pushing training budgets toward personalized, just-in-time platforms. Enterprises leverage AI tutors to shorten certification cycles and embed practice simulations within everyday productivity apps, demonstrating direct ROI through reduced onboarding costs and higher employee retention.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data Privacy and Child Protection Regulations Raising Compliance Costs | -1.8% | Global, strictest in Europe and North America | Short term (≤ 2 years) |

| Limited Availability of High-Quality Local Language Content | -1.4% | Emerging markets in APAC, MEA, and Latin America | Long term (≥ 4 years) |

| Teacher and Parent Skepticism Toward AI-Driven Pedagogy | -1.1% | Global, most pronounced in traditional education systems | Medium term (2-4 years) |

| High Computing Costs for Real-Time Adaptive Feedback in Low-Income Regions | -0.9% | Sub-Saharan Africa, rural APAC, and Latin America | Long term (≥ |

| Source: Mordor Intelligence | |||

Data-Privacy and Child-Protection Compliance Costs

Updated COPPA rules require granular parental consent for behavioral data used in AI personalization, increasing onboarding friction and raising legal spend by 35% among K-12-focused vendors.[2]Federal Trade Commission, “COPPA Rule Review 2024,” ftc.gov European GDPR oversight forces data-minimization techniques such as federated learning, which add compute overhead and may dilute model accuracy. Compliance advantages larger incumbents with in-house counsel, intensifying consolidation.

Limited Availability of High-Quality Local-Language Content

English-centric datasets underpin most AI tutor models, leading to diminished accuracy in Hindi, Arabic, and Swahili contexts. UNESCO notes that localized content deficits perpetuate learning inequality, as smaller linguistic markets cannot justify translation economics. Providers now crowdsource open-license curricular materials and partner with regional publishers, yet coverage remains uneven across multi-language nations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Infrastructure Drives Scalability

Cloud-based platforms accounted for 71.22% of the AI Tutors market share in 2024, thanks to their elastic compute and seamless update cycles. Institutions favor managed services that offload maintenance and include built-in security certifications. The cloud portion of the AI Tutors market size is forecast to grow at 11.3% between 2025-2030 as rural bandwidth improves. On-premise installations appeal to entities with strict data-sovereignty rules, especially defense academies and public universities in jurisdictions mandating local storage. Vendors now offer hybrid models that park sensitive data on site while running inference in the cloud, an approach that balances privacy with continuous model improvement.

Momentum toward cloud delivery accelerates integration with learning-management systems and analytics dashboards, simplifying procurement decisions for IT-constrained schools. Major hyperscalers have launched education-specific compliance blueprints that shorten pilot-to-production timelines. As a result, total cost of ownership tilts decisively toward subscription models, and long-term contracts increasingly bundle AI tutor seats with collaboration software licenses.

By End User: Professional Learning Accelerates Fastest

K-12 settings held 45.62% of 2024 revenue, reflecting established device programs and standardized testing regimes. The professional-learning slice of the AI Tutors market size, however, is rising at 14.65% CAGR on the back of corporate reskilling imperatives linked to automation. Enterprises deploy internal AI tutors that map competency gaps to career-path frameworks, encouraging continuous self-directed learning. Universities adopt AI tutors for high-enrollment gateway courses, using analytics to flag at-risk students early.

Professional learners value time-flexible micro-modules, prompting vendors to integrate calendar-based nudges and voice interfaces for commute-time lessons. Certification providers embed adaptive practice within exam prep packages, reducing failure rates and thus boosting their brand reputation. The pivot toward lifelong learning positions AI tutors as core infrastructure for knowledge-intensive industries.

By Subject/Discipline: Language Learning Gains Momentum

STEM dominated 34.78% of 2024 revenue, consistent with AI’s strength in step-wise problem generation. Language learning is the breakout category, posting a 14.38% CAGR to 2030 as conversational engines mature. The AI Tutors market size attached to language applications benefits from natural language processing breakthroughs that enable real-time pronunciation feedback and cultural context prompts. Test-preparation platforms integrate AI tutors for personalized study plans, while arts and humanities remain niche due to complex evaluative benchmarks.

As avatar-led storytelling improves, humanities modules are expected to attract new users seeking narrative-driven exploration. Concurrently, interdisciplinary courses that merge coding with language or ethics use AI tutors to orchestrate cross-subject projects, expanding the addressable base beyond single-discipline silos.

By Technology Interface: Avatar Integration Transforms Engagement

Chatbots captured 55.11% share in 2024, favored for their low-bandwidth text exchanges. Yet avatar-based interfaces are on a 12.78% CAGR trajectory, leveraging facial expression and body-language cues to elevate learner motivation. In the AI Tutors market, voice-only agents are gaining in accessibility contexts, assisting visually impaired users. Mixed-reality tutors, though nascent, allow spatial visualization of complex topics such as molecular geometry and mechanical design.

Educators report higher completion rates when avatars personalize greetings and track emotional sentiment through sentiment analysis. Hardware costs and content-creation pipelines currently restrain immersive adoption, but falling headset prices are expected to remove barriers by 2027.

Geography Analysis

North America’s early-mover advantage stems from federal grants incentivizing digital-equity projects and high per-student technology spending. State-level procurement frameworks streamline vendor onboarding, creating predictable revenue pipelines for AI tutor suppliers. Institutions in the United States invest heavily in evidence-based solutions, spurring rigorous efficacy reporting and continuous product iterations.

Asia Pacific’s outsized growth reflects youthful demographics and public-sector commitments to AI-driven education transformation. National broadband missions in Indonesia and Vietnam lower access costs, while teacher-training schemes include AI literacy modules to ensure classroom integration. Private cram-school chains in China pioneer AI tutors for high-stakes exam prep, showcasing measurable score improvements that win parental trust.

Europe emphasizes GDPR alignment, driving demand for privacy-by-design architectures and local data centers. Public procurement often bundles AI tutoring with device leasing and teacher professional-development packages, ensuring holistic implementation. Latin America exhibits mixed progress: urban hubs in Brazil and Mexico adopt AI tutors for language acquisition, whereas rural connectivity hurdles persist. Africa’s e-learning ecosystems latch onto mobile-first AI tutors that operate on lightweight conversational channels, offering foundational literacy modules even on 3G networks.

Competitive Landscape

The AI tutors market remains moderately fragmented, with the top five players controlling roughly 30% of global revenue. Established names such as Carnegie Learning, Duolingo, and Squirrel AI compete alongside tech giants integrating tutoring into broader education suites. Strategic partnerships dominate: publishers license proprietary content to AI start-ups in exchange for adaptive-learning engines that modernize legacy catalogs. Mergers have accelerated since 2024 as compliance costs and data-security demands outstrip smaller vendors’ resources.

Technological differentiation hinges on proprietary language models fine-tuned for pedagogy, patented feedback loops, and integration APIs for school information systems. Investment trends favor cloud-agnostic architectures that minimize vendor lock-in for institutional buyers. Patent filings focused on adaptive-assessment algorithms rose significantly in 2024, reflecting a race to secure defensible IP positions.[3]United States Patent and Trademark Office, “Educational Technology Patent Trends 2024,” uspto.gov

Regulatory scrutiny over algorithmic bias pressures companies to publish audit methodologies; those that demonstrate transparent model-update governance gain procurement preference. Emerging disruptors court niche segments such as vocational trades or neurodiverse learner support with tailored datasets. Competitive intensity is expected to increase as hyperscalers bundle AI tutors within productivity subscriptions, potentially displacing stand-alone niche providers unless they secure unique content advantages.

AI Tutors Industry Leaders

Carnegie Learning, Inc.

Squirrel AI Learning Inc.

Century-Tech Ltd.

Querium Corporation

Alelo Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Microsoft launched the Elevate Washington program to equip every student and teacher in its home state with AI-powered learning tools, backed by the company’s new USD 4 billion Elevate fund.

- September 2025: Carnegie Learning’s high-impact math tutoring service was chosen as an Accelerate Evidence for Impact grantee, funding a randomized controlled trial during the 2025-26 school year.

- August 2025: OpenAI introduced a dedicated ChatGPT Education offering that lets colleges deploy GPT-5 campus-wide with expanded message limits, custom GPT creation and enterprise-grade privacy controls.

- July 2025: Microsoft pledged more than USD 4 billion in cash, cloud credits and training to help 20 million learners earn AI certificates through its new Elevate Academy initiative.

Global AI Tutors Market Report Scope

| Cloud |

| On-Premise |

| K-12 Schools |

| Higher Education Institutions |

| Professional Learners and Certification Seekers |

| Enterprises/Corporate Training |

| STEM |

| Language Learning |

| Test Preparation |

| Humanities and Arts |

| Chatbot-Based Tutors |

| Voice-Based Tutors |

| Avatar/AR Tutors |

| Mixed Reality and Immersive Tutors |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Deployment | Cloud | |

| On-Premise | ||

| By End User | K-12 Schools | |

| Higher Education Institutions | ||

| Professional Learners and Certification Seekers | ||

| Enterprises/Corporate Training | ||

| By Subject/Discipline | STEM | |

| Language Learning | ||

| Test Preparation | ||

| Humanities and Arts | ||

| By Technology Interface | Chatbot-Based Tutors | |

| Voice-Based Tutors | ||

| Avatar/AR Tutors | ||

| Mixed Reality and Immersive Tutors | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the AI Tutors market?

The AI Tutors market size stands at USD 3.55 billion in 2025.

How fast will the AI Tutors market grow through 2030?

Aggregate revenue is forecast to rise at a 12.69% CAGR, reaching USD 6.45 billion.

Which deployment model leads adoption of AI tutors?

Cloud platforms dominate, accounting for 71.22% of 2024 spending thanks to scalability and lower maintenance.

Which user group is expanding quickest in adopting AI tutors?

Professional learners and certification seekers are growing fastest at a 14.65% CAGR due to corporate reskilling demands.

Which region is expected to deliver the highest growth in AI tutor adoption?

Asia Pacific is projected to expand at a 14.88% CAGR, led by China and India’s policy-driven digitization efforts.

What is the biggest regulatory hurdle facing AI tutor providers?

Heightened data-privacy and child-protection rules particularly COPPA updates and GDPR enforcement elevate compliance costs and complexity.

Page last updated on: