Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

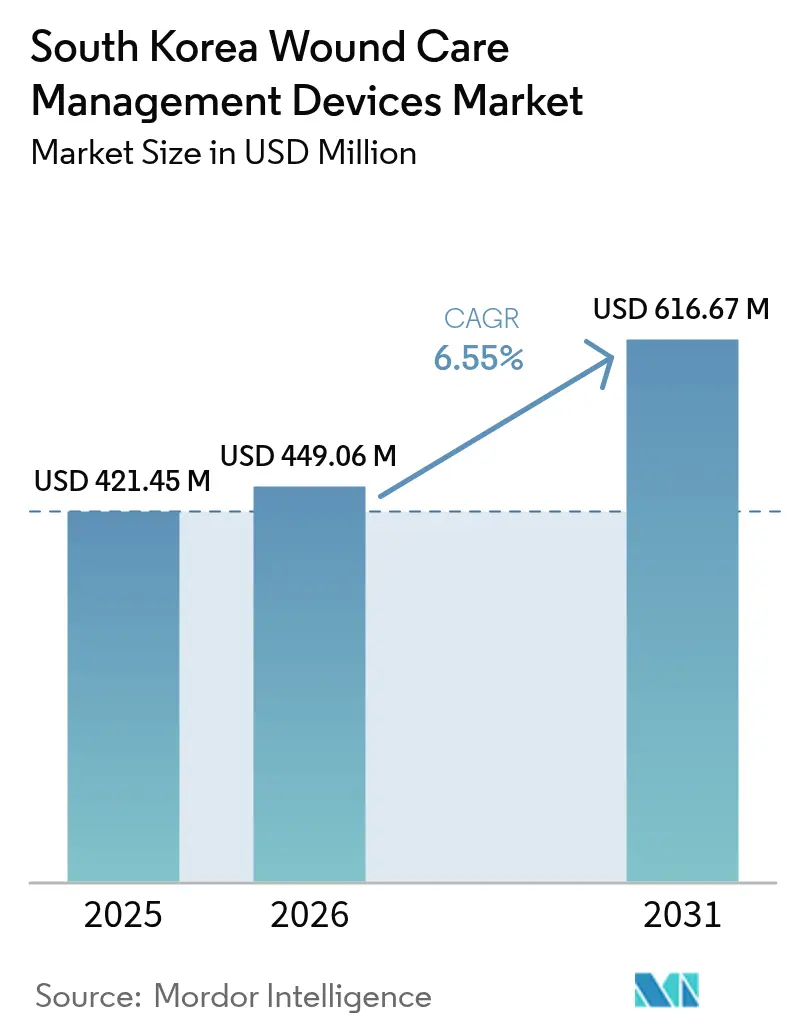

| Base Year Market Size (2025) | USD 421.45 Million |

| Market Size (2026) | USD 449.06 Million |

| Market Size (2031) | USD 616.67 Million |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Wound Care Management Devices Market Analysis by Mordor Intelligence

The South Korea wound care management devices market size was valued at USD 421.45 million in 2025 and estimated to grow from USD 449.06 million in 2026 to reach USD 616.67 million by 2031, at a CAGR of 6.55% during the forecast period (2026-2031). A super-aged demographic profile, rising lean-diabetes incidence, and supportive government R&D funding are converging to keep demand for advanced dressings, negative-pressure wound therapy (NPWT) systems, and smart monitoring tools strong. The Ministry of Science and ICT’s record KRW 24.8 trillion 2025 budget and the Korean ARPA-H program [1]Ministry of Health and Welfare, "Korean ARPA-H Project, an innovative R&D project that challenges solving national problems, begins in earnest," mohw.go.kr are accelerating domestic device innovation. Hospitals remain the primary purchasers, yet telehealth-enabled home care is expanding rapidly, encouraged by the Digital Medical Products Act that took effect in 2025. Persistent reimbursement gaps for silver-impregnated dressings and other premium consumables temper market potential, but the overall outlook for the South Korea wound care management devices market remains positive through 2030 [2]Ji Min Kim, "Lean diabetes: 20-year trends in its prevalence and clinical features among Korean adults," BMC Public Health, bmcpublichealth.biomedcentral.com.

Key Report Takeaways

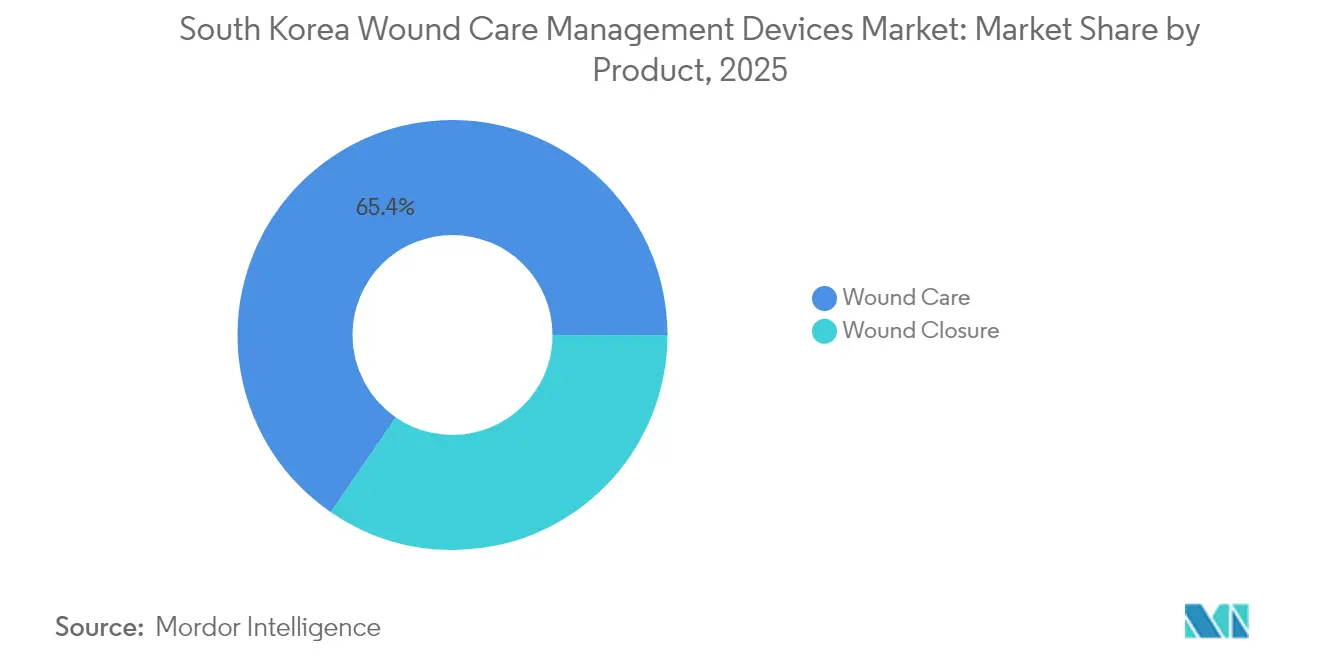

- By product category, Wound Care items led with 65.42% revenue share of the South Korea wound care management devices market in 2025.

- By product category, Wound Closure devices are forecast to expand at a 6.88% CAGR through 2031.

- By wound type, chronic wounds accounted for a 59.92% share of the South Korea wound care management devices market size in 2025, while acute wounds are set to grow at 6.84% annually.

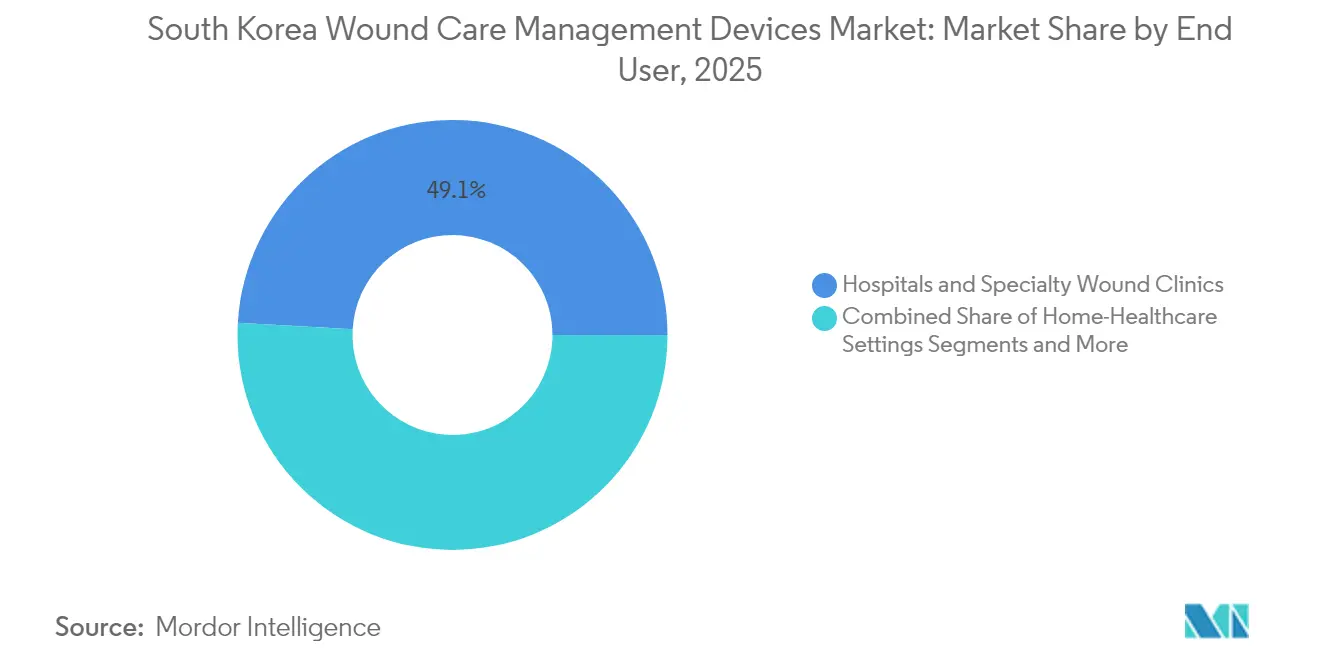

- By end user, hospitals and specialty wound clinics held 49.10% of South Korea wound care management devices market share in 2025; home healthcare settings record the highest projected 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in diabetes prevalence & ageing population | +1.5% | National, urban hubs | Long term (≥ 4 years) |

| Rising incidence of chronic wounds & surgical procedures | +1.2% | National, metro hospitals | Medium term (2-4 years) |

| Government incentives for domestic med-tech innovation | +0.8% | Seoul & Daejeon R&D hubs | Medium term (2-4 years) |

| Adoption of advanced wound care technologies including NPWT and bioactive dressings | +1.1% | Tertiary hospitals nationwide | Short term (≤ 2 years) |

| Telehealth-enabled home-based wound care | +0.7% | Rural communities | Medium term (2-4 years) |

| Integration of AI & IoMT smart dressings | +0.6% | Tech-advanced centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increase in Diabetes Prevalence & Ageing Population

Diabetes generated 25,439 disability-adjusted life years per 100,000 Koreans in 2020. Lean diabetes, defined by BMI < 23 kg/m², climbed from 6.6% to 8.8% between 2001 and 2021, a 33.3% surge that complicates wound healing because of low insulin reserves. Hypertension affects 28.0% of adults and frequently co-exists with diabetes, combining to slow tissue repair. Korea University Guro Hospital alone treated 180,872 wound cases during 2018-2022, underscoring the scale of clinical need. Catheter-related injuries already make up 45.3% of admitted wounds, illustrating how multiple comorbidities magnify complexity in the South Korea wound care management devices market [3]Yun-Sun Jung, "Measuring the Burden of Disease in Korea Using Disability-Adjusted Life Years (2008–2020)," JKMS, jkms.org.

Rising Incidence of Chronic Wounds & Surgical Procedures

An ageing population drives pressure-ulcer prevalence, adding direct medical costs and longer stays for geriatric patients. Simultaneously, medical tourism brought in 606,000 foreign patients in 2023, upping surgical case counts and postoperative wound volumes. Insurance rules still restrict silver dressings to major burns despite proven efficacy in chronic ulcers. Specialist dressing teams in tertiary centers keep complication rates low at 0.08% by standardizing care. Preventive protocols are therefore viewed as essential cost-containment levers across the South Korea wound care management devices market.

Government Incentives for Domestic Med-Tech Innovation

The 55 billion KRW ARPA-H program prioritizes multi-modal wound care technologies and decentralized delivery. In parallel, the Act on Nurturing the Medical Devices Industry has already cleared 85 AI-based devices, indicating regulator openness to novel tools. The National Health Insurance “Preliminary Benefit” pathway lets evidence-light innovations earn provisional payment while collecting outcomes data. These policies reduce time-to-market and create fertile ground for domestic SMEs, expanding the competitive field within the South Korea wound care management devices market.

Adoption of Advanced Wound Care Technologies Including NPWT and Bioactive Dressings

NPWT accelerates closure in pressure ulcers; a Korean randomized study showed mesh-assisted NPWT cut wound size faster than standard therapy. Korean surgeons have adapted low-cost wall suction NPWT to suit budget-sensitive facilities. Silver-coated dressings under vacuum significantly reduce bacterial counts, mitigating infection risk. University labs published nanoglass composites doped with cobalt that match clinical drugs in healing diabetic ulcers by stimulating angiogenesis. Such breakthroughs reinforce the premium placed on innovation in the South Korea wound care management devices market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure cost & reimbursement gaps | -1.8% | Rural communities | Short term (≤ 2 years) |

| Stringent MFDS regulatory pathway | -0.9% | Nationwide | Medium term (2-4 years) |

| Shortage of certified wound-care nurses | -0.6% | Rural & suburban | Medium term (2-4 years) |

| Raw-material supply chain vulnerabilities | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost & Reimbursement Gaps

National Health Insurance still reimburses silver dressings mainly for severe burns, not for chronic ulcers, restricting access to technologies that would otherwise lower infection rates. The fixed-rate payment model forces long-term care centers to absorb 7.3% of monthly tracheostomy spending solely on suction catheters. While a KRW 10 trillion reform package aims to raise undervalued medical-service fees, implementation remains uncertain. These cost barriers delay adoption of best-in-class dressings in the South Korea wound care management devices market.

Stringent MFDS Regulatory Pathway

Class III and IV devices need direct MFDS approval, extending timelines and adding compliance costs. The Digital Medical Products Act layers extra validation steps for AI wound analyzers, challenging small developers. Ongoing GMP audits and mandatory adverse-event reporting further stretch limited resources. Collectively, these hurdles can slow new-product flow into the South Korea wound care management devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound Care Dominance Drives Innovation

South Korea wound care management devices market size for Wound Care items stood at USD 276.71 million in 2025, equal to 65.42% of total revenue. Traditional gauze still sells well for routine cases, yet sales momentum clearly favors advanced lipidocolloid and bioactive dressings that slash healing time in pressure ulcers. NPWT compatibility and antimicrobial coatings are the fastest-moving value-adds because tertiary centers demand infection control. Domestic firms collaborate with university labs on herbal extract-infused hydrogels, merging Eastern remedies with Western clinical practice. Competitive moats center on intellectual property, hospital contracts, and educator outreach that trains nurses in protocol-driven dressing changes.

Wound Closure devices contribute a smaller share today but carry a 6.88% CAGR, the highest among all categories within the South Korea wound care management devices market. Korean engineers are embedding antibiotics and anti-inflammatory drugs into absorbable sutures to combat resistant organisms. Electronic sutures developed by DGIST provide real-time inflammation data, a technology that could re-define postoperative care workflows. Tissue adhesives benefit from nanoparticle-enhanced formulations delivering 7.15-fold stronger adhesion than cyanoacrylates. Surgical stapler demand rises in lockstep with inbound elective-surgery patients, underscoring why product pipelines increasingly target ergonomic, single-use staplers optimized for Korean operating rooms.

By Wound Type: Chronic Wounds Lead Amid Demographic Shifts

Chronic lesions command 59.92% of South Korea wound care management devices market share in 2025. Diabetic foot-ulcer incidence climbs in parallel with lean diabetes growth, a phenotype presenting lower insulin and diminished muscle mass that slows closure rates. Pressure-ulcer prevention programs now include nutrition counseling and early mobilization, yet facility data still show stubborn recurrence in bedbound elders. Venous leg-ulcer therapy blends compression with advanced hydrogels, tapping both Western evidence and Korean traditional insights for herbal anti-inflammatories. Home-visiting nurses use smartphone apps to document weekly progress, feeding clinical dashboards that alert physicians to infection signs early, an approach scaling rapidly across the South Korea wound care management devices market.

Acute wounds expand faster at a 6.84% CAGR through 2031. Surgical and traumatic wounds dominate volume thanks to higher orthopedic and cosmetic surgery counts among domestic and foreign patients. Korean burn units are experimenting with cobalt-doped nanoglass grafts that temper inflammation and spur angiogenesis, matching performance of growth-factor drugs without cold-chain constraints. Emergency centers integrate dermal templates and cell therapy to speed soft-tissue repair after accidents, shortening ICU stays. For dermatologic procedures popular with medical tourists, clinics increasingly hand out post-laser hydrogel patches bundled with smartphone after-care instructions, reflecting consumer-centric propositions in the South Korea wound care management devices market.

By End User: Hospitals Maintain Leadership While Home Care Surges

Hospitals and specialty clinics controlled 49.10% of the South Korea wound care management devices market size in 2025. Tertiary centers like Seoul National University Hospital rely on NPWT systems for large soft-tissue defects, and internal dressing teams keep protocol adherence high. On-device AI now classifies pressure-ulcer stage with 84.6% accuracy, aiding triage decisions. Reimbursement ceilings push administrators to standardize supply formularies and negotiate bulk discounts. Despite workforce strain, institutional demand drives volume for advanced consumables, particularly as hospitals adopt UDI-enabled inventory tracking to curb waste.

Home healthcare is the fastest riser at 7.12% CAGR. The 2026 Integrated Community Care mandate funds home medical centers and tele-nursing platforms that allow photo uploads for remote evaluation. Pilot tele-consultation projects under Long-Term Care Insurance delivered higher family satisfaction metrics versus in-person visits. Government hiring created 28,154 nursing roles dedicated to home care, easing the scarcity of certified wound specialists in rural districts. These programs embed digital-first workflows, accelerating technology uptake across the South Korea wound care management devices market.

By Mode of Purchase: Institutional Procurement Leads Digital Transformation

Institutional buyers accounted for 64.78% of all purchases in 2025, leveraging Group Purchasing Organization schemes that reward volume commitments. Hospitals increasingly request platform solutions that bundle dressings, NPWT units, and training. UDI mandates, coupled with e-tracking portals, boost demand for smart packaging that integrates RFID chips, expanding the technological bar required to compete in the South Korea wound care management devices market.

Retail and over-the-counter sales grow fastest at 7.28% CAGR. Korea’s digital-health market ballooned from USD 1.3 billion in 2021 to USD 4.8 billion in 2022, creating omni-channel routes for wound tapes, sprays, and sensor-embedded dressings. The Digital Medical Products Act legitimizes consumer-grade AI wound analyzers sold online, widening addressable households. Packaging now favors single-patient kits with video QR codes that guide application, increasing compliance and outcomes while fitting Korea’s tech-savvy aging population profile.

Geography Analysis

Seoul metropolitan area concentrates nearly half of Korea’s population and hosts the lion’s share of tertiary hospitals, anchoring the South Korea wound care management devices market. High bed density dovetails with an elderly urban demographic, swelling chronic-wound caseloads handled by advanced centers equipped with NPWT and AI-triage systems. Government reforms earmark part of the KRW 10 trillion 2028 health-enhancement package for capital-region facilities, reinforcing infrastructure dominance.

Regional disparities prompt targeted programs elsewhere. The Integrated Support for Community Care Act requires each province to build home medical centers by 2026, spurring demand for portable NPWT pumps and easy-use dressings in smaller cities. Tele-consultation pilots under Long-Term Care Insurance show particular impact in Gangwon and Jeolla provinces where specialist density is low; wound-photo upload systems demonstrated strong concordance with in-person assessment. Provincial governments now invest in 5G-enabled remote-monitoring platforms, scaling access across mountainous terrain.

Supply-chain hubs coalesce in the Seoul-Incheon economic corridor that handles most device imports and domestic manufacturing distribution. Enforcement of the Digital Medical Products Act applies uniformly nationwide, yet metropolitan tech clusters adapt quickest, giving local startups a head start in launching smart dressings. Diabetes hot-spots align with urban lifestyles; the 33.3% surge in lean diabetes since 2001 is most visible in Seoul’s dense districts. Collectively, geography shapes procurement priorities and product-mix decisions across the South Korea wound care management devices market.

Regulatory Landscape

South Korea regulates wound care management devices under the Ministry of Food and Drug Safety (MFDS). Its four-tier, risk-based classification (Class I to IV) sets the review intensity, with notification/certification routes for lower-risk products and direct MFDS approval for Class III and IV devices. The Digital Medical Products Act, effective January 24, 2025, creates a dedicated framework for software-driven and AI-enabled products, which raises documentation and validation expectations for digital wound assessment tools and connected monitoring used across hospital and home-care workflows.

MFDS tightened regulatory expectations through 2026. It updated medical device GMP requirements in February 2026 to reinforce lifecycle quality oversight, and on April 28, 2026, amended the Regulation on the Permission, Notification, and Review of Medical Devices (MFDS Notification No. 2026-34) to clarify procedures and reduce administrative friction. Separately, amendments to the Medical Devices Act (amended December 30, 2025) took effect on July 1, 2026, strengthening the legal basis for the Manufacturing and Quality Management System (QMS) Conformity Recognition Scheme, which affects manufacturers and importers supplying advanced dressings, NPWT systems, and wound closure devices.

Value Chain Analysis

The value chain begins with upstream materials and components, including nonwoven substrates, hydrocolloid and silicone adhesives, polymer films, superabsorbents, antimicrobials (including silver-based inputs), and electromechanical parts for NPWT pumps and canisters. Domestic manufacturers such as Genewel, T&L, and CGBIO operate at the conversion and assembly layer, while global suppliers complement local supply with imported branded advanced dressings and NPWT platforms that require Korea-specific labeling and documentation aligned with MFDS expectations.

Downstream, distribution is concentrated around the Seoul-Incheon corridor, where import logistics, warehousing, and regulatory-support services are clustered. Products then reach hospitals and specialty wound clinics through institutional procurement and GPO-style contracting, while home-care channels increasingly bundle tele-nursing support. Compliance activities (KGMP/QMS conformity, technical documentation, and post-market obligations) cut across the chain and influence lead times and supplier selection for both domestic and imported SKUs. Commercial activation also relies on industry platforms and exhibitions, illustrated by CGBIO reporting KRW 5.3 billion in contracts at KIMES 2026.

Competitive Landscape

Global multinationals—Johnson & Johnson, Smith & Nephew, Medtronic—retain strongholds via broad product lines, hospital rebates, and robust MFDS experience. Domestic challengers such as Daewoong Pharmaceutical and Genewel exploit faster iteration cycles and lower labor costs to release niche hydrogel and film dressings customized to Korean user preferences. Competition centers increasingly on data-driven solutions; DGIST’s electronic suture shows how academic-industry collaboration can leapfrog conventional closure products.

Digital convergence raises the bar: startups marry cloud analytics with sensor-equipped bandages, offering pay-per-use platforms attractive to overstretched home-care nurses. The Digital Medical Products Act sets clear digital-health rules, favoring firms that invest early in cybersecurity and real-world-evidence generation. Overseas technology vendors increasingly partner with local distributors for MFDS navigation and cultural alignment, creating joint ventures that bundle Western devices with Korean tele-nursing apps.

White-space opportunities persist in rural outreach where nurse shortages limit service coverage. Companies providing turnkey tele-consultation kiosks or AI triage apps gain a first-mover advantage. Hospital GPOs reward suppliers that deliver integrated portfolios spanning basic gauze to advanced NPWT, prompting ongoing consolidation in the South Korea wound care management devices market as mid-sized players seek scale to match procurement expectations.

South Korea Wound Care Management Devices Industry Leaders

-

Smith and Nephew

-

Coloplast A/S

-

Medtronic

-

Convatec

-

Smith & Nephew

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is emerging from faster pathways and evidence generation for innovative wound care technologies. In January 2026, MFDS introduced the Market Immediate Entry Medical Technology system, reducing the route to clinical use from as long as 490 days to about 80 to 140 days for designated categories. This creates room for suppliers that can package MFDS-ready technical files and provide hospital implementation support for advanced dressings, NPWT, and digitally assisted wound assessment. The Digital Medical Products Act (effective 2025) also formalizes digital requirements, encouraging competition around validated performance, cybersecurity, and real-world data collection across home-care and long-term care workflows.

Capital formation and domestic ecosystem building provide additional expansion channels across the wound care value chain. In May 2026, KHIDI initiated a bidding process for a research project to design a dedicated medical device investment fund aimed at de-risking early-stage startups and attracting private capital, in line with the broader government-backed R&D momentum referenced in the report context, including the 2025 record KRW 24.8 trillion budget and the Korean ARPA-H program. Manufacturers that can align February 2026 GMP updates with scalable production, while building reimbursement-ready clinical dossiers for premium consumables where coverage gaps persist, have a clearer path to broaden adoption across hospitals and the expanding telehealth-enabled home-care segment.

Recent Industry Developments

- May 2026: Medtronic signed an MOU with Asan Medical Center to collaborate on robotic surgery technology development, clinical research, and education around the Hugo RAS ecosystem. Higher robotic procedure volumes increase demand for reliable wound closure and postoperative wound management protocols, reinforcing the pull-through for stapling, sealing, and complication-mitigation solutions used in surgical pathways.

- October 2025: Smith+Nephew shared new scientific data supporting its ALLEVYN LIFE/ALLEVYN COMPLETE CARE foam dressing portfolio. The added clinical evidence strengthens hospital formulary positioning in a reimbursement-sensitive environment and supports conversion from basic dressings toward advanced foam solutions in chronic wound pathways.

- March 2024: KAIST introduced a wireless thermal-mapping patch designed to track diabetic-wound healing trajectories. The work underscores the technology direction toward sensor-based monitoring that can support telehealth-enabled wound management and earlier intervention outside tertiary centers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of wound care management devices sold and used in South Korea for preventing infection, supporting healing, and closing acute and chronic wounds in clinical and home-care settings.

Scope exclusions: Consumer first-aid kits and basic OTC wound packs sold mainly for self-care are excluded.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Data Sources, Market Sizing, and Validation

Desk Research

We start by mapping the care pathway and procurement flow for wound care products in South Korea, so the model follows how devices are bought and used across hospitals and home-care. Public sources are then used to anchor demand signals and care setting trends, such as Statistics Korea population tables, Korean Statistical Information Service health and hospital indicators, National Health Insurance Service publications on utilization, and Ministry of Food and Drug Safety notices on medical devices.

Next, we review manufacturer product catalogs, public regulatory listings, annual reports, and investor presentations to understand which device types are actively marketed and in what settings. We also review reputable clinical literature and society guidance (including wound care and diabetes care publications) to sense-check where utilization should be higher, especially for chronic wounds. Where needed, we use paid subscriptions for company financials and intelligence, patent databases, and news and financial filings to cross-check timelines and revenue signals. The sources listed here are illustrative, and many other public references were also used for collection, clarification, and validation.

Primary Interviews and Surveys

To close gaps that public data cannot answer well, we validate assumptions through interviews and structured surveys with stakeholders across hospitals, specialty wound clinics, distributors, and device-focused teams. Because the scope is South Korea only, conversations were kept centered on local pricing behavior, reimbursement realities, and shifts between inpatient, outpatient, and home-care usage, so our totals remain realistic for the categories included.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | |

| Mid tier: 60% | Functional/Unit leaders: 40% | |

| Smaller Players: 15% | Managers: 46% |

Market-Sizing & Forecasting

Sizing starts from the demand pool for wound treatment across care settings in South Korea, where prevalence and treated-case flows are used to reconstruct how many patients move through acute and chronic wound pathways. We translate those pathways into device demand using a combined top-down and bottom-up logic, where national utilization signals and care-setting splits set the frame, and then selective supplier and channel checks are used to keep the results grounded.

Key inputs include diabetes prevalence and the aging mix, inpatient and outpatient procedure volumes tied to wound closure, the share of chronic wounds treated in specialty clinics, the adoption rate of advanced dressings and negative pressure wound therapy in indicated cases, and typical replacement or consumption frequencies by setting. Pricing is modeled using observed list-price ranges and payer-relevant net price behavior discussed in interviews, with adjustments for product mix shifts rather than a single flat inflation factor.

For forecasting, we use scenario analysis that links demand growth to the pace of chronic disease burden, care shifting toward home treatment, and reimbursement-driven access to premium products. Where bottom-up rollups are incomplete, missing players are handled using share-of-channel assumptions and sanity checks against import and manufacturing signals before final totals are set.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals, such as procedure and hospital activity indicators, observed category adoption patterns, and pricing ranges from procurement discussions. When a segment moves beyond expected clinical use, we re-check the assumptions, revisit sources, and re-contact selected experts to confirm whether the variance is real or data-driven.

Before sign-off, the full model goes through multi-step internal reviews where math, unit logic, and year-to-year movements are checked, followed by a final consistency pass across segments and end users. Reports are refreshed annually, and material events, including reimbursement changes or major regulatory shifts, trigger interim updates so the latest market view is captured.

Mordor Intelligence's South Korea Wound Care Management Devices Market Size Compared Against Other Published Estimates

Published numbers for this market can look far apart because publishers do not always count the same product basket, and they often apply different price realization and care-setting assumptions. Differences also show up when some studies anchor on a broad retail wound-care spend, while others stay focused on physician-directed devices used in formal treatment.

OTC first-aid kits sit outside Mordor Intelligence's scope, which naturally lowers totals versus estimates that bundle retail bandages and topical products into the same headline number. Gaps also come from whether negative pressure wound therapy utilization is modeled from treated-case eligibility versus broad hospital equipment counts, and from how currency timing and net price discounts are applied to imported products.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.42 B (2025) | |

| Industry Publisher A | USD 0.15 B (2024) | Uses an earlier base year and a narrower device set, with limited visibility into premium device adoption in hospitals and specialty wound clinics, which can understate value. |

| Consultancy B | USD 1.38 B (2024) | Appears to cover the broader wound care market, folding in dressings, bandages, and topical agents beyond device-led management, which inflates totals versus device-only scope. |

The spread in the table is mainly explained by what gets counted as a device market versus a full wound care spend, followed by how utilization and net pricing are translated into revenue. By keeping inputs tied to treated-case demand, care-setting splits, and realistic price realization checks, the final estimate stays traceable to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the South Korea wound care management devices market?

The market stands at USD 449.06 million in 2026 and is projected to reach USD 616.67 million by 2031.

Which product segment commands the largest share?

Wound care products lead with 65.42% revenue share of the South Korea wound care management devices market in 2025.

Which end-user segment is growing the fastest?

Home healthcare settings show the highest momentum with a 7.12% CAGR expected through 2031.

How are government policies influencing market expansion?

A KRW 24.8 trillion 2025 R&D budget and the Digital Medical Products Act create funding and fast-track approval paths for AI-driven wound devices.

What are the biggest hurdles to wider adoption of advanced wound products?

High procedure costs, limited reimbursement for premium dressings, and stringent MFDS approval requirements slow uptake.

Which technology trends are reshaping competitive dynamics?

Negative-pressure wound therapy, AI-enabled smart dressings, and electronic sutures with real-time inflammation monitoring are redefining standards and driving innovation.

Page last updated on: