Self-Supervised Learning Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

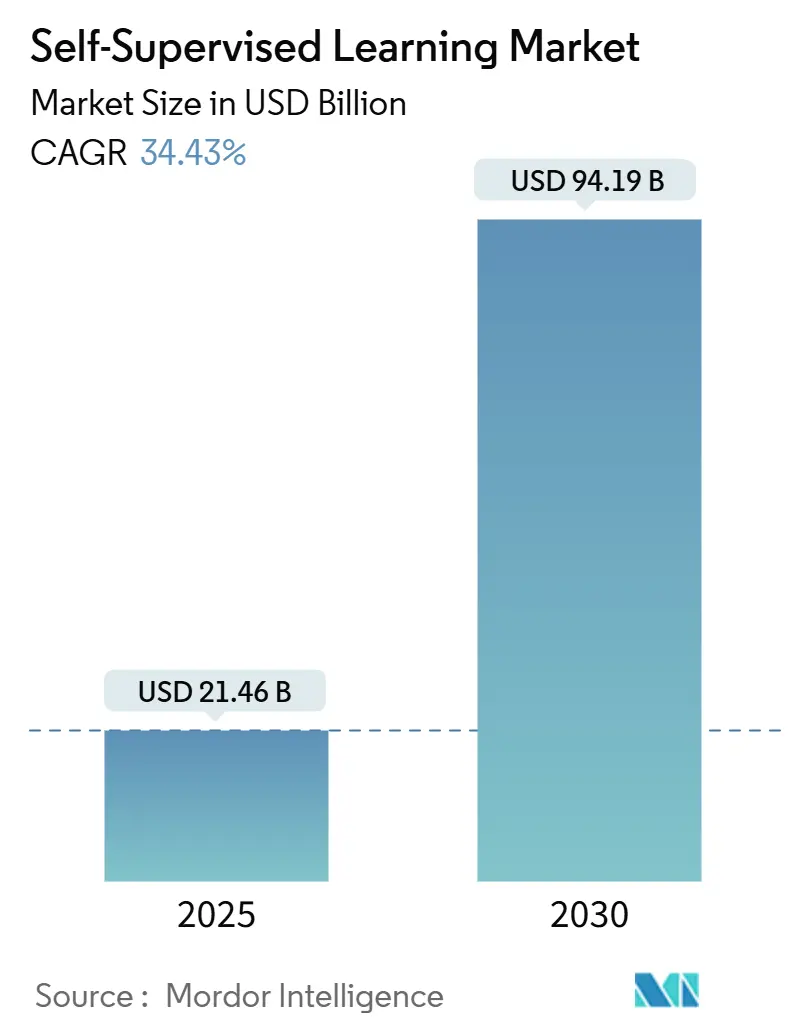

| Market Size (2025) | USD 21.46 Billion |

| Market Size (2030) | USD 94.19 Billion |

| Growth Rate (2025 - 2030) | 34.43% CAGR |

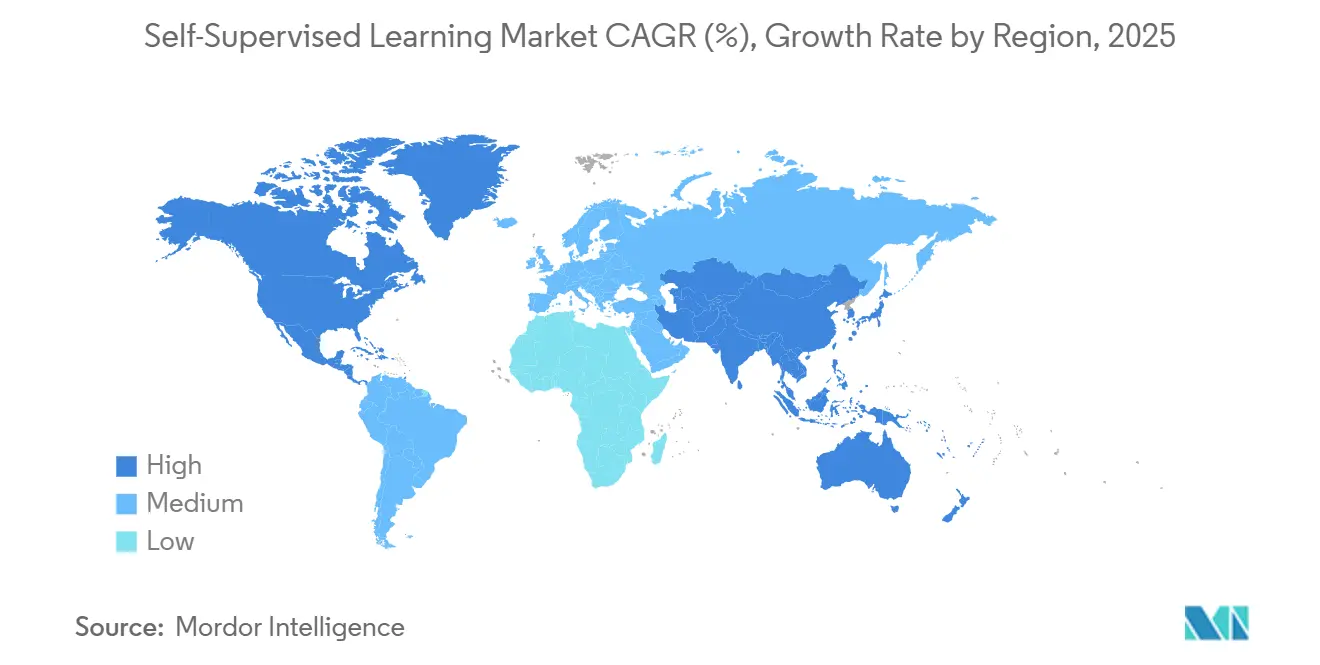

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

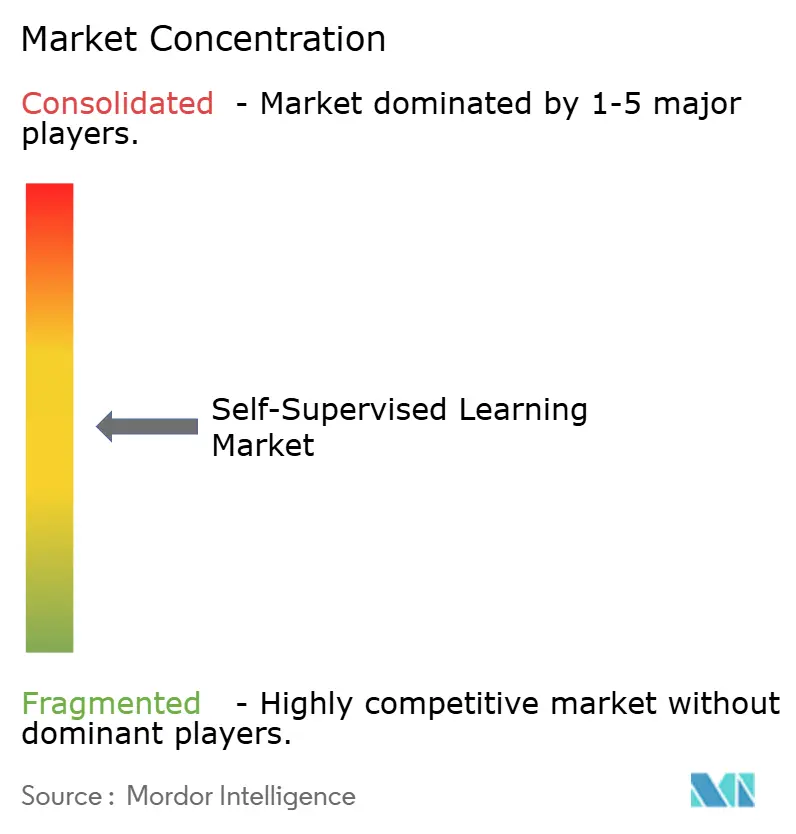

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Self-Supervised Learning Market Analysis by Mordor Intelligence

The self-supervised learning market size stands at USD 21.46 billion in 2025 and is projected to reach USD 94.19 billion by 2030, delivering a 34.43% CAGR through the forecast period. Enterprises are scaling the use of models that learn directly from raw data, eliminating costly labeling and accelerating deployment cycles. Wider availability of foundation models, falling cloud-compute prices per GPU-hour, and steady gains in transformer efficiency have expanded pilot programs in healthcare, automotive, finance, and retail. Vendors differentiate through multimodal capabilities, on-device optimization, and curated industry datasets that reduce time-to-value. Strategic partnerships between cloud providers and model developers further propel the self-supervised learning market as enterprises look for turnkey solutions and predictable pricing.

Key Report Takeaways

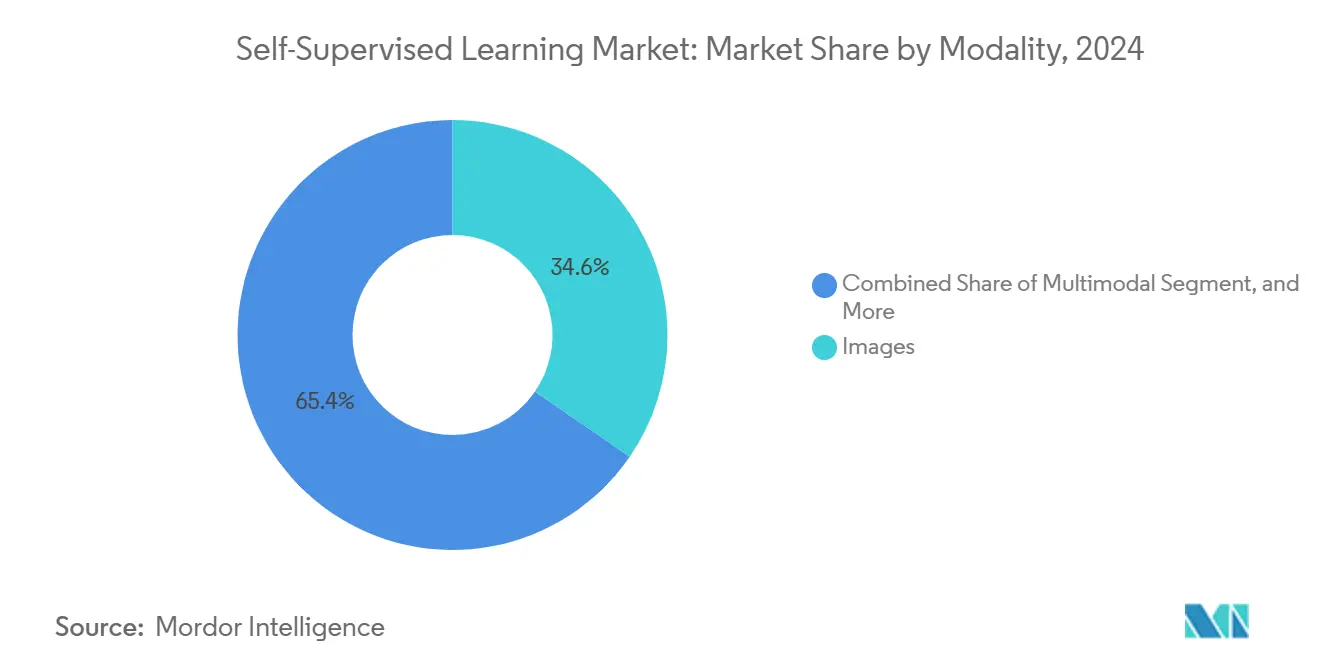

- By modality, images led with 34.57% of self-supervised learning market share in 2024, while multimodal approaches are advancing at a 34.69% CAGR through 2030.

- By application, natural language processing held 39.84% of the self-supervised learning market size in 2024 and robotics and autonomous systems are forecast to expand at a 34.47% CAGR.

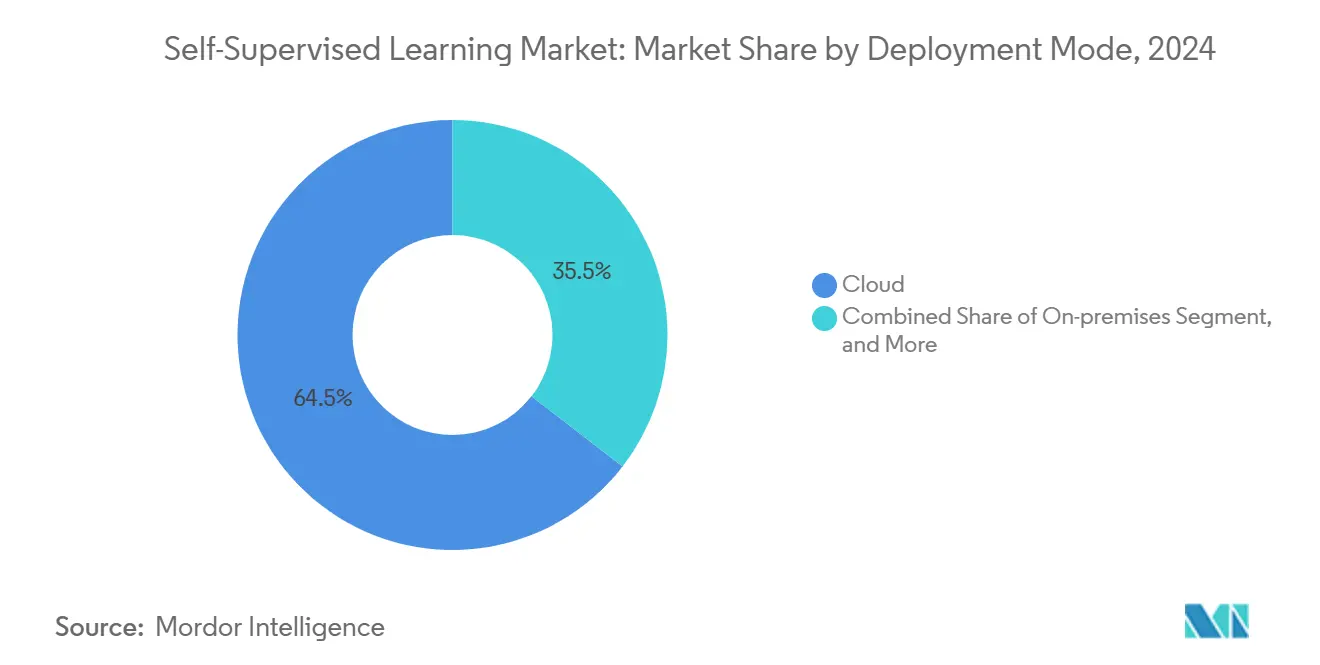

- By deployment mode, cloud accounted for 64.52% of the self-supervised learning market size in 2024; edge deployment is projected to post a 36.83% CAGR.

- By component, pre-trained models commanded 43.52% share of the self-supervised learning market size in 2024 and remain on track for a 34.77% CAGR.

- By industry vertical, healthcare generated 19.83% revenue share in 2024, whereas automotive and transportation are expected to climb at a 34.51% CAGR.

- By geography, North America contributed 37.37% revenue in 2024 and Asia-Pacific is set to record a 34.64% CAGR to 2030.

Market Trends and Insights

Drivers Impact Analysis of Self-Supervised Learning Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for data-efficient model training | +8.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Need to cut annotation cost and time for enterprise AI | +7.8% | Global, particularly Asia-Pacific emerging markets | Short term (≤ 2 years) |

| Rapid performance gains in multimodal foundation models | +6.9% | North America and EU core, spillover to Asia-Pacific | Medium term (2-4 years) |

| Adoption of self-supervised pre-training in edge devices | +5.4% | Asia-Pacific core, expanding to global markets | Long term (≥ 4 years) |

| Open-source ecosystems lowering entry barriers | +4.1% | Global, with developer concentration in North America | Short term (≤ 2 years) |

| Emergence of synthetic-data-centric pipelines | +3.8% | North America and EU, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Data-Efficient Model Training

Organizations have recognized that manually labeled datasets are cost-prohibitive, prompting a rapid pivot toward methods that extract representations from unlabeled data. Meta’s Data2vec showed state-of-the-art accuracy across speech, vision, and text while trimming annotation needs by 90%. Enterprises rolling out a portfolio of models can now direct investments to compute rather than labeling, unlocking use cases that span multiple business units.

Need to Cut Annotation Cost and Time for Enterprise AI

Hospitals that applied self-supervised techniques to X-ray classification trimmed annotation time by 70% yet maintained diagnostic precision equal to supervised baselines.[1]Nature Medicine, “Self-Supervised Learning in Medical Imaging: A Comprehensive Review,” nature.com Finance teams building fraud models report comparable gains with 60% fewer labeled instances. Those savings reallocate scarce expert hours toward higher-value tasks such as feature engineering and governance.

Rapid Performance Gains in Multimodal Foundation Models

Advances in contrastive learning have tightened alignment across text, vision, and audio, elevating zero-shot accuracy while slashing compute by 40% relative to earlier releases.[2]OpenAI Research, “Learning Transferable Visual Models From Natural Language Supervision,” openai.com Google’s PaLI-X underscores how unified architectures deliver best-in-class reasoning on benchmarks that demand both visual context and language understanding. Enterprises consequently converge on a single multimodal stack rather than siloed point solutions.

Adoption of Self-Supervised Pre-Training in Edge Devices

Apple deployed compact language models on iPhone that reach 85% of cloud accuracy while requiring only 1.2 GB of memory. Qualcomm’s Snapdragon 8 Gen 3 integrates neural units engineered for self-supervised inference, cutting handset power draw by 60%. The approach enables privacy-preserving apps such as on-device summarization and multilingual translation, accelerating edge demand across Asia-Pacific markets.

Restraints Impact Analysis of Self-Supervised Learning Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High compute and energy requirements of pre-training | -4.2% | Global, particularly regions with high energy costs | Medium term (2-4 years) |

| Scarcity of benchmark standards for industrial use-cases | -3.1% | Global, with emphasis on regulated industries | Short term (≤ 2 years) |

| Regulatory uncertainty over foundation-model liability | -2.8% | EU and North America, expanding globally | Long term (≥ 4 years) |

| Talent shortage in representation-learning research | -2.3% | Global, acute in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Compute and Energy Requirements of Pre-Training

Training GPT-4-scale models costs up to USD 200 million in compute and consumes 1,287 MWh electricity, equivalent to 120 U.S. households. These barriers tilt bargaining power to hyperscale firms. Parameter-efficient tuning and distillation partially relieve the burden, yet capital-constrained companies still face long amortization cycles.

Scarcity of Benchmark Standards for Industrial Use-Cases

Manufacturers experimenting with anomaly detection lack universal metrics to gauge self-supervised performance, unlike established supervised accuracy scores.[3]IEEE Standards Association, “IEEE 3119 Standard for Artificial Intelligence Systems,” standards.ieee.org Without shared baselines, procurement teams struggle to compare vendors, delaying purchase decisions and raising compliance hurdles in safety-critical settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Self-Supervised Learning Market Segment Analysis

By Modality:

Multimodal Integration Drives InnovationImages accounted for 34.57% of the self-supervised learning market share in 2024. Multimodal architectures are forecast to grow at a 34.69% CAGR as enterprises combine text, vision, and audio to build holistic user experiences. The self-supervised learning market benefits from declining GPU memory needs that make cross-modal pre-training commercially viable. Video and audio adoption rises in parallel as contrastive objectives mature. Shared embedding spaces trim deployment costs by allowing one model to power diverse tasks such as search, summarization, and generation. Meta’s ImageBind demonstrated unified embeddings across six modalities without aligned pairs.

Early movers now replace siloed computer-vision pipelines with multimodal stacks that streamline maintenance. E-commerce players integrate product photos with textual reviews to improve retrieval relevance. Media firms mine simultaneous speech and frame data for real-time captioning. The trajectory confirms that multimodality will be the default design choice for the self-supervised learning market.

By Application:

Robotics Emerges as Growth LeaderNatural language processing represented 39.84% of the self-supervised learning market size in 2024. Robotics and autonomous systems, however, are scaling at a 34.47% CAGR through 2030 as unlabeled interaction data replaces scripted instruction sets. Warehouse operators apply self-supervised manipulation policies that cut task programming from weeks to hours. Computer vision stays relevant for inspection and driver assistance, while speech models gain new languages through unlabeled broadcast archives.

The robotics surge stems from falling sensor prices and greater model portability. Cross-modal reasoning lets mobile robots parse audio cues and visual landmarks concurrently. Automotive OEMs embed self-supervised perception modules that adapt to novel road layouts without manual relabeling. As synthetic environments expand, simulated mileage augments real-world driving logs, compounding data network effects for leaders in the self-supervised learning market.

By Industry Vertical:

Healthcare Leadership with Automotive AccelerationHealthcare produced 19.83% of the self-supervised learning market revenue in 2024. Radiology groups fine-tune vision transformers on unlabeled scans to identify anomalies with limited expert feedback. Drug-discovery teams reduce candidate screening cycles by mining chemical structures through graph encoders. Automotive and transportation, posting the fastest 34.51% CAGR, leverage huge dash-cam corpora to enhance perception for autonomous driving.

Financial institutions deploy fraud-detection embeddings trained on unlabeled transactions to flag outliers across payment rails. Retailers refine recommendation engines via clickstream-based self-supervised objectives, driving cross-sell uplift. Manufacturing plants use vibration signatures to predict equipment failure without exhaustive fault labels. Diversification across verticals broadens the customer base for the self-supervised learning market.

By Deployment Mode:

Edge Computing Gains MomentumCloud remained dominant with 64.52% of the self-supervised learning market size in 2024. Edge deployment is expected to outpace at a 36.83% CAGR as privacy rules and latency needs converge. Consumer electronics integrate on-device vision summarization that runs after each video capture, avoiding cloud uploads. Industrial IoT sensors host lightweight language models that parse and process logs locally, shrinking bandwidth use by 80%.

Regulators in Europe and Asia require sensitive data to stay within national boundaries, accelerating sovereign edge clusters. Hardware roadmaps from NVIDIA, Qualcomm, and Apple include transformer-optimized accelerators that democratize computing at the edge. These shifts reinforce a hybrid paradigm where pre-training happens centrally, and inference moves closer to data origin, expanding total addressable demand for the self-supervised learning market.

By Component:

Pre-Trained Models Drive Market ValuePre-trained models captured 43.52% of the self-supervised learning market share in 2024 and will expand at a 34.77% CAGR. Buying a ready foundation model shortens project timelines and reallocates budgets toward fine-tuning. The Hugging Face hub hosts more than 150,000 pretrained checkpoints accessible via permissive licenses. Frameworks and libraries provide a scaffolding layer for bespoke tasks, while services teams wrap inference APIs with domain adaptation.

Hardware accelerators such as the NVIDIA H200 promise 2.5x transformer throughput with 30% lower power draw, reducing total cost of ownership for training runs. System integrators bundle low-code interfaces and performance SLAs that appeal to mid-market enterprises. This ecosystem structure consolidates margins around model providers while opening service niches for consulting partners in the self-supervised learning industry.

Geography Analysis

North America Self-Supervised Learning Market

North America generated 37.37% of the self-supervised learning market revenue in 2024 on the back of deep research talent, venture capital, and hyperscale compute footprints. U.S. providers extended GPU clusters and spent USD 155 billion on AI infrastructure during 2025 to advance foundation models. Early adopters in healthcare and financial services continued large-scale pilots that matured into production rollouts. Canada supplied groundbreaking techniques in contrastive learning through the Vector Institute and MILA, anchoring regional innovation.

APAC Self-Supervised Learning Market

Asia-Pacific is forecast to post a 34.64% CAGR, the fastest worldwide. Beijing, Shenzhen, and Hangzhou saw conglomerates allocate more than CNY 540 billion (USD 75.6 billion) to multimodal research, with Alibaba alone pledging CNY 380 billion (USD 53.2 billion) for self-supervised breakthroughs. Governments subsidize GPU parks, easing entry for startups focused on agriculture and education. Japan and South Korea direct efforts into robotics and semiconductor embedding, while India pilots cost-effective healthcare chatbots that function offline.

EMEA and South America Self-Supervised Learning Market

Europe maintains steady momentum through regulatory clarity and industrial automation. Germany leverages self-supervised perception inside automotive assembly lines. France’s aerospace sector tunes multimodal models on maintenance logs, and the U.K. financial hub experiments with retrieval-augmented advisory systems. The European Union’s AI Act incentivizes documentation and explainability, pushing local vendors to invest in interpretability tooling and ethical auditing. Middle East and Africa and South America remain nascent but record growing pilots in energy and agritech, respectively.

Competitive Landscape

The self-supervised learning market is moderately fragmented. OpenAI, Meta, and Google lead in parameter count and model performance, while Microsoft and Amazon convert cloud dominance into turnkey offerings. NVIDIA anchors the hardware stack with GPUs tuned for transformer kernels. Startups such as Anthropic pursue safety-aligned architectures, and Cohere targets retrieval-augmented generation for enterprise use. Hardware challengers like Cerebras and Graphcore deliver wafer-scale and IPU-based accelerators that compress training cycles.

Competitive differentiation centers on multimodal reach, latency optimization, and licensing terms. Patent filings for self-supervised methods jumped 340% between 2024 and 2025, signaling a race to lock in intellectual property. Vendors bundle model weights with guardrail toolkits to satisfy emerging liability regulations. Strategic alliances multiply: Microsoft partnered with Hugging Face to merge Azure orchestration with an expanding catalog of models, and Amazon invested USD 4 billion in Anthropic for constitutional AI research.

Marketing narratives stress energy efficiency, privacy, and domain specificity. Leaders publish benchmark scores that exceed prior baselines while highlighting reduced GPU hours. Specialized firms seize white-space in manufacturing, biotech, and legal tech by pairing subject-matter expertise with fine-tuned embeddings. This interplay suggests ongoing consolidation around cloud-scale platforms, balanced by a long tail of niche innovators in the self-supervised learning market.

Self-Supervised Learning Industry Leaders

OpenAI, Inc.

Anthropic PBC

Hugging Face SA

Meta Platforms, Inc.

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Self-Supervised Learning Market Companies Covered in this Report

- OpenAI, Inc.

- Anthropic PBC

- Hugging Face SA

- Meta Platforms, Inc.

- Google LLC

- Microsoft Corporation

- Amazon Web Services, Inc.

- Baidu, Inc.

- Alibaba Group Holding Limited

- Tencent Holdings Limited

- Cohere, Inc.

- Stability AI Ltd.

- Databricks, Inc.

- Scale AI, Inc.

- DeepMind Technologies Limited

- NVIDIA Corporation

- IBM Corporation

- Snowflake Inc.

- Adept AI Labs, Inc.

- Runway AI, Inc.

Recent Industry Developments in Self-Supervised Learning Market

- September 2025: Meta announced a USD 65 billion program to build next-generation multimodal self-supervised systems.

- August 2025: OpenAI introduced GPT-5 with 40% stronger reasoning and 25% lower compute requirements.

- July 2025: NVIDIA unveiled the H200 Tensor Core GPU delivering 2.5× transformer throughput at 30% less energy.

- June 2025: Google DeepMind shipped Gemini Ultra 2.0 for real-time multilingual multimodal processing.

Global Self-Supervised Learning Market Report Scope

Segmentation Overview

| Images |

| Text |

| Audio |

| Video |

| Multimodal |

| Computer Vision |

| Natural Language Processing |

| Speech Recognition |

| Recommendation Systems |

| Anomaly Detection |

| Robotics and Autonomous Systems |

| Healthcare |

| Automotive and Transportation |

| Retail and E-commerce |

| Banking, Financial Services and Insurance (BFSI) |

| Manufacturing |

| Media and Entertainment |

| Other Industry Verticals |

| Cloud |

| On-premises |

| Edge |

| Frameworks and Libraries |

| Pre-trained Models |

| Hardware Accelerators |

| Services and Integration |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Modality | Images | ||

| Text | |||

| Audio | |||

| Video | |||

| Multimodal | |||

| By Application | Computer Vision | ||

| Natural Language Processing | |||

| Speech Recognition | |||

| Recommendation Systems | |||

| Anomaly Detection | |||

| Robotics and Autonomous Systems | |||

| By Industry Vertical | Healthcare | ||

| Automotive and Transportation | |||

| Retail and E-commerce | |||

| Banking, Financial Services and Insurance (BFSI) | |||

| Manufacturing | |||

| Media and Entertainment | |||

| Other Industry Verticals | |||

| By Deployment Mode | Cloud | ||

| On-premises | |||

| Edge | |||

| By Component | Frameworks and Libraries | ||

| Pre-trained Models | |||

| Hardware Accelerators | |||

| Services and Integration | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the self-supervised learning market?

It is valued at USD 21.46 billion in 2025.

How fast is the market expected to expand through 2030?

The forecast CAGR is 34.43%.

Which region will register the quickest growth?

Asia-Pacific is projected to grow at 34.64% CAGR thanks to large-scale AI investments.

Which deployment mode is gaining the most momentum?

Edge deployment is advancing at a 36.83% CAGR because of privacy and latency benefits.

Which industry currently spends the most?

Healthcare leads with a 19.83% revenue share driven by imaging and drug-discovery use cases.

Why are enterprises preferring pre-trained models?

Pre-trained models reduce development time and hold 43.52% market share due to turnkey availability.

Page last updated on: