Mobile Video Advertising Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

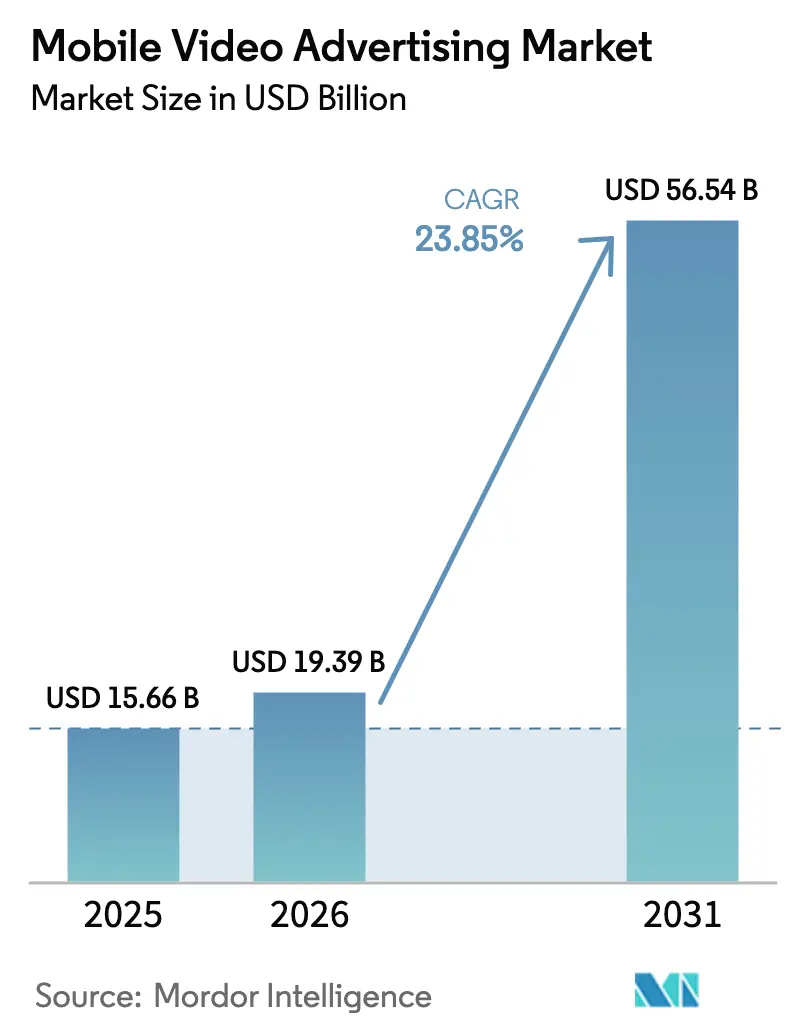

| Market Size (2026) | USD 19.39 Billion |

| Market Size (2031) | USD 56.54 Billion |

| Growth Rate (2026 - 2031) | 23.85% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Mobile Video Advertising Market Analysis by Mordor Intelligence

The mobile video advertising market size in 2026 is estimated at USD 19.39 billion, growing from 2025 value of USD 15.66 billion with 2031 projections showing USD 56.54 billion, growing at 23.85% CAGR over 2026-2031. This trajectory mirrors the clear shift toward mobile screens for daily video consumption. Expansion is reinforced by AI-generated dynamic creatives, on-device machine learning for contextual targeting, and rapid 5G rollouts that cut load times and lift completion rates. Asia-Pacific leads with a 37.2% 2024 share while telco–media zero-rating deals spur adoption in the Middle East and Africa. In-stream placements remain the revenue anchor, yet rewarded video formats grow fastest as gaming apps swap intrusive spots for value-exchange views. Operating system diversification continues as HarmonyOS rises, creating a third ecosystem and fresh inventory for the mobile video advertising market.

Key Report Takeaways

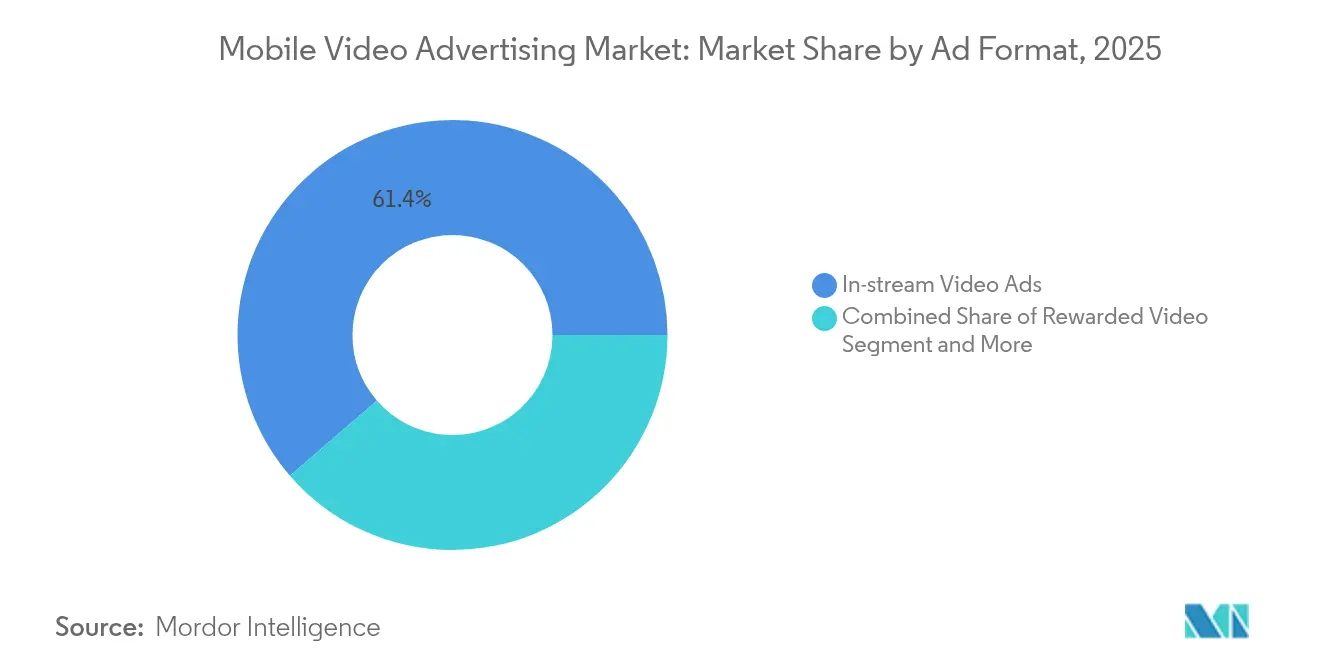

- By ad format, in-stream video held 61.35% of mobile video advertising market share in 2025; rewarded video is forecast to expand at a 27.85% CAGR through 2031.

- By operating system, Android retained 76.10% share of the mobile video advertising market in 2025; HarmonyOS is advancing at a 29.6% CAGR.

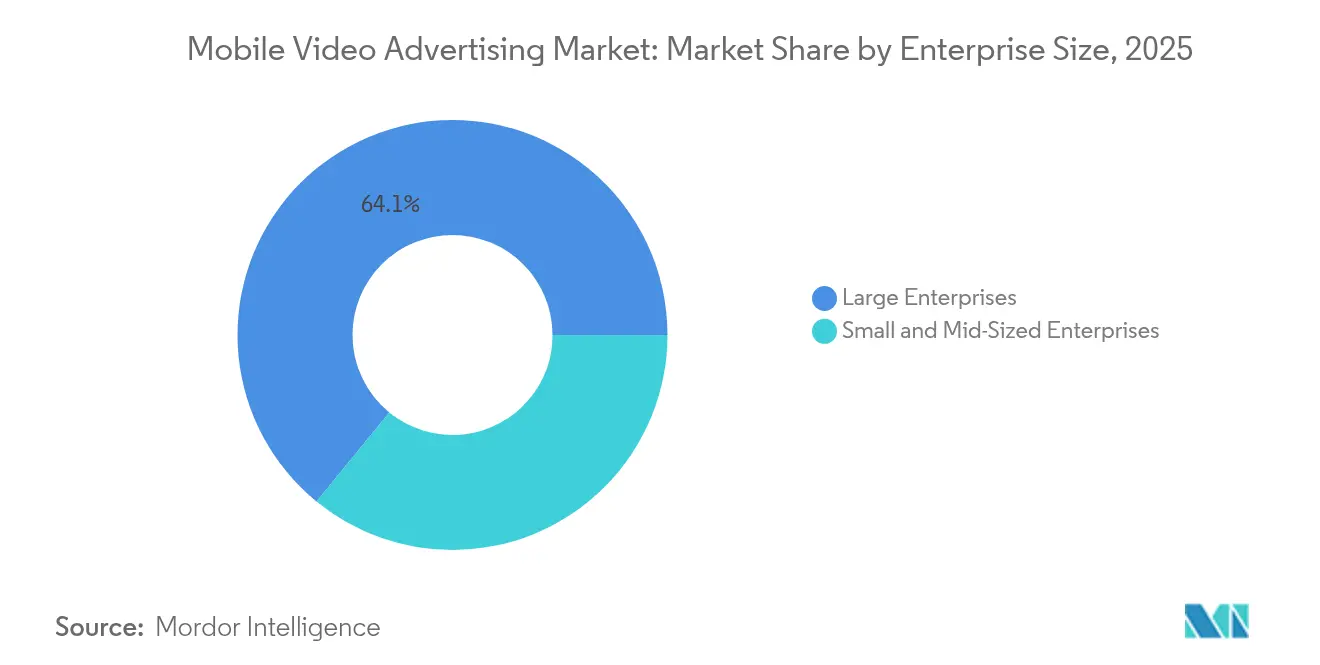

- By enterprise size, large enterprises captured 64.10% revenue share in 2025, while SMEs are set to grow at a 26.3% CAGR.

- By end-user vertical, retail and e-commerce commanded 23.25% share of the mobile video advertising market size in 2025; gaming is projected to rise at a 28.05% CAGR.

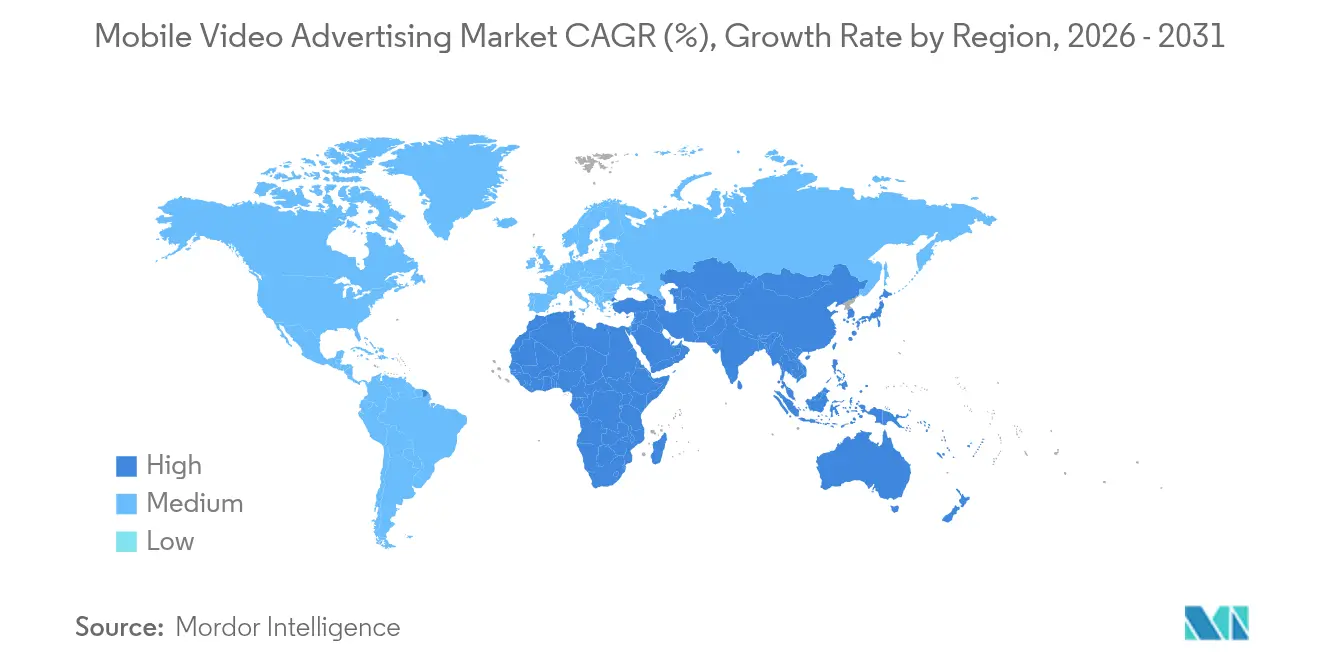

- Asia-Pacific led regional revenue with 36.85% in 2025; the Middle East and Africa mobile video advertising market is expected to post a 29.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mobile Video Advertising Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in short-form vertical video on 5G networks | +6.80% | Asia-Pacific; spillover to North America | Medium term (2-4 years) |

| Shoppable video ads inside social-commerce ecosystems | +5.40% | North America; Europe | Medium term (2-4 years) |

| Rewarded video adoption by mobile-gaming publishers | +4.20% | South America; Global | Short term (≤ 2 years) |

| On-device ML contextual targeting | +3.50% | North America; Europe | Medium term (2-4 years) |

| Telco–media zero-rating partnerships | +2.90% | Middle East; Africa | Long term (≥ 4 years) |

| AI-generated dynamic creatives | +2.10% | Europe; North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Short-Form Vertical Video Consumption on 5G Networks Across Asia-Pacific

Rapid 5G rollout across China, South Korea, and Japan cuts video load times by 73% and lets brands extend ad length from 15 to 30 seconds without higher drop-offs. Completion rates for vertical clips now sit 42% above horizontal units while short videos account for 44.5% of all digital viewing in Southeast Asia. Advertisers use the richer format to layer storytelling that feels native to social feeds. Higher view time opens space for calls to action that push trial and purchase. The outcome is more inventory, higher CPMs, and stronger brand recall that powers the mobile video advertising market.

Integration of Shoppable Video Ads Within Social-Commerce Ecosystems in North America

Shoppable clips fold product discovery and purchase into one tap, cutting the path to purchase touches from 5.7 to 2.3 by 2025 and lifting conversion by 37% . Platforms like TikTok report 70% user ease with shoppable units, giving retailers richer first-party data. Meta notes a 30% lift in return on ad spend for brands using its clickable formats in 2024. This commerce-content convergence gives advertisers measurable revenue rather than proxy engagement, anchoring budgets in the mobile video advertising market.

Adoption of Rewarded Video Ads by Mobile-Gaming Publishers in South America

Rewarded spots trade in-game currency for opt-in viewing and deliver 2.8 times higher eCPMs than interstitials. Brazilian and Argentine publishers see retention jump 35% because value exchange improves sentiment. Session length rises 42% as players seek more rewards. The format sidesteps payment friction in markets with low card penetration, which expands monetization and fuels the mobile video advertising market.

On-Device ML-Based Contextual Targeting for Privacy-Preserving Video Ads

Machine learning that stays on the handset trims data transfer by 64% and lifts relevance scores by 28% while respecting privacy mandates. Real-time signals guide dynamic creative optimization, driving engagement 31% above static campaigns. Advertisers gain compliant targeting in strict regions like the EU, supporting spend resilience in the mobile video advertising market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| IDFA deprecation reducing deterministic accuracy | -3.20% | North America; Europe | Short term (≤ 2 years) |

| Attention-metric scrutiny under EU DSA | -2.10% | Europe; potential global spillover | Medium term (2-4 years) |

| Rising ad-block adoption on Android | -1.40% | Global | Medium term (2-4 years) |

| Higher publisher viewability thresholds | -1.00% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

IDFA Deprecation Reducing Deterministic Targeting Accuracy in North America and Europe

Apple’s App Tracking Transparency lowers opt-in to 25% and cuts attribution accuracy 41%, trimming game revenue by up to USD 10 billion yearly. Advertisers shift to probabilistic models that raise uncertainty. Brands rebuild tactics with contextual cues and first-party data, yet the near-term drag slows wider mobile video advertising market spend.

Regulatory Scrutiny Over Attention-Metric Claims Under EU Digital Services Act

The DSA demands evidence for attention methods and bans manipulative design which triggers a 27% pullback in attention-guaranteed deals. Platforms must disclose methodology and ensure ad repositories, pushing new cost on publishers. Compliance work sparks innovation in standard metrics though near-term friction tempers growth in the mobile video advertising market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ad Format: Rewarded Video Redefines Value Exchange

In-stream video commanded 61.35% of mobile video advertising market share in 2025 as pre-roll units post 30% higher completion than mid-roll placements. This format remains prized due to seamless alignment with existing content and guaranteed viewability, which secures premium CPMs. The mobile video advertising market size for in-stream ads is projected to advance steadily through 2031 as publishers prioritize quality inventory.

Rewarded video is scaling fastest at a 27.85% CAGR. Opt-in nature means completion often exceeds 90% while user sentiment stays positive. Gaming titles and non-gaming apps now integrate reward loops for surveys or coupons, broadening appeal. Advertisers use deterministic signals such as level completion or app milestones to serve contextually apt offers that spur purchase. Performance lifts raise budgets and diversify revenue streams within the mobile video advertising market. Out-stream and interstitial formats hold niche roles, offering incremental reach in text-based feeds or transitional screens, yet they face greater user-experience scrutiny.

By Operating System: HarmonyOS Disrupts the Duopoly

Android retained 76.10% share in 2025, underpinning broad reach especially in emerging economies where device entry price is low. iOS, though smaller in users, continues to fetch premium bid rates given 1.8 times higher revenue per user. Privacy changes force creative contextual methods, yet advertiser demand persists due to high spend power.

HarmonyOS climbs at a 29.6% CAGR, marking the fastest growth path among platforms. Huawei’s Petal Ads now serves 53,000 apps and showcases tools at events like Think Tank 2025 in Japan . Rising adoption in Asia opens fresh audiences for the mobile video advertising market. Advertisers craft flexible creatives that suit varied user interfaces, and agencies build buying pipes that span three operating systems, reducing reliance on the Google-Apple duopoly.

By Enterprise Size: SMEs Embrace Video’s Accessibility

Large enterprises owned 64.10% spending in 2025. Their budgets fund high-production assets and multi-platform orchestration. Cross-channel flows lift brand recall 37% as teams test an average of 12.4 creatives per campaign. The scale advantage safeguards dominance in mobile video advertising market investment.

SMEs grow faster at 26.3% CAGR thanks to template tools and programmatic access with low minimum spend. Digital ads now beat traditional returns for 78% of small firms. Mobile video campaigns yield 2.3 times higher engagement than static images, pushing SMEs to increase allocation. Platforms answer with simplified dashboards that auto-optimize creative, expanding the mobile video advertising market breadth.

By End-User Vertical: Gaming Monetization Accelerates

Retail and e-commerce led 23.25% of 2025 revenue as shoppable formats trim purchase journeys and boost conversion. Retail media networks leverage first-party data to fine-tune mobile videos and retarget buyers. The mobile video advertising market size for retail remains strong due to near-real-time revenue feedback loops.

Gaming posts the quickest 28.05% CAGR. Rewarded units drive retention and revenue with 2.8 times higher eCPMs, making video the core monetization layer in free-to-play app. Publishers segment users by play style and serve context aware offers that sustain long term value. Media and entertainment, plus BFSI, also boost mobile adoption to simplify complex services or promote new content bundles, rounding out vertical diversity within the mobile video advertising market.

Geography Analysis

Asia-Pacific holds the top position with 36.85% revenue in 2025, backed by mobile-first habits and rapid 5G penetration that lifts completion rates. The region embraces short vertical videos on platforms such as TikTok and Kuaishou, which encourages larger brand budgets. HarmonyOS uptake creates incremental inventory through Petal Ads that attracts cross-border advertisers at events like Think Tank 2025. Mature markets concentrate on premium immersive formats while developing ones favor lightweight creative suited to data-savvy users, ensuring balanced growth in the mobile video advertising market.

North America ranks second and drives format innovation with shoppable and interactive units that compress funnels. Apple IDFA changes push marketers toward contextual signaling and server-side conversions, yet programmatic share reaches 75% of digital video buys in 2024. Continuous measurement innovation and AI personalization support stable spend across the mobile video advertising market despite privacy headwinds.

The Middle East and Africa mobile video advertising market exhibits the fastest 29.1% CAGR through 2031. Zero-rating partnerships between telcos and media cut data costs and lift view time 3.2 times. Youthful demographics and broader 4G-5G coverage add momentum though rural bandwidth gaps remain. Advertisers adopt adaptive streaming to maintain quality and capitalize on rising smartphone penetration, supporting long-term revenue lift.

Competitive Landscape

Google, Meta, and ByteDance dominate user attention and ad tech with ByteDance targeting USD 186 billion revenue in 2025. YouTube Shorts, Reels, and TikTok foster vertical scroll behavior that positions them at the core of the mobile video advertising market. Consolidation shapes the ecosystem as Mediaocean merges with Innovid to grant marketers unified control across channels.[1]Mediaocean, “Mediaocean Completes Acquisition of Innovid,” innovid.com

Specialists like Unity and ironSource focus on in-game inventory while Verve buys Receptiv to blend location data with high-impact video.[2]Global Banking and Finance Review, “Verve Acquires Receptiv,” globalbankingandfinance.com Huawei’s HarmonyOS builds a third pillar that diversifies supply and forces agencies to refine cross-platform creative. Growth in shoppable and rewarded formats spurs platform tool kits that automate product feeds, video creation, and bidding, enhancing advertiser outcomes in the mobile video advertising market.

Artificial intelligence underpins creative scale and targeting. Google AdMob introduces high-engagement settings, Meta rolls out ROAS optimization tied to ad impressions, and TikTok expands shoppable video capabilities. Brands that harness AI for iteration see engagement lift of 41% compared with static content, reinforcing the strategic value of data informed creative within the mobile video advertising market.

Mobile Video Advertising Industry Leaders

Google LLC

Meta Platforms Inc.

Amazon Ads

Snap Inc.

Unity Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Verve acquired Receptiv, expanding high-performing in-app video formats and publisher relationships

- April 2025: Huawei Petal Ads hosted Think Tank 2025 in Japan to showcase HarmonyOS advertising tools

- February 2025: Mediaocean completed its Innovid acquisition to build an independent ad tech platform

- January 2025: Huawei launched HarmonyOS Next with the Mate 70 smartphone, adding a third global mobile ecosystem

Global Mobile Video Advertising Market Report Scope

Mobile video advertising promotes products, services, or brands through a video format designed for viewing on mobile devices such as smartphones and tablets. Video ad networks act as intermediaries between app publishers and advertisers, helping to efficiently distribute video ads within mobile apps. Ad revenue generated from mobile apps through various forms of in-app advertising is one of the most popular monetization methods for app developers.

The mobile video advertising market is segmented by end-user (BFSI, IT and telecom, healthcare, media and entertainment, education, retail, other end-users), by geography (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| In-stream Video Ads |

| Out-stream Video Ads |

| Rewarded Video Ads |

| Interstitial Video Ads |

| Android |

| iOS |

| Others (HarmonyOS, KaiOS) |

| Large Enterprises |

| Small and Mid-Sized Enterprises |

| Retail and E-commerce |

| Media and Entertainment |

| Gaming |

| BFSI |

| Healthcare and Pharma |

| Automotive |

| Education |

| Others (Travel, Government) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Ad Format | In-stream Video Ads | |

| Out-stream Video Ads | ||

| Rewarded Video Ads | ||

| Interstitial Video Ads | ||

| By Operating System | Android | |

| iOS | ||

| Others (HarmonyOS, KaiOS) | ||

| By Enterprise Size | Large Enterprises | |

| Small and Mid-Sized Enterprises | ||

| By End-user Vertical | Retail and E-commerce | |

| Media and Entertainment | ||

| Gaming | ||

| BFSI | ||

| Healthcare and Pharma | ||

| Automotive | ||

| Education | ||

| Others (Travel, Government) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the mobile video advertising market?

The mobile video advertising market stands at USD 19.39 billion in 2026 and is forecast to reach USD 56.54 billion by 2031.

Which ad format is growing fastest?

Rewarded video ads are the fastest growing with a 27.85% CAGR projected for 2026-2031, supported by strong gaming adoption.

How does HarmonyOS affect advertisers?

HarmonyOS expands available inventory outside the Android-iOS duopoly, growing at a 29.6% CAGR and opening new audiences for campaigns.

Why are shoppable video ads important?

Shoppable formats lower the path to purchase from 5.7 to 2.3 touches and raise conversion by 37%, making them attractive for retail brands.

What regions will see the quickest growth?

The Middle East and Africa mobile video advertising market is forecast to grow at 29.1% CAGR through 2031 due to zero-rating partnerships and rising smartphone penetration.

How are privacy changes reshaping targeting?

IDFA deprecation and stricter EU rules push brands toward on-device machine learning and contextual signals that uphold relevance while protecting privacy.

Page last updated on: