Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

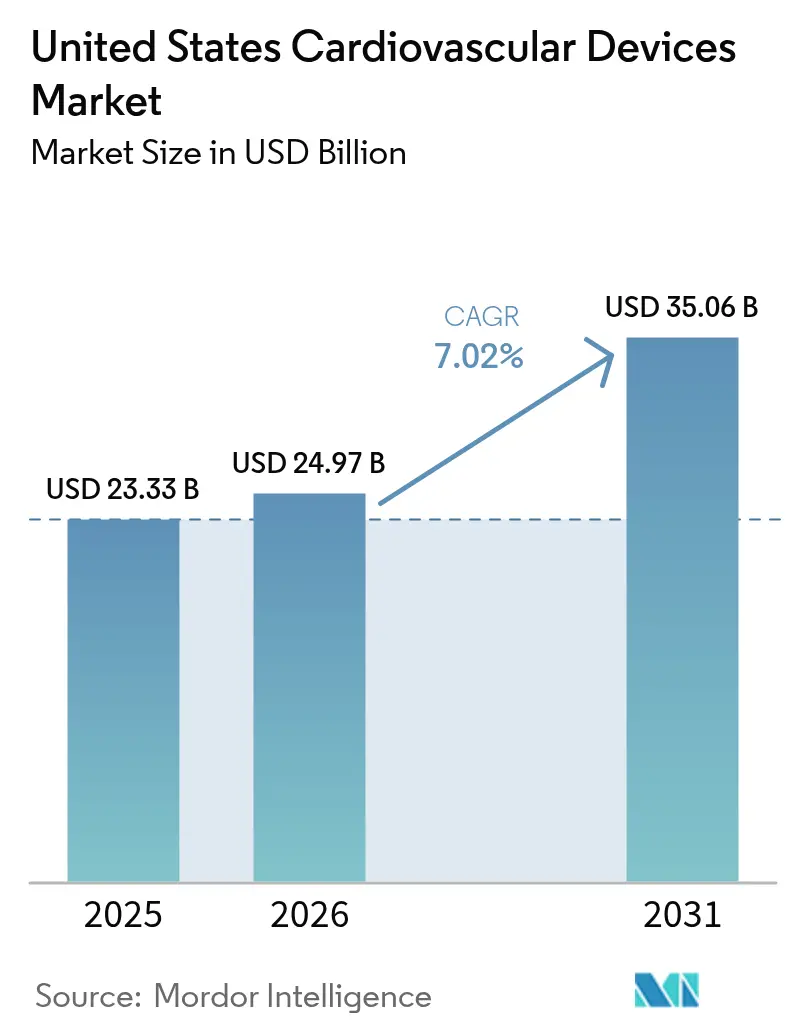

| Base Year Market Size (2025) | USD 23.33 Billion |

| Market Size (2026) | USD 24.97 Billion |

| Market Size (2031) | USD 35.06 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

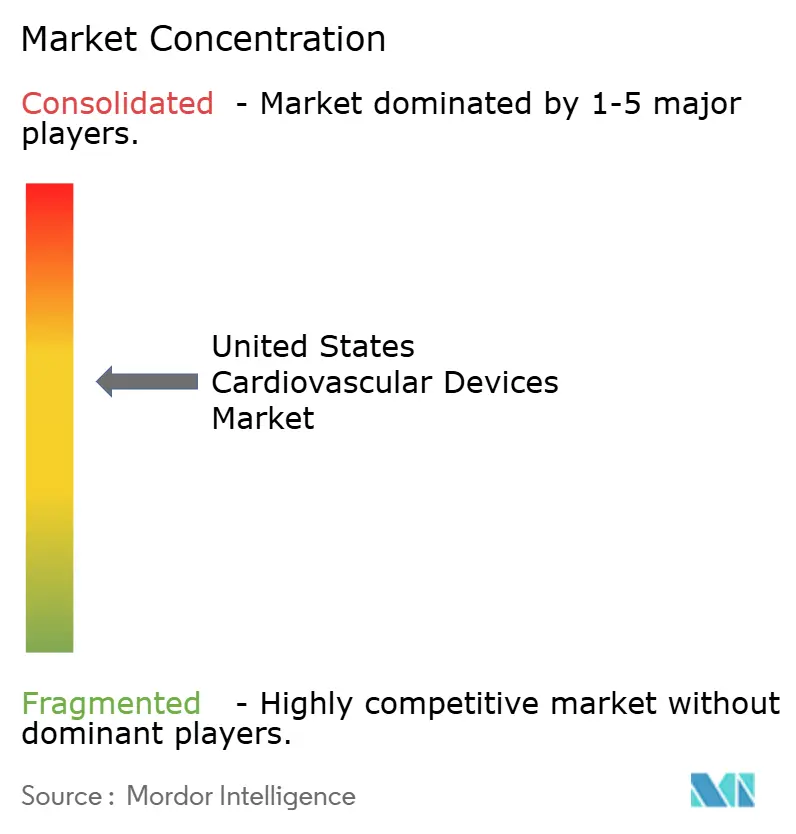

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Cardiovascular Devices Market Analysis by Mordor Intelligence

The United States cardiovascular devices market size in 2026 is estimated at USD 24.97 billion, growing from 2025 value of USD 23.33 billion with 2031 projections showing USD 35.06 billion, growing at 7.02% CAGR over 2026-2031. Growth stems from the rising prevalence of cardiovascular disease, affecting 126.9 million adults, and steady procedure volumes that stimulate recurring demand for devices. Artificial-intelligence-enabled diagnostics, transcatheter therapeutic breakthroughs, and payment reforms that reward cost-saving technologies are reshaping competitive priorities. Providers increasingly bundle diagnostic and interventional tools to secure volume-based discounts, subtly shifting bargaining power toward large health systems. Venture capital inflows, particularly in structural heart start-ups, expand the innovation pipeline even as hospital capital constraints intensify.

Key Report Takeaways

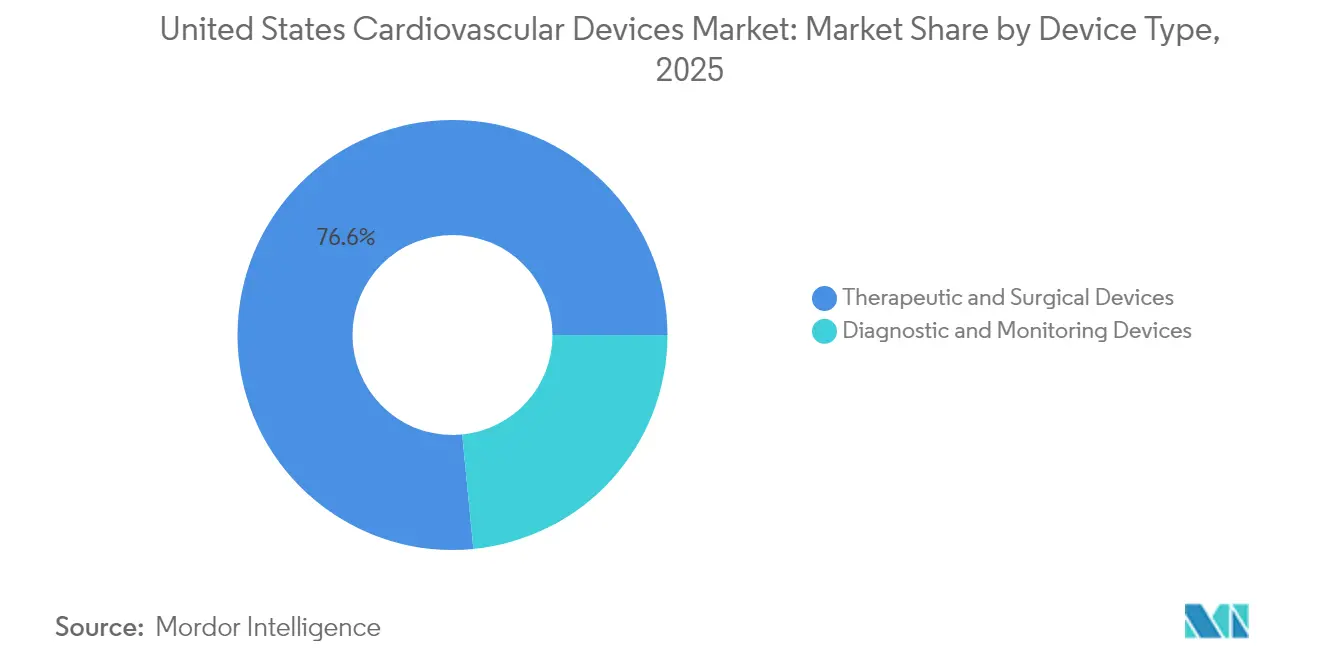

- By device type, therapeutic & surgical devices led the United States cardiovascular devices market with a 76.55% market share in 2025, while diagnostic & monitoring devices are forecast to advance at an 8.12% CAGR through 2031.

- By indication, coronary artery disease accounted for 54.78% of the United States' cardiovascular devices market size in 2025; valvular heart disease is projected to grow at a 6.56% CAGR through 2031.

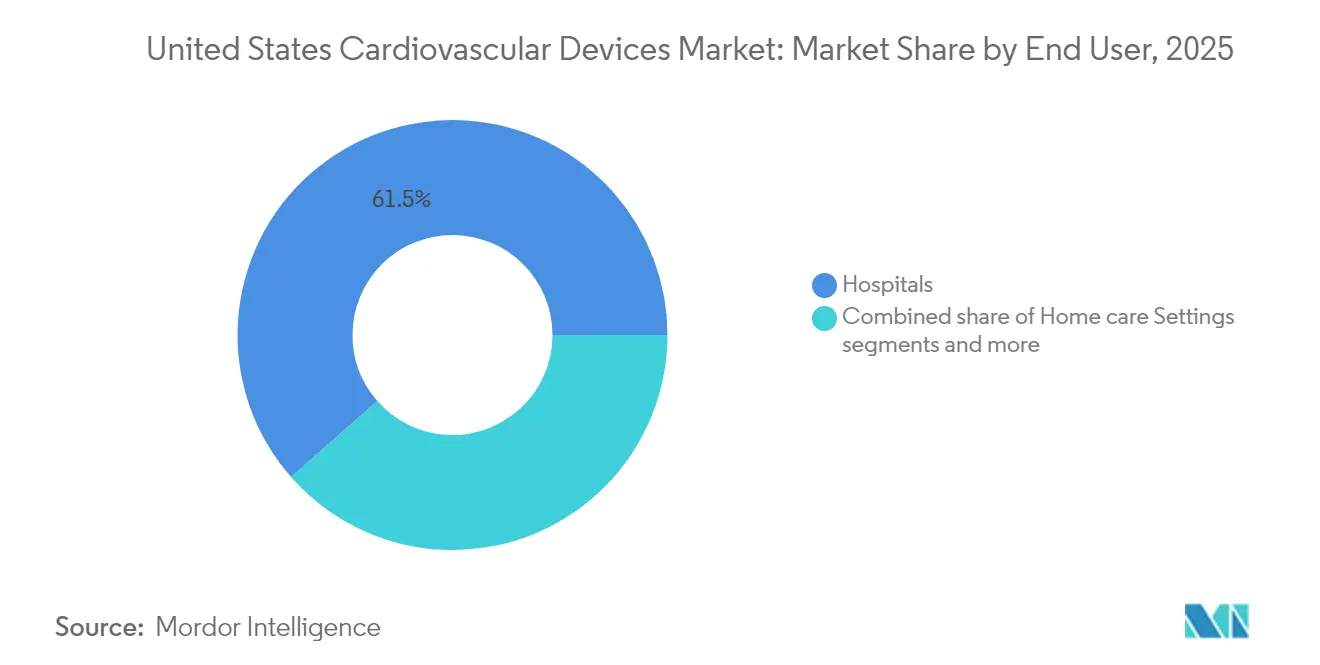

- By end user, hospitals accounted for 61.48% revenue in 2025, whereas home-care settings are poised for a 7.55% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Cardiovascular Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Obesity-Linked PAD Surge Driving Use of Drug-Coated Balloons | +1.8 | National, with higher impact in Southern states | Medium term (3-4 yrs) | |

| ACC/AHA Reimbursement Revisions Incentivizing CRT-D Upgrades | +1.2 | National | Short term (≤2 yrs) | |

| Growth of Office-Based & ASC Cath-Labs via CMS Site-of-Service Differential | +1.5 | National, with early gains in metropolitan areas | Medium term (3-4 yrs) | |

| Venture Capital Influx into Percutaneous Mitral Repair Start-ups | +0.9 | National, with concentration in innovation hubs | Long term (≥5 yrs) | |

| Rapid Adoption of TAVR Post-FDA Low-Risk Approval & Expanded CMS Coverage | +1.6 | National, with higher adoption in urban centers | Short term (≤2 yrs) | |

| Infection-Control Policies Boosting Demand for Single-Use Diagnostic Catheters | +1.1 | National, with emphasis on hospital systems | Medium term (3-4 yrs) | |

| Source: Mordor Intelligence | ||||

Obesity-Linked Pad Surge Driving Use Of Drug-Coated Balloons

Peripheral artery disease now affects 10 million Americans, with 2 million facing critical limb-threatening ischemia. Trial evidence showing a 51.3% fall in target-lesion failure after sirolimus delivery is accelerating hospital adoption of drug-coated balloons, especially for below-the-knee work. Hospitals in high-obesity Southern states are restocking coated balloons, while large systems negotiate multiprocedure discounts that lower per-unit pricing. Device makers respond by adding smaller diameters and extended coating life to suit infrapopliteal anatomy. Payers increasingly cover these balloons once registry data confirm reduced repeat interventions, thereby reinforcing the momentum for uptake.

ACC/AHA Reimbursement Revisions Incentivizing CRT-D Upgrades

The 2025 criteria broaden access to cardiac resynchronization therapy defibrillators and reward extended battery life, yielding USD 15,120 in Medicare savings per patient over six years. Hospitals are pre-ordering premium CRT-D models to capture both clinical benefit and cost share. Early claims data reveal a 17% year-over-year increase in elective generator replacements as providers expedite swaps before older devices reach their elective-replacement indicators. Manufacturers highlight remote-monitoring firmware that dovetails with home-care expansion, strengthening the therapy’s economic case.

Growth Of Office-Based & ASC Cath-Labs Via CMS Site-Of-Service Differential

Approximately 10% of catheterization and PCI cases have shifted to ambulatory surgery centers, where reimbursement is 36% to 47% lower than that in hospital outpatient departments[1]Source: ECG Management Consultants, “Cardiology Procedures in ASCs,” ecgmc.com . Cardiologists with ASC equity stakes often buy devices directly, compressing the supply chain and forcing vendors to supply pre-sterile kits sized for smaller stockrooms. The 2025 OPPS rule raises total payments by USD 4.7 billion, reinforcing ASC economics. Expect stent and balloon unit volumes to rise the fastest in urban ASCs, where parking, scheduling efficiency, and bundled payments attract commercially insured patients.

Venture-Capital Influx Into Percutaneous Mitral Repair Start-Ups

Capstan Medical’s USD 110 million Series C funding round epitomizes investor faith in the mitral and tricuspid valve market. In this field, half of patients with severe mitral regurgitation still lack access to surgery. Venture backing enables entrants to secure premium component pricing and conduct longer trials, thereby positioning them as attractive acquisition targets. Structural-heart majors now allocate dedicated scouting teams to incubators, intensifying competition for intellectual property. Hospitals anticipate broader device menus that can tailor therapy to individual anatomy and comorbidities, potentially reducing procedure counts.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hospital Capital Budget Freezes After Medicare Rate Cuts | -1.4% | National, with higher impact in rural areas | Short term (≤2 yrs) |

| Stringent Regulatory Requirements and Product Recalls | -0.8% | National | Medium term (≈3-4 yrs) |

| Semiconductor Shortages Disrupting ICD Generator Supply | -1.2% | National, with higher impact on specialized cardiac centers | Short term (≤2 yrs) |

| Stringent 510(k) Predicate Requirements for Bioresorbable Scaffolds | -0.7% | National, with focus on innovation centers | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Hospital Capital Budget Freezes After Medicare Rate Cuts

A 2.83% physician-fee reduction, effective January 2025, tightened hospital cash flow, as the moment inflation-adjusted Medicare rates had already fallen 33% over the previous two decades. Boards are deferring non-essential cath-lab upgrades, prioritizing devices with precise cost-offset data. Vendors offering subscription pricing or pay-per-use agreements gain ground because they spare hospitals upfront outlays. Rural hospitals face sharper strain; some divert complex cases to regional centers, slowing local device turnover.

Stringent Regulatory Requirements And Product Recalls

Medical device recalls reached a four-year high in 2024, with more than 10 % flagged as the most serious class[2]Source: Modern Healthcare, “Medical Device Recalls FDA 2024,” modernhealthcare.com . Simultaneously, the FDA's clearance rate for moderate-risk cardiovascular devices continued to decline, suggesting longer review times. Manufacturers are reacting by incorporating in-house regulatory expertise earlier in the development process, a move that raises fixed costs but may help curb delays. A notable market reaction is that insurers are increasingly requesting post-market safety statistics before issuing coverage decisions, extending the requirement for real-world evidence well beyond the FDA approval milestone.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic Revenue Dominance, Diagnostic Momentum Intensifies

Therapeutic & surgical products captured 76.55% of the United States cardiovascular devices market share in 2025, underpinned by stents, valve implants, and rhythm-management devices that anchor high-value procedures. Drug-eluting stents remain the mainstay; however, bioresorbable options and intravascular lithotripsy catheters, now under development by Johnson & Johnson, offer additional revenue streams. Physicians value single-vendor kits that bundle guidewires and imaging catheters, a tactic that deepens wallet share for integrated suppliers.

Diagnostic & monitoring devices are forecast to clock an 8.12% CAGR to 2031, the fastest of any category. Cloud analytics, such as EchoGo Amyloidosis, which achieves 84.5% sensitivity and 89.7% specificity, convert ultrasound systems into a source of subscription revenue. Growing reliance on remote physiologic monitoring prompts device makers to embed cellular radios, shifting BOM costs to connectivity chips while generating service-fee income.

By Indication: CAD Scale Endures, Valves Accelerate

Coronary artery disease applications accounted for 54.78% of the United States' cardiovascular devices market size in 2025, as complex-lesion tools widen per-case spending. CTO microcatheters and laser atherectomy systems are experiencing rising demand as interventionalists tackle previously surgical cases. Hospitals now stock lesion-specific inventories, underscoring the continued pull of CAD on capital budgets.

Valvular heart disease is expected to pace the market at a 6.56% CAGR through 2031. TAVR volumes have surpassed those of surgery, and next-generation devices are targeting aortic regurgitation and low-risk patients. Transcatheter mitral and tricuspid therapies are scaling quickly, aided by venture funding and pending acquisitions. Hospitals convert hybrid ORs to multi-valve suites, maximizing throughput and reinforcing device pull-through for imaging probes and closure systems.

By End User: Hospital Stronghold, Home-Care Breakout

Hospitals generated 61.48% of 2025 revenue, reflecting the concentration of high-acuity interventions. Yet administrators increasingly favor multipurpose labs over single-procedure rooms to boost utilization and blunt capital expense. Vendor service contracts that guarantee uptime now influence purchase decisions as much as list price.

Home-care settings are slated for a 7.55% CAGR to 2031. Medicare’s RPM payments soared from USD 6.8 million in 2019 to USD 194.5 million in 2023, signalling policy tailwinds. Hypertension dominates RPM use, but heart-failure pressure sensors and post-TAVR monitoring patches broaden the range of applications. Device suppliers bundle tablet hubs and cloud dashboards, capturing service revenue that cushions hardware margin pressure.

Geography Analysis

The Northeast and West lead adoption of advanced structural-heart and electrophysiology technologies, buoyed by academic centers and venture clusters. States such as Massachusetts and California host early feasibility trials, giving local hospitals first access to next-generation valves. These regions also exhibit higher penetration of home-monitoring programs, which aligns with robust broadband coverage.

The South shows the fastest growth in device demand, propelled by elevated obesity and hypertension prevalence. Black and Hispanic populations experience higher PAD amputation risk, spurring regional uptake of drug-coated balloons. Site-of-service incentives are catalyzing ASC build-outs around Atlanta, Dallas, and Houston, attracting commercial payers seeking cost savings.

Midwestern markets exhibit mounting interest in office-based labs as integrated delivery networks offload lower-acuity PCI cases. State certificate-of-need laws and ASC regulations moderate the speed of shift; California’s rules, for instance, restrict specific cardiac procedures outside hospitals, tempering West Coast migration.

Rural locales lag in capital outlays yet benefit from tele-cardiology and RPM, narrowing access gaps. The American Heart Association’s HeartCorps initiative trains local health workers, fostering community adoption of preventive tech. Remote-first device designs long-life sensors with Bluetooth upload to target this dispersed patient base.

Competitive Landscape

Medtronic, Abbott, Boston Scientific, and Edwards Lifesciences anchor a moderately concentrated arena. Medtronic spans every significant cardiovascular segment, leveraging scale to negotiate system-wide contracts. Edwards doubles down on structural heart, posting 88% tricuspid-therapy growth in Q4 2024. Boston Scientific expands its vascular reach through Silk Road Medical, complementing its WATCHMAN and FARAPULSE franchises.

Johnson & Johnson’s USD 13.1 billion purchase of Shockwave Medical secures intravascular lithotripsy for heavily calcified lesions, intensifying the rivalry in coronary stent technology. Capstan Medical’s USD 110 million war chest underscores the venture capital appetite for robotics in valve repair, while Abbott’s dual-chamber leadless pacemaker approval signals the march of miniaturization.

Artificial-intelligence capability is emerging as a differentiator; Ultromics secured FDA clearance for EchoGo Amyloidosis, broadening the software’s reimbursement case. Firms struggle to integrate AI risk product obsolescence as hospitals shift toward data-rich decision support.

United States Cardiovascular Devices Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Edwards Lifesciences

Medtronic PLC

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Medtronic plc, a frontrunner in healthcare technology, received U.S. Food and Drug Administration (FDA) approval for an expanded use of its OmniaSecure defibrillation lead. The lead is now sanctioned for placement in the left bundle branch (LBB) region, intended to enhance conduction system pacing (CSP) and better align with the heart's innate physiology.

- February 2025: The ACC issued updated ACS guidelines recommending ticagrelor or prasugrel over clopidogrel, which influences stent adjunct therapy.

- November 2024: The United States FDA launched a recall-communication pilot to tighten timelines for high-risk cardiovascular devices.

United States Cardiovascular Devices Market Report Scope

As per the scope of the report, cardiovascular diseases are a group of disorders of the heart and blood vessels that include coronary heart disease, peripheral arterial disease, congenital heart disease, and cerebrovascular disease. Cardiovascular devices are used to treat or prevent different cardiovascular conditions. The United States cardiovascular devices market is segmented by Device Type (Diagnostic & Monitoring Devices [ECG Systems, Remote Cardiac Monitor, and More], Therapeutic & Surgical Devices [Coronary Stents, Catheters, Cardiac Rhythm Management, Heart Valves, Ventricular Assist Devices, and More]), Indication (Coronary Artery Disease, Arrhythmia, and More). The Market Forecasts are Provided in Terms of Value (USD).

By Device

| Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | ||

| Cardiac MRI | ||

| Cardiac CT | ||

| Echocardiography / Ultrasound | ||

| Fractional Flow Reserve (FFR) Systems | ||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents |

| Bare-Metal Stents | ||

| Bioresorbable Stents | ||

| Catheters | PTCA Balloon Catheters | |

| IVUS/OCT Catheters | ||

| Cardiac Rhythm Management | Pacemakers | |

| Implantable Cardioverter Defibrillators | ||

| Cardiac Resynchronization Therapy Devices | ||

| Heart Valves | TAVR/TAVI | |

| Mechanical Valves | ||

| Tissue/Bioprosthetic Valves | ||

| Ventricular Assist Devices | ||

| Artificial Hearts | ||

| Grafts & Patches | ||

| Other Cardiovascular Surgical Devices | ||

By Indication

| Coronary Artery Disease |

| Arrhythmia |

| Heart Failure |

| Valvular Heart Disease |

By End User

| Hospitals |

| Home Care Settings |

| Others |

| By Device | Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | |||

| Cardiac MRI | |||

| Cardiac CT | |||

| Echocardiography / Ultrasound | |||

| Fractional Flow Reserve (FFR) Systems | |||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents | |

| Bare-Metal Stents | |||

| Bioresorbable Stents | |||

| Catheters | PTCA Balloon Catheters | ||

| IVUS/OCT Catheters | |||

| Cardiac Rhythm Management | Pacemakers | ||

| Implantable Cardioverter Defibrillators | |||

| Cardiac Resynchronization Therapy Devices | |||

| Heart Valves | TAVR/TAVI | ||

| Mechanical Valves | |||

| Tissue/Bioprosthetic Valves | |||

| Ventricular Assist Devices | |||

| Artificial Hearts | |||

| Grafts & Patches | |||

| Other Cardiovascular Surgical Devices | |||

| By Indication | Coronary Artery Disease | ||

| Arrhythmia | |||

| Heart Failure | |||

| Valvular Heart Disease | |||

| By End User | Hospitals | ||

| Home Care Settings | |||

| Others | |||

Key Questions Answered in the Report

What is the current size of the United States cardiovascular devices market?

• The United States cardiovascular devices market size reached USD 24.97 billion in 2026.

Who are the key players in United States Cardiovascular Devices Market?

• The market is projected to expand at a 7.02% CAGR from 2026 to 2031, reaching USD 35.06 billion by the end of the forecast period.

Which device segment is growing the quickest in the U.S. cardiovascular devices market?

• Diagnostic & monitoring devices are the fastest-growing category, forecast to register an 8.12% CAGR through 2031 as remote patient monitoring adoption accelerates.

What reimbursement changes are influencing device purchasing decisions?

• The 2025 ACC/AHA criteria reward longer-life CRT-D implants, saving Medicare about USD 15,120 per patient over six years and encouraging hospitals to upgrade sooner.

Page last updated on: