Advanced Wound Care Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.44 Billion |

| Market Size (2031) | USD 18.22 Billion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

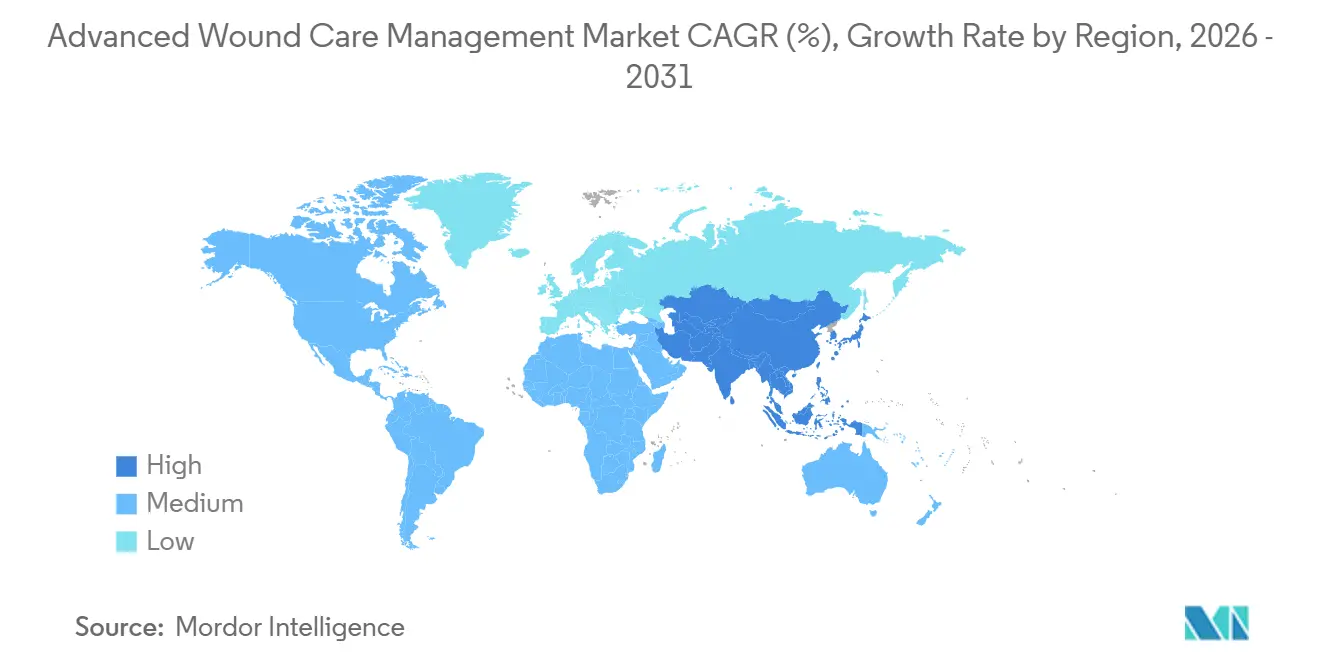

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Wound Care Management Market Analysis by Mordor Intelligence

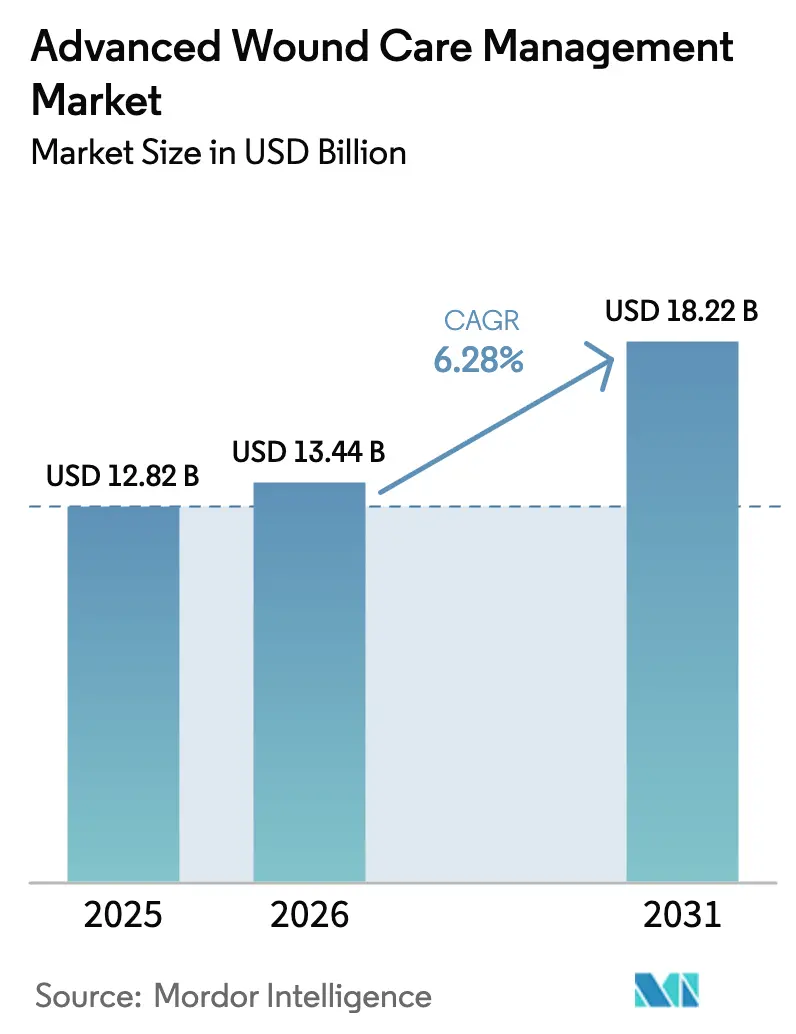

The Advanced Wound Care Management Market size is expected to increase from USD 12.82 billion in 2025 to USD 13.44 billion in 2026 and reach USD 18.22 billion by 2031, growing at a CAGR of 6.28% over 2026-2031.

Rapid technology adoption, the aging population, rising diabetes prevalence, and payer moves toward outcome-based reimbursement are working together to reshape treatment protocols. Clinicians favor therapies that shorten healing time, such as negative-pressure systems and bio-engineered grafts, over passive coverage, while hospital buyers reward vendors that can supply complete product bundles. Portable devices designed for unsupervised use at home are extending the continuum of care beyond hospital walls, and digital monitoring platforms are turning dressings into data sources that support preventive interventions. Manufacturers able to align clinical evidence with payer requirements are capturing share as formularies tighten around products that demonstrate cost avoidance.

Key Report Takeaways

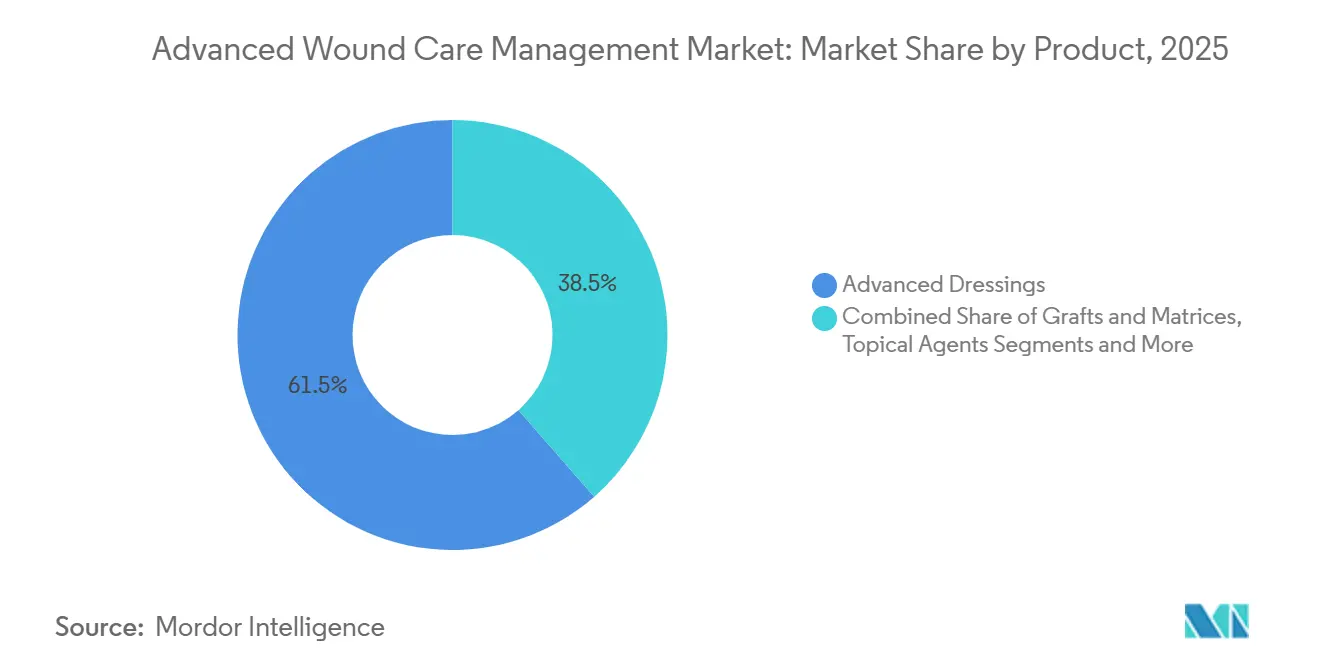

- By product, advanced dressings led with 61.46% revenue share in 2025; devices and accessories are projected to expand at a 9.46% CAGR through 2031.

- By wound type, surgical and traumatic wounds commanded 33.66% revenue share in 2025; burns and other complex wounds are forecast to grow at a 10.34% CAGR through 2031.

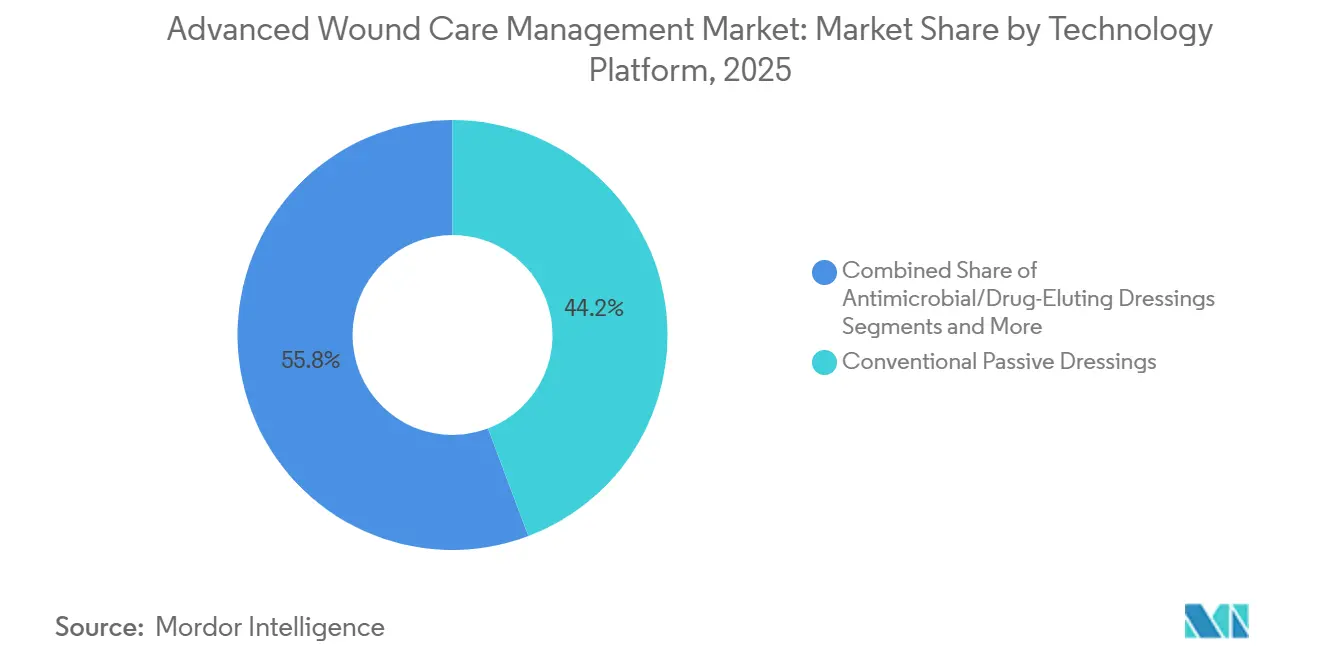

- By technology platform, conventional passive dressings held 44.24% share in 2025; smart sensor-integrated platforms will rise at a 9.35% CAGR through 2031.

- By patient age group, adults (18–64) accounted for 53.37% share in 2025; the geriatric cohort (65+) will advance at an 8.03% CAGR during 2026-2031.

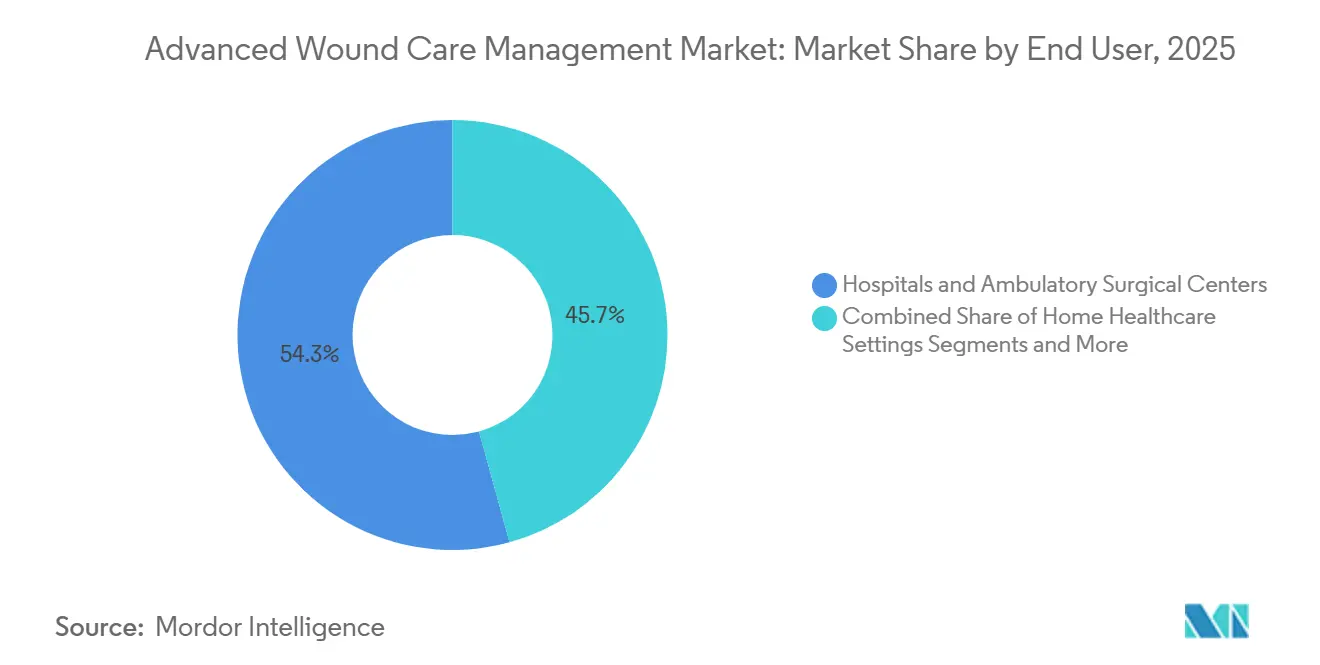

- By end user, hospitals and ambulatory surgical centers captured 54.28% share in 2025; home healthcare is set for a 10.54% CAGR to 2031.

- By distribution channel, direct hospital procurement represented 61.57% of revenue in 2025; e-commerce will expand at a 10.68% CAGR through 2031.

- By geography, North America generated 36.41% of global revenue in 2025; Asia-Pacific is projected to post an 8.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Advanced Wound Care Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic wounds linked to diabetes and aging | +1.8% | Global, highest in Asia-Pacific and North America | Long term (≥ 4 years) |

| Next-generation antimicrobial, moisture dressings | +1.2% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Expanded reimbursement and home healthcare | +1.4% | North America and Western Europe | Medium term (2-4 years) |

| Smart sensor dressings for tele-monitoring | +0.9% | North America, Western Europe, pilot programs in GCC | Long term (≥ 4 years) |

| Biologic and stem-cell skin substitutes | +0.7% | North America, Europe, opening pathways in Asia-Pacific | Long term (≥ 4 years) |

| Bio-sourced sustainable materials | +0.3% | Europe, with spillover to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Prevalence Surge of Chronic Wounds Linked to Diabetes and Aging Populations

Diabetes continues to rise, and older adults are growing as a share of the population, creating a steady inflow of patients with hard-to-heal ulcers. In the United States and Western Europe, readmission penalties have made chronic wound prevention a financial priority for hospitals. Medtronic recorded high single-digit growth in wound management during fiscal 2024 after increased procedure volumes among elderly patients.[1]Ryan Weispfenning, “Medtronic Reports Full Year and Fourth Quarter Fiscal 2024 Financial Results,” Medtronic, filecache.investorroom.com Health systems now view advanced dressings, biologic grafts, and negative-pressure devices as tools to reduce costly complications. As amputations and prolonged hospital stays drive payer spending, demand for comprehensive wound solutions escalates. Investments in multidisciplinary outpatient centers are further reinforcing consistent protocol adoption.

Rapid Adoption of Next-Generation Antimicrobial and Moisture-Retentive Dressings

Hospitals are standardizing silver, polyhexanide, honey, and iodine dressings to curb surgical site infections. The procedural pivot intensified after pandemic-era infection-control measures highlighted the value of antimicrobial barriers. Smith & Nephew published 2024 data showing its PICO single-use negative-pressure platform cut infection rates, and adoption of ALLEVYN LIFE foam into prevention bundles followed. Moisture-retentive foams and hydrocolloids reduce dressing changes, freeing nursing time and improving patient comfort. As formulary committees weigh total episode cost instead of unit price, suppliers with clinical dossiers that demonstrate readmission reduction gain preferred status. Vendor support programs that train staff on protocol updates also expedite uptake.

Expanded Reimbursement and Home-Healthcare Utilization

Payers in the United States and Europe approved fee schedules for portable negative-pressure devices and advanced dressings used outside hospitals. Home healthcare therefore emerges as the fastest end-user channel, with growth reinforced by patient preference for recovery at home. The U.K. National Institute for Health and Care Excellence has an active guidance pipeline that shapes local reimbursement and often informs European counterparts.[2]National Institute for Health and Care Excellence, “Wound Management | Topic | NICE,” National Institute for Health and Care Excellence, nice.org.uk Ireland’s Health Service Executive ties listing to peer-reviewed evidence and price benchmarks, ensuring that only products with demonstrable value enter public schemes.[3]kburns, “Criteria for Urinary Incontinence Products,” Health Service Executive, hse.ie Portable pumps designed for single-patient use simplify clinical oversight, letting visiting nurses manage complex wounds without hospital readmission. Manufacturers building device-dressing combinations accompanied by tele-support gain competitive traction.

Smart Sensor-Integrated Dressings Enabling Tele-Wound Monitoring

Dressings embedded with pH, temperature, and oxygen sensors transmit data to electronic health records, enabling clinicians to identify deterioration early. Hospitals investing in remote monitoring platforms adopt these dressings to shorten inpatient stays and reduce emergency visits. Smith & Nephew’s LEAF system, launched in 2024, added patient-movement analytics to its existing portfolio and contributed to 20.6% growth in device revenue that year. Regulatory pathways are evolving but payers already reimburse remote patient monitoring codes, making the business case clear. Uptake concentrates in North America and Western Europe, while pilot programs in Gulf Cooperation Council markets address surging diabetes burdens. Integration with predictive analytics bakes prevention into care pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High per-patient cost and fragmented reimbursement | -0.8% | Latin America, Middle East and Africa, Southeast Asia | Medium term (2-4 years) |

| Shortage of certified wound-care specialists | -0.6% | Global, most acute in rural and emerging markets | Long term (≥ 4 years) |

| Supply-chain risk for alginate and foam inputs | -0.4% | Global, exposure where seaweed harvests dominate supply lines | Medium term (2-4 years) |

| Regulatory ambiguity for nano and bio-engineered dressings | -0.3% | Global, with differing FDA and EMA classifications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Per-Patient Cost and Fragmented Reimbursement in Emerging Economies

Advanced wound therapies often cost more than USD 500 per treatment cycle, a figure that eclipses average monthly incomes in many emerging countries. Out-of-pocket spending dominates these markets, and public formularies tend to exclude premium devices and biologics. Manufacturers must navigate province- or emirate-level approval processes, each with distinct submission formats, prolonging time to market. Private hospitals serving affluent urban patients adopt the newest products, but volume remains limited. As a result, conventional gauze and low-priced foams persist across public systems, moderating overall growth potential.

Shortage of Certified Wound-Care Specialists Globally

The advanced wound care management market depends on nurses and physicians who can perform debridement, apply negative-pressure pumps, and interpret sensor data. Many countries report vacancy rates that leave general practitioners managing complex wounds without specialized training. Certification programs take four to six years to scale, so supply is unlikely to meet demand before the next decade. To compensate, vendors design devices with simplified interfaces and offer online training modules, yet hospitals still hesitate to invest in technologies requiring expertise they lack. The workforce gap thus keeps adoption below potential, especially in rural settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Devices Capture Momentum Within Dressing-Led Portfolio

Devices and accessories, primarily negative-pressure pumps, will record a 9.46% CAGR, the fastest in the segment hierarchy. Advanced dressings retain volume dominance with a 61.46% stake, ensuring they remain the economic backbone of the advanced wound care management market. Evidence linking portable NPWT to infection reduction strengthened payer support, and Smith & Nephew’s RENASYS EDGE launch illustrated how user-friendly engineering accelerates uptake. Grafts and matrices occupy niche indications, notably third-degree burns and diabetic ulcers, where autografts are unsuitable. Topical agents complement these products, especially in enzymatic debridement protocols that precede negative-pressure therapy.

Although price sensitivity restrains biologics in public facilities, targeted reimbursement in specialty centers fosters steady demand. Devices enjoy bundled payment alignment because hospitals can offset acquisition cost through shorter length of stay. Consequently, suppliers with integrated device-dressing solutions capture cross-selling synergies. Competitors that lack capital equipment offerings risk marginalization as procurement committees consolidate vendor lists around full-portfolio partners.

By Wound Type: Complex Cases Propel Above-Average Growth

Burns and other complex wounds will climb at a 10.34% CAGR, well ahead of surgical and traumatic wounds that currently hold a 33.66% slice of spending. Rising industrial activity and urban traffic in developing nations increase severe trauma incidence, expanding the addressable pool for advanced grafts. Kerecis fish-skin matrices demonstrated superiority over standard care in severe diabetic foot ulcers, validating biologic alternatives to traditional grafts. Surgical sites remain a stable revenue base, but growth moderates because advanced dressings are already standard in most operating rooms. Pressure ulcer prevention gains regulatory focus, steering long-term care facilities toward prophylactic foam usage.

Diabetic foot and venous leg ulcers yield recurring revenues because they demand months of treatment. However, reimbursement caps limit product mix to cost-effective choices in many health systems. Manufacturers that offer tiered portfolios can match clinical need with payer constraints, sustaining participation across wound classes. Overall, heterogeneity in wound etiology requires differentiated solutions, and vendors that articulate segment-specific value propositions capture upside.

By Technology Platform: Sensors and Bioactives Challenge Passive Approaches

Smart sensor dressings will outpace all peers at a 9.35% CAGR as health providers shift monitoring into the community. Passive foams and gauze still facilitate high-volume basic care, representing 44.24% of 2025 revenue, but they face margin compression from private-label competition. Drug-eluting variants that deliver silver or iodine meet infection-control mandates without separate topical use, improving workflow efficiency. Bio-engineered substrates, including acellular dermal matrices, find footholds in burn centers and multidisciplinary diabetic clinics.

Negative-pressure systems, both reusable and single-use, remain central to protocols that target high-exudate wounds. Single-patient devices, such as PICO, address home-care needs and fit bundled readmission penalties. Electrical and ultrasound stimulation continues as a niche therapy in stubborn ulcers. Regulatory complexity escalates with product sophistication, so firms must sustain clinical trial pipelines and post-market surveillance. The widening gulf between commodity and premium technologies underscores the importance of R&D-driven differentiation within the advanced wound care management market.

By Patient Age Group: Geriatric Needs Drive Future Upside

Adults between 18 and 64 years supplied 53.37% of 2025 revenue thanks to sheer demographic weight and high surgical volumes. The geriatric cohort is poised for an 8.03% CAGR, reflecting rising life expectancy and comorbidity burdens. Pressure ulcers and venous leg ulcers appear disproportionately among older adults, necessitating long treatment windows that favor advanced dressings with extended wear times. Sensor-enabled platforms allow caregivers to detect early tissue compromise, aligning with quality metrics tied to ulcer prevention.

Pediatric wounds comprise a small but specialized segment focused on atraumatic removal and reduced adhesive strength. Innovation remains incremental because volumes are limited, yet hospitals value child-friendly designs that lower anxiety. Market messaging now emphasizes age-appropriate solutions, ranging from low-profile NPWT pumps for adolescents to foam cut-outs that distribute pressure in frail seniors. Players that segment their portfolios by life stage can tailor marketing and clinical education for maximal relevance.

By End User: Home Healthcare Emerges as High-Velocity Channel

Hospitals and ambulatory centers still lead with 54.28%, but portable therapy platforms are shifting significant volumes into domiciliary care. Home healthcare will expand at 10.54% CAGR, propelled by Medicare policies that reimburse negative-pressure pumps used outside institutional settings. Smith & Nephew’s PICO system exemplifies device miniaturization and ease of use, helping hospitals reduce inpatient days while maintaining therapeutic intensity. Long-term care facilities remain price-conscious and rely heavily on prophylactic foam dressings, but quality-linked funding encourages gradual adoption of sensor technologies.

Hospitals face tighter diagnosis-related group payments, pressing them to discharge patients sooner. Consequently, manufacturers create product lines that transfer seamlessly from ward to home, preserving continuity of care. Education programs for visiting nurses and caregivers become differentiators, supporting adherence and outcomes. The advanced wound care management market therefore rewards firms that master cross-setting coordination.

By Distribution Channel: Digital Commerce Redefines Access

Direct hospital purchasing represents 61.57% of global value, anchored by group buying organizations that secure large-volume discounts. E-commerce, the smallest channel today, will thrive at a 10.68% CAGR as chronic wound patients reorder supplies through subscription platforms integrated with telehealth portals. Companies confront channel conflict because online sales expose pricing and erode distributor margins. Still, digital storefronts widen reach to rural users and allow data capture on consumption patterns.

Retail pharmacies and medical supply stores cater to walk-in traffic and small clinics, offering immediate availability at moderate margins. Advanced devices that require prescription remain tied to professional settings, but over-the-counter foams and alginates populate shelves alongside first-aid items. Omnichannel strategies that blend institutional contracts with consumer convenience underpin competitive advantage. Vendors investing in logistics and digital marketing secure early mover benefits before the next wave of online penetration sweeps through the advanced wound care management market.

Geography Analysis

North America contributed 36.41% of 2025 revenue, underpinned by broad insurance coverage, specialized clinician density, and extensive NPWT adoption. Bundled payment models reward interventions that cut readmissions, making premium biologics and connected dressings financially attractive. Regulatory pathways are well defined, enabling nimble product introductions. Hospitals leverage integrated wound centers to standardize protocols and monitor outcomes.

Europe exhibits slower but steady growth as public health systems negotiate aggressive price ceilings. The National Institute for Health and Care Excellence continues to publish technology evaluations, and its guidance informs hospital formularies across the region. Ireland’s evidence-linked pricing framework tightens spending but secures patient access to validated innovations. Cold plasma and other novel modalities await additional local evidence before widespread inclusion, moderating near-term acceleration.

Asia-Pacific is the fastest mover with an 8.04% CAGR through 2031, energized by urban diabetes prevalence exceeding 14% in China and India. Public-private hospital build-outs and regulatory harmonization shorten device approval timelines. Japan and South Korea adopt high-end solutions amid aging populations, although reimbursement caps curb volume escalation. Multinational manufacturers partner with domestic distributors to navigate price control mechanisms and regional tender cycles. Despite heterogeneity, the scale of unmet need positions Asia-Pacific as the principal expansion engine within the advanced wound care management market.

The Middle East and Africa advance from a low base. High diabetes rates in Gulf Cooperation Council states support demand, but out-of-pocket payments still limit uptake of high-cost biologics. South Africa anchors Sub-Saharan momentum with expanding private insurance penetration. Supply-chain constraints and workforce gaps temper broader regional progress.

South America is led by Brazil and Argentina, where private hospitals value premium therapies for burns and surgical wounds. Currency volatility and economic cycles influence purchasing power, yet targeted investments in tertiary centers sustain a modest pipeline of device orders. Broader adoption awaits deeper reimbursement alignment and clinician training infrastructure.

Mordor Intelligence provides coverage of the advanced wound care management market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The top five suppliers include Smith & Nephew, Mölnlycke, ConvaTec, Coloplast, and Solventum, giving the sector a moderate concentration profile. Portfolio breadth spanning dressings, devices, and biologics secures preferred-supplier status under bundled tenders. Mölnlycke’s acquisition of a wound-cleansing specialist in March 2025 strengthened vertical integration, adding pre-treatment capability to its dressing line. Smith & Nephew leverages the RENASYS and PICO platforms plus LEAF analytics to lock in multi-year hospital contracts, and double-digit device growth in 2024 demonstrated strategy efficacy.

Niche innovators attack white spaces in sensor dressings and fish-skin matrices. Coloplast’s agreement to acquire Kerecis extended its biologic footprint to 130 additional countries and diversified revenue beyond continence care. Digital capabilities are emerging as a deciding factor; vendors integrating imaging software and remote-monitoring dashboards improve stickiness under value-based purchasing. Commodity foam and gauze segments face private-label encroachment that compresses margins, pushing established brands to emphasize evidence-backed premium lines.

Omnichannel distribution now influences pricing negotiations. E-commerce exposes standard pricing and erodes distributor leverage, while hospital systems demand service bundles, including staff training and inventory optimization. Companies capable of orchestrating institutional, retail, and online touchpoints gain strategic flexibility. As regulation advances and payer models evolve, competitive differentiation will increasingly rest on data-proven outcomes and digital engagement rather than sheer product count within the advanced wound care management market.

Advanced Wound Care Management Industry Leaders

Smith & Nephew

ConvaTec Group PLC

Coloplast A/S

Mölnlycke Health Care AB

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Solventum introduced the V.A.C. Peel and Place Dressing in the United Kingdom, an all-in-one negative-pressure solution applied in under two minutes and wearable for up to seven days.

- January 2026: A surgeon in Texas became the first in the United States to use TYBR Health’s flowable collagen-based B3 GEL System for tissue protection during healing.

- January 2026: Tiger BioSciences acquired Platelet-Rich Fibrin Matrix technology and a proprietary dressing platform from Bahia Medical to expand its regenerative portfolio.

- January 2026: StimLabs launched Allacor P, a human umbilical cord device for acute and chronic wounds, following FDA clearance earlier in 2024.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the advanced wound care management market as the annual revenue generated worldwide from moisture-retentive dressings, bio-engineered skin substitutes, growth-factor gels, and therapy devices such as negative-pressure or hyperbaric systems that treat complex acute and chronic wounds. We track factory-gate sales, government tenders, and distributor invoices.

Scope Exclusion: Products meant only for first-aid (dry gauze, adhesive tapes, cotton pads) remain outside our study.

Segmentation Overview

- By Product

- Advanced Dressings

- Devices & Accessories (e.g., NPWT)

- Grafts & Matrices

- Topical Agents

- By Wound Type

- Surgical & Traumatic Wounds

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Leg Ulcers

- Burns & Other Complex Wounds

- By Technology Platform

- Conventional Passive Dressings

- Antimicrobial/Drug-Eluting Dressings

- Smart Sensor-Integrated Dressings

- Bio-engineered Skin Substitutes

- Negative-Pressure Wound Therapy Systems

- Electrical & Ultrasound Stimulation Devices

- Others

- By Patient Age Group

- Pediatric (0–17 yrs)

- Adult (18–64 yrs)

- Geriatric (65 yrs +)

- By End User

- Hospitals & Ambulatory Surgical Centers

- Home Healthcare Settings

- Long-Term Care & Rehabilitation Facilities

- By Distribution Channel

- Direct Hospital Procurement

- Retail & Specialty Stores

- E-commerce

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Phone interviews and e-mail surveys with wound-care nurses, hospital procurement heads, and regional distributors across North America, Europe, and Asia let us validate prevalence rates, typical selling prices, and device adoption curves, filling gaps that desk research alone cannot close.

Desk Research

Our team starts with freely available datasets from WHO, CDC, OECD Health Statistics, UN Comtrade, and Eurostat, which reveal wound incidence patterns, hospital procedure volumes, and global trade in advanced dressings. We next layer in company 10-K splits, device shipment filings, and guideline updates. Paid resources, such as D&B Hoovers for financials, Dow Jones Factiva for news flow, and Questel for patent intensity, help us size manufacturer pipelines and track competitive launches. The sources named are illustrative; many additional references supported data collection and verification.

Market-Sizing & Forecasting

One workbook links a top-down patient-cohort build with selected bottom-up supplier roll-ups. Key drivers include diabetic foot ulcer prevalence, surgical episode growth, NPWT penetration, hospital ASP trends, reimbursement revisions, and foam-to-film substitution rates. This model delivers a baseline value. Future values through the forecast period are generated with ARIMA projections that are stress-tested against expert consensus and scenario checks.

Data Validation & Update Cycle

Each quarter, an analyst reviews new shipment logs, tender awards, and currency moves, flags anomalies, and reruns scenarios before annual publication. Interim refreshes occur when material events arise, ensuring clients receive an up-to-date view.

Why Mordor's Advanced Wound Therapy Devices Baseline Commands Reliability

Published estimates often diverge because firms choose different product baskets, pricing ladders, and refresh cadences. Open publications place 2025 values between USD 11.76 billion and USD 16.33 billion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 12.14 B | Mordor Intelligence | - |

| USD 11.76 B | Global Consultancy A | Moist dressings only, limited geography |

| USD 13.37 B | Regional Consultancy B | Aggressive ASP growth assumption |

| USD 16.33 B | Trade Journal C | Hospital spend survey extrapolation |

The comparison shows totals swing by over USD 4 billion when scope, pricing progression, or geographic weighting differ. By documenting every assumption and refreshing the model yearly, we deliver a balanced, traceable baseline that decision-makers can depend upon.

Key Questions Answered in the Report

What is the current value of the advanced wound care management market?

The market stands at USD 13.44 billion in 2026 and is forecast to reach USD 18.22 billion by 2031.

Which product segment is growing fastest?

Devices and accessories, particularly negative-pressure systems, are projected to rise at a 9.46% CAGR through 2031.

Why is home healthcare important in wound management?

Reimbursement incentives and portable technologies allow complex wound therapy to continue at home, driving a 10.54% CAGR for the segment.

Which region shows the strongest growth outlook?

Asia-Pacific leads with an expected 8.04% CAGR thanks to high diabetes prevalence and expanding healthcare infrastructure.

How are smart dressings changing care delivery?

Sensor-integrated dressings transmit real-time data that helps clinicians intervene early, reducing readmissions and supporting tele-monitoring programs.

Page last updated on: