Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

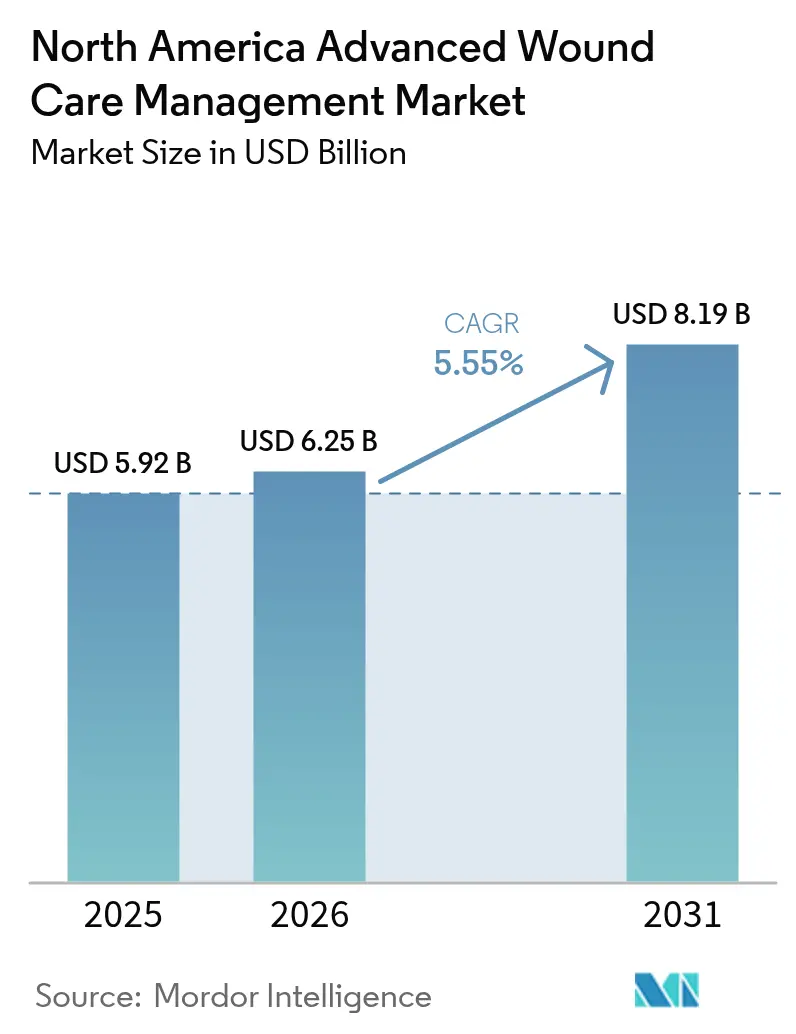

| Base Year Market Size (2025) | USD 5.92 Billion |

| Market Size (2026) | USD 6.25 Billion |

| Market Size (2031) | USD 8.19 Billion |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Advanced Wound Care Management Market Analysis by Mordor Intelligence

The North America advanced wound care management market size was valued at USD 5.92 billion in 2025 and estimated to grow from USD 6.25 billion in 2026 to reach USD 8.19 billion by 2031, at a CAGR of 5.55% during the forecast period (2026-2031). Chronic wounds remain the largest clinical burden by volume, while innovation and care-delivery shifts are changing product mix and site-of-care economics across the North America advanced wound care management market. Active wound care is the fastest-growing product cluster due to payer receptivity to biologics where cost-per-healed-wound improves overall episode costs. Care is migrating from hospitals to home, supported by remote monitoring and portable devices approved for in-home use across the North America advanced wound care management market. The United States drives scale and reimbursement depth, Mexico leads growth on improved access and coverage, and Canada advances through provincial telehealth and formulary decisions that shape adoption.

Key Report Takeaways

- By product category, moist wound care led with 45.12% revenue share in 2025. Active wound care is projected to expand at a 7.26% CAGR to 2031.

- By wound type, chronic wounds accounted for 61.02% of 2025 treatment volume. Acute wounds are forecast to grow at a 6.93% CAGR through 2031.

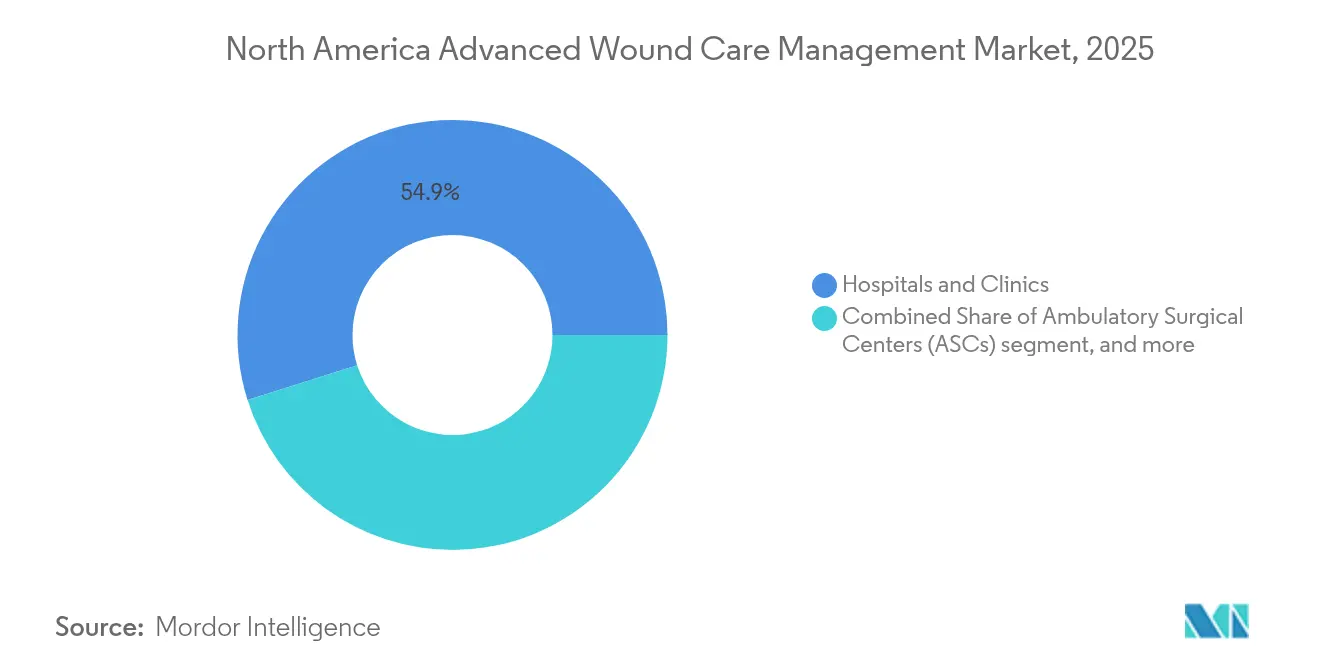

- By end user, hospitals and clinics held a 54.88% share in 2025. Home healthcare settings are projected to grow at an 8.12% CAGR through 2031.

- By mode of purchase, OTC channels held a 62.71% share in 2025. OTC channels are on track to grow at a 6.95% CAGR through 2031.

- By geography, the United States accounted for an 88.05% share in 2025. Mexico is the fastest-growing at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Advanced Wound Care Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Chronic Wounds | +1.8% | US & Canada core, spillover to Mexico | Long term (≥ 4 years) |

| Growing Geriatric Population | +1.5% | US & Canada dominant, urban Mexico emerging | Long term (≥ 4 years) |

| Technological Advancements in Wound Care Products | +1.2% | US early adoption, Canada lag, Mexico niche pockets | Medium term (2-4 years) |

| Increasing Healthcare Expenditure | +0.7% | US leading, Canada provincial variation, Mexico rising | Medium term (2-4 years) |

| Rising Awareness and Prevention Programs | +0.3% | National, with gains in underserved US rural areas | Short term (≤ 2 years) |

| Strategic Collaborations and Partnerships | +0.2% | Global players in US, regional alliances in Mexico | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic Wounds

Chronic wounds such as diabetic foot ulcers, pressure ulcers, and venous leg ulcers represented 61.54% of the 2024 treatment mix, reflecting the combined effects of aging, obesity, and diabetes across the North America advanced wound care management market. Diagnosed diabetes cases in the United States exceeded 38 million in 2024, and clinical literature indicates that up to 15% of people with diabetes develop foot ulcers over their lifetime, with a sizeable subset progressing to amputation without advanced intervention. Pressure ulcers affect millions of Americans in hospitals and long-term care, which reinforces demand for advanced dressings and negative-pressure therapies in high-risk settings[1]Michael S. Conte et al., “Current Status and Principles for the Treatment and Prevention of Diabetic Foot Ulcers,” Circulation, ahajournals.org. Biofilm formation is implicated in a large share of non-healing wounds, which strengthens the case for antimicrobial and biofilm-disruption technologies in the North America advanced wound care management market. Mexico’s public health data show a rising burden of diabetes-related lower-extremity complications, which has triggered new clinic capacity and targeted subsidies for advanced wound management. The FDA’s 510(k) program continued to clear wound-contact materials and antimicrobial dressings in 2024, supporting product refresh cycles and clinical adoption.

Growing Geriatric Population

The 65-plus cohort in North America is expanding, which increases the prevalence of pressure ulcers, delayed surgical healing, and multi-morbidity that complicates wound closure in the North America advanced wound care management market. By 2030 all U.S. baby boomers will be Medicare-eligible, creating a 73 million beneficiary pool with elevated wound risk and sustained demand for advanced therapies. Canada faces a similar aging profile with seniors projected to comprise about one quarter of the population by 2030, which is reinforcing home-based models and provincial telehealth to extend specialist access[2]Daniel Paniagua-Herrera, “The Health Care Situation of People Living with Diabetes in Mexico,” Revista Diabetes, revistadiabetes.org. This demographic shift favors devices and dressings that reduce caregiver burden, such as self-adherent foams and transparent films that enable visual checks without removal. Mexico’s 60-plus population has grown quickly since 2020, and families are leaning on OTC channels and private nursing for chronic-wound care, aligning with observed OTC volume and growth. Payer controls like prior authorization and clinical criteria are shaping site-of-care and product choice, which creates a split between hospital use of advanced biologics and outpatient default to moisture-retentive dressings.

Technological Advancements in Wound Care Products

Active wound care that includes biomaterials, skin substitutes, and growth factors is projected to grow at 7.54% through 2030 due to evidence of faster closure and payer willingness to cover higher upfront costs when episode economics improve. FDA clearances have advanced allografts and bioengineered matrices that leverage placental and porcine tissue as well as recombinant growth factors, which are expanding options for recalcitrant diabetic and venous ulcers. Medicare coverage expansions cited by U.S. manufacturers have increased eligibility for certain cellular and tissue-based products, which has raised procedure volumes in outpatient settings. Portable negative-pressure devices such as PICO enable early discharge and home management while maintaining therapy continuity under clinician oversight. Antimicrobial innovation is diversifying beyond silver to formulations such as polyhexamethylene biguanide and medical-grade honey that target pathogens while limiting cytotoxicity, which aligns with infection-control goals. The FDA’s Digital Health Center of Excellence has supported connected imaging and measurement apps that standardize wound documentation and integrate with health records for remote monitoring.

Increasing Healthcare Expenditure

U.S. national health expenditure was USD 4.8 trillion in 2024, and complex wound care consumes a notable share through hospital days, surgical revisions, and infection management, which sustains demand for advanced products in the North America advanced wound care management market. Medicare’s hospital outpatient payment updates in 2024 supported application services for cellular and tissue-based products, which aligned with value-based pressure to close wounds within defined windows. In Canada, provincial funding and formulary controls create uneven access where some provinces enable home-based negative pressure for post-surgical patients while others limit higher-cost biologics to specialist clinics. Ontario’s community care programs allocate targeted funds per chronic-wound episode such as CAD 300 (USD 222), which influences product selection and frequency of dressing changes. Mexico’s public insurers fund foundational wound care, and private insurers have begun to add benefits for prevention and advanced treatments, which supports higher-value product adoption in urban centers. Medicare coverage pathways that favor hospital-administered therapies, combined with limited pharmacy benefit coverage for dressings, reinforce OTC purchasing for simpler products and retain specialty channels for high-cost biologics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Wound Care Products | -0.9% | US commercial plans, Canada provinces, Mexico private sector | Medium term (2-4 years) |

| Stringent Regulatory Approvals | -0.5% | US FDA dominant, Health Canada parallel, COFEPRIS lag | Long term (≥ 4 years) |

| Limited Reimbursement Policies | -0.7% | US Medicare gaps, Canada provincial caps, Mexico out-of-pocket | Medium term (2-4 years) |

| Lack of Skilled Healthcare Professionals | -0.4% | Rural US, Northern Canada, underserved Mexico regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Wound Care Products

Bioengineered skin substitutes and cellular allografts are priced from USD 800 to USD 2,500 per application, which can exceed episode payments for uncomplicated wounds in several coverage programs and limit patient uptake. Medicare’s 20% Part B coinsurance means out-of-pocket amounts can reach USD 500 per treatment when list prices are high, which redirects some cases to standard moist dressings. Manufacturers have reported that prior-authorization denials and copay burdens lead to abandonment at the point of sale, which slows adoption of premium biologics. Hospitals under inpatient DRG payments must balance biologic use against fixed reimbursements, which drives selective deployment for high-risk cases and preserves volume for lower-cost foams and alginates. In Mexico, private clinics serve a price-sensitive middle-income segment where a single advanced dressing can be a significant share of household income, which supports a two-tier product mix. U.S. hospital price transparency has revealed wide variation in charges for skin-substitute procedures, yet patient shopping is limited by clinical urgency and referral patterns.

Stringent Regulatory Approvals

The FDA’s PMA pathway for higher-risk wound devices demands robust clinical evidence and multi-year timelines, which can strain mid-sized manufacturers and consolidate innovation within larger portfolios in the North America advanced wound care management market. Draft guidance on real-world evidence for wound endpoints in 2024 signaled flexibility, although standardizing imaging and documentation across sites remains a practical challenge. Health Canada’s device reviews and labeling requirements add time and complexity to multi-country launches and can delay Canadian availability of newer technologies. COFEPRIS has historically followed FDA and Health Canada decisions with a lag, which affects the pace of adoption in Mexico relative to the U.S. and Canada[3]. Post-market surveillance obligations under FDA reporting rules require tracking adverse events for wound products, which imposes compliance costs that can be significant for smaller firms. ISO 13485 certification and regular audits are needed for quality management and are prerequisites for broad distribution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Biomaterial Innovation Challenges Moist Dressing Incumbency

Moist wound care held 45.1 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov% of the North America advanced wound care management market share in 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov5, spanning foam, hydrocolloid, film, alginate, hydrogel, and collagen formats that support a moist healing environment under widely used protocols. Foam dressings lead within this subsegment due to absorbency and ease of use for venous leg ulcers and pressure injuries in home and long-term care, which sustains repeat purchasing. Hydrocolloid and alginate dressings are used for moderate to heavy exudate, while films often serve as secondary covers that reduce nursing time by allowing visual checks. Active wound care is projected to grow at 7. 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov6% through 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 3Health Canada, “Medical Devices Directorate,” Government of Canada, canada.ca1 as payers support biologics where total episode costs fall with faster closure in the North America advanced wound care management market. Hospital infection-control teams are gradually adding non-silver antimicrobials to formularies, which broadens options for biofilm-laden wounds. Manufacturers are integrating antimicrobial layers into bordered foams to simplify stocking and selection in ambulatory settings. Collagen dressings fill a niche when tendon or bone is exposed, but higher per-unit costs and wear-time constraints limit broader use in generalist settings. Regulatory clearances for contact materials require biocompatibility per ISO 1099 3Health Canada, “Medical Devices Directorate,” Government of Canada, canada.ca and safety data that support routine use in diverse care settings. Health Canada’s oversight of Class III products that include live cells or recombinant factors adds post-market reporting that can slow Canadian access compared with the United States. The growth gap between commoditized moist dressings and higher-value active therapies is steering incumbent strategies toward private-label contracts and GPO partnerships while challengers lean on peer-reviewed evidence and value analyses. This product dynamic will continue to reshape category mix in the North America advanced wound care management industry as providers match patients to interventions that close wounds within target windows.

By Wound Type: Chronic Wounds Command Volume, Acute Wounds Drive Growth

Chronic wounds accounted for 6 3Health Canada, “Medical Devices Directorate,” Government of Canada, canada.ca58885" class="citation-tooltip" aria-label="Agency for Healthcare Research and Quality, “Preventing Pressure Ulcers in Hospitals,” AHRQ, ahrq.gov"> 1.Agency for Healthcare Research and Quality, “Preventing Pressure Ulcers in Hospitals,” AHRQ, ahrq.gov0 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov% of clinical activity in 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov5, reflecting extended care cycles for diabetic foot ulcers, pressure injuries, and venous ulcers that require consistent moisture management and offloading. Diabetic foot ulcers recur frequently after closure, which sustains demand for foam dressings and selective use of biologics when conservative therapy stalls in the North America advanced wound care management market. Pressure injuries in skilled-nursing and home-bound seniors generate steady use of silicone-bordered foams and repositioning protocols, which aligns with the rise of home healthcare. Venous and arterial ulcers prompt use of compression with antimicrobial dressings, which drives bundled offerings for vascular practices. The North America advanced wound care management industry increasingly targets biofilm control within chronic wounds to accelerate time to closure.

Acute wounds held a smaller 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov5 share but are forecast to grow at 6.9 3Health Canada, “Medical Devices Directorate,” Government of Canada, canada.ca% through 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 3Health Canada, “Medical Devices Directorate,” Government of Canada, canada.ca1, reflecting expanding ambulatory surgery volumes and greater adoption of negative-pressure incisional therapy to reduce complications. Surgical-site events still impose heavy costs per episode, which strengthens the case for prophylactic antimicrobials and portable negative-pressure systems. Burn care is adopting bioengineered dermal substitutes and collagen scaffolds that speed re-epithelialization in specialized centers. Traumatic injuries create episodic demand in regions with higher industrial or construction activity, which supports inventory of hemostatic dressings in EMS and urgent care. Oversight includes ongoing surveillance for surgical meshes and implants that influence wound healing, while mandated staffing ratios in some states support early identification of post-operative complications.

By End User: Home Healthcare Settings Disrupt Hospital-Centric Models

Hospitals and clinics retained 54.88% share in 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov5, driven by complex chronic wounds that need debridement, negative-pressure therapy, and multidisciplinary oversight that is concentrated in institutional settings. Academic centers operate referral programs that standardize protocols and support education, which encourages adoption of advanced therapies where indicated across the North America advanced wound care management market. Ambulatory surgery centers gained procedures with Medicare’s expanded ASC-list, which reduced facility costs for selected skin-substitute applications.

Home healthcare is projected to grow at 8.1 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov% annually as hospital-at-home programs and telehealth workflows demonstrate comparable healing outcomes at lower cost. Care at home favors self-adherent foams, transparent films for visual checks, and single-dose antimicrobial gels that reduce dosing errors. Portable negative-pressure systems such as PICO and Prevena are FDA-cleared for home use, which supports early discharge without compromising therapy continuity. Telehealth imaging platforms such as Swift Medical extend specialist reach and enable remote plan adjustments within standard care pathways. Long-term care facilities maintain a stable share with basic moisture-retentive products under per-diem budgets, while freestanding wound centers concentrate high-intensity services like hyperbaric oxygen and advanced grafting.

By Mode of Purchase: OTC Dominance Reflects Self-Care Shift and Access Barriers

OTC channels captured 6 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov.71% of the North America advanced wound care management market in 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov5 by transaction volume, supported by retail pharmacy and e-commerce access that eases replenishment for minor wounds and ulcer maintenance. OTC products include foams, hydrocolloids, films, and non-prescription antimicrobials that patients select under clinician guidance between visits, which reduces delays from benefit authorization. Subscription delivery through major retailers reduces stockouts for rural patients who manage chronic wounds at home.

Prescription channels retain high-value products such as biologics, certain antimicrobials, and negative-pressure components that require physician orders and specialty pharmacy logistics. Slower growth in the prescription channel reflects benefit design, step edits, and prior authorization that can delay starts by several days in the North America advanced wound care management market. FDA monograph rules limit OTC labeling to minor-wound claims, which keeps advanced indications in prescription categories even when consumers use OTC dressings as part of long-term regimens. Health Canada requires DINs for non-prescription wound products and enforces safety and labeling standards for pharmacy sale. In Mexico, COFEPRIS permits OTC sale of basic dressings while reserving more advanced antimicrobials for prescription, which splits access between retail and hospital channels.

Geography Analysis

The United States held 88.05% of the North America advanced wound care management market share in 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov5, supported by high per-capita health spending, deep insurer coverage, and a dense network of wound centers that use both traditional and advanced products. Medicare and Medicaid cover large beneficiary populations with elevated wound risk, which sustains demand for dressings, debridements, biologics, and negative-pressure therapy across care settings. Market expansion in the United States is tied to innovation and value-based payment models that reward earlier closure, not to greenfield access, within the North America advanced wound care management market. FDA’s review and surveillance infrastructure supports rapid product iteration and safe deployment. National and local coverage determinations for skin substitutes widened access criteria in 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov4 in select indications, which manufacturers cited as tailwinds for procedure growth.

Canada contributes a mid-single-digit share under provincial control of coverage and drug-device formularies that create variation across the North America advanced wound care management market. Ontario uses exceptional-access processes for higher-cost dressings while Alberta’s plans support broader negative-pressure coverage at home under specific criteria. Federal and provincial research investments emphasize telehealth for remote and Indigenous communities to mitigate high diabetes prevalence and access barriers to urban wound centers. Health Canada’s timelines and cautious adoption pace often follow U.S. experience, which reduces clinical risk but slows Canadian uptake of the latest wound technologies. Group purchasing in hospitals exerts downward price pressure on commoditized categories like foams and hydrocolloids. Mexico is the fastest-growing geography at a 6.18% CAGR through 2Centers for Medicare & Medicaid Services Staff, “National Health Expenditure Data,” U.S. CMS, cms.gov0 3Health Canada, “Medical Devices Directorate,” Government of Canada, canada.ca1, driven by expanded private insurance, medical tourism for elective procedures, and public programs targeting diabetic amputations in the North America advanced wound care management market. Public systems cover foundational care while private hospitals in major cities use cellular allografts and negative-pressure therapies covered by employer or individual policies. USMCA preferences encourage local production in states such as Jalisco and Nuevo León that supply domestic and export markets, which improves pricing and availability. COFEPRIS reforms launched to shorten device approval times through reliance on FDA and Health Canada clearances aim to accelerate access but are still in transition. Compliance in Mexico relies on registration and GMP audits with stronger enforcement in large metros, prompting reputable suppliers to use ISO 1 3Health Canada, “Medical Devices Directorate,” Government of Canada, canada.ca485 quality systems to maintain trust and export readiness.

Regulatory Landscape

Advanced wound care products in North America are regulated as medical devices and biologic or combination products. In the United States, this is anchored by FDA pathways, including 510(k) for many wound dressings and device-based therapies and PMA for higher-risk products, with parallel frameworks in Canada (Health Canada Medical Devices Regulations) and Mexico (COFEPRIS registrations). A key U.S. compliance milestone is the FDA Quality Management System Regulation (QMSR), which updates device CGMP expectations in line with ISO 13485 and became effective on February 2, 2026. The change raises the bar on lifecycle quality, documentation, and supplier controls for manufacturers selling advanced dressings, negative pressure wound therapy systems, and related accessories.

In Canada, modernization is progressing through staged amendments to the Medical Devices Regulations. Phase 1 changes covering areas such as recalls and establishment licensing were published July 3, 2024 and came into force December 14, 2024. Health Canada has also signaled continued work on Phase 2 amendments through its 2026-2028 Forward Regulatory Plan, including planned finalization in fall 2026. For companies operating across the region, these actions increase the need for harmonized quality systems, tighter post-market vigilance, and readiness for evolving establishment license and compliance expectations, particularly for distributors and importers serving hospital, home health, and OTC channels.

Value Chain Analysis

The value chain spans upstream specialty inputs, including medical-grade silicones and films for foam and bordered dressings, collagen and placental and other tissue-derived matrices for active wound care, and antimicrobial agents such as silver and non-silver chemistries. It also covers manufacturing and sterilization, regulatory and quality release through ISO 13485-aligned systems and biocompatibility testing such as ISO 10993, and multi-channel distribution into hospitals, ASCs, long-term care, home health, and retail/OTC. Larger multinational suppliers (for example, 3M/Solventum, Smith+Nephew, ConvaTec, Mölnlycke, and Medline Industries) run more integrated models that combine broad product portfolios with direct-to-facility logistics and contracting capabilities, which becomes more relevant as purchasing consolidates through IDNs and GPOs.

Downstream, procurement and utilization depend on formulary decisions, bundled kit strategies, and reimbursement workflows for higher-cost cellular and tissue-based products and negative-pressure systems. High-volume moist dressings move more heavily through central distribution and retail replenishment. Key friction points in the chain include sterilization capacity for complex biologics, testing capacity for newer formulations, and exposure to logistics bottlenecks for imported raw materials and components. These constraints keep supplier diversification and resilient distribution networks at the center of operational planning for manufacturers serving the United States, Canada, and Mexico.

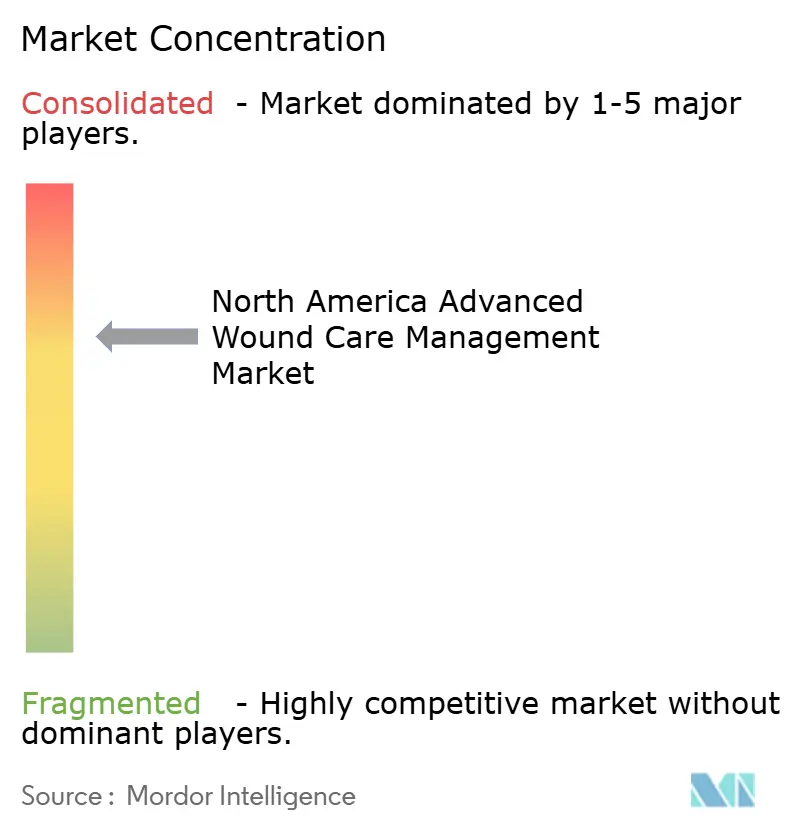

Competitive Landscape

The North America advanced wound care management market remains moderately fragmented with top global players sharing space with focused biologics firms and regional distributors that serve long-term care and home-health channels. Strategic emphasis is moving toward integrated ecosystems that combine devices, digital monitoring, and service models that build switching costs and drive adherence. Partnerships between device makers and telehealth platforms enable remote troubleshooting and data capture that support earlier intervention and supply optimization.

In the active wound care segment, product competition centers on cost-per-healed-wound outcomes for diabetic foot and venous ulcers, which payers scrutinize during coverage and policy updates in the North America advanced wound care management market. Companies reported that wider Medicare criteria in 2024 increased eligible volumes, although price competition pressured average selling prices for biologics. Negative-pressure portfolios are defended by intellectual property and incremental design improvements such as longer battery life and connectivity for home use. Patent expirations approaching 2026 to 2030 may invite new entrants and litigation that shapes pricing.

Digital wound-imaging tools are becoming a differentiator and are being bundled with consumables or offered as subscriptions to integrate with hospital and home-health workflows in the North America advanced wound care management market. Regulatory and registration costs for multi-country distribution concentrate pan-regional scale within larger firms while enabling smaller specialists to succeed within a single national market. Consolidation has been limited, but logistics and distribution assets that steer formulary decisions in ASC and home-health channels are attractive targets for private capital.

North America Advanced Wound Care Management Industry Leaders

-

3M Company

-

Smith + Nephew

-

Integra Life Sciences

-

Johnson & Johnson (Ethicon)

-

Baxter International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Care shifting to the home and post-acute settings creates room for advanced wound care offerings that combine portable therapy with standardized digital documentation. In the current market, remote assessment and documentation platforms (such as Swift Medical) are already used to extend specialist reach, and FDA-cleared portable negative-pressure systems used in-home (such as PICO and Prevena) support earlier discharge workflows. This alignment creates a clearer packaging opportunity for manufacturers to bundle consumables, monitoring, and service support designed for home-health agencies and hospital-at-home programs.

Product and evidence modernization is another active opportunity area. Regulators and stakeholders are pushing for improved endpoints and better data capture for nonhealing chronic wounds. The FDA scheduled a Patient-Focused Drug Development public meeting on nonhealing chronic wounds in 2026, while industry stakeholders have also advanced proposals to update legacy chronic ulcer guidance with greater use of digital wound assessment and contemporary trial design. That direction supports demand for tools that standardize imaging and measurement, along with therapies that can show episode-level value through more explicit documentation. On the supply side, capacity localization and expansion activity, including new or expanded manufacturing investments tied to wound care materials and biologics production platforms, supports more reliable availability. It also offers a contracting lever with large health system buyers and provides a route to compete in GPO-driven channels that increasingly shape product access and utilization.

Recent Industry Developments

- July 2026: Mölnlycke Health Care announced three wound care product launches in the United States, including Granudacyn Wound Wash Solution, the Tortoise Lite Turning and Positioning System, and Mepi Press 2 and Mepi Press Lite compression systems. The updates expand its acute-to-chronic offering across cleansing, pressure injury prevention, and compression, supporting cross-selling into hospital systems and post-acute providers that standardize protocols across sites of care.

- November 2025: Solventum entered into a definitive agreement to acquire Acera Surgical for USD 725 million in cash plus up to USD 125 million in contingent milestone payments. The transaction expands Solventum's position in regenerative wound care materials and strengthens portfolio depth in higher-value advanced therapies alongside its established dressing and care-delivery channels.

- November 2024: Geistlich signed an exclusive national distribution partnership with StimLabs in the United States for Derma-Gide Advanced Wound Matrix, shifting all commercial activities to StimLabs. The arrangement increases product reach through an established wound care commercial footprint and can accelerate adoption in both acute and chronic wound settings where distributor access and clinician education affect utilization.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenues earned from advanced wound care management products and related therapies used to treat acute and chronic wounds across the United States, Canada, and Mexico, across care settings ranging from hospitals to home health.

Scope exclusions: We exclude conventional cotton gauze, basic adhesive bandages, and veterinary wound products.

Segmentation Overview

-

By Product

-

Moist Wound Care

- Foam Dressings

- Hydrocolloid Dressings

- Film Dressings

- Alginate Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other Advanced Dressings

-

Antimicrobial Wound Care

- Silver

- Non-silver

-

Active Wound Care

- Biomaterials

- Skin-substitute

- Growth Factors

-

Moist Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous & Arterial Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical Wounds

- Burns

- Traumatic & Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers (ASCs)

- Home Healthcare Settings

- Long-Term Care & Skilled Nursing Facilities

- Specialty Wound Care Centers

-

By Mode of Purchase

- Prescription-based (Rx)

- Over-the-Counter (OTC)

-

By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by building a simple demand picture for advanced wound care in North America, then aligning that view with how care is delivered across hospital, outpatient, and home settings. Public sources such as the US CDC, the US Census Bureau, Statistics Canada, the OECD, and peer reviewed clinical journals were used to anchor diabetes burden, aging trends, procedure volumes, and wound prevalence patterns that influence product usage.

We also reviewed supporting secondary materials such as regulatory and reimbursement updates, product recall notices, public company filings and investor presentations, association websites, and reputed press coverage to understand shifts in product mix and adoption speed by therapy type. Select paid subscriptions were used for company financials and intelligence, news and financials, and patent databases, mainly to avoid missing launches and to sense check the direction of growth at an aggregated level. The sources listed here are illustrative, and many other references were used to collect data points, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary interviews and surveys were used to validate what desk research signals could not fully explain, mainly the split between advanced dressings, devices, closure consumables, biologic therapies, and prescription topical agents, and how usage differs by site of care. Respondents included manufacturers, distributors, clinicians involved in wound care, and procurement and reimbursement focused roles across the United States, Canada, and Mexico. The findings were then used to tighten pricing bands and adoption assumptions for each product group.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 13% | |

| Mid tier: 58% | Functional/Unit leaders: 34% | |

| Smaller Players: 15% | Managers: 53% |

Market-Sizing & Forecasting

Sizing began with a top-down build where chronic and acute wound treatment activity in North America was reconstructed using prevalence and treated patient pools, procedure volumes, and care setting mix, and then translated into product-level demand. To keep the model practical, we focused on a limited set of inputs, including diabetes prevalence, age-band population trends, surgical volume direction, the share of chronic wounds managed in outpatient and home settings, and observed mix shift toward negative pressure and biologic options.

After the macro build, selective bottom-up approximations were used to confirm totals and adjust them when needed. This included sampling average selling price ranges by product class and applying them to implied unit volumes, followed by channel checks on distribution intensity. Where direct unit visibility was weak, we used conservative adoption bands informed by interviews, and then aligned them with country-level care pathway differences. Forecasts were produced using scenario analysis, with the base case guided by expert views on reimbursement stability, product substitution rates, and the expected pace of adoption for newer therapies, then checked for consistency with historical growth behavior.

Data Validation & Update Cycle

Model outputs were validated through triangulation across independent signals, then followed by variance checks at the country and product class level to spot outliers that did not match known clinical and purchasing patterns. When an anomaly appeared, we revisited assumptions and triggered targeted re-contacts to confirm whether the issue was driven by pricing, channel mix, or category definitions.

Before sign-off, the work goes through multiple analyst review steps so calculations, units, and currency conversions stay consistent. Reports are refreshed annually, with interim updates when material events occur such as a regulatory change, a reimbursement shift, or a disruptive product recall. Right before delivery, an analyst completes a fresh pass so clients receive the latest updated view.

Mordor Intelligence's North America Advanced Wound Care Management Market Market Sizing Compared With Other Published Estimates

Published market sizes for advanced wound care in North America do not always align because included product families and therapy boundaries vary, and because base year selection and currency timing are not always consistent. Differences also show up when one estimate is built from treated wound populations and care-setting mix, while another relies more on broad revenue assumptions by category.

US share signals, country-level growth patterns, and cross-checks on what is counted as advanced, including negative-pressure and oxygen devices, active or biologic therapies, and prescription topical agents (not just advanced dressings), are the evidence that supports a consistent North America scope across the United States, Canada, and Mexico in Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.92 B (2025) | |

| Industry Publisher A | USD 5.60 B (2024) | Uses a different base year and may apply a tighter inclusion list, which can undercount the full advanced therapy mix and also miss part of Mexico when rolling up North America totals. |

| Research Publisher B | USD 6.55 B (2024) | Uses an earlier base year and can apply faster adoption or higher pricing progression for premium categories, which can lift the total before care-setting mix and utilization checks are applied. |

The spread in the table is mainly explained by what product groups are included, which countries are counted inside North America, and how prices are carried forward from the base year. When inputs are anchored to treated demand signals and then rechecked at the category level, the final number stays easier to trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size and 2031 outlook for the North America advanced wound care management market?

The market reached USD 5.92 billion in 2025 and is estimated to grow from USD 6.25 billion in 2026 to reach USD 8.19 billion by 2031, reflecting a 5.55% CAGR based on current growth dynamics.

Which product categories are leading growth in North America advanced wound care?

Active wound care products such as cellular matrices and growth factor therapies are the fastest-growing at a 7.26% CAGR, while moist wound care remains the largest by share.

How is the site of care shifting in North America advanced wound management?

Hospitals and clinics hold the largest share today, but home healthcare settings are growing at 8.12% annually due to telehealth, connected devices, and payer support for lower-cost sites.

Which countries are driving growth within North America advanced wound care?

The United States dominates with an 88.05% share, while Mexico is the fastest-growing at a 6.18% CAGR through 2031 as coverage and private insurance expand.

What factors are propelling adoption of advanced therapies in North America advanced wound care?

Rising chronic-wound burden, an aging population, payer-aligned episode economics, and FDA-cleared portable and digital tools are pushing adoption across care settings.

How do OTC channels influence adoption in North America advanced wound care?

OTC channels captured 62.71% of transactions in 2025 and are growing at 6.95%, as self-care for minor wounds and ulcer maintenance reduces friction from prior authorization and copays.

Page last updated on: