Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

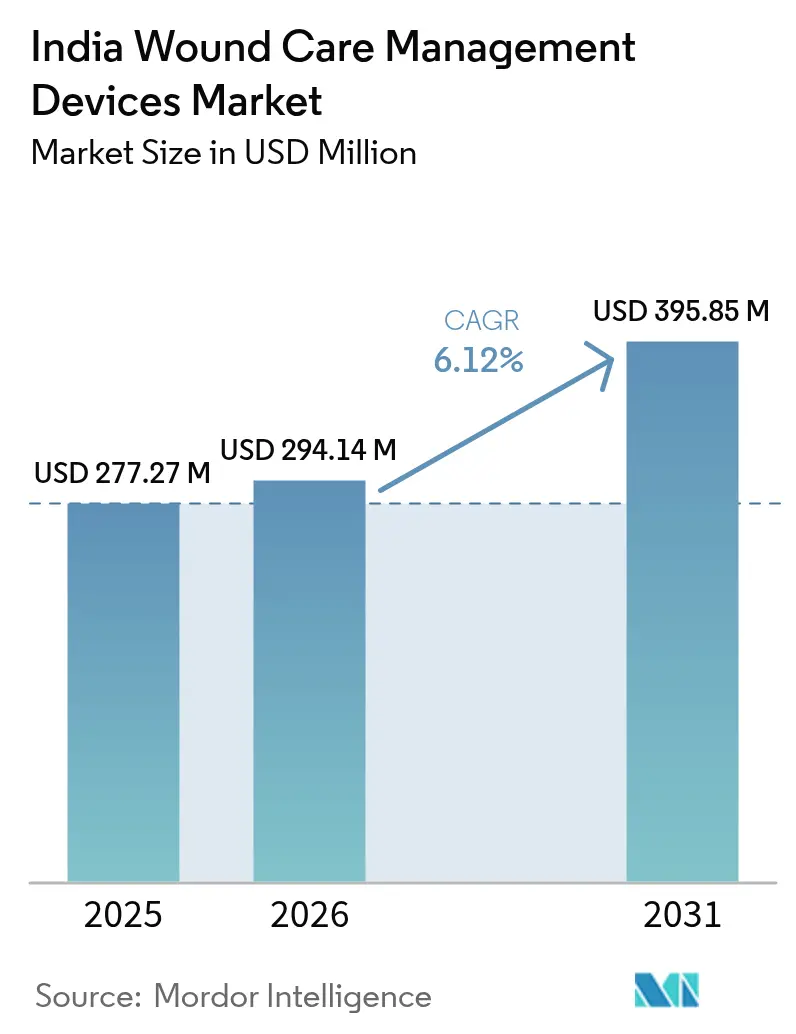

| Base Year Market Size (2025) | USD 277.27 Million |

| Market Size (2026) | USD 294.14 Million |

| Market Size (2031) | USD 395.85 Million |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Wound Care Management Devices Market Analysis by Mordor Intelligence

The India Wound Care Management Devices Market size is projected to be USD 277.27 million in 2025, USD 294.14 million in 2026, and reach USD 395.85 million by 2031, growing at a CAGR of 6.12% from 2026 to 2031.

India’s escalating prevalence of diabetes, rising surgical volumes, and the spread of home healthcare services are reshaping product demand and distribution. As the diabetes burden climbs, hospitals report higher diabetic foot ulcer caseloads, while sports-medicine clinics boost demand for convenient adhesive bandages. Multinational and domestic manufacturers are racing to localize production to pre-empt possible price controls and to qualify for indirect incentives under the Production Linked Incentive scheme. Government procurement portals are already tendering portable NPWT units and dermal substitutes, confirming that public facilities are gradually moving beyond gauze toward advanced modalities.

Key Report Takeaways

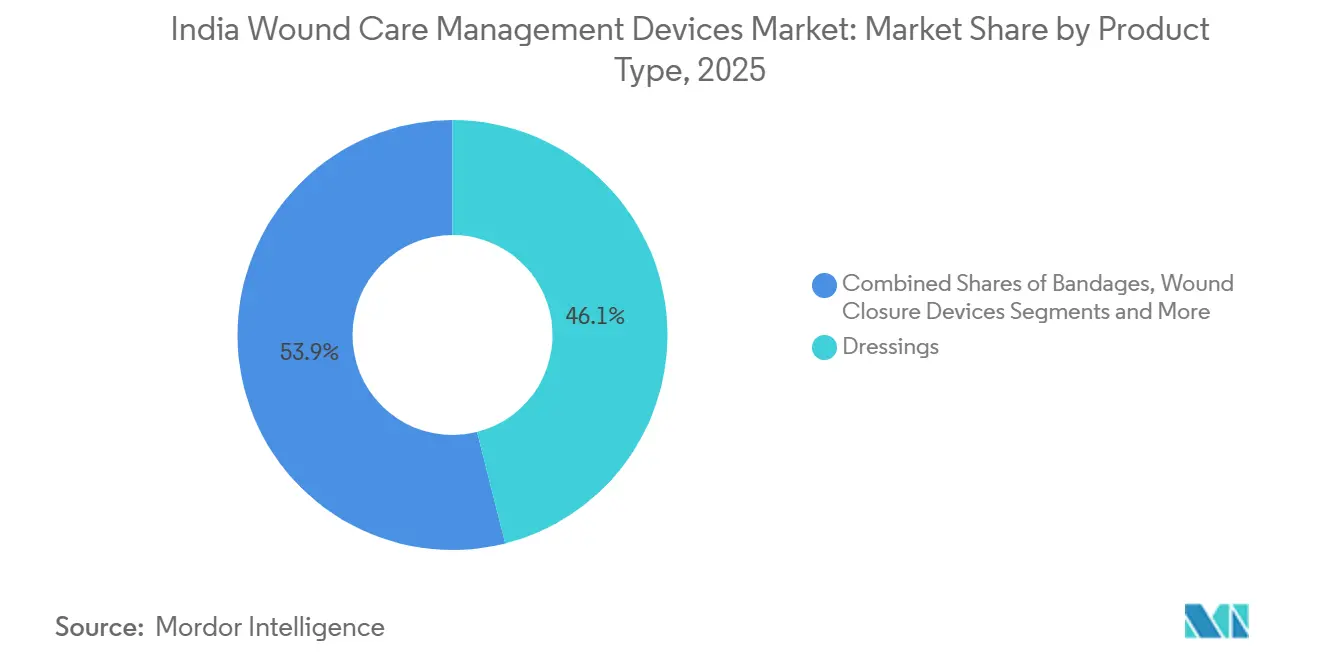

- By product type, dressings led with 46.06% of the India wound care management devices market share in 2025, while bandages are forecast to post the fastest 9.22% CAGR through 2031.

- By wound type, chronic wounds accounted for 64.55% of the India wound care management devices market size in 2025 and are expected to grow at an 8.56% CAGR to 2031.

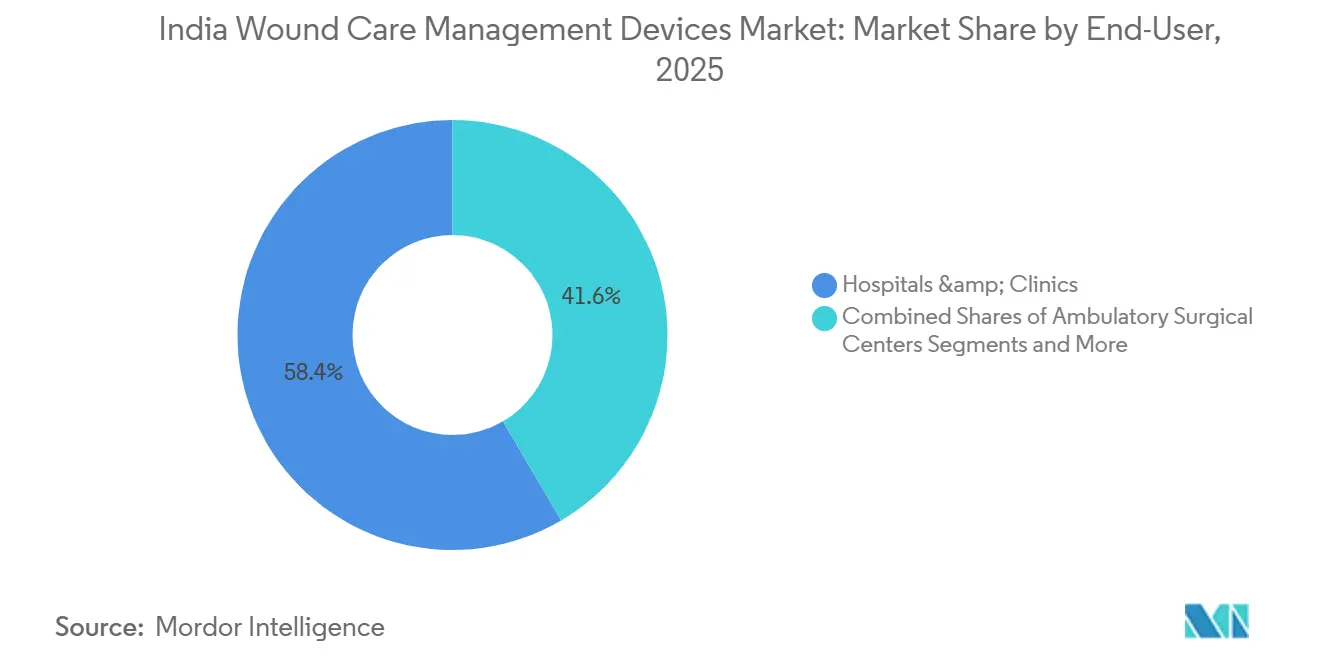

- By end user, hospitals & clinics accounted for 58.44% of revenue share in 2025, whereas home healthcare is set to expand at an 8.93% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising diabetes-linked diabetic foot ulcer burden | +1.2% | National, especially metros and tier-1 cities | Long term (≥ 4 years) |

| Increasing surgical volumes across India | +0.9% | National, fastest in tier-2 and tier-3 cities | Medium term (2-4 years) |

| Product & Technology Innovation in Dressings & NPWT | +0.8% | National, led by metro R&D hubs | Medium term (2-4 years) |

| Indigenous low-cost NPWT & smart dressings adoption | +0.7% | National, early uptake in government hospitals | Short term (≤ 2 years) |

| Government PLI scheme for local device manufacturing | +0.5% | Manufacturing clusters in Haryana, Uttarakhand, and Rajasthan | Long term (≥ 4 years) |

| Growing sports & fitness injuries | +0.4% | Urban fitness hubs and metros | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes-Linked Diabetic Foot Ulcer Burden

India hosts more than 101 million people with diabetes and 136 million with pre-diabetes, translating into 6.2% diabetic foot ulcer prevalence. Lower-limb amputations exceed 100,000 annually, creating sustained demand for advanced dressings, offloading devices, and NPWT.[1]National Center for Biotechnology Information, “Diabetic Foot Ulcer: A Comprehensive Review of Pathophysiology and Management Modalities,” ncbi.nlm.nih.gov Indigenous offloading alternatives, such as the Bohler and Mandakini designs, match total-contact casting outcomes yet remain confined to a few tertiary centers. Manufacturers must balance affordability with efficacy, which favors modular kits over single-use matrices.

Increasing Surgical Volumes Across India

At 1,385 surgeries per 100,000 population in 2025, India still trails the WHO benchmark, leaving headroom for hospital expansion. Surgical-site infection rates of 9% in community facilities versus 2-3% in accredited centers are driving adoption of antimicrobial dressings and NPWT to reduce dehiscence.[2]National Center for Biotechnology Information, “Diabetic Foot Ulcer: A Comprehensive Review of Pathophysiology and Management Modalities,” ncbi.nlm.nih.gov March 2024 tenders for portable canistered NPWT and hemoglobin spray show public institutions are gearing up for advanced wound closure. Price-cutting moves such as Covidien’s 60% suture discount illustrate how volume-led strategies work in price-sensitive settings.

Product & Technology Innovation in Dressings & NPWT

Indian research hubs have prototyped self-powered silver-nanoparticle dressings that generate microcurrents to accelerate epithelialization and pH-responsive hydrogels that change color upon infection, enabling visual monitoring without lab tests. Though still in validation, these innovations signal a shift from passive barriers to sensor-enabled platforms that transmit wound metrics to clinician dashboards.

Indigenous Low-Cost NPWT & Smart Dressings Adoption

Hospitals, recognizing the value, are willing to pay a 2× premium for a frugal NPWT protocol priced at INR 1,200 (approximately USD 14) per cycle. This cost delivers granulation results comparable to commercial devices priced between INR 7,000 and 15,000 (approximately USD 84-181) per week. The shorter hospital stays further justify the expense, effectively offsetting rental fees. Vendors such as Datt Mediproducts and Triage Meditech supply local NPWT kits, but Ayushman Bharat’s packages do not yet reimburse rental, forcing providers to bill patients directly.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited awareness of advanced wound care in primary care | -0.6% | Rural areas and tier-3 cities | Medium term (2-4 years) |

| High treatment cost of advanced products | -0.5% | Low-income and rural populations | Long term (≥ 4 years) |

| Reimbursement gaps under Ayushman Bharat | -0.4% | National, state variations in coverage | Medium term (2-4 years) |

| NPPA price-control risk for imported devices | -0.3% | National, import-heavy categories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Awareness of Advanced Wound Care in Primary Care

Primary-health centers still rely on gauze and povidone-iodine, and many clinicians lack training in NPWT or hydrocolloids. National Health Mission curricula omit wound-care competencies, prolonging referrals and escalating complications. Stock-outs and cold-chain gaps further limit advanced product use outside metros. Rural areas face additional barriers: supply-chain fragility means advanced dressings frequently stock out, and cold-chain requirements for biological matrices remain unmet in facilities without reliable refrigeration.

High Treatment Cost of Advanced Products

Out-of-pocket spending remains 62.6% of health expenditure. A weekly NPWT rental can equal a month’s income in tier-3 cities, making uptake highly price-elastic. Hospitals restrict advanced modalities to severe cases where clinical need justifies expenditure, suppressing volumes and keeping unit prices high. Hospitals face margin pressure when advanced products are not reimbursed under insurance schemes, leading to selective use only when clinical necessity overrides cost considerations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bandages Accelerate on Sports-Injury Demand

Dressings captured 46.06% of 2025 revenue, while bandages are on track for a 9.22% CAGR thanks to sports-medicine protocols favoring adhesive formats over gauze. Hospitals standardize dressings for diabetic ulcers, anchoring volumes, and bandage makers exploit dual distribution through institutional tenders and retail pharmacies. The India wound care management devices market for dressings will continue to outpace other categories, while bandages are carving a premium niche by positioning around rapid return-to-activity outcomes. Sensor-enabled dressings entering validation could bifurcate the category into commodity and smart-platform segments, reshaping pricing tiers.

The suture-dominated wound-closure device cluster benefits from locked-in hospital formulary contracts led by Ethicon and Covidien. NPWT, hemostats, and biological matrices remain niche as cost and reimbursement uncertainties limit scale. Once Ayushman Bharat broadens coverage, these high-margin segments are poised for catch-up growth within the India wound care management devices market.

By Wound Type: Chronic Cases Drive Value Amid Diabetes Surge

Chronic wounds held 64.55% of the 2025 value and will grow 8.56% annually as diabetic and pressure ulcers multiply with India’s aging cohort. Pressure ulcer incidence is rising in intensive care units where nurse-to-patient ratios remain stretched. Manufacturers focus on registry data to demonstrate how advanced dressings reduce hospitalization days, building the evidence base for wider reimbursement. The India wound care management devices market share for chronic wounds will therefore remain dominant through 2031.

Acute wounds trail in share but benefit from rising surgical throughput. Standardized closure protocols guarantee baseline demand for sutures and antimicrobial dressings. Burns are treated in specialized centers where premium dermal matrices justify higher prices, while trauma-related lacerations flow through emergency departments and sports clinics that prefer convenience-oriented sprays and adhesive strips.

By End-User: Home Healthcare Expands Fastest Under Cost-Containment Push

Hospitals & clinics accounted for 58.44% of 2025 sales, serving as gatekeepers for complex modalities that require sterile settings and trained nurses. They dominate the consumption of NPWT and biological matrices. Ambulatory surgical centers, while still nascent, are adopting single-use closure kits to maximize procedure turnover. Long-term care facilities remain underpenetrated, limiting revenue from pressure ulcer devices.

Home healthcare will log an 8.93% CAGR through 2031, reflecting payer efforts to shift post-acute care out of hospitals to cut occupancy costs. Diabetic foot ulcer patients often continue six-week dressing regimens at home, creating demand for caregiver-friendly hydrocolloids and smartphone-enabled wound monitoring. Manufacturers aligning product design with simplified application and retail supply chains stand to capture incremental share of the India wound care management devices market.

Geography Analysis

Metro cities Delhi, Mumbai, Bengaluru, Chennai, Kolkata, and Hyderabad accounted for the bulk of advanced product consumption in 2025 because tertiary hospitals, corporate chains, and insurance-empaneled centers cluster there. These institutions routinely stock NPWT kits, dermal substitutes, and antimicrobial dressings as part of standard formularies. Tier-1 cities such as Pune, Ahmedabad, Jaipur, and Lucknow are closing in as private hospital groups replicate metro treatment protocols, adding 150- to 300-bed facilities that quickly adopt surgical closure devices and advanced dressings.

Tier-2 and tier-3 cities lag by about 40% in advanced-product penetration, relying mainly on gauze and adhesive bandages supplied through government tenders. Polymed’s INR 750 crore investment in manufacturing plants at Faridabad, Haridwar, and Jaipur aims to shorten supply lines to these emerging demand centers and to reduce landed costs that deter adoption.

Regional epidemiology shapes product mix. Southern states exhibit higher diabetic foot ulcer prevalence, driving disproportionate consumption of chronic wound dressings and offloading devices. Northern states with younger populations lean toward trauma and surgical products. Western states, home to Gujarat’s and Maharashtra’s device clusters, speed local innovation adoption thanks to proximity and established supply chains. Eastern states trail because of limited tertiary infrastructure and lower insurance penetration, but expanding primary-care networks present volume potential for low-cost indigenous alternatives.

The strategic opportunity lies in tier-2 and tier-3 urban corridors where hospital capacity is expanding, middle-class insurance coverage is growing, and distributors seek differentiated portfolios. Manufacturers that invest early in clinician education and service networks stand to secure sustainable positions as these geographies climb the technology ladder.

Competitive Landscape

The India wound care management devices market is moderately fragmented. 3M leads in transparent films and medical tapes; Ethicon tops sutures and staplers; and Smith & Nephew and Coloplast dominate select advanced dressings. Yet no single company controls more than one-quarter of total revenue. Multinationals lean on global clinical evidence and long-standing formulary relationships with tertiary hospitals. Domestic firms compete on price, localized service, and faster customization, as seen in Covidien’s 60% surge in suture sales after strategic discounting.

Players are targeting three white-space arenas. First, portable NPWT systems engineered for home-care use that bypass hospital rental models. Second, sensor-integrated hydrocolloids and foams that transmit temperature, pH, or moisture data to telehealth dashboards, enabling remote intervention. Third, low-cost offloading devices priced at one-tenth of imported casts yet delivering equivalent healing, crucial for diabetic ulcers prevalent in resource-constrained settings.

Technology pipelines center on chitosan hemostats, silk-protein biomaterials, and pH-responsive hydrogels that visually flag infection. Indian start-ups registered under the Tracxn database are progressing clinical trials to secure CDSCO and the United States FDA clearances. To hedge against potential NPPA price ceilings, multinationals and local firms alike are stepping up localization of assembly and component sourcing. However, aligning the quality system with global standards adds 12-18 months to launch timelines.

India Wound Care Management Devices Industry Leaders

3M Company

Medtronic PLC

Smith & Nephew

Coloplast A/S

B Braun SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SCTIMST unveiled CholeDerm, an acellular dermal dressing derived from farm-animal gall bladders, and licensed it to Alicorn Medical for commercialization.

- November 2025: Colonox launched as India’s first nitric-oxide wound dressing targeted at diabetic foot-ulcer healing acceleration.

- July 2025: A national manual was published to standardize advanced wound-care protocols across hospitals, clinics, and home-health providers.

India Wound Care Management Devices Market Report Scope

As per the report's scope, wound management products are mainly used to treat complex wounds. Wounds and injuries are common afflictions that affect billions of people worldwide. The products are highly resistant to environmental inhibitors and foreign particles and are used by a nurse under the physician's orders and supervision for various reasons. Rising risk factors and the need for cost-efficient treatments drive demand for better wound care products.

The Indian wound care management market is segmented by product type and wound type. By product type, the market is segmented into dressing, bandages, wound closure devices, and other wound care products. By end user, the market is segmented into hospitals & clinics, ambulatory surgical centers, home healthcare, and others. By wound type, the market is segmented into chronic wounds and acute wounds. The report offers the value (USD) for all the above segments.

By Product Type

| Dressings |

| Bandages |

| Wound Closure Devices |

| Other Wound Care Products |

By Wound Type

| Chronic Wounds | Diabetic Foot Ulcer |

| Pressure Ulcer | |

| Other Chronic Wounds | |

| Acute Wounds | Surgical Wounds |

| Burns | |

| Other Acute Wounds |

By End User

| Hospitals & Clinics |

| Ambulatory Surgical Centers |

| Home Healthcare |

| Others |

| By Product Type | Dressings | |

| Bandages | ||

| Wound Closure Devices | ||

| Other Wound Care Products | ||

| By Wound Type | Chronic Wounds | Diabetic Foot Ulcer |

| Pressure Ulcer | ||

| Other Chronic Wounds | ||

| Acute Wounds | Surgical Wounds | |

| Burns | ||

| Other Acute Wounds | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgical Centers | ||

| Home Healthcare | ||

| Others | ||

Key Questions Answered in the Report

How big is the India Wound Care Management Device Market?

The India Wound Care Management Device Market size is expected to reach USD 277.27 million in 2025 and grow at a CAGR of 6.12% to reach USD 395.85 million by 2031.

What is the current India Wound Care Management Device Market size?

In 2026, the India Wound Care Management Device Market size is expected to reach USD 294.14 million.

Who are the key players in India Wound Care Management Device Market?

3M Company, Medtronic PLC, Smith & Nephew, Coloplast A/S and B Braun SE are the major companies operating in the India Wound Care Management Device Market.

Which product segment hold the major market share?

Dressings lead with 46.06% market share in 2025.

Page last updated on: