Digital Audio Workstation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

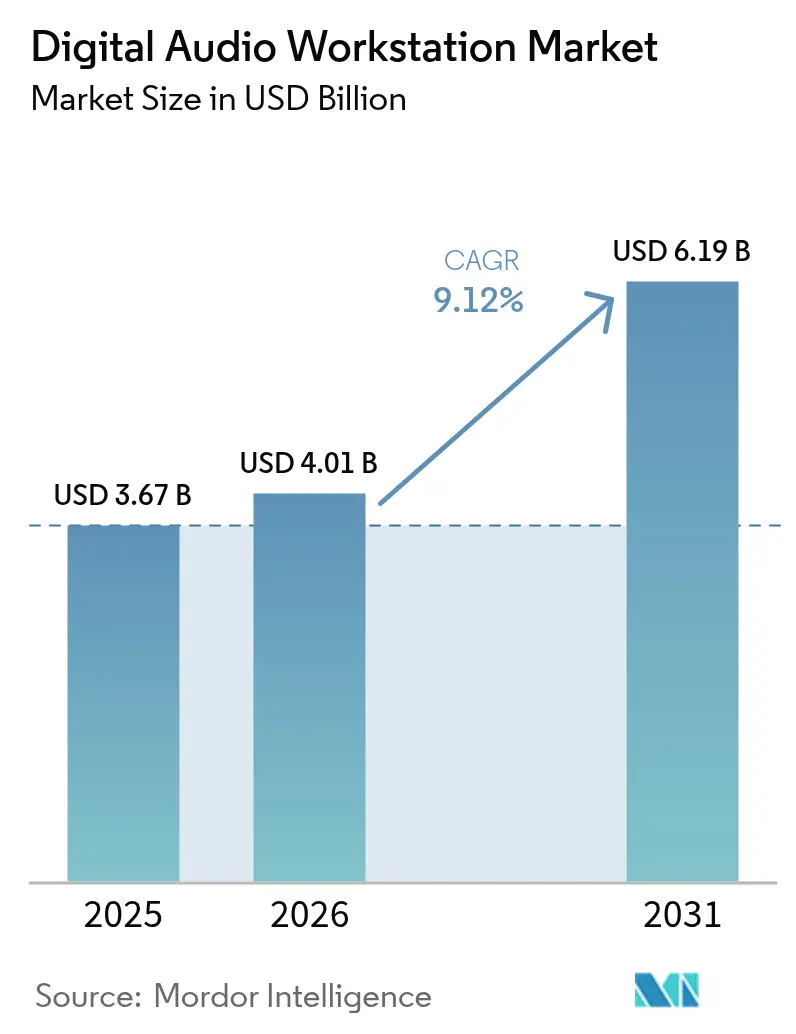

| Market Size (2026) | USD 4.01 Billion |

| Market Size (2031) | USD 6.19 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

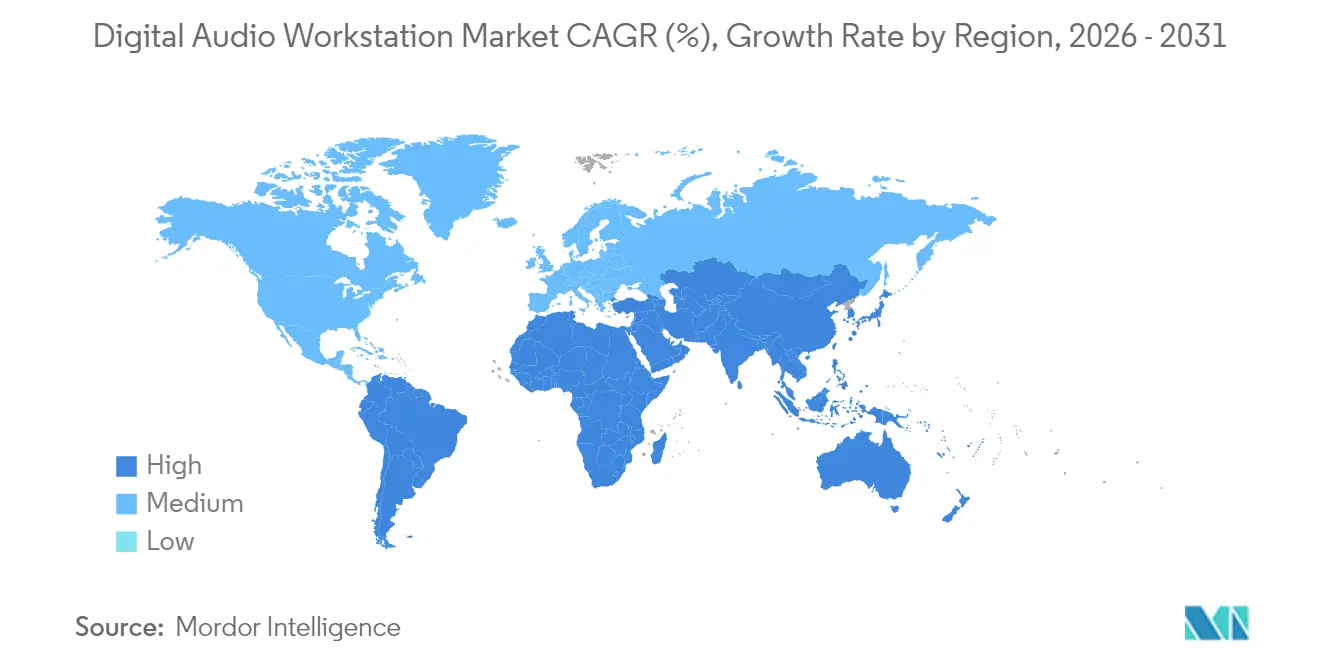

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Audio Workstation Market Analysis by Mordor Intelligence

Digital audio workstation market size in 2026 is estimated at USD 4.01 billion, growing from 2025 value of USD 3.67 billion with 2031 projections showing USD 6.19 billion, growing at 9.12% CAGR over 2026-2031. Cloud-native production, AI-assisted composition, and spatial-audio workflows are expanding the addressable user base while lifting spending among seasoned professionals. Subscription models have lowered up-front costs, bringing new hobbyists into paid ecosystems even as freemium rivals intensify price sensitivity. Remote collaboration-once a pandemic workaround-has become standard practice, accelerating migration to SaaS architectures and cross-platform toolchains. Meanwhile, spatial-audio demand from film, OTT, and gaming studios is forcing vendors to embed Dolby Atmos, binaural rendering, and object-based mixing natively. Competitive intensity is rising as suppliers bundle marketplaces, sample libraries, and AI utilities to deepen platform stickiness and defend against open-source alternatives.

Key Report Takeaways

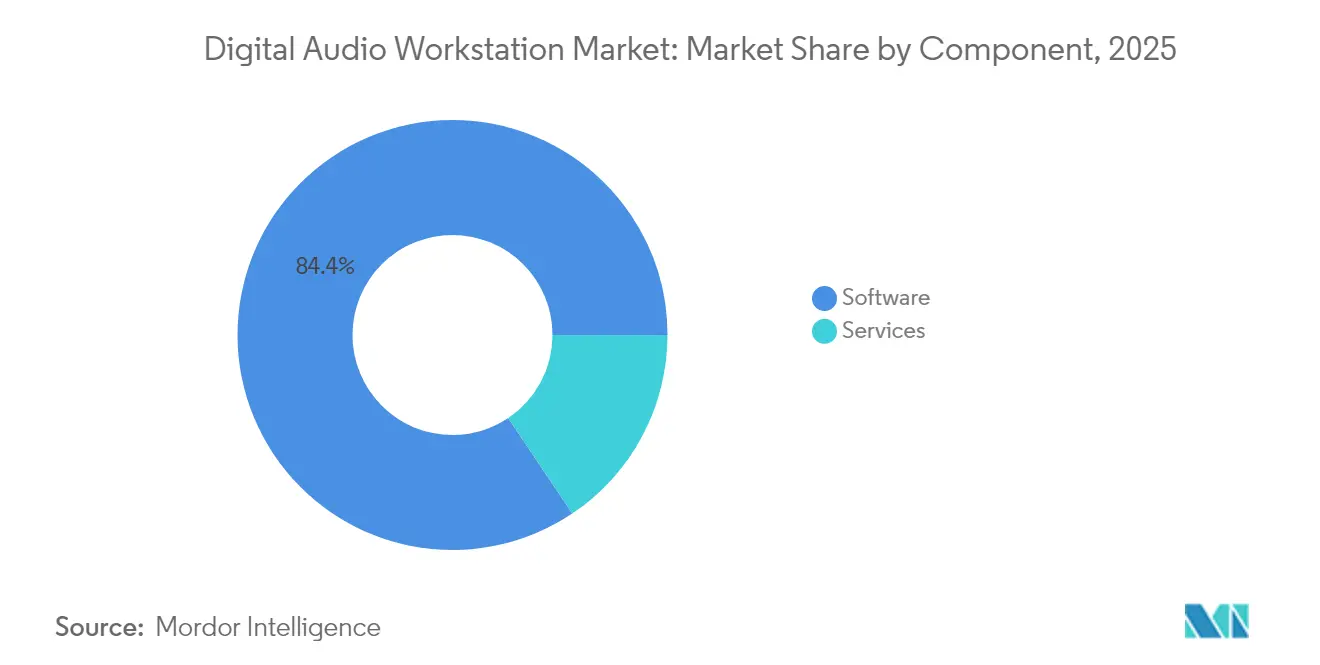

- By component, software controlled 84.40% of the digital audio workstation market share in 2025, while services are on track for 11.32% CAGR through 2031.

- By operating system, Windows led with 56.40% of the digital audio workstation market share in 2025; other OS platforms are set to expand at 12.18% CAGR to 2031.

- By deployment mode, on-premise solutions held 69.20% of the digital audio workstation market share in 2025, whereas cloud and SaaS offerings are forecast to grow 13.65% CAGR.

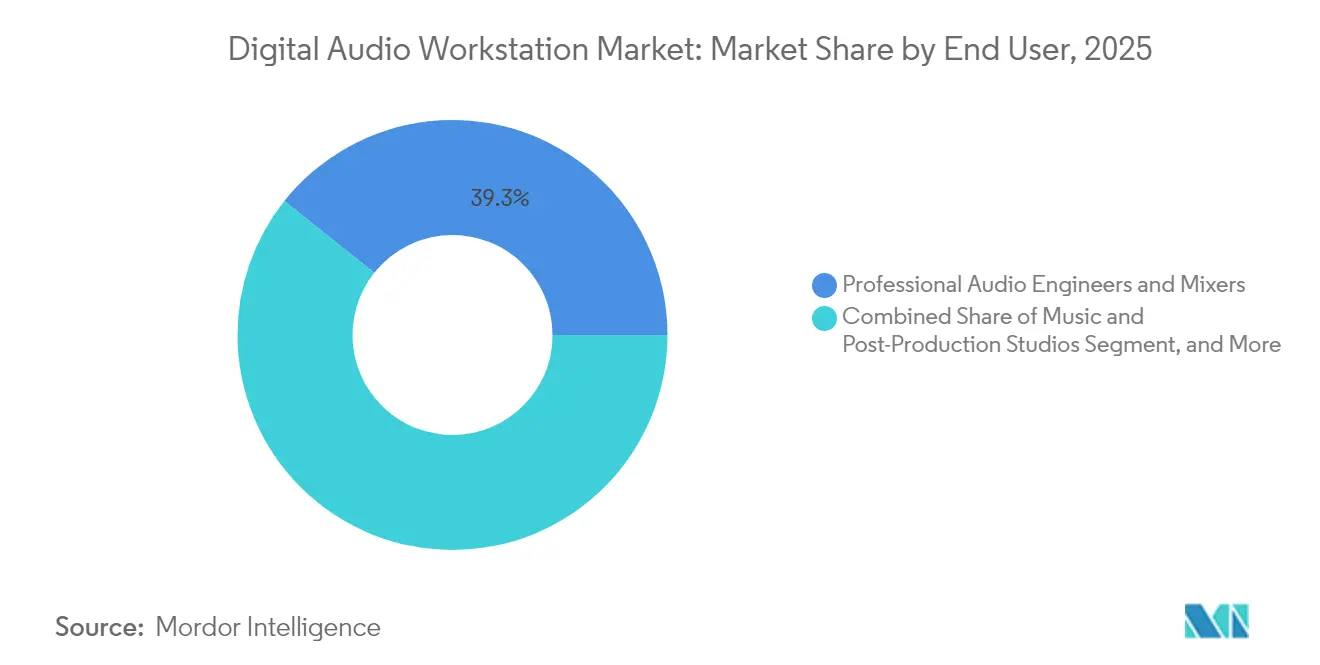

- By end user, professional audio engineers and mixers accounted for 39.30% of the digital audio workstation market share in 2025; podcast and content creators record the fastest CAGR at 13.08% to 2031.

- By application, music production commanded 59.10% of the digital audio workstation market share in 2025, and podcasting/live-streaming is advancing at 12.84% CAGR.

- By geography, North America captured 34.70% of the digital audio workstation market share in 2025; Asia-Pacific is the fastest-growing region at 11.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Digital Audio Workstation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing shift toward cloud-based DAWs among independent music producers | +2.1% | Global (early adoption in North America and EU) | Medium term (2-4 years) |

| Demand surge for immersive spatial-audio production driven by OTT and gaming studios | +1.8% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Adoption of AI-assisted composition tools by home-studio creators | +1.5% | Global (developed markets) | Short term (≤ 2 years) |

| Rising podcast monetization creating need for turn-key editing suites | +1.3% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| 5G roll-outs enabling low-latency remote collaboration workflows | +0.9% | Asia-Pacific, North America, select EU | Long term (≥ 4 years) |

| Proliferation of subscription-based pricing expanding paid user base | +0.7% | Global (mature markets) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Shift Toward Cloud-Based DAWs Among Independent Music Producers

Cloud adoption is climbing as creators seek affordable workstations that run on modest hardware and sync sessions across devices. Image-Line’s FL Cloud introduced tiered subscriptions that bundle 69 instruments and effects, illustrating how SaaS offerings replace one-time licenses while cutting storage and update overhead.[1]Image-Line, “FL Studio 2024 Adds FL Cloud Plug-Ins, AI, More,” mixonline.com Automatic versioning, real-time collaboration, and device-agnostic access resonate with mobile-first musicians. Reduced piracy risk and recurring revenue also encourage vendors to prioritize cloud roadmaps. For users, the ability to co-produce from different cities with minimal latency has turned cloud workflows from novelty to necessity, reinforcing a medium-term boost to the digital audio workstation market.

Demand Surge for Immersive Spatial-Audio Production Driven by OTT and Gaming Studios

Streaming platforms now mandate Dolby Atmos mixes for flagship releases, while flagship games rely on object-based audio for realism. Steinberg Nuendo’s native Dolby Atmos renderer and Netflix loudness presets demonstrate vendor responses. L-Acoustics’ L-ISA Studio extends object mixing to 16 outputs, broadening access for smaller facilities.[2]L-Acoustics, “L-ISA Studio | Spatial Audio Mixing Tool,” l-acoustics.com As immersive experiences become an expectation, DAWs that simplify channel-based authoring, head-tracking monitoring, and automated down-mixing gain competitive advantage, adding long-term momentum to the digital audio workstation market.

Adoption of AI-Assisted Composition Tools by Home-Studio Creators

Apple Logic Pro 11’s AI virtual bandmates generate rhythm tracks, bass lines, and keyboard parts on demand soundonsound.com. Similar tools inside FL Studio supply chord progressions and automated mastering. These assistants reduce skill barriers, letting hobbyists craft polished demos without session musicians. Stem-separation engines speed remixing, while intelligent arrangement features facilitate rapid experimentation. As AI moves from novelty to workflow staple, entry-level creators join the paid tier, expanding the digital audio workstation market and pressuring vendors to refine machine-learning pipelines.

Rising Podcast Monetization Creating Need for Turn-Key Editing Suites

Podcast ad revenue growth has elevated production quality expectations, prompting editors to adopt DAWs that automate noise reduction, loudness normalization, and transcript alignment. Adobe added interactive fade handles and AI audio-category tagging to streamline episode assembly.[3]Adobe, “MEDIA ALERT: Adobe Premiere Pro Innovations Make Audio Editing Faster, Easier and More Intuitive,” adobe.com Soundtrap’s user surge during the pandemic showed how simplified interfaces entice non-engineers into multi-track editing.[4]Research Studies in Music Education, “Soundtrap usage during COVID-19,” ncbi.nlm.nih.gov As podcasters diversify into video, integrated audio-video workflows become essential, expanding medium-term growth for the digital audio workstation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of freemium and open-source DAWs eroding paid licenses | -1.4% | Global (higher in emerging markets) | Medium term (2-4 years) |

| High GPU/CPU requirements limiting mobile and emerging-market adoption | -1.1% | Asia-Pacific emerging, Latin America, MEA | Long term (≥ 4 years) |

| Complex IP and sample-clearance regulations increasing compliance costs | -0.8% | North America, Europe, developed Asia-Pacific | Medium term (2-4 years) |

| Hardware supply-chain volatility causing audio-interface shortages | -0.6% | Global (manufacturing hubs) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prevalence of Freemium and Open-Source DAWs Eroding Paid Licenses

Reaper’s low-cost plan and Audacity’s no-cost feature set force commercial publishers to prove added value beyond basic tracking and editing. Browser-based tools further lower switching barriers, particularly in price-sensitive regions. Vendors counter with subscription tiers that amortize costs yet still face resistance from users familiar with perpetual licenses. This competitive tug reduces near-term monetization potential for the digital audio workstation market.

High GPU/CPU Requirements Limiting Mobile and Emerging-Market Adoption

AI mastering, real-time convolution, and high-track counts strain entry-level devices. Apple Silicon’s M-series chips double plug-in headroom over legacy Intel builds, but those processors ship mainly in premium hardware. Budget-conscious creators in Asia-Pacific and Latin America often defer upgrades, slowing penetration. Thermal, battery, and storage constraints on smartphones add complexity for mobile DAW design, tempering long-term growth in the digital audio workstation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Innovation

Software accounted for 84.40% of 2025 revenue, underscoring its centrality to end-to-end workflows and ecosystem control. Services, though smaller, are expanding 11.32% CAGR as creators pay for cloud storage, AI mastering, and collaboration hubs. Software captured 84.40% of the digital audio workstation market share in 2025, while value-added services such as FL Cloud’s tiered plug-in bundles deepen vendor lock-in. As creators migrate sessions among devices, integrated cloud libraries and automated backups transform one-time purchasers into recurring subscribers. The resulting annuity revenue encourages rapid feature rollouts that keep the digital audio workstation market growing.

Service uptake also reflects skill-set gaps among hobbyists who outsource mastering or stem separation to online engines. Apple's dual-pricing-USD 199.99 perpetual on Mac or USD 4.99 monthly on iPad-illustrates how vendors flex price to match device use cases. By 2031, higher-margin services will cushion software commoditization, reinforcing a mixed-model approach across the digital audio workstation market.

By Operating System: Windows Leadership Faces Platform Diversification

Windows retained a 56.40% foothold thanks to broad audio-interface driver support and entrenched studio workflows. Yet mobile-first creators and Arm-based laptops are chipping away, pushing other OS platforms to a 12.18% CAGR. Windows machines controlled 56.40% of the digital audio workstation market size in 2025, but native Arm builds like Steinberg SpectraLayers 12 hint at a multi-architecture future. Smartphones and tablets expand content creation moments, requiring touch-optimized UIs and cloud sync.

Cross-platform parity now shapes buying decisions; users expect the same session to open on desktop and handheld devices without compromise. Vendors that deliver seamless migrations will capture incremental spend, spreading adoption across device ecosystems and lifting the digital audio workstation market.

By Deployment Mode: Cloud Transition Accelerates Despite On-Premise Dominance

On-premise deployments still generated 69.20% of 2025 revenue, favored by studios demanding deterministic latency and absolute data ownership. Nevertheless, cloud models are compounding at 13.65% CAGR as 5G coverage and zero-install browsers redefine collaboration. BandLab’s browser-based DAW showcases frictionless onboarding, while Avid’s price re-alignment reflects infrastructure cost recovery. Software captured 69.20% of the digital audio workstation market size in on-premise environments, yet every major vendor now offers session syncing or full SaaS tiers, signaling inevitable cloud ascendancy.

For independents, cloud saves eliminate catastrophic data loss and enable ad-hoc co-production. For enterprises, hybrid stacks combine local DSP acceleration with remote asset management. As internet reliability improves, more workloads will shift off the desktop, reshaping revenue mix in the digital audio workstation market.

By End User: Professional Segments Lead While Creator Economy Expands

Professional engineers and mixers contributed 39.30% of 2025 spend, valuing high-track counts, surround routings, and certification programs. Their loyalty anchors predictable yearly upgrades and plugin bundles. Conversely, podcast and content creators post a 13.08% CAGR, pulled by ad-supported business models and the need for turnkey editing. As monetization pathways multiply, hobbyists migrate from freemium apps to mid-tier subscriptions, enlarging the digital audio workstation market.

Educational institutions also uptick, embedding production curricula to meet rising creative-tech career interest. Vendors respond with site licenses and simplified modes that hide advanced routing until learners need it. Such stratification keeps entry affordable while creating up-sell paths as skills mature, sustaining momentum across the digital audio workstation market.

By Application: Music Production Dominance Faces Diversification

Music production and mastering held 59.10% revenue in 2025, rooted in album workflows and virtual instrument demand. Still, podcasting and live-streaming are scaling fastest at 12.84% CAGR as audiences seek on-demand talk and real-time creator interactions. Podcasting is projected to claim a 13.05% slice of the digital audio workstation market size by 2031. Film and OTT post-production, buoyed by spatial-audio mandates, require tight integration with video timelines and loudness meters, presenting upsell prospects.

Game developers crave adaptive music stems and low-latency middleware bridges, spurring specialized toolkits. Meanwhile, live streamers prioritize CPU efficiency and quick presets that publish directly to social platforms. This widening spectrum ensures no single use case dominates future product roadmaps, keeping the digital audio workstation market diversified.

Geography Analysis

North America commanded 34.70% of 2025 revenue, supported by Hollywood, Nashville, and a dense network of game and OTT studios. Stable broadband, early 5G rollouts, and high per-capita spending on creative software underpin premium adoption. However, market saturation and pushback against rising subscription fees temper incremental growth.

Asia-Pacific is the growth engine with 11.32% CAGR, led by China’s USD 3 billion digital-music sector and mobile-first creator culture. Smartphone penetration and short-form-video ecosystems push cross-device workflow demand, enlarging the digital audio workstation market. Government-backed 5G coverage and youth demographics accelerate cloud adoption, though hardware affordability remains a friction point in emerging economies.

Europe occupies a balanced profile-mature yet innovative. Strong IP enforcement supports premium pricing, while public arts funding sustains niche DAWs tailored to classical and broadcast markets. Latin America and MEA log lower absolute spend but exhibit high creator enthusiasm. Freemium and mobile-only apps dominate entry, positioning vendors with localized payment models to capture future upgrades. Collectively, geographic diversity insulates the digital audio workstation market from single-region downturns and encourages differentiated go-to-market tactics.

Competitive Landscape

The field is moderately concentrated: Apple, Avid, Steinberg, and Adobe anchor professional workflows, while Image-Line, BandLab, and Ableton court indie creators. Continuous AI infusion, spatial-audio compliance, and real-time collaboration differentiate offerings. Apple’s vertical integration across macOS, iPadOS, and silicon chips deepens lock-in, evidenced by Logic Pro’s device-specific pricing. Avid’s Splice tie-up injects a 100-million-sample library directly into Pro Tools, tightening its grip on post facilities.

Emergent challengers focus on niche pain points: Udio’s visual song editor targets AI-assisted arrangement, while Soundtrap leverages classroom workflows. Vendors also hedge against supply-chain risk; software-only innovations mitigate hardware interface shortages caused by chip constraints. As AI commoditizes core features, community ecosystems, content marketplaces, and educational modules will define competitive edges in the digital audio workstation market.

Digital Audio Workstation Industry Leaders

Apple Inc.

Adobe Inc.

Avid Technology Inc.

Steinberg Media Technologies GmbH

Native Instruments GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Steinberg released SpectraLayers 12 with new unmixing modules and native Windows Arm support,

- June 2025: Udio launched “Sessions,” an AI visual editing workstation for music production amid ongoing copyright litigation.

- June 2025: Avid integrated Splice’s sample library into Pro Tools, broadening creative resources within the DAW.

- June 2025: Avid released Pro Tools 2025.6 with AI speech-to-text analysis and expanded MIDI tools.

- May 2025: Apple introduced Logic Pro 11 featuring AI virtual bandmates and stem separation.

Global Digital Audio Workstation Market Report Scope

A digital audio workstation is an electronic network drafted fundamentally to facilitate recording, editing, and playing back digital audio files. Due to technological advancements, these processes have become smoother than ever, and the devices provide various functionalities that are complex and are controlled by a single computer unit. The digital audio workstations are used to edit, manipulate, and record the audio.

The digital audio workstation market is segmented by operating system (Mac, Windows), by end-user (professional/audio engineers and mixers, electronic musicians, music studios), and by geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa).

The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Software |

| Services |

| macOS |

| Windows |

| Other Operating System |

| On-Premise/Perpetual License |

| Cloud/SaaS |

| Professional Audio Engineers and Mixers |

| Music and Post-Production Studios |

| Electronic and Independent Musicians |

| Education and Music Schools |

| Podcast and Content Creators |

| Music Production and Mastering |

| Film/TV/OTT Post-Production |

| Game-Audio and Immersive Media |

| Podcasting and Live-Streaming |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| By Component | Software | ||

| Services | |||

| By Operating System | macOS | ||

| Windows | |||

| Other Operating System | |||

| By Deployment Mode | On-Premise/Perpetual License | ||

| Cloud/SaaS | |||

| By End User | Professional Audio Engineers and Mixers | ||

| Music and Post-Production Studios | |||

| Electronic and Independent Musicians | |||

| Education and Music Schools | |||

| Podcast and Content Creators | |||

| By Application | Music Production and Mastering | ||

| Film/TV/OTT Post-Production | |||

| Game-Audio and Immersive Media | |||

| Podcasting and Live-Streaming | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Israel | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

Key Questions Answered in the Report

What is the current value of the digital audio workstation market?

The market generated USD 4.01 billion in revenue in 2026 and is projected to reach USD 6.19 billion by 2031.

Which segment holds the largest digital audio workstation market share?

Software components led with an 84.40% share in 2025, reflecting their central role in production workflows.

Why is Asia-Pacific the fastest-growing region in the digital audio workstation market?

Smartphone penetration, a USD 3 billion Chinese digital-music sector, and rapid 5G expansion drive an 11.32% CAGR in Asia-Pacific.

How is AI influencing digital audio workstation adoption?

AI virtual bandmates, stem-separation tools, and auto-mix engines lower skill barriers and speed workflows, attracting new creators into paid tiers.

What challenges could slow digital audio workstation market growth?

Freemium competition, high CPU/GPU requirements for advanced features, and hardware supply-chain volatility may temper revenue expansion.

Which deployment mode is expanding the quickest?

Cloud and SaaS deployments are growing at 13.65% CAGR as creators prioritize remote collaboration and subscription affordability.

Page last updated on: