Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

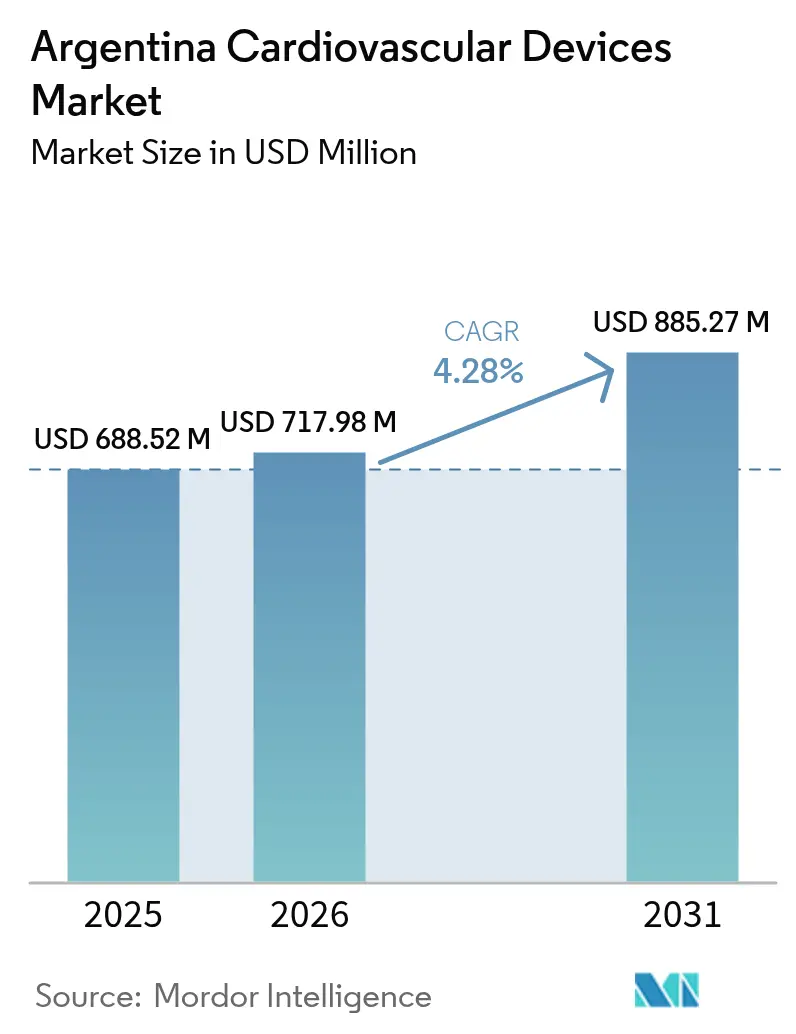

| Base Year Market Size (2025) | USD 688.52 Million |

| Market Size (2026) | USD 717.98 Million |

| Market Size (2031) | USD 885.27 Million |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

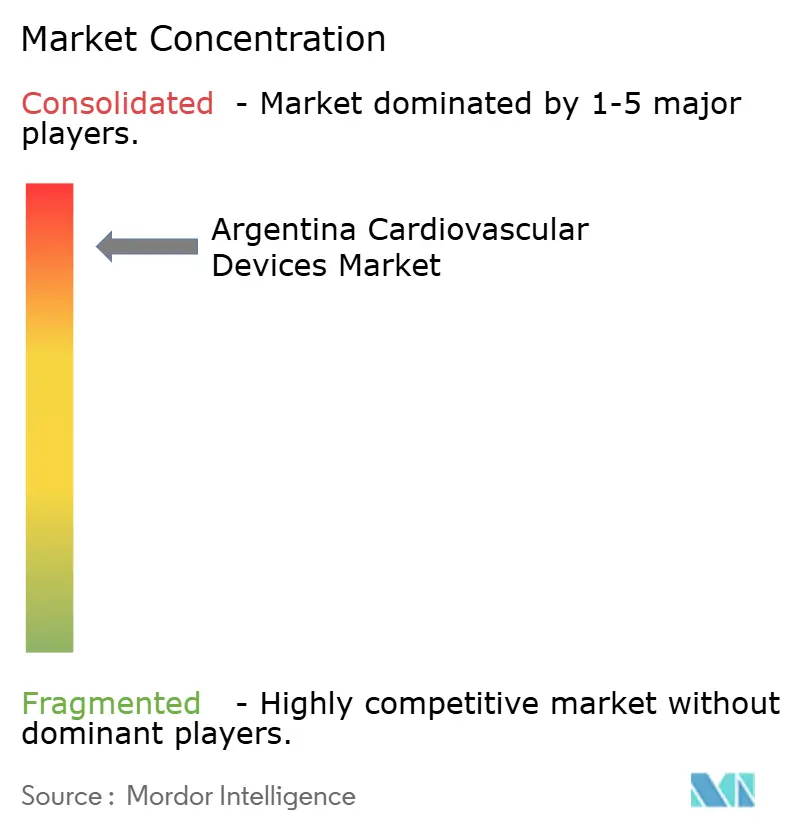

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Cardiovascular Devices Market Analysis by Mordor Intelligence

Argentina Cardiovascular Devices Market size in 2026 is estimated at USD 717.98 million, growing from 2025 value of USD 688.52 million with 2031 projections showing USD 885.27 million, growing at 4.28% CAGR over 2026-2031.

High‐risk patient concentrations, rapid private‐insurance uptake, expanded cath‐lab capacity, and a streamlined ANMAT fast-track pathway are enlarging procedure volumes, especially for coronary, electrophysiology, and structural-heart interventions. Currency depreciation is accelerating leasing and pay-per-use models that lower up-front costs for hospitals, while domestic trade pacts with Brazil intensify price competition in entry-level segments. Multinational manufacturers are localizing supply chains to counter customs delays and are launching tiered portfolios to accommodate premium and value-oriented buyers. On the demand side, provincial workforce shortages are elevating interest in remote monitoring and wearable diagnostics to bridge gaps in specialist care. Collectively, these forces are steering the Argentina cardiovascular devices market toward solutions that balance clinical sophistication with affordability.

Key Report Takeaways

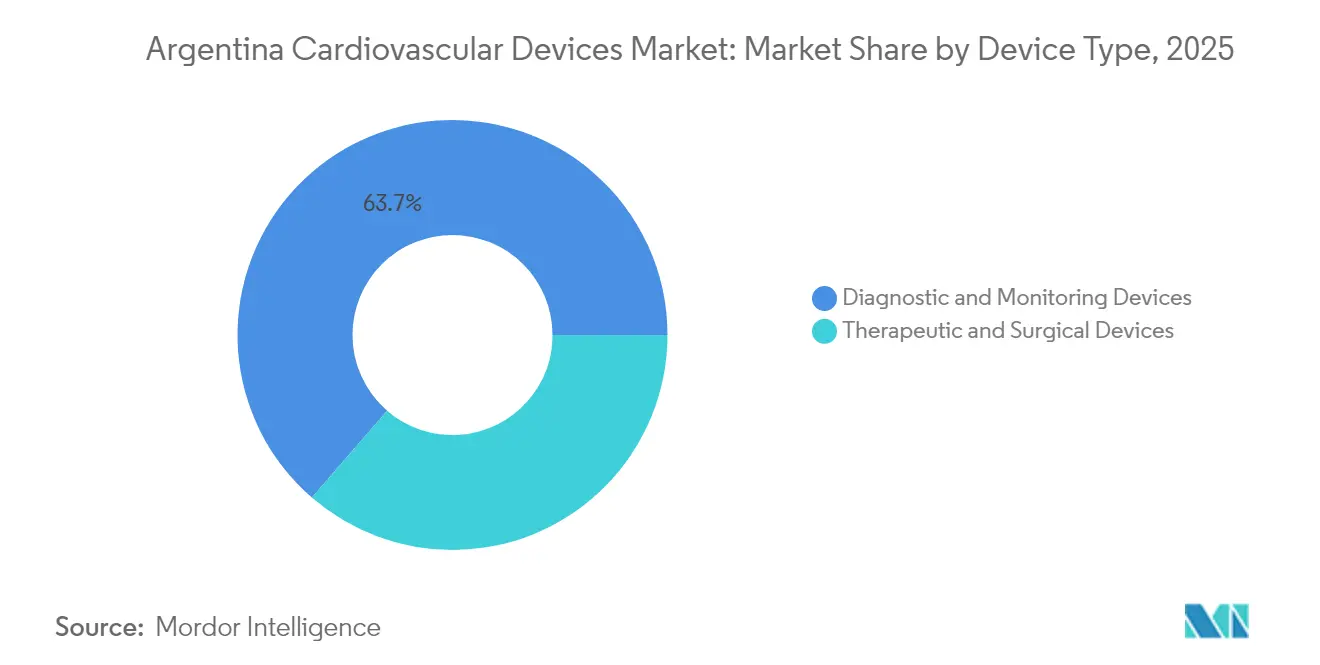

- By device type, diagnostic & monitoring solutions held 63.65% of the Argentine cardiovascular devices market share in 2025, and this segment is advancing at a 4.97% CAGR through 2031.

- By application, coronary artery disease accounted for 41.72% Argentina's cardiovascular devices market size in 2025 and remains the largest revenue contributor; structural heart disease is projected to expand at the fastest 5.78% CAGR between 2026 and 2031.

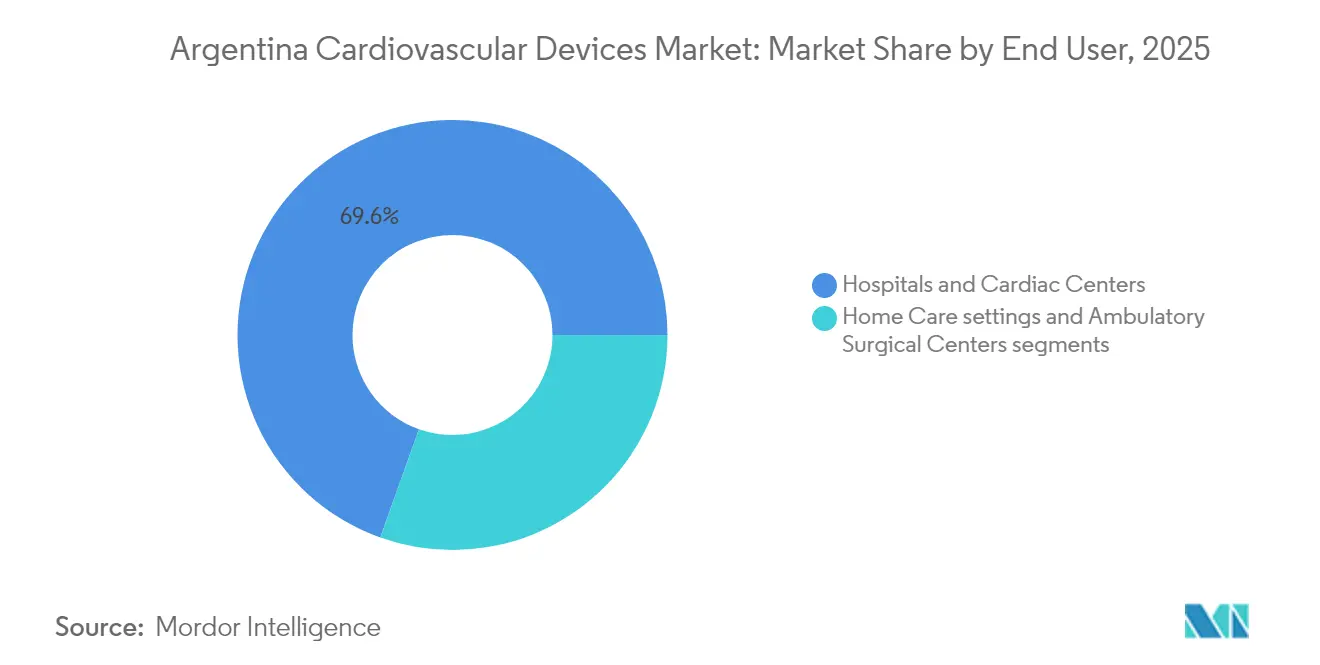

- By end-user, hospitals & cardiac centers commanded 69.55% of the Argentine cardiovascular devices market in 2025, whereas home-care settings led growth with a 6.52% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| High Prevalence of Hypertensive & Diabetic Population Concentrated | +1.8 | National, with concentration in urban centers | Long term (≥ 5 yrs) |

| Rapid Uptake of Private Health Insurance Driving Elective Interventional Procedures | +1.2 | Urban centers, particularly Buenos Aires | Medium term (~ 3-4 yrs) |

| Expansion of Cath-Lab Infrastructure | +0.9 | Major cities, with limited expansion in provincial areas | Medium term (~ 3-4 yrs) |

| ANMAT Fast-Track Pathway for High-Risk Cardiovascular Implants (2024) Easing Market Entry | +0.7 | National | Short term (≤ 2 yrs) |

| Argentine Peso Depreciation Spurring Imported Device Leasing & Pay-per-Use Models | +0.6 | National, with higher impact in private healthcare sector | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

High Prevalence of Hypertensive & Diabetic Population

Argentina cardiovascular devices market growth is strongly anchored in disease burden. Registry data show 22.3% of STEMI patients arrive with heart failure, raising in-hospital mortality to 28.4% and underscoring the need for hemodynamic monitoring, implantable cardioverter defibrillators, and mechanical-circulatory support [1]Source: Gustavo Massoullié, “Heart Failure at Admission Complicating ST-Elevation Myocardial Infarction in a Middle-Income Country,” Current Problems in Cardiology.. Nationwide hypertension surveillance identifies uncontrolled blood pressure as the leading modifiable risk factor, elevating demand for ambulatory pressure monitors and wearable diagnostics [2]Source: Ministerio de Salud de la Nación, “Enfermedades Cardiovasculares,” Argentina.gob.ar.. Device makers are consequently prioritizing multi-parameter implants capable of managing comorbid profiles rather than single-indication tools.

Rapid Uptake of Private Health Insurance

Elimination of premium caps allowed insurers to raise prices by up to 40% in 2024, unlocking richer benefit tiers for higher-income groups and stimulating demand for elective TAVR, atrial-fibrillation ablation, and leadless-pacemaker procedures. Hospitals in the private network now perform 3.6 elective interventions for every public-sector case, shifting OEM marketing budgets toward premium product lines. Simultaneously, public hospitals face slowing replacement cycles, pushing suppliers to introduce stripped-down versions of flagship devices.

Expansion of Cath-Lab Infrastructure

Argentina added 21 catheterization suites between 2022 and 2024, raising the installed base to 127 and widening access to coronary, structural, and peripheral interventions. Yet equipment prices rose 300–500% in local-currency terms, while reimbursement rates stagnated, prompting hospitals to focus on high-acuity cases over profitability. Suppliers with modular upgrade paths and outcome-based pricing are gaining traction by letting providers scale capabilities incrementally.

ANMAT Fast-Track Pathway for High-Risk Implants

ANMAT introduced a streamlined dossier review in 2024 that reduces testing redundancies for Class III and IV cardiovascular devices. Early adopters reported approval cycles compressing to under 8 months for next-generation heart-valve and electrophysiology systems, shortening the lag between global launch and Argentine debut. This predictability is incentivizing multinational firms to include Argentina in the first wave of regional rollouts, thereby increasing the domestic pipeline for novel therapies and contributing 0.7 percentage points to CAGR.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Limited Reimbursement Coverage for Next-Gen TAVR & VAD Procedures | -1.5 | National | Medium term (~ 3-4 yrs) |

| Shortage of Electrophysiologists Outside Buenos Aires Province | -0.8 | Provincial areas outside Buenos Aires | Long term (≥ 5 yrs) |

| Competing Domestic Policies Favouring Low-Cost Brazilian Imports | -0.7 | National, with higher impact on public healthcare sector | Medium term (~ 3-4 yrs) |

| Persistent Customs Delays Increasing Lead-Times for Life-Saving Implants | -0.5 | National, affecting all import-dependent procedures | Short term (≤ 2 yrs) |

| Source: Mordor Intelligence | |||

Shortage of Electrophysiologists Outside Buenos Aires

Argentina counts fewer than 80 board-certified electrophysiologists, and 62% practice in the capital, restricting advanced rhythm-management procedures in provincial hospitals. Remote monitoring of cardiac implantable electronic devices in elderly cohorts reduced unscheduled visits by 38% in multicenter trials, underscoring tele-cardiology's role in mitigating manpower shortages. Device vendors promoting cloud-connected implants and AI-based arrhythmia triage are differentiating themselves in underserved provinces.

Competing Domestic Policies Favoring Low-Cost Brazilian Imports

Mercosur duty exemptions and currency differentials allow Brazilian suppliers to undercut multinationals on commoditized ECGs, monitors, and basic catheters. Public tenders now specify price ceilings aligned with Brazilian benchmarks, squeezing gross margins of premium brands. In response, global OEMs are rebadging previous-generation products as value lines to retain share while preserving flagship pricing in private hospitals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Diagnostics Scale, Therapeutics Diversify

Diagnostics & monitoring devices accounted for 63.65% of the Argentina cardiovascular devices market size in 2025, due to their broad applicability across primary, secondary, and tertiary care. ECG, Holter, and transthoracic echo platforms remain staples; demand is reinforced by AI-enabled decision support that reduces interpretation time. Strong 4.97% CAGR through 2031 is underpinned by rising home-monitoring adoption and continuous device miniaturization. The Argentine cardiovascular devices market also benefits from hospitals adopting integrated ultrasound-angiography suites that lower referral leakage and improve throughput.

Therapeutic & surgical devices trail in volume yet punch above their weight in value, with DES, bioresorbable scaffolds, and leadless pacemakers attracting the bulk of R&D dollars. Pricing pressure intensified once the peso devaluation magnified USD-denominated import costs. Hospitals, therefore, prioritize devices with proven outcomes, such as drug-coated balloons, in small-vessel disease. Suppliers that can package implants with flexible financing and local physician-training retain an advantage in the expanding therapeutic share of the Argentina cardiovascular devices market.

By Application: Coronary Pre-eminence, Structural Heart Ascent

Coronary artery disease interventions commanded 41.72% of Argentina cardiovascular devices market share in 2025, anchored by mature PCI pathways and high STEMI incidence. Disposable volumes remain high despite reimbursement tensions because balloon-preparation and DES kits are viewed as life-saving essentials. Forward growth, however, is moderated by plateauing primary PCI volumes in densely populated urban areas.

Structural heart disease is the fastest-growing application, with a projected 5.78% CAGR. TAVR procedural indications broadened to intermediate-risk patients, while mitral and tricuspid repair devices move from trial to early commercial stages. Procedural success rates of above 95% in cases of pure aortic regurgitation have shifted referral patterns toward less invasive solutions. Heart-failure management devices, including implantable hemodynamic sensors, are gaining purchase as hospitals seek tools that reduce readmissions.

By End-User: Hospital Core, Home-Care Velocity

Hospitals & cardiac centers controlled 69.55% of Argentina cardiovascular devices market size in 2025, aided by concentrated cath-lab capacity and nuclear imaging assets, including 389 SPECT and 42 PET scanners. Economic headwinds, however, forced administrators to ration electives when reimbursement failed to offset the costs of imported stents. Hospitals, therefore, gravitate toward platforms that maximize multi-disciplinary use and minimize per-case consumable expense.

Home-care settings, advancing at 6.52% CAGR, leverage remote CIED monitoring and wearable ECG patches that transmit data directly to cloud dashboards. Pay-per-use subscription models make adoption financially feasible for provincial clinics that lack capital budgets. The influx of AI triage algorithms that flag actionable arrhythmia events in real-time further accelerates uptake, reinforcing home care’s rising role in the Argentine cardiovascular devices market.

Geography Analysis

Buenos Aires province generated 47.35% of national cardiovascular procedures in 2025, benefiting from 62% of the country’s electrophysiology workforce and the densest cath-lab network. This concentration shapes corporate launch strategies that prioritize key opinion leader (KOL) adoption in urban centers before rolling out to secondary cities. The Argentina cardiovascular devices market size for Buenos Aires is growing 6.12% annually as private insurers finance elective structural-heart interventions.

The Central corridor comprising Córdoba, Rosario, and Santa Fe contributed 28.15% of procedure volumes and is expanding at 7.62% CAGR, propelled by aggressive private-hospital expansion. Provincial governments co-invest in tele-cardiology hubs that connect rural clinics to urban specialists, fostering demand for remote monitoring devices. Vendors offering cloud-based arrhythmia analytics see 30% of their national sales in this corridor.

The Northwest and Patagonian regions combined deliver only 24.50% of interventional activity but are forecast to post the highest CAGR at 8.88% through 2031, aided by mining revenue and public-private partnerships. However, these areas face longer customs lead times because freight enters via Buenos Aires before overland transport. Distributors with regional warehouses cut delivery cycles by half, gaining share against rivals limited to capital depots.

Competitive Landscape

Five multinational firms—Medtronic, Abbott, Boston Scientific, Edwards Lifesciences, and Terumo—held majority of Argentina cardiovascular devices market revenue in 2024. Local distributor Promedon partners with Brazilian OEMs to supply cost-effective diagnostic catheters, underscoring regional price sensitivity.

Strategic moves include Medtronic’s 2025 launch of a peso-denominated leasing program that bundles cath-lab robotics, imaging, and service. Abbott established a Córdoba training center offering hands-on TAVI simulations that certified 60 interventional cardiologists within its first year. Boston Scientific introduced risk-sharing contracts that refund stent costs if target lesion revascularization exceeds 6% at 12 months. Domestic firm Griensu installed a bonded warehouse near Ezeiza airport to slash customs clearance times by 40%.

Argentina Cardiovascular Devices Industry Leaders

W. L. Gore & Associates, Inc

Siemens Healthineers AG

Medtronic PLC

Canon Medical Systems Corporation

Philips Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Baird Medical Investment Holdings Ltd., a prominent provider of Microwave Ablation (MWA) technology, secured regulatory approval for its systems in Argentina. This achievement propels the company's global expansion efforts and aligns with its mission to enhance patient access to effective, minimally invasive cardiovascular treatments, among others.

- February 2024: Government deregulated private health-insurance pricing, triggering premium hikes of up to 40% and reshaping demand for elective cardiovascular procedures.

- December 2024: ANMAT issued Disposición 11362/2024 to update health-product labeling under the Healthy Food Promotion Law, reaffirming its active oversight of medical-device regulation

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts every new cardiovascular device that reaches Argentine healthcare providers, from wearable ECG monitors through implantable heart valves, as long as the device is regulated by ANMAT under Class II-IV active or passive cardiac technology.

Scope Exclusion: refurbished or reprocessed hardware is not included, even when sold with a fresh warranty.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- ECG Systems

- Remote Cardiac Monitor

- Cardiac MRI

- Cardiac CT

- Echocardiography / Ultrasound

- Fractional Flow Reserve (FFR) Systems

- Therapeutic & Surgical Devices

- Coronary Stents

- Drug-Eluting Stents

- Bare-Metal Stents

- Bioresorbable Stents

- Catheters

- PTCA Balloon Catheters

- IVUS/OCT Catheters

- Cardiac Rhythm Management

- Pacemakers

- Implantable Cardioverter Defibrillators

- Cardiac Resynchronization Therapy Devices

- Heart Valves

- TAVR/TAVI

- Mechanical Valves

- Tissue/Bioprosthetic Valves

- Ventricular Assist Devices

- Artificial Hearts

- Grafts & Patches

- Other Cardiovascular Surgical Devices

- Coronary Stents

- Diagnostic & Monitoring Devices

- By Application

- Coronary Artery Disease

- Arrhythmia

- Heart Failure

- Structural Heart Disease

- Hypertension

- Others

- By End-User

- Hospitals & Cardiac Centers

- Home-Care Settings

- Ambulatory Surgical Centers

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed interventional cardiologists in Buenos Aires, supply-chain managers at private hospitals in Cordoba, and device importers serving Patagonia. Structured questionnaires validated unit volumes, typical lease rates, and uptake hurdles, while short web surveys reached home-monitoring users to gauge out-of-pocket spending.

Desk Research

We began with public datasets from the National Ministry of Health, INDEC trade statistics, PAHO mortality dashboards, and the Central Bank's import records, which together sketch the nation's demand pool, price bands, and shipment flows. Supplementary context came from trade associations such as the Argentine Society of Cardiology, peer-reviewed journals (Revista Argentina de Cardiologia), and press releases captured through Dow Jones Factiva. Company 10-Ks and local distributor filings helped us map channel margins and average selling prices.

D&B Hoovers, Questel patent analytics, and ANMAT approval archives were then mined for competitive intensity indicators, pipeline launches, and technology refresh rates. The sources cited illustrate our coverage; many other documents and databases were also consulted to cross-check facts and fill data gaps.

Market-Sizing & Forecasting

A top-down reconstruction starts with procedure counts and prevalence-to-treated cohorts, multiplies them by device utilization ratios, and adjusts for public versus private insurance coverage. Results are corroborated with selective bottom-up checks, sampled distributor volumes, and blended ASP × units before finalizing totals. Key model drivers include hypertension prevalence trends, cath-lab capacity additions, ANMAT clearance lead times, import duty shifts, peso-dollar exchange forecasts, and replacement cycles for rhythm-management implants. Multivariate regression with scenario analysis projects these variables to 2030, allowing us to stress-test best and worst-case paths.

Data Validation & Update Cycle

Every draft model passes an anomaly screen, peer review, and senior sign-off. We refresh assumptions annually and trigger mid-cycle updates whenever currency swings above 15 percent or a major reimbursement policy changes. Clients receive an analyst re-check just before delivery.

Why Mordor's Argentina Cardiovascular Devices Baseline Stand Up to Scrutiny

Published estimates rarely align because firms choose different device lists, pricing assumptions, and refresh cadences.

Key gap drivers we uncovered include narrower product baskets that omit single-use catheters, aggressive use of factory-gate prices without channel mark-ups, and forecasts built on generic Latin American growth rates rather than Argentine inflation-adjusted purchasing power.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 688.5 M (2025) | Mordor Intelligence | - |

| USD 201.4 M (2025) | Regional Consultancy A | Excludes diagnostic wearables and applies unverified 30 percent import duty rebate |

| USD 250 M (2023) | Trade Journal B | Uses pre-pandemic base year and rolls forward with flat 5 percent CAGR, ignoring peso depreciation |

These comparisons show that when scope breadth, local price inflation, and real procedure counts are applied consistently, Mordor's baseline offers executives a balanced, transparent figure they can trace to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

How large is the Argentina cardiovascular devices market in 2026?

It stands at USD 717.98 million in 2026 and is forecast to grow at a 4.28% CAGR to USD 885.27 million by 2031.

Which device category holds the largest share?

Diagnostic & monitoring solutions held a 63.65% revenue share in 2025, driven by broad usage across primary, secondary, and tertiary care.

What is the key growth driver for structural-heart devices?

The ANMAT fast-track pathway reduces approval timelines, boosting adoption of TAVR and related implants.

How are peso fluctuations influencing purchasing decisions?

Currency depreciation is pushing hospitals toward leasing and pay-per-use models that lower up-front capital requirements.

Why is specialist shortage a concern outside Buenos Aires?

Only 38% of electrophysiologists practice in provincial regions, limiting access to advanced rhythm-management procedures and spurring demand for remote monitoring solutions.

Page last updated on: