Native Advertising Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

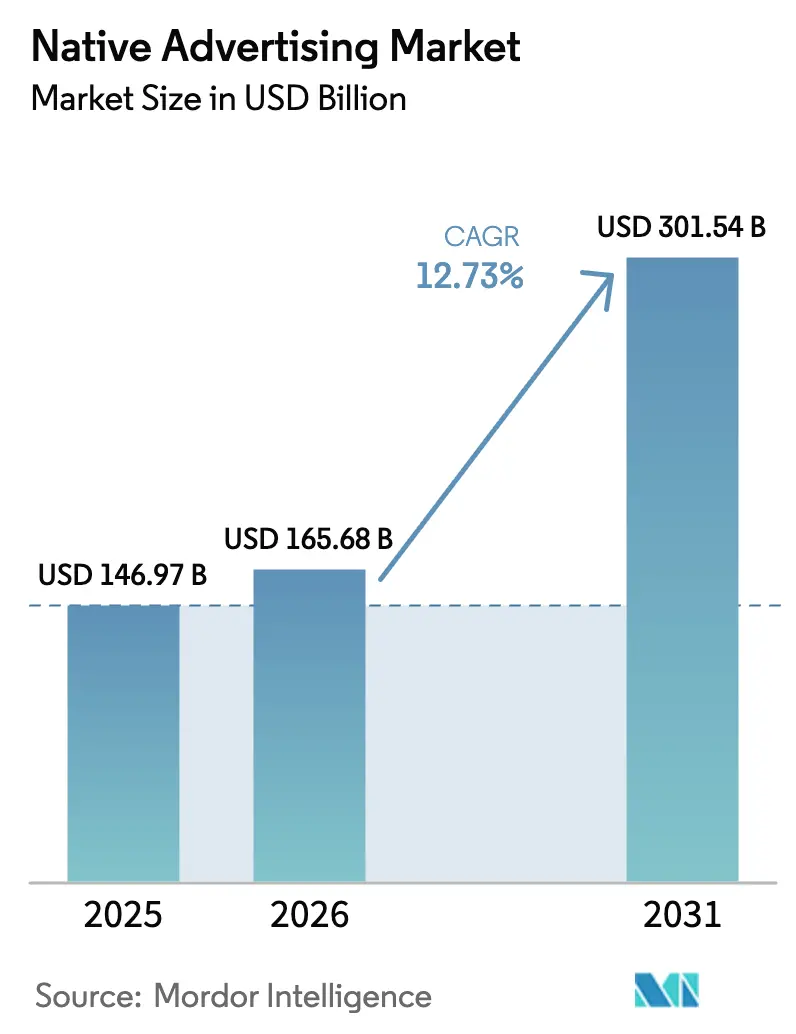

| Market Size (2026) | USD 165.68 Billion |

| Market Size (2031) | USD 301.54 Billion |

| Growth Rate (2026 - 2031) | 12.73% CAGR |

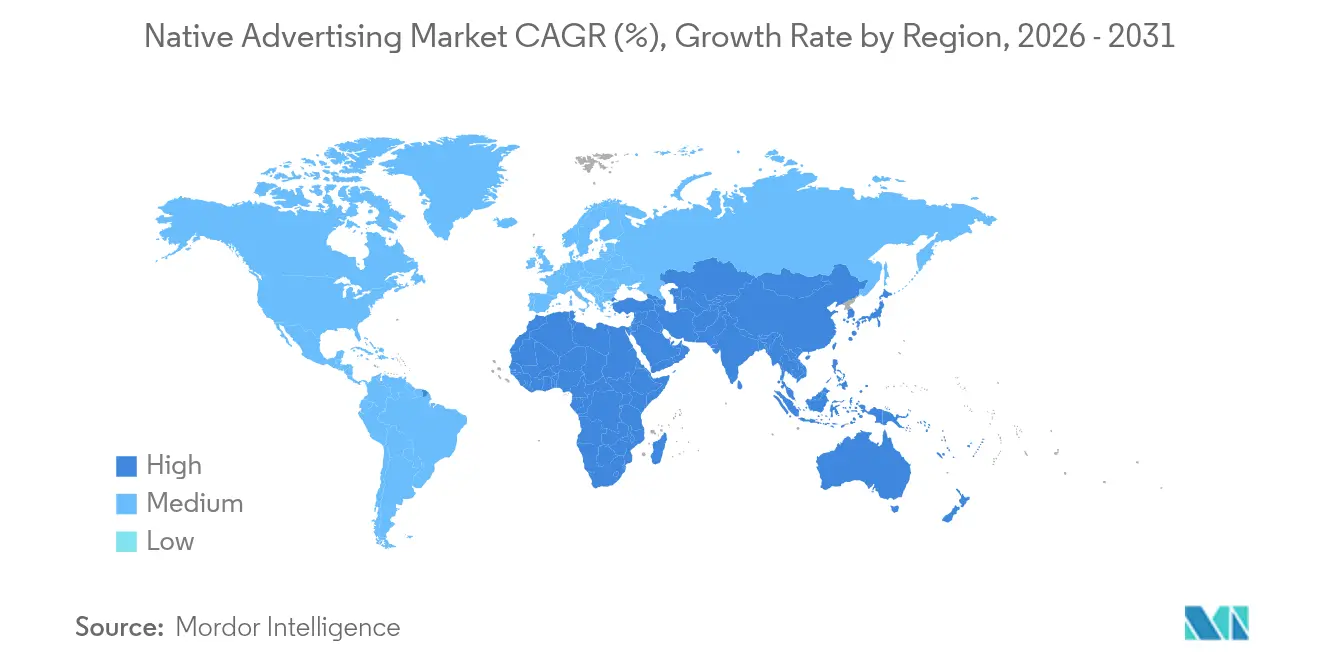

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Native Advertising Market Analysis by Mordor Intelligence

The native advertising market size is expected to grow from USD 146.97 billion in 2025 to USD 165.68 billion in 2026 and is forecast to reach USD 301.54 billion by 2031 at 12.73% CAGR over 2026-2031. Advertisers are migrating budget from standard banners to units that sit naturally within content feeds, search results, product grids, and streaming menus; this pivot is already evident in the United States, where native formats accounted for almost 60% of total display spend last year. Three structural shifts underpin the expansion. First, retailers have built full-funnel media networks that package first-party shopper data with sponsored listings and in-feed video, attracting net-new budgets. Second, the programmatic stack has matured to guarantee premium connected-TV (CTV) inventory at scale, allowing brand-safe, non-skippable native video. Third, Asia’s roll-out of 5G is unlocking rich-media experiences for short-form video platforms, pushing engagement far above traditional social feeds. Together these forces lift revenue while insulating buyers against the signal loss caused by third-party-cookie deprecation.

Key Report Takeaways

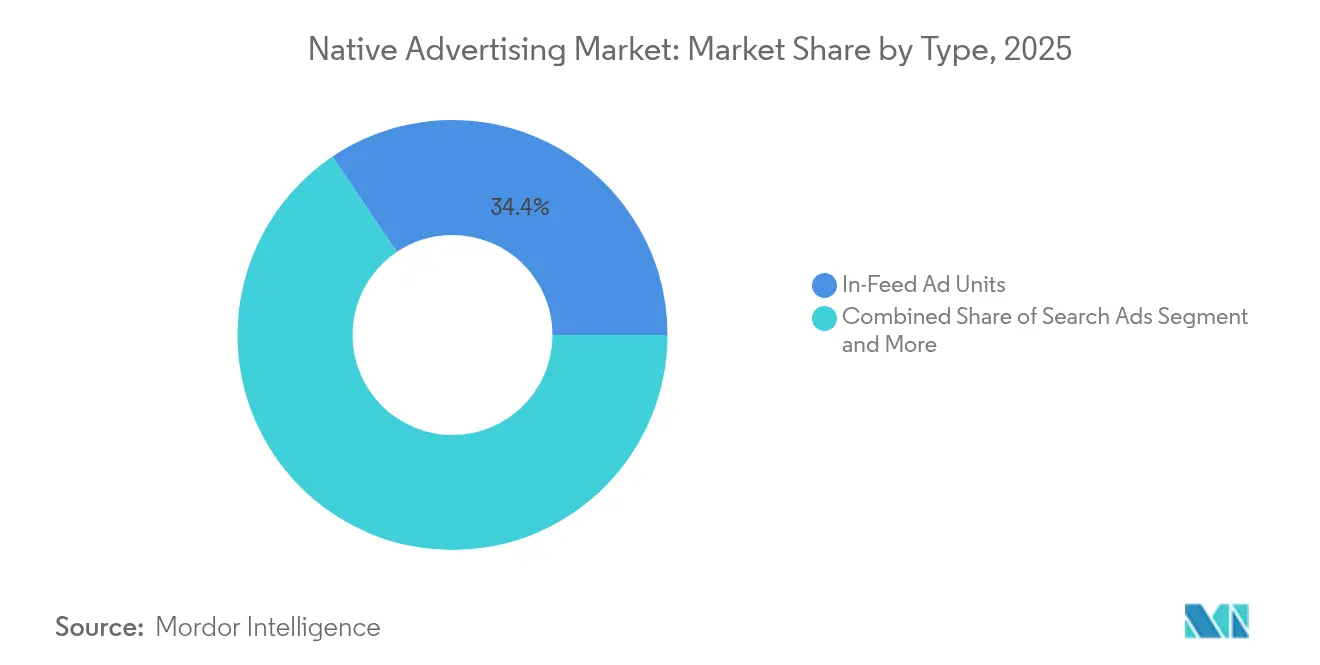

- By ad-format, In-Feed Ad Units held 34.42% of native advertising market share in 2025, while Recommendation Units are projected to expand at a 15.55% CAGR through 2031.

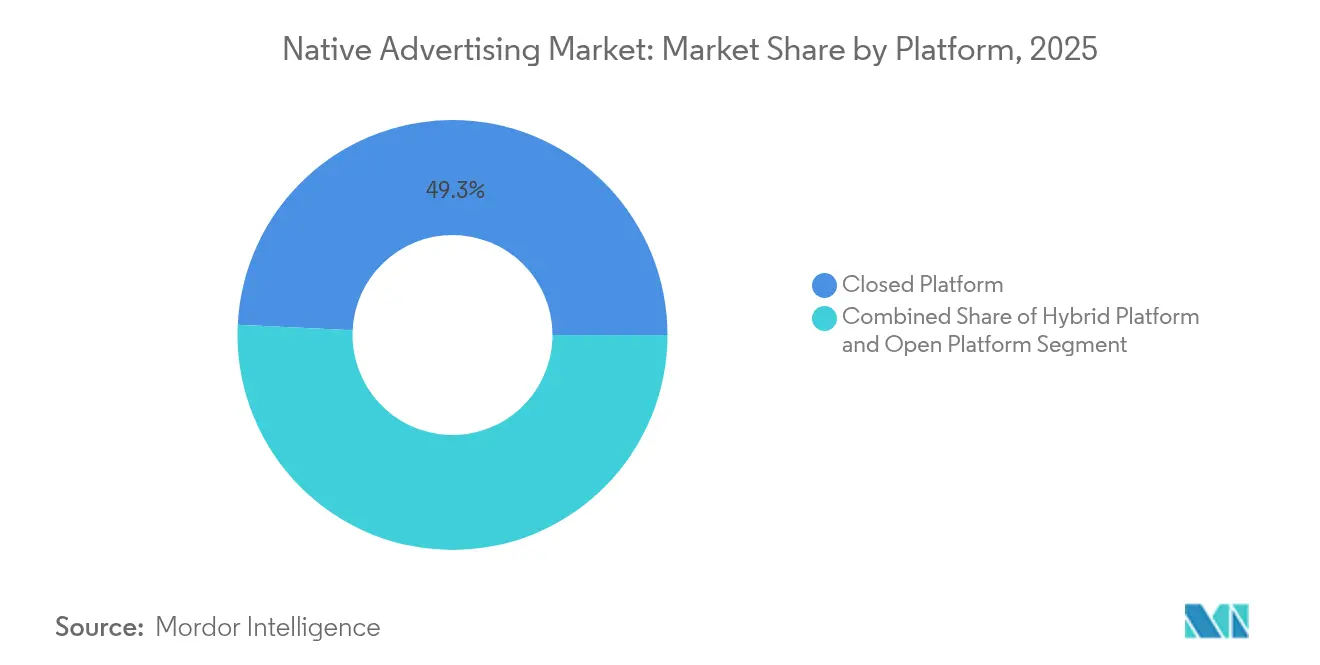

- By platform model, Closed Platforms commanded 49.25% of the native advertising market size in 2025; Hybrid Platforms show the fastest trajectory at an 17.72% CAGR to 2031.

- By region, North America captured 39.45% revenue in 2025; Asia-Pacific is forecast to post a 16.05% CAGR between 2026-2031.

- By company concentration, Outbrain and Teads together handled USD 1.7 billion in placed spend during 2025, reflecting recent consolidation that is reshaping buying route

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Native Advertising Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Monetisation push by retail-media networks | +3.20% | North America, spillover to Europe | Medium term (2-4 years) |

| De-cookie contextual native adoption | +2.80% | Europe, North America | Short term (≤ 2 years) |

| 5G-enabled rich-media formats | +2.50% | Asia-Pacific, global spillover | Medium term (2-4 years) |

| Programmatic guaranteed buying on CTV apps | +2.10% | North America, Europe | Short term (≤ 2 years) |

| Brand-safety preference for in-feed native | +1.80% | Global | Medium term (2-4 years) |

| AI-based creative generation tools | +1.60% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Monetisation push by retail-media networks in North America

Retailers are now full-service media owners. Aggregate retail-media revenue is set to surpass USD 176.9 billion in 2025, overtaking linear TV spend US chains such as 7-Eleven run proprietary networks that insert sponsored products and branded content across mobile apps, loyalty portals, and in-store screens . Using first-party basket data, these networks deliver an average 12X return on ad spend and 24% conversion for participating bran. Because budgets are largely incremental, retailers are growing the total addressable pool rather than cannibalising existing display lines. This dynamic adds more than three percentage points to the market growth profile, setting a new baseline for demand.

De-cookie strategies prompting contextual native adoption in Europe

Google’s staged retirement of third-party cookies, which started with 1% of Chrome users in early 2024, has accelerated context-based buying. European publishers now scan on-page semantics to serve in-feed units aligned to article themes rather than user IDs. Dentsu’s Contextual Intelligence suite spans 96% of United Kingdom domains, allowing brands to match content tone with campaign messaging while remaining compliant with GDPR and the Digital Markets Act. Advertisers complement these placements with triangulated measurement that blends multi-touch attribution, mix modelling, and hold-out testing. As proof of momentum, contextual impressions rose double digits across premium news environments last quarter, underscoring a pivot that is structural rather than temporary.

5G-enabled rich-media native formats surge across Asia

Ultra-low-latency networks let platforms embed high-definition video, dynamic 3-D product views, and interactive overlays without buffering. China’s 5G rollout alone is forecast to inject almost USD 260 billion into its digital economy by 2030. TikTok short-video ads already outperform legacy in-feed placements on push accuracy and interactivity. India mirrors this pattern on connected TVs, where the installed base expanded 32% year over year, opening fresh canvas for native video in premium streaming hubs. Across Asia-Pacific, these advances add roughly 2.5 percentage points to compound growth, positioning the region as the engine of volume expansion.

Programmatic guaranteed buying uptake on CTV apps

CTV publishers now transact the bulk of impressions through programmatic guaranteed deals that blend reserved inventory with data-driven precision. In 2024, 75% of all CTV buys in the United States cleared via programmatic pipes. Disney aims for 75% programmatic penetration by 2027, indicating a long-run shift toward API-based workflows. Simpli.fi’s guaranteed CTV marketplace offers exclusive slots from AMC, Samsung, and Sling, reducing fragmentation and assuring advertisers of delivery against audience targets. The arrangement supports non-skippable native video that renders within platform interfaces, marrying the lean-back viewing mode with performance metrics once limited to mobile.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Restrictions on third-party domain-spoofing detection | -1.20% | Global; higher impact in North America and Europe | Short term (≤ 2 years) |

| Ad-blocking extensions targeting native placements | -1.10% | North America, Europe | Short term (≤ 2 years) |

| High creative production cost for dynamic native video | -0.90% | Asia-Pacific, Latin America, Middle East and Africa | Medium term (2-4 years) |

| Platform-lock-in risk for DTC brands | -0.80% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Restrictions on third-party domain-spoofing detection

The Digital Markets Act and Digital Services Act restrict cross-domain data exchange, hampering independent verification tools that flag counterfeit URLs . Fraudsters exploit the gap by creating look-alike sites that siphon ad spend away from legitimate publishers. Tactics range from DNS spoofing to webpage camouflaging, often escaping conventional filters. Publishers are resorting to anomaly detection and SSL monitoring, but those methods are piecemeal and inflate operational overhead. As a result, buyers price in higher fraud risk, trimming growth by more than one percentage point until compliant detection standards mature.

Ad-blocking extensions now targeting native placements

Global ad-block use reached 42.7% of internet users in 2024, erasing an estimated USD 54 billion in publisher revenue . Advanced plug-ins employ AI to identify sponsored labels, thumbnail patterns, and brand logos inside content widge. In response, media owners embed server-side ad insertion for native video, but the tactic raises integration costs and complicates measurement The tug-of-war drags growth down by 1.1 percentage points, a drag likely to persist until creative approaches deliver value users are willing to whitelist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Recommendation units outpace traditional formats

Recommendation Units captured rising attention despite In-Feed Ad Units holding 34.42% revenue in 2025. Buyers favour them for mid-funnel discovery, where algorithmic widgets surface related articles or products alongside editorial lists. This non-interruptive approach lifted click-throughs more than 20% year over year across major publisher exchange. Search Ads and Promoted Listings still dominate lower-funnel conversions because they appear adjacent to high-intent queries on retail sites. In-Ad Custom Content stays relevant at the top of the funnel, supporting brand storytelling in lifestyle sections. Deep-learning optimisation, as deployed by MediaGo’s award-winning engine, predicts user propensity and tailors creative even within identical slot dimensions.

Advertisers allocate larger creative budgets to dynamic video versions that auto-render according to user context, yet high production cost keeps adoption uneven across emerging markets. Even so, global output of recommendation slots is projected to rise at a 15.55% CAGR through 2031, outpacing other formats. The native advertising market size for recommendation inventory is expected to reach USD 72.1 billion by the end of the decade, equal to nearly one quarter of total spend. This trajectory underscores a broader shift from interruptive to content-embedded discovery pathways.

By Platform: Hybrid models bridge ecosystem divide

Closed Platforms, led by social networks and retail media, commanded 49.25% of revenue in 2025 because their login environments generate reliable first-party identifiers. Yet advertisers increasingly seek flexibility, fuelling an 17.72% CAGR for Hybrid Platforms that merge closed precision with open-web reach. Taboola’s Realize illustrates the model by letting buyers extend first-party segments into partner feeds while retaining control over cost-per-outcome pricing. Programmatic infrastructure plays a critical role; native display already represents 95% of programmatic display outlays in the United States.

Hybrid providers also simplify creative trafficking across devices. They route assets into CTV apps, commerce grids, and news feeds from a single user interface, reducing fragmentation. Open Platforms continue to offer scale, but regulatory pressure on third-party cookies tempers their growth rate. Over the forecast window, the native advertising market share for hybrid deployment is on track to climb toward 27.15%, reflecting advertisers’ preference for controlled yet expansive campaigns.

Geography Analysis

North America led with 39.45% of spend in 2025 on the back of retailer data pipes, programmatic CTV, and deep brand budgets. Home-grown chains such as 7-Eleven integrated sponsored products into loyalty apps, while Microsoft Retail Media bundled automated creative and audience targeting that averaged a 12X return on ad spend. More than 75% of CTV impressions now clear programmatically, giving buyers uniform access to native video slots inside streaming menus. These conditions keep the region at the forefront, although growth moderates as the base widens.

Asia-Pacific stands out for speed. The region’s native advertising market is projected to advance at a 16.05% CAGR to 2031, propelled by 5G, short-form video, and consumer commerce integration. China’s ecosystem, led by TikTok and other super-apps, combines shoppable streams with context-matched banners that sit inside content feedse. India’s CTV households rose one-third year on year, opening premium inventory unencumbered by legacy cable contracts. Across Southeast Asia, telecom operators partner with publishers to bundle zero-rating offers that encourage video viewing, further boosting rich-media adoption.

Europe navigates a complex regulatory setting that both constrains and catalyses innovation. The Digital Markets Act tightens consent rules, prompting publishers to roll out contextual engines. Dentsu’s tool now covers almost the entire UK internet universe, helping offset the decline in behavioural identifiers. Retail media momentum is strong as supermarkets extend sponsored listings and recommendation tiles across web shops, driving a 22% jump in sponsored-product revenue last year . Collectively, these initiatives preserve Europe’s relevance even as privacy rules reshape campaign playbooks.

Competitive Landscape

Market structure sits in the mid-concentrated zone. The February 2025 union of Outbrain and Teads combined USD 1.7 billion in spend under one roof, serving 17,000 advertisers and 4,000 publishers. [1]SEC, “Outbrain Inc. – Form 10-K 2024,” sec.govThe deal boosts omnichannel reach that spans video, display, and in-feed widgets, giving the merged entity scale comparable with newer retail media entrants. Technology remains a key differentiator. MediaGo’s five deep-learning models earned Gold at the 2025 Native Advertising Awards by predicting user paths and updating bids in real time. Taboola widened its addressable pool by launching Realize, positioning itself against search and social budgets valued at USD 55 billion.

Retail media operators add competition from outside traditional ad-tech circles. Microsoft Retail Media offers an AI studio that auto-generates native creatives, compressing production cycles and lowering barriers for mid-sized brands.[2] Microsoft Advertising, “Microsoft Retail Media for Brands,” about.ads.microsoft.com Hardware ecosystems also flex scale: Roku and Comcast’s FreeWheel automate CTV buying, bringing native video to living-room screens.[3]Streaming Media, “The State of OTT and CTV Monetization 2025,” streamingmedia.com Against this backdrop, smaller point solutions focus on niche innovations such as AI-based fraud detection, hoping to be acquired or embedded into broader stacks.

Finally, market participants confront rising user expectations. Ad-block prevalence forces continuous iteration toward value-adding formats that blend information with commerce. Vendors that can supply measurement transparency, privacy safeguards, and creative agility are best placed to capture incremental budgets through 2030.

Native Advertising Industry Leaders

Sharethrough Inc.

Zelto Inc.

Taboola Inc.

Nativo Inc.

TripleLift Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Outbrain acquired Teads for USD 900 million, forming an omnichannel platform handling USD 1.7 billion in annual ad spend

- February 2025: Taboola launched Realize to push performance advertising beyond social and search

- January 2025: Microsoft released Retail Media Creative Studio, an AI tool that automates native creative across onsite, offsite, and in-store channels

- December 2024: Roku deepened its programmatic partnership with FreeWheel to expand CTV automation

Global Native Advertising Market Report Scope

The native advertising market refers to the digital advertising sector where ads are designed to blend seamlessly with the surrounding content, appearing in a way that makes them look like part of the platform or medium on which they appear. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

The native advertising market is segmented by type (In Feed Ad Units, Search Ads, Promoted Listings, Recommendation Units and In-Ad Custom Content), by platform (Closed Platform, Open Platform and Hybrid Platform), and by geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| In-Feed Ad Units |

| Search Ads |

| Promoted Listings |

| Recommendation Units |

| In-Ad Custom Content |

| Closed Platform |

| Open Platform |

| Hybrid Platform |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Type | In-Feed Ad Units | |

| Search Ads | ||

| Promoted Listings | ||

| Recommendation Units | ||

| In-Ad Custom Content | ||

| By Platform | Closed Platform | |

| Open Platform | ||

| Hybrid Platform | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the native advertising market?

The native advertising market size stands at USD 165.68 billion in 2026 and is projected to reach USD 301.54 billion by 2031.

Which region grows fastest over the forecast horizon?

Asia-Pacific shows the highest momentum, with a projected 16.05% CAGR thanks to 5G rollouts, short-video engagement, and rising CTV adoption.

Why are hybrid platforms gaining popularity?

Hybrid platforms combine closed-garden targeting accuracy with open-web reach, enabling advertisers to manage first-party data while extending scale.

How does retail media influence native advertising budgets?

Retailers leverage first-party shopper data to run sponsored listings and in-feed ads, generating incremental budgets and lifting overall market growth by over three percentage points.

What technological trend most affects future creative formats?

AI-powered creative generation and optimisation tools speed up production cycles and dynamically tailor native ads to context, enhancing performance metrics.

Page last updated on: