Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.55 Billion |

| Market Size (2031) | USD 26.42 Billion |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

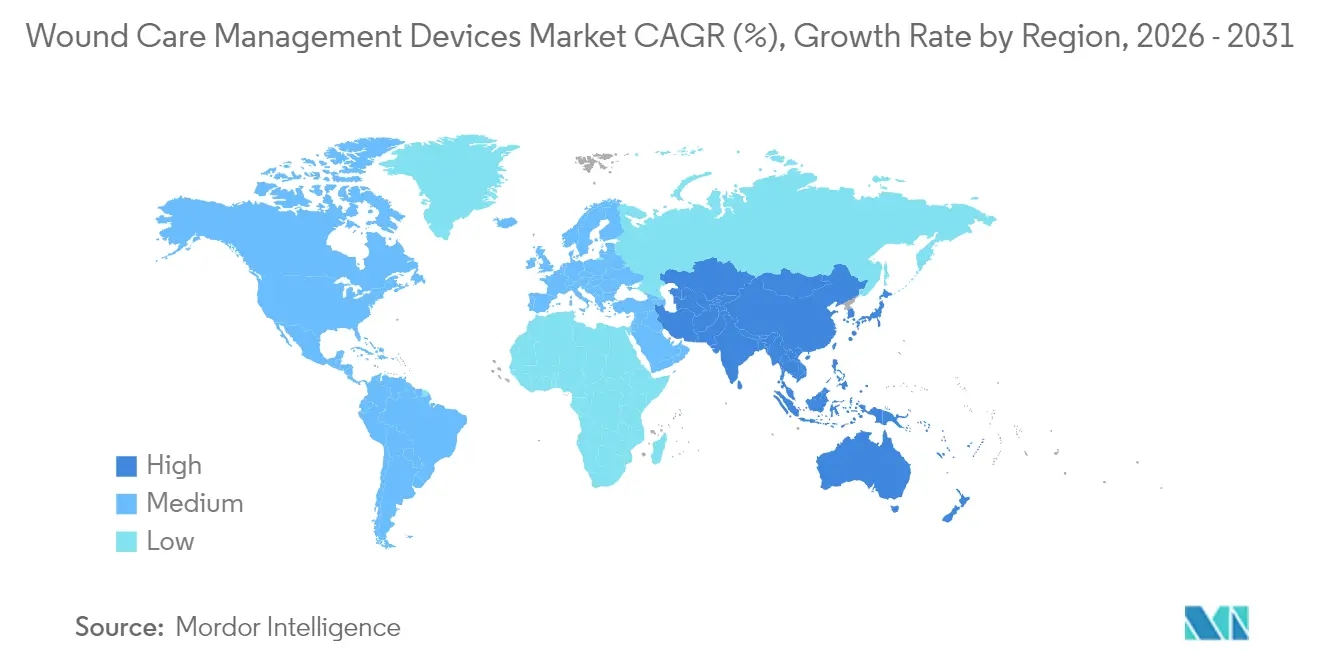

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

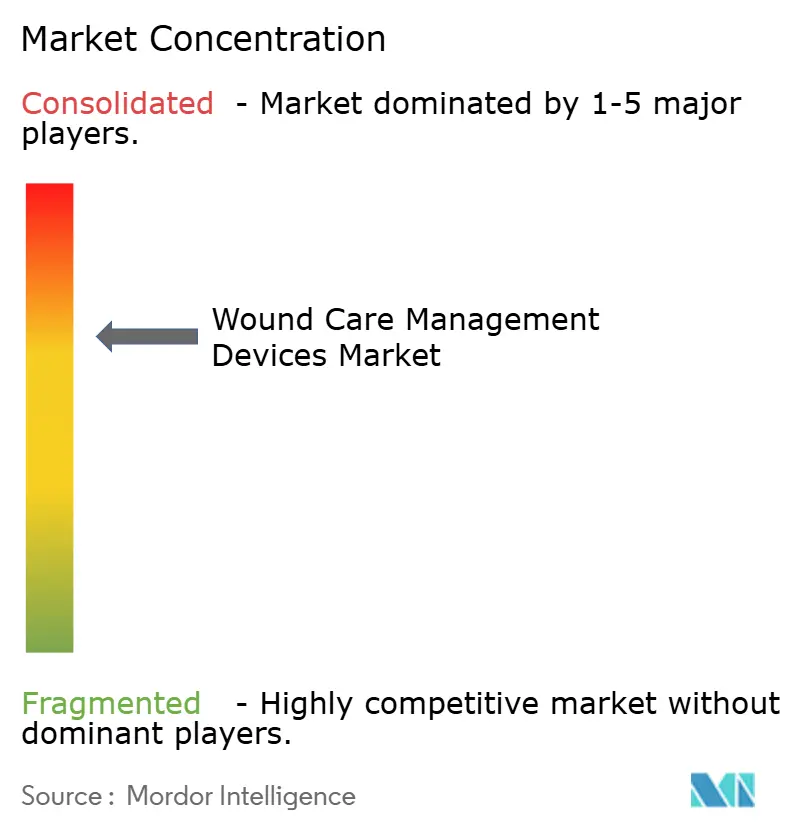

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Wound Care Management Devices Market Analysis by Mordor Intelligence

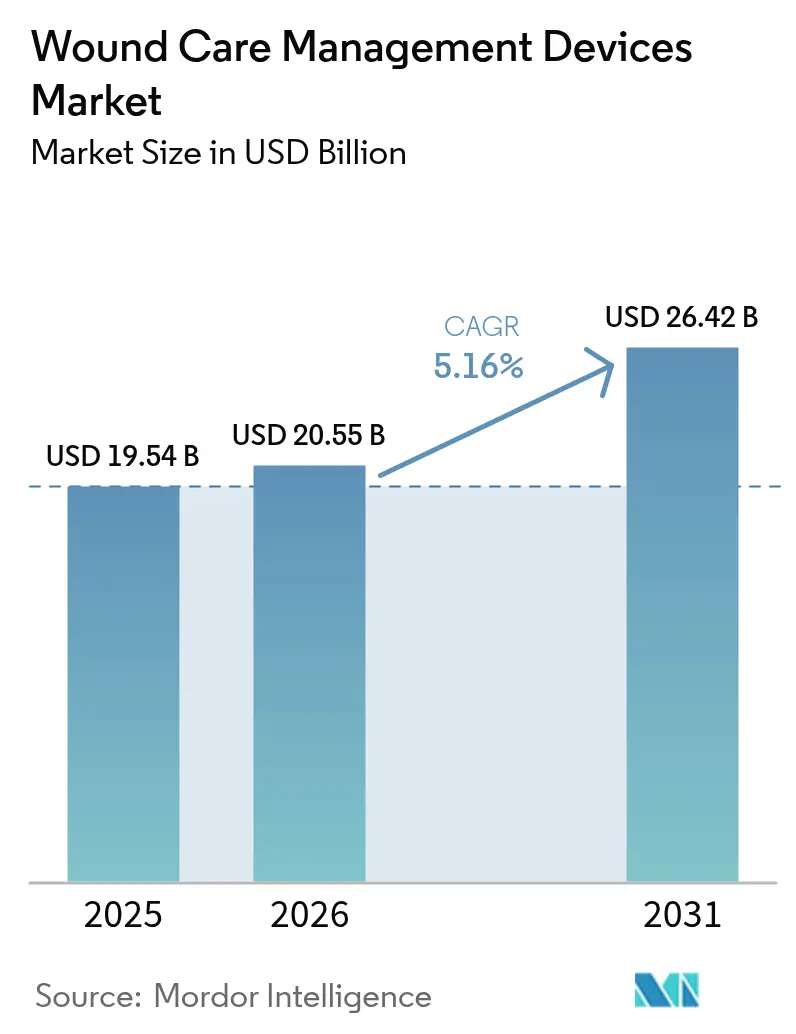

The wound care management devices market size was valued at USD 19.54 billion in 2025 and estimated to grow from USD 20.55 billion in 2026 to reach USD 26.42 billion by 2031, at a CAGR of 5.16% during the forecast period (2026-2031). Aging populations, the rising prevalence of diabetes, and steady growth in surgical procedures provide persistent demand tailwinds [1]Nasire Uluç, "Non-invasive measurements of blood glucose levels by time-gating mid-infrared optoacoustic signals," Nature Metabolism, nature.com. Hospitals are investing in negative-pressure wound therapy (NPWT) and smart dressings to curb readmissions, while retailers expand over-the-counter offerings that empower home-based treatment. Breakthroughs such as algae-derived hemostatic gels and bioengineered tissue matrices are shortening healing times and lowering long-term costs. Regulatory pathways in the United States and the European Union now fast-track class-I liquid bandages and other low-risk devices, accelerating commercialization. Market incumbents respond by forging alliances with AI specialists to embed real-time imaging and decision support into dressings and pumps.

Key Report Takeaways

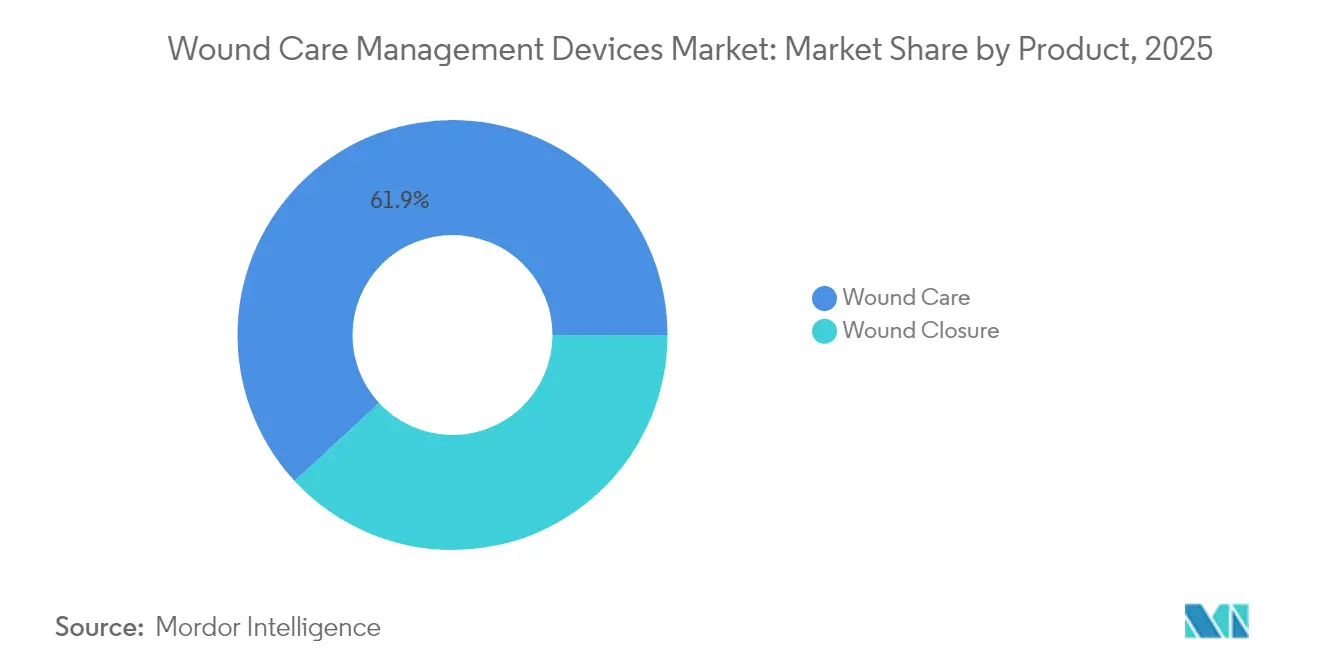

- By product category, wound care maintained 61.88% of the wound care management devices market share in 2025, while wound closure products registered the fastest 5.62% CAGR through 2031.

- By wound type, chronic wounds accounted for a 57.92% share of the wound care management devices market size in 2025, whereas acute wounds are poised for a 5.74% CAGR to 2031.

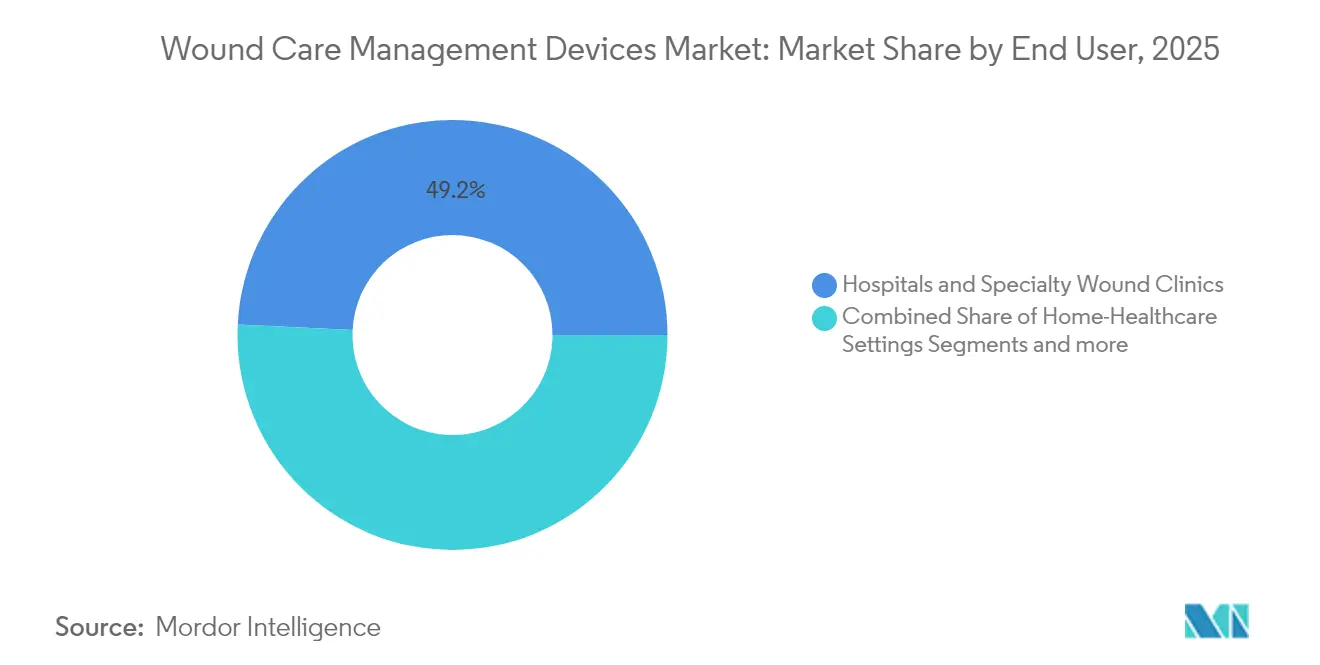

- By end user, hospitals and specialty clinics held 49.22% revenue share in 2025; home healthcare is projected to grow at 5.81% CAGR through 2031.

- By mode of purchase, institutional procurement commanded 58.84% of 2025 revenue, while retail and over-the-counter sales will expand at 5.86% CAGR to 2031.

- By geography, North America held 39.86% revenue share in 2025; Asia-Pacific is projected to grow at 6.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of chronic & diabetic wounds | +1.2% | North America & Europe highest; global relevance | Long term (≥ 4 years) |

| Escalating global surgical volumes | +0.9% | Developed markets lead; emerging markets catching up | Medium term (2-4 years) |

| Continuous product & material innovations | +0.8% | North America & EU leading; APAC adoption | Medium term (2-4 years) |

| Shift toward home-care & single-use NPWT | +0.7% | North America & Europe first; APAC expanding | Short term (≤ 2 years) |

| AI-enabled wound imaging & decision support | +0.5% | North America & EU core; spill-over to APAC | Medium term (2-4 years) |

| Outcome-based reimbursement reforms | +0.4% | North America & EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic & Diabetic Wounds

Diabetic foot ulcers now affect 15% of patients living with diabetes, driving hospitals to adopt multidisciplinary programs that pair advanced dressings with continuous glucose monitoring. Time-gated mid-infrared optoacoustic sensors enable depth-selective glucose readings, allowing clinicians to adjust therapy before complications arise. Early intervention strategies are shrinking hospitalization days and lowering amputation risks. Payers reward these outcomes with bundled payments that cover dressings, sensors, and telehealth follow-ups. Manufacturers are therefore integrating electronics into dressings to transmit moisture, pH, and temperature data, aligning device design with chronic-care protocols.

Escalating Global Surgical Volumes

Worldwide elective and trauma procedures rebounded in 2025, increasing demand for advanced closure strips, tissue sealants, and NPWT canisters. Mohs micrographic surgery trials on the scalp confirmed that pinch grafting reduces healing times versus second-intention protocols [2]Willenbrink, Tyler J. MD, "Pinch Grafts Versus Second Intention Wound Healing for Mohs Micrographic Surgery Defects Below the Knee: A Prospective Randomized Trial," Dermatologic Surgery, journals.lww.com. As ambulatory surgical centers scale throughput, they deploy compact NPWT pumps that fit same-day discharge models. Ultrasound-guided debridement heads off infection risk, and real-time imaging helped cut readmission penalties at high-volume hospitals in the United States. These results encourage procurement teams to refresh closure portfolios despite budget pressures.

Continuous Product & Material Innovations

Chitosan dressings loaded with silver nanoparticles achieve broad-spectrum antimicrobial activity while stimulating TGF-β and EGF expression, expediting tissue regeneration [3]Roma M, "Chitosan nanoparticle applications in dentistry: a sustainable biopolymer," Frontiers in Chemistry, frontiers.org. Start-ups are layering hydrogel matrices with stem-cell exosomes to trigger angiogenesis in ischemic wounds. Sustainability considerations now guide substrate choice, pushing suppliers toward biodegradable polymers and recyclable secondary packaging. Device makers test smart patches that release growth factors when sensor-detected oxygen drops below set thresholds. These active systems transition the wound care management devices market away from passive coverings to therapeutics that adapt in situ.

Shift Toward Home-Care & Single-Use NPWT Devices

Disposable NPWT kits weighing under 200 g allow patients to ambulate without mains-powered pumps, aligning therapy with outpatient reimbursement codes. Remote dashboards transmit pressure and exudate levels to nurses who adjust settings without clinic visits, halving follow-up travel costs in pilot programs across Germany and Michigan. Home-care agencies bundle these kits with education modules delivered by nurse practitioners, boosting adherence and shortening therapy cycles. The retail channel benefits as pharmacies list dressings pre-trimmed for single-use pumps, extending access in rural regions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited reimbursement in emerging markets | -0.6% | APAC, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| High total cost of advanced therapies | -0.4% | Global; acute in price-sensitive economies | Medium term (2-4 years) |

| Environmental burden of single-use disposables | -0.3% | North America & EU regulatory focus | Long term (≥ 4 years) |

| Shortage of skilled wound-care nurses | -0.2% | Developed markets with aging workforces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Reimbursement in Emerging Markets

Many public insurers in Southeast Asia and Latin America still cover only basic gauze, delaying uptake of NPWT or bioengineered skin substitutes. Rural clinics often face supply-chain gaps that further limit access. Governments are piloting tiered benefit packages that reimburse advanced dressings for diabetic foot ulcers when primary dressings fail, but budget ceilings remain tight. Local assemblers that source polyurethane foams domestically and fill canisters onsite lower price barriers, yet clinician training lags. Public-private partnerships are beginning to bundle devices with outcome-based financing to bridge the affordability gap.

High Total Cost of Advanced Therapies

Comprehensive cost models show that sophisticated pumps, disposables, and service contracts can triple expenditure relative to standard dressings over a 12-week healing cycle. Hospital administrators increasingly demand real-world evidence linking device use to fewer complications or shorter length of stay. Manufacturers are responding with risk-share agreements that refund part of the device cost if healing milestones are missed. Payers in North America now mandate health-economic dossiers before approving formulary inclusion, slowing rollout for new classes such as electro-spun nanofiber scaffolds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound Care Dominance Drives Innovation

The wound care segment held 61.88% of 2025 revenue as clinicians favored antimicrobial foams, hydrofibers, and portable NPWT systems for complex cases. This dominance underscores how the wound care management devices market continues pivoting toward products that cut infection risk and support granulation. Wound closure items—including staples, adhesives, and absorbable barbed sutures—recorded a 5.62% CAGR outlook through 2031, buoyed by growing orthopedics and cardiovascular volumes. Traditional gauze retains relevance in low-acuity settings but yields share to dressings imbued with silver or PHMB for postoperative wounds.

Manufacturers integrating AI chips into dressings enable automatic moisture alerts and dosing of embedded antimicrobials, meeting hospital protocols for pressure-injury prevention. Meanwhile, topical biologics migrate from hospital pharmacies to outpatient infusion centers, expanding reach. The wound care management devices market is seeing combination products that pair a smart sensor layer with a hydrogel drug reservoir, supporting reimbursement under newly issued bundled CPT codes. Suppliers that align material science with digital monitoring gain bargaining power in tenders set by group purchasing organizations.

By Wound Type: Chronic Care Complexity Drives Premium Solutions

Chronic wounds controlled 57.92% of 2025 revenue, reflecting the resource intensity of diabetic foot ulcers, pressure injuries, and venous leg ulcers. These indications demand prolonged therapy, and payers approve high-end dressings when audits confirm reduced readmissions. Acute wounds, including trauma and post-operative incisions, are expanding at a 5.74% CAGR thanks to rising global surgery rates. Burn centers adopt enzymatic debriders paired with biosynthetic skin substitutes to reduce grafting needs.

Predictive algorithms embedded in electronic health records flag patients at ulcer risk, prompting early application of off-loading shoes and moisture-managing foams. Pressure-injury protocols now employ surface sensors that adjust mattress air cells to redistribute load. Diabetic ulcer management benefits from handheld imaging spectrometers that detect perfusion deficits, steering clinicians toward vascular interventions earlier in the care pathway. Such workflow changes reinforce premium product demand within the wound care management devices market.

By End User: Home Healthcare Transformation Accelerates

Hospitals and specialty wound clinics remained the largest buyers with 49.22% share in 2025, yet home healthcare agencies showed the fastest 5.81% CAGR trajectory as payers push care outside inpatient walls. Portable NPWT and smart bandages validated for layperson application underpin this migration. Long-term care facilities keep a constant need for pressure-ulcer prevention pads and repositioning aids, sustaining steady device turnover.

Nurse practitioners now spearhead mobile wound rounds, employing tablet-linked imaging apps that quantify surface area and exudate color in real time. Telehealth portals schedule asynchronous reviews by plastic surgeons, expanding specialist reach into rural homes. These models widen the addressable patient pool, ensuring the wound care management devices market captures value across settings. Vendors that bundle hardware with software dashboards can negotiate multi-year service contracts, smoothing revenue.

By Mode of Purchase: Retail Channel Expansion Reflects Consumer Empowerment

Institutional purchasing—hospital, clinic, and government tenders—controlled 58.84% of 2025 global turnover. Nonetheless, retail and over-the-counter channels will post a 5.86% CAGR to 2031 as sophisticated foams, hydrogels, and silicone dressings move onto pharmacy shelves. Online marketplaces further democratize access, giving caregivers in remote areas a broader catalog than local distributors stock.

Consumer-friendly packaging now includes step-by-step QR-code videos, addressing self-application anxiety. Pharmacies host wound-care kiosks staffed by certified nurses on weekends, bridging advice gaps for minor injuries. Tele-consult platforms partner with e-commerce sites so that a virtual visit seamlessly triggers same-day shipment of prescribed dressings. As a result, the wound care management devices market builds omnichannel resilience that reduces reliance on hospital budget cycles.

Geography Analysis

North America leads the wound care management devices market, generating 39.86% of the market revenue in 2025. As sophisticated insurance models fund high-end dressings, NPWT, and bioengineered tissues. In the United States, bundled payments under value-based contracts reward quicker closure and fewer complications, encouraging hospitals to trial next-generation hydrogels and sensor-enabled foams. The Food and Drug Administration exempts low-risk liquid bandages from 510(k) clearance, shortening launch times for consumer-oriented products. Canada’s single-payer system invests in home-care NPWT pilots that cut outpatient clinic load by 18% in 2025. Mexico continues upgrading surgical facilities, opening bids for mid-priced closure strips and polyurethane films.

Europe remains a mature yet innovation-receptive arena. National health systems fund chronic wound bundles that cover sensor-enabled dressings when evidence shows shorter healing cycles. Germany’s hospitals adopt AI-guided imaging to comply with new pressure-injury reporting mandates, stimulating device replacement. The United Kingdom rolls out community nurse–led diabetic foot programs supported by portable imaging tablets. Meanwhile, Southern Europe pursues cost-effective hydrogels that still meet EU Medical Device Regulation (MDR) documentation, creating niches for mid-range suppliers.

Asia-Pacific registers the fastest momentum for the wound care management devices market, registering a CAGR of 6.03% through 2031, fueled by healthcare infrastructure expansion and growing elective surgery capacity. China’s centralized bulk-procurement schemes now include NPWT pumps, driving local manufacture of canisters and foam dressings to meet price caps. Japan prioritizes aging-in-place policies that reimburse home-care dressings and sensor patches, fostering innovation in ultra-thin silicone adhesives suited to fragile skin. India’s state insurance programs begin covering advanced dressings for diabetic foot ulcers in tertiary centers, catalyzing distributor networks that penetrate tier-2 cities. Throughout Southeast Asia, private hospitals differentiate through specialty wound clinics equipped with tele-dermatology portals, widening regional market reach.

Regulatory Landscape

Regulatory requirements remain uneven across low-risk wound products and more complex devices that combine materials, software, and active therapy. In the United States, the FDA keeps risk-based device oversight, and in February 2026 the agency transitioned away from the Quality System Inspection Technique (QSIT), changing how manufacturers prepare for inspections across wound dressings, NPWT systems, and monitoring accessories.

In Europe, compliance under Regulation (EU) 2017/745 (EU MDR) continues to shape technical documentation, UDI, and post-market vigilance for wound care portfolios. In March 2026, the European Commission adopted two delegated regulations (C(2026) 1798 and C(2026) 1809) that expand the list of Well-Established Technologies (WET), easing certain MDR evidence and documentation burdens for additional device categories relevant to wound and surgical care. EUDAMED module requirements also became operational for specific reporting workflows in 2026, reinforcing the need for data-ready quality and vigilance systems. Separately, proposed Section 301 tariff actions published by the U.S. Trade Representative in June 2026 introduced cost and sourcing considerations for globally integrated supply chains that depend on EU, UK, and Swiss manufacturing footprints.

Competitive Landscape

The wound care management devices market sits in a moderately consolidated state where the top five players control a large amount of of global revenue. Multinationals leverage broad catalogs—from basic gauze to AI-enabled dressings—and possess the scale to negotiate favorable distributor terms. Start-ups focus on single-use NPWT, bioactive foams, or sensor patches, often licensing technology to majors post-proof-of-concept. Competitive intensity rose in 2025 when several AI imaging firms partnered with established dressing makers to embed depth cameras into contact layers.

Strategic mergers enhance vertical integration. Berry Global’s tie-up with Glatfelter forms a USD 3.6 billion specialty materials supplier that secures advanced spun-lace substrates for antimicrobial foams. Similar alliances give incumbents proprietary access to breathable films and hydrocolloid adhesives, defending margin. Meanwhile, Smith+Nephew’s USD 75 million U.S. Department of Defense contract for NPWT devices signals that government tenders can swing share quickly.

Regulatory agility grows more decisive. Firms that secure Breakthrough Device Designation for smart bandages gain payer attention and clinician trial budgets ahead of slower rivals. Intellectual-property moats now blend materials science patents with machine-learning algorithms, complicating traditional freedom-to-operate assessments. To protect share in the wound care management devices market, established brands increasingly invest in post-market surveillance platforms that feed real-world performance data back into product iteration loops.

Wound Care Management Devices Industry Leaders

-

Medtronic PLC

-

Smith & Nephew

-

ConvaTec Group PLC

-

Coloplast

-

Solventum

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White-space is emerging for dressings that reduce nursing workload while supporting pressure injury prevention and chronic-wound pathways, especially as hospitals move protocols into home-healthcare workflows. A concrete example is Smith+Nephew's March 2026 launch of ALLEVYN COMPLETE CARE Foam Dressing in the United States, positioned around high-performance wound management and prevention, with a stated plan for broader rollout beyond the initial market. This type of platform refresh can create room for suppliers offering standardized product families that cover prevention through treatment, which in turn can support procurement teams as they rationalize formularies across hospitals, specialty wound clinics, long-term care facilities, and home-healthcare settings.

The technology roadmap is shifting from passive coverage toward multi-modal, data-informed therapy, supported by both research activity and regulatory clarification. In July 2026, the FDA published draft guidance for chronic wound product development covering clinical trial design, endpoints, and the use of real-world evidence, which helps developers structure evidence packages for advanced dressings, NPWT adjuncts, and monitoring-enabled solutions. In parallel, academic work reported in 2026 on flexible bioelectronic dressings that combine electrical stimulation with controlled delivery points points to opportunities for next-generation devices that integrate sensing, therapy, and remote monitoring into single-use or simplified systems aligned with home-care adoption and outcome-based purchasing.

Recent Industry Developments

- July 2026: The FDA published draft guidance for developing products intended for chronic wound treatment, addressing clinical trial design, endpoints, and the role of real-world evidence. The update tightens how developers frame evidence for advanced dressings, device-enabled therapies, and monitoring-supported care pathways, and it supports more consistent payer and provider review of clinical claims.

- April 2026: The European Commission expanded the Well-Established Technologies list under the MDR to include additional wound care device categories. This regulatory move reduces evidence and documentation burdens for the expanded set of products and aligns with data-vigilance requirements across member states.

- May 2025: Smith+Nephew was awarded a USD 75 million U.S. Department of Defense contract to supply advanced wound therapy systems. The award underscores the influence of large government tenders on NPWT and advanced wound therapy placement, and reinforces the importance of service capability and supply reliability for institutional procurement.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from wound care management devices used to support wound closure, protection, and healing in acute and chronic wounds across care settings. It includes device-led therapies and related consumables sold through institutional and retail channels, across all major regions.

Scope exclusions: We exclude over-the-counter antiseptics, basic first-aid gauze, and pharmaceutical biologics that are not sold as wound care devices.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Topical Agents

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand context and the care-setting mix using public health and system indicators, then mapping it to device usage patterns. For baseline burden and spending context, we typically refer to the World Health Organization for burden trends, the World Bank for health spending context, CDC publications for wound-related risk factors, and OECD health statistics for hospital and long-term care utilization.

To translate the clinical picture into an addressable device market, we review regulatory and standards signals (for example, FDA device databases and selected ISO-related guidance notes). We then check pricing and adoption signals from manufacturer filings, investor presentations, and pages from medical associations. For trade-flow and supply-side sanity checks, we use shipment-level import-export data alongside company financials and an intelligence subscription, mainly to confirm regional availability and category scale. The sources mentioned above are illustrative and not exhaustive, and additional references are used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to test the practical market boundaries and to confirm how devices are bought and used across hospitals, clinics, and home care settings. We speak with manufacturers, distributors, clinicians, and procurement voices across APAC, EMEA, and the Americas, so the therapy mix, channel pricing logic, and adoption timing assumptions can be corrected before the model is finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 16% | APAC: 37% |

| Mid tier: 41% | Functional/Unit leaders: 37% | EMEA: 36% |

| Smaller Players: 21% | Managers: 47% | Americas: 27% |

Market-Sizing & Forecasting

Sizing is built using a top-down and bottom-up mix, where treated wound pools and care-setting activity are reconstructed first, then translated into device demand through penetration and therapy-mix assumptions. To keep the unit logic consistent, we tie each major device group to a realistic usage rate per patient episode and an average selling price range that is checked in interviews.

The model uses a small set of market fingerprints tracked year over year. These include diabetes prevalence signals that influence chronic wounds, hospitalization and surgery volumes that drive acute wounds, adoption of negative-pressure wound therapy in inpatient and outpatient settings, home care shift indicators, and price changes linked to reimbursement and tender behavior in larger markets. Where data gaps exist for smaller countries, we bridge them using proxy markets with a similar care-setting mix and income levels, then re-check the output against import patterns and interview feedback.

For forecasting, we apply scenario analysis so the outlook reflects how quickly therapy adoption and care migration can change under different reimbursement and staffing conditions. The final curve is adjusted using expert consensus on device penetration changes and expected pricing progression in key regions, and assumptions are documented so they can be repeated and updated.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals, including regional procedure activity, health spending direction, and category-level growth statements from public disclosures. We then compare those signals with what primary respondents report happening in channels. If the model indicates unusual jumps, we trace the drivers back to the relevant assumption level and re-test outlier inputs before sign-off.

Before publication, the analysis goes through multi-step internal review to catch calculation errors and scope mismatches early. Reports are refreshed annually, and interim updates are made when a material event can change adoption or pricing patterns. Right before delivery, an analyst performs a fresh pass so clients receive the most current view available.

Mordor Intelligence's Global Wound Care Management Devices Market Market Estimate Compared With Other Published Estimates

It is common to see different market values for wound care management devices because publishers do not always count the same product basket. They may also anchor demand to different care settings and pricing assumptions, including how they treat device versus consumable contributions in each year.

The year used as the starting point and the way currency conversion is handled can also widen the spread, even when the growth story looks similar. A major driver in this category is whether the estimate folds in non-device items like OTC antiseptics and basic first-aid gauze, and whether biologic therapies are treated as part of the same spend pool or kept separate. Another difference comes from how therapy devices and related consumables are counted, where some models apply faster penetration changes for negative-pressure therapies or assume a flatter global pricing curve. The spread is best explained by keeping the excluded non-device items out of the device total, as done by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.54 B (2025) | |

| Global Consultancy A | USD 22.37 B (2025) | The higher value is consistent with a broader product basket that blends therapy devices with a wider set of wound care items, with less explicit separation of OTC and basic first-aid categories from device revenue. |

| Industry Research Group B | USD 23.25 B (2025) | The estimate likely reflects a more expansive scope and quicker assumed uptake of therapy devices across settings, with regional pricing and channel mix treated more uniformly than what interview checks typically support. |

Across the three published figures, the spread mainly comes from what gets counted as a device market and how quickly therapy mix and pricing are allowed to change by region. By keeping the inputs tied to clear demand indicators and by separating out adjacent non-device spending, we arrive at a transparent total that can be repeated when new utilization or pricing signals emerge.

Key Questions Answered in the Report

What is the current value of the wound care management devices market?

The market is valued at USD 20.55 billion in 2026 and is projected to reach USD 26.42 billion by 2031.

Which product category generates the highest revenue?

Advanced wound care dressings and related systems hold 61.88% of 2025 revenue, making them the dominant product group.

Why is home healthcare growing faster than hospital purchasing?

Portable NPWT devices and smart dressings enable safe self-management, and payers reward lower inpatient costs, driving a 5.81% CAGR for home-based care through 2031.

How are AI technologies impacting wound care?

AI-enabled imaging platforms provide objective wound measurements, guide debridement, and trigger automated dressing adjustments, improving healing outcomes and reducing follow-up visits.

What restrains adoption in emerging markets?

Limited reimbursement and high device costs slow uptake, although public-private partnerships and locally manufactured consumables aim to close the affordability gap.

Which regions will see the fastest market growth?

Asia-Pacific is the fastest-growing region thanks to expanding surgical capacity, healthcare infrastructure investment, and widening access to advanced dressings.

Page last updated on: