Europe Advanced Wound Care Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

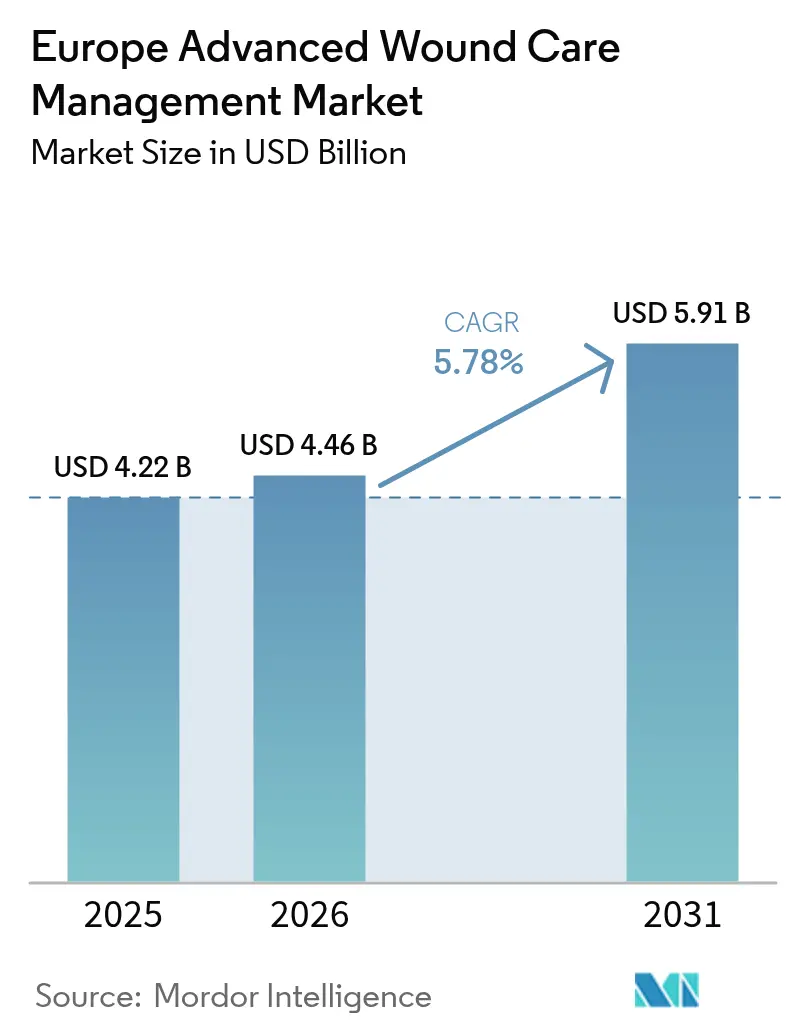

| Base Year Market Size (2025) | USD 4.22 Billion |

| Market Size (2026) | USD 4.46 Billion |

| Market Size (2031) | USD 5.91 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Advanced Wound Care Management Market Analysis by Mordor Intelligence

The Europe advanced wound care management market size in 2026 is estimated at USD 4.46 billion, growing from 2025 value of USD 4.22 billion with 2031 projections showing USD 5.91 billion, growing at 5.78% CAGR over 2026-2031. Healthy demand stems from growing chronic disease incidence, supportive reimbursement reforms, and rapid uptake of evidence-based technologies that shorten healing cycles while lowering readmissions. Technology convergence across biomaterials, negative-pressure platforms, and real-time analytics is accelerating product differentiation, while hospital budget pressures push clinicians toward solutions with verifiable total-cost-of-care reductions. Demographic ageing and steadily climbing surgical volumes intensify the clinical imperative for faster, infection-free recovery, reinforcing sustained investment in product innovation and integrated care pathways across the Europe advanced wound care management market.

Key Report Takeaways

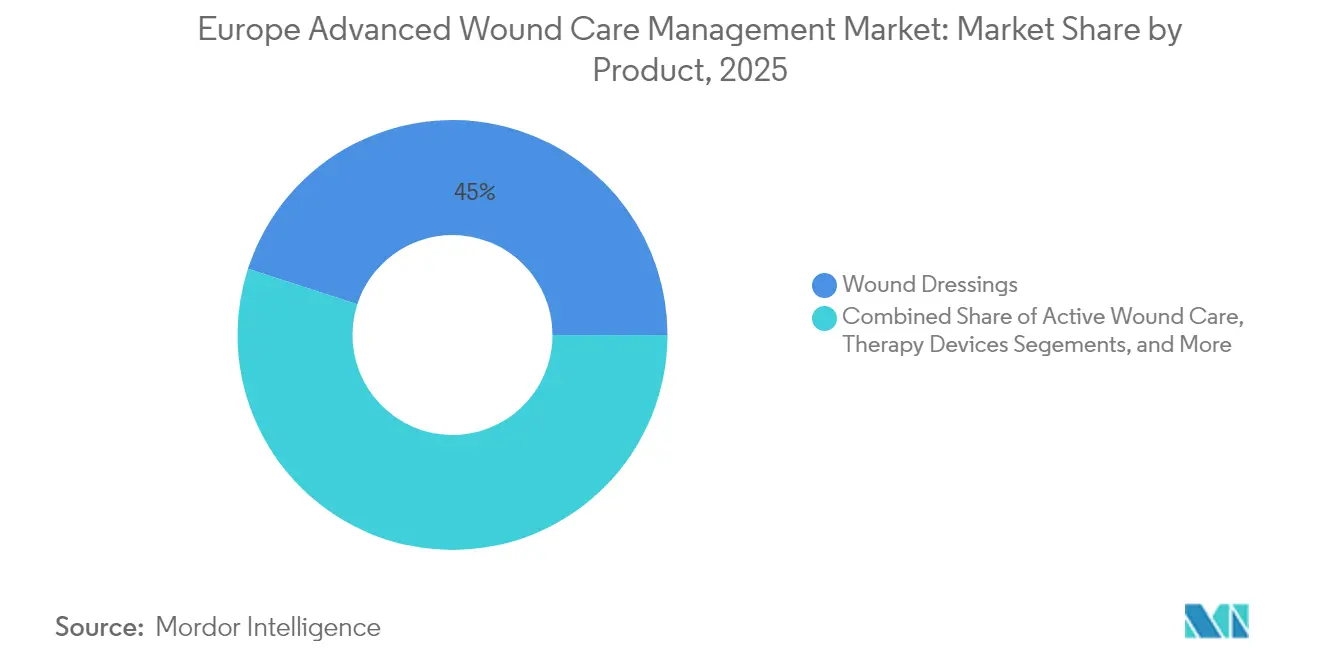

- By product type, wound dressings led with 45.02% of the Europe advanced wound care management market share in 2025, whereas therapy devices are forecast to expand at a 6.61% CAGR to 2031.

- By wound type, chronic wounds accounted for 57.41% share of the Europe advanced wound care management market size in 2025, while acute wounds post the fastest growth at 6.82% CAGR through 2031.

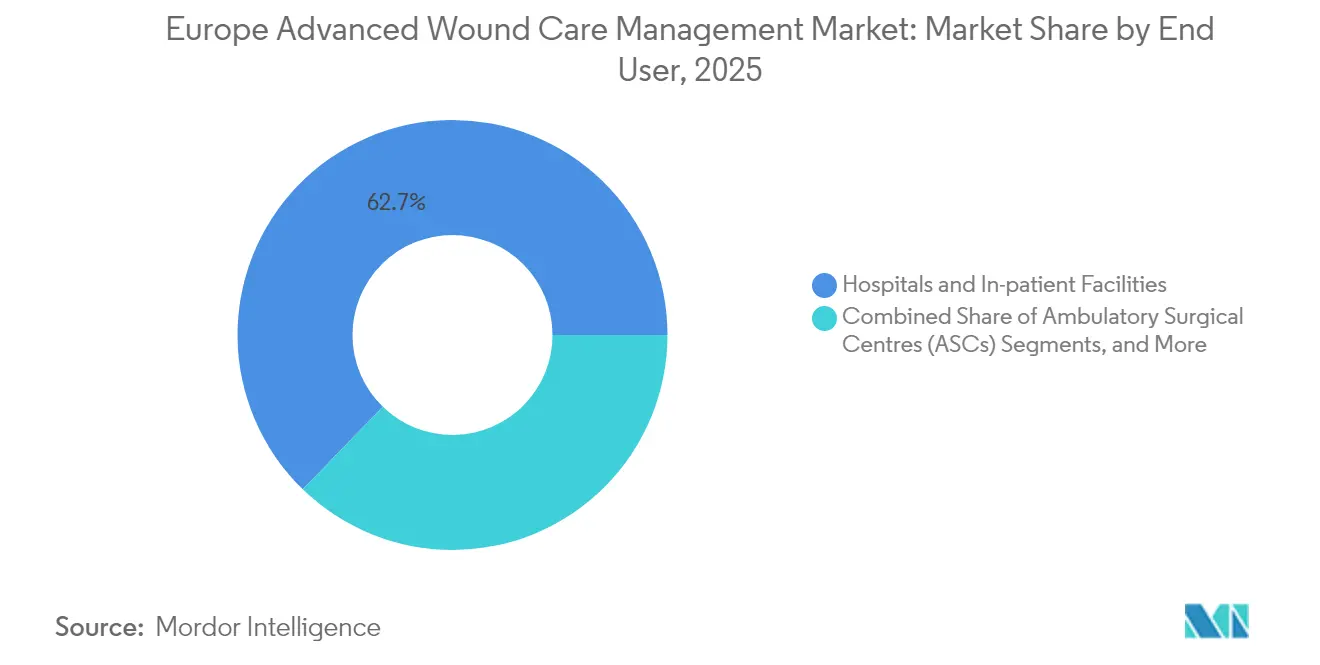

- By end user, hospitals held 62.74% of the Europe advanced wound care management market share in 2025; home-care settings record the highest projected CAGR at 6.55% during 2026-2031.

- By geography, Germany commanded 22.41% of regional revenue in 2025, whereas the United Kingdom is projected to grow the quickest at 7.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on advanced wound care management market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Advanced Wound Care Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidences of chronic wounds & diabetic ulcers | +1.8% | EU-wide, concentrated in Eastern & Southern Europe | Long term (≥ 4 years) |

| Rising geriatric population base in Europe | +1.4% | Western Europe primary, spreading to Central Europe | Long term (≥ 4 years) |

| Increase in volume of surgical procedures | +1.2% | Germany, France, UK leading adoption | Medium term (2-4 years) |

| Technological advances in NPWT & bio-engineered dressings | +1.0% | Nordic countries, Germany, Netherlands early adopters | Medium term (2-4 years) |

| Growing technological advancements | +0.8% | Technology hubs: Germany, UK, Switzerland | Short term (≤ 2 years) |

| Increasing demand for faster recovery of wounds | +0.6% | Urban centers across major EU markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Incidences of Chronic Wounds & Diabetic Ulcers

Chronic wounds affect 2.21 per 1,000 population across Europe and impose sizable fiscal pressure on care systems. Spain’s primary care network alone spent EUR 34,991,854 on chronic wound management over three years, of which treatment materials accounted for EUR 8,455,787 [1]Maria T. Olivera, “Clinical and Economic Burden of Chronic Wounds in Primary Care,” ScienceDirect, sciencedirect.com. Diabetic foot ulcers show 6.3% prevalence among diabetic patients and cost the NHS close to GBP 7,800 per case. These metrics prompt large-scale clinical adoption of advanced dressings and negative-pressure devices that close wounds faster and cut downstream expenditure. Consequently, demand for innovative modalities keeps expanding in the Europe advanced wound care management market as payers embrace value-based coverage structures that reward proven healing outcomes.

Rising Geriatric Population Base

Older Europeans face higher rates of pressure ulcers, venous insufficiency, and delayed tissue repair, spurring sustained need for sophisticated wound solutions. Governments align elderly-care strategies with effective wound prevention and treatment to lower hospitalization days and preserve independence. Countries with mature social insurance platforms reimburse advanced dressings more readily, helping clinicians deploy moisture-managing foams, collagen matrices, and antimicrobial films at earlier care stages. This demographic tailwind secures a long-run growth pillar for the Europe advanced wound care management market amid ageing curves that remain steep.

Increase in Surgical Procedures Volume

Elective and trauma surgeries continue to rebound, lifting demand for prophylactic closure technologies that curb infection and accelerate recovery timelines. Negative-pressure systems incorporated immediately post-operation have proven to shrink application time by 61% and trim costs 41% through extended wear capabilities. Large surgical centers formalize advanced protocols that include bioactive dressings, pushing suppliers to demonstrate ease of use and workflow efficiency. Higher throughput expectations reinforce technology upgrades across orthopedic, cardiovascular, and oncology theaters, adding new revenue layers to the Europe advanced wound care management market.

Technological Advances in NPWT & Bio-engineered Dressings

Smart dressings with embedded pH, temperature, and moisture sensors transition from pilot projects to routine clinical evaluation, giving caregivers real-time insight into wound status. Bioelectrically activated bandages reached 99.75% closure rates versus 94.00% for conventional options in recent trials [2]Stephen G. Thomas, “Bioelectrical Dressings for Chronic Ulcer Closure,” MDPI, mdpi.com. Meanwhile, collagen, chitosan, and hyaluronic-acid dressings meet both healing and environmental criteria due to biodegradability advantages. Artificial-intelligence triage tools guide therapy selection but must comply with GDPR, requiring strong data-governance assurances. Collectively, these advances intensify competitive differentiation inside the Europe advanced wound care management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High treatment costs for advanced modalities | -1.2% | Cost-sensitive markets: Eastern Europe, Southern Europe | Medium term (2-4 years) |

| Fragmented & inconsistent reimbursement across EU-27 | -0.8% | Cross-border care regions, smaller EU markets | Long term (≥ 4 years) |

| Supply-chain constraints on collagen/alginate inputs due to new environmental rules | -0.6% | Manufacturing hubs: Germany, Netherlands, Denmark | Short term (≤ 2 years) |

| Slow uptake of AI-driven wound assessment owing to GDPR-linked data-privacy hurdles | -0.4% | Technology-forward markets: Nordic countries, Germany, Netherlands | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

High Treatment Costs for Advanced Modalities

Premium pricing restricts access in cost-sensitive markets, where individual claims for bioengineered skin substitutes can exceed USD 1 million [3]Summit Re, “Cost Trends in Bioengineered Skin Substitutes,” summit-re.com . Payers experiment with outcomes-based contracts that refund only when predefined healing milestones are reached, but adoption remains uneven. Start-ups face funding gaps until robust real-world evidence substantiates cost-effectiveness, slowing introduction of breakthrough solutions. These fiscal pressures temper uptake across parts of the Europe advanced wound care management market despite strong clinical merit.

Fragmented & Inconsistent Reimbursement Across EU-27

Identical dressings may receive divergent coverage decisions between adjoining member states, complicating launch sequencing and physician education. Limited harmonization also disrupts cross-border care initiatives because clinicians cannot rely on uniform product formularies. Manufacturers allocate incremental regulatory resources to secure approvals and navigate multiple health-technology assessments, translating into longer commercialization cycles and higher overhead. Such fragmentation moderates growth in the Europe advanced wound care management market, especially for novel device classes reliant on volume to reach scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Dressings Dominate Despite Device Innovation

Wound dressings accounted for 45.02% of the Europe advanced wound care management market share in 2025, underscoring their central role in daily clinical protocols across settings. This segment’s resilience reflects the wide availability of foam, hydrogel, and antimicrobial film formats that provide moisture balance, microbial control, and patient comfort. Foam and silicone-coated super-absorbent variants gain ground because they prevent maceration during extended wear. Collagen and alginate alternatives, valued for regenerative properties, regain clinician interest as environmental regulations favor natural polymers. Although dressings maintain the largest revenue contribution, therapy devices are projected to expand at a 6.61% CAGR through 2031, propelled by portable negative-pressure systems and bioactive platforms with integrated sensors.

Device providers highlight evidence of faster closure and shortened nursing time to justify higher capital expense. New disposable-canister NPWT lines enable cost-effective deployment in community care, while emerging ultrasound-based debridement units show promise in stubborn biofilm disruption. Vendors co-develop clinical pathways with hospital networks to embed protocols and lock in longer term contracts. Active wound care products such as growth factors and skin substitutes claim a niche but premium share, and their uptake depends on successful value-based reimbursement pilots. Sustained research funding and clinician training continue to shape adoption curves inside the Europe advanced wound care management industry, keeping competitive pressure high on both dressings and devices.

By Wound Type: Chronic Care Complexity Drives Innovation

Chronic wounds held 57.41% of the Europe advanced wound care management market share in 2025 thanks to the heavy burden of diabetic foot ulcers, venous leg ulcers, and pressure ulcers. Diabetic ulcers alone cost EUR 4,888 per patient and last 194 days when hospitalization is needed. Chronic-wound management protocols rely on multilayer compression, antimicrobial foams, and enzymatic debriding agents, but growing use of NPWT and bioengineered tissues aims to shorten recovery and avert amputations. The Europe advanced wound care management market size for chronic ulcers is forecast to post a 5.55% CAGR, supported by multidisciplinary diabetic-foot centers and digital-monitoring platforms that flag early deterioration.

Acute wounds are poised for 6.82% CAGR through 2031, fueled by rebounding elective surgeries and trauma cases that demand infection prevention and rapid closure. Prophylactic NPWT post-orthopedic or cardiothoracic surgery is increasingly routine, and combined hemostatic plus antimicrobial dressings accelerate epithelialization. Burn units adopt spray-on skin formulations and bioactive scaffolds to minimize grafting. As surgical wards benchmark key performance indicators such as stay length and cosmetic outcome, advanced dressings become integral to enhanced-recovery pathways across the Europe advanced wound care management market.

By End User: Home Care Transformation Accelerates

Hospitals remained the prime purchasers with 62.74% revenue share in 2025, reflecting concentrated expertise and inventory requirements for complex cases. Larger university centers deploy wound-specialist nurse teams and maintain formularies spanning dressings, NPWT pumps, and enzymatic debriders to manage severe chronic ulcers and post-surgical sites. Hospitals also pilot predictive analytics that flag non-healing wounds, guiding early escalation to advanced devices. Nevertheless, home-care settings record the fastest 6.55% CAGR, steered by payer policies to shift routine dressing changes outside expensive inpatient environments. Insurers reimburse portable pumps, and telehealth portals transmit real-time images for clinician oversight. The Europe advanced wound care management market size for home settings is projected to grow from USD 1.17 billion in 2025 to USD 1.71 billion by 2031 as providers scale remote wound-monitoring programs.

Integrated care pathways linking hospital discharge planning with community nursing lower readmission risk and free bed capacity. Technology vendors bundle devices, consumables, and software dashboards for subscription fees aligned with outcomes. Despite 76% of referrals denying home health in 2022, referral volume grew 11% since 2020, indicating unmet demand and room for service expansion. The Europe advanced wound care management industry increasingly revolves around multi-setting continuity, encouraging innovations that function seamlessly from acute wards to patient homes.

Geography Analysis

Germany captured 22.41% of the Europe advanced wound care management market in 2025, enabled by strong reimbursement, a dense network of wound centers, and early adoption of silicone super-absorbent dressings that boosted PAUL HARTMANN’s wound division to EUR 608.9 million revenue that year. German payers rely on meticulous health-technology assessment, so suppliers emphasize randomized trials and real-world registries to secure formulary listings. Collaboration between industry and university hospitals nurtures product co-development, while state-level public health programs subsidize home-based NPWT rentals for post-discharge care.

The United Kingdom, although navigating post-Brexit regulatory realignment, at a 7.08% CAGR through 2031 becomes the fastest-growing part of the Europe advanced wound care management market. New UKCA marking and the UK Responsible Person framework lengthen approval cycles yet give local manufacturers clearer guidance. NHS wound spend hits GBP 8.3 billion annually, spurring procurement bodies to trial outcome-linked contracts that substitute high-performance dressings for frequent conventional changes. Community nurse shortages intensify reliance on advanced devices with longer wear times, accelerating technology rotation despite fiscal constraints.

France, Italy, and Spain remain key contributors, each shaped by unique funding and regional autonomy. France’s centralized payer negotiates list prices aggressively but funds advanced therapy when cost-effectiveness is proven. Italy’s regional procurement can create heterogeneous access, encouraging companies to pilot region-specific care models. Spain’s three-year chronic wound cost of EUR 34,991,854 underscores the financial rationale for adopting therapies that shorten healing. Elsewhere, Scandinavian markets, though smaller, act as early adopters of sensor-embedded dressings and AI triage due to robust digital infrastructure. Eastern European countries, guided by EU cohesion funds, upgrade surgical wards and gradually scale advanced dressing budgets, presenting long-run upside for the Europe advanced wound care management market.

Regulatory Landscape

Advanced wound care products marketed in Europe (including advanced dressings, active wound care products, and therapy devices such as NPWT systems) fall under Regulation (EU) 2017/745 (EU MDR). Access depends on CE marking via Notified Bodies and ongoing post-market obligations, with compliance efforts supported by EUDAMED modules as they come online. The MDR transition timetable extended by Regulation (EU) 2023/607 remains a central compliance anchor for legacy portfolios, with deadlines of December 31, 2027 for higher-risk classes (including Class III and Class IIb implantables) and December 31, 2028 for Class IIb non-implantables, Class IIa, and certain Class I devices (sterile/measuring/up-classified). These dates continue to shape recertification sequencing for multi-country commercialization.

In 2026, the European Commission adopted delegated acts expanding the list of Well-Established Technologies (WET), including certain wound and soft-tissue device types. For eligible products, this can reduce parts of the clinical evidence and technical documentation burden under MDR pathways. Separately, a December 2025 European Commission legislative proposal to amend MDR/IVDR to streamline processes remains in the legislative cycle, so manufacturers are still planning around current MDR requirements, notified-body capacity, and country-level reimbursement and health-technology assessment decisions that influence adoption after CE marking.

Value Chain Analysis

The value chain starts with raw materials and intermediates used across advanced dressings and devices, including polymers, silicones and adhesives, absorbent layers, antimicrobials, and biologic or natural inputs such as collagen and alginates. It then moves through converting, sterilization, and packaging under medical-device quality systems. Finished products are supplied via direct tenders to hospitals and group purchasing bodies, distributor networks for smaller providers, and home-care channels where portable NPWT and longer-wear dressings are dispensed with training and follow-up. Digital documentation and remote wound assessment workflows are increasingly supporting these routes.

Manufacturers are tightening sourcing and strengthening manufacturing resilience in Europe while maintaining downstream availability. For instance, Lohmann & Rauscher acquired a 49% stake in Portugals ADA Group in January 2025 to strengthen European delivery capability for disposables that complement wound-care regimens. On the innovation-to-market path, companies increasingly rely on evidence-led approaches, using multi-center clinical programs to support CE marking under MDR and to support national reimbursement and formulary placement, as reflected by major portfolio updates and pipeline showcases at EWMA 2026 (Bremen), alongside investments and partnerships that support scaling, training, and product availability across multiple care settings.

Competitive Landscape

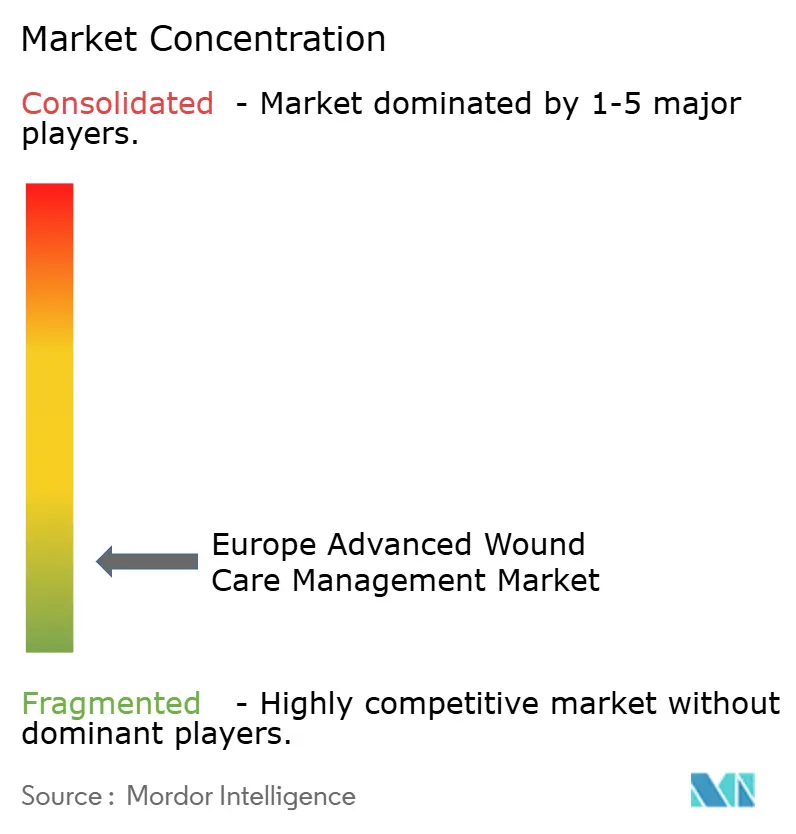

The Europe advanced wound care management market is moderately fragmented, with the top tier of Smith+Nephew, ConvaTec, Mölnlycke, and PAUL HARTMANN vying through broad portfolios and continuous R&D. ConvaTec posted 6.7% organic wound-segment growth in H1 2024, buoyed by Aquacel Ag+ Extra and InnovaMatrix launches that offered demonstrable biofilm reduction and faster epithelial coverage. Mölnlycke leverages proprietary Safetac silicone technology across Mepilex dressings, maintaining clinician loyalty through low-trauma removal and robust clinical dossiers.

Regulatory hurdles under EU MDR raise costs for smaller firms, prompting alliances with contract-research organizations and notified bodies that streamline file compilation. Suppliers integrate smart-monitor patches and cloud dashboards, often via partnerships with MedTech software specialists, to differentiate commoditizing dressings. Sustainability also gains prominence as hospitals embrace green procurement: Mölnlycke’s plant in Apeldoorn migrated to 100% renewable electricity in 2024, targeting Scope 3 emissions reductions. Mid-sized players such as Urgo Medical and Lohmann & Rauscher emphasize specialized offerings like contact-layer dressings and compression systems, exploiting niches not fully covered by multinationals.

Digital-first entrants apply AI to wound-image classification, providing decision support that standardizes staging and product selection. They collaborate with device vendors to embed algorithms inside secure mobile apps compliant with GDPR. Larger incumbents acquire or license such platforms to enrich service bundles. Procurement trends shift toward outcome guarantees: ConvaTec and several NHS trusts piloted pay-for-performance agreements in 2024 that tie reimbursement to predefined healing metrics. These collaborative frameworks are reshaping competitive dynamics in the Europe advanced wound care management market and reward companies able to couple device efficacy with data-driven proof.

Europe Advanced Wound Care Management Industry Leaders

Coloplast AS

ConvaTec Group PLC

Smith & Nephew

Integra Lifesciences

Paul Hartmann AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One clear whitespace in Europe is at the intersection of standardized, evidence-based surgical incision management and procurement models that pay for fewer complications rather than higher volumes of dressing changes. The July 2026 German expert consensus on single-use negative pressure wound therapy (sNPWT) in closed surgical incisions provides a risk-based framework that supports protocolization in high-volume surgical centers. This helps hospitals adopt prophylactic NPWT more consistently, align purchasing to defined patient-risk segments, and connect products to measurable outcomes within enhanced-recovery pathways.

Manufacturing localization and capacity additions across Europe are also creating room for suppliers that can serve multi-country tenders and home-care growth with fewer stock-out risks. In 2026, Convatec completed a GBP 24 million expansion of its Rhymney, South Wales site to strengthen supply of Hydrofiber wound-care material, and Mölnlycke announced a EUR 40 million investment across facilities in Mikkeli (Finland) and Oldham (UK) to increase wound-care manufacturing capacity and optimize production. At the same time, the MDR compliance bar keeps entry selective, which raises the commercial value of CE-marking readiness, clinical evidence generation, and partnerships that bridge innovators to scale, including funding aimed at completing clinical trials and finalizing CE marking for new dressing technologies.

Recent Industry Developments

- July 2026: Convatec completed a GBP 24 million expansion of its Rhymney, South Wales manufacturing site to strengthen supply of advanced wound care solutions based on its Hydrofiber technology. The additional capacity supports higher-volume fulfillment for hospital and community-care channels and reinforces European manufacturing as a supply anchor for global distribution.

- June 2026: Kerecis (Coloplast) expanded insurance coverage for its intact fish-skin graft products, adding 40 million covered lives. Broader payer coverage improves affordability and prescribing confidence for biologic graft options used in hard-to-heal wounds and supports scale-up of advanced biologics within treatment pathways.

- July 2024: Sonoma Pharmaceuticals expanded its European distributor network by partnering with Smart Healthcare Company (SHC) s.r.o. to distribute Microdacyn60 wound care products in Ukraine. The move broadened regional reach through local distribution infrastructure, improving availability in an in-scope European market where continuity of supply is critical for routine wound management.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated in Europe from advanced wound care management products used to treat acute and chronic wounds across care settings, where the product has an active healing function or a specialized therapy component beyond basic coverage.

Scope exclusions: Traditional gauze, cotton rolls, and simple adhesive bandages are excluded from this market size.

Segmentation Overview

- By Product

- Wound Dressings

- Film Dressings

- Foam Dressings

- Hydrogel Dressings

- Collagen Dressings

- Other Dressings

- Active Wound Care

- Skin Substitutes

- Growth Factors

- Therapy Devices

- Negative Pressure Wound Therapy

- Pressure Relief Devices

- Hyperbaric Oxygen Equipment

- Compression Therapy

- Other Therapy Devices

- Other Advanced Wound-Care Products

- Wound Dressings

- By Wound Type

- Chronic Wound

- Diabetic Foot Ulcer

- Pressure Ulcer

- Arterial & Venous Ulcer

- Other Chronic Wound

- Acute Wound

- Surgical Wounds

- Burns

- Other Acute Wounds

- Chronic Wound

- By End User

- Hospitals & In-patient Facilities

- Ambulatory Surgical Centres (ASCs)

- Home-care Settings

- Long-term & Nursing Homes

- Geography

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was first used to set the market boundaries, map the commonly used therapy types, and understand country-level care pathways that influence adoption in Europe. We relied on publicly available health system statistics and clinical references to keep the model tied to treatment patterns, including sources such as Eurostat, the World Health Organization, the OECD, and national health ministries and procurement bodies.

For demand signals, we reviewed items such as hospital activity data, diabetes and aging population indicators, and published clinical guidance and peer reviewed wound care literature that helps explain typical product use by wound type. Company annual reports, investor presentations, and reputable press were also checked to understand portfolio mix and regional revenue exposure. Where disclosures were limited, a paid subscription for company financials and news helped with faster cross-checks. These desk sources are illustrative only, and many other public references were also used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test the desk assumptions, especially around therapy mix (for example, advanced dressings versus NPWT), channel pricing logic, and how usage differs by setting such as hospitals versus home care. We spoke with a mix of manufacturers, distributors, procurement and tender-oriented buyers, and clinical stakeholders across major European countries so the sizing could be adjusted where reimbursement, formularies, and care pathways differ.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | |

| Mid tier: 54% | Functional/Unit leaders: 35% | |

| Smaller Players: 17% | Managers: 49% |

Market-Sizing & Forecasting

Sizing started with a top-down demand pool build using Europe level and country level indicators that link back to wound burden and care delivery, then the totals were shaped by therapy penetration and average spend per treated case. For this market, the key inputs included chronic wound prevalence signals (such as diabetic foot and pressure ulcer risk), surgical procedure volumes, hospital and long term care capacity, the share of cases moving to outpatient and home care, and the typical treatment duration where advanced products are clinically preferred.

To keep the numbers realistic, we corroborated outputs with selective bottom-up approximations, such as sampling product price bands, checking distributor markups, and rolling up a limited set of supplier revenue disclosures where Europe splits were available. Gaps were handled by using proxy ratios from similar countries, followed by primary feedback to confirm whether the proxy matched local reimbursement and tender behavior. Forecasts were built using scenario analysis supported by measurable drivers, mainly procedure volume trends, chronic disease progression, and adoption changes for advanced therapies, and then refined based on what interviewees expected for switching, substitution, and pricing.

Data Validation & Update Cycle

Before sign-off, the model is triangulated across more than one lens, including epidemiology-driven demand, therapy adoption logic, and price and channel checks, which helps reduce single-source bias. Outliers are flagged at country and therapy level, then reviewed again against external signals like procurement intensity, care setting shifts, and reported business performance.

A second analyst review is completed when major assumptions change, and respondents are re-contacted if a variance cannot be explained by a visible market driver. Reports are refreshed annually, with interim updates when material events occur, and a final data pass is completed close to delivery so clients receive the latest updated view.

Mordor Intelligence's Europe Advanced Wound Care Management Market Market Size Measured Against Other Published Estimates

Published market sizes for advanced wound care in Europe can look far apart because the scope line is not always drawn the same way, and because price and therapy mix assumptions vary by country. Differences also show up when one study uses a different base year, converts currencies at a different timing, or applies a faster adoption curve for premium therapies.

Traditional gauze and simple adhesive bandages sit outside Mordor Intelligence's scope, which removes basic wound care volumes that some sources keep inside broader wound care totals, and that single inclusion difference can shift the headline value a lot. Another gap driver is how therapy devices are treated, where some estimates focus mainly on advanced dressings and undercount device-related disposables, while others assume a higher share of higher priced skin substitutes without matching it to reimbursement reality and setting-level usage.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.46 B (2026) | |

| Industry Report A | USD 2.82 B (2023) | Uses an earlier base year and appears centered on advanced dressings by product group, which can understate therapy devices and their associated consumables when compared on a like for like basis. |

| Regional Research House B | USD 3.20 B (2024) | Uses a different forecast window and pricing progression, and the scope description is less clear on whether bundled disposables for therapy equipment are counted consistently across countries. |

Across the three figures, the spread is mainly explained by the year being referenced and what is counted inside advanced wound care versus broader wound care baskets, followed by how devices and their recurring items are handled. By keeping the inputs tied to treated case demand, care setting mix, and realistic pricing bands that are cross checked through interviews, the final number stays traceable to repeatable steps and practical market signals.

Key Questions Answered in the Report

How big is the Europe Advanced Wound Care Market?

The Europe Advanced Wound Care Market size is expected to reach USD 4.46 billion in 2026 and grow at a CAGR of 5.78% to reach USD 5.91 billion by 2031.

Which product category leads the Europe advanced wound care management market?

Wound dressings remain the largest category, holding 45.02% revenue share in 2025, supported by broad clinical applicability and cost-effective use.

Who are the key players in Europe Advanced Wound Care Market?

Coloplast AS, ConvaTec Group PLC, Smith & Nephew, Integra Lifesciences and Paul Hartmann AG are the major companies operating in the Europe Advanced Wound Care Market.

Why are therapy devices growing faster than dressings?

Portable negative-pressure systems, bioactive pumps, and sensor-enabled platforms deliver measurable healing acceleration and workflow savings, propelling a 6.61% CAGR through 2031.

Page last updated on: