Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

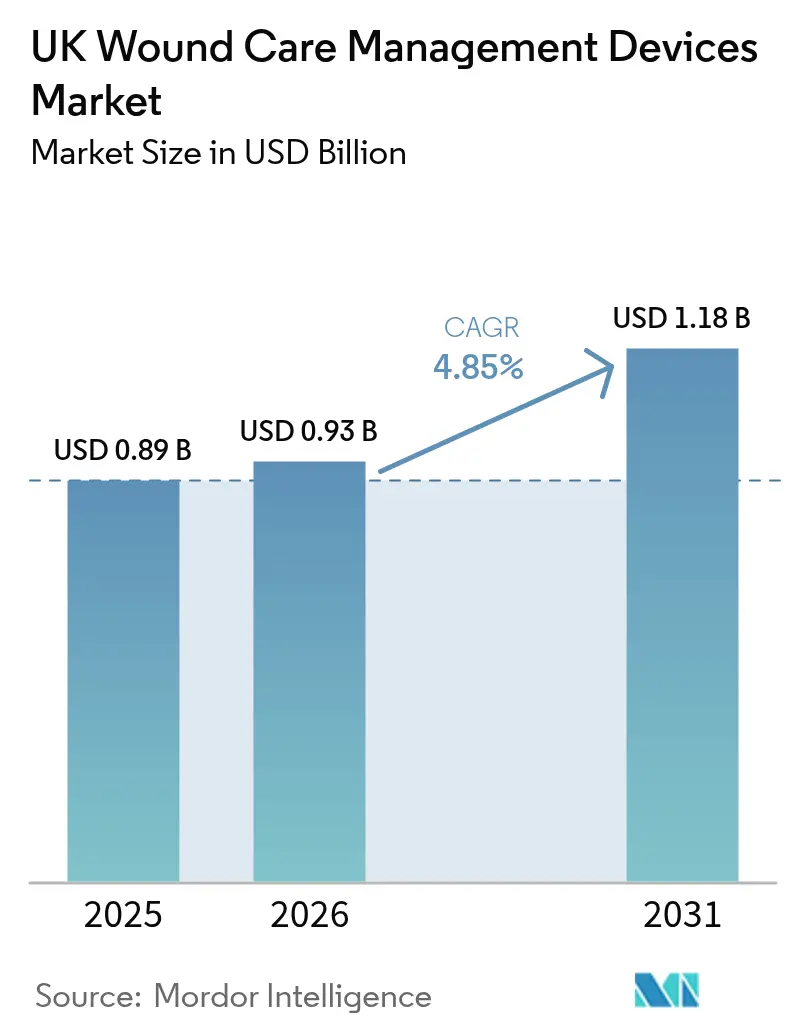

| Base Year Market Size (2025) | USD 0.89 Billion |

| Market Size (2026) | USD 0.93 Billion |

| Market Size (2031) | USD 1.18 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

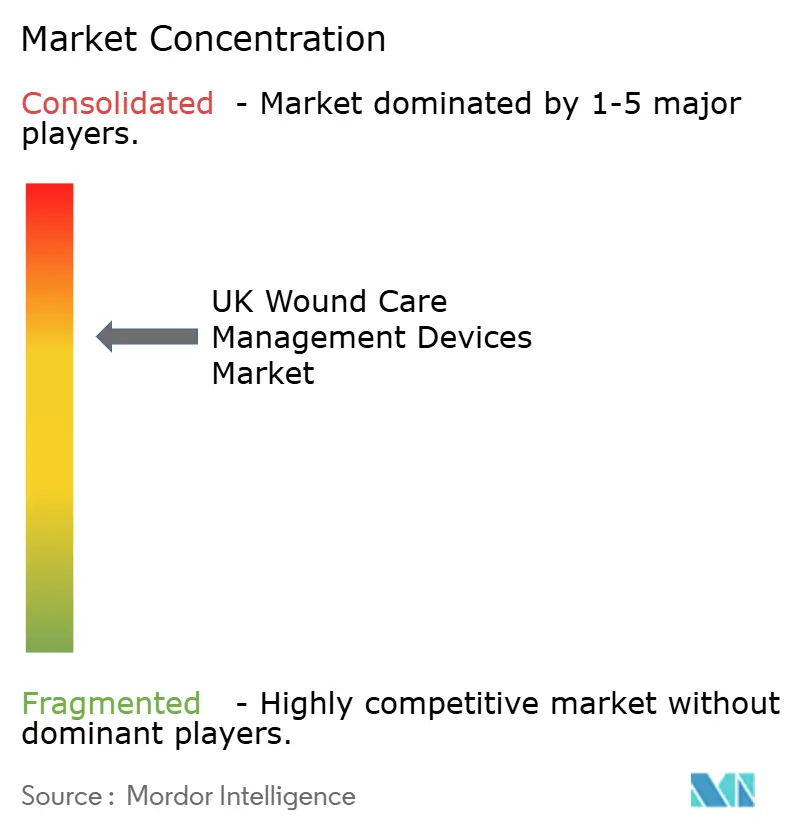

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UK Wound Care Management Devices Market Analysis by Mordor Intelligence

UK wound care management devices market size in 2026 is estimated at USD 0.93 billion, growing from 2025 value of USD 0.89 billion with 2031 projections showing USD 1.18 billion, growing at 4.85% CAGR over 2026-2031. Persistent demographic pressure from an aging population, the NHS directive to shift care into community settings, and the resumption of elective surgery are combining to lift demand for both traditional dressings and technologically advanced closure systems. Post-Brexit dual‐regulation costs are encouraging local innovation while deterring some EU-centric suppliers, subtly reshaping the competitive mix. Procurement teams are prioritizing devices that shorten healing times, lower readmissions, and align with Net-Zero goals, which is steering capital toward negative-pressure therapy, bio-based dressings, and AI-enabled assessment platforms. At the same time, staffing shortages inside hospital wards are tempering adoption of the most labor-intensive technologies, handing momentum to simpler, home-use solutions that can be deployed with minimal clinician oversight.

Key Report Takeaways

- By product type, Wound Care accounted for 63.05% of UK wound care management devices market share in 2025, while the Wound Closure segment is advancing at a 5.52% CAGR to 2031.

- By wound type, Chronic Wounds captured 59.10% revenue share in 2025; Acute Wounds are set to post the fastest 5.65% CAGR through 2031.

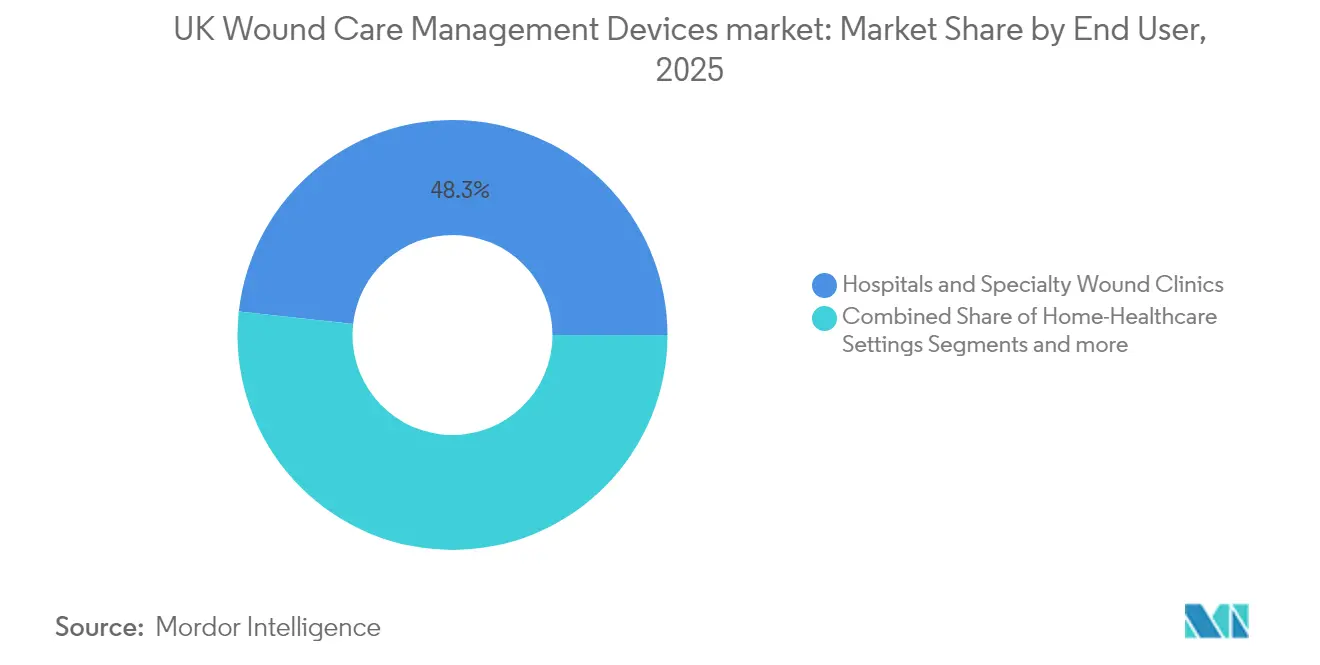

- By end user, Hospitals & Specialty Wound Clinics held 48.25% of total demand in 2025, whereas Home-Healthcare Settings expand at 5.88% CAGR to 2031.

- By mode of purchase, Institutional Procurement retained 64.70% share in 2025, yet Retail/OTC channels are growing at 5.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in geriatric population | +1.2% | UK-wide, concentrated in rural and coastal areas | Long term (≥ 4 years) |

| Growing burden of chronic wounds & related diseases | +1.0% | National, higher prevalence in deprived areas | Medium term (2-4 years) |

| Technological advances in surgical procedures & devices | +0.8% | Major urban centers and teaching hospitals | Medium term (2-4 years) |

| NHS-backed shift toward community-based wound clinics | +0.7% | National rollout, early adoption in England | Short term (≤ 2 years) |

| AI-enabled digital wound assessment platforms | +0.5% | Pilot programs in London, Manchester, Birmingham | Short term (≤ 2 years) |

| Bio-based dressings aligned with UK Net-Zero targets | +0.3% | National sustainability initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increase in Geriatric Population

The proportion of UK residents aged 65 and older continues to climb and is projected to reach 26% by 2065, pushing up the incidence of venous leg ulcers, diabetic foot ulcers, and pressure injuries [1]Center for Ageing Better, "The State of Ageing 2025," ageing-better.org.uk. Older patients often present with multiple comorbidities that slow healing, creating repeat demand for absorbent, antimicrobial, and negative-pressure dressings. Rural and coastal communities face extended travel times to acute hospitals, so tele-enabled wound assessment tools are becoming critical for home-based care. Suppliers that bundle AI triage software with easy-to-apply dressings are therefore well positioned. Over the long term, sustained geriatric growth will underpin baseline volumes in the UK wound care management devices market, encouraging manufacturers to spread fixed costs across larger unit throughput and keep prices competitive.

Growing Burden of Chronic Wounds & Related Diseases

A Health Foundation projection indicates 9.3 million UK residents will be living with major illness by 2040, with 80% of working-age increases located in the most deprived districts [2]The Health Foundation, "Health inequalities in 2040: current and projected patterns of illness by deprivation in England," health.org.uk. Rising diabetes prevalence inflates the pool of chronic wounds, leading the NHS to allocate a reported 3% of its entire budget to wound care. Procurement teams in high-burden regions are prioritizing products proven to shorten time-to-heal, such as ConvaTec’s InnovaMatrix and Aquacel Ag+ lines, which helped the company deliver 6.7% organic wound-care growth in 2024. Regional inequalities are steering additional funding to northern urban centers where chronic disease rates are highest. As these geographies widen specialist clinic capacity, the UK wound care management devices market gains incremental volume from advanced dressings, skin substitutes, and remote-monitoring hardware.

Technological Advances in Surgical Procedures & Devices

Minimally invasive and robotic-assisted surgeries are shortening in-patient stays, driving higher expectations for closure materials that minimize infection and speed convalescence. Smith+Nephew’s CORI robotic system now integrates with its negative-pressure portfolio, signaling a move toward bundled peri-operative solutions that span incision to recovery. Solventum’s Peel & Place dressing reduces application time by 61% and extends wear to seven days, trimming nursing labor and total cost per episode. Smart bandages such as Caltech’s iCares prototype monitor nitric oxide and hydrogen peroxide levels and trigger alerts when healing stalls, promising earlier intervention. Taken together, these innovations are nudging hospitals and community clinics to refresh formularies, which feeds premium-tier growth inside the UK wound care management devices market.

NHS-Backed Shift Toward Community-Based Wound Clinics

The National Wound Care Strategy Programme is guiding a transition from ward-centric to community-delivered care, allowing patients to receive specialist treatment closer to home. Clinical Commissioning Groups are investing in local hubs that emphasize portability, ease of use, and digital connectivity. West Suffolk NHS Foundation Trust’s GBP 300,000 remote-monitoring contract exemplifies how virtual wards deliver acute-level services in domestic settings [3]Government of United Kingdom, "Provision of Remote Patient Monitoring," find-tender.service.gov.uk. This push accelerates sales of lightweight negative-pressure devices and single-patient-use dressings that can be applied by a nurse during brief visits. The outcome is faster bed turnover at district general hospitals and sustained channel growth for community suppliers inside the UK wound care management devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced wound devices | -0.9% | National, particularly affecting smaller trusts | Medium term (2-4 years) |

| Limited reimbursement for home-care consumables | -0.6% | England and Wales primary care settings | Short term (≤ 2 years) |

| Post-Brexit UKCA regulatory delays & supply risk | -0.4% | National manufacturing and import channels | Short term (≤ 2 years) |

| Clinical staffing shortages for tech-intensive devices | -0.3% | Widespread, acute in northern England | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Wound Devices

Next-generation skin substitutes can cost thousands of dollars per square inch, stretching the budgets of smaller NHS trusts that lack central purchasing leverage. Even when clinical efficacy is favorable, financial directors scrutinize net-present-value calculations to ensure benefits outweigh expense. Manufacturers are responding with value-based contracting, pay-for-performance clauses, and health-economic dossiers that quantify reductions in readmission or amputation rates. Hartmann’s 4.4% organic sales rise in 2024 illustrates how competitively priced silicone-based super-absorbent dressings, supported by solid evidence, can still penetrate cost-constrained formularies. Until price points fall or reimbursement widens, uptake of premium devices will remain concentrated in teaching hospitals, tempering aggregate growth for the UK wound care management devices market.

Limited Reimbursement for Home-Care Consumables

Patients discharged to home often shoulder out-of-pocket costs for advanced dressings and sensor-equipped monitors because current reimbursement frameworks prioritize acute settings. This mismatch undermines the 6.12% CAGR potential of the home-healthcare channel. Variation among Clinical Commissioning Groups means residents in one county may receive full coverage while neighbors in another must pay from personal funds. The Department of Health and Social Care’s GBP 475,000 digital-skills grant indicates policymakers recognize the gap, yet material funding shifts have not yet followed. Until a unified reimbursement scheme materializes, growth in community deployments inside the UK wound care management devices market will rely on manufacturer assistance programs and evidence that demonstrably lowers total system cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Advanced Technologies Drive Adoption

Wound Care products represented 63.05% of UK wound care management devices market share in 2025, reflecting decades-long clinical familiarity and a broad catalog ranging from gauze to bioactive matrices. Negative-pressure wound therapy (NPWT) systems, disposable canisters, and silver-impregnated foams account for a rising slice of this pool, in part because RENASYS EDGE won a global design award that underscored its patient-mobility advantage. The smaller Wound Closure category is on a 5.52% CAGR path as robotic and laparoscopic procedures broaden indications for absorbable staplers and topical tissue adhesives. Manufacturers are embedding RFID tags and moisture sensors into dressings, converting what was once inert material into data-rich platforms that integrate with electronic health records. Traditional gauze retains a role for low-exudate wounds, yet advanced silicone-based super-absorbents from Hartmann are gaining formulary priority after proving cost-effective in multicenter audits.

Second-generation skin substitutes, recombinant growth factors, and bioresorbable meshes are poised to command premium price bands, though their diffusion will depend on cost-effectiveness dossiers. ConvaTec’s InnovaMatrix, for instance, employs porcine dermis to accelerate tissue regeneration, supporting the firm’s 6.7% organic revenue rise in H1 2024. As hospitals align procurement with Net-Zero, bio-based and recyclable packaging gains influence. AI algorithms that flag early infection signs from dressing photos are being bundled with starter kits, a move that elevates switching barriers and anchors account loyalty. Taken together, product differentiation, regulatory compliance, and sustainability credentials direct purchasing decisions in the UK wound care management devices market.

By Wound Type: Chronic Cases Lead, Acute Growth Accelerates

Chronic Wounds accounted for 59.10% of revenue in 2025, cementing their role as the largest demand driver for the UK wound care management devices market. Venous leg ulcers and pressure injuries dominate incidence tables, although diabetic foot ulcers incur the steepest per-patient cost because of high amputation risk. NICE endorsement of UrgoStart Plus opened reimbursement pathways for oxidative and protease-modulating dressings, sharpening the focus on evidence-backed therapies. AI-enabled prediction tools are reducing variability in chronic-wound assessment, steering clinicians toward early intervention protocols that rely on antimicrobial foams and skin substitutes.

Acute Wounds are set to expand at a 5.65% CAGR through 2031, driven by the rebound in trauma presentations and elective surgeries. Johnson & Johnson’s antibacterial Ethicon Plus sutures report lower infection odds, which is encouraging theatre departments to standardize on coated suture packs. Burns units are trialing hydrogel membranes embedded with slow-release analgesics that cut dressing-change pain, enhancing patient compliance and outcomes. Military and emergency-response markets are demanding lightweight haemostatic patches that function under austere conditions, introducing new end-user segments. The interplay between chronic complexity and acute episode volume underpins a dynamic product-development cycle inside the UK wound care management devices market.

By End User: Decentralization Reshapes Care Models

Hospitals & Specialty Wound Clinics held 48.25% of sales in 2025, underpinned by the concentration of complex cases, surgical wounds, and reimbursement workflows. Specialist centers employ multidisciplinary teams that can apply advanced tissue substitutes and NPWT canisters with integrated instillation. Community nursing constraints, however, are shifting follow-up care to the patient’s residence once stability is achieved. This trend is propelling Home-Healthcare Settings forward at a 5.88% CAGR to 2031, as illustrated by West Suffolk’s virtual ward program that saved bed days while sustaining clinical outcomes. Vendors are therefore engineering single-use pumps and color-coded dressing kits that non-specialists can deploy after a brief online tutorial.

Long-term Care Facilities remain integral for immobile elderly patients susceptible to pressure ulcers. Staff turnover and budget limitations in these facilities intensify demand for dressings that can stay in place longer, minimizing change frequency and training overhead. Across all settings, electronic wound-tracking apps are bridging knowledge gaps, allowing consultants in tertiary hospitals to supervise care remotely. This convergence of telehealth and portable hardware continues to expand the serviceable volume of the UK wound care management devices market.

By Mode of Purchase: Institutional Dominance Meets Retail Momentum

Institutional Procurement commanded 64.70% of 2025 orders because the NHS leverages framework agreements to capture scale economics and enforce standard practice. The GBP 1.5 billion tech-devices framework, for example, bundles wound equipment with imaging and IT solutions, enabling trusts to streamline adjudication and logistics. Supplier scorecards now include carbon-footprint metrics alongside clinical value, aligning purchasing with NHS Net-Zero. Retail/OTC channels are expanding at a 5.83% CAGR as self-treating patients, especially those with minor post-surgical wounds, turn to pharmacy chains for siliconized foams and hydrocolloids endorsed by pharmacist consults.

E-commerce uptake accelerated during pandemic lockdowns and remains sticky, prompting manufacturers to develop direct-to-consumer web portals that ship dressings on subscription. User-friendly packaging, step-by-step video guides, and virtual nurse hotlines help mitigate the risk of misuse. Over the forecast horizon, the UK wound care management devices market size for OTC dressings is expected to surpass USD 252.6 million, equivalent to roughly 20.75% of all non-institutional volume, under the assumption that current CAGR trajectories hold.

Geography Analysis

England, home to more than 55 million residents and the majority of teaching hospitals, anchors procurement volume in the UK wound care management devices market. London, Manchester, and Birmingham host early-stage pilots for AI triage platforms, accelerating technology diffusion. Scotland’s integrated health-board structure facilitates cohesive formulary decisions across rural Highlands, where telehealth solutions mitigate distance barriers. The country’s centralized data systems also ease post-market surveillance, giving innovators a clear route for real-world-evidence generation.

Wales and Northern Ireland face distinct logistical challenges tied to topography and parallel EU medical-device regulation within Northern Ireland. Delays in UKCA marking implementation have prompted some suppliers to divert stock away from mainland trusts, temporarily widening lead times. Despite this friction, Northern Ireland leverages EU-aligned pathways to pilot continental innovations, offering a proof-of-concept environment that later expands UK-wide. Chronic-disease prevalence is highest in northern England and parts of Wales, reinforcing regional demand for super-absorbent and antimicrobial technologies and driving clinical-skill investment in community nursing teams.

Coastal regions such as Cornwall and East Anglia harbor significant elderly populations, creating pockets of heightened chronic-wound incidence. Community hospitals in these areas are expanding virtual wards that integrate negative-pressure pumps with smartphone-based assessment, shortening travel for frail patients. Overall, geographic diversity in prevalence, regulation, and digital infrastructure translates into a patchwork of purchasing behaviors that seasoned suppliers must navigate to capture full value from the UK wound care management devices market.

Regulatory Landscape

Wound care management devices in Great Britain are regulated by the Medicines and Healthcare products Regulatory Agency (MHRA) under the Medical Devices Regulations 2002 (as amended) and the Medicines and Medical Devices Act 2021. To preserve continuity post-Brexit, the Medical Devices (Amendment) (Great Britain) Regulations 2025 came into force in May 2025 to prevent the sunsetting of key assimilated EU provisions, while CE-marked devices continue to be accepted in Great Britain under transitional arrangements running to 30 June 2030.

Regulatory direction is moving toward simplified access routes and stronger traceability. In July 2025, the MHRA published a response on routes to market, confirming work on international reliance and simplification around UKCA requirements, and in March 2026 it launched a consultation on indefinite recognition of CE-marked medical devices in Great Britain. Separately, Unique Device Identification (UDI) is being positioned to reduce labeling friction, with the intent to remove mandatory physical UKCA marking once UDI is operational, supported by transition periods differentiated for general medical devices and IVDs.

Competitive Landscape

The UK wound care management devices market is moderately consolidated around a blend of long-established multinationals and agile digital entrants. Smith+Nephew’s 12.2% Advanced Wound Management growth in 2024 was propelled by RENASYS EDGE NPWT pumps and GRAFIX PLUS cellular matrices. ConvaTec’s InnovaMatrix launch and Aquacel Ag+ expansion yielded a 6.7% organic uptick, confirming sustained appetite for antimicrobial hydrofiber material.

AI platform providers such as Swift Medical processed more than 600,000 wound evaluations per month in 2024, demonstrating scalability and clinician acceptance. Partnerships between analytics firms and dressing manufacturers aim to embed decision support directly into dressings, a move likely to blur hardware-software boundaries. Acquisition momentum is building: Gentell’s purchase of Integra LifeSciences’ traditional wound business in February 2025 bolstered its presence in absorbent foams and hydrocolloids. Sustainability credentials now serve as table stakes, with suppliers publicizing lifecycle assessments and recyclable packaging initiatives to align with NHS Net-Zero procurement scoring.

Pricing strategies are gradually shifting from unit sales to outcomes-based reimbursement, especially for skin substitutes and long-wear NPWT consumables. Early adopters are experimenting with shared-savings models that rebate trusts if healing milestones are not met. Competitive differentiation also hinges on regulatory agility; companies that completed UKCA transition well ahead of the July 2025 deadline gained preferred-supplier status during multi-year tenders. As technological convergence, sustainability imperatives, and value-based care converge, the contest for leadership within the UK wound care management devices market is moving beyond scale toward solution breadth and data-driven proof of value.

UK Wound Care Management Devices Industry Leaders

-

Smith & Nephew

-

Convatec Inc.

-

Medtronic PLC

-

Coloplast

-

Solventum

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

NHS-led standardization and pathway transformation are creating whitespace for suppliers that can bundle products with measurable outcomes and interoperable data. The Wound Care Information Standard provides a national framework for recording assessment, observations, and treatments, which increases the value of digital wound assessment platforms and connected devices that can carry consistent metrics across services. Alongside this, the National Wound Care Strategy Programme (NWCSP) Lower Limb Recommendations have transitioned to local Integrated Care Boards (ICBs), shifting adoption dynamics toward service-level commissioning, where suppliers can support leg-ulcer pathways through training, auditing tools, and evidence packages that reduce unwarranted variation.

Planned regulatory change also supports near-term execution opportunities for manufacturers and importers that can align technical files and supply chains early. The MHRA published a draft Medical Devices (Amendment) Regulations 2026 on 8 May 2026, proposing an international reliance pathway, Unique Device Identifiers, and risk-proportionate classification rules for the Great Britain market, with the package slated for anticipated adoption in December 2026 and an intended commencement in June 2027. With standardized NHS data requirements and evolving routes to market converging, demand is being shaped toward wound care portfolios that can be deployed in community settings, digitally tracked, and supported by compliance-ready labeling and traceability capabilities.

Recent Industry Developments

- July 2026: ConvaTec completed a GBP 24 million expansion of its Rhymney, South Wales manufacturing facility to increase production capacity for Hydrofiber wound dressing material. Adding UK-based capacity strengthens supply resilience for core advanced dressing lines used in chronic wound care, supporting continuity for NHS and community channels.

- May 2026: ConvaTec highlighted advanced wound care pipeline updates and product focus at EWMA 2026, including ConvaNiox and ConvaFoam. The activity reinforced the company’s push to broaden advanced dressing and adjunct-therapy options, strengthening competitive positioning as procurement shifts toward products that reduce clinician time and support community-delivered care.

- December 2024: Belluscura formed a joint venture with Separation Design Group and a major medical device company to explore oxygen-based wound care solutions. The collaboration broadened R&D optionality around oxygen therapy approaches in wound management, adding another innovation thread alongside established dressings and NPWT in the UK ecosystem.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers devices and products used in the United Kingdom to assess, protect, close, or heal wounds, and it is sized in value terms based on sales into care settings.

Scope exclusions: We exclude biologic grafts, pure service fees, and generic surgical consumables that are not purchased specifically for wound management.

Segmentation Overview

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping what is sold and where it is used, and then aligning it to UK healthcare delivery (acute care, community settings, and home care). We rely on public, non-paywalled sources such as NHS England publications, Office for National Statistics datasets, MHRA guidance and device safety notices, National Institute for Health and Care Excellence evidence summaries, and peer-reviewed clinical journals covering wound prevalence and treatment pathways.

To translate those signals into a usable model, we also review company annual reports and investor presentations, distribution and association websites, and reputable press for pricing moves and supply availability. In parallel, we use paid subscriptions for company financials and intelligence, plus patent databases and shipment-level import and export trackers where they help validate product flow into the UK. The sources listed here are illustrative only, and many other references were used for data collection, validation, and clarification during the research process.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that desk sources rarely answer cleanly, including how often products are switched, how negative pressure wound therapy is procured, and what drives protocol choice for chronic wounds. We spoke with a mix of clinicians, procurement teams, distributors, and manufacturer-side experts across the UK so that treatment setting differences and channel markups could be cross-checked, then fed back into the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 17% | |

| Mid tier: 52% | Functional/Unit leaders: 24% | |

| Smaller Players: 19% | Managers: 59% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the demand pool from treated wound volumes in the UK and then applies a typical therapy mix by setting, which is later adjusted for product change frequency and average selling price (ASP) ranges. Once the totals are formed, they are corroborated with selective bottom-up checks, such as sampling supplier revenue exposure to the UK, channel checks on tender and distributor pricing, and unit-to-value conversions for high-usage items.

A few of the practical inputs that shape the model include the chronic versus acute wound split, adoption of negative pressure wound therapy in hospital versus community care, dressing change frequency, the share of advanced dressings within total dressings, and the timing of price changes linked to procurement cycles. Where data gaps remain, we use conservative ranges agreed during interviews, and then keep the assumptions consistent across years so trend direction is not driven by one-off inputs. Forecasting is run using scenario analysis, anchored to expected patient load, care pathway shifts toward community care, and gradual ASP movement, with the final path selected based on expert consensus from primary discussions.

Data Validation & Update Cycle

Validation is done in steps so that the final number is not dependent on one data stream. We compare the modeled output against independent signals such as procurement patterns, product-mix expectations from clinicians, and visible trade flows, and then investigate any outliers before the estimate is signed off.

A second analyst reviews key assumptions, and re-contacts are triggered when we see large variances versus expected treatment volumes or pricing bands. Reports are refreshed annually, with interim updates when material events occur that can shift demand, availability, or pricing. Before delivery, a final check is completed so clients receive the most current view available at that time.

Mordor Intelligence's UK Wound Care Management Devices Market Size Compared With Other Published Estimates

It is common to see different market sizes published for UK wound care because the category boundaries are not uniform, and because some studies mix products and therapies that are purchased and used in very different ways. Differences also come from how each publisher handles pricing, the year used as the base, and whether estimates are tuned using real-world procurement feedback.

In practice, the biggest gaps usually show up in three places, including whether advanced wound care is blended with broader wound products, whether negative pressure systems are counted as equipment only or as equipment plus consumables, and how currency timing and inflation are treated across the forecast window. Some estimates also lean on aggressive adoption assumptions for community care, without checking how often protocols can change inside NHS purchasing cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.89 B (2025) | |

| Industry Publisher A | USD 1.39 B (2024) | Uses a broader category set by mixing wound care management devices with adjacent wound product buckets, and it reports an earlier base year that can sit higher if pricing was elevated in that period. |

| Industry Publisher B | USD 1.10 B (2026) | Covers advanced wound care only, and the inclusion of compression therapy demand plus a different adoption curve for NPWT can move the total away from a devices-led scope. |

The spread in published numbers is mostly explained by what gets counted as part of wound care and how therapy mix is applied year by year. By keeping NPWT split into capital items and consumable kits, and by excluding biologic grafts and pure service fees, the sizing stays tied to a repeatable purchasing-based view that was refreshed with UK channel checks, which is a key modeling choice applied by Mordor Intelligence.

Key Questions Answered in the Report

What is the current size of the UK wound care management devices market?

The market stands at USD 0.93 billion in 2026 and is forecast to reach USD 1.18 billion by 2031 on a 4.85% CAGR trajectory.

Which product segment holds the largest UK wound care management devices market share?

Wound Care products, including traditional and advanced dressings, captured 63.05% share in 2025.

Why are home-healthcare settings growing faster than hospitals?

NHS policy favors community care, remote-monitoring technology now supports safe home treatment, and patients prefer recovery in familiar environments, producing a 5.88% CAGR for the segment.

How is Brexit affecting device suppliers?

Dual compliance with UKCA and EU MDR adds regulatory cost but also provides an opening for non-EU innovators willing to certify exclusively for the UK.

What are the main restraints on market growth?

High prices for premium devices and inconsistent reimbursement for home-care consumables collectively subtract 1.5 percentage points from the forecast CAGR.

Which companies are leading innovation in AI-enabled wound assessment?

Swift Medical’s Skin & Wound 2 platform handles over 600,000 evaluations each month, while several dressing manufacturers are embedding sensors and analytics into their product lines.

Page last updated on: