Agentic AI In Education And Learning Technologies Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

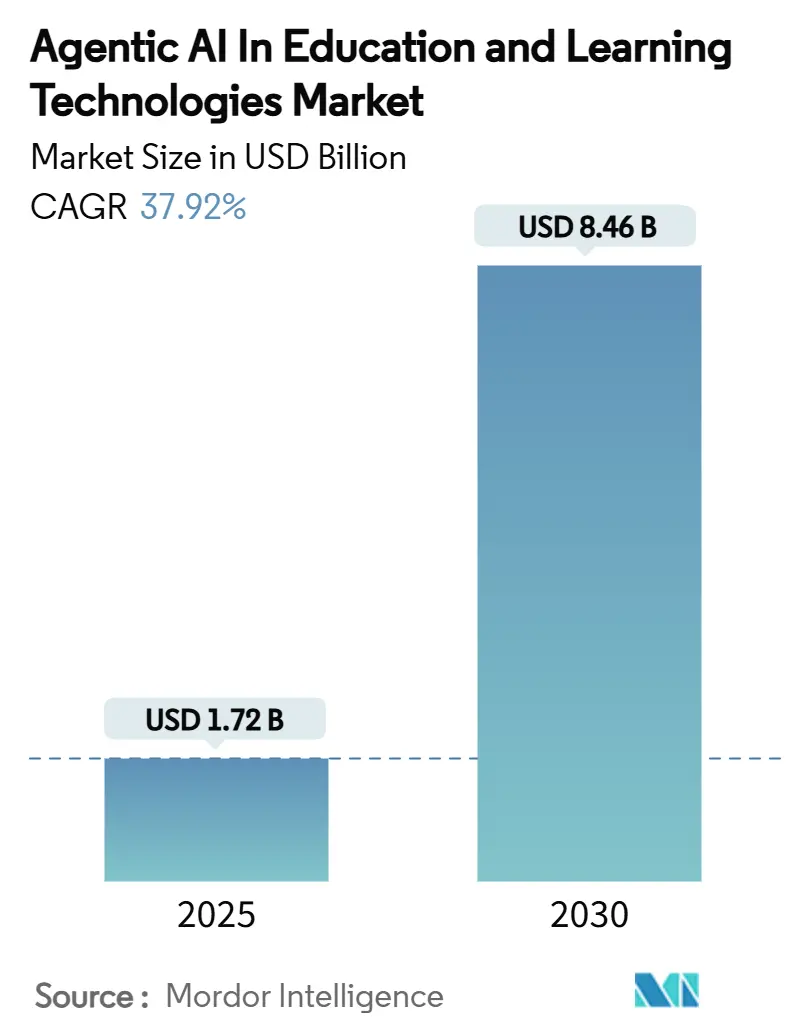

| Market Size (2025) | USD 1.72 Billion |

| Market Size (2030) | USD 8.46 Billion |

| Growth Rate (2025 - 2030) | 37.92% CAGR |

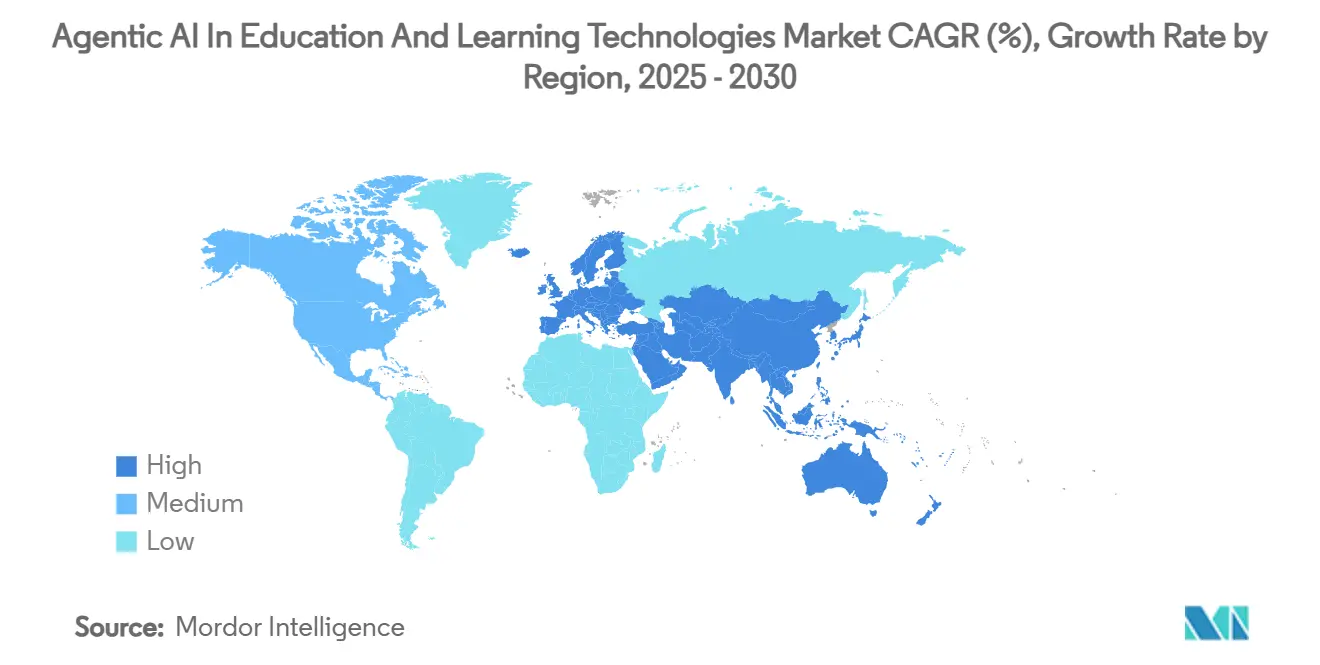

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agentic AI In Education And Learning Technologies Market Analysis by Mordor Intelligence

The Agentic AI in Education and Learning Technologies market is valued at USD 1.72 billion in 2025 and is forecast to reach USD 8.46 billion by 2030, expanding at a 37.92% CAGR. Current momentum reflects an industry-wide pivot from static e-learning tools toward autonomous agents that generate content, orchestrate learning paths, and make real-time instructional decisions. Robust government funding, such as the US Executive Order allocating USD 3.3 billion for AI research in fiscal 2025, signals sustained policy support. At the institutional level, measurable uplifts-Aurora Public Schools recorded a 28% improvement in literacy proficiency after adopting AI tutors-demonstrate the technology’s educational ROI.[1]“Executive Order on the Safe, Secure, and Trustworthy Development and Use of Artificial Intelligence,” WhiteHouse.gov, whitehouse.gov Strategic cloud investments in Southeast Asia lower entry barriers and accelerate deployments, while advances in large language models unlock multimodal capabilities that improve engagement and retention. Nevertheless, privacy regulation, teacher re-skilling needs, and high inference costs in low-income regions temper the market’s near-term velocity.

Key Report Takeaways

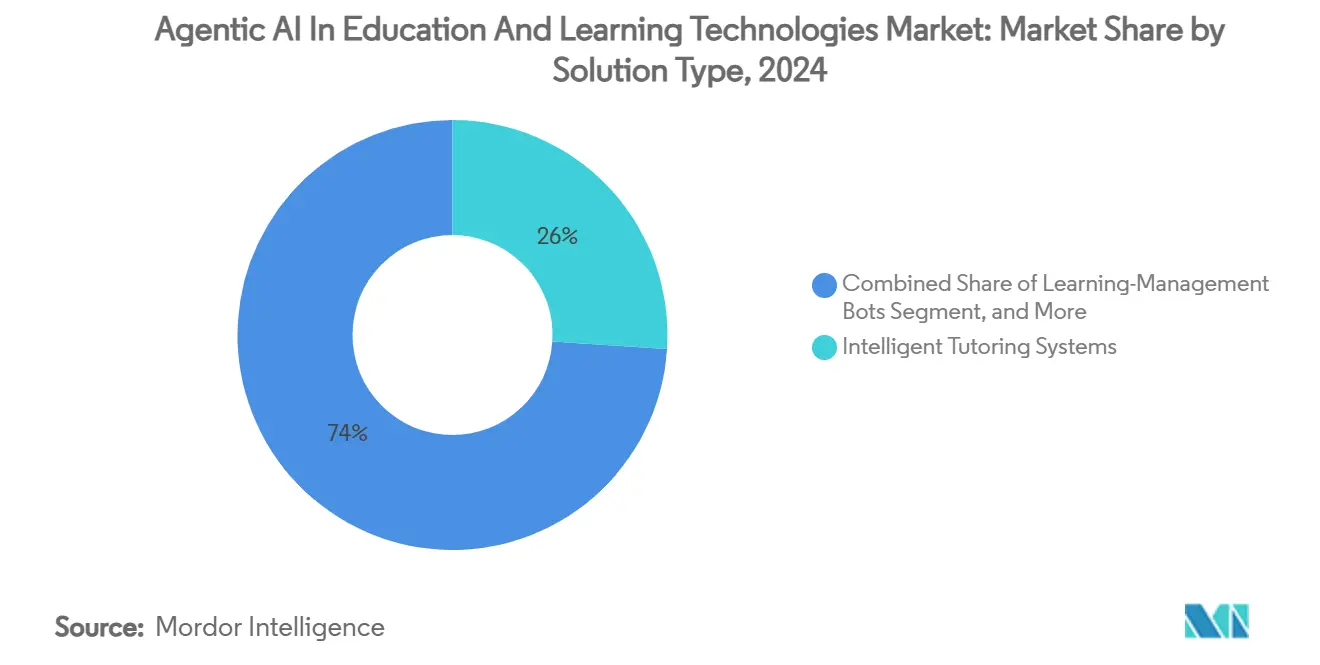

- By solution type, Intelligent Tutoring Systems led with 26.04% of the Agentic AI in Education and Learning Technologies market share in 2024; Assessment and Feedback Agents are projected to expand at a 44.36% CAGR through 2030.

- By deployment model, cloud platforms accounted for 71.64% of the Agentic AI in Education and Learning Technologies market size in 2024 and are set to grow at a 42.58% CAGR to 2030.

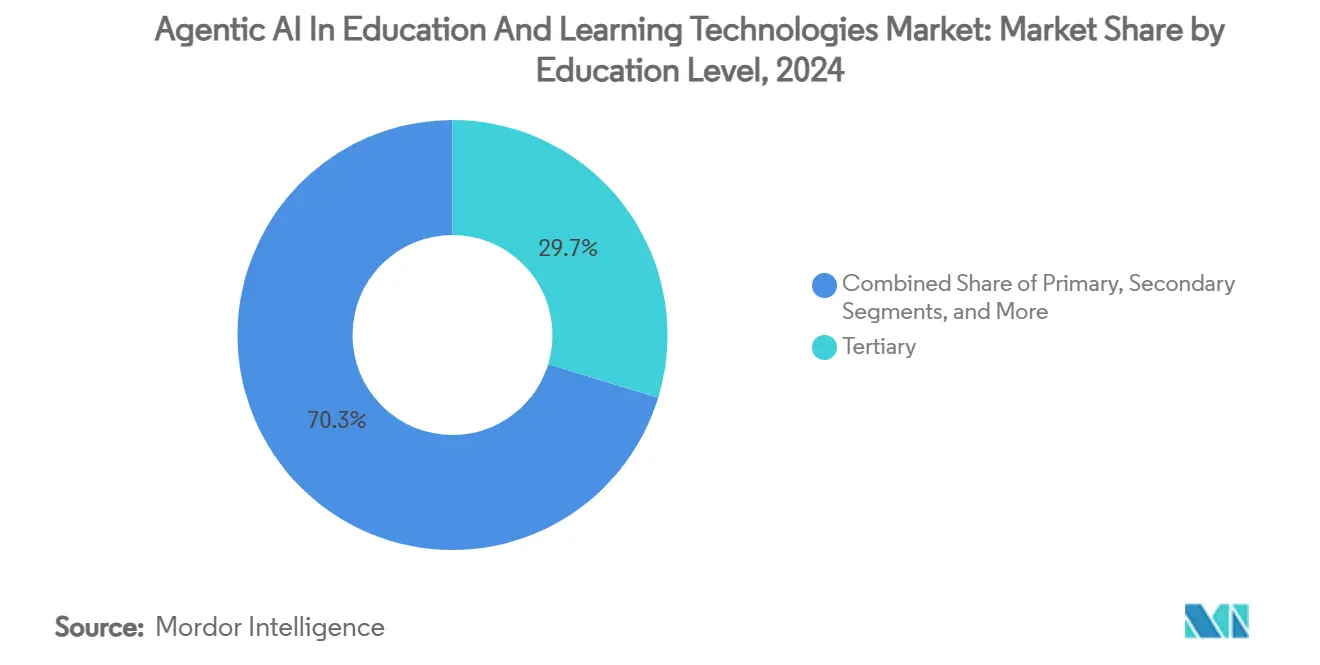

- By education level, tertiary institutions captured 29.71% of the Agentic AI in Education and Learning Technologies market size in 2024, while continuing education posts the fastest 42.78% CAGR through 2030.

- By end-user, K-12 institutions held 33.81% of the Agentic AI in Education and Learning Technologies market share in 2024; corporate and professional training is forecast to register a 43.81% CAGR to 2030.

- By geography, North America commanded 37.71% of the Agentic AI in Education and Learning Technologies market share in 2024, whereas Asia-Pacific is progressing at a 44.82% CAGR over the forecast horizon.

Global Agentic AI In Education And Learning Technologies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adaptive learning demand for personalised instruction | +8.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Government funding and national AI-Ed strategies | +7.5% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Cloud‐based delivery lowering IT barriers | +6.8% | Global, accelerated in emerging markets | Short term (≤ 2 years) |

| Rich data exhaust from LMS and classroom IoT | +5.1% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Emergence of LLM-powered autonomous content agents | +4.9% | Global, led by technology hubs | Long term (≥ 4 years) |

| Micro-credentialing driving competency verification bots | +3.8% | North America & EU, corporate training focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adaptive Learning Demand for Personalised Instruction

Institutions increasingly abandon one-size-fits-all models in favor of agents that adjust difficulty, modality, and sequencing in real time. A 28% literacy-rate jump in Aurora Public Schools validates the approach as more than a pilot exercise. Patent activity intensifies-IBM’s learner-embedding technology under US10282411B2 shows how natural-language analytics refine individualized curricula.[2]International Business Machines Corporation, “System, Method, and Recording Medium for Natural Language Learning,” US Patent 10,282,411 B2, patents.google.com Positive student sentiment at UC San Diego, where 70% favored AI tutors over traditional support, confirms rising learner acceptance. Neurosymbolic AI widens the personalization frontier by pairing knowledge graphs with neural networks to match content precisely to each learner’s cognitive profile. These factors collectively reinforce an 8.2% incremental lift in forecast CAGR.

Government Funding and National AI-Ed Strategies

Sovereign competitiveness agendas are translating into rapid capital deployment. China’s nationwide AI-education mandate by 2025 accelerates domestic demand, while the US National Science Foundation earmarked USD 8 million for EducateAI in 2025. South Korea’s LG- and Samsung-backed robot roll-out underscores public-private orchestration. The EU’s Digital Education Action Plan funds AI literacy in alignment with rigorous GDPR safeguards. Japan’s appeal to OpenAI for a regional headquarters highlights policy-driven ecosystem magnetism. Such top-down initiatives shorten sales cycles and reduce perceived risk for institutions contemplating adoption.

Cloud-Based Delivery Lowering IT Barriers

Cloud infrastructure neutralizes capital-expenditure hurdles that once restricted AI to elite universities. Microsoft’s USD 2.2 billion investment in Malaysia exemplifies hyperscalers’ regional edge build-outs that offer instant access to model-training capacity. Amazon’s hands-on AI education service (US11551652) demonstrates how platform-as-a-service abstracts complexity, letting educators work at the application layer. Smaller schools leverage the same multimodal agents as research powerhouses, flattening competitive disparities. Continuous remote updates ensure pedagogy keeps pace with model improvements, anchoring a 6.8% boost to market CAGR.

Rich Data Exhaust from LMS and Classroom IoT

High-velocity data streams from learning-management systems and sensor-based classrooms feed ever-deeper learner models. Patents like US10559215B2 detail multi-modal cognition frameworks that convert behavioral signals into dynamic reward structures.[3]James R. Kozloski et al., “Education Reward System and Method,” US Patent 10,559,215 B2, patents.google.com Eye-tracking and biometric sensors flag disengagement before grades decline, enabling preemptive intervention. While privacy regimes tighten, compliant analytics pipelines that anonymize and encrypt data unlock powerful predictive insight. Institutions with mature data architectures build defensible differentiation by training agents on proprietary engagement patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict student-data privacy regulations (FERPA, GDPR) | -4.2% | Global, strictest in EU and North America | Medium term (2-4 years) |

| Teacher digital-skill gaps and change-management hurdles | -3.8% | Global, acute in developing regions | Long term (≥ 4 years) |

| Hallucination-led instructional liability risks | -2.9% | Global, regulatory uncertainty | Short term (≤ 2 years) |

| High real-time inference costs in low-income regions | -2.1% | Emerging markets, rural areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict Student-Data Privacy Regulations (FERPA, GDPR)

Robust personalization depends on sensitive behavioral and performance data, yet regulations demand explicit consent, minimization, and deletion on request. Autonomous agents complicate accountability by making independent data-handling decisions, exposing institutions to fines. Solutions combine on-device processing with differential privacy techniques, but such safeguards increase development cycles and cost, shaving 4.2% from potential CAGR.

Teacher Digital-Skill Gaps and Change-Management Hurdles

Effective AI adoption transforms educators into facilitators who audit agent outputs, tune prompts, and curate resources. Many teachers lack these competencies, necessitating extensive professional development. The USD 23 million Microsoft-OpenAI-Anthropic teacher-training initiative illustrates the scale of reskilling. Resistance is strongest where educators fear erosion of professional autonomy, extending adoption timelines beyond the initial technology purchase.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Tutoring Systems Lead Content Revolution

Intelligent Tutoring Systems held 26.04% of the Agentic AI in Education and Learning Technologies market share in 2024, demonstrating institutional confidence in mature learner-modeling algorithms. The segment’s robust foundations allow rapid integration of generative engines that tailor explanations and assessments on the fly, expanding addressable use cases. Assessment and Feedback Agents are projected to grow at 44.36% CAGR as institutions seek automated grading of open-ended responses, a traditional bottleneck in scaling personalized instruction.

Hybrid agent architectures merge rule-based pedagogy with creative LLM components, enhancing student engagement. Platforms featuring multimodal capabilities-text, audio, and simulation-drive better retention, thereby widening adoption across STEM and language courses. The Agentic AI in Education and Learning Technologies market size for content-generation agents is expected to rise sharply as curriculum-design bots mature, yet tutoring remains the gateway purchase that seeds broader platform penetration.

By Deployment Model: Cloud Dominance Accelerates Innovation

Cloud implementations captured 71.64% of the Agentic AI in Education and Learning Technologies market size in 2024, reflecting hyperscaler efforts to bundle AI services with education-specific compliance frameworks. Subscription pricing converts capital expenditure into operational outlays, aligning costs with enrollment cycles. Hybrid architectures grow where institutions want local control over sensitive datasets while bursting to cloud for training peaks, sustaining a 42.58% CAGR for cloud services overall.

Edge-inference advances ensure latency-sensitive tasks such as voice feedback remain performant even on modest bandwidth. Meanwhile, on-premise deployments persist in defense academies and healthcare schools requiring strict data sovereignty, but their relative share declines. As governments impose residency clauses, regional cloud zones proliferate, lowering compliance friction and fortifying the cloud’s strategic centrality.

By Education Level: Tertiary Leadership Drives Innovation

Universities held 29.71% of the Agentic AI in Education and Learning Technologies market size in 2024 and act as testbeds for cutting-edge agentic experimentation. Research budgets fund bespoke LLM fine-tuning for domain-specific content such as medical diagnostics or quantum computing. Continuing education, growing at 42.78% CAGR, capitalizes on micro-credential demand from professionals seeking career pivots.

Primary and secondary schools adopt AI more cautiously, focusing on foundational literacy and numeracy gains. Nonetheless, K-12 pilots that demonstrate substantial outcome lifts often trigger district-wide scale-ups, creating a pipeline that feeds future tertiary adoption. Adult-learning platforms integrate workplace analytics, allowing agents to map learning outcomes directly to job performance, tightening enterprise ROI narratives.

By End-User: K-12 Institutions Pioneer Scalable Solutions

K-12 institutions accounted for 33.81% of the Agentic AI in Education and Learning Technologies market share in 2024, leveraging standardized curricula and high student volumes for scale effects. Cloud-hosted dashboards give administrators district-level insight into agent efficacy, reinforcing procurement decisions. Corporate and professional training posts a 43.81% CAGR as enterprises embed AI into talent-management suites for personalized upskilling.

Higher-education players prioritize advanced research and cross-faculty collaboration, while vocational centers deploy agents for hands-on simulation in sectors like welding and nursing. Lifelong-learning platforms bundle AI tutors with subscription libraries, monetizing self-directed adult learners. This end-user diversity cushions the overall market against cyclical funding variations in any single education tier.

Geography Analysis

North America retained 37.71% of the Agentic AI in Education and Learning Technologies market share in 2024, supported by deep venture-capital pools, favorable IP regimes, and the presence of foundational model vendors. Federal and state grants de-risk early adoption, while privacy statutes such as FERPA create clear compliance playbooks that vendors can operationalize into product features. Cross-border collaborations with Canadian research labs further enrich the innovation ecosystem.

Asia-Pacific is the fastest-growing geography at a 44.82% CAGR. China’s 2025 mandate for AI-infused curricula triggers immediate procurement across public schools, and massive population baselines amplify absolute spending. Japan’s attraction of OpenAI’s Indo-Pacific hub underscores regional talent depth, while Indonesia and Malaysia secure multi-billion-dollar cloud investments that democratize access for emerging-market institutions. Cultural receptivity to new technology expedites classroom integration, reducing sales-cycle friction relative to Western markets.

Europe couples stringent GDPR enforcement with substantial digital-education grants, spurring demand for privacy-preserving agent architectures. Policymakers champion ethical-AI frameworks, prompting vendors to embed explainability and bias-detection modules as default. South America and the Middle East & Africa remain nascent but promising; the cloud’s pay-as-you-go model enables universities to pilot AI without upfront hardware spend, laying groundwork for broader regional uptake once connectivity gaps close.

Competitive Landscape

The Agentic AI in Education and Learning Technologies industry remains moderately fragmented, with incumbent ed-tech firms, cloud hyperscalers, and AI-native startups vying for mindshare. Duolingo’s 38% year-over-year revenue bump in Q1 2025 validates the monetization power of personalized agents at scale. Traditional publishers such as Pearson partner with big-tech firms to embed generative models into legacy content libraries, safeguarding relevance while accelerating feature velocity.

Technology giants leverage horizontal AI stacks-compute, orchestration, and foundation models-to enter education through strategic alliances. Microsoft’s free Khanmigo for Teachers program exemplifies a land-and-expand tactic: seed classrooms with value, then upsell premium analytics. Startups differentiate via domain depth; SchoolAI’s focus on classroom-level workflows yielded USD 25 million Series A funding and a footprint in 1 million classrooms across 80 countries.

Intellectual-property filings surge as competitors race to lock in proprietary tutor personas, assessment protocols, and multimodal learning objects. Patents such as US12261893 on reinforcement-learning-based communication management showcase how vendors seek defensible positions in adaptive dialogue. Over the next five years, expect roll-ups of niche assessment or scheduling bots by broader platform providers aiming for full-suite offerings that deliver seamless learner journeys from discovery to credentialing.

Agentic AI In Education And Learning Technologies Industry Leaders

Duolingo Inc.

Carnegie Learning, Inc.

DreamBox Learning, Inc.

Squirrel AI Learning, Inc.

2U, Inc. (edX)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SchoolAI raised USD 25 million in Series A funding to expand its AI-powered classroom tools, which are currently used in over 1 million classrooms across 80 countries, demonstrating significant market validation for agentic AI educational platforms. The capital accelerates product localization and boosts sales capacity.

- April 2025: The United States Executive Order on AI Education was signed, establishing federal coordination for AI integration in education systems and allocating USD 3.3 billion for AI research and development in fiscal year 2025. The directive de-risks procurement for public schools and catalyzes vendor-ecosystem growth.

- March 2025: Microsoft, OpenAI, and Anthropic announced a USD 23 million investment in the National Academy for AI Instruction to train 400,000 K-12 teachers over 5 years, addressing the critical skills gap in AI education implementation. The program creates a skilled downstream user base for their AI services.

- March 2025: China mandated AI education nationwide by 2025, with Beijing leading early implementation efforts as part of the country's broader strategy to enhance technology education and maintain global AI competitiveness. The policy ensures guaranteed domestic demand for AI-education solutions.

Global Agentic AI In Education And Learning Technologies Market Report Scope

| Curriculum Design Agents |

| Intelligent Tutoring Systems |

| Learning-Management Bots |

| Assessment and Feedback Agents |

| Administrative Automation Agents |

| Cloud-based |

| On-premise |

| Hybrid |

| Primary |

| Secondary |

| Tertiary |

| Continuing Education |

| K-12 Institutions |

| Higher-Education Institutions |

| Corporate and Professional Training |

| Vocational and Skill-Development Centres |

| Lifelong/Adult Learners |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Solution Type | Curriculum Design Agents | ||

| Intelligent Tutoring Systems | |||

| Learning-Management Bots | |||

| Assessment and Feedback Agents | |||

| Administrative Automation Agents | |||

| By Deployment Model | Cloud-based | ||

| On-premise | |||

| Hybrid | |||

| By Education Level | Primary | ||

| Secondary | |||

| Tertiary | |||

| Continuing Education | |||

| By End-User | K-12 Institutions | ||

| Higher-Education Institutions | |||

| Corporate and Professional Training | |||

| Vocational and Skill-Development Centres | |||

| Lifelong/Adult Learners | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected growth rate for the Agentic AI in Education and Learning Technologies market?

The market is expected to expand at a 37.92% CAGR from 2025 to 2030, rising from USD 1.72 billion to USD 8.46 billion.

Which solution segment currently leads the market?

Intelligent Tutoring Systems lead, holding 26.04% of the Agentic AI in Education and Learning Technologies market share in 2024.

Why is Asia-Pacific considered the fastest-growing region?

Aggressive government mandates, substantial cloud investments, and large student populations are driving a 44.82% CAGR in Asia-Pacific.

What is the primary deployment preference among institutions?

Cloud-based models dominate with 71.64% of the market in 2024, thanks to scalable infrastructure and lower upfront costs.

How are data-privacy regulations affecting adoption?

Strict frameworks such as FERPA and GDPR impose compliance costs and data-handling constraints, reducing forecast CAGR by an estimated 4.2%.

What is the biggest regulatory restraint on adoption?

Strict student-data privacy frameworks such as FERPA and GDPR reduce the market’s projected CAGR by 4.2%.

Page last updated on: