Acute Wound Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

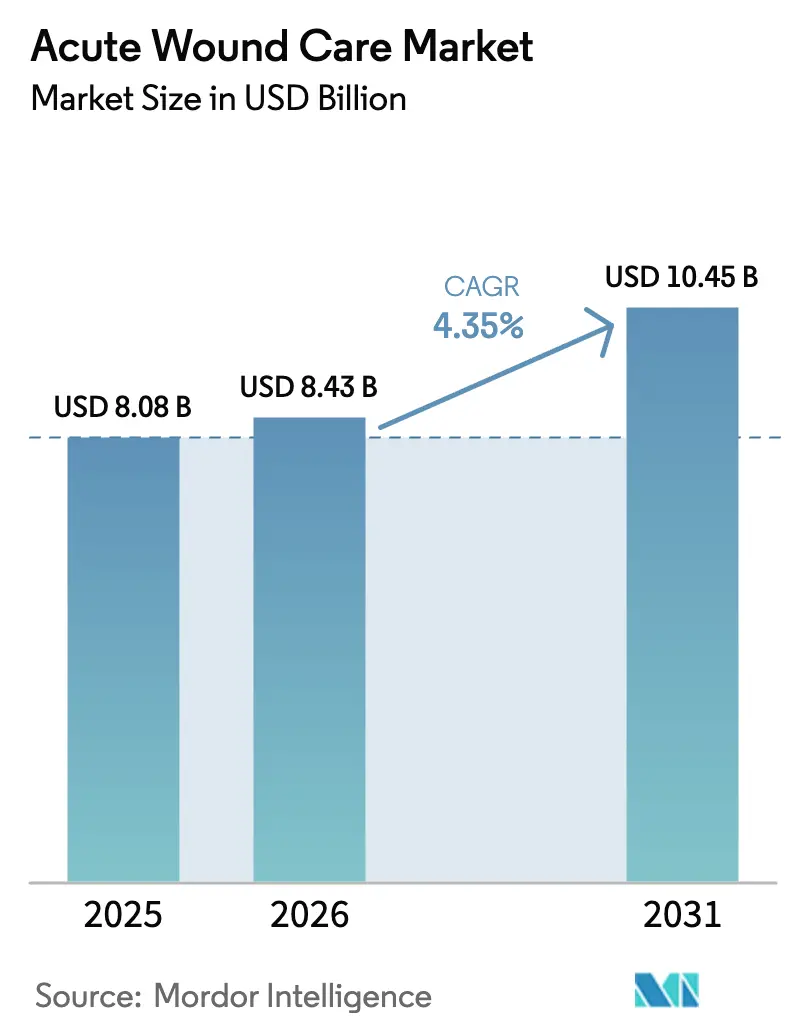

| Market Size (2026) | USD 8.43 Billion |

| Market Size (2031) | USD 10.45 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

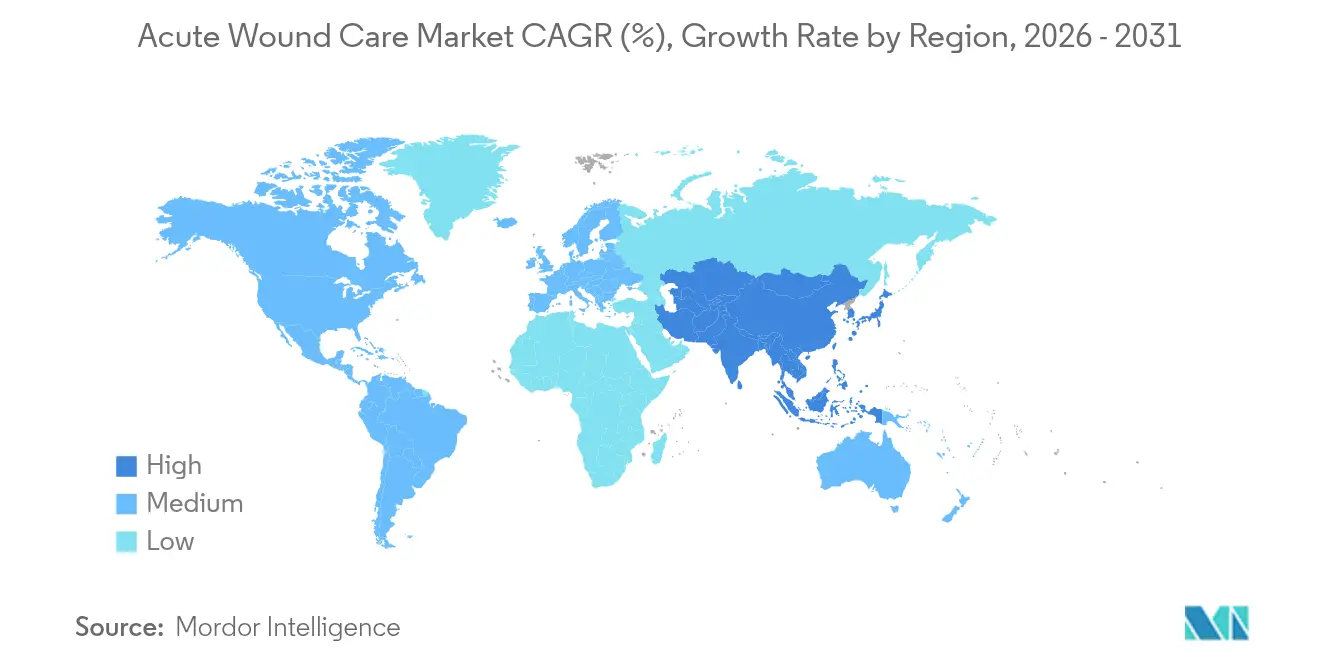

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

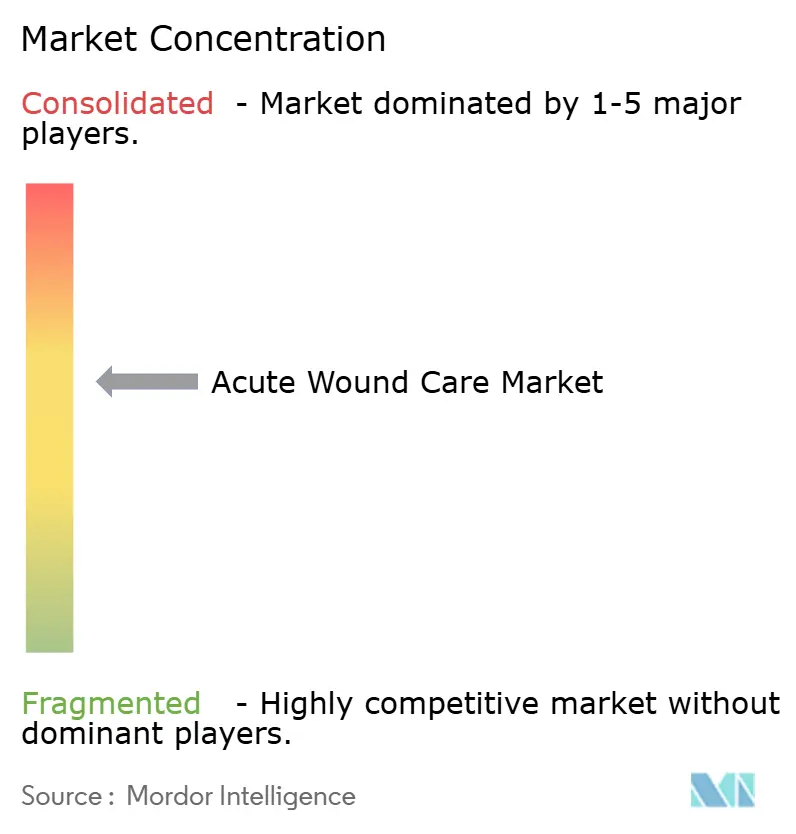

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acute Wound Care Market Analysis by Mordor Intelligence

Acute Wound Care Market size in 2026 is estimated at USD 8.43 billion, growing from 2025 value of USD 8.08 billion with 2031 projections showing USD 10.45 billion, growing at 4.35% CAGR over 2026-2031. The upswing reflects rising surgical volumes, robust uptake of closed-incision negative pressure wound therapy (NPWT), and the steady migration of procedures to ambulatory settings that favor fast, uncomplicated recovery. Aging populations, higher obesity rates, and expanding trauma caseloads reinforce the need for products that control infection, seal incisions, and accelerate tissue repair. Companies are responding with hybrid dressings that merge antimicrobial protection and suction-based exudate removal, while reimbursement changes now reward caregiver education and home-based follow-up, broadening demand. Concurrently, regulators in the United States and Europe are tightening evidence standards, steering manufacturers toward data-driven product claims and rigorous supply-chain oversight.

Key Report Takeaways

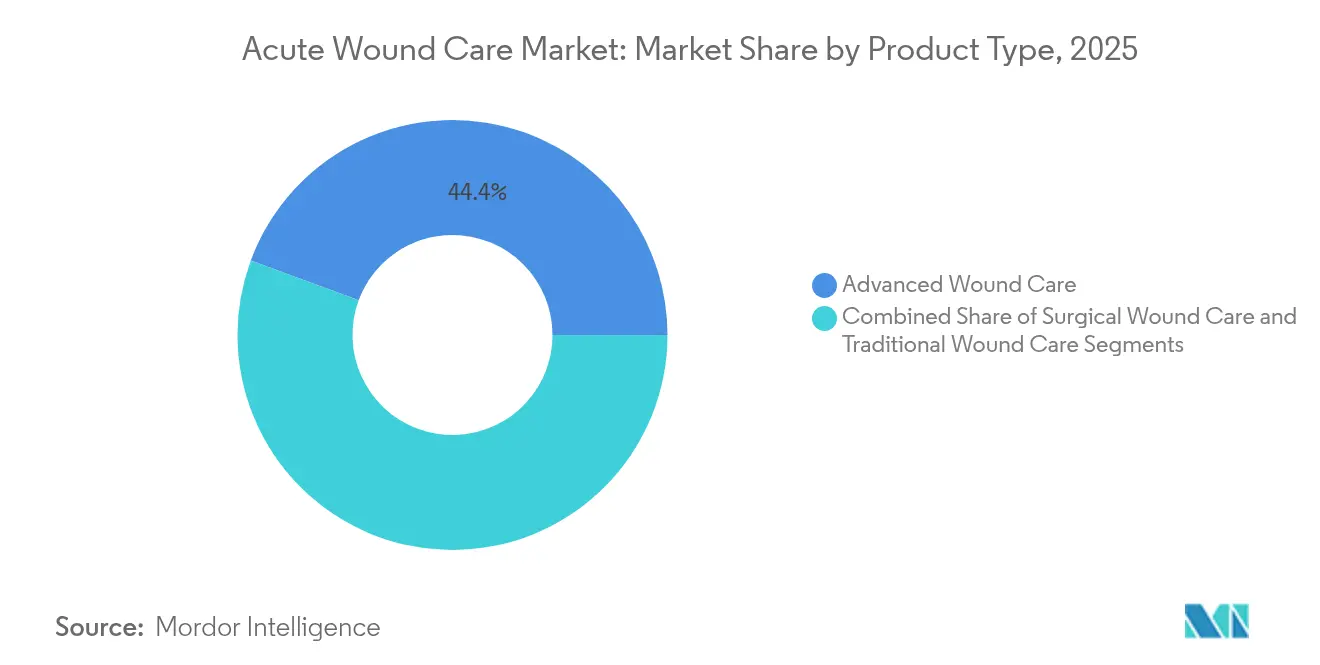

- By product type, advanced wound care captured 44.37% of acute wound care market share in 2025; surgical wound care is set to expand at a 5.62% CAGR through 2031.

- By wound type, surgical and traumatic wounds held 68.72% of the acute wound care market size in 2025, while burns treatment is forecast to accelerate at a 5.34% CAGR to 2031.

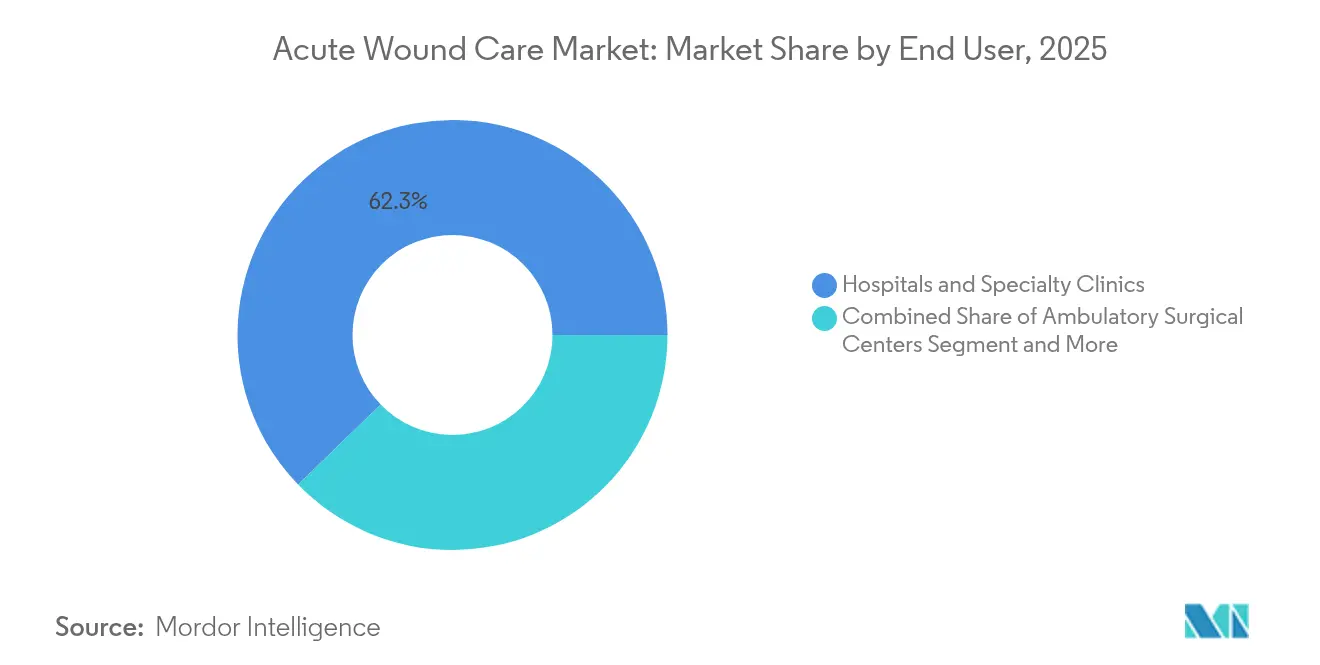

- By end user, hospitals and specialty clinics commanded 62.25% share of the acute wound care market in 2025, whereas home-care settings are advancing at a 5.76% CAGR through 2031.

- By geography, North America led with 37.98% revenue share in 2025; Asia-Pacific is projected to register the fastest 6.04% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Acute Wound Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Volume of Surgical Procedures | +1.2% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Rapid Rise in Road-Traffic and Occupational Trauma Cases | +0.8% | APAC core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Accelerated Adoption of Closed-Incision NPWT and Hybrid Dressings | +1.0% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Growing Geriatric Population with Impaired Healing | +0.9% | Global, with highest impact in developed markets | Long term (≥ 4 years) |

| Outpatient Shift to Ambulatory Surgery Centers Boosting Topical Haemostats | +0.7% | North America, expanding to Europe | Short term (≤ 2 years) |

| Military and Disaster-Relief Stock-Piling of Advanced Kits | +0.5% | Global, with focus on NATO countries and disaster-prone regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Volume of Surgical Procedures

Global surgical workloads continue to climb, and the median patient age is approaching 61 years, a demographic that heals more slowly and risks higher complication rates.[1]Smith+Nephew’s RENASYS EDGE Negative Pressure Wound Therapy System won the Red Dot Award for Design Concept 2024, highlighting its portability and user-centric interface. Rising body-mass indices add further strain on postoperative recovery, prompting hospitals to embed advanced dressings and NPWT into standard protocols. Medicare’s 2025 payment rule introduces billing codes that reimburse caregiver wound-care training, formalizing a broader circle of stakeholders and prolonging therapy beyond the inpatient stay.

Accelerated Adoption of Closed-Incision NPWT and Hybrid Dressings

Randomized studies in elderly flap reconstruction show that closed-incision NPWT halves drainage volume and cuts infection risk versus conventional dressings.[2]Source: Blessing Aderibigbe, “Alginate in Wound Dressings,” mdpi.com Commercial systems such as Smith+Nephew’s RENASYS EDGE now target outpatient use with light, portable pumps that patients can manage at home, contributing to the USD 33 billion annual cost burden reduction for chronic wounds in the United States. Hybrid variants that fuse suction with antimicrobial foams are moving through regulatory pipelines, promising single-step infection control and fluid management.

Growing Geriatric Population with Impaired Healing

Age-linked hormonal changes and polypharmacy slow every phase of tissue repair, elevating demand for moisture-balanced dressings, oxygen therapies, and growth-factor-infused substitutes. Telehealth programs funded under new Medicare codes equip family members to monitor exudate levels and flag early infection signs, supporting transition of elderly patients to lower-cost care sites without compromising outcomes.

Outpatient Shift to Ambulatory Surgery Centers Boosting Topical Haemostats

Ambulatory surgery centers (ASCs) perform many orthopedic and soft-tissue procedures at 25–50% lower cost than hospital outpatient departments while posting lower infection rates. Surgeons therefore favor topical haemostats that achieve immediate bleeding control and let patients discharge within hours, lifting unit demand for sprayable sealants and resorbable matrices optimized for ASC workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Consumables and Capital Devices | -0.9% | Global, with highest impact in price-sensitive markets | Short term (≤ 2 years) |

| Stringent FDA And EU MDR Evidence Requirements | -0.6% | North America & Europe, with spillover to global markets | Medium term (2-4 years) |

| Supply-Chain Fragility for Alginate and Hydrocolloid Raw Materials | -0.5% | Global, with concentration in seaweed-dependent regions | Short term (≤ 2 years) |

| Growing Antimicrobial Resistance Limits Silver-Based Dressings | -0.4% | Global, with highest impact in hospital settings | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Consumables and Capital Devices

Alginate dressings can cost three times more than gauze in post-surgical care, pressuring budget-conscious hospitals to justify value through reduced length of stay and rehospitalization rates. Hyperbaric oxygen sessions vary from USD 200 to USD 1,250 in the United States, limiting access for uninsured patients despite clear outcome benefits in complex ulcers. The cost-effectiveness challenge intensifies in emerging markets where healthcare budgets prioritize basic care delivery over advanced wound management technologies.

Supply-Chain Fragility for Alginate and Hydrocolloid Raw Materials

Seaweed harvest disruptions have swung alginate prices sharply in recent years, echoing fluid-bag shortages that prompted the United States to invoke the Defense Production Act after Hurricane Helene shut a key plant. Suppliers are diversifying cultivation sites and stockpiling critical inventories, yet sustained volatility continues to pinch gross margins and may delay product launches relying on these biopolymers.[3]Source: J.W. Jeong, “Closed-Incision NPWT in Elderly Patients,” BMC Geriatrics, doi.org Supply chain diversification efforts are underway, but the specialized nature of these materials limits alternative sourcing options and maintains pricing volatility that affects wound care product costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Advanced Solutions Drive Premium Positioning

Advanced wound care held 44.37% of acute wound care market share in 2025 as clinicians pivoted to dressings that maintain optimal moisture, regulate bacterial load, and shorten recovery cycles. Surgical products are catching up, growing at a 5.62% CAGR on the back of bioactive sutures and topical sealants tailored to minimally invasive techniques. This bifurcation illustrates how hospitals weigh cost-per-patient savings over sticker price when outcomes data are compelling. Smith+Nephew reported 12.2% growth in its Advanced Wound Management unit in Q4 2024 after rolling out the RENASYS EDGE line, reinforcing that evidence-backed innovations translate into swift uptake.

Conventional gauze and tape remain staples in first-aid and low-complexity cases, yet their commodity pricing constricts margins. Manufacturers are countering with turnkey kits that bundle basic and advanced items, enabling procurement teams to lock in volume discounts while upgrading standard of care. Skin substitutes spearheaded by university-industry collaborations, such as the UGRSKIN artificial dermis, are showing 80% survival in severe burn patients and could capture incremental acute wound care market size over the decade.

By Wound Type: Surgical Dominance Meets Burns Innovation

Surgical and traumatic injuries accounted for 68.72% of acute wound care market size in 2025, aligning with the global increase in operating-room throughput. Standardized perioperative protocols guarantee baseline product consumption, anchoring predictable revenue streams. In parallel, the burns sub-segment is projected to outpace the core market at 5.34% CAGR through 2031, propelled by bioengineered grafts and oxygen-rich matrices that accelerate epithelialization. Academic trials using acellular fish-skin grafts have demonstrated superior donor-site healing, pointing to scalable, cost-effective alternatives for wide-area injuries.

Trauma-oriented solutions integrate rapid haemostasis agents with antimicrobial hydrofibers, critical during the “golden hour” of emergency care. Defense agencies, motivated by battlefield casualty data, are stockpiling vacuum dressings and freeze-dried plasma to stabilize wounds before surgical evacuation, indirectly expanding civilian access as surplus flows into public hospitals.

By End User: Hospital Centricity Yields to Home Care

Hospitals and specialty clinics retained 62.25% revenue in 2025, yet referral patterns reveal a gradual decentralization. Home-care providers are projected to lift their share on 5.76% CAGR tailwinds as tele-monitoring platforms guide dressing changes and escalate alerts when infections loom. For hospitals, bundling acute wound care kits into discharge plans limits readmission penalties under value-based purchasing mandates.

ASCs occupy a strategic middle ground. Spinal and orthopedic surgeons cite 25–50% cost savings and reduced infection risk when operating in ASC suites, incentivizing supply directors to stock sprayable haemostats and pre-sterilized NPWT canisters suited for same-day turnover. Long-term care facilities mirror hospital protocols but adopt dressings that can remain in situ for five to seven days, minimizing staff workload.

Geography Analysis

North America dominated with 37.98% of acute wound care market share in 2025 as private insurers and federal payers funded high-end solutions, including smart bandages embedded with impedance sensors that track moisture and pH in real time. Medicare’s new caregiver-training codes reinforce adoption by paying for education that supports safe home transitions. Defense Department contracts, such as the USD 75 million award to Smith+Nephew for NPWT kits, inject additional volume and underwrite R&D geared toward extreme environments.

Europe tracks a steadier pace under the Medical Device Regulation, which favors firms with mature quality systems and extensive clinical dossiers. Germany, France, and the United Kingdom maintain dense hospital networks that standardize evidence-based wound protocols, sustaining premium price points for silver-alginate foams with documented antimicrobial stewardship benefits. Southern European nations leverage medical-tourism inflows to justify investments in laser-assisted skin substitutes and oxygen chambers, broadening the region’s product mix.

Asia-Pacific is the fastest-growing zone at 6.04% CAGR through 2031. China channels public and private investment into geriatric care centers, while Japan blends Western dressings with herbal extracts to tailor solutions for diabetic ulcers. Indian state governments are subsidizing NPWT pumps for district hospitals, unlocking rural demand. Australia and South Korea serve as R&D hubs, testing wearable electroceuticals that deliver mild currents to enhance granulation. Collectively, the region’s demographic surge and infrastructure builds expand the addressable acute wound care market.

Competitive Landscape

The industry is moderately concentrated: the top five suppliers control an estimated substantial share of global sales, balanced by agile startups pushing sensors, 3D-printed grafts, and enzymatic debriders. Smith+Nephew’s 12.2% Q4 2024 uplift stemmed from the RENASYS EDGE launch and double-digit NPWT adoption among U.S. trauma centers. Johnson & Johnson expanded its biosurgery line with ETHIZIA, a patch designed to seal diffuse bleeding in laparoscopic procedures.

Regulatory shifts amplify competitive stakes. The FDA’s proposed rule to reclassify antimicrobial dressings obliges companies to furnish clinical evidence that products do not fuel resistance, potentially sidelining generic silver foams and rewarding innovators with broad-spectrum, low-resistance chemistries. European Notified Bodies, already backlogged, prioritize dossiers from suppliers with ISO-aligned processes, nudging consolidation as smaller firms seek partnerships to shoulder compliance costs.

Technological convergence is blurring boundaries between device and digital domains. Start-ups backed by venture capital are embedding Bluetooth modules in dressings that transmit exudate data to cloud dashboards, enticing home-care agencies. Established players respond by acquiring sensor tech outfits or co-developing platforms that lock buyers into integrated ecosystems. The race now hinges on producing peer-reviewed outcome data that satisfy payers looking to curb total cost of care.

Acute Wound Care Industry Leaders

Coloplast A/S

Medtronic PLC

Smith+Nephew

Convatec Inc.

Medline Industries, LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Smith+Nephew’s RENASYS EDGE Negative Pressure Wound Therapy System won the Red Dot Award for Design Concept 2024, highlighting its portability and user-centric interface.

- October 2024: StimLabs introduced Corplex P in the United States, marking it one of the first medical device derived from human umbilical cord extracellular matrix (ECM) to receive United States Food and Drug Administration (FDA) clearance. The dehydrated human umbilical cord particulate (dHUCP) device is designed for the treatment of hard-to-heal wounds, offering key advantages in its composition, configuration, and moisture regulation.

- September 2024: Solventum introduced the V.A.C. Peel and Place Dressing, an integrated solution that simplifies application to under two minutes and provides continuous wear for up to seven days. This innovation contrasts with traditional negative pressure wound therapy dressings, which require more time for application, multiple components, and frequent changes.

Global Acute Wound Care Market Report Scope

As per the scope of this report, acute wound care involves the assessment and treatment of sudden injuries, such as cuts, burns, or surgical incisions, to promote rapid healing and prevent infection. This process emphasizes timely intervention, proper wound cleaning, and the application of appropriate dressings to restore skin integrity effectively. The acute wound care market is segmented by product type, wound care, end user, and geography. The product type segment is further segmented into advanced wound care, surgical wound care, and traditional wound care. The advanced wound care segment is further segmented into advanced wound care dressings, wound therapy devices, and topical agents. The surgical wound care segment is further divided into sutures, staplers, and tissue adhesive, sealants, and glues. The traditional wound care segment is further segmented into medical tapes, dressings, and cleansing agents. The wound care segment is segmented into surgical and traumatic wounds and burns & other wounds. The end-user segment is divided into hospitals, specialty clinics, home care settings, and other end users. The geography segment is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in USD for the above segments.

| Advanced Wound Care | Advanced Dressings |

| Negative-Pressure Wound-Therapy (NPWT) Devices | |

| Oxygen & Electro-stimulation Systems | |

| Surgical Wound Care | Sutures |

| Staplers | |

| Tissue Adhesives, Sealants and Glues | |

| Traditional Wound Care | Medical Tapes |

| Gauze and Basic Dressings | |

| Cleansing Agents |

| Surgical and Traumatic Wounds |

| Burns |

| Other Acute Wounds |

| Hospitals and Specialty Clinics |

| Ambulatory Surgical Centers |

| Home-Care Settings |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Advanced Wound Care | Advanced Dressings |

| Negative-Pressure Wound-Therapy (NPWT) Devices | ||

| Oxygen & Electro-stimulation Systems | ||

| Surgical Wound Care | Sutures | |

| Staplers | ||

| Tissue Adhesives, Sealants and Glues | ||

| Traditional Wound Care | Medical Tapes | |

| Gauze and Basic Dressings | ||

| Cleansing Agents | ||

| By Wound Type | Surgical and Traumatic Wounds | |

| Burns | ||

| Other Acute Wounds | ||

| By End User | Hospitals and Specialty Clinics | |

| Ambulatory Surgical Centers | ||

| Home-Care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the acute wound care market in 2031?

The acute wound care market is expected to reach USD 10.45 billion by 2031.

Which product segment is growing fastest?

Surgical wound care is forecast to expand at a 5.62% CAGR between 2026 and 2031.

Why are ambulatory surgery centers important for acute wound care suppliers?

ASCs deliver 25–50% cost savings over hospital outpatient departments and demand haemostatic agents that enable same-day discharge, lifting product turnover.

Which region will post the highest growth rate through 2031?

Asia-Pacific is set to record a 6.04% CAGR, driven by healthcare infrastructure expansion and aging populations.

How are regulators shaping product development?

The FDA’s proposal to reclassify antimicrobial dressings and the EU Medical Device Regulation both require stronger clinical evidence, favoring companies with robust R&D and compliance capabilities.

Page last updated on: