Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

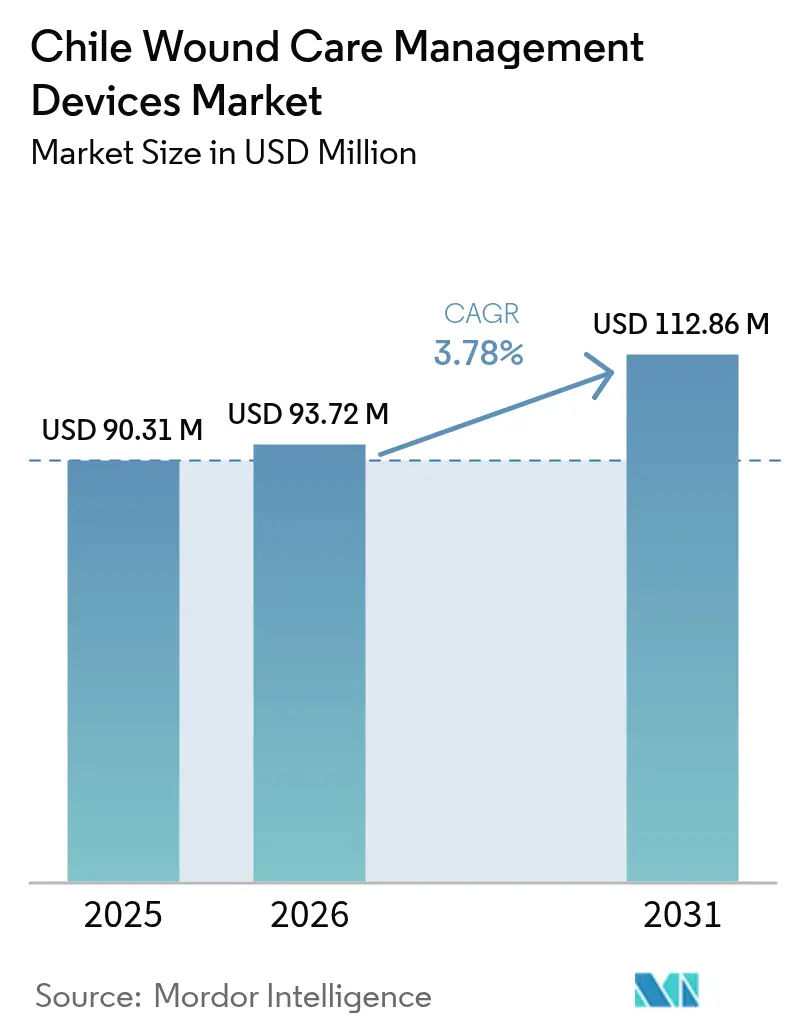

| Base Year Market Size (2025) | USD 90.31 Million |

| Market Size (2026) | USD 93.72 Million |

| Market Size (2031) | USD 112.86 Million |

| Growth Rate (2026 - 2031) | 3.78% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Chile Wound Care Management Devices Market Analysis by Mordor Intelligence

The Chile wound care management devices market size was valued at USD 90.31 million in 2025 and estimated to grow from USD 93.72 million in 2026 to reach USD 112.86 million by 2031, at a CAGR of 3.78% during the forecast period (2026-2031). This growth curve reflects the country’s demographic shift toward an older society, the sustained diabetes burden, and hospital infrastructure modernization. Higher surgical throughput in private ISAPRE facilities, 2.8 times that of public FONASA hospitals, accelerates demand for advanced dressings, closure systems, and negative pressure wound therapy (NPWT) units [1]María Jesús Lira, "Disparity in access to orthopedic surgery between public and private healthcare insurance: a nationwide population-based study," BMC Musculoskeletal Disorders, bmcmusculoskeletdisord.biomedcentral.com. Government investments in specialized wound units, coupled with regulatory reforms that enable online pharmaceutical sales, further widen patient access to sophisticated products. At the same time, import-dependent supply chains and limited outpatient reimbursement temper short-term momentum but do not derail the upward trajectory of the Chile wound care management devices market.

Key Report Takeaways

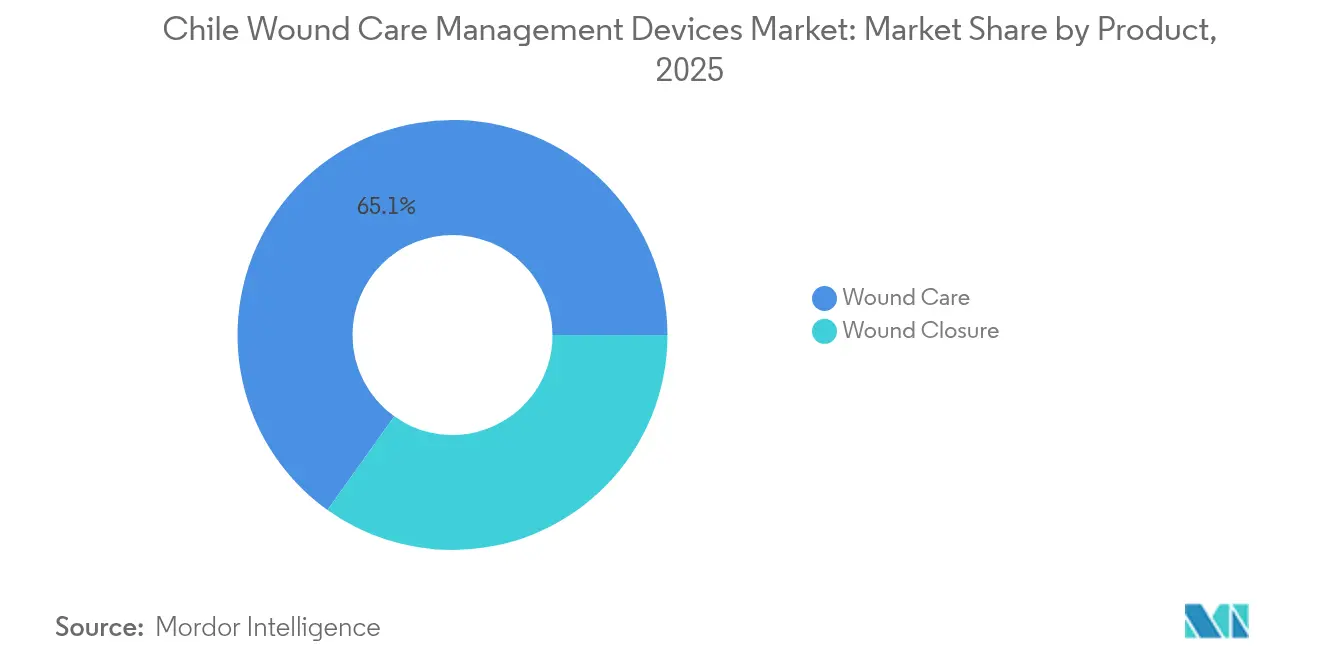

- By product category, wound care devices captured 65.12% of the Chile wound care management devices market share in 2025, whereas wound closure is on track to expand at a 4.21% CAGR through 2031.

- By wound type, chronic wounds held 61.85% share of the Chile wound care management devices market size in 2025; acute wounds are projected to advance at a 4.24% CAGR to 2031.

- By end user, hospitals and specialty wound clinics commanded 51.98% share in 2025, while home healthcare settings are set to grow fastest at 4.38% CAGR.

- By mode of purchase, institutional procurement controlled 64.62% of transactions in 2025, whereas the retail/OTC channel is forecast to rise at a 4.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chile Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic wounds, ulcers & diabetic ulcers | +1.2% | National, with concentration in Santiago, Valparaíso, Concepción | Long term (≥ 4 years) |

| Growing incidence of injuries from road traffic & sports accidents | +0.8% | National, with higher impact in urban centers | Medium term (2-4 years) |

| Ageing population increasing demand for advanced wound care | +1.1% | National, accelerating in metropolitan regions | Long term (≥ 4 years) |

| Government investment in public-hospital wound units | +0.6% | National, prioritizing underserved regions | Medium term (2-4 years) |

| Expansion of private health-insurance coverage boosting AWC adoption | +0.7% | National, with early gains in Santiago, Valparaíso, Concepción | Medium term (2-4 years) |

| Emergence of locally-made cost-competitive NPWT systems | +0.4% | National, with manufacturing focus in central regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising burden of chronic wounds, ulcers & diabetic ulcers

Diabetes affects 11% of Chilean adults, and diabetic foot ulcers afflict 11% of those patients, translating into persistent demand for advanced dressings, NPWT units, and limb-salvage technologies. Venous ulcers constitute 70% of chronic wounds nationwide, while pressure ulcers appear in 28% of hospitalized patients, increasing material consumption in public and private hospitals alike. Multidisciplinary programs that prioritize limb preservation are spreading from metropolitan hospitals to regional centers, stimulating adoption of microsurgical techniques and tissue-regeneration devices. Cost-effective local manufacturing initiatives target the public sector, ensuring that the Chile wound care management devices market remains accessible despite pricing pressures.

Growing incidence of injuries from road traffic & sports accidents

Rapid urbanization and rising sports participation translate into higher trauma volumes and post-operative wound care needs. Emergency departments increasingly deploy tissue adhesives and surgical staplers that shorten closure time and reduce infection risk. ISAPRE facilities first integrate these advanced tools, but diffusion to FONASA hospitals is expected as national trauma protocols standardize. This pathway underpins medium-term growth in the Chile wound care management devices market and reinforces demand for disposable closure and dressing kits.

Ageing population increasing demand for advanced wound care

By 2040, more than 20% of Chile’s population will be aged 60 or older, and multimorbidity drives complex wound profiles requiring sustained management. Home healthcare programs record that 73.8% of participants are seniors with high dependency levels, prompting the Ministry of Health to publish gerontogeriatric nursing guidelines that highlight prevention, rapid diagnosis, and evidence-based therapy selection. Consequently, easy-to-use foam dressings, silver-impregnated antimicrobials, and portable NPWT devices gain traction in the Chile wound care management devices market.

Government investment in public-hospital wound units

Chile’s inclusion in the Alliance for Primary Health Care in the Americas underscores its commitment to upgrade public hospital capabilities, including specialized wound units staffed by multidisciplinary teams [2]PAHO, "Chile becomes latest country to join the Alliance for Primary Health Care in the Americas," paho.org. Procurement policies emphasize cost-effective standardized kits, opening the door for domestic suppliers of gauze, hydrocolloids, and second-generation NPWT systems. The resulting infrastructure improvement narrows the treatment gap between public and private facilities and delivers a predictable demand stream that supports the Chile wound care management devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment cost of advanced wound care devices | -0.9% | National, with greater impact in public healthcare sector | Medium term (2-4 years) |

| Limited reimbursement for outpatient wound therapies | -0.7% | National, affecting both public and private sectors | Long term (≥ 4 years) |

| Shortage of certified wound-care nurses in regional hospitals | -0.5% | National, with concentration in rural and peripheral regions | Medium term (2-4 years) |

| Import-dependent supply chain vulnerable to FX volatility | -0.3% | National, with higher impact on premium device segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High treatment cost of advanced wound care devices

Commercial NPWT sessions exceed USD 870 per treatment, compared with open-source alternatives under USD 75, a 58-fold differential that restricts uptake in the public sector. Private patients also experience out-of-pocket strain because healthcare spending exceeds 30% of total expenditure, limiting premium device penetration. Local innovators now prototype affordable NPWT kits, yet regulatory clearance remains a hurdle that slows adoption and marginally suppresses the Chile wound care management devices market [3]Carla Castillo-Laborde, "Access to medicines for the treatment of chronic diseases in Chile: qualitative analysis of perceived patient barriers and facilitators in five regions of the country," BMC Health Services Research, bmchealthservres.biomedcentral.com.

Limited reimbursement for outpatient wound therapies

Chile’s guaranteed benefits scheme omits many chronic wound consumables, pushing patients toward self-funded purchases. This gap deters widespread use of home-based NPWT and advanced dressings despite clinical necessity, redirecting complex cases back to inpatient settings. Online pharmacies partially alleviate access barriers, but sustained policy reform is required to unleash the full potential of home management within the Chile wound care management devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound care dominance drives innovation

In 2025, wound care devices commanded 65.12% of the Chile wound care management devices market share due to the prevalence of chronic ulcers and pressure injuries. Advanced dressings deliver 47.1% fewer changes and 58.6% cost savings relative to traditional gauze, fostering rapid uptake in tertiary hospitals. The Chile wound care management devices market size for wound care products is projected to grow at a 3.92% CAGR to 2031, underpinned by local NPWT prototypes that close the affordability gap for public clinics. Traditional materials still circulate in resource-constrained rural hospitals, while silver and hydrogel variants expand fastest in private facilities.

Wound closure is the fastest-growing product category at 4.21% CAGR, propelled by higher orthopedic procedures and sports injury repairs. Surgical staplers and cyanoacrylate adhesives reduce operating room time and lower infection risk, making them attractive to both private and public surgeons. The uptick in device clinical trials—33 registrations in 2024—signals that multinational firms view Chile as a test bed for next-generation closure platforms, further enriching the Chile wound care management devices market.

By Wound Type: Chronic wounds reflect demographic reality

Chronic wounds held 61.85% of the Chile wound care management devices market size in 2025, mainly attributable to diabetic foot ulcers, venous leg ulcers, and pressure ulcers in bedridden seniors. Multidisciplinary limb-salvage teams are mainstreaming epidermal growth factor therapies and integrated offloading protocols that extend dressing lifespans and minimize amputations. Advanced compression systems earn steady adoption within public diabetes clinics, confirming the long-term volume base for chronic wound supplies across the Chile wound care management devices market.

Acute wounds expand at 4.24% CAGR as urban trauma volumes climb. Emergency services embed single-use stapling kits and antimicrobial suture materials that accelerate closure while containing infection. The popularity of adventure sports in metropolitan regions such as Santiago and Valparaíso fuels retail demand for waterproof adhesive dressings that support rapid return to activity. This momentum keeps the acute segment a vibrant contributor to the Chile wound care management devices market.

By End User: Home healthcare transformation accelerates

Hospitals and specialty wound clinics accounted for 51.98% revenue in 2025, sustaining high usage of advanced dressings, biologics, and NPWT. Yet the move toward decentralized care shifts growth to patient homes where portable devices and easy-application dressings prevail. The home care segment is forecast to rise at 4.38% CAGR through 2031, supported by national gerontogeriatric guidelines and family caregiver training programs. As a result, the Chile wound care management devices market continually innovates toward smaller, battery-operated NPWT units and simplified dressing kits suitable for layperson use.

Long-term care facilities maintain a stable share because of entrenched pressure ulcer protocols for residents with mobility limitations. In regional hospitals, the shortage of certified wound nurses encourages adoption of foam dressings with wear indicators and pre-set suction pumps that reduce manual oversight. These dynamics collectively broaden the customer base inside the Chile wound care management devices market.

By Mode of Purchase: Retail channel gains momentum

Institutional procurement dominated 64.62% of 2025 orders thanks to centralized tenders that prioritize cost-effectiveness and supply-chain reliability. Local manufacturers exploit this environment by courting public buyers with standardized kits that satisfy nationwide formularies. These large-volume contracts underpin predictable demand patterns for the Chile wound care management devices market.

The retail/OTC channel is growing at a 4.27% CAGR as regulatory changes allow licensed online pharmacies to ship wound products directly to patients. Chronic ulcer sufferers who face reimbursement gaps increasingly buy foam dressings, antimicrobial gels, and compression wraps out of pocket. Pharmacies partner with courier services to guarantee 48-hour delivery across metropolitan regions, enhancing convenience and fueling consumer trust in e-commerce within the Chile wound care management devices market.

Geography Analysis

Chile’s highly centralized population places the largest share of the Chile wound care management devices market in the Santiago Metropolitan Region, followed by Valparaíso and Concepción. These hubs host the majority of tertiary hospitals and private surgical centers, which adopt advanced dressings early and generate strong demand for NPWT rentals. ISAPRE-insured patients in these cities undergo surgeries at rates 2.8 times greater than their FONASA counterparts, ensuring a receptive audience for premium wound closure systems.

Outside metropolitan zones, northern macro-regions such as Antofagasta and Atacama display steady yet lower consumption, constrained by fewer specialists and longer referral pathways. The sale of Bupa-owned San José Clinic in Arica exemplifies ongoing realignment among secondary hospitals seeking operational efficiencies. Consequently, public tenders in these areas favor economical foam dressings and reusable compression wraps that match budget limits, yet still add volume to the Chile wound care management devices market.

In southern zones like Los Ríos and Aysén, harsh weather and dispersed communities complicate logistics and lengthen lead times for imported devices. Government investments in telehealth and primary-care wound programs bridge access gaps by enabling remote follow-up and nurse-guided home dressing changes. As infrastructure improves, regional consumption of portable NPWT and infection-control dressings rises, incrementally boosting the overall Chile wound care management devices market.

The Ñuble Health Service posts the highest diabetic screening coverage at 49.5%, indicating robust chronic-disease management infrastructure that supports early ulcer intervention. In contrast, the Central Metropolitan Service lags at 15%, illuminating disparities even within urban settings. Public-private partnership programs are targeting these gaps through mobile wound caravans and shared clinical-rotation schemes, ensuring that the Chile wound care management devices market expands on a nationwide, rather than purely metropolitan, basis.

Competitive Landscape

The Chile wound care management devices market shows moderate concentration, where multinationals and agile local firms share turf. Smith+Nephew reported 3.8% growth in its Advanced Wound Management portfolio in Q1 2025, crediting demand for foam dressings and NPWT. Its recent USD 75 million Department of Defense contract may yield technology spillovers that reach Chilean buyers. Baxter International also logged high single-digit gains in its Medical Products & Therapies unit as hospitals replenish dressing and closure inventories.

Domestic innovators focus on low-cost NPWT devices made from locally sourced components, addressing the public sector’s strict pricing ceilings. Prototype pumps priced below USD 75 have completed clinical pilot studies, and ongoing regulatory reviews aim to grant market entry in 2026. These developments intensify competition by offering an attractive alternative to imported systems in the Chile wound care management devices market.

Strategic alliances between pharmaceutical distributors and medical device firms enable bundled offerings that package antimicrobial dressings with oral antibiotics or pain management kits. Such integration appeals to hospital procurement offices seeking comprehensive solutions that reduce vendor fragmentation. Concurrently, Chile’s role as a regional clinical-trial hub—hosting 33 device trials in 2024—draws global companies to establish in-country subsidiaries, raising the innovation bar across the Chile wound care management devices market.

Chile Wound Care Management Devices Industry Leaders

-

Smith & Nephew

-

Solventum

-

Medtronic

-

Convatec

-

Coloplast

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Chile joined the Alliance for Primary Health Care in the Americas, a Pan American Health Organization initiative that aligns resources for stronger primary care and improved wound service delivery.

- March 2025: The Ministry of Health issued Decree 5 Exempt, broadening regulatory oversight from immunohematology reagents to a wider range of medical devices, signaling stricter safety standards for wound-care equipment.

- February 2024: Bupa Chile divested its San José Clinic in Arica to Red Interclínica, reflecting healthcare sector restructuring aimed at operational efficiency.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Chile wound-care management devices market as all single-use and reusable hardware, such as negative-pressure wound therapy systems, oxygen and electrical stimulation units, and mechanical closure tools, sold for the prevention or treatment of acute and chronic lesions across hospitals, long-term facilities, and home-care settings. Values are expressed at manufacturer invoice level in USD terms for 2024 as base year and 2025-2030 forecasts.

Dressings, creams, and purely pharmaceutical topical agents are not counted, since they belong to consumables rather than devices.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Topical Agents

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Detailed Research Methodology and Data Validation

Primary Research

Telephone interviews and online surveys with Chilean wound-care nurses, biomedical engineers, procurement heads, and import distributors helped us test secondary assumptions, verify channel mark-ups, and gauge replacement cycles for key devices. Insights from Latin American key-opinion surgeons were blended in to benchmark therapy penetration outside Santiago.

Desk Research

Mordor analysts first mapped the addressable pool using open data from the Chilean Ministry of Health procedure database, Servicio Nacional de Aduanas import codes, OECD Health Statistics, Pan-American Health Organization epidemiology bulletins, and trade association releases such as Sociedad Chilena de Heridas. Company financials were screened through D&B Hoovers and news archives on Dow Jones Factiva to track local revenue splits of global suppliers.

We enriched the picture with hospital tender notices on Tenders Info, patent trends on Questel, and clinical-trial registries that signal upcoming technology adoption. These references establish incidence rates, installed base, and average selling prices that anchor sizing inputs. The sources listed illustrate the range consulted; many additional documents were reviewed to cross-validate figures and clarify gray areas.

Market-Sizing & Forecasting

The core model begins with a top-down reconstruction of manufacturer sales obtained by aligning import-export statistics and local production declarations, which are then adjusted for channel margins and parallel trade. Sampled bottom-up checks, unit deliveries of NPWT pumps, estimated procedure counts for diabetic foot ulcers, and average closure device use per surgery, provide reality checks that refine totals. Critical variables include diabetes prevalence, elective surgical backlog, public-hospital capital budget growth, inflation-indexed device ASPs, and gradual uptake of portable NPWT kits. A multivariate regression, validated through ARIMA overlap tests, projects each driver to 2030; scenario analysis captures policy or currency shocks, and gaps in bottom-up inputs are bridged with weighted regional benchmarks.

Data Validation & Update Cycle

Outputs pass variance screens against historic series and peer signals; anomalies trigger analyst review and, if needed, re-contact of experts. Reports refresh every twelve months, with interim updates when material events, such as reimbursement rule changes, occur, and each delivery includes a last-minute sense-check by a fresh analyst pair.

Why Mordor Intelligence's Chile Wound Care Management Devices Baseline Commands Reliability

Published estimates frequently diverge because publishers choose unlike product baskets, pricing layers, and refresh rhythms.

Key gap drivers include whether consumable dressings are mixed with devices, how home-care OTC sales are treated, the currency inflator chosen, and the cadence at which new reimbursement ceilings are folded in. Mordor's disciplined scope, annual refresh, and dual-path validation mean its baseline stays closest to the observable device market.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 90.31 M (2025) | Mordor Intelligence | - |

| USD 180 M (2024) | Global Consultancy A | Includes dressings and topical products plus pharmacy OTC sales |

| USD 179.35 M (2024) | Industry Journal B | Uses list prices and bundles advanced consumables with capital devices |

In sum, while other publishers widen or compress totals by shifting boundaries or cost layers, Mordor's transparent variable set and documented steps deliver a balanced, reproducible baseline that decision-makers can track year after year.

Key Questions Answered in the Report

What is the current size of the Chile wound care management devices market?

The market is valued at USD 93.72 million in 2026.

Which product category holds the largest share?

Wound care devices lead with 65.12% market share in 2025.

Which segment is growing fastest by end user?

Home healthcare settings are expanding at a 4.38% CAGR through 2031.

How does diabetes influence demand for wound care solutions in Chile?

Diabetes affects 11% of adults and drives persistent demand for advanced dressings, NPWT, and limb-salvage technologies.

What is the key regulatory change affecting retail access to wound products?

A 2020 decree authorizes online pharmaceutical sales, boosting growth of the retail/OTC channel.

Why are locally manufactured NPWT systems important?

They lower therapy costs, easing adoption in public hospitals and supporting market expansion despite budget constraints.

Page last updated on: