Self-Expanding Stents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

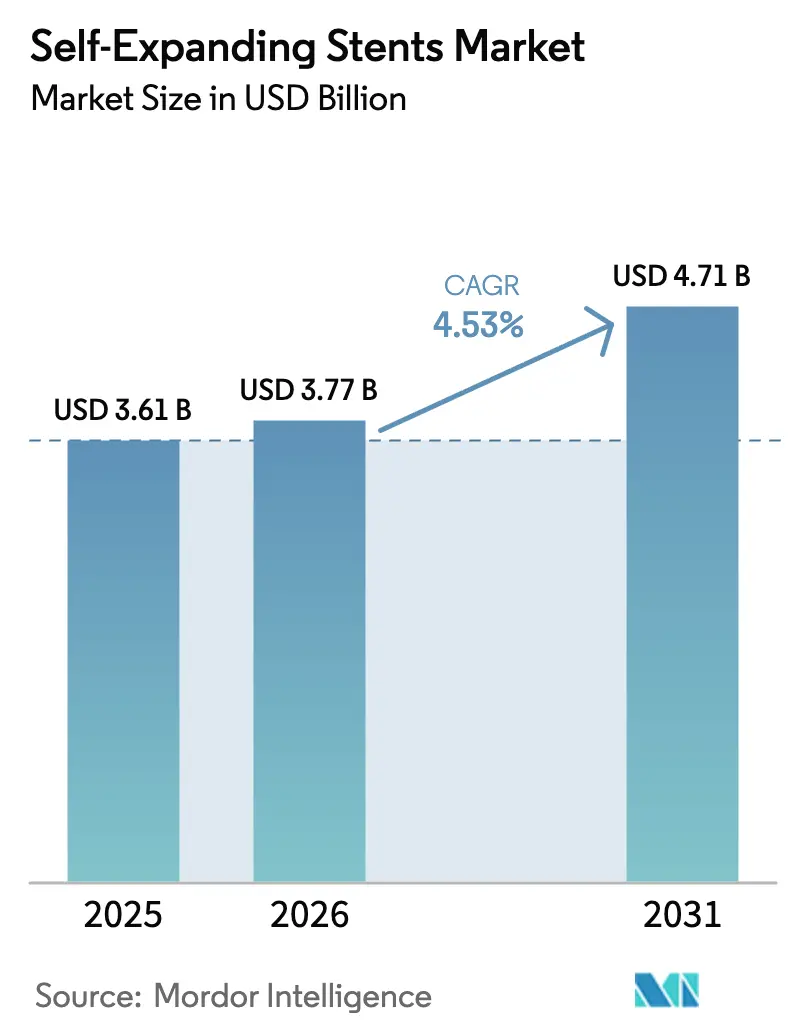

| Market Size (2026) | USD 3.77 Billion |

| Market Size (2031) | USD 4.71 Billion |

| Growth Rate (2026 - 2031) | 4.53% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Self-Expanding Stents Market Analysis by Mordor Intelligence

Self expanding stents market size in 2026 is estimated at USD 3.77 billion, growing from 2025 value of USD 3.61 billion with 2031 projections showing USD 4.71 billion, growing at 4.53% CAGR over 2026-2031. Moderate expansion reflects a mature competitive environment, rising head-to-head pressure from drug-coated balloons, and increasing availability of alternative interventional therapies. Nevertheless, larger elderly populations and a steady climb in minimally invasive procedure volumes continue to anchor demand. Technology remains the axis of competition: nitinol-based designs prevail for their flexibility and radial strength, yet polymer-hybrid scaffolds are challenging metallic dominance through superior biocompatibility. Regionally, high reimbursement ceilings in North America sustain premium device uptake, while regulatory streamlining and local manufacturing spur rapid growth in Asia-Pacific.

Key report Takeaways

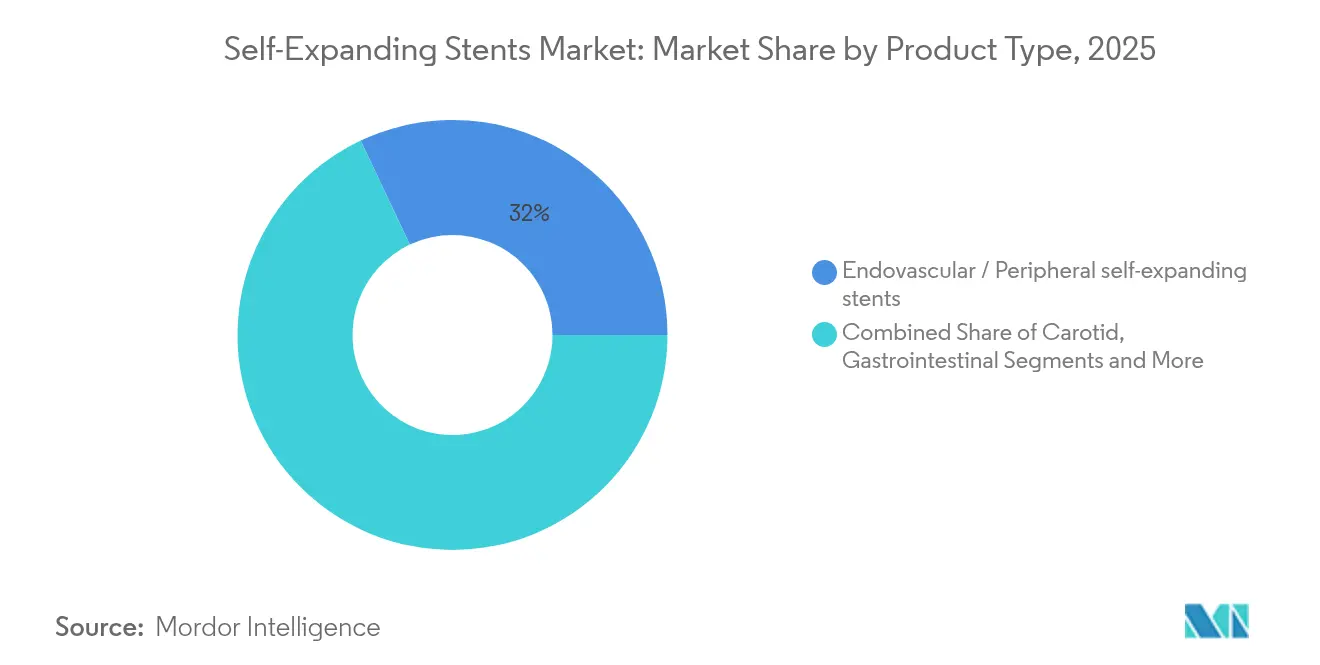

- By product type, endovascular and peripheral systems led with 32.02% of self expanding stents market share in 2025; intracranial devices are projected to expand at a 6.58% CAGR through 2031.

- By material, nitinol retained a 68.77% share of the self expanding stents market size in 2025, whereas polymer-hybrid composites are advancing at an 7.93% CAGR to 2031.

- By application, femoropopliteal procedures accounted for 39.02% of the self expanding stents market size in 2025; below-the-knee interventions record the highest 7.45% CAGR outlook.

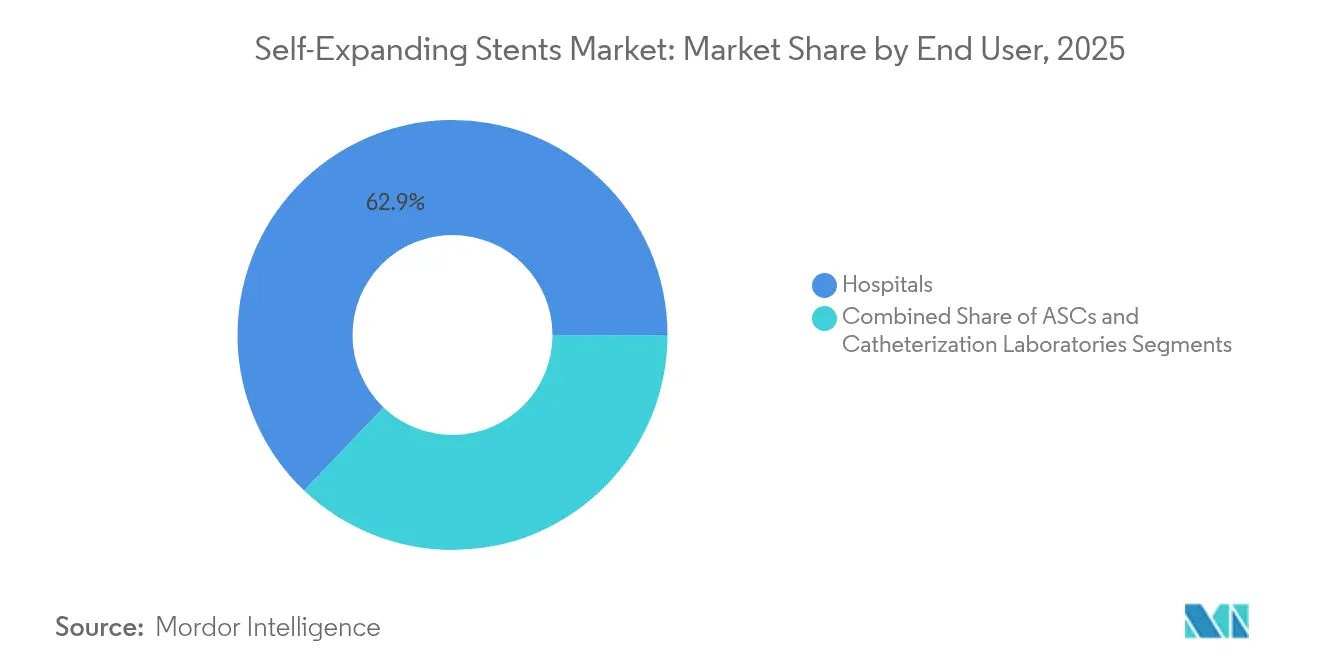

- By end-user, hospitals captured 62.88% revenue share in 2025, while ambulatory surgical centers are rising at a 7.01% CAGR.

- By delivery mode, over-the-wire systems accounted for 52.02% of self expanding stents market share in 2025, whereas stent-on-a-wire platforms show the quickest 7.52% CAGR through 2031.

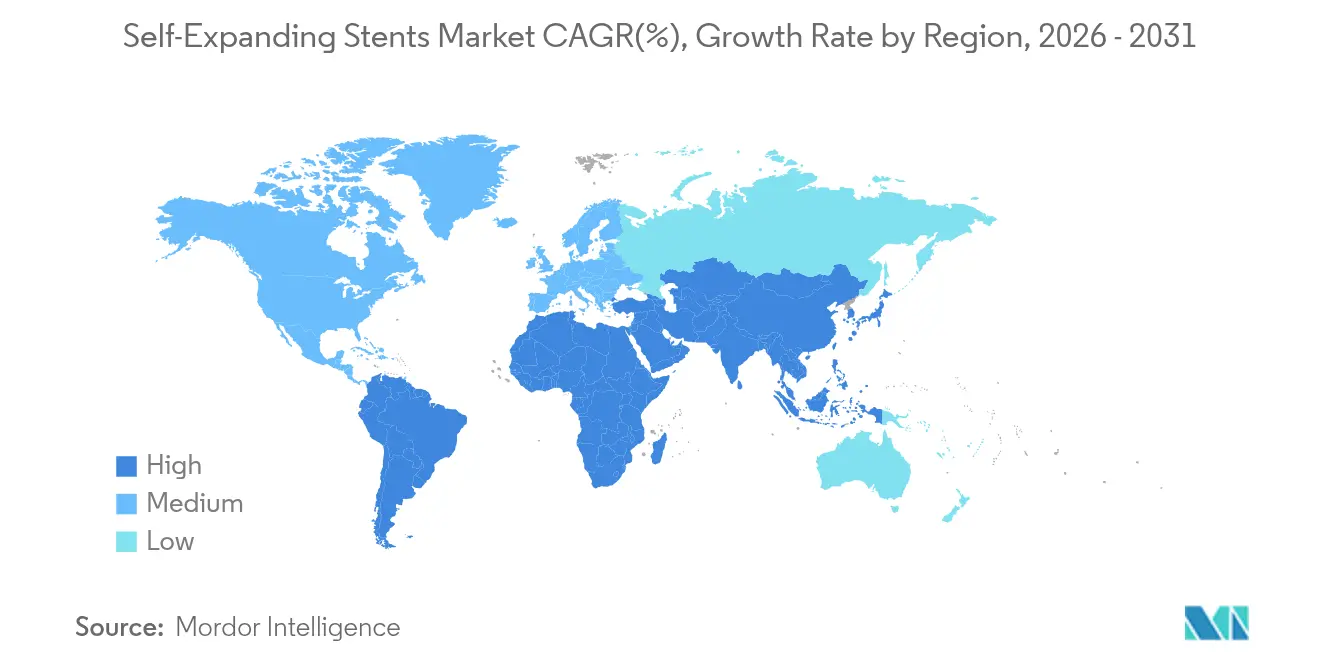

- By geography, North America commanded 38.11% of the self expanding stents market share in 2025; Asia-Pacific is the fastest-growing region at 7.32% CAGR to 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Self-Expanding Stents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Prevalence Of Cardiovascular & PAD Cases | +1.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Surge In Minimally-Invasive Peripheral Interventions | +0.9% | Global, led by Asia-Pacific growth | Medium term (2-4 years) |

| Rapid Nitinol & Imaging Technology Improvements | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Ambulatory Surgery Shift In Vascular Care | +0.6% | North America & EU core markets | Short term (≤ 2 years) |

| Drug-Coated Self-Expanding Stents For BTK Ischemia | +0.5% | Global, early adoption in US & EU | Long term (≥ 4 years) |

| AI-Enabled Procedural Planning & Sizing Tools | +0.4% | North America & EU, selective APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High prevalence of cardiovascular and PAD cases

Cardiovascular disease still affects 127.9 million U.S. adults, representing 48.6% of residents aged 20 years and older, despite a fall in heart-disease death rates to 162.1 per 100,000 in 2023. Peripheral artery disease (PAD) now burdens 113 million people aged 40 years and older worldwide. Diabetic patients show an 11.2% PAD prevalence, and elevated triglycerides further heighten risk. These figures guarantee a steady procedural pipeline for the self expanding stents market.

Surge in minimally-invasive peripheral interventions

Endovascular approaches achieve a 97.7% technical success rate in iliac artery lesions classified as TASC II A/B.[1]Le Duc Tin, "Outcomes of balloon angioplasty and stent placement for iliac artery lesions," Frontiers in Surgery, frontiersin.org Office-based labs and ambulatory surgical centers are performing an increasing share of PAD treatments, which lowers admission costs while maintaining comparable outcomes. AI-enhanced real-time device tracking for carotid stent placements has reached remarkable precision levels.[2]Yuya Sakakura et al., "Real time artificial intelligence assisted carotid artery stenting," Journal of NeuroInterventional Surgery, jnis.bmj.com These efficiency gains reinforce adoption.

Rapid nitinol & imaging technology improvements

Titanium-nitride-oxide coatings cut 5-year major adverse cardiac events to 16% versus 39% for bare metal comparators. Deep-learning plaque quantification aligns closely with intravascular ultrasound, improving procedural planning. Such advances enlarge the addressable pool for self expanding stents market therapies.

Ambulatory surgery shift in vascular care

Ambulatory centers show a 7.35% CAGR to 2030 as payers reward shorter stays. Medicare already reimburses outpatient carotid artery stenting following favorable stroke-prevention data. Same-day discharge protocols boost patient satisfaction and capacity utilization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Balloon-Angioplasty & Drug-Therapy Alternatives | -0.8% | Global, strongest in EU markets | Medium term (2-4 years) |

| Product Recalls & Stringent Regulatory Pathways | -0.6% | Global, highest impact in US & EU | Long term (≥ 4 years) |

| Nitinol Supply-Chain Bottlenecks | -0.5% | Global manufacturing impact | Short term (≤ 2 years) |

| Limited Long-Term Clinical Surveillance Data | -0.4% | Global, regulatory focus markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Balloon-angioplasty & drug-therapy alternatives

The BASIL-3 trial found major amputation or death in 58% of drug-eluting stent cases versus 66% for plain balloon angioplasty.[3]Haozhi Gong et al., “Drug-eluting stents versus bare-metal stents for intracranial atherosclerotic stenosis,” BMJ Open, bmjopen.bmj.com Drug-coated balloons and optimized pharmacotherapy offer competitive outcomes without a permanent implant, constraining the self expanding stents market.

Product recalls & stringent regulatory pathways

Warning letters underscore strict data-integrity expectations, stretching device development to 5-7 years. European MDR certification further raises compliance costs, favoring incumbents with robust quality systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Peripheral dominance drives innovation

Peripheral and endovascular systems held 32.02% of the self expanding stents market in 2025. Femoral and iliac disease prevalence, together with reimbursement parity for minimally invasive approaches, underpins steady hospital demand. Intracranial devices are advancing at 6.58% CAGR on the back of drug-eluting designs that cut restenosis by 77% versus bare metal. Gastrointestinal units pivot toward biodegradable alternatives after Japan’s 2025 clearance of the ELLA-BD polymer esophageal scaffold. Airway and lung indications benefit from polydioxanone stents demonstrating 89.7% clinical effectiveness across a decade.

By Material: Nitinol supremacy faces polymer challenge

Nitinol retained a 68.77% self expanding stents market share in 2025 on the strength of shape-memory performance. Cost pressure aside, suppliers continue to refine fatigue resistance and deliver smaller-profile platforms. Polymer-hybrid composites, expanding at 7.93% CAGR, use tailored collagen to hasten endothelial repair without eluting drugs. Iron-based bioresorbables and cobalt-chromium alloys serve niche high-force applications.

By Application: Fem-Pop leadership amid BTK innovation

Femoropopliteal disease accounted for 39.02% of the self expanding stents market size in 2025. Boston Scientific’s Eluvia drug-eluting line achieved 85.4% primary patency at 1 year versus 76.3% for bare metal controls. Below-the-knee chronic limb-threatening ischemia is the fastest-growing application following Abbott’s dissolving scaffold approval, widening therapy options for severe diabetes-related PAD.

By End-User: Hospital dominance shifts toward ambulatory care

Hospitals captured 62.88% of 2025 revenue, yet ambulatory surgical centers grow at 7.01% CAGR as payers incentivize outpatient models. Integrated embolic-protection systems permit “one-stop” peripheral work in same-day settings, reducing bed demand and bolstering physician-owned center economics.

By Delivery Mode: OTW systems lead innovation push

Over-the-wire (OTW) platforms contributed 52.02% of 2025 sales thanks to superior torque and lesion-crossing ability. Stent-on-a-wire hybrids expand at 7.52% CAGR as operators favor simplified exchanges. Through-the-scope devices remain critical for bile duct and tracheal work, benefiting from continuous miniaturization.

Geography Analysis

North America retained 38.11% of 2025 revenue. Broad insurance coverage for carotid, coronary, and peripheral procedures sustains premium adoption. Breakthrough device designations accelerate U.S. launches, illustrated by Abbott’s Esprit BTK scaffold win in 2024. Canada adopts similar protocols, while Mexico enlarges access through public-hospital investments.

Europe remains a clinical excellence hub with cautious spending. The SPORTS trial in 2025 reported 94.5% freedom from target-lesion revascularization for Eluvia versus 80.7% for drug-coated balloons, reinforcing evidence-based uptake. MDR certification rules, however, raise compliance costs and slow rollouts, ultimately consolidating supplier ranks.

Asia-Pacific delivers a 7.32% CAGR through 2031. China’s NMPA cleared MicroPort’s VitaFlow Liberty Flex system in 2025, underscoring domestic innovation. Japan leads biodegradable gastrointestinal stents, and India embraces next-generation coronary designs such as Abbott’s XIENCE Sierra. Government insurance expansion and localized manufacturing lower per-procedure costs, broadening market reach.

Competitive Landscape

Industry consolidation continued as Teleflex agreed to acquire Biotronik’s vascular intervention unit for EUR 760 million, while Boston Scientific purchased Silk Road Medical for USD 1.26 billion. Leaders aim to provide complete procedure ecosystems blending stents, guidewires, and AI-planning software. Emerging entrants focus on polymer-hybrid and retrievable designs; Reflow Medical secured FDA de novo status in May 2025 for the Spur retrievable stent, signaling novel competitive angles. Material price instability—especially nitinol—adds cost risk, encouraging vertical integration and diversified sourcing.

Self-Expanding Stents Industry Leaders

-

Medtronic

-

Boston Scientific

-

Abbott

-

Cook Medical

-

BD

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Reflow Medical received FDA de novo clearance for the Spur Peripheral Retrievable Stent System.

- February 2025: Teleflex agreed to acquire Biotronik’s vascular intervention business for EUR 760 million.

- December 2024: Merit Medical’s WRAPSODY Endoprosthesis gained FDA premarket approval, with U.S. commercialization slated for 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the self-expanding stents market as the value of newly manufactured metallic or hybrid lattice devices that spring open once deployed through a delivery catheter into peripheral, carotid, coronary, gastrointestinal, airway, or neurovascular vasculature.

Scope exclusion: Balloon-expandable, bio-absorbable, or any post-market refurbishment units remain outside our scope.

Segmentation Overview

-

By Product Type

- Carotid self-expanding stents

- Gastrointestinal self-expanding stents

- Endovascular / Peripheral self-expanding stents

- Airway / Lung self-expanding stents

- Intracranial self-expanding stents

- Others

-

By Material

- Nitinol

- Cobalt-chromium

- Stainless steel

- Polymer / Hybrid

-

By Application

- Fem-Pop artery

- Iliac artery

- Carotid artery

- Biliary strictures

- Tracheo-bronchial airway

- Intracranial stenosis

- Others

-

By End-User

- Hospitals

- Ambulatory Surgical Centers

- Catheterization Laboratories

-

By Delivery Mode

- Over-the-Wire (OTW) systems

- Through-the-Scope (TTS) systems

- Stent-on-a-Wire systems

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Cardiologists, vascular surgeons, cath-lab managers, and materials scientists across North America, Europe, and Asia-Pacific were interviewed. Their insights refined assumed average selling prices, typical stent length mix, and the speed at which drug-coated balloons are cannibalizing femoropopliteal placements.

Desk Research

We began with public clinical statistics from bodies such as the World Health Organization, the Centers for Disease Control and Prevention, and Eurostat, which let us size the underlying procedure pool for peripheral arterial disease and carotid stenosis. Trade registries like the UN Comtrade and Volza helped our team quantify global flows of nitinol tubing, a proxy for manufacturing output.

Next, our analysts mined regulatory disclosures from the US FDA 510(k) database, the European CE-mark database, and Japan's PMDA to track annual product clearances. Company 10-Ks, device recall notices, and peer-reviewed journals supplied supplementary adoption rates, while paid platforms, D&B Hoovers for revenue splits and Dow Jones Factiva for deal news, rounded out competitive signals. This roster is illustrative and not exhaustive; many other public and subscription sources informed our desk work.

Market-Sizing & Forecasting

We rebuilt demand using a top-down and bottom-up blend. National procedure counts and prevalence data were converted into treatable case pools, which are then multiplied by stent utilization rates and calibrated with sampled ASP × volume roll-ups from distributor channel checks. Key variables like PAD incidence, carotid intervention penetration, nitinol price trends, outpatient shift share, and regulatory approval cadence drive year-on-year changes. Forecasts through 2030 rely on multivariate regression that weights those inputs alongside interview-based consensus on reimbursement shifts. Where supplier roll-ups left gaps, we prorated missing geographies using device import elasticities.

Data Validation & Update Cycle

Our output passes anomalies, variance, and plausibility tests before a senior reviewer signs off. Reports refresh annually, and interim updates trigger when material recalls, guideline changes, or major product launches occur. Just before release, an analyst reruns key checks so clients receive the freshest view.

Why Mordor's Self-Expanding Stents Baseline Inspires Confidence

Published values often diverge because publishers choose different procedure bundles, price points, and refresh cadences. Our disciplined scope selection and variable weighting keep figures reproducible even for junior analysts explaining them on a client call.

Key gap drivers include whether coronary stents are folded into totals, how aggressively outpatient migration is modeled, the currency-conversion month, and the cadence at which aging ASP assumptions are refreshed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.61 B (2025) | Mordor Intelligence | - |

| USD 3.62 B (2025) | Global Consultancy A | Includes bio-absorbable and balloon-expandable units; fewer primary interviews |

| USD 3.80 B (2024) | Trade Journal B | Uses static ASPs and blends coronary with peripheral volumes |

| USD 3.22 B (2022) | Industry Association C | Older base year, limited geographic granularity, no import-export validation |

In sum, because Mordor analysts align scope strictly to mechanical self-expanding devices, refresh critical variables yearly, and validate assumptions through field interviews, our baseline offers a transparent, balanced foundation for strategic planning.

Key Questions Answered in the Report

What is the current size of the self expanding stents market?

The self expanding stents market is valued at USD 3.77 billion in 2026 and is projected to reach USD 4.71 billion by 2031, growing at a 4.53% CAGR.

Which material dominates the self expanding stents market?

Nitinol dominates with 68.77% market share due to its unique shape-memory properties and superior flexibility, though polymer-hybrid composites are growing faster at 7.93% CAGR through 2031.

What is driving growth in the intracranial stent segment?

Intracranial self-expanding stents are growing at 6.58% CAGR due to breakthrough clinical evidence showing drug-eluting designs reduce restenosis rates by 77% compared to bare-metal alternatives.

How are ambulatory surgical centers affecting the self expanding stents market?

Ambulatory surgical centers are the fastest-growing end-user segment at 7.01% CAGR, driven by improved device deliverability, favorable reimbursement policies, and the shift toward outpatient procedures.

Page last updated on: