Data Mining Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

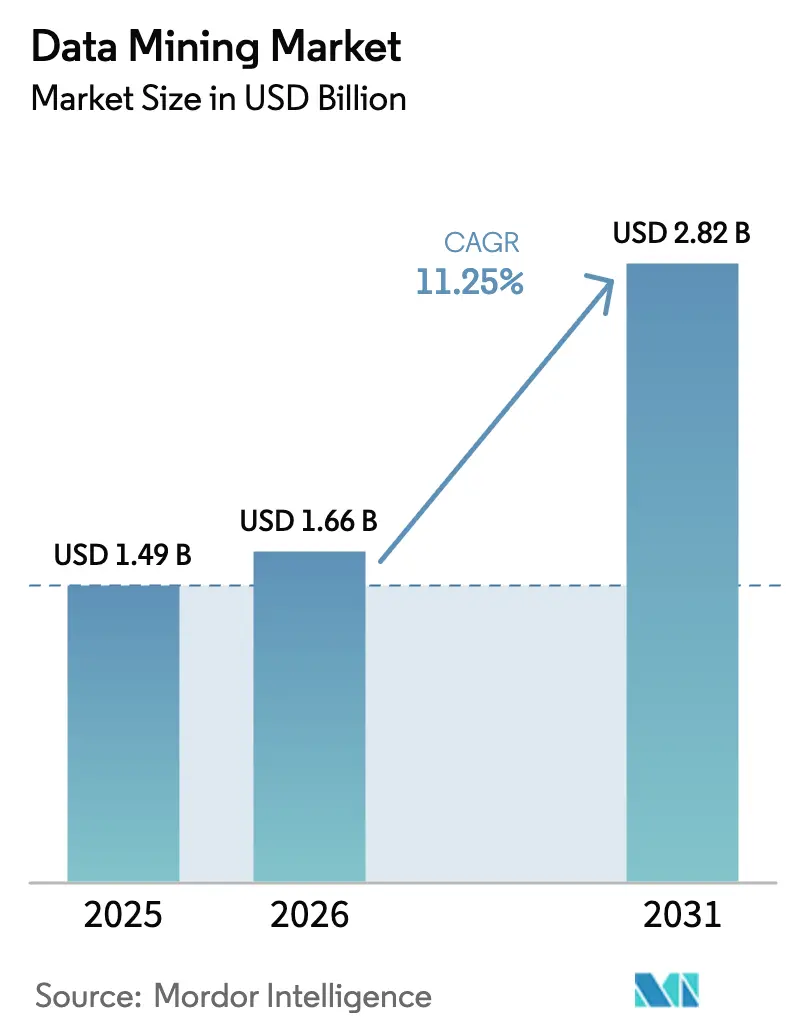

| Market Size (2026) | USD 1.66 Billion |

| Market Size (2031) | USD 2.82 Billion |

| Growth Rate (2026 - 2031) | 11.25% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

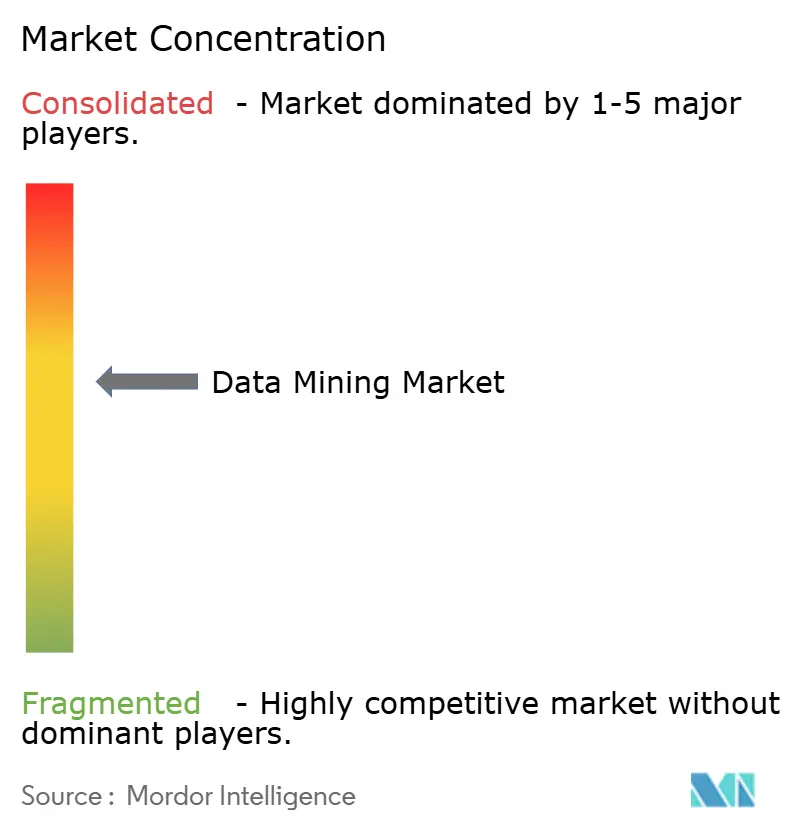

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Mining Market Analysis by Mordor Intelligence

The global data mining market size in 2026 is estimated at USD 1.66 billion, growing from 2025 value of USD 1.49 billion with 2031 projections showing USD 2.82 billion, growing at 11.25% CAGR over 2026-2031. This robust expansion stems from enterprises scaling AI-enabled analytics that turn raw information into business insight, alongside cloud-first models that lower entry barriers. Demand also rises as data centers’ electricity use in the United States climbed to 4.4% of national consumption in 2023 and could reach 9% by 2030, underscoring the infrastructure intensity behind large-scale analytics. AutoML platforms, edge-level mining, and strict regulatory reporting requirements further accelerate platform adoption, while escalating energy costs and a widening data-science skills gap temper growth prospects.

Key Report Takeaways

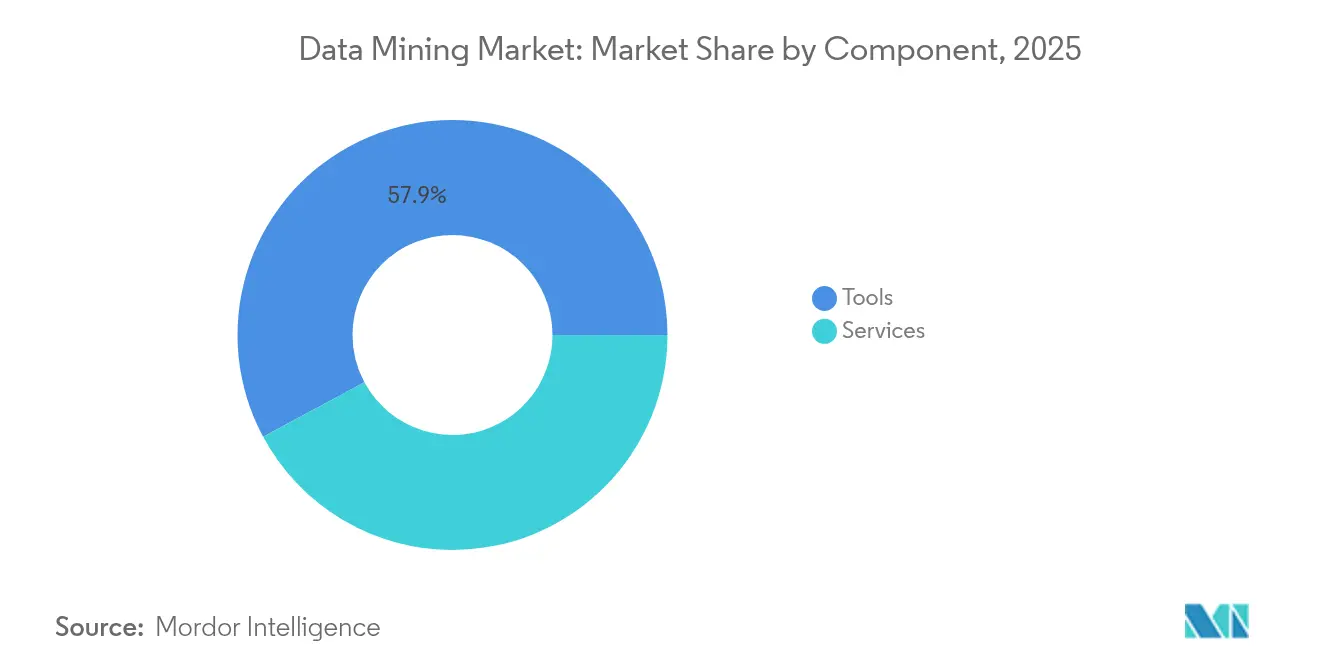

- By component, tools led with 57.85% share in 2025; the services segment is projected to grow at a 12.23% CAGR to 2031.

- By end-user enterprise size, large companies held 62.70% of the data mining market share in 2025, yet SMEs are set to expand at a 14.34% CAGR through 2031.

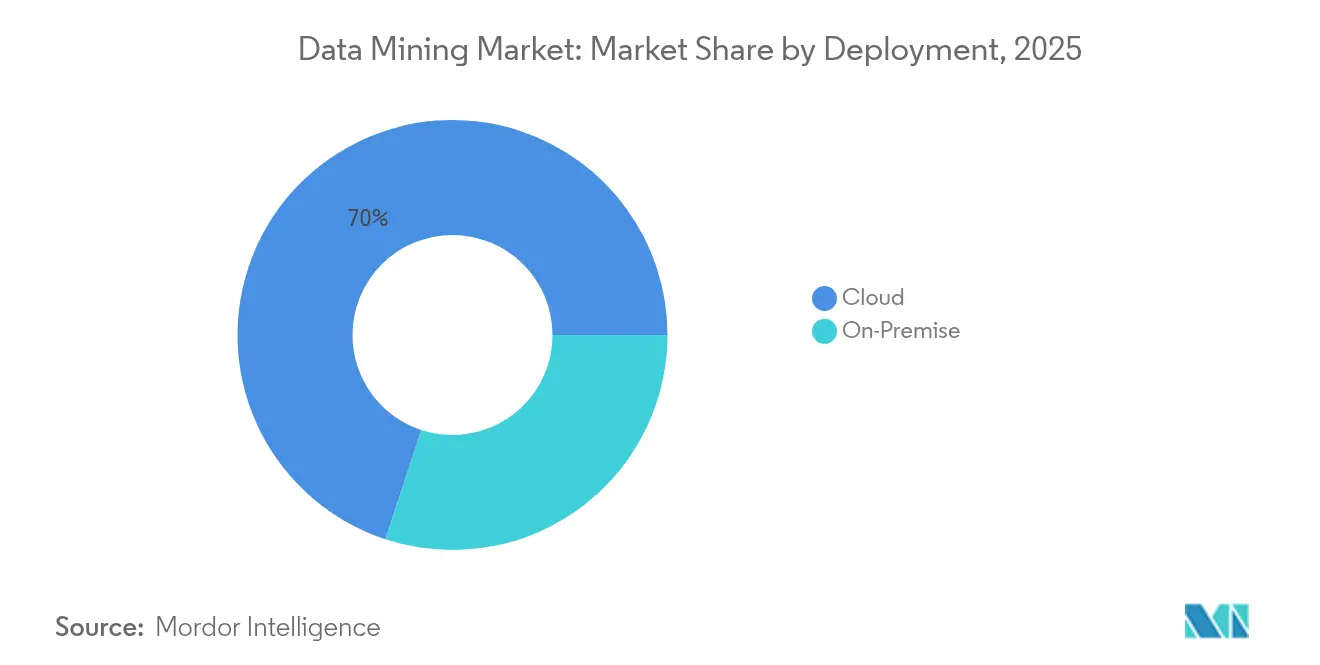

- By deployment, cloud captured 69.95% of the data mining market size in 2025 and is advancing at a 16.92% CAGR between 2026-2031.

- By end-user industry, BFSI commanded 21.05% of revenue in 2025, while healthcare and life sciences are forecast to grow at a 13.19% CAGR through 2031.

- By geography, North America held 34.30% revenue share in 2025; Asia-Pacific records the fastest growth at a 12.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Data Mining Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data explosion across IoT and enterprise systems | +2.8% | Global, led by Asia-Pacific IoT rollouts | Medium term (2-4 years) |

| Rapid enterprise adoption of AI-enabled analytics | +2.5% | North America and Europe extending to Asia-Pacific | Short term (≤ 2 years) |

| Cloud-first subscription models | +2.1% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Strict regulatory reporting requirements | +1.8% | North America and EU, expanding worldwide | Medium term (2-4 years) |

| Edge-level mining for industrial IoT | +1.4% | Manufacturing hubs in Asia-Pacific and North America | Long term (≥ 4 years) |

| AutoML democratisation for citizen users | +1.2% | Global, SME focus in emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data explosion across IoT and enterprise systems

Connected devices generate terabytes of sensor information each day, driving organisations to integrate sophisticated analytics that handle real-time and historical streams. Studies estimate that intelligent IoT will create between USD 3.9 trillion and USD 11.1 trillion in economic value by 2025 [1] J. Manyika, “Internet of Things Value 2025,” ScienceDirect, sciencedirect.com. Manufacturers adopting predictive maintenance report 8-12% cost savings and 35-45% lower downtime after applying AI-driven insights. Edge computing pushes first-stage processing closer to devices, which reduces latency and network traffic while opening new revenue pools for edge-optimised platforms within the data mining market.

Rapid enterprise adoption of AI-enabled analytics

Large corporations roll out domain-specific AI to improve fraud detection, customer segmentation, and operational efficiency. IBM’s generative AI revenue reached USD 6 billion in Q1 2025. JPMorgan now provides an internal LLM suite to 220,000 employees, while PwC equips 270,000 staff with an AI chatbot that drafts reports. These large-scale deployments showcase tangible ROI and create reference models that spur broader acceptance across the data mining market.

Cloud-first data-mining subscription models

Subscription pricing lowers upfront capital needs for analytics projects and ensures continuous platform upgrades. Oracle’s cloud services revenue climbed 21% year over year to USD 5.6 billion in its fiscal 2025 first quarter, while cloud infrastructure surged 45% to USD 2.2 billion. Flexible consumption patterns appeal to SMEs and mid-tier enterprises that previously lacked resources to deploy in-house clusters, enhancing market inclusivity.

Strict regulatory reporting requirements

Governments mandate clear audit trails and detailed disclosures for AI models. Europe’s AI Act compels model providers to document data lineage, and similar transparency clauses appear in pending U.S. legislation [2]Neudata, “Key Provisions in the EU AI Act,” Neudata, neudata.com. Financial institutions automate compliance reporting, while healthcare organisations apply privacy-preserving techniques to meet patient-data rules. Vendors that embed governance features gain an adoption edge in the data mining market.

Restraints Impact Analysis of Data Mining Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Heightened data-privacy and sovereignty laws | -1.9% | Global, led by EU and California | Short term (≤ 2 years) |

| Shortage of skilled data-science talent | -1.6% | Global, acute in advanced economies | Medium term (2-4 years) |

| Escalating energy costs for high-performance infrastructure | -1.2% | North America and Europe | Medium term (2-4 years) |

| Regulatory uncertainty around AI training data usage | -1.0% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Heightened data-privacy and sovereignty laws

New and revised privacy statutes raise compliance costs and limit cross-border data flows. The EU’s GDPR and state-level U.S. laws prompt firms to adopt differential privacy and federated learning, which add architectural complexity. Healthcare networks must balance patient confidentiality with clinical analytics, often turning to vendors such as Datavant for tokenised data pipelines that safeguard privacy while retaining analytical value.

Shortage of skilled data-science talent

Global demand for data scientists outpaces supply, with an estimated 220,000 open data roles in the United States alone for 2025 and 36% projected growth through 2033. Salaries for machine-learning engineers average USD 168,730, double that of data analysts, creating budget pressures for mid-sized businesses. AutoML softens the gap, yet complex projects still require expert oversight, constraining the pace of adoption within the data mining market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Data Mining Market Segment Analysis

By Component:

Services Accelerate Despite Tools DominanceTools accounted for 57.85% of revenue in 2025, reflecting the necessity of ETL pipelines, workbenches, machine-learning platforms, and visual analytics software in any data mining market deployment. Demand for these solutions remains steady as enterprises pursue unified platforms that handle ingestion, transformation, and modelling at scale. ETL utilities address persistent data-quality challenges across legacy systems, while next-generation workbenches deliver low-code features that encourage broader user participation.

The services segment grows the fastest at a 12.23% CAGR to 2031 as firms seek specialised integration, model-tuning, and managed-service arrangements. Professional services dominate thanks to custom architectures that weave analytics backbones into existing ERP and CRM landscapes, whereas managed offerings attract companies that lack in-house expertise. Platform vendors now bundle consulting with subscriptions, creating integrated ecosystems that deepen customer lock-in and elevate the overall data mining market value proposition.

By End-user Enterprise Size:

SMEs Drive Growth Through Cloud AdoptionLarge enterprises retained 62.70% of the data mining market share in 2025 based on their sizeable IT budgets and multi-department analytics programs. Their investments span customer behaviour modelling, predictive maintenance, and enterprise risk analytics, aided by partners such as Databricks whose top 50 customers each spend more than USD 10 million annually.

SMEs represent the most dynamic growth pocket, projected to expand at 14.34% CAGR through 2031. The OECD D4SME study shows that 72% of SMEs now use data to inform decisions, yet only 10% have deployed big-data analytics . Cloud subscriptions, low-code platforms, and vertical AI packages lower entry barriers, enabling smaller firms to pursue targeted initiatives in marketing, inventory optimisation, and customer support. As SMEs comprise 90% of global businesses, their digital adoption trajectory will heavily influence the future scale of the data mining market.

By Deployment:

Cloud Dominance Accelerates Edge IntegrationThe cloud model captured 69.95% of the data mining market size in 2025 and is set to grow at 16.92% CAGR to 2031. Clients benefit from elastic compute, frequent upgrades, and usage-based fees that align cost with value. On-premise installations persist in heavily regulated sectors, while hybrid architectures gain momentum as firms mix local control with cloud scalability.

Edge deployments complement this hierarchy by executing latency-sensitive analytics on factory floors, oilfields, and vehicles, trimming bandwidth needs and cutting response times. Emerging architectures send summarised insights from edge nodes to central clouds for deep modelling, creating a layered system that balances immediacy with depth. Vendors that integrate edge orchestration into their portfolios enhance competitiveness across the data mining market.

By End-user Industry:

Healthcare Emerges as Growth LeaderBFSI led spending with 21.05% of 2025 revenue due to intense regulatory scrutiny and fraud-related losses, both of which drive demand for explainable AI and transaction monitoring. TCS notes that 82% of financial institutions increased AI budgets during 2024, with priorities spanning virtual assistance and personalised services.

Healthcare and life sciences register the highest CAGR at 13.19% through 2031 as electronic health records, remote diagnostics, and genomics create data sets ripe for mining. Privacy-preserving analytics enable clinical insight without exposing patient identity. Manufacturing, retail, telecom, and public-sector agencies adopt predictive maintenance, demand forecasting, and cybersecurity analytics respectively, contributing diversified revenue streams that buoy the overall data mining market.

Geography Analysis

North America Data Mining Market

North America generated 34.30% of 2025 revenue owing to its concentration of hyperscale cloud providers, venture funding, and enterprise AI deployments. United States utilities supplied 4.4% of total electricity to data centers in 2023, with projections of a 9% share by 2030 as analytics workloads intensify . Canada applies analytics in resource extraction and healthcare, while Mexico’s manufacturers adopt real-time quality inspection systems. Federal frameworks balance innovation and privacy, yet divergent state rules increase compliance complexity for cross-border projects.

APAC Data Mining Market

Asia-Pacific is the fastest-expanding region with a 12.07% CAGR to 2031, propelled by government digital-economy agendas and rapid data-center construction. China leads in industrial IoT, Japan and South Korea focus on automotive analytics, and ASEAN governments invest in smart-city platforms. Edge computing and 5G rollouts support low-latency applications, keeping the data mining market on a steep growth curve in the region.

Europe Data Mining Market

Europe maintains steady momentum where GDPR and the AI Act encourage responsible AI while stimulating demand for governance-enabled platforms. Germany champions Industry 4.0 analytics, the United Kingdom underscores financial-services innovation, and Nordic countries deploy advanced telecom analytics in renewable energy grids. High energy prices and data-sovereignty concerns nudge certain workloads toward local cloud nodes, shaping a regionally balanced data mining market strategy.

Competitive Landscape

The industry shows moderate concentration. IBM, Oracle, Microsoft, SAS, and SAP combine broad software portfolios with deep client relationships, capturing nearly half of global revenue. IBM reported USD 6 billion in generative-AI sales in Q1 2025. Oracle posted USD 13.3 billion total revenue in the same quarter, with cloud services up 21%. Microsoft generated USD 245 billion overall 2024 revenue, and Azure grew 30% year over year, reinforcing platform heft.

Specialists such as Teradata, with USD 570 million public-cloud ARR growing 26%, and SAS, generating more than USD 3 billion annually, preserve share through domain expertise. Disruptors including Databricks forecast USD 3.7 billion annualised revenue by July 2025, expanding 50% year on year, powered by its lakehouse architecture that merges analytics and AI workloads.

Strategic MandA reshapes the field. IBM acquired Hakkoda to enhance Snowflake implementation services, while Snowflake purchased Reka AI for USD 1 billion to fold cutting-edge models into its platform. OpenAI added vector-database specialist Rockset to bolster enterprise retrieval. Partnerships, such as Snowflake and Acxiom’s AI-ready marketing lake, illustrate ecosystem-centric competition that continually raises the capability bar across the data mining market.

Data Mining Industry Leaders

Oracle Corporation

IBM Corporation

SAS Institute Inc.

Teradata Corporation

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Data Mining Market Companies Covered in this Report

- IBM Corporation

- Oracle Corporation

- Microsoft Corporation

- SAS Institute Inc.

- Teradata Corporation

- SAP SE

- Altair Engineering Inc. (RapidMiner)

- KNIME AG

- Google LLC (Kaggle)

- Amazon Web Services Inc.

- Alteryx Inc.

- OpenText Corporation

- Hitachi Vantara LLC

- TIBCO Software Inc.

- QlikTech International AB

- MicroStrategy Incorporated

- Sisense Inc.

- Orange S.A. (Orange Data Mining)

- Togaware Pty Ltd (Rattle GUI)

- FICO (Fair Isaac Corporation)

- H2O.ai Inc.

- Dataiku SAS

- Databricks Inc.

Recent Industry Developments in Data Mining Market

- June 2025: Snowflake partnered with Acxiom to deliver AI-powered marketing data infrastructure that blends first-party data with secure analytics.

- June 2025: IBM acquired Seek AI and opened a New York AI accelerator, adding natural-language query talent to its Watsonx portfolio.

- April 2025: Dataminr secured USD 100 million from Fortress Investment Group to accelerate enterprise expansion and international growth

- April 2025: IBM completed its acquisition of Hakkoda, adding hundreds of SnowPro-certified consultants to its data-transformation practice.

Data Mining Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the global data-mining market as revenue generated from purpose-built software tools and the related professional or managed services that apply statistical, machine-learning, and AI techniques to uncover patterns in structured and unstructured enterprise data.

Scope exclusion: We exclude bespoke in-house analytics stacks, single-project consulting engagements, and digital-mining technologies designed for physical ore extraction.

Segments Covered in This Report

- By Component

- Tools

- ETL and Data Preparation

- Data-Mining Workbench

- ML and Advanced Analytics Platforms

- Visualisation and Reporting

- Services

- Professional Services

- Managed Services

- Tools

- By End-user Enterprise Size

- Small and Medium-Sized Enterprises (SMEs)

- Large Enterprises

- By Deployment

- Cloud

- On-Premise

- Hybrid

- By End-user Industry

- BFSI

- IT and Telecom

- Government and Defence

- Manufacturing

- Healthcare and Life Sciences

- Energy and Utilities

- Retail and E-commerce

- Transportation and Logistics

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts spoke with data-platform architects, procurement leads in banking, and regional cloud resellers across North America, Europe, and Asia-Pacific. These interviews clarified seat-based pricing, adoption hurdles, and churn triggers, helping us triangulate assumptions flagged during desk work. This is where Mordor Intelligence differentiates, as our frequent re-contacts ensure every major geography and buyer cohort is represented.

Desk Research

We began by compiling macro and ICT spending baselines from the US Bureau of Labor Statistics, Eurostat, and OECD datasets, then aligned those with company disclosures retrieved through SEC EDGAR and annual reports. Subscriptions to Dow Jones Factiva and D&B Hoovers supplied real-time revenue splits and M&A indicators, while Questel patent counts signaled emerging algorithm families. Additional context came from technology associations such as the Cloud Security Alliance, Bitkom, and open customs data on analytics software flows. The sources cited are illustrative; many other public resources were reviewed to corroborate figures and fill data gaps.

Market-Sizing & Forecasting

We constructed a top-down demand pool by mapping enterprise analytics budgets and isolating the share earmarked for dedicated data-mining solutions, then cross-checked totals with sampled average-selling-price times user-volume roll-ups shared by respondents. Key model variables include cloud migration ratios, algorithm-training compute costs, average dataset growth per employee, regulation-driven audit workloads, and data-science talent availability. A multivariate regression, anchored on cloud penetration and data-volume expansion, drives the outlook for the forecast period. Our baseline value is established through this methodology.

Data Validation & Update Cycle

Outputs pass a three-layer analyst review; variance thresholds trigger fresh expert calls, and models refresh annually, with interim updates after material events to keep clients current.

How Mordor Intelligence's Data Mining Market Size Compares to Other Published Estimates

Published estimates vary because firms pick different component mixes, base years, and currency treatments, which alters totals before any forecasting begins.

Mordor's disciplined scope alignment, annual refresh cadence, and hybrid validation curb those distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.49 B (2025) | Mordor Intelligence | - |

| USD 1.31 B (2025) | Global Consultancy A | Tools-only scope; limited primary checks |

| USD 1.19 B (2024) | Global Consultancy B | Excludes services; earlier base year |

| USD 1.17 B (2024) | Industry Journal C | Narrow SME sampling; constant-2023 currency rates |

The comparison shows that by integrating services revenue, running multi-source validations, and updating models every twelve months, we provide decision-makers a transparent, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current size of the data mining market?

The data mining market stands at USD 1.66 billion in 2026 and is projected to grow steadily to USD 2.82 billion by 2031.

Which component segment is growing the fastest?

Services exhibit the highest momentum with a 12.23% CAGR through 2031 as firms seek integration expertise and managed analytics.

How dominant is cloud deployment in this space?

Cloud models captured 69.95% of 2025 revenue and are expanding at a 16.92% CAGR, reflecting the shift to scalable, pay-as-you-use analytics.

Which industry vertical will lead future growth?

Healthcare and life sciences are forecast to post the strongest 13.19% CAGR through 2031 as digital health records and genomics data explode.

Why is Asia-Pacific the fastest-growing region?

Massive digital infrastructure investments, smart-city initiatives, and rapid industrial IoT adoption fuel a 12.07% regional CAGR.

What key restraint could slow adoption?

A global shortage of skilled data-science talent limits in-house project capacity, prompting higher reliance on external services and AutoML tools.

Page last updated on: