Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

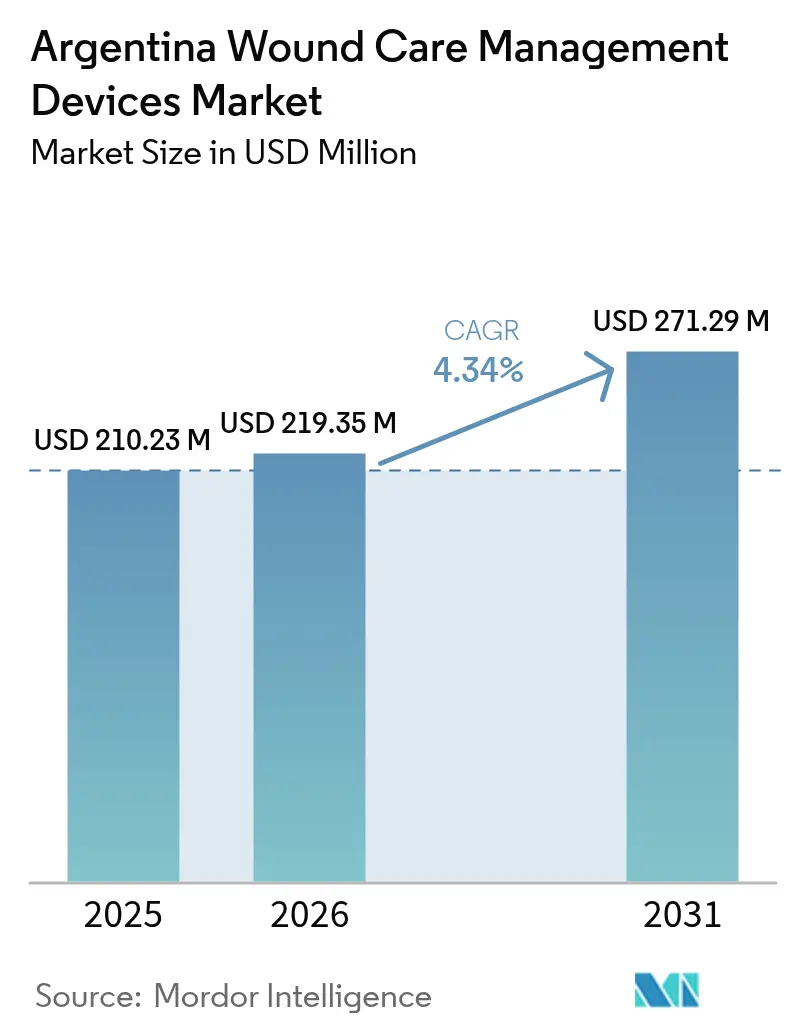

| Base Year Market Size (2025) | USD 210.23 Million |

| Market Size (2026) | USD 219.35 Million |

| Market Size (2031) | USD 271.29 Million |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Wound Care Management Devices Market Analysis by Mordor Intelligence

The Argentina wound care management devices market size was valued at USD 210.23 million in 2025 and estimated to grow from USD 219.35 million in 2026 to reach USD 271.29 million by 2031, at a CAGR of 4.34% during the forecast period (2026-2031). Argentina is Latin America’s fourth-largest pharmaceutical destination, and close to 80% of its medical devices are imported, so currency swings and global supply dynamics heavily influence pricing and product availability. Demand climbs because 12.4% of the 45.7 million residents are now aged 65 years or older [1]Pan American Health Organization, “Argentina: Health in the Americas Profile 2024,” paho.org , while the national diabetes prevalence rose, sharply lifting the need for sophisticated wound therapies. Government health expenditure at 6.51% of GDP in 2021 signals sustained public backing for hospital upgrades and reimbursement of essential wound care. Meanwhile, ANMAT’s EU-style four-class risk framework keeps product quality high but lengthens market-entry timelines, compelling foreign suppliers to work closely with local distributors. Currency volatility—Argentina’s inflation exceeded 200% in 2024—adds another layer of complexity but also encourages hospitals to adopt inventory-light models that favor advanced dressings with proven cost-benefit profiles.

Key Report Takeaways

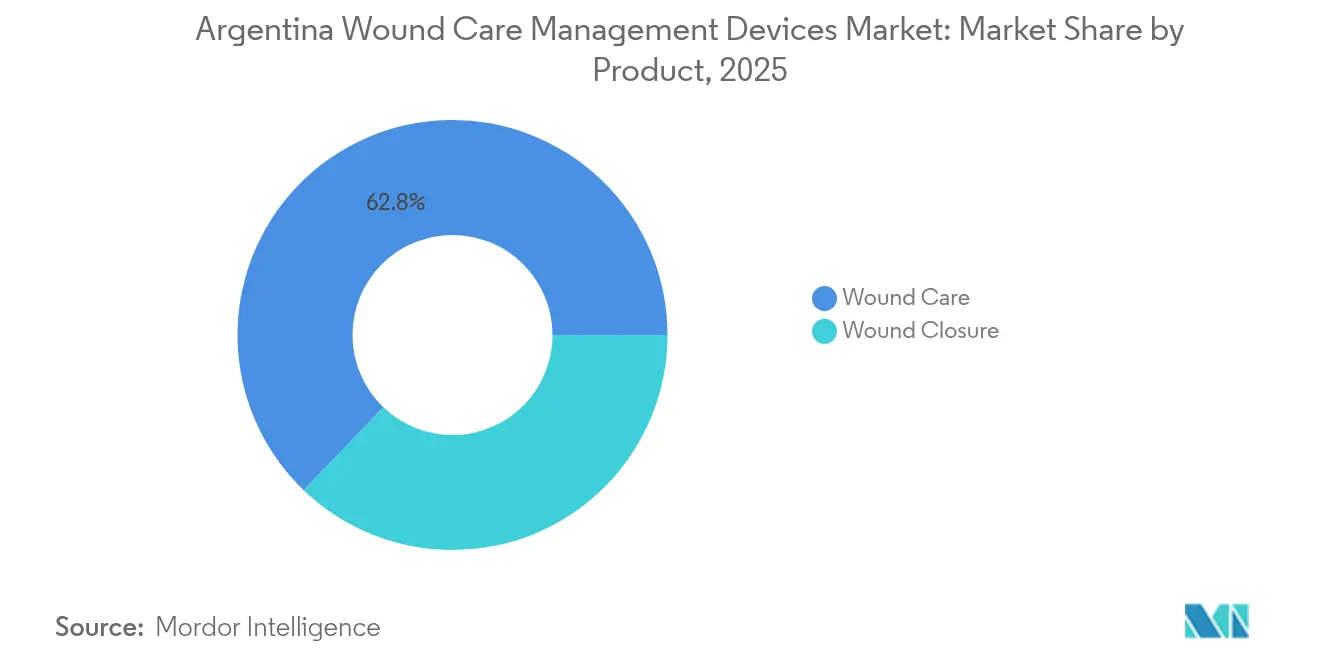

- By product category, Wound Care products led with 62.84% of Argentina wound care management devices market share in 2025, while Wound Closure is forecast to expand at a 5.05% CAGR through 2031.

- By wound type, Chronic Wounds held 58.35% share of the Argentina wound care management devices market size in 2025; Acute Wounds show the fastest growth at 5.18% CAGR to 2031.

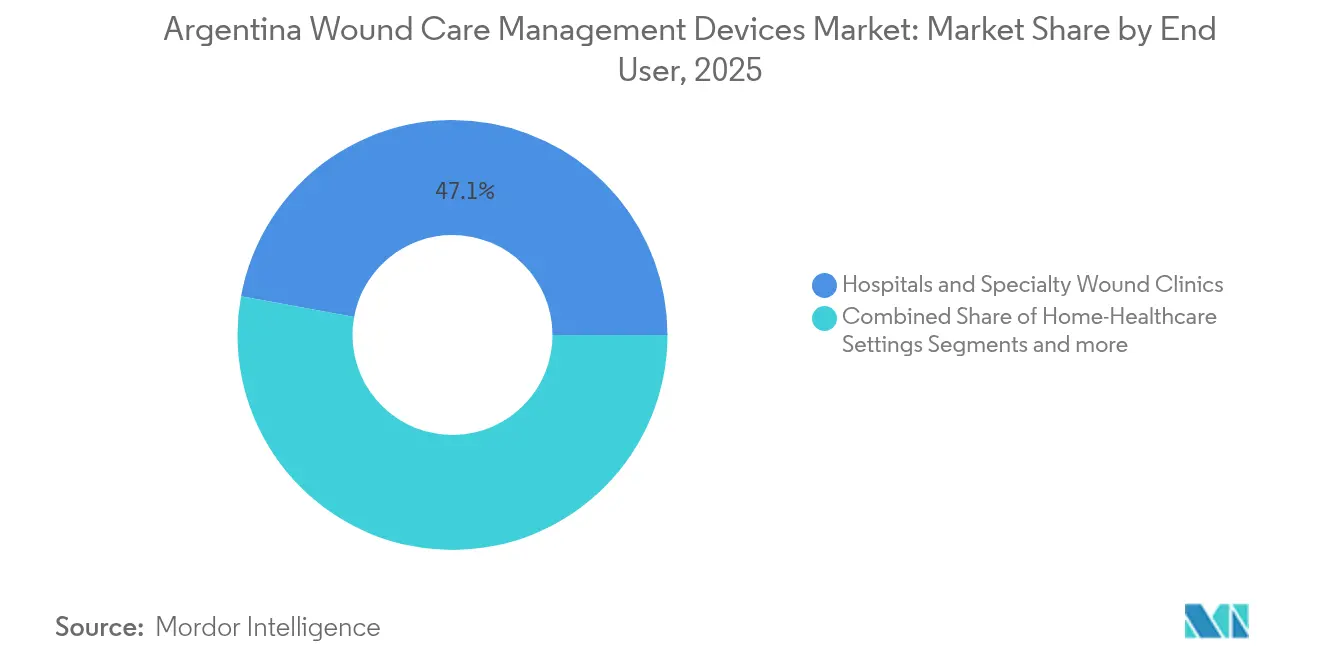

- By end user, Hospitals & Specialty Wound Clinics accounted for 47.12% of the Argentina wound care management devices market share in 2025, whereas Home-Healthcare Settings will grow at a 5.22% CAGR.

- By mode of purchase, Institutional Procurement commanded 65.02% share of the Argentina wound care management devices market size in 2025, while the Retail/OTC channel is projected to rise at a 5.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Wound Care Management Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in chronic wounds & diabetic ulcers | +1.2% | National, highest in Buenos Aires, Córdoba, Santa Fe | Medium term (2-4 years) |

| Rising geriatric population | +0.9% | National, higher in large urban centers | Long term (≥ 4 years) |

| Growing surgical procedure volume | +0.8% | National, centered on tertiary hospitals in metros | Short term (≤ 2 years) |

| Expansion of advanced home-care solutions | +0.7% | Urban first, spreading to suburbs | Medium term (2-4 years) |

| Rising health spending & infrastructure | +0.6% | National, with emphasis on underserved provinces | Long term (≥ 4 years) |

| Provincial tele-medicine reimbursement (NPWT) | +0.3% | Early adopters in Buenos Aires province | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in Chronic Wounds & Diabetic Ulcers

Argentina’s diabetes prevalence jump keeps advanced wound devices in steady demand. A 2024 national manual on pressure-injury prevention standardizes care, reducing inter-hospital practice gaps and clarifying device specifications. Multidisciplinary guidelines highlight evidence-based dressings, driving hospitals to procure products whose clinical dossiers match protocol thresholds. Because diabetic ulcers often require multi-layered intervention, clinics now bundle negative-pressure systems with antimicrobial foams, ensuring continuity from debridement through closure. Consistent national protocols also help distributors plan inventory, trimming procurement delays tied to Argentina’s split public, social-security and private payor landscape [2]Argentina Ministry of Health, “Manual de prevención de lesiones por presión 2024,” argentina.gob.ar .

Rising Geriatric Population

People aged 65 years and above now represent 12.4% of residents, meaning more chronic wounds, slower tissue regeneration and higher comorbidity loads. Expansion of the Sumar Program to 20 million beneficiaries introduces explicit wound-care packages, funneling older patients into reimbursed pathways instead of out-of-pocket purchases. Senior-focused clinic upgrades—including bariatric beds and mobile NPWT pumps—raise demand for durable devices able to survive multi-patient use cycles. Infusion of public funds into geriatric wards anchors long-term growth because even in economic downturns the government protects elder-care budgets; device makers therefore align product roadmaps to gerontology protocols.

Growing Surgical Procedure Volume

A 2024 survey of 232 hospitals revealed stark capacity gaps between city centers and peripheral regions, yet both segments report rising elective and trauma surgeries. Complex procedures need advanced closure products—cyanoacrylate adhesives, antimicrobial sutures and novel absorbable meshes—that accelerate recovery and minimize infection risk. Public–private integration initiatives encourage single formularies for suture kits, reducing duplication and standardizing consumption volumes. As economic recovery improves patient ability to pay co-pays, the caseload for orthopedics and cardiovascular surgery rises, feeding demand for specialty closure devices and post-operative dressings.

Expansion of Advanced Home-Care Wound Solutions

Evidence from international studies shows that chronic wound patients heal effectively under supervised home programs, where nurse visits and tele-monitoring trim hospital stays. Argentina mirrors this shift: payors reimburse portable NPWT sets that log exudate volume and upload data to cloud dashboards. Pharmacy chains market silver-foam dressings in consumer packs, which families can reorder online, spurring retail throughput. Device makers simplify instructions with QR codes that launch Spanish video guides, boosting adherence and lowering follow-up costs for insurers. Home-care momentum creates fresh shelf space for compact pumps, smart bandages and enzymatic debriders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced wound products | -0.8% | Nation-wide, worst in public hospitals | Medium term (2-4 years) |

| Stringent reimbursement ceilings | -0.6% | Varies by payor subsector | Short term (≤ 2 years) |

| Scarce private insurance coverage | -0.4% | Urban pockets with higher private uptake | Medium term (2-4 years) |

| Peso-linked import-price volatility | -0.9% | Nation-wide, hits all import-dependent devices | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Wound Care Products

A 2024 antitrust probe revealed collusion among prepaid insurers, lifting procedure prices by more than 140% in six months and forcing regulators to cap future hikes at inflation rates. Simultaneously, real health-care spending fell 35% after budget cuts, squeezing hospital procurement lines and delaying upgrades from gauze to active dressings. Currency-driven inflation pushes importers to re-price monthly, so public facilities often postpone buying foam or NPWT kits until tariff-free windows open. Clinician brain-drain further erodes adoption, as surgeons relocating abroad diminish local expertise in advanced closure protocols.

Peso-Linked Import-Price Volatility

Relying on imports for around four-fifths of supply makes the Argentina wound care management devices market highly sensitive to peso swings. Inflation hit 224% in 2024, forcing suppliers to quote short-validity prices, which complicates tender planning and leaves stockouts when bids expire. Hospitals use spot-rate hedges but still face 10-20% cost jumps between purchase order and delivery. The World Bank notes that macro-volatility deters private capital investments in health tech, so start-ups struggle to fund local assembly lines [3]World Bank Group, “Argentina Economic Update April 2024,” worldbank.org . Devices with high-end electronic components suffer most, as suppliers pay for imports in USD but collect reimbursements in pesos months later, eroding margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Wound Care Dominance Drives Market Expansion

The Argentina wound care management devices market size for Wound Care products accounted for 62.84% of revenue. Traditional gauze and tape dominate volume because they fit tight budgets; however, advanced dressings—hydrofibers, alginates and silver foams—gain traction where outcome-based procurement models reward faster healing. Negative-pressure wound therapy (NPWT) systems record double-digit unit growth as clinical trials confirm lower infection rates and shorter stays. Smith & Nephew’s global Q1 2025 report cited 3.8% underlying growth in Advanced Wound Management, validating local interest in premium devices.

Wound Closure, although smaller, leads with a 5.05% CAGR; cyanoacrylate tissue sealants and antibacterial sutures find ready buyers in trauma centers handling rising roadway injuries. Single-use NPWT canisters also appeal to outpatient surgery units that desire zero-maintenance gear. Growing tele-monitoring integration pushes suppliers to embed sensors in dressings, adding data-analytics value yet keeping disposables within standard reimbursement thresholds. Argentina’s push toward pressure-injury prevention protocols ties hospitals to evidence-backed product lists, creating predictable reorder cycles for advanced dressings.

By Wound Type: Chronic Wounds Shape Treatment Paradigms

Chronic lesions captured 58.35% of 2025 revenue, reflecting the nation’s aging profile and diabetes burden. Diabetic foot ulcers remain the dominant subsegment, often presenting late and requiring multilayer interventions. Pressure ulcers follow, prompting long-term demand for breathable foam and silicone border dressings that minimize shear. Venous leg ulcers show uptake of compression-compatible dressings that maintain moisture without slippage.

Conversely, Acute Wounds post a faster 5.18% CAGR as surgical volumes rebound after pandemic delays. Hospitals standardize antimicrobial sutures for orthopedic repairs and deploy film dressings in minimally invasive procedures, accelerating turnover of single-patient kits. Burns and other trauma wounds spur interest in collagen matrices and bio-engineered skin substitutes, especially after AVITA Medical’s Cohealyx launch in 2025. Standardization of chronic-wound codes in payer formularies now steers clinics toward devices that document measurable closure outcomes, further professionalizing purchasing decisions.

By End User: Home Healthcare Emerges as Growth Catalyst

Hospitals & Specialty Wound Clinics generated 47.12% of revenue in 2025, mainly because complex cases still arrive at tertiary facilities. Nonetheless, the home-healthcare subsegment is forecast to expand at 5.22% CAGR, outpacing all other settings. Payors see cost savings when nurse-led home rounds substitute for inpatient beds, so they reimburse portable NPWT pumps and antimicrobial wraps delivered directly to patients.

Tele-consult follow-ups cut travel for rural seniors, letting specialists in Buenos Aires review wounds via smartphone images. Long-term care facilities remain steady because frail elders require daily dressing changes; these centers favor silicones that lift without tearing fragile skin. Hospitals form partnerships with home-care agencies, shipping patients home with ready-packed dressing kits and digital instructions, reducing readmission risk and cementing demand for consumer-friendly packaging.

By Mode of Purchase: Institutional Procurement Drives Market Structure

Institutional buying held 65.02% share in 2025 as public hospitals, social-security entities, and large private chains pool volumes to win bulk discounts. E-tender platforms increasingly demand CE-, FDA- or ANMAT-approved dossiers and local service plans, so authorized distributors enjoy a compliance moat.

Argentina wound care management devices market size in institutional channels is forecast to reach USD 176.8 million by 2031. Retail and OTC outlets—pharmacy chains, online marketplaces and grocery-attached drugstores—post a 5.12% CAGR, buoyed by consumer migration toward self-care for minor lacerations and diabetes-related skin maintenance. Pharmacies stock convenient all-in-one kits that bundle foam pads with saline sprays, while e-commerce sites offer next-day delivery even to provincial towns. Hybrid “click-and-collect” services allow patients to redeem digital reimbursement vouchers issued by insurers, blending institutional funding with retail logistics.

Geography Analysis

Metropolitan Buenos Aires, Córdoba and Santa Fe provinces anchor demand because they host the bulk of tertiary hospitals, specialized wound clinics and higher-income patients. These areas import sophisticated NPWT pumps and smart dressings faster, thanks to better reimbursement flows and shorter supply chains. In contrast, northwest and Patagonian provinces prioritize essential supplies and rely on tele-dermatology to access specialists, a practice that boosts uptake of camera-enabled bandages.

Provincial budgets are uneven: Entre Ríos’ 2025 plan targets expanded health allocations, whereas resource-tight Chaco leans on national grants for device purchases. Diabetes prevalence sits above the national mean in urbanized belts, aligning advanced dressing sales with city pharmacies; yet rural zones record more trauma wounds from agriculture and transport mishaps, sustaining gauze and suture volume.

Inflation and freight surcharges create notable price gaps between port-proximate and interior regions. Importers stage bulk stock in Buenos Aires warehouses, then forward small loads inland when peso volatility recedes, which occasionally triggers shortages up-country. ANMAT’s single registration system applies nation-wide, but on-the-ground inspections lag in distant provinces, allowing grey-market dressings to surface. The 2024 national manual on pressure-injury prevention aims to cut these disparities by mandating standardized protocols and approved product rosters for all provinces. Home-care growth is most visible in suburban belts around big cities where broadband coverage supports video consults; as 4G expands, similar models should reach Patagonia and the northwest within four years.

Competitive Landscape

The Argentina wound care management devices market hosts a mix of global brands—Smith & Nephew, ConvaTec, Medtronic—and local distributors that secure ANMAT clearances and after-sales service. No single player exceeds 25% share, yielding moderate concentration. Smith & Nephew’s 2025 trade update showed global advanced-wound revenue of USD 1.24 billion, aided by acquisitions such as Osiris for skin substitutes, evidence of continued pipeline investment.

ConvaTec delivered 6.7% organic lift in its 2024 wound division, proof that innovation in silicone foams and hydro-fiber dressings resonates even in cost-pressured markets. Start-ups such as Biomiq tout nano-hydrogel PureGel for antimicrobial action, hunting niches in infection-prone diabetic ulcers.

Currency gyrations intensify rivalry: foreign OEMs hedge in USD, while local distributors quote in pesos, so contract terms now include adjustment clauses pegged to monthly inflation. Hospitals compare lifecycle costs instead of sticker prices, rewarding suppliers that bundle clinician training and remote analytics. Regulatory probes into pricing practices make transparent tender documentation a competitive differentiator. Meanwhile, tele-medicine ready devices create a moat; smart bandages like iCares, which transmit pH and temperature data, promise lower rehospitalization rates and draw interest from both public insurers and private prepaid plans. With device imports still near 80% of supply, firms that localize final assembly may skirt some tariffs and gain speed-to-market benefits.

Argentina Wound Care Management Devices Industry Leaders

Medtronic PLC

Smith & Nephew

ConvaTec Group PLC

Coloplast

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The iCares smart bandage enables real-time biomarker monitoring for chronic wounds. Argentina’s hospitals could adopt such digital tools to enhance remote wound management, especially in underserved rural areas.

- April 2025: The iCares smart bandage enables real-time biomarker monitoring for chronic wounds. Argentina’s hospitals could adopt such digital tools to enhance remote wound management, especially in underserved rural areas.

- February 2025: Biomiq’s PureGel is a nano-hydrogel that provides extended antimicrobial action using hypochlorous acid. Its relevance is high in Argentina, where infection control in chronic wounds remains a clinical priority.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Argentina wound care management devices market as all professional-grade products and devices used to clean, protect, close, or actively heal acute and chronic wounds, from traditional gauze dressings to negative-pressure and oxygen therapy systems, delivered through institutional or retail channels. According to Mordor Intelligence, home first-aid items such as adhesive strips and cosmetic scar reducers remain outside the scope.

Scope Exclusion: Over-the-counter first-aid bandages and purely cosmetic skin-care products are not included in sizing.

Segmentation Overview

- By Product

- Wound Care

- Dressings

- Traditional Gauze & Tape Dressings

- Advanced Dressings

- Wound-Care Devices

- Negative Pressure Wound Therapy (NPWT)

- Oxygen & Hyperbaric Systems

- Electrical Stimulation Devices

- Other Wound Care Devices

- Other Wound Care Products

- Dressings

- Wound Closure

- Sutures

- Surgical Staplers

- Tissue Adhesives, Strips, Sealants & Glues

- Wound Care

- By Wound Type

- Chronic Wounds

- Diabetic Foot Ulcer

- Pressure Ulcer

- Venous Leg Ulcer

- Other Chronic Wounds

- Acute Wounds

- Surgical/Traumatic Wounds

- Burns

- Other Acute Wounds

- Chronic Wounds

- By End User

- Hospitals & Specialty Wound Clinics

- Long-term Care Facilities

- Home-Healthcare Settings

- By Mode of Purchase

- Institutional Procurement

- Retail / OTC Channel

Detailed Research Methodology and Data Validation

Primary Research

To validate desk findings, our team interviewed Buenos Aires-based vascular surgeons, wound-care nurses in Córdoba, procurement heads at two public hospitals, and distributors covering Santa Fe pharmacies. The conversations clarified average selling prices, import clearance lags, and the growing shift of low-risk cases to home care, helping us stress-test model assumptions.

Desk Research

Mordor analysts began with trade and health datasets issued by the Argentine Ministry of Health, INDEC customs import codes 9018.90 and 3005.90, and WHO Global Health Expenditure tables, which anchor local procedure counts, import dependence, and spending trends. We then referred to peer-reviewed journals such as Revista Argentina de Cirugía and Diabetes Care for the incidence of diabetic foot ulcers, and association portals such as the Latin American Wound Care Society for clinical guidelines. For price discovery and firm-level revenue splits, paid databases like D&B Hoovers and Dow Jones Factiva were tapped, complemented by annual reports and SEC 10-Ks of multinational device makers. This list is illustrative; several other public and subscription sources were consulted to cross-check facts and fill gaps.

Market-Sizing & Forecasting

A top-down build starts with 2024 hospital and retail spending on wound devices reconstructed from import values, local manufacturing output, and public-sector purchase ledgers. Results are reconciled with selective bottom-up checks such as sampled ASP × volume data from five key distributors. Variables fed into the model include diabetes prevalence (12 % of adults), annual surgical procedures per 1,000 population, peso-to-USD inflation, negative-pressure device penetration, and aging population growth. Multivariate regression projects each driver through 2030, while scenario analysis adjusts for currency shocks. Where distributor splits were missing, weighted averages from comparable Latin American markets were applied and clearly flagged inside the workbook.

Data Validation & Update Cycle

Outputs undergo variance checks against manufacturer Latin America revenue, customs tallies, and hospital procurement audits. Any deviation beyond five percentage points prompts a re-contact with field experts before sign-off. Reports refresh once a year, with interim updates triggered by peso devaluation above 10 % or major reimbursement changes. A final analyst review ensures clients receive the most current baseline.

Why Mordor's Argentina Wound Care Management Baseline Commands Confidence

Published figures often differ because firms pick unique product baskets, price assumptions, and refresh cadences, so direct comparisons can be misleading. By aligning scope strictly with therapeutic wound devices and indexing values to actual import prices, Mordor reduces noise that distorts many headline numbers.

Key gap drivers include wider SKU inclusion by some publishers (they bundle OTC bandages), aggressive inflation pass-through methods, or reliance on Latin America roll-downs rather than Argentina-specific data. Our annual refresh and peso-adjusted ASP audit further narrow variance.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 210.23 M (2025) | Mordor Intelligence | - |

| USD 410 M (2024) | Anonymized label | Includes OTC first-aid lines and applies regional price uplift without local inflation audit |

| USD 190.7 M (2023) | Anonymized label | Uses hospital procurement only, omits retail channel and currency adjustments |

Taken together, the comparison shows that Mordor's disciplined scope selection, dual-track modeling, and yearly peso calibration provide a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current value of the Argentina wound care management devices market?

It stands at USD 219.35 million in 2026 and is forecast to reach USD 271.29 million by 2031.

Which product segment leads revenue?

Wound Care products hold 62.84% of the Argentina wound care management devices market share as of 2025.

How fast is home-healthcare demand growing?

Home-Healthcare Settings record the highest end-user CAGR at 5.22% through 2031.

Why does currency volatility matter for suppliers?

Roughly 80% of devices are imported, so peso swings immediately affect landed costs and tender viability.

What regulatory body oversees medical devices in Argentina?

ANMAT administers a four-class risk framework similar to EU norms, governing safety, efficacy and market access.

Which wound type shows the quickest future growth?

Acute Wounds are projected to grow at a 5.18% CAGR, benefiting from rising surgical volumes and trauma care upgrades.

Page last updated on: