Automated Machine Learning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

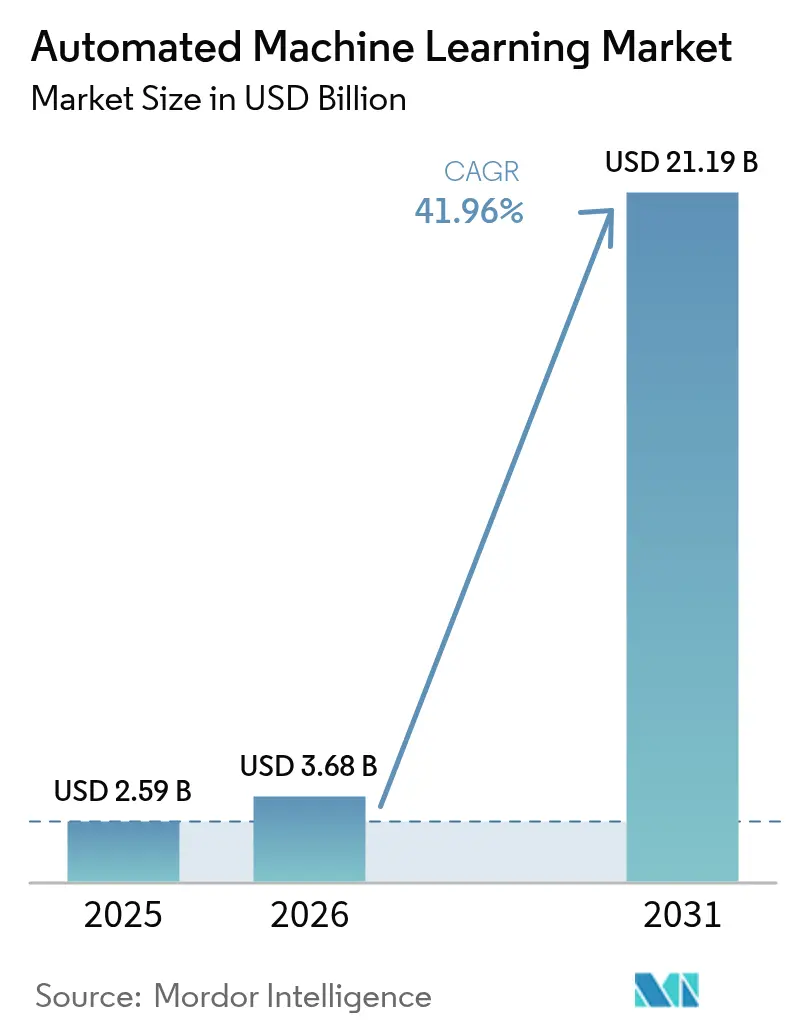

| Market Size (2026) | USD 3.68 Billion |

| Market Size (2031) | USD 21.19 Billion |

| Growth Rate (2026 - 2031) | 41.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Machine Learning Market Analysis by Mordor Intelligence

The Automated Machine Learning Market size was valued at USD 2.59 billion in 2025 and estimated to grow from USD 3.68 billion in 2026 to reach USD 21.19 billion by 2031, at a CAGR of 41.96% during the forecast period (2026-2031).

Commercial demand is reinforced by rapid cloud adoption, the need to scale artificial-intelligence initiatives without large data-science teams, and regulatory expectations for model transparency. Cloud-native offerings already account for 64% of global revenue and are expanding at 45.01% CAGR, underscoring the preference for managed infrastructure that shortens deployment cycles while lowering capital costs. Modeling automation holds the largest functional share, yet feature-engineering tools are growing faster as companies realise that data quality drives predictive accuracy more than algorithm selection. Large enterprises still dominate spending, but growth momentum is shifting to small and medium enterprises thanks to no-code interfaces and public-sector funding that offsets talent shortages. Regionally, North America leads in installed base, whereas Asia Pacific shows the strongest trajectory as governments embed AI goals into manufacturing and smart-city programs.

Key Report Takeaways

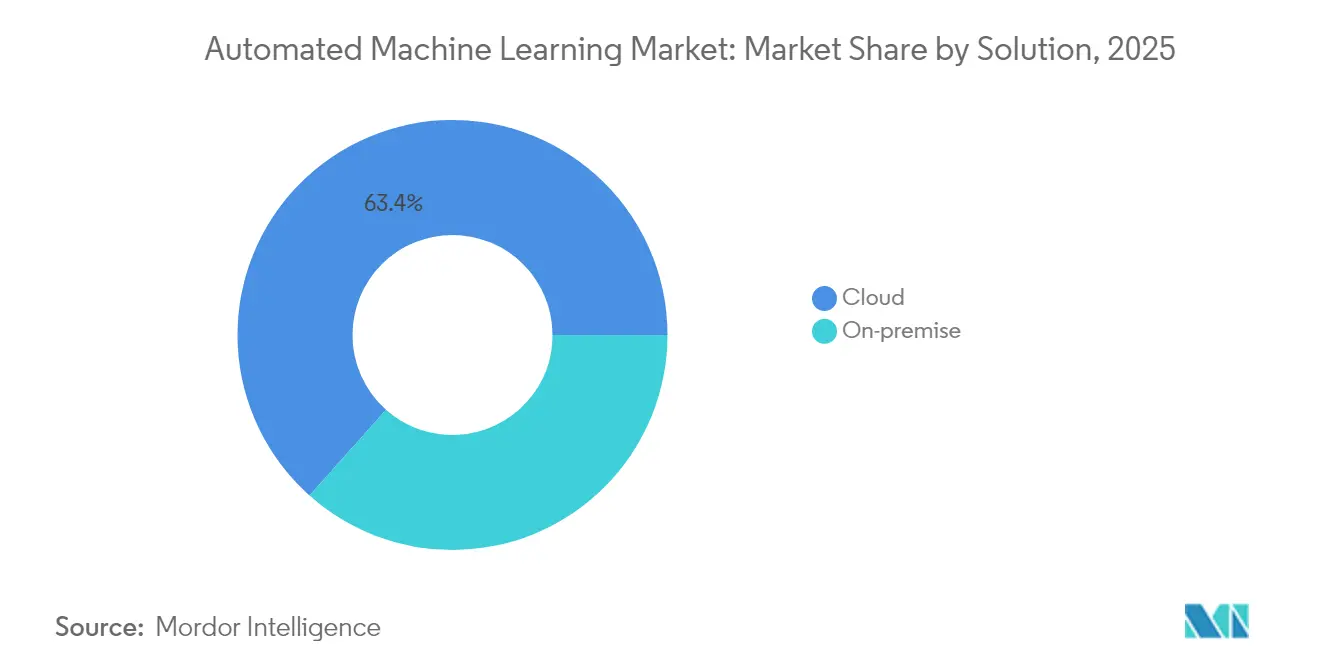

- By solution, cloud deployments led with 63.42% of the automated machine learning market share in 2025, while the segment is projected to increase at 43.72% CAGR through 2031.

- By automation type, modeling automation held 40.35% revenue share in 2025; feature engineering is forecast to expand at 43.11% CAGR to 2031.

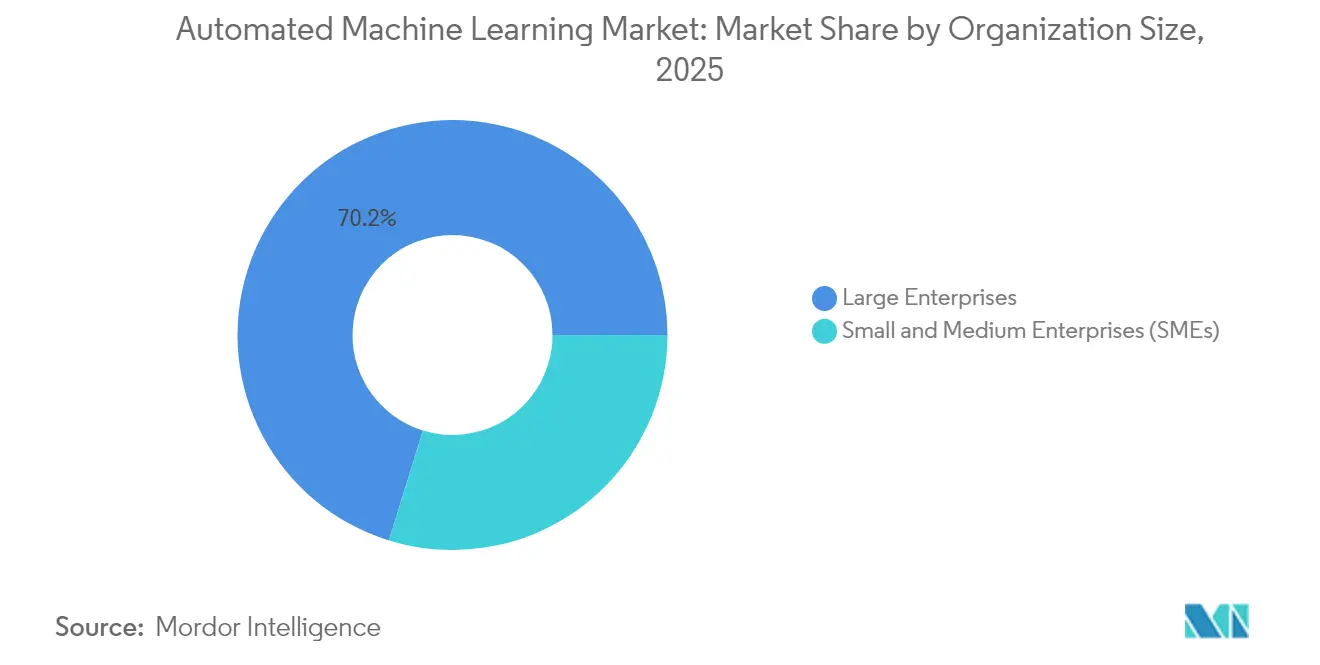

- By organization size, large enterprises captured 70.22% share of the automated machine learning market size in 2025, yet small and medium enterprises are advancing at 42.85% CAGR through 2031.

- By end-user, banking, financial services, and insurance commanded 30.44% of 2025 revenue, whereas healthcare is growing at 43.26% CAGR through 2031.

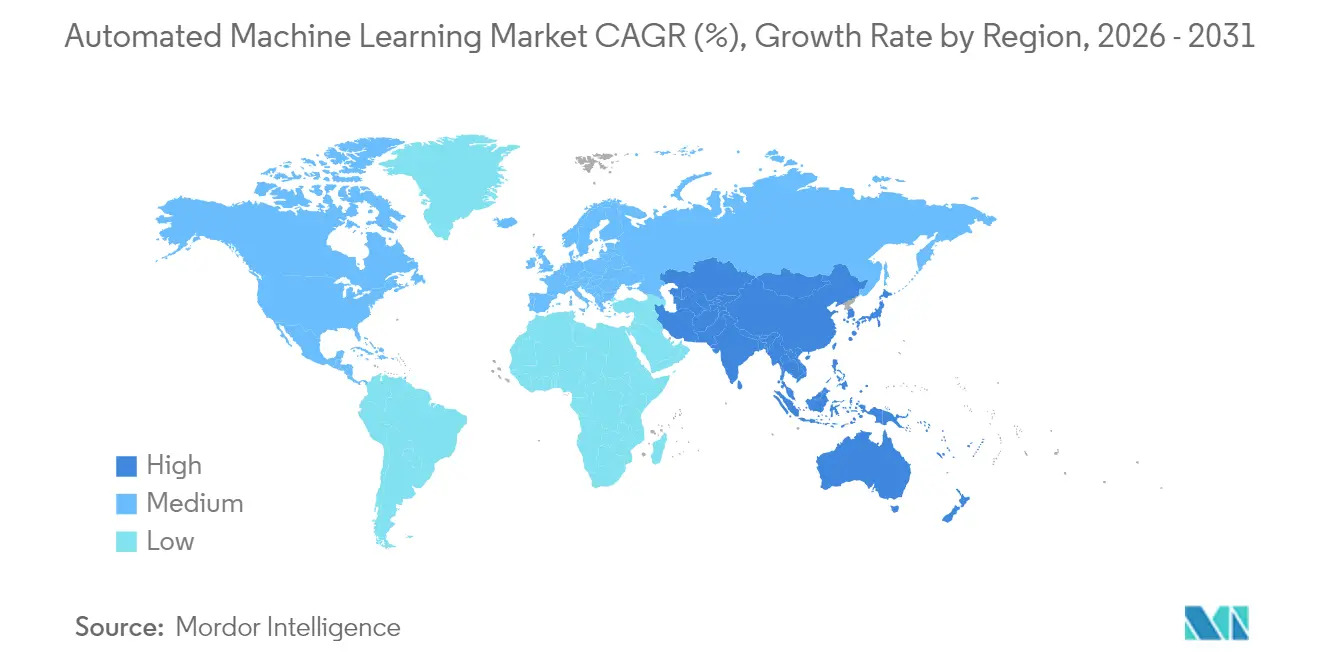

- By geography, North America accounted for 45.38% of 2025 revenue, while Asia Pacific is projected to register a 44.63% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automated Machine Learning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for efficient fraud-detection models | +8.2% | Global, concentrated in North America & Europe | Short term (≤ 2 years) |

| Increasing need for intelligent business processes | +7.1% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Cloud-first ML strategy of enterprises | +9.4% | Global, led by North America and Asia Pacific | Medium term (2-4 years) |

| Shortage of skilled data-science labour | +6.8% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Edge-native AutoML for on-device inference | +4.3% | Asia Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Regulatory push for model explainability | +5.7% | Europe & North America, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Efficient Fraud-Detection Models

Financial institutions are moving from static rule sets to AutoML-based fraud systems that learn from real-time transaction flows, cutting false positives and improving recovery rates. Insurers expect savings of USD 80–160 billion by 2032 as automated models mine structured and unstructured data for suspicious claims. Built-in natural-language processing allows platforms to digest call-centre transcripts and social-media signals, giving underwriters granular context for risk decisions. Vendors that deliver dashboards linking explanatory metrics to each prediction command price premiums because finance regulators are tightening disclosure standards. The net effect sustains an 8.2% uplift on forecast CAGR through 2026.

Increasing Need for Intelligent Business Processes

Enterprises are embedding AutoML inside manufacturing, retail, and healthcare workflows to move beyond rule-based robotics toward adaptive optimisation. Sensor-driven predictive maintenance trims unplanned downtime by up to 30% and improves overall equipment effectiveness across semiconductor fabrication lines[1]Tracey Countryman, “Predictive Maintenance in Industry 4.0,” McKinsey, mckinsey.com. Retailers apply AutoML to demand planning and dynamic pricing, with pilots showing 22.7% revenue lifts when AI-generated insights feed merchandising engines. Oracle’s Clinical Digital Assistant illustrates healthcare gains, reducing physician documentation time by as much as 40% and freeing capacity for patient care. The convergence of analytics, workflow orchestration, and low-code modelling tools propels a 7.1% contribution to growth through mid-decade.

Cloud-First ML Strategy of Enterprises

Enterprises are shedding on-premises hardware in favour of elastic GPU clusters delivered as a service, which adds 9.4% to the forecast CAGR. Microsoft’s FY-2025 results highlight multibillion-dollar Azure AI bookings tied to AutoML model training and governance add-ons. AWS is scaling Project Rainier, a Trainium-2 super-cluster that multiplies available compute by fivefold to support large AutoML workloads. Oracle’s backlog of AI infrastructure contracts exceeds USD 12 billion, signalling durable demand for cloud capacity that aligns with data-sovereignty rules through region-specific availability zones. Multi-cloud procurement reduces lock-in while accelerating proof-of-concept timelines from months to weeks.

Shortage of Skilled Data-Science Labour

Global demand for data-science roles outstrips supply, adding 6.8% to market growth as AutoML bridges capability gaps. Brazil reports a deficit of 500,000 AI professionals and relies on no-code AutoML to extend advanced analytics into business functions. The European Union’s adoption rate for AI nearly doubled to 13% between 2021 and 2024, yet many firms outsource model development because internal teams lack deep statistical expertise. Platforms such as Google AutoML popularise drag-and-drop interfaces, empowering marketing managers and operations analysts to build predictive models without Python or R coding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slow enterprise adoption & culture gap | -4.8% | Global, pronounced in traditional industries | Short term (≤ 2 years) |

| Data-security & privacy concerns in cloud workflows | -3.2% | Europe & North America, expanding globally | Medium term (2-4 years) |

| Algorithmic bias compliance costs | -2.1% | Europe & North America, regulatory spillover | Medium term (2-4 years) |

| Limited AutoML accuracy on long-horizon time-series | -1.9% | Global, sector-specific impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Slow Enterprise Adoption and Culture Gap

Legacy processes, risk-averse leadership, and workforce apprehension about job displacement slow AutoML rollouts, reducing market momentum by 4.8%. Many Asian banks still rely on manual anti-money-laundering reviews because their aged core systems complicate data integration. Small manufacturing firms in South Africa cite unclear frameworks and limited managerial sponsorship as primary impediments to AI projects, pushing deployment cycles beyond initial forecasts. Successful transformations combine training, change-management programs, and targeted incentives that align AI outcomes with employee performance metrics.

Data-Security and Privacy Concerns in Cloud Workflows

Global privacy legislation mandates granular control over personal data, slicing 3.2% from forecast growth as firms weigh compliance versus agility. The EU’s General Data Protection Regulation obliges companies to explain automated decisions and to honour user rights to opt out of profiling, prompting demand for local hosting or hybrid architectures. Apple’s decision to postpone certain AI features in the EU underscores how rule-making can delay product launches. Financial services providers conduct extensive validation before uploading sensitive datasets, lengthening procurement cycles. Vendors now offer encryption-in-use and audit logging to reassure risk officers without reverting to costly on-premises stacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Cloud Dominance Accelerates Infrastructure Shift

Cloud platforms generated 63.42% of revenue in 2025, and the segment is on track for 43.72% CAGR through 2031, a trajectory that validates the cost advantages of shared infrastructure. The automated machine learning market size for cloud deployments is projected to widen as hyperscalers integrate dedicated accelerators and serverless training pipelines. Continuous feature releases, enterprise-grade security certifications, and usage-based billing appeal to organisations seeking agility over hardware control. Bedrock, AWS’s model marketplace, lists more than 100 foundational and task-specific models, letting clients evaluate algorithms without owning GPUs, which compresses experimentation cycles.

On-premises deployments persist in finance, defence, and public sectors where data-residency mandates prohibit external hosting. Their share, however, is eroding as confidential-computing techniques allow secure processing in public-cloud environments. Hybrid patterns have emerged in which training occurs in the cloud while inference runs on edge devices to meet latency targets. Edge-native offerings enable offline operation for factories and retail outlets, ensuring business continuity when connectivity drops.

By Automation Type: Feature Engineering Emerges as Growth Leader

Modeling automation retained 40.35% of 2025 revenue yet feature engineering’s 43.11% CAGR signals a shift toward data-centric AI. The automated machine learning market share for feature automation is expanding because structured-data projects often fail without robust variable construction. Large language models now assist in mapping raw fields to domain-ready features, automating semantic joins and text embeddings that previously demanded specialist knowledge.

Visualization and data-processing automation support wider adoption by translating plain-language questions into SQL queries and interactive charts. Research combining evolutionary algorithms with LLM prompts has cut computation time while improving predictive lift on benchmark datasets. Healthcare and finance users benefit most, as domain-specific ontologies are embedded into feature pipelines, satisfying auditing requirements without manual intervention.

By Organization Size: SME Acceleration Drives Market Democratization

Large enterprises held 70.22% of spending in 2025, yet SMEs register a 42.85% CAGR that outpaces the wider market. Government grants and cloud credits lower entry barriers, allowing mid-market firms to test AutoML before committing large budgets. The automated machine learning market size for SMEs is forecast to double every 18 months in Latin America, following Brazil’s BRL 23 billion AI fund that subsidises tooling and talent programs.

No-code interfaces reduce reliance on scarce data scientists, and templated solutions target common use cases such as churn prediction, inventory planning, and invoice fraud. Research shows medium-sized firms gain more from perceived relative advantage than smaller peers, pointing to organisational maturity as a success factor. Return-on-investment studies reveal payback in under 14 months when AutoML enhances export documentation and trade financing processes.

By End-User: Healthcare Acceleration Outpaces Financial-Services Leadership

Financial services institutions captured 30.44% of the 2025 demand thanks to early fraud-detection and risk-modelling use cases. Healthcare grows faster at 43.26% CAGR as clinical-decision support, imaging triage, and patient-flow optimisation mature. The automated machine learning market size for healthcare is underpinned by explainability modules that satisfy medical-device regulators and hospital ethics boards.

Retail and e-commerce deploy AutoML for personalisation engines that lift conversion by double-digit percentages. Manufacturing applies real-time quality control on production lines, while energy utilities model load patterns to stabilise smart grids. Government agencies increasingly automate benefits adjudication; Brazil’s social-security institute aims to process 55% of welfare claims via AI by 2025.

Geography Analysis

North America generated 45.38% of global revenue in 2025 on the back of dense cloud-infrastructure footprints, a mature venture-capital ecosystem, and high adoption in banking and technology sectors. Oracle’s cloud-infrastructure revenue rose 52% in fiscal 2025 as regulated industries moved core workloads to its FedRAMP-compliant regions. Venture investors closed more than 200 AutoML-related funding rounds in 2024, feeding a vibrant start-up pipeline that accelerates product innovation.

Asia Pacific records the strongest trajectory with 44.63% CAGR through 2031 as governments deploy national AI strategies. Japan’s AI economy is projected to expand from USD 4.5 billion to USD 7.3 billion by 2027, driven by smart-city pilots, predictive maintenance programs in heavy industry, and local-language conversational agents. China leads in patent publications for 37 of 44 critical technologies, affirming its status as a powerhouse for both research and commercial implementation. Southeast Asian manufacturers adopt AutoML for yield optimisation to offset rising labour costs and supply-chain volatility.

Europe presents a mixed environment. The GDPR and forthcoming AI Act introduce strict governance that elongates sales cycles but ultimately favours platforms with embedded transparency controls. The region’s AI adoption doubled to 13% by 2024, yet many firms outsource technical builds, creating fertile ground for managed AutoML services. National recovery funds earmark billions of euros for digital-transformation projects, including health-data spaces that require automated modelling engines.

The Middle East pursues headline investments to diversify economies. Saudi Arabia has earmarked USD 100 billion for AI and digital infrastructure under Vision 2030, with further capital allocated to a planned 6-gigawatt data-centre corridor. The United Arab Emirates expects its AI Strategy 2031 to cut federal-service costs by 50%, driving procurement of AutoML platforms that automate citizen services. South America benefits from Brazil’s national AI strategy, which funds Portuguese-language models and HPC upgrades. Africa is an emerging frontier; 40% of surveyed institutions are piloting AI, and cloud-hosted AutoML lowers the barrier where local compute resources remain scarce.

Competitive Landscape

The market remains moderately fragmented. Hyperscale cloud providers such as Microsoft, AWS, and Oracle leverage integrated infrastructure, global data-centre grids, and large engineering teams to bundle AutoML into platform subscriptions. AWS’s Bedrock service adopts an open-model catalogue, while Microsoft aligns closely with proprietary LLM distributors. Oracle’s planned USD 40 billion procurement of Nvidia hardware for its Texas facility under the Stargate project illustrates capital intensity that new entrants struggle to match.

Specialist vendors differentiate through domain expertise and governance. DataRobot introduced an enterprise suite with pre-built compliance workflows aligned to the EU AI Act, targeting financial services and healthcare buyers. H2O.ai focuses on transparent algorithms and open-source lineage, appealing to regulated industries requiring auditability[3]Sri Ambati, “Explainable AI at Scale,” H2O.ai, h2o.ai . Alteryx embeds generative AI across its analytics platform, bridging data preparation, model building, and decision automation for business users.

Edge-native innovations create white-space opportunities. Start-ups file patents for distributed model-training approaches that handle intermittent connectivity on factory floors and in autonomous vehicles. Vendors able to offer one-click deployment from cloud training to edge inference stand to capture the spend allocated to latency-sensitive applications. As regulatory scrutiny deepens, platforms that combine automation with explainability and monitoring are likely to consolidate share.

Automated Machine Learning Industry Leaders

Datarobot Inc.

Amazon web services Inc.

dotData Inc.

IBM Corporation

Dataiku

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Oracle committed USD 40 billion to purchase Nvidia GPUs for the OpenAI-backed Stargate data centre in Texas, scheduled to go live in 2026.

- June 2025: AWS unveiled Project Rainier, deploying hundreds of thousands of Trainium 2 chips across US sites to quintuple available AI-training capacity.

- March 2025: Brazil’s Senate passed a national AI law defining transparency, accountability, and the remit of a new oversight agency.

- November 2024: DataRobot released its Enterprise AI Suite with enhanced observability and pre-configured compliance templates for the EU AI Act.

Global Automated Machine Learning Market Report Scope

Automated machine learning or AutoML refers to automating the time-consuming, iterative tasks of machine learning model development. It allows data scientists, developers, and analysts to build large-scale, productive, and efficient ML models while sustaining model quality.

The automated machine learning market is segmented by solution (standalone or on-premise and cloud), automation type (data processing, feature engineering, modeling, and visualization), end user (BFSI, retail and e-commerce, healthcare, manufacturing, and other end users), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| On-premise |

| Cloud |

| Data Processing |

| Feature Engineering |

| Modeling |

| Visualization |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Retail and E-commerce |

| Healthcare |

| Manufacturing |

| Other End-users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Argentina |

| Brazil | |

| Rest of South America |

| By Solution | On-premise | |

| Cloud | ||

| By Automation Type | Data Processing | |

| Feature Engineering | ||

| Modeling | ||

| Visualization | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises (SMEs) | ||

| By End-user | BFSI | |

| Retail and E-commerce | ||

| Healthcare | ||

| Manufacturing | ||

| Other End-users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the automated machine learning market?

The automated machine learning market is valued at USD 3.68 billion in 2026 and is projected to reach USD 21.19 billion by 2031.

Which deployment model grows fastest in automated machine learning?

Cloud-based solutions expand at 43.72% CAGR because they provide elastic compute, frequent feature updates, and lower upfront costs.

Why is healthcare the fastest-growing end-user segment?

Regulatory clarity and the need for clinical decision support drive healthcare to a 43.26% CAGR, outpacing other industries in adopting explainable AutoML tools.

How are talent shortages influencing adoption?

Limited availability of data-science professionals pushes firms toward no-code AutoML platforms, adding 6.8% to overall market CAGR.

What regions present the highest growth potential through 2031?

Asia Pacific leads with a 44.63% CAGR, fuelled by national AI policies, manufacturing modernisation, and rising cloud penetration.

How do data-privacy regulations affect cloud AutoML uptake?

Strict frameworks such as the EU GDPR slow deployments by 3.2% CAGR points as firms demand hybrid or local-hosted options with strong auditing capabilities.

Page last updated on: