Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

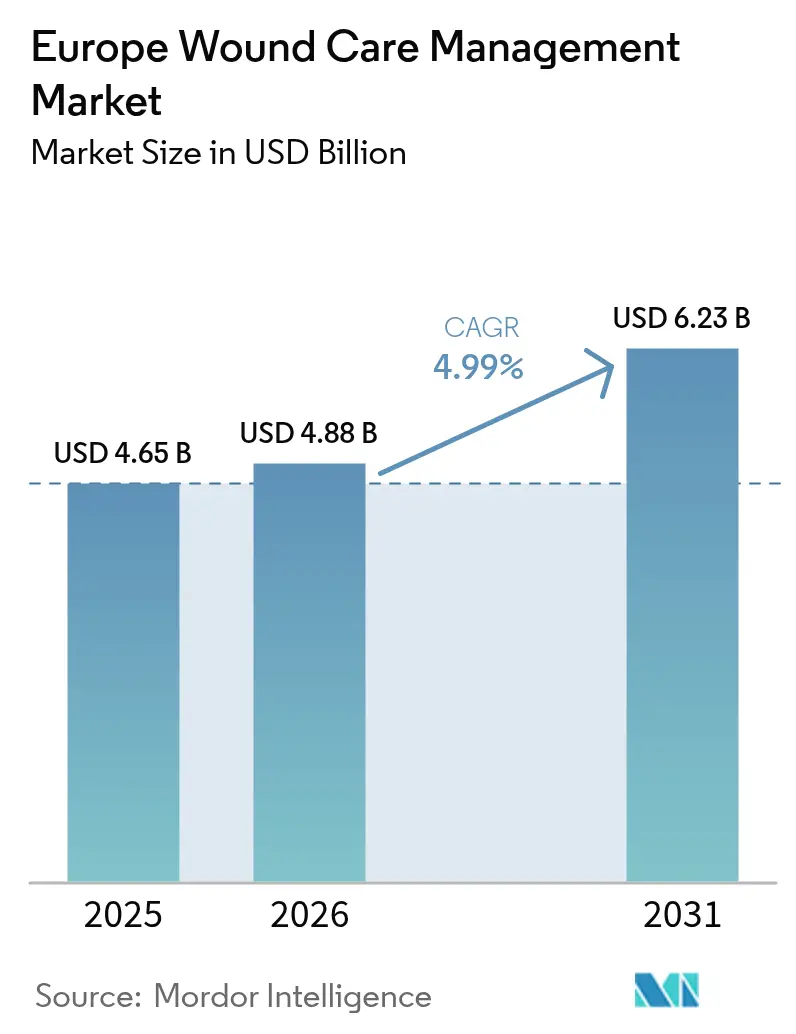

| Base Year Market Size (2025) | USD 4.65 Billion |

| Market Size (2026) | USD 4.88 Billion |

| Market Size (2031) | USD 6.23 Billion |

| Growth Rate (2026 - 2031) | 4.99% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Wound Care Management Market Analysis by Mordor Intelligence

The European wound care management market size was valued at USD 4.65 billion in 2025 and estimated to grow from USD 4.88 billion in 2026 to reach USD 6.23 billion by 2031, at a CAGR of 4.99% during the forecast period (2026-2031). A confluence of rapid population ageing, the diabetes epidemic, and widespread adoption of AI-enabled imaging keeps the European wound care management market on a clear expansion path [1]Nóra Kovács, "Lifestyle and metabolic risk factors, and diabetes mellitus prevalence in European countries from three waves of the European Health Interview Survey," Scientific Reports, nature.com. Growing surgical procedure volumes, tighter regulatory standards under the EU-MDR, and the shift from hospital to home care are reshaping procurement criteria and product design priorities across the European wound care management market. Leading vendors now bundle data-rich dressings with telehealth platforms, helping providers shorten length of stay and lower rehospitalisation rates. While Germany remains the revenue anchor, France outpaces all other countries, driven by favorable reimbursement pilots and strong digital health uptake.

Key Report Takeaways

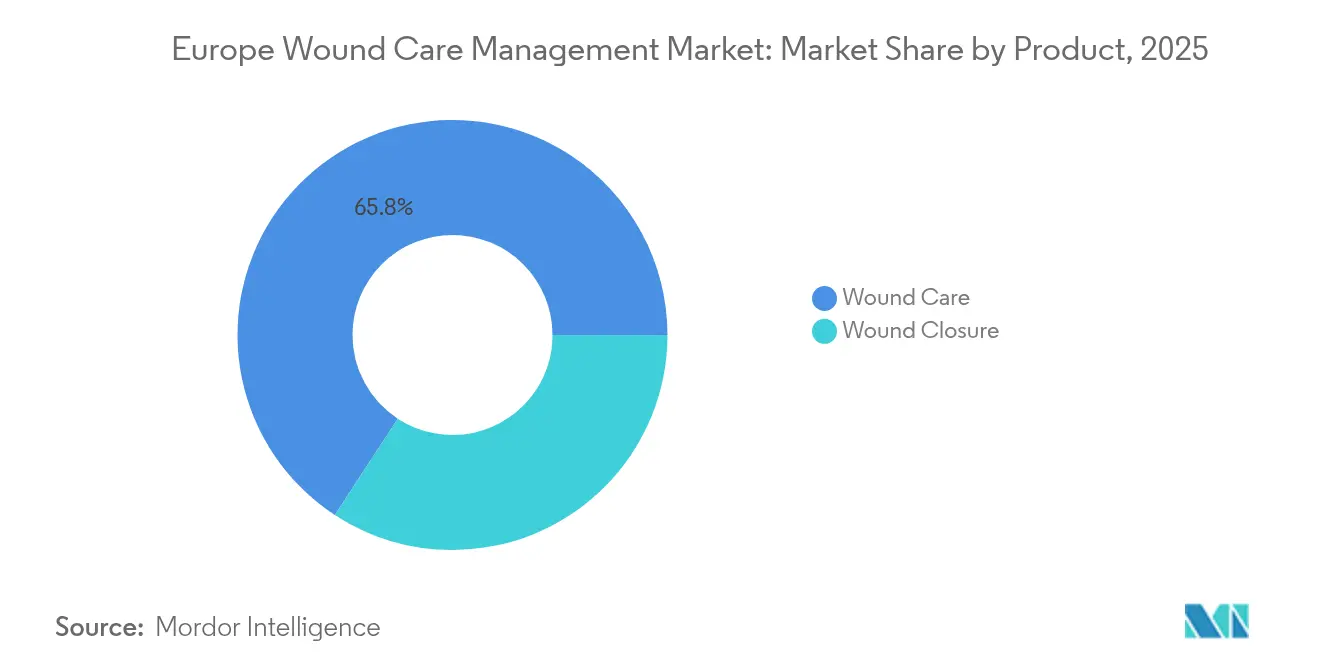

- By product category, wound care products held 65.78% of the European wound care management market share in 2025; wound closure solutions are projected to grow at a 5.72% CAGR through 2031.

- By wound type, chronic wounds accounted for 59.05% of the European wound care management market size in 2025, whereas acute wounds are projected to grow at a 5.63% CAGR through 2031.

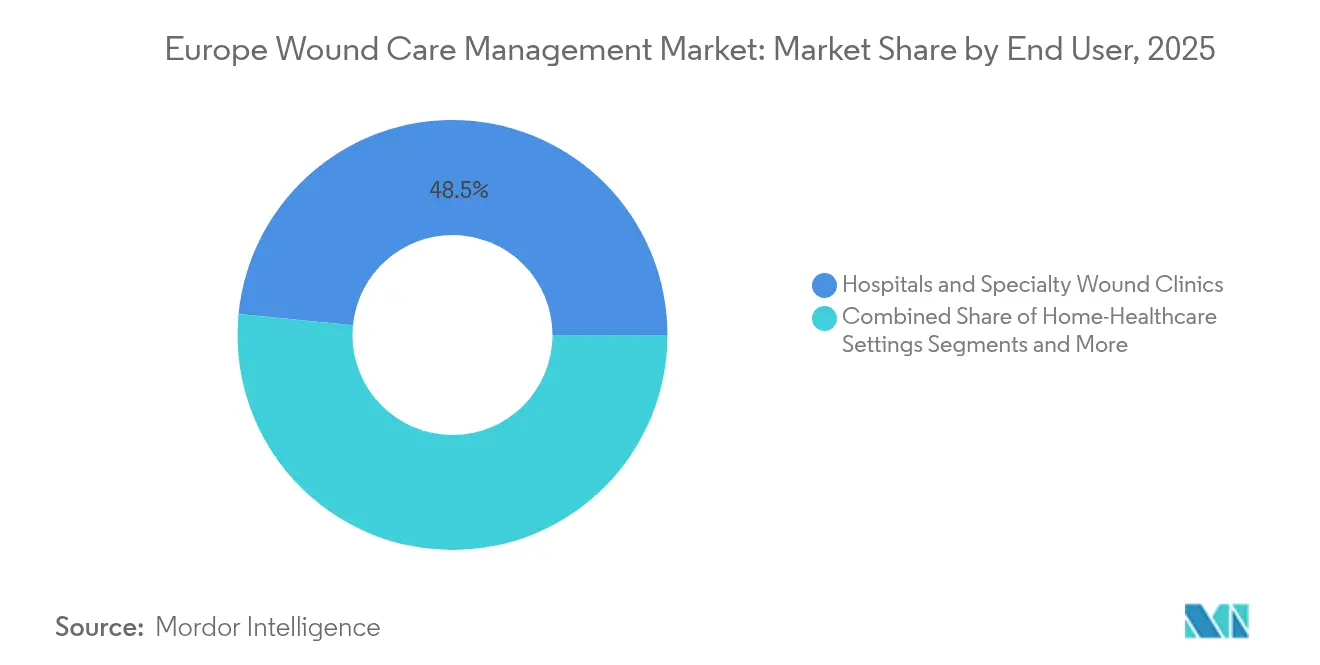

- By end user, hospitals and specialty wound clinics captured a 48.45% revenue share in 2025, while the home healthcare segment is forecast to post the fastest 5.74% CAGR to 2031.

- By mode of purchase, institutional channels dominated with 61.74% of 2025 sales; retail and over-the-counter outlets are expanding at a 5.7% CAGR.

- By geography, Germany accounted for 20.12% of the 2025 revenue; France is the fastest-growing country market, with a 5.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Europe Wound Care Management Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidences of chronic wounds & diabetic ulcers | +1.2% | Pan-European, concentrated in Germany, UK, France | Long term (≥ 4 years) |

| Escalating volume of elective & trauma-related surgeries | +0.8% | Germany, France, Italy, Spain | Medium term (2-4 years) |

| Rapidly ageing European population base | +1.0% | Pan-European, acute in Germany, Italy | Long term (≥ 4 years) |

| Rising prevalence of diabetes & obesity | +0.9% | Eastern & Southern Europe, UK | Long term (≥ 4 years) |

| Adoption of AI-enabled digital wound imaging for precision treatment | +0.6% | Germany, UK, France, Nordic countries | Short term (≤ 2 years) |

| Hospital-to-home shift driving portable NPWT uptake | +0.5% | Germany, UK, France, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing incidences of chronic wounds & diabetic ulcers

Prevalence of diabetes mellitus in EU member states climbed from 7.01% in 2009 to 7.96% in 2019, translating into 61 million adults now living with the condition. Chronic wounds affect 2.21 per 1,000 citizens and carry an average treatment bill of EUR 15,000 (USD 17,476) per diabetic-foot-ulcer patient in Germany, encouraging hospitals to move rapidly toward bioactive dressings and portable NPWT platforms that help compress episode-of-care costs. Real-world data from the Barcelona metro area indicate wound treatment outlays of EUR 34.99 million (USD 40.77 million) over three years, suggesting EUR 1.76 billion (USD 2.05 billion) in national spending for Spain. Socioeconomic disparities exacerbate the burden, as lower educational levels and unemployment are associated with higher ulcer incidence, particularly in Eastern and Southern Europe [2]Miguel Ángel Díaz-Herrera, "The financial burden of chronic wounds in primary care: A real-world data analysis on cost and prevalence," ScienceDirect, sciencedirect.com.

Escalating volume of elective & trauma-related surgeries

Deferred procedures from the pandemic era have pushed surgical caseloads above pre-2020 baselines across top European centres. Robotic, image-guided, and day-surgery pathways shorten hospital stay but demand sophisticated post-operative dressings that can transition safely to home care [3]Anders Wanhainen, "European Society for Vascular Surgery (ESVS) 2024 Clinical Practice Guidelines on the Management of Abdominal Aorto-Iliac Artery Aneurysms," Eur J Vasc Endovasc Surg, portailvasculaire.fr. Average reimbursements for complex tissue transfers range from EUR 5,933 (USD 6,912) for pedicled flaps to EUR 8,517 (USD 9,922) for free flaps across five major economies, underscoring high stakes for reliable closure technologies. Staple-compatible dressings and absorbable sealants are therefore gaining mindshare among theatre managers seeking to curtail operating-room turnover times.

Rapidly ageing European population base

The European Commission projects a sharp upswing in the over-65 cohort, resulting in parallel increases in comorbidities that slow the natural healing process. Health systems already face a shortage of 1.2 million professionals, intensifying reliance on automated wound assessment, tele-mentoring, and longer-wear dressings. WHO Europe reports that 1 in 6 residents still die before 70 from noncommunicable diseases, many needing recurring wound interventions along the care continuum.

Adoption of AI-enabled digital wound imaging for precision treatment

Swift Medical’s Skin & Wound platform surpassed 50 million clinical scans in 2024, confirming demand for objective measurement tools that directly integrate into electronic health record workflows. Devices such as Wound Viewer have lowered per-encounter costs by 35% while boosting healing performance, and the Healico mobile app already supports more than 3,800 clinicians in France and Germany by standardising remote consultations. Rapid uptake of these AI tools is elevating data analytics to a core competitive differentiator within the European wound care management market.

Restraints Impact Analysis of Europe Wound Care Management Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement hurdles for advanced wound care across major EU economies | -0.7% | Germany, France, UK, Italy, Spain | Medium term (2-4 years) |

| High episode-of-care costs versus conventional dressings | -0.4% | Pan-European, acute in cost-sensitive markets | Short term (≤ 2 years) |

| EU-MDR compliance burden squeezing SME margins | -0.6% | Pan-European, disproportionate impact on SMEs | Long term (≥ 4 years) |

| Supply-chain volatility in collagen/alginate raw materials & growing AMR concerns | -0.3% | Pan-European, supply chain dependent regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Reimbursement hurdles for advanced wound care across major EU economies

German statutory insurance data show that 76% of leg ulcer patients depend on older hydroactive or foam dressings, revealing a collision between clinician preference and budget caps. French surveys echo the concern: 89% of caregivers would rather opt for premium therapies, yet formularies limit their freedom of choice. Although economic models demonstrate that NPWT delivers superior long-term savings, high first-invoice prices and fragmented approval pathways hinder penetration, effectively diluting growth prospects for the European wound care management market in price-sensitive regions.

EU-MDR compliance burden squeezing SME margins

The average MDR certificate now takes 18 to 24 months to obtain. It can cost as much as EUR 100,000 (USD 116,505), a figure that is forcing 50% of surveyed manufacturers to shrink their portfolios and threatens the withdrawal of roughly one-third of devices. TEAM-NB reports a backlog of 10,000 unapproved products awaiting notified-body capacity, which extends the time-to-market and concentrates market share in the hands of well-capitalized multinationals. SMEs therefore face rising exit risk, adding consolidation pressure within the European wound care management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Wound Care Management Market Segment Analysis

By Product:

Closure momentum rises beside dominant dressingsWound care products accounted for 65.78% of the European wound care management market share in 2025, driven by hydrofiber, alginate, and antimicrobial dressings that reduce the frequency of changes and infection risk. Hospitals still purchase gauze for basic cases, yet advanced dressings are winning formularies where staff shortages and infection-control metrics drive procurement. Leading portfolios now pair dressings with cloud-connected imaging dashboards, reinforcing loyalty contracts with group purchasing organisations.

Wound closure solutions, although smaller, are set to record a 5.72% CAGR through 2031. Sutures remain theatre stalwarts, but staplers and topical adhesives are quickly gaining traction in minimally invasive segments. Smith+Nephew’s RENASYS pipeline and Solventum’s V.A.C. Peel & Place dressing, which allows seven-day wear, underscore the direction of innovation. Growth prospects hinge on the European wound care management market size for OR-compatible sealants, which could reach over USD 1.6 billion by 2031 under current adoption trends.

By Wound Type:

Chronic complexity still dominates spendChronic wounds accounted for 59.05% of applications in the European wound care management market in 2025, reflecting the high prevalence of diabetes and vascular diseases. Diabetic foot and venous leg ulcers attract intensive resource utilization, with German per-patient expenditures reaching EUR 15,000. Molecular profiling now links down-regulated FGF7 and elevated MMP10 to stalled healing, paving the way for precision topical therapies.

Acute wounds display the fastest 5.63% CAGR, aligned with surging surgical backlogs and trauma admissions. Burns, surgical incisions, and lacerations favour rapid-closure kits and absorbable barrier films, creating scope for hybrid dressings integrating silver or iodine reservoirs. The future addressable Europe wound care management market size for acute indications may reach approximately USD 2.08 billion by 2031 if theatre volumes maintain their 2025 trajectory.

By End User:

Home-care acceleration reshapes channel mixHospitals and specialty clinics retained 48.45% of sales in 2025; however, staffing gaps and bed-capacity strain encourage earlier discharge, routing complex cases to outpatient settings, where AI triage tools help sustain quality benchmarks. Academic medical centres operate as testbeds for sensor-enabled dressings that transmit moisture and temperature data to wound-care teams.

Home healthcare, expanding at a 5.74% CAGR, anchors the future of the European wound care management market. Portable NPWT units, such as Avance Solo and Avelle, demonstrate equal efficacy to inpatient pumps while reducing episode costs by up to USD 8,500. Tele-nursing platforms now coach family caregivers through routine dressing changes, and reimbursement pilots in France and the Netherlands validate payment models for remote monitoring subscriptions.

By Mode of Purchase:

Institutions lead as retail gains tractionInstitutional buyers secured 61.74% of the product flow in 2025, leveraging bulk tendering and total-cost-of-ownership scoring matrices. Deals increasingly cover multi-year service wraps that bundle clinician training, inventory analytics, and predictive maintenance for NPWT pumps.

Retail and OTC outlets are growing at a 5.7% CAGR, driven by diabetic self-care and the expansion of pharmacy-based clinical services across Germany and the UK. Consumer-grade advanced dressings with clear-window technology illustrate how vendors reposition hospital-proven materials for everyday buyers. If the European wound care management market size for retail channels continues to grow at its current pace, direct-to-consumer platforms could reach USD 965 million by 2031.

Geography Analysis

Germany Wound Care Management Market

Germany commanded 20.12% of revenue in 2025, underpinned by a mature reimbursement framework and a 30,000-strong certified wound-nurse workforce. Hydroactive dressings cover three-quarters of leg ulcer cases. At the same time, the adoption of portable NPWT is experiencing double-digit growth, reinforcing the nation’s status as the reference market for pan-European rollouts. Medical-device exports safeguard price elasticity, enabling German suppliers to cross-subsidise compliance costs and keep catalogue breadth intact.

France Wound Care Management Market

France is the breakout growth engine, expected to post a 5.17% CAGR through 2031, fuelled by telehealth penetration and progressive home-care reimbursement pilots for NPWT with instillation. Digital platform Healico’s widespread adoption sharpens data sharing between community nurses and hospital specialists, shortening referral windows and enhancing adherence. The regulatory climate supports ahead-of-curve deployment of AI imaging under sandbox guidelines, accelerating innovation within the European wound care management market.

Broader European Markets

The United Kingdom emphasizes cost-effectiveness through NICE guidance, triggering widespread formularies for antimicrobial foams and atraumatic silicone dressings. Italy’s regionalized healthcare service results in patchy adoption rates; northern provinces exhibit uptake comparable to Germany, whereas southern regions still rely heavily on traditional gauze. Spain bears a EUR 1.76 billion chronic-wound burden, prompting autonomous communities to pilot value-based procurement schemes. Nordic countries showcase the highest per-capita spend as e-health platforms link municipal caregivers with tertiary centers in near real-time, and Eastern Europe prioritizes lower-cost alginate dressings while upgrading supply-chain transparency to satisfy EU-MDR traceability clauses. Collectively, these dynamics indicate a European wound care management market that, although unified by regulation, remains heterogeneous in terms of adoption pace and care-delivery models.

Competitive Landscape

Competition is moderate. Smith+Nephew delivered 5.3% underlying revenue growth in 2024 and reported nearly 12.2% expansion in Advanced Wound Management during Q4, thanks to the PICO and RENASYS portfolios. HARTMANN booked EUR 608.9 million (USD 649.5 million) in wound-care revenue at 4.4% organic growth, leveraging entrenched distributor arrangements and clinician education modules. Mölnlycke extended its community-care footprint through the single-use Avance Solo NPWT system, bundling remote-monitoring APIs for district nurses.

Strategic acquisitions complement organic expansion. Merit Medical paid USD 120 million for Biolife’s haemostatic portfolio, granting exposure to high-margin surgical-bleed control niches. Healiva acquired cell-therapy assets from Smith+Nephew, signaling momentum toward personalized regenerative solutions. Smaller innovators capture white space: SolasCure secured FDA Fast Track designation for its Aurase enzymatic gel, while Kerecis’ fish-skin matrix demonstrated superior outcomes in Scandinavian trials for diabetic foot ulcers.

Supply-chain digitisation is now decisive. European device makers spend up to 20% of revenue on logistics, prompting a shift to predictive demand-planning and regional raw-material sourcing. Firms redirect 3-5% of annual revenue into supply-chain analytics to counter inflation and geopolitical risk, strengthening resilience across the Europe wound care management market. MDR hurdles are simultaneously thinning the long-tail of micro-vendors, nudging the sector toward higher concentration even as newcomers carve digital niches.

Europe Wound Care Management Industry Leaders

-

ConvaTec Group PLC

-

Smith & Nephew

-

Coloplast AS

-

Medtronic

-

Solventum

- *Disclaimer: Major Players sorted in no particular order

Europe Wound Care Management Market Companies Covered in this Report

- Solventum

- Smiths Group

- Molnlycke Health Care

- Coloplast

- Hartmann Group

- B. Braun

- Cardinal Health

- ConvaTec Group plc

- Medtronic

- Johnson & Johnson

- Essity AB (BSN medical)

- Lohmann & Rauscher GmbH

- Baxter

- Acelity LP Inc. (KCI)

- Medela

- Integra LifeSciences Corp.

- Organogenesis Holdings

- Urgo Medical

- Derma Sciences (Integra)

- Advanced Medical Solutions Group

Recent Industry Developments in Europe Wound Care Management Market

- April 2025: Convatec confirms an initial German launch of ConvaNiox, a nitric-oxide antimicrobial dressing focused on diabetic-foot ulcers.

- March 2025: Mérieux Equity Partners acquires a majority stake in German manufacturer Curea Medical to expand its advanced-dressing footprint.

- March 2025: SolasCure enrolled the first patient in its Phase II CLEANVLU2 trial for Aurase Wound Gel, an enzymatic treatment.

- December 2024: Belluscura entered a joint venture with Separation Design Group and a major medical-device company to explore oxygen-based wound-care solutions.

Europe Wound Care Management Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the European wound management market as the annual sales value of devices and dressings that actively treat or close acute or chronic skin lesions, including film, foam, alginate, and antimicrobial dressings, negative-pressure systems, sutures, staplers, tissue adhesives, and sealants, supplied to hospitals, long-term facilities, pharmacies, and home-care channels across 32 continental and UK markets.

Scope exclusions include services such as nursing time, inpatient bed costs, home-health contracts, and purely pharmaceutical topical antibiotics, which are outside this valuation.

Segments Covered in This Report

-

By Product

-

Wound Care

-

Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

-

Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Topical Agents

- Other Wound Care Products

-

Dressings

-

Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

-

Wound Care

-

By Wound Type

-

Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

-

Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

-

Chronic Wounds

-

By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

-

By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

-

By Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interview European wound-care nurses, purchasing managers, hospital biomaterials chiefs, and distributors in Germany, the United Kingdom, France, Italy, Spain, and the Nordics. These conversations validate average selling prices, gauge home-care penetration, and test the realism of growth drivers uncovered in secondary work.

Desk Research

We start with structured reviews of open datasets issued by bodies such as Eurostat, the OECD Health Statistics portal, the International Diabetes Federation, and national ministries of health, which reveal procedure volumes, ulcer prevalence, and aging population curves. Trade associations like EWMA and MedTech Europe supply import-export and reimbursement updates, while peer-reviewed journals help our analysts benchmark healing timelines and adoption rates for advanced dressings. Company filings, investor decks, and CE-mark approval databases round out the evidence base. D&B Hoovers and Dow Jones Factiva give us verified financials and news that signal pricing shifts. The sources listed are illustrative; many others were queried to cross-check figures and fill contextual gaps.

Market-Sizing & Forecasting

A top-down build begins with procedure counts, diabetic foot prevalence, and pressure injury incidence, which are then multiplied by clinically accepted treatment episodes and device utilization ratios. Results are reconciled with selective bottom-up supplier roll-ups and channel checks to refine totals. Key variables like average length of therapy with NPWT, dressings per ulcer, currency-adjusted ASP shifts, and EU MDR compliance surcharges inform our five-year multivariate regression forecast. Where hospital surveys yield partial data, we interpolate using country-level reimbursement ceilings before triangulating against import statistics.

Data Validation & Update Cycle

Each model passes an anomaly screen, a peer review, and a senior analyst sign-off. We refresh every twelve months, re-running the variance checks after material events such as reimbursement code changes or mid-year vendor price lists.

How Mordor Intelligence's Europe Wound Care Management Market Size Compares to Other Published Estimates

Published estimates often diverge because firms select different product baskets, base years, and currency deflators, leaving buyers unsure which figure to trust.

Key gap drivers include whether traditional gauze and hospital service spend are counted, how aggressively future ASP erosion is assumed, and the speed at which home care demand is layered into projections. Mordor keeps to devices only, uses blended ASPs verified on the ground, and refreshes annually, whereas others may mix service revenue, apply list prices, or roll forward earlier data for several years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.65 B (2025) | Mordor Intelligence | - |

| USD 5.80 B (2023) | Regional Consultancy A | Includes Turkey and select Middle East sales; older base year retained |

| USD 7.57 B (2025) | Global Consultancy A | Adds traditional consumables and home nursing fees; list price ASPs |

| USD 5.80 B (2024) | Trade Journal B | Focuses on advanced dressings only, omits closure devices |

Taken together, the comparison shows that when scope creep, price assumptions, and refresh cadence are normalized, Mordor's disciplined, device-only approach offers decision-makers a transparent, reproducible baseline they can rely on for strategic planning.

Key Questions Answered in the Report

What is the current size of the Europe wound care management market?

The market is valued at USD 4.88 billion in 2026 and is projected to reach USD 6.23 billion by 2031.

Which country leads revenue in Europe’s wound-care device space?

Germany holds the top spot with 20.12% of 2025 sales thanks to strong clinical infrastructure and early adoption of advanced therapies.

Which segment is growing fastest within the Europe wound care management market?

Wound closure solutions, driven by staplers and tissue adhesives, are projected to grow at a 5.72% CAGR through 2031.

Why is home healthcare important for wound-care growth?

Home-based care enables cost savings, addresses workforce shortages and supports patient comfort, pushing portable NPWT and tele-wound platforms to a 5.74% CAGR.

How does EU-MDR affect device makers?

Certification now takes up to 24 months and can cost EUR 100,000, prompting many SMEs to trim portfolios and causing a potential 33% device withdrawal.

What role does AI play in wound management?

AI-driven imaging platforms standardise measurements, cut assessment time and feed data into treatment algorithms, improving healing outcomes and lowering total care costs.

Page last updated on: