Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

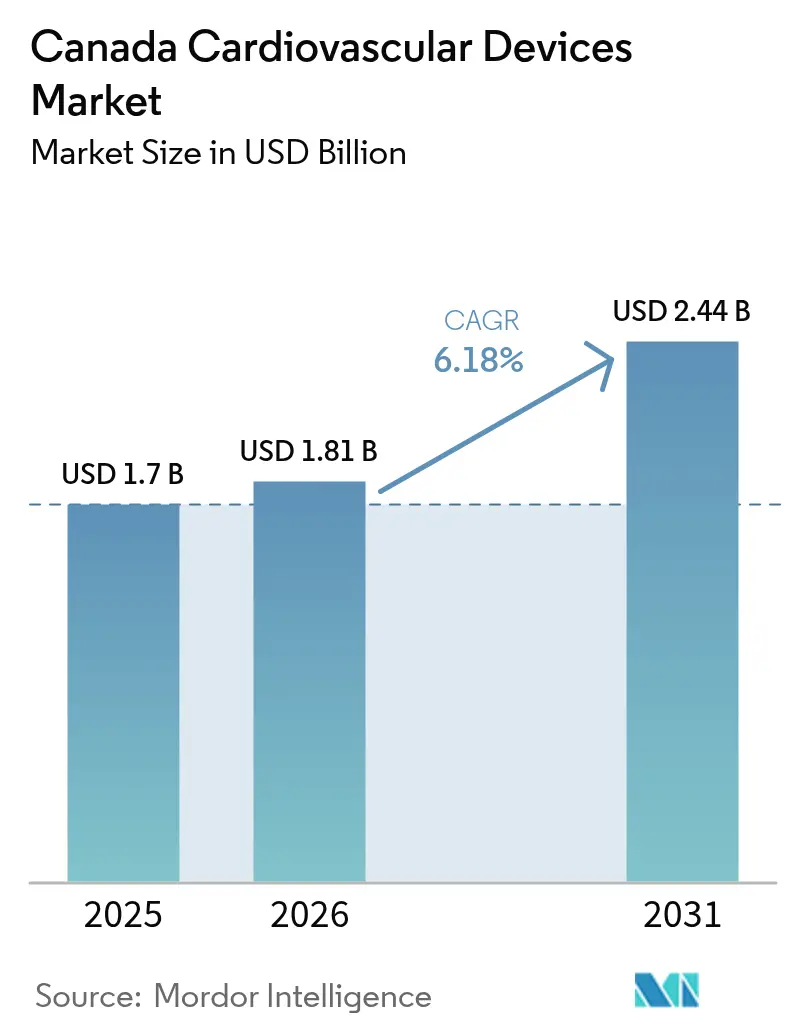

| Base Year Market Size (2025) | USD 1.7 Billion |

| Market Size (2026) | USD 1.81 Billion |

| Market Size (2031) | USD 2.44 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

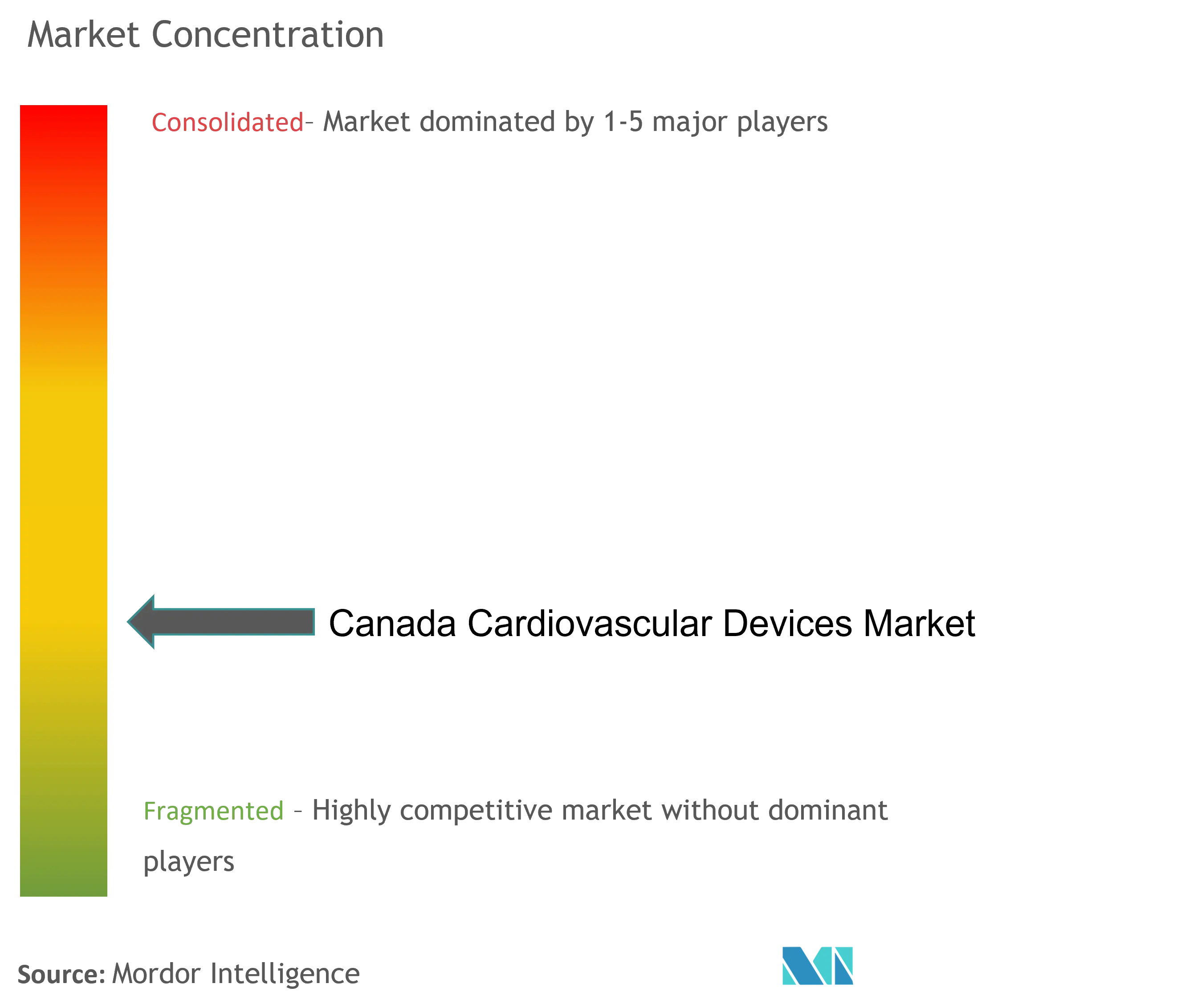

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canada Cardiovascular Devices Market Analysis by Mordor Intelligence

The Canada cardiovascular devices market size in 2026 is estimated at USD 1.81 billion, growing from 2025 value of USD 1.7 billion with 2031 projections showing USD 2.44 billion, growing at 6.18% CAGR over 2026-2031. Growing procedure volumes tied to an aging population, provincial capital spending on cardiac catheterization labs, and the rapid expansion of remote patient monitoring platforms are setting a durable growth foundation for the Canada cardiovascular devices market. Solid gains are occurring even as centralized group purchasing organizations (GPOs) negotiate lower unit prices, forcing manufacturers to prove quantifiable clinical and economic value. Provincial commitments such as Ontario’s USD 31 million Windsor cath-lab expansion and Alberta’s fast-tracked Red Deer opening are intensifying competition among suppliers vying for procurement lots. Meanwhile, the Medical Device Single Audit Program (MDSAP) is compressing regulatory timelines, although Health Canada approvals for next-generation ablation catheters continue to lag FDA clearances by several months.

Key Takeaways

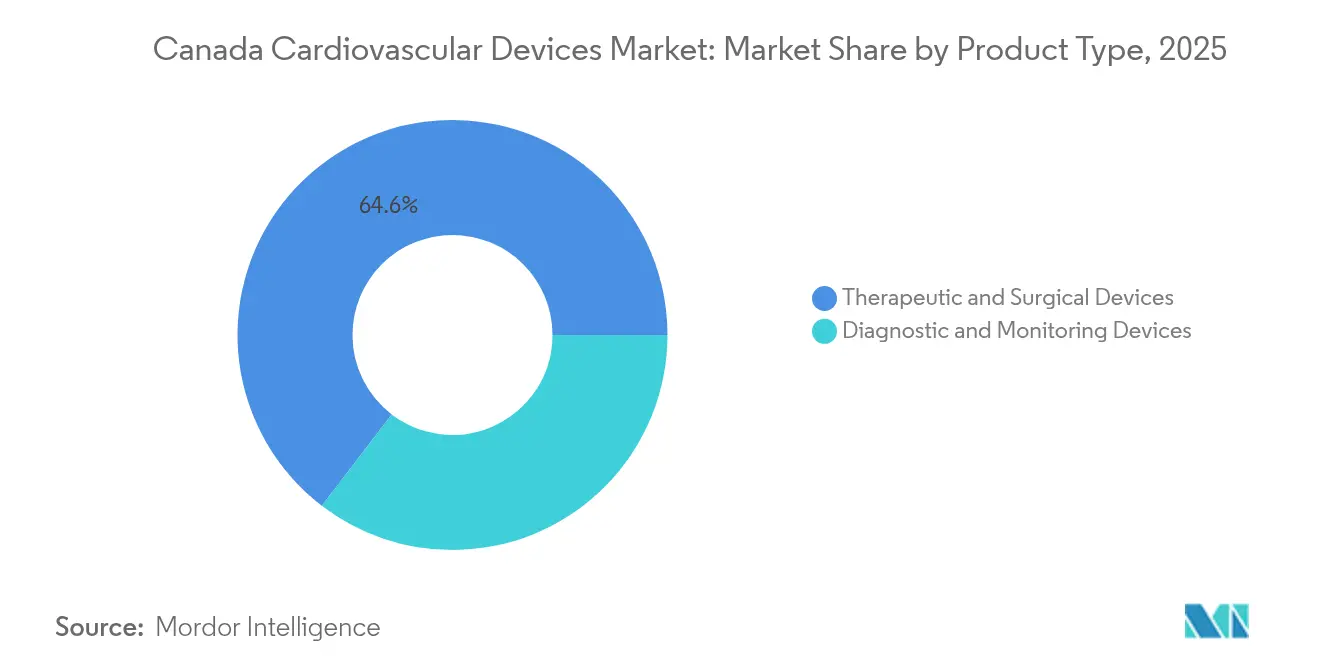

- By product type, therapeutic and surgical devices led with 64.60% of the Canada cardiovascular devices market share in 2025, whereas diagnostic and monitoring devices are projected to post the fastest 6.7% CAGR through 2031

- By application, coronary artery disease dominated 2025 revenue with 40.10% share of the Canada cardiovascular devices market size, while heart failure and cardiomyopathy are forecast to expand at a 6.95% CAGR between 2026-2031

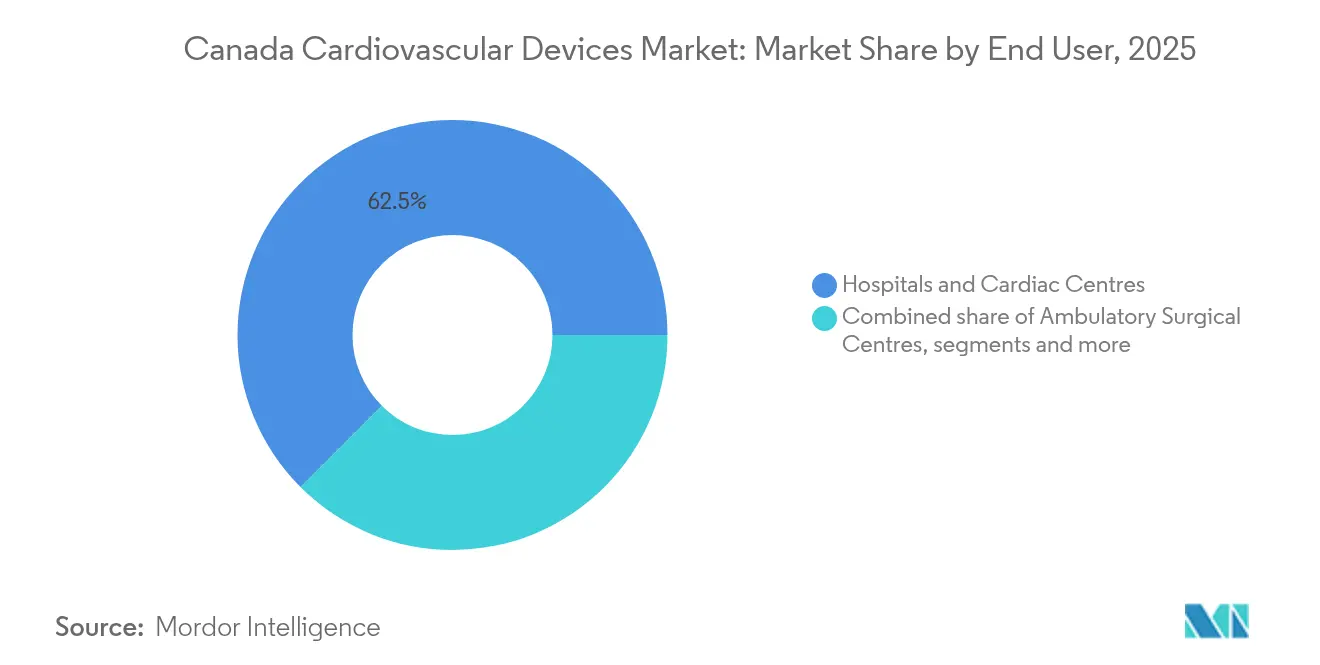

- By end user, hospitals controlled 62.50% of the Canada cardiovascular devices market size in 2025, but home-care settings are on track for a 6.55% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Cardiovascular Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population Driving Procedure Volumes | +1.8% | National, with concentration in Ontario, Quebec, and British Columbia | Long term (≥5 yrs) |

| Provincial Funding for New Catheterization & EP Labs | +1.2% | Ontario, Quebec, Alberta, with limited impact in British Columbia | Medium term (≈3-4 yrs) |

| Rapid Uptake of Minimally-Invasive Transcatheter Therapies | +0.9% | Urban centers with tertiary care facilities, limited rural penetration | Medium term (≈3-4 yrs) |

| Elevated Diabetes & Obesity Rates among Indigenous Populations | +0.7% | Northern territories, rural communities, Indigenous reserves | Long term (≥5 yrs) |

| MDSAP Harmonization Streamlining Device Approvals | +0.6% | National, with greater impact for multinational manufacturers | Short term (≤2 yrs) |

| Med-tech Clusters Fueling Domestic Innovation | +0.4% | Toronto, Vancouver, with limited spillover to other regions | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Aging Population Driving Procedure Volumes

Nineteen percent of Canadians are now 65 or older, a proportion projected to rise steadily through 2030[1]Statistics Canada. "Canadian Population Demographics and Health Statistics." March 2025. www150.statcan.gc.ca. . Seniors account for 27% of diagnosed ischemic heart disease cases, creating sustained demand for advanced stents, valve implants, and monitoring devices. Beyond sheer volume, older patients present higher comorbidity loads, steering hospitals toward minimally invasive approaches that lower perioperative risk. Device makers are therefore prioritizing smaller-profile catheters and AI-assisted imaging that simplify complex anatomies and shorten recovery times. Provincial health ministries increasingly link capital budgets to population-aging metrics, reinforcing the long-term pull on the Canada cardiovascular devices market.

Provincial Funding for New Catheterization & EP Labs

Ontario’s USD 31 million Windsor Regional Hospital project will add a second cath table and enable 24-hour service, addressing local wait lists and lifting utilization of coronary guide wires, drug-eluting stents, and hemostasis devices. Alberta’s decision to open Red Deer’s lab five years early has similar ripple effects, boosting demand for radiopaque contrast, radial access kits, and mapping catheters in the region. Quebec’s St. Mary’s General Hospital, funded for a third lab, now manages 43% higher patient throughput than comparable facilities, amplifying purchases of ablation consoles and structural heart closure systems. Collectively, these targeted outlays are reshaping procurement schedules and intensifying supplier competition in the Canada cardiovascular devices market.

Rapid Uptake of Minimally Invasive Transcatheter Therapies

Saskatchewan’s 2025 launch of an Interventional Tricuspid Valve Repair Program underscores provincial determination to cut surgical backlogs via catheter-based solutions[2]Government of Saskatchewan. "Saskatchewan Expands In-Province Cardiac Care with New Specialized Procedure." September 2024. www.saskatchewan.ca. . Wait-time studies suggest that timely transcatheter access could trim mortality for high-risk patients by 29%. Hospitals consequently allocate more budget to steerable sheaths, closure devices, and transcatheter valve platforms, accelerating revenue migration from open-surgery cannulas to minimally invasive portfolios. Urban cardiac centers also report shorter ICU stays and bed-day savings, buttressing value-based procurement arguments amid GPO price negotiations.

Elevated Diabetes & Obesity Rates among Indigenous Populations

First Nations communities experience heart-disease prevalence of 17% versus 7% among non-Indigenous Canadians. Earlier onset of coronary disease tilts demand toward durable stents and longer-life implantable devices able to serve younger patients. Remote northern settings further elevate the need for handheld ultrasound probes and cloud-connected ECG patches that enable immediate triage before air transfers. Device firms partnering with Indigenous health services are piloting culturally responsive education modules that highlight technology outcomes, aiming to raise usage rates and narrow treatment gaps.

Restraint Imoact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Provincial GPOs Compress Premium-Device Pricing | -1.2% | National, with strongest effect in provinces with centralized procurement | Medium term (≈3-4 yrs) |

| Health Canada Licence Lag for Next-Gen Ablation Catheters | -0.8% | National, with greater impact on electrophysiology segment | Short term (≤2 yrs) |

| Rural Dispersion Limiting Access to Advanced Cardiology | -0.7% | Rural communities across all provinces, particularly in Northern territories | Long term (≥5 yrs) |

| Reimbursement Push-back After High-Profile Implant Recalls | -0.4% | National, with greater impact on implantable device segments | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Provincial GPOs Compress Premium-Device Pricing

Value-oriented tenders from organizations such as HealthPRO and Mohawk MedBuy are generating 8-12% price reductions on premium cardiovascular products. Suppliers must now furnish longitudinal cost-effectiveness data and real-world outcome evidence to secure formulary positions, raising pre-sale investment requirements. Tiered rebate structures tied to readmission metrics are also gaining traction, incentivizing manufacturers to support post-implant remote monitoring and training programs.

Health Canada Licence Lag for Next-Gen Ablation Catheters

Johnson & Johnson’s VARIPULSE pulse-field platform obtained Health Canada clearance in July 2024, months after its U.S. authorization, highlighting enduring lag times. Subsequent safety alerts in March 2025 triggered a voluntary pause and Type 1 recall, undermining physician confidence and delaying large-scale adoption. Similar timelines affect other emerging electrophysiology tools, narrowing the near-term addressable market for advanced ablation disposables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Monitoring Devices Gain Ground Amid Remote-Care Momentum

Diagnostic and monitoring devices, however, are on course for a 6.7% CAGR, signaling rising preference for preventive and home-based care. Hospitals continue to allocate sizable capital toward transcatheter valves, drug-eluting stents, and mapping catheters, but provincial telehealth funding now channels incremental dollars toward wearable ECG sensors and cloud-connected blood-pressure systems. Hamilton Health Sciences’ MyChart Care Companion program illustrates this pivot, enrolling heart-failure patients in continuous symptom tracking that reduced readmissions during 2024 pilots.

Real-world evidence reinforces the economic advantage of early detection. Boston Scientific’s mCRM System delivered a 97.5% complication-free rate in Canadian trial sites, bolstering hospital case for adopting leadless pacemaker–S-ICD combinations. Parallel advances in AI interpretation lower clinician workload and accelerate diagnoses, expanding addressable volumes for monitoring devices nationwide. The Canada cardiovascular devices market readily absorbs these innovations, supported by MDSAP-enabled synchronized North American launches.

By Application: Heart Failure Treatments Accelerate Beyond Traditional CAD Interventions

Coronary artery disease applications commanded 40.10% of 2025 revenue within the Canada cardiovascular devices market share, underpinned by high PCI volumes. Yet heart-failure and cardiomyopathy devices are growing faster, at a 6.95% CAGR, buoyed by a 25% rise in heart-failure hospitalizations over the past decade. Pulmonary-artery pressure sensors, next-generation LV assist devices, and remote hemodynamic monitors underpin this surge. Saskatchewan’s tricuspid valve repair initiative demonstrates provincial readiness to fund structural solutions that reduce rehospitalizations.

Peripheral vascular disease devices also gain momentum as diabetes prevalence climbs, especially among Indigenous populations, steering provincial screening budgets toward duplex ultrasound and atherectomy disposables. Digital health overlay—such as Edmonton Zone’s Virtual Home Hospital—enables remote titration of therapies, further validating investment in connected devices [BMJOPENQUALITY.BMJ.COM]. The layering of digital platforms onto device hardware enlarges lifetime revenue per patient, reinforcing application-segment diversification inside the Canada cardiovascular devices market.

By End User: Home-Care Settings Emerge as Fastest-Growing Channel

Hospitals owned 62.50% of Canada cardiovascular devices market size in 2025, reflecting concentration of high-acuity interventions in tertiary centers . However, home-care environments will expand at a 6.55% CAGR as provincial payers seek to curb readmissions and optimize bed capacity. Canada’s Drug Agency catalogued 11 active cardiac remote-monitoring programs, with Ontario’s Medly application demonstrating tangible cost offsets. Wearable device penetration accelerates adoption in domiciliary settings, buttressed by Canadian primary-care physicians’ broadened telehealth adoption post-pandemic.

Ambulatory surgical centers and cardiology/EP clinics also capture volume from elective EP ablations and day-case TAVI. Reimbursement parity initiatives promote migration of lower-risk procedures away from inpatient wards, incentivizing suppliers to tailor device kits for short-stay workflows. Manufacturers responding with bundled disposables and portable imaging further embed their offerings across diversified care sites, ensuring robust channel mix within the Canada cardiovascular devices market.

Geography Analysis

Ontario and Quebec jointly account for the largest provincial revenue, driven by population scale and dense networks of cardiac institutes. Ontario’s USD 31 million Windsor expansion and Kitchener’s third-lab build strengthen procurement leverage, attracting competitive bids for balloons, guides, and closure devices. Quebec’s analogous investments sustain double-digit growth in mapping catheters and structural heart systems. Western provinces narrow the gap; Alberta’s early Red Deer cath-lab opening and Saskatchewan’s valve-repair program push local equipment spending ahead of national averages.

Atlantic provinces and northern territories face prolonged wait times for invasive procedures, prompting health authorities to deploy tele-echocardiography trucks and satellite clinics. British Columbia’s omission of a Nanaimo cath-lab allocation in its 2025 budget sparked stakeholder criticism and highlighted geographic inequity. Device makers respond by promoting compact imaging systems and AI-triage algorithms suitable for constrained settings, thereby expanding order books in these underserved areas.

Urban–rural gradients shape procurement timetables. Metropolitan centers adopt pulse-field ablation platforms rapidly once approved, whereas rural sites rely longer on radiofrequency systems due to training gaps. The Edmonton Zone Virtual Home Hospital shows how decentralized programs can bridge access disparities while maintaining quality outcomes. Such initiatives create incremental pull for wearable telemetry, ensuring continuous coverage across Canada’s varied geography and reinforcing the broad-based momentum of the Canada cardiovascular devices market.

Competitive Landscape

The Canada cardiovascular devices market exhibits moderate concentration, with the top five multinational players controlling more than half of 2024 revenue. Medtronic, Abbott, Boston Scientific, and Edwards Lifesciences leverage full-line portfolios and established relationships with premier teaching hospitals, while niche innovators target specific domains such as AI cardiac imaging or Indigenous care pathways. Provincial GPO price compression amplifies competition by rewarding vendors that supply robust clinical-economic dossiers and support outcome-based contracts.

Medtronic secured Health Canada licensing for its Symplicity Spyral renal-denervation system in March 2024, reinforcing hypertension management offerings. Domestic contenders, nurtured by Toronto and Vancouver innovation clusters, introduce disruptive software such as SickKids’ myocardial stiffness digital biomarker and TAHSN-incubated AI echocardiography tools. These entrants compel incumbents to partner on data analytics and localized service models to preserve share in the Canada cardiovascular devices market.

White-space opportunities remain in rural telecardiology, AI-guided triage, and devices tailored to younger Indigenous patients. Firms demonstrating tangible reductions in hospital length-of-stay or readmissions gain procurement preference, realigning competitive success metrics away from purely technological novelty toward end-to-end care value.

Canada Cardiovascular Devices Industry Leaders

-

Biotronik

-

Boston Scientific Corporation

-

Siemens Healthcare GmbH

-

Medtronic

-

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Merit Medical Systems secured Health Canada clearance for its WRAPSODY Cell-Impermeable Endoprosthesis, launching immediately via its Toronto hub.

- May 2024: Medtronic obtained Health Canada licence for the Symplicity Spyral multi-electrode renal-denervation system for uncontrolled hypertension

Canada Cardiovascular Devices Market Report Scope

As per the scope of the report, cardiovascular diseases are a group of disorders of the heart and blood vessels, including coronary heart disease, peripheral arterial disease, congenital heart disease, and cerebrovascular disease.

The Canadian cardiovascular devices market is segmented by device type (diagnostic and monitoring devices (electrocardiogram (ECG), remote cardiac monitoring, and other diagnostic and monitoring devices), and therapeutic and surgical devices (cardiac assist devices, cardiac rhythm management devices, catheter, grafts, heart valves, stents, and other therapeutic and surgical devices)). The report offers the value (in USD million) for the above segments.

By Product Type

| Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | ||

| Cardiac MRI | ||

| Cardiac CT | ||

| Echocardiography / Ultrasound | ||

| Fractional Flow Reserve (FFR) Systems | ||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents |

| Bare-Metal Stents | ||

| Bioresorbable Stents | ||

| Catheters | PTCA Balloon Catheters | |

| IVUS/OCT Catheters | ||

| Cardiac Rhythm Management | Pacemakers | |

| Implantable Cardioverter Defibrillators | ||

| Cardiac Resynchronization Therapy Devices | ||

| Heart Valves | TAVR/TAVI | |

| Mechanical Valves | ||

| Tissue/Bioprosthetic Valves | ||

| Ventricular Assist Devices | ||

| Artificial Hearts | ||

| Grafts & Patches | ||

| Other Cardiovascular Surgical Devices | ||

By Application

| Coronary Artery Disease |

| Arrhythmia & Conduction Disorders |

| Heart Failure & Cardiomyopathy |

| Structural & Congenital Heart Defects |

| Peripheral Vascular Disease |

By End User

| Hospitals & Cardiac Centres |

| Ambulatory Surgical Centres |

| Cardiology/EP Clinics |

| Home-care & Remote Monitoring Programs |

| By Product Type | Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | |||

| Cardiac MRI | |||

| Cardiac CT | |||

| Echocardiography / Ultrasound | |||

| Fractional Flow Reserve (FFR) Systems | |||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents | |

| Bare-Metal Stents | |||

| Bioresorbable Stents | |||

| Catheters | PTCA Balloon Catheters | ||

| IVUS/OCT Catheters | |||

| Cardiac Rhythm Management | Pacemakers | ||

| Implantable Cardioverter Defibrillators | |||

| Cardiac Resynchronization Therapy Devices | |||

| Heart Valves | TAVR/TAVI | ||

| Mechanical Valves | |||

| Tissue/Bioprosthetic Valves | |||

| Ventricular Assist Devices | |||

| Artificial Hearts | |||

| Grafts & Patches | |||

| Other Cardiovascular Surgical Devices | |||

| By Application | Coronary Artery Disease | ||

| Arrhythmia & Conduction Disorders | |||

| Heart Failure & Cardiomyopathy | |||

| Structural & Congenital Heart Defects | |||

| Peripheral Vascular Disease | |||

| By End User | Hospitals & Cardiac Centres | ||

| Ambulatory Surgical Centres | |||

| Cardiology/EP Clinics | |||

| Home-care & Remote Monitoring Programs | |||

Key Questions Answered in the Report

What is the current value of the Canada cardiovascular devices market?

The market was valued at USD 1.81 billion in 2026 and is forecast to reach USD 2.44 billion by 2031.

Which product segment is expanding the fastest?

Diagnostic and monitoring devices are growing at a 6.7% CAGR, outpacing therapeutic categories.

How are provincial GPOs affecting device pricing?

Centralized tenders are achieving 8-12% price compression on premium cardiovascular products, compelling manufacturers to supply strong health-economic evidence.

Why is heart-failure treatment demand increasing in Canada?

Improved survival after acute coronary events has expanded the heart-failure patient pool, driving a 25% rise in related hospitalizations and boosting uptake of monitoring and assist devices.

Page last updated on: