Education ERP Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

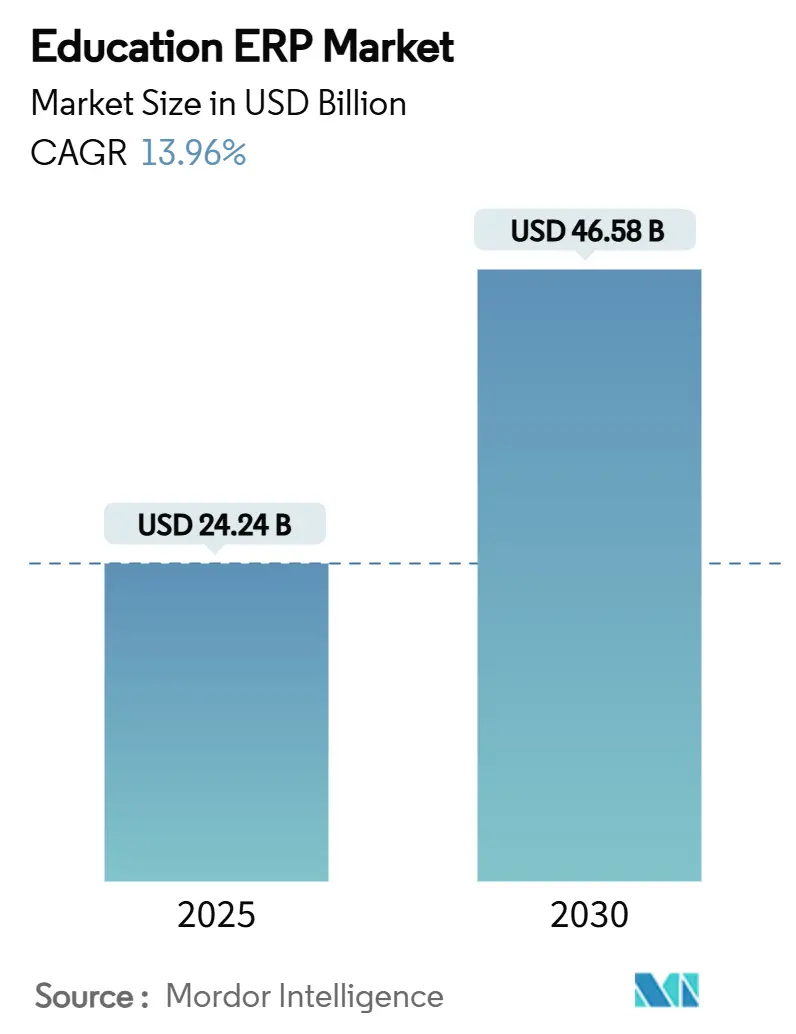

| Market Size (2025) | USD 24.24 Billion |

| Market Size (2030) | USD 46.58 Billion |

| Growth Rate (2025 - 2030) | 13.96% CAGR |

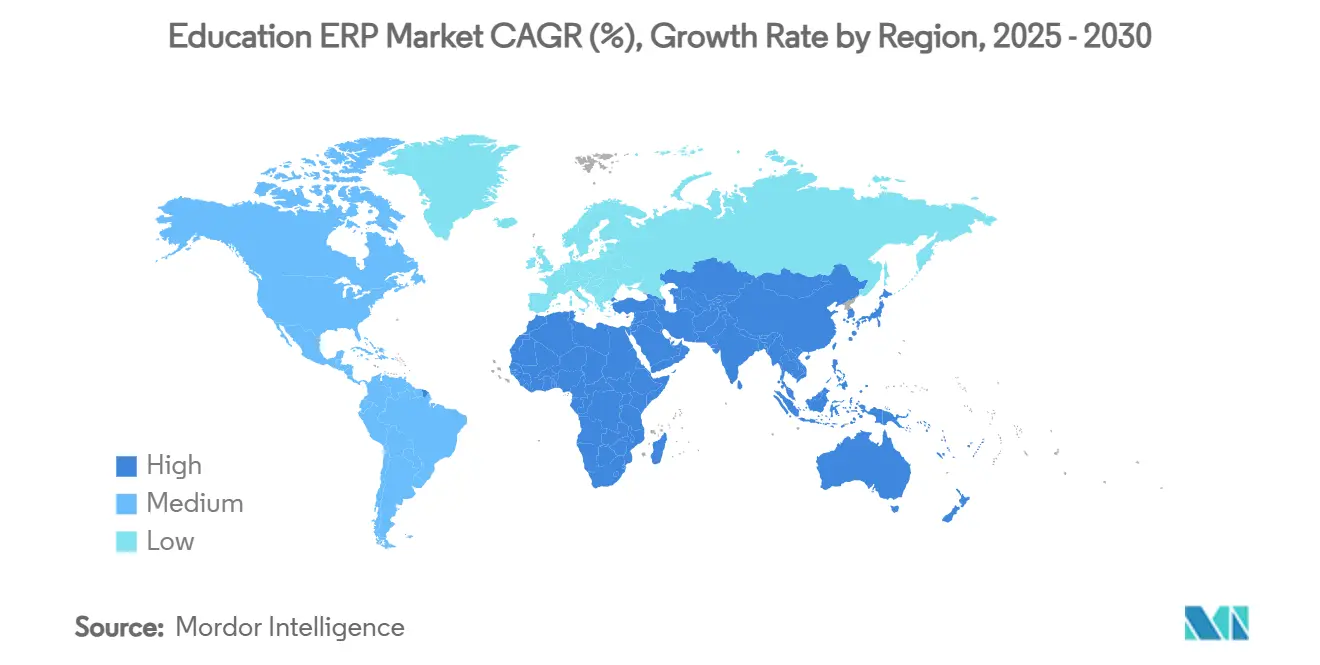

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Education ERP Market Analysis by Mordor Intelligence

The education ERP market size reached USD 24.24 billion in 2025 and is projected to attain USD 46.58 billion by 2030, registering a 13.96% CAGR. Institutions pivoted from legacy systems toward integrated cloud platforms to support hybrid learning, real-time data analytics, and compliance mandates. Government digitization programs, cyber-insurance requirements, and AI-driven predictive analytics further accelerated platform adoption. Strategic consolidation among leading vendors tightened competitive dynamics, while low-code configuration tools began lowering implementation barriers for mid-tier institutions. Despite the market’s momentum, data-sovereignty regulations and shortages of ERP-literate administrators tempered rollout speed in regions that mandated in-country hosting.

Key Report Takeaways

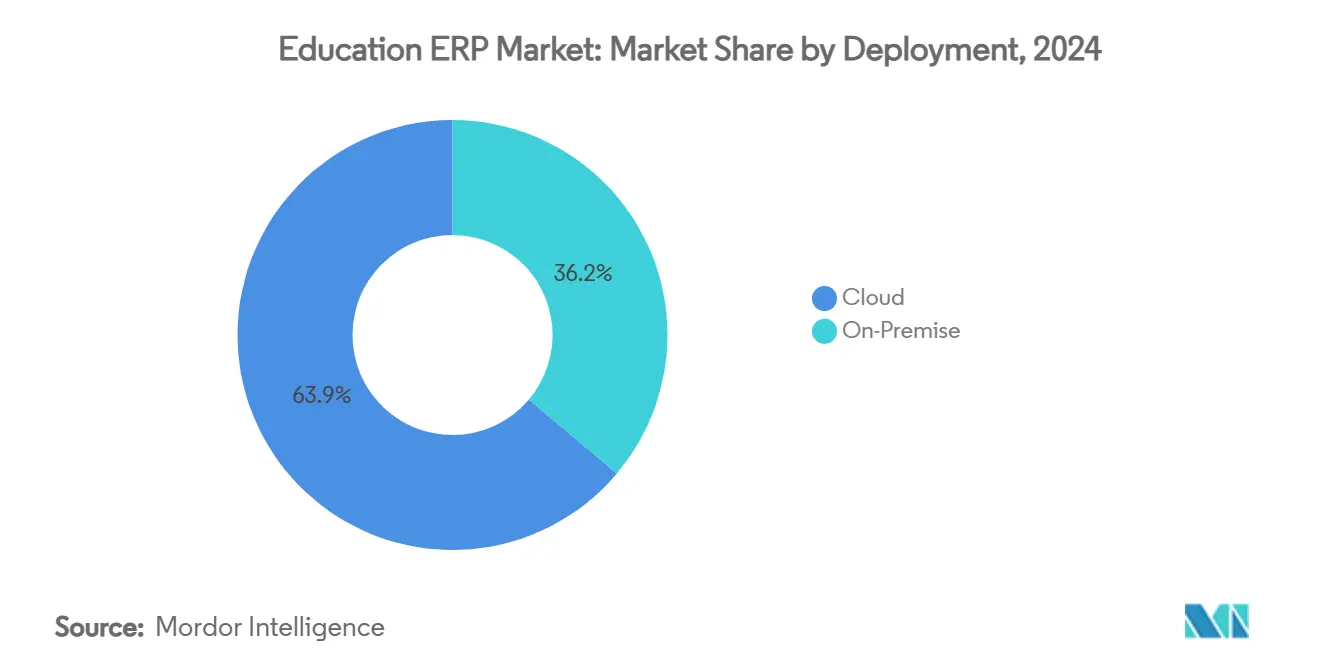

- By deployment, cloud solutions captured 63.85% of education ERP market share in 2024.

- By institution level, vocational and training centers advanced at a 14.89% CAGR through 2030, the fastest rate among all segments.

- By function, Student Information and Administration modules held 34.48% of education ERP market size in 2024.

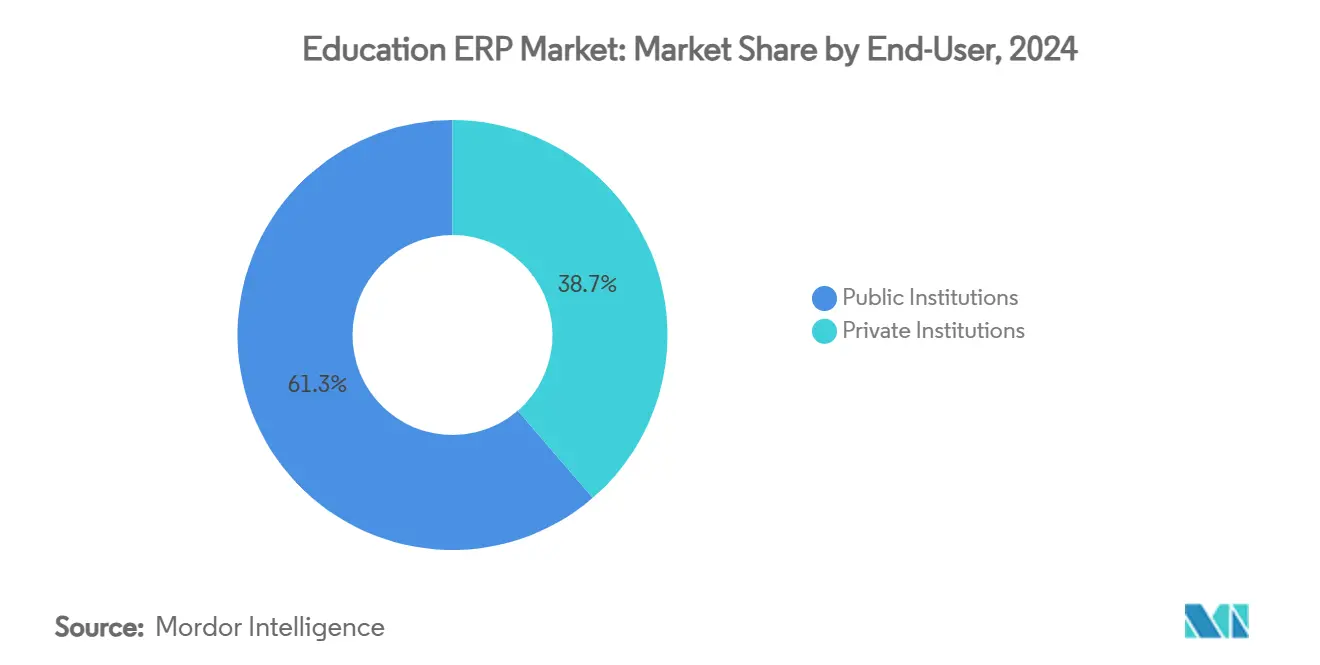

- By end-user, private institutions recorded a 14.62% CAGR to 2030, outpacing public counterparts.

Global Education ERP Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first digital transformation mandates in higher education | +3.2% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Hybrid learning models demanding real-time data flow | +2.8% | Global, accelerated in APAC and North America | Short term (≤ 2 years) |

| Government stimulus for digitising K-12 administration | +2.1% | North America, EU, with expansion to emerging markets | Medium term (2-4 years) |

| Rising cyber-insurance requirements for data-compliant ERP stacks | +1.9% | Global, with highest impact in North America and EU | Short term (≤ 2 years) |

| AI-powered predictive analytics improving enrollment and retention | +2.4% | North America, EU, expanding to APAC | Medium term (2-4 years) |

| Low-code platforms slashing customization cost | +1.8% | Global, with particular relevance in cost-sensitive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Digital Transformation Mandates in Higher Education

Universities worldwide adopted cloud-first policies that replaced campus data centers with scalable SaaS ERP suites. The California State University system illustrated operational savings and faster analytics after its cloud migration.[1]Rhea Kelly, “Scalable Cloud Strategies: Values for Higher Education,” Campus Technology, campustechnology.com SAP customers across APAC faced a 2027 cloud deadline that intensified upgrade planning. Institutions reported heightened security, continuous feature releases, and reduced downtime after abandoning on-premise frameworks. These advantages fostered integrated ecosystems linking finance, HR, and learning tools in a single data fabric.

Hybrid Learning Models Demanding Real-Time Data Flow

Post-2020 pedagogy required ERP backbones that merged in-person and virtual learning datasets. The Idaho Digital Learning Alliance used a centralized analytics hub that lifted course pass rates by 2.27% despite rising enrollments.[2]Google Cloud, “Idaho Digital Learning Alliance,” cloud.google.com Universities leveraged APIs to pull live signals from LMS, IoT, and student portals into risk dashboards with up to 90% retention-prediction accuracy. Vendor roadmaps consequently prioritized open integration frameworks and event-stream processing.

Government Stimulus for Digitising K-12 Administration

Federal grants under the Supporting America's School Infrastructure Program disbursed USD 37 million for facility data systems that often sit inside ERP suites. Florida allocated USD 25 million for technology career education, acknowledging ERP skills as workforce assets. American Rescue Plan funds also bolstered digital administration in school districts, heightening demand among cash-constrained K-12 buyers.

AI-Powered Predictive Analytics Improving Enrollment and Retention

Institutions embedded AI modules within ERP workflows to surface risk profiles, personalize outreach, and boost persistence. Southern New Hampshire University lifted retention from over 30% to nearly 80% using real-time advising triggers. The University of Kentucky recorded a 10% rise after targeting support programs driven by engagement metrics.[3]EDUCAUSE Review, “Avoiding the College Enrollment Cliff With AI,” er.educause.edu Vendors fused machine-learning engines with SIS records, marketing funnels, and financial aid data to identify prospects most likely to enroll.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget freezes at public institutions | -2.4% | Global, with highest impact in North America and EU | Short term (≤ 2 years) |

| Lengthy change-management cycles | -1.8% | Global, particularly affecting large institutions | Medium term (2-4 years) |

| Data-sovereignty regulations restricting multi-tenant SaaS | -1.6% | EU, expanding to other regions | Long term (≥ 4 years) |

| Shortage of ERP-literate administrators | -1.3% | Global, with acute shortages in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Freezes at Public Institutions

Major state systems imposed hiring and capital-spending cuts that delayed large-scale ERP upgrades. Sonoma State University eliminated 46 faculty positions and over 20 programs after a USD 24 million deficit tied to enrollment decline. Such austerity extended system lifecycles well beyond manufacturer support windows, forcing phased cloud migrations or shared-service strategies to lower upfront cost.

Lengthy Change-Management Cycles

Academic governance and calendar constraints often stretched ERP rollouts across multiple fiscal years. The Dallas Independent School District revealed staff resistance that slowed adoption despite robust training budgets. Idaho's Luma ERP project incurred USD 117 million in costs amid procurement reruns and user-acceptance hurdles. Extended timelines inflated total ownership cost and postponed efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Accelerates Migration

Cloud solutions commanded 63.85% of education ERP market share in 2024, expanding at a 15.1% CAGR as institutions relinquished on-premise servers in favor of elastic subscription models. Cloud vendors packaged automatic patching, zero-trust security, and disaster-recovery orchestration, attributes that heightened appeal during ransomware upticks. The education ERP market size for cloud deployments was projected to more than double by 2030 as multi-tenant architectures matured. Institutions that preserved hybrid footprints often did so to satisfy country-specific residency laws, but even these buyers mapped phased migrations for non-sensitive workloads. Vendor deadlines such as SAP’s 2027 cloud milestone in APAC further spurred accelerated timelines.

On-premise suites ceded relevance; administrators cited high maintenance overhead, hardware refresh cycles, and patch latency as deal breakers. Some research universities retained niche modules behind campus firewalls, yet they increasingly wrapped them in API gateways that synced with SaaS finance and human-capital cores. Subscription pricing also reshaped budgeting culture, distributing expenditure across operating rather than capital accounts.

By Institution Level: Vocational Training Centers Drive Growth

Higher education institutions held 48.76% of 2024 revenue, reflecting broad program portfolios and research compliance needs. However, vocational centers recorded a 14.89% CAGR, the fastest clip inside the education ERP market. Workforce reskilling imperatives demanded platforms that managed competency badges, apprenticeship logs, and employer feedback loops—requirements underserved by generic academic modules.

The Philippines’ Industry 4.0 training initiatives illustrated surging demand for flexible scheduling, equipment usage tracking, and micro-credential issuance. These features elevated procurement priority at technical and community colleges that supported adult learners. The education ERP market size linked to vocational centers was therefore on course to surpass USD 8 billion by 2030, benefiting vendors that tailored blue-collar skill taxonomies and job-matching APIs.

By End-User: Private Institutions Accelerate Adoption

Public entities retained 61.32% revenue share in 2024 due to scale, yet private institutions advanced at 14.62% CAGR through 2030. Tuition-driven business models rewarded rapid digital transformation that streamlined recruiting funnels and donor stewardship. The education ERP market size attributable to private campuses was forecast to reach USD 19 billion by decade end.

Private colleges bypassed lengthy legislative approvals, enabling quicker vendor selection and go-live cycles. Consortium buying groups among smaller faith-based schools emerged, sharing best-practice templates and integration work. Meanwhile, public systems piloted shared-service centers for HR and finance to stretch limited funds, but governance complexity slowed uniform adoption across campuses.

By Function: Student Information Systems Lead Integration

Student Information and Administration modules comprised 34.48% of revenue in 2024 and grew at 14.95% CAGR through 2030. Institutions demanded consolidated admission, registration, advising, and analytics tooling that eliminated data silos. Finance and Accounting modules kept pace as grant oversight and multi-currency tuition billing required granular tracking.

Integrated academic-program management climbed the priority list in competency-based education models. Monterrey Institute lifted retention and graduation after adopting Ellucian Banner for outcome mapping, proving that course sequencing analytics had tangible ROI. Procurement and inventory modules lagged because many universities already ran specialized research-equipment systems; nonetheless, connectors to the central ledger improved spend visibility.

Geography Analysis

North America held a 36.75% share in 2024 revenue on account of robust higher-education infrastructure and federal stimulus earmarked for administrative modernization. The American Rescue Plan injected nearly USD 122 billion into K-12 relief that accelerated ERP procurements, especially in states promoting cloud first agendas. Private-equity acquisitions such as Bain Capital’s USD 5.6 billion PowerSchool deal reinforced investor optimism in the region.

European growth steadied as GDPR shaped buying criteria. Institutions weighed private-cloud or sovereign-cloud instances to maintain compliance. The University of Siena achieved a 50% cut in student wait times after adopting a no-code platform that respected Italian data-hosting rules. Multilingual capabilities and regional funding mechanisms underpinned vendor roadmaps.

APAC emerged as the fastest-growing territory, fueled by tertiary enrollment hikes and government subsidies for digital campuses, with a CAGR of 14.12% during the forecast period. SAP’s 2027 cloud mandate forced universities to reconsider roadmaps, with many locking in phased modernization budgets by 2025. Pilot rollouts in Thailand and Australia highlighted the importance of post-launch support and user training to mitigate adoption dips.

Competitive Landscape

The education ERP market displayed moderate consolidation. Oracle, SAP, and Workday competed on extensive cloud suites that bundled ERP with analytics and HCM. Ellucian and Jenzabar focused on higher-education nuances, securing loyalty through specialized student success tooling. Bain Capital’s take-private transaction for PowerSchool and KKR’s acquisition of Instructure signaled intensified private-equity participation aimed at scaling AI innovation.

Technology differentiation pivoted toward embedded machine learning, low-code extensibility, and open API ecosystems. Johns Hopkins selected Workday for an enterprise-wide modernization spanning finance, HR, and supply chain, underscoring the pull of unified cloud stacks. White-space opportunities persisted among mid-sized colleges and emerging-market vocational centers where budgets and regulatory contexts differed from research-intensive universities.

Acquisition pipelines stayed active. IBM agreed to purchase Applications Software Technology LLC, enhancing consulting depth for Oracle Cloud implementations in the public-sector education vertical. Thesis and Ready Education drew growth investments to expand SIS and student engagement offerings, respectively, illustrating that niche specialists continued to carve defensible territories.

Education ERP Industry Leaders

Ellucian Company L.P.

Oracle Corporation

SAP SE

Workday Inc.

Unit4 N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Jenzabar reported that 134 institutions adopted its suite during 2024, alongside a new cloud finance module and Google Cloud alliance

- January 2025: IBM announced the acquisition of Applications Software Technology LLC to deepen Oracle Cloud ERP expertise for education clients

- June 2024: Bain Capital completed its USD 5.6 billion PowerSchool acquisition, pledging AI investments via the PowerBuddy roadmap

- October 2024: Transact Campus allied with Anthology to integrate payment and CRM modules with ERP cores for seamless campus workflows

Global Education ERP Market Report Scope

| Cloud |

| On-Premise |

| K-12 Schools |

| Higher Education |

| Vocational and Training Centers |

| Public Institutions |

| Private Institutions |

| Student Information and Administration |

| Finance and Accounting |

| Human Resources and Payroll |

| Academic and Curriculum Management |

| Procurement and Inventory |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment | Cloud | ||

| On-Premise | |||

| By Institution Level | K-12 Schools | ||

| Higher Education | |||

| Vocational and Training Centers | |||

| By End-User Type | Public Institutions | ||

| Private Institutions | |||

| By Function / Module | Student Information and Administration | ||

| Finance and Accounting | |||

| Human Resources and Payroll | |||

| Academic and Curriculum Management | |||

| Procurement and Inventory | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the global education ERP market value in 2025?

It peaked at USD 24.24 billion, rising toward USD 46.58 billion by 2030.

Which deployment model led education ERP adoption in 2024?

Cloud solutions held 63.85% market share, reflecting institutions’ shift from on-premise frameworks.

How are AI capabilities influencing education ERP investments?

Predictive analytics modules boosted retention to nearly 80% at early adopters, prompting wider rollouts.

Which region is expanding fastest?

APAC is experiencing the highest CAGR, supported by government digitization programs and upcoming cloud-migration deadlines.

What factor most restrains public-sector ERP projects?

Budget freezes have postponed large-scale upgrades, resulting in prolonged reliance on legacy systems.

Page last updated on: