Non-vascular Stents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

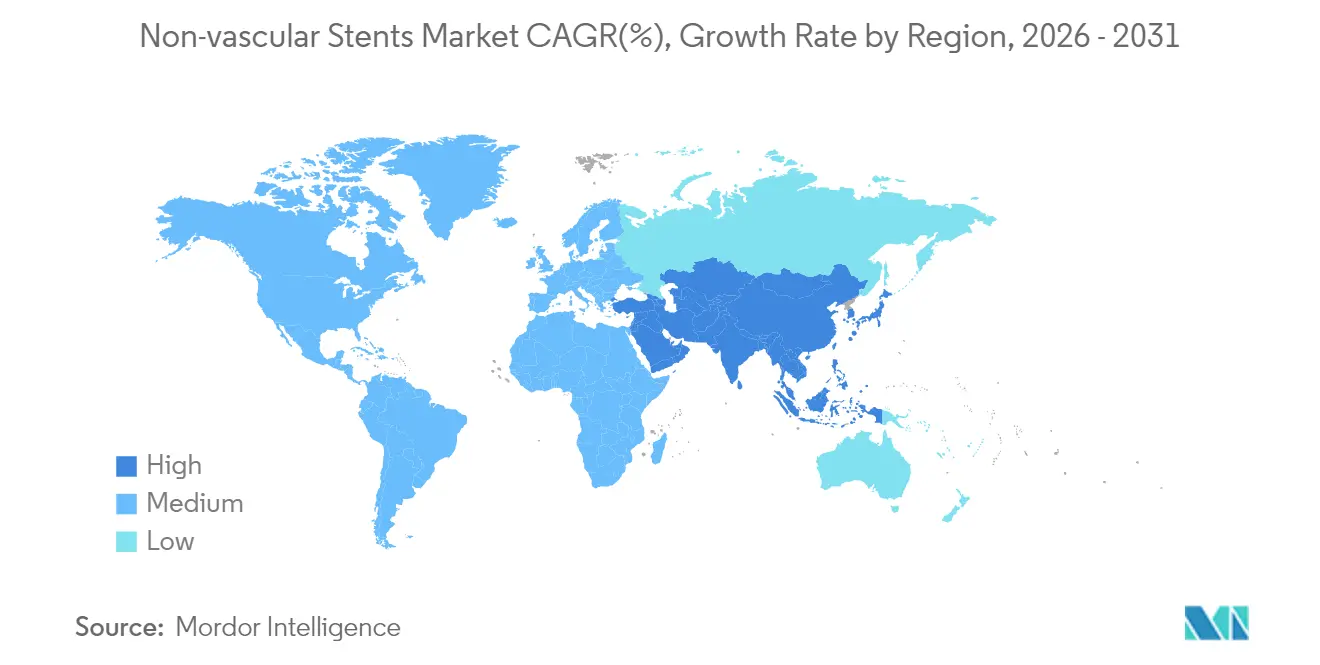

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

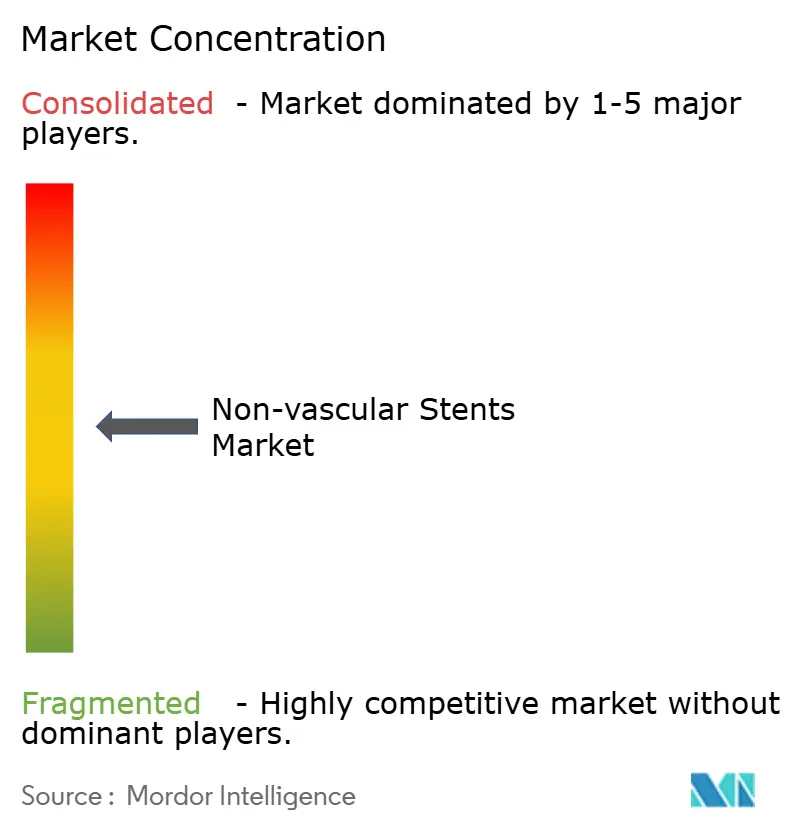

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-vascular Stents Market Analysis by Mordor Intelligence

The non-vascular stents market size was valued at USD 1.81 billion in 2025 and estimated to grow from USD 1.89 billion in 2026 to reach USD 2.31 billion by 2031, at a CAGR of 4.18% during the forecast period (2026-2031). The measured growth pace reflects a maturing segment in which material science breakthroughs, especially bioresorbable polymers and patient-specific 3-D printing, complement entrenched metallic designs to meet diverse clinical demands. Manufacturers are absorbing up to 20% increases in specialty-alloy input costs, yet long-term demand resilience is anchored in a rapidly aging global population, a wider clinical shift toward minimally invasive procedures, and regulatory programs that shorten time-to-market for breakthrough devices. Competitive differentiation centers on novel coatings that curb restenosis, software-guided deployment systems that enhance procedural precision, and closer alignment between device life-cycle and sustainability mandates. Pulmonary, biliary and tracheal indications illustrate how procedure volumes continue to migrate from open surgery to endoscopic and bronchoscopic routes, reinforcing willingness to pay for advanced stent platforms.

Key Report Takeaways

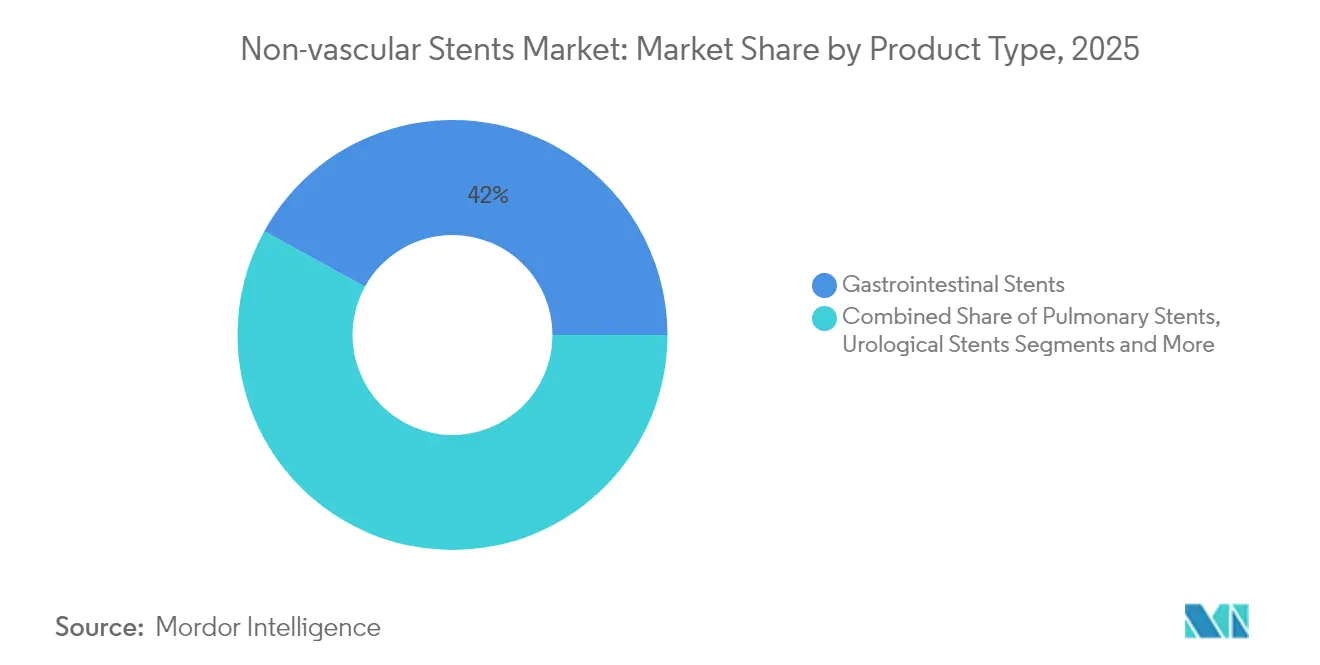

- By product type, gastrointestinal devices led with 41.98% of non-vascular stents market share in 2025, while pulmonary stents are projected to log the fastest 7.41% CAGR through 2031.

- By material, metallic devices held 61.10% share of the non-vascular stents market size in 2025; bioresorbable and drug-eluting coated variants are advancing at an 8.63% CAGR.

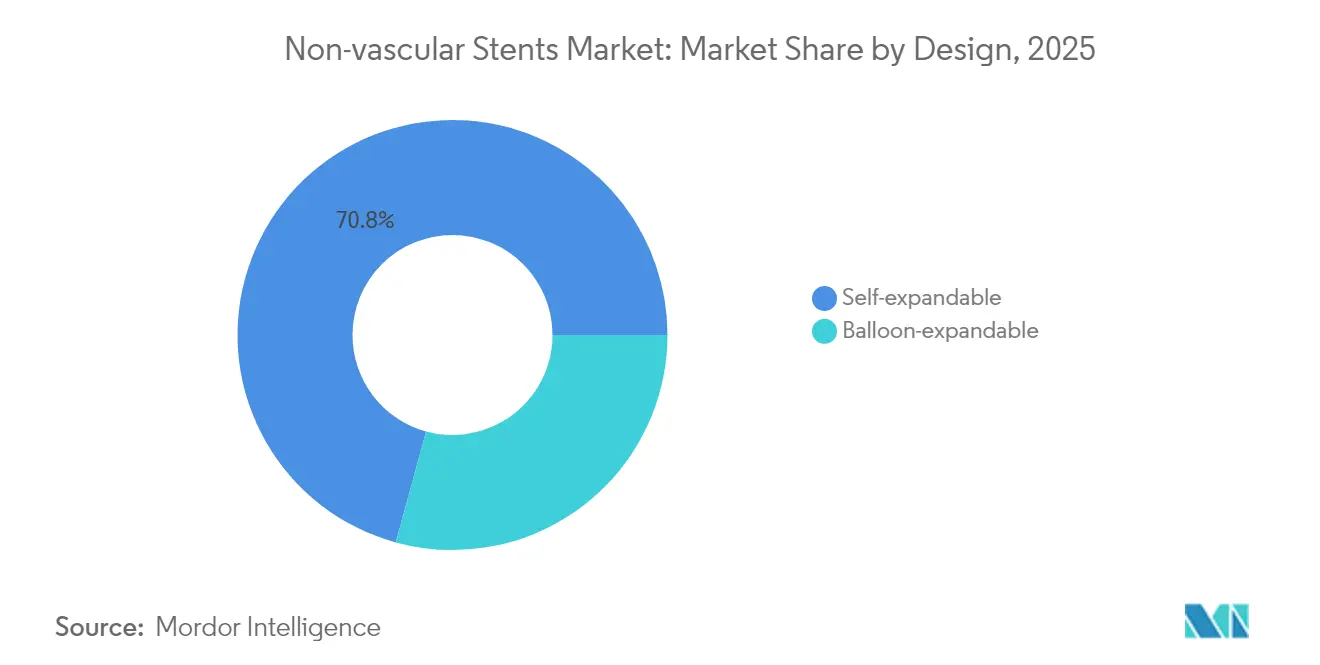

- By design, self-expandable formats commanded 70.75% of non-vascular stents market share in 2025 and are tracking a 6.32% CAGR to 2031.

- By end user, hospitals accounted for 64.70% share of the non-vascular stents market size in 2025, whereas ambulatory surgical centers are growing at 6.56% CAGR.

- By geography, North America captured 36.10% revenue share in 2025, but Asia-Pacific is pacing the field with a 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-vascular Stents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Geriatric Population & Chronic Disease Prevalence | +1.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Technological Advancements In Materials & Coatings | +0.8% | Global, led by North America & APAC innovation hubs | Medium term (2-4 years) |

| Rising Demand For Minimally-Invasive Procedures | +0.7% | Global, accelerated in developed markets | Short term (≤ 2 years) |

| 3D-Printed Patient-Specific Stents Gain Clinical Traction | +0.4% | North America & Europe early adoption | Medium term (2-4 years) |

| Fast-Track Regulatory Pathways | +0.3% | Primarily North America & Europe | Short term (≤ 2 years) |

| Advantages Associated with Biodegradable Polymer Stents | +0.5% | Global, with premium market focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Geriatric Population and Chronic Disease Prevalence

Population aging intersects with higher incidences of gastrointestinal, pulmonary and urological disorders, lifting procedure volumes across every therapeutic class within the non-vascular stents market.[1]Yongduo Yu, “Global burden of paralytic ileus and intestinal obstruction in adults aged 65 and over,” BMC Gastroenterology, biomedcentral.com Forecasts to 2040 show colorectal, pancreatic and liver cancers remaining on an upward trajectory, creating multi-organ intervention requirements among elderly cohorts, whose tissue fragility and comorbidities demand stents with improved conformability and reduced inflammatory profiles. Growth therefore reflects not only rising absolute case numbers but also repeat procedures as patients live longer with chronic conditions.

Technological Advances in Materials and Coatings

Next-generation molybdenum-rhenium alloys combine high fatigue strength with biocompatibility, unlocking new design freedom beyond conventional nitinol Argus Media. Laser micro-patterning techniques can suppress smooth-muscle proliferation by 75% while enhancing endothelialization twofold. Drug-free collagen-functionalized platforms similarly shorten healing times without relying on anti-proliferative agents.[2]Haoshuang Wu, “A drug-free cardiovascular stent functionalized with tailored collagen supports in-situ healing of vascular tissues,” Nature Communications, nature.com Collectively, these innovations are widening addressable patient pools by reducing restenosis risks and metal allergy concerns.

Rising Demand for Minimally Invasive Procedures

Venous sinus stenting for idiopathic intracranial hypertension carries <1% complication risk and yields symptom relief inside 3 months, exemplifying the procedural shift toward low-trauma solutions. Electrocautery-enhanced lumen-apposing metal stents achieve 94.8% technical and 100% clinical success in gallbladder drainage for high-risk surgical patients, displacing open cholecystectomy in fragile populations. These outcomes underscore payer and provider preference for same-day discharge pathways that compress inpatient costs.

3-D-Printed Patient-Specific Stents

FDA clearance of individualized oral stents and the production of more than 600 airway implants through AI-driven design workflows demonstrate how additive manufacturing personalizes lumen geometry to each patient. Validated finite-element models now forecast balloon-expandable stent behavior under patient-specific loading, refining sizing accuracy and limiting over-expansion risks. Hospitals are exploring in-house 3-D print farms to fabricate biodegradable ureteral devices that degrade 11% in three weeks, pointing to a future of just-in-time production and streamlined logistics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complications: Migration, Occlusion & Infection | -0.6% | Global, higher impact in emerging markets | Short term (≤ 2 years) |

| Availability Of Alternative Therapies | -0.4% | Developed markets with advanced healthcare | Medium term (2-4 years) |

| Supply-Chain Risk For Ni-Ti Alloys & Rare Metals | -0.3% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Sustainability Pressure On Single-Use Devices | -0.2% | Europe & North America regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Complications: Migration, Occlusion and Infection

Biliary stent migration appears in 8.4% of treated patients and frequently triggers cholangitis or obstruction that require urgent retrieval, adding cost and clinical burden. Rare intracardiac displacement of ureteral devices illustrates the severity spectrum, with endovascular extraction and multidisciplinary care raising hospital resource use. Despite improved anchoring designs, complication anxiety weighs on clinician decision-making, especially in regions lacking advanced retrieval tools.

Availability of Alternative Therapies

Drug-coated balloons now treat in-stent restenosis without leaving behind permanent scaffolds; 2025 literature confirms durable lumen patency and 96.7% procedural success, thereby challenging repeat stenting in coronary interventions. EUS-guided gastroenterostomy delivers superior re-intervention rates versus metallic stents for gastric outlet obstruction, steering gastroenterologists toward anastomosis over stenting in complex malignancies. As clinicians gain confidence in these modalities, share-of-procedure for non-vascular stents may plateau in select indications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Gastrointestinal Dominance Faces Pulmonary Challenge

Gastrointestinal platforms generated 41.98% of the non-vascular stents market in 2025 on the strength of entrenched protocols for esophageal, biliary and colorectal procedures. Hospitals deploy self-expandable metal designs to treat malignant obstruction where palliative decompression can avert emergency surgery and preserve quality of life. Technical success consistently exceeds 90%, while fully covered devices are entering benign esophageal strictures, broadening application scope. Pulmonary stents, although a smaller base, are expanding 7.41% per year as interventional pulmonology gains acceptance for both malignant airway obstruction and benign tracheobronchomalacia.

Clinical guidelines now position silicone and hybrid metal-silicone tubes as first-line for central lesions, but biodegradable polydioxanone alternatives have achieved 89.7% effectiveness in adult cohorts after two months, easing later removal. Custom tracheobronchial units produced through AI-enabled 3-D modeling further compress lead times compared with labor-intensive manual molding. In parallel, urological devices continue to capture physician mind-share thanks to extractable strings that cut removal pain scores from 5.23 to 0.86 and slash dwell time to 16 days, saving patients USD 146 in follow-up costs. Oral oncology stents represent another high-value niche, protecting surrounding tissue during radiotherapy and underscoring how additive manufacturing unlocks low-volume bespoke use cases.

By Material Type: Metallic Supremacy Challenged by Biodegradable Innovation

Metallic constructions, primarily nitinol, contributed 61.10% of 2025 revenue, benefiting from decades of clinical familiarity, high radial force and kink resistance. Supply chain turbulence, however, has raised alloy costs by 20%, prompting both diversification and renewed interest in iron and magnesium bioresorbables. Second-generation magnesium scaffolds such as AMS-2.1 restore vessel strength yet complete degradation inside 720 days, answering clinician calls for temporary support that avoids permanent caging. Iron scaffolds still corrode too slowly, though surface texturing and galvanic coupling show early promise.

Polymer-based designs accelerate degradation but often rely on metallic backbones for strength; hybrid models therefore combine poly-l-lactide or poly-dioxanone sleeves with thin nitinol frameworks. Drug-eluting layers using sirolimus or paclitaxel further cut neointimal hyperplasia, supporting 8.63% growth for coated systems. Sustainability mandates are also shaping R&D, with firms testing cellulose-based delivery sheaths and recyclable tray materials to align with EU packaging rules effective in 2026.

By Design: Self-Expandable Dominance Reflects Clinical Preference

Self-expandable formats captured 70.75% of non-vascular stents market share in 2025 because they adapt to anatomical changes, tolerate compression and simplify sizing in tortuous ducts. Five-year outcomes from the MER carotid study illustrate the durability of braided nitinol constructs, which reported only 7% restenosis at follow-up. For gastrointestinal cases, radial force must balance luminal patency against tissue over-expansion; braided designs offer a gentle force curve that limits perforation risk. Balloon-expandable devices maintain relevance where precise diameters and symmetric expansion are critical, especially in calcified colonic strictures. New digital sizing algorithms simulate expansion against real-time CT models, trimming oversizing complications. Emerging shape-memory polymers may bridge both paradigms by delivering self-expansion with programmable final diameters.

By End User: Hospital Dominance Faces Outpatient Migration

Hospitals retained 64.70% of the non-vascular stents market size in 2025 given their ability to manage high-risk patients and respond to procedural emergencies. Interventional suites equipped with fluoroscopy and anesthesiology teams remain essential for complex airway and biliary cases. Nevertheless, ambulatory surgical centers are posting a 6.56% CAGR as payers encourage site-of-service shifts that lower total episode cost. Same-day discharge after colorectal decompression or ureteral stent placement is increasingly routine when post-operative pain and bleeding risks are minimal. Specialized digestive-disease clinics now conduct routine stent exchanges under conscious sedation, freeing hospital capacity for acute care. Reimbursement parity initiatives in the United States and Japan continue to propel outpatient penetration as long as patient safety benchmarks remain uncompromised.

Geography Analysis

North America consolidated 36.10% revenue in 2025, buoyed by Medicare coverage pathways that guarantee reimbursement for breakthrough devices within six months of FDA clearance.The FDA has already granted 1,041 Breakthrough Device designations, 128 of which reached the market, turbo-charging domestic adoption of advanced polymer and AI-assisted platforms. Outpatient migration is particularly strong, with hospital outpatient departments swiftly integrating electrocautery-enhanced stents for gallbladder drainage.

Asia-Pacific is advancing at a 7.52% CAGR, the fastest worldwide, as demographic aging intersects with expanded state insurance programs. Japan remains the region’s technology bellwether, importing high-precision U.S. stent systems for complex biliary and airway cases despite conservative physician adoption cycles. Regional policymakers are also courting technology transfer deals that pair Western intellectual property with local mass-production capacity, helping offset foreign-exchange exposure and supply chain volatility. Venture funding compressed in 2024 yet proprietary 3-D printed airway devices still secured regulatory approvals, signaling continued investor appetite for differentiated indications.

Europe represents a stabilizing influence with demand anchored in universal coverage schemes and early adoption of sustainability directives. Packaging regulations effective from 2026 oblige device makers to account for end-of-life recycling even in sterile environments, nudging R&D toward light-weight trays and QR-code-enabled traceability. Middle East & Africa and South America collectively hold a smaller footprint yet exhibit rising tender activity for modular endoscopy suites that support rapid deployment of stent programs in tertiary hospitals.

Competitive Landscape

Industry structure remains moderately fragmented as no single vendor controls more than one-third of the non-vascular stents market. Boston Scientific’s USD 1.26 billion purchase of Silk Road Medical broadened its carotid portfolio and demonstrates how incumbent firms absorb niche innovators to extend clinical reach. Teleflex’s planned €760 million acquisition of BIOTRONIK’s Vascular Intervention unit brings in-house drug-coated balloons and peripheral self-expanding products, illustrating a trend toward portfolio convergence across vascular and non-vascular specialties. Medtronic partnered with Contego Medical for Neuroguard to deepen neuro-protection capabilities and mitigate stroke risk during carotid deployment. Supply resilience now ranks alongside innovation as a strategic imperative, with multinationals centralizing alloy procurement and qualifying secondary sources in India and Vietnam to buffer geopolitical disruptions.

Start-ups are carving white-space in patient-specific and biodegradable niches. VisionAir has already designed more than 600 custom airway units through cloud-based AI modeling, while Kallisio’s FDA-cleared oral stent underscores opportunity in radiation oncology adjuncts. Investors continue to reward device makers that marry material innovation with digital planning tools capable of shortening operating room times and raising first-pass success, thereby lowering overall episode cost.

Non-vascular Stents Industry Leaders

Medtronic

Becton, Dickinson and Company

Boston Scientific Corporation

CONMED Corporation

Cook Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex agreed to acquire BIOTRONIK’s Vascular Intervention business for approximately €760 million (USD 825 million) to deepen its interventional cardiology portfolio.

- October 2024: Peytant Solutions received FDA Class II clearance for the AMStent Tracheobronchial Covered Stent System to treat malignant airway strictures.

- July 2024: VisionAir Solutions surpassed 600 patient-specific airway stents produced through its AI VisionAir 3-D platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global non-vascular stents market as revenue generated from newly manufactured gastrointestinal, pulmonary (airway), and urological stents that keep non-vascular lumens open after malignant or benign obstruction.

According to Mordor Intelligence, trauma repair plugs, vascular stents, dilation balloons, and reusable drainage catheters are outside this remit.

Segmentation Overview

- By Product Type

- Gastrointestinal Stents

- Pulmonary (Airway) Stents

- Urological Stents

- Others

- By Material Type

- Metallic

- Non-metallic

- Biodegradable / Drug-eluting Coated

- By Design

- Self-expandable

- Balloon-expandable

- By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with interventional gastroenterologists, pulmonologists, urologists, clinical engineers, and purchasing heads across North America, Europe, and Asia-Pacific. These interviews tightened assumptions on procedure mix, average selling price, and the rising share of biodegradable designs before we finalized the model.

Desk Research

We gathered baseline demand and pricing clues from tier-1 sources such as the World Health Organization cancer registry, Global Burden of Disease, OECD hospital procedure files, and FDA/CE device clearance logs. We then enriched them with trade data and peer-reviewed outcome studies. Paid libraries, D&B Hoovers for supplier revenues and Questel for stent patent families, helped verify production trends. The sources named here illustrate the breadth consulted; many additional datasets informed our desk work.

Market-Sizing & Forecasting

Our top-down build multiplies country-level procedure counts for strictures by validated stent utilization rates and weighted ASPs, followed by supplier roll-ups that flag outliers. Inputs include colorectal-cancer incidence, COPD prevalence, ureteroscopic surgery volumes, alloy-specific price erosion, and reimbursement shifts. Multivariate regression, anchored to aging curves, oncologic trends, and technology substitution, extends the view to 2030, while bottom-up cross-checks adjust totals when material variance emerges.

Data Validation & Update Cycle

Outputs undergo anomaly screens, peer review, and re-contact triggers; sizeable deltas prompt fresh interviews. Reports refresh each year, with interim updates for major regulatory or recall events, so clients receive the latest view.

Why Mordor's Non-vascular Stents Baseline Gains Trust

Published estimates vary because firms differ in scope choices, ASP treatment, and refresh cadence. Our disciplined boundaries and yearly recalibration narrow those gaps.

Key discrepancies stem from adding vascular devices, applying flat price escalation, or extrapolating one-region data to the globe.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.81 B (2025) | Mordor Intelligence | - |

| USD 1.71 B (2024) | Global Consultancy A | Asia-Pacific volumes excluded; 2023 ASPs held constant |

| USD 1.80 B (2024) | Market Publisher B | Includes venous stents; minimal primary validation |

| USD 1.60 B (2023) | Research House C | Flat 3 % annual price growth; three-year update cycle |

The comparison shows that Mordor's clear scope, primary confirmation, and annual refresh deliver a balanced, transparent baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the non-vascular stents market?

The market generated USD 1.89 billion in 2026 and is forecast to reach USD 2.31 billion by 2031.

Which product segment leads today?

Gastrointestinal devices hold 41.98% of 2025 revenue, reflecting their long-standing use in esophageal, biliary and colorectal procedures.

What material trends are shaping future growth?

Metallic nitinol remains dominant, but bioresorbable iron, magnesium and polymer hybrids are growing at 8.63% as clinicians seek temporary scaffolds.

How fast is Asia-Pacific expanding?

The region is projected to grow at 7.52% CAGR through 2031, making it the fastest-growing geography.

Why are ambulatory surgical centers gaining share?

Stent procedures increasingly allow same-day discharge, aligning with payer efforts to lower costs and patient preference for outpatient care.

What complications still restrain adoption?

Migration, occlusion and infection remain key risks, with biliary migration reported in 8.4% of cases and necessitating additional interventions.

Page last updated on: