Pericardial Patches Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

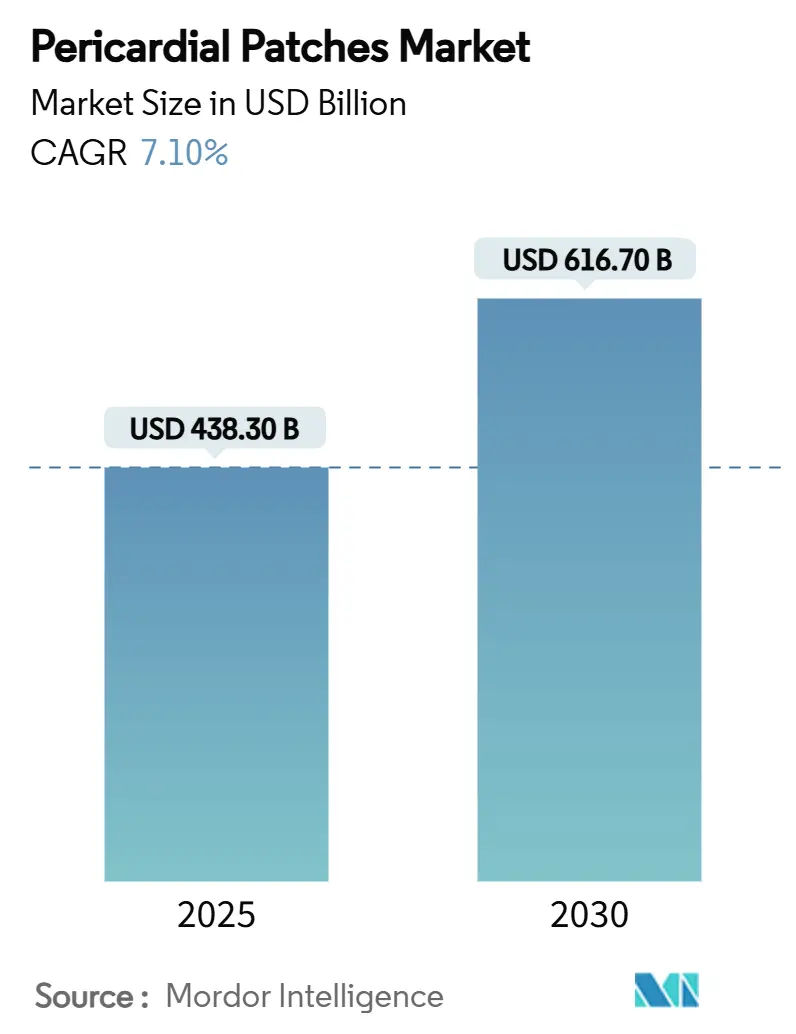

| Market Size (2025) | USD 438.30 Billion |

| Market Size (2030) | USD 616.70 Billion |

| Growth Rate (2025 - 2030) | 7.10% CAGR |

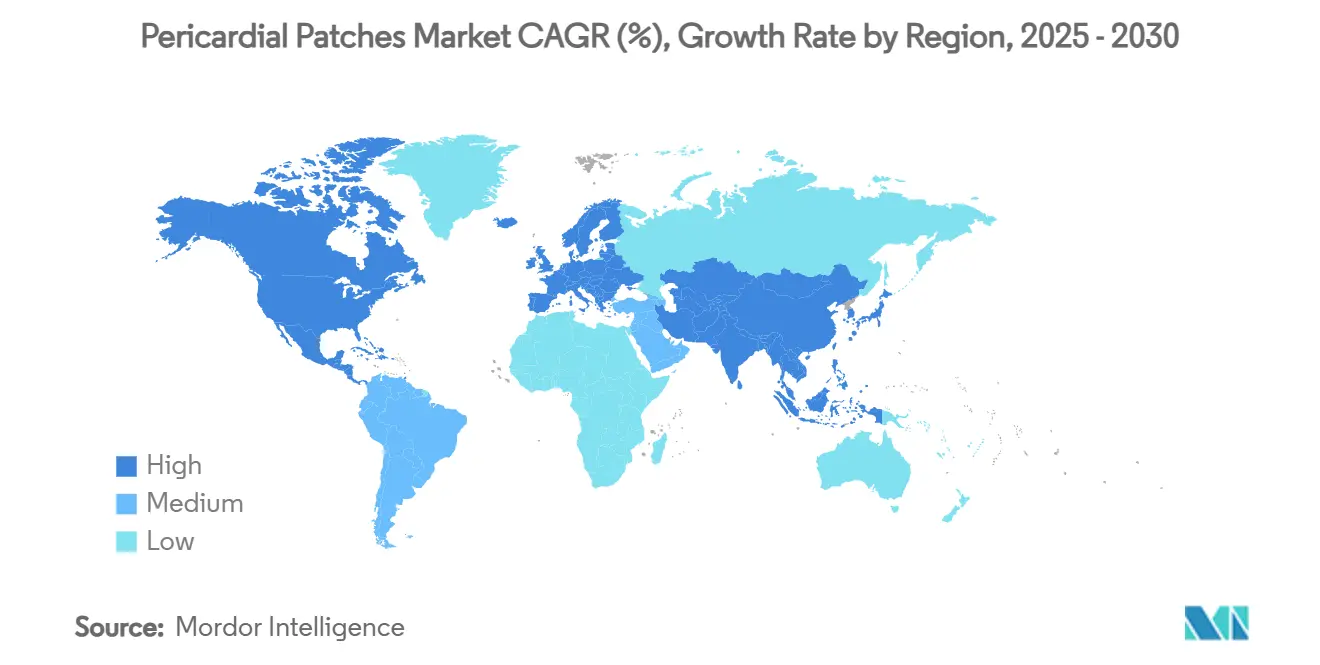

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pericardial Patches Market Analysis by Mordor Intelligence

The pericardial patch market reached a market size of USD 438.3 million in 2025 and is projected to expand at a 7.1% CAGR to USD 616.7 million by 2030. Rising procedure volumes for congenital and acquired cardiac defects, steady substitution of sutures with patch‐based repair, and material innovations that cut re-operation risk are the dominant forces shaping the pericardial patch market. Early adoption of minimally invasive cardiac techniques has tightened the link between advanced patch handling characteristics and surgeon preference. Manufacturers that combine anti-calcification chemistry with refined decellularization are capturing premium price tiers as hospitals prioritize long-term durability over initial acquisition cost. Supply resilience, particularly for bovine tissue, remains a competitive differentiator as global demand outstrips traditional sourcing hubs.

Key Report Takeaways

- By product type, biologic patches held 66.5% of the pericardial patch market share in 2024, whereas synthetic solutions are projected to expand at an 11.2% CAGR through 2030.

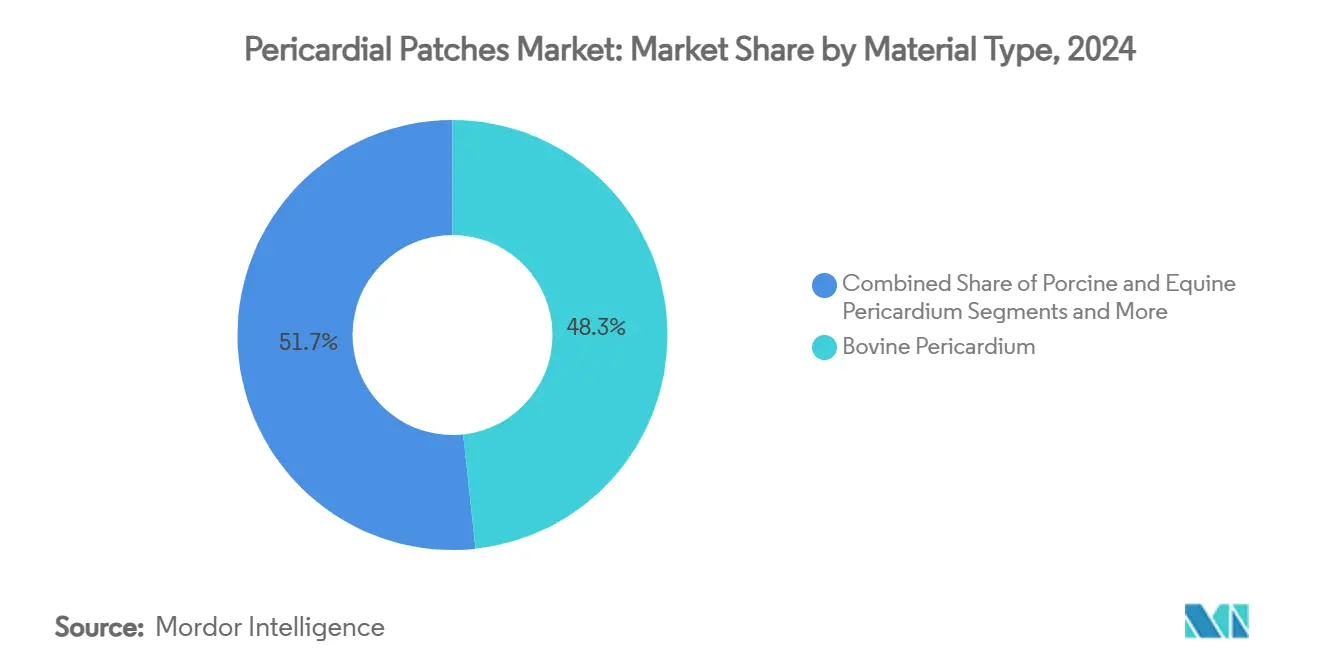

- By material, bovine pericardium accounted for 48.3% of the pericardial patch market size in 2024, while expanded PTFE is the fastest-growing material at an identical 11.2% CAGR.

- By application, cardiac reconstruction generated 42.7% of demand in 2024, yet dural closure is forecast to advance at a 13.4% CAGR to 2030.

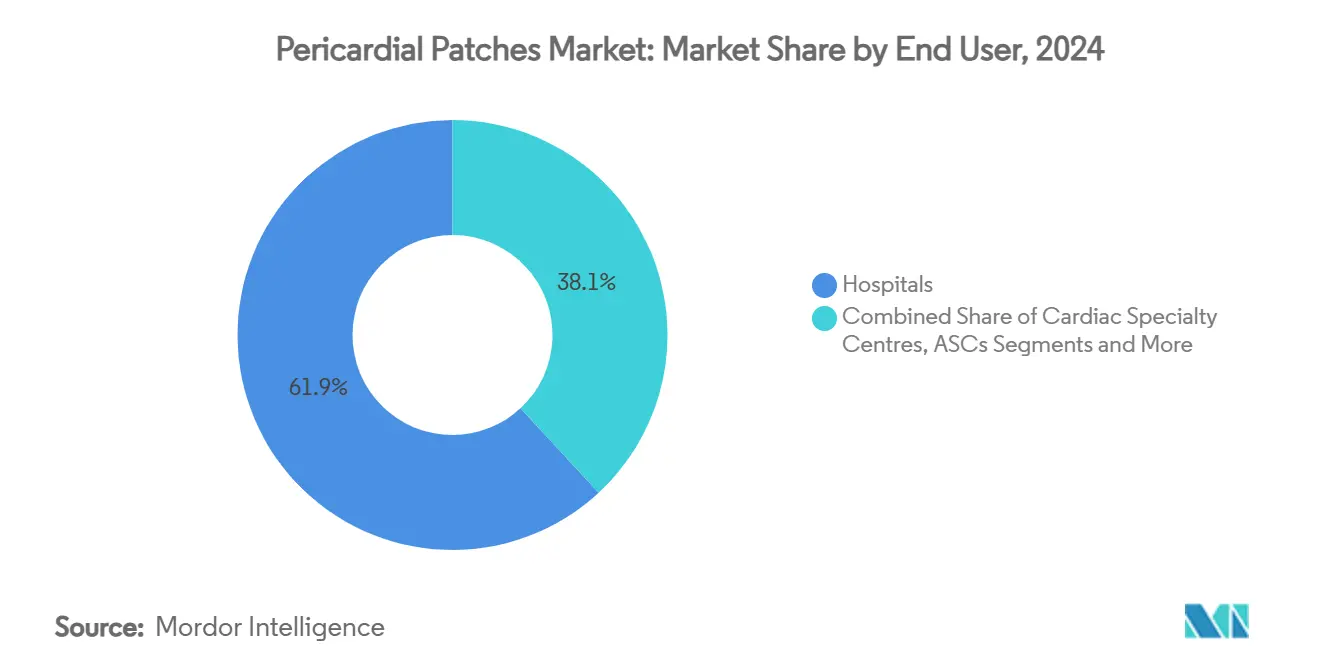

- By end user, hospitals commanded 61.9% revenue share in 2024, whereas ambulatory surgical centers are expanding at a 10.1% CAGR.

- By region, North America led with 38.7% share in 2024, while Asia-Pacific is poised for the quickest growth at an 8.0% CAGR through 2030.

Global Pericardial Patches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of congenital & acquired cardiac defects | +1.80% | Global with concentration in North America & Europe | Long term (≥ 4 years) |

| Growing adoption of minimally invasive cardiac surgery | +1.50% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Ageing population driving valvular repair volumes | +1.20% | Global, particularly developed markets | Long term (≥ 4 years) |

| Decellularized & bio-resorbable scaffold innovation | +0.90% | North America & EU core markets | Medium term (2-4 years) |

| Cross-specialty expansion into neuro/dural repair | +0.80% | Global, early adoption in US & Europe | Short term (≤ 2 years) |

| Fast-track xenopericardial approvals in developing countries | +0.80% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Congenital & Acquired Cardiac Defects

Congenital heart disease affects 1% of live births worldwide, while ageing populations boost acquired defect volumes, creating predictable demand for advanced patches. Studies on ANGPTL4-loaded hydrogels show enhanced vascularization and reduced inflammation, underscoring the shift to bio-active platforms that strengthen repair outcomes.[1]M.K. Lee et al., “Paintable and Adhesive Hydrogel Cardiac Patch With Sustained Release of ANGPTL4,” Bioactive Materials, pubmed.ncbi.nlm.nih.gov Hospitals now specify anti-inflammatory grafts for complex pediatric reconstructions, ensuring the pericardial patch market captures recurring procedure revenues across a patient’s lifetime. Robust screening programs in Europe and North America identify defects earlier, further enlarging the addressable pool and sustaining the driver’s long-term impact.

Growing Adoption of Minimally Invasive Cardiac Surgery

Evidence from a 10-year, 958-patient series confirms zero procedure-related mortality and high repair durability for valve surgeries performed via mini-thoracotomy, with bovine patches used in 87.5% of cases.[2]Anil Sharma et al., “Right Thoracotomy With Central Cannulation for Valve Surgery,” Journal of Cardiothoracic Surgery, doi.org Smaller access ports require pliable, low-bleed materials, prompting suppliers to redesign product geometry for rapid suture anchoring. Ambulatory surgical centers that specialize in minimally invasive repairs report double-digit growth, reinforcing the pericardial patch market’s migration toward outpatient venues and encouraging further device miniaturization.

Ageing Population Driving Valvular Repair Volumes

Patients older than 65 now account for the majority of surgical aortic valve replacements, and survival curves favor bovine pericardium over porcine tissue beyond eight years post-implant. Surgeons opt for patch materials that mirror valve leaflet mechanics, which elevates demand for bovine sources with proven long-term performance. As OECD nations approach median ages above 45, annual case numbers for degenerative valve disease continue to climb, positioning the pericardial patch market for steady expansion in mature health economies.

Decellularized & Bio-Resorbable Scaffold Innovation

Poly(itaconate-co-citrate-co-octanediol) scaffolds trigger lower macrophage infiltration versus glutaraldehyde-fixed grafts, marking a step change in host integration. Manufacturers combine decellularization with anti-calcification chemistries to achieve eight-year freedom-from-failure rates above 99% in aortic positions. Hospitals use these data to justify premium purchasing, and payers increasingly recognize reduced re-intervention costs, amplifying the driver’s CAGR contribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Calcification & infection risk with biologics | -1.40% | Global, particularly developing markets | Medium term (2-4 years) |

| High cost of bovine / porcine-derived patches | -1.10% | Emerging markets, cost-sensitive segments | Short term (≤ 2 years) |

| Ethical & supply challenges for bovine materials | -0.80% | Regions with animal welfare concerns | Long term (≥ 4 years) |

| Sterilization-validation delays for next-gen devices | -0.70% | North America & EU regulatory markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Calcification & Infection Risk with Biologics

Glutaraldehyde-fixed bovine tissue retains mechanical strength but shows variable long-term calcification, driving clinicians to demand additives that quench residual aldehydes. Device makers counter with proprietary rinses, yet pediatric surgeons remain cautious where decades-long graft durability is needed. This restraint curbs full adoption in cost-sensitive regions lacking routine echocardiographic follow-up.

High Cost of Bovine / Porcine-Derived Patches

Bundled reimbursement rules treat pericardial closure as integral to cardiac surgery, limiting standalone billing and squeezing hospital budgets.[3]Society of Thoracic Surgeons, “Coding and Reimbursement,” sts.orgFacilities in Latin America and parts of Africa, therefore, favor synthetic PTFE, dampening biologic sales despite clinical advantages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biologics Maintain Command Amid Synthetic Upswings

Biologic solutions captured 66.5% of the pericardial patch market in 2024 thanks to decades of clinical confidence and lower suture-line bleeding. Edwards’ RESILIA platform posts 99.3% freedom from structural deterioration over eight years, reinforcing surgeon loyalty. Manufacturers scale decellularization lines to boost throughput, underpinning a pericardial patch market size leadership that is expected to persist.

Synthetic offerings are growing at an 11.2% CAGR as ePTFE and microporous polyurethane win contracts in budget-constrained systems. Lower infection risk and batch-to-batch consistency appeal to value purchasers, while R&D on iron-based absorbable meshes could bridge the bio-integration gap. Vendors that can hybridize synthetic scaffolds with collagen coatings may siphon share from traditional xenografts over the forecast frame.

By Material: Bovine Pericardium Leads While ePTFE Accelerates

Bovine tissue held 48.3% of the pericardial patch market share in 2024, supported by studies showing superior resistance to crack propagation versus porcine leaflets. Scalability challenges—spanning feed costs to abattoir traceability—keep input prices high, yet hospitals tolerate premiums for proven longevity.

Expanded PTFE enjoys identical mechanical specifications lot-to-lot and zero animal-welfare debate, helping the segment clock the same 11.2% CAGR. As supply chain unpredictability surrounding bovine tissue intensifies, procurement managers hedge with multi-year PTFE contracts, a trend that supports margin stability for synthetic-only manufacturers.

By Application: Cardiac Reconstruction Dominant, Dural Closure Surging

Cardiac reconstruction generated 42.7% of 2024 revenue, making it the anchor of the pericardial patch market. Transcatheter structural heart programs funnel complex redo surgeries to high-volume centers, where hybrid surgical-catheter techniques rely on pliable patches for atrial or ventricular septal repairs.

Dural closure is the fastest riser, with a 13.4% CAGR. Systematic reviews cite lower cerebrospinal fluid leak rates when bovine pericardium is used for infratentorial repairs, accelerating cross-specialty demand. Neurosurgical uptake encourages suppliers to brand smaller-footprint SKUs that eliminate the need for custom trimming.

By End User: Hospitals Pre-eminent, ASCs Closing the Gap

Hospitals retained 61.9% of revenue in 2024, given their capacity to handle high-risk congenital and redo valve repairs. Teaching hospitals double as clinical trial hubs, ensuring the early deployment of next-generation anti-calcification patches.

Ambulatory surgical centers post a 10.1% CAGR as minimally invasive valve and atrial appendage closure procedures transition to outpatient settings. FDA approvals such as the TriClip G4 broaden the mix of transcatheter repairs suitable for same-day discharge, compelling suppliers to kit patches with hemostatic sealants optimized for ASC workflows.

Geography Analysis

North America controlled 38.7% of 2024 revenue, reflecting robust reimbursement and device innovation ecosystems. The United States alone generated USD 1.0 billion in TAVR sales for Edwards, validating hospital budgets for adjunct patch technologies that ensure durable closures. Canada follows similar clinical pathways, while Mexico’s private cardiovascular chains increasingly import biologic patches to compete on outcomes.

Asia-Pacific is the fastest-growing region at an 8.0% CAGR as China, India and Southeast Asian nations expand cardiac surgery capacity. Streamlined device approval pathways and public investment in tertiary centers are helping the pericardial patch market gain critical mass. Japanese hospitals focus on super-aged patients who demand extended graft durability, a specification that favors high-end bovine and RESILIA-class offerings.

Europe remains a mature yet innovation-centric cluster. Germany and France emphasize lifetime durability metrics during procurement, preserving premium pricing. The EU Medical Device Regulation raises the bar for clinical data, but top suppliers leverage long follow-up registries to maintain market access. Southern and Eastern European systems with tighter budgets balance purchases between bovine and synthetic patches depending on case complexity.

Competitive Landscape

The pericardial patch market has a moderate concentration: the top five companies hold an estimated significant market share. Edwards Lifesciences, Baxter, and LeMaitre Vascular headline the biologic spectrum, each pairing proprietary anti-calcification chemistry with surgeon education programs. In Q2 2024, Edwards posted 7% sales growth, helped by valve and patch synergies that bundle pricing across cardiac service lines.

Technology differentiation drives competition. Proprietary decellularization steps and dry-storage packaging that simplify OR logistics create switching barriers. Suppliers also court neurosurgeons and reconstructive surgeons to diversify revenue beyond cardiac, diluting seasonality tied to elective heart procedures.

Niche innovators such as Aziyo Biologics target bio-resorbable and aseptic-preserved grafts, hoping to bypass glutaraldehyde’s calcification profile. These firms often partner with contract manufacturers to win FDA clearance swiftly, then license distribution to large cardiovascular houses that provide global sales reach.

Pericardial Patches Industry Leaders

Edwards Lifesciences

LeMaitre Vascular

Baxter International

W. L. Gore & Associates

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Teijin announced the launch of a new cardiovascular surgical patch in Japan, expanding product availability in the Asia-Pacific region and demonstrating continued innovation in pericardial patch technologies for cardiac reconstruction applications.

- April 2024: Edwards Lifesciences launched the SAPIEN 3 Ultra RESILIA valve in Europe, utilizing advanced anti-calcification technology that represents breakthrough developments in pericardial tissue processing methods applicable to patch manufacturing.

- February 2024: Edwards EVOQUE Tricuspid Valve Replacement System received FDA approval as an artificial heart valve made from bovine pericardial tissue, demonstrating advanced processing techniques for xenograft materials used in patch applications.

Global Pericardial Patches Market Report Scope

| Biologic Pericardial Patch |

| Synthetic Pericardial Patch |

| Bovine Pericardium |

| Porcine Pericardium |

| Equine Pericardium |

| Autologous (Human) Pericardium |

| Synthetic (ePTFE, PTFE) |

| Cardiac Reconstruction |

| Vascular Reconstruction |

| Dural Closure / Neuro Repair |

| Soft-Tissue / Thoracic Repair |

| Others |

| Hospitals |

| Cardiac Specialty Centres |

| Ambulatory Surgical Centres |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Biologic Pericardial Patch | |

| Synthetic Pericardial Patch | ||

| By Material | Bovine Pericardium | |

| Porcine Pericardium | ||

| Equine Pericardium | ||

| Autologous (Human) Pericardium | ||

| Synthetic (ePTFE, PTFE) | ||

| By Application | Cardiac Reconstruction | |

| Vascular Reconstruction | ||

| Dural Closure / Neuro Repair | ||

| Soft-Tissue / Thoracic Repair | ||

| Others | ||

| By End User | Hospitals | |

| Cardiac Specialty Centres | ||

| Ambulatory Surgical Centres | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the pericardial patch market in 2025?

The pericardial patch market size stands at USD 438 million in 2025 and is forecast to grow at a 7.0% CAGR to USD 616 million by 2030.

Which material accounts for the highest share of sales?

Bovine pericardium leads with 48.3% share, favored for its mechanical strength and long-term durability.

What segment is expanding the fastest?

Dural closure applications are registering a 13.4% CAGR as neurosurgeons shift to bovine patches for lower cerebrospinal fluid leak rates.

Which region shows the quickest growth through 2030?

Asia-Pacific is projected to advance at an 8.0% CAGR, propelled by expanding cardiac care infrastructure in China and India.

Who are the top players to watch?

Edwards Lifesciences, Baxter International, and LeMaitre Vascular hold leading positions, each investing in anti-calcification and minimally invasive solutions.

Page last updated on: