Acute Care Telemedicine Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 31.70 Billion |

| Market Size (2030) | USD 98.71 Billion |

| Growth Rate (2025 - 2030) | 15.20% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acute Care Telemedicine Market Analysis by Mordor Intelligence

The acute care telemedicine market size stood at USD 31.70 billion in 2025 and is forecast to climb to USD 98.71 billion by 2030, translating into a robust 15.2% CAGR during the period. Accelerated adoption stems from mounting intensivist shortages, the proven ability of tele-ICU programs to cut ICU mortality odds by 25%, and expanding reimbursement parity that makes virtual critical-care encounters financially sustainable. Hospitals also prize the operational efficiencies that remote patient-monitoring dashboards and AI-driven early-warning engines deliver, cutting avoidable readmissions and boosting bed turnover. Health-system CFOs increasingly consider virtual critical-care hubs a strategic hedge against labor volatility, while cloud-native platforms and satellite links extend real-time expertise to rural ICUs that previously lacked specialty coverage. Together, these forces anchor a long-run growth narrative in which the acute care telemedicine market becomes a standard layer of the global critical-care stack rather than an emergency workaround.

Key Report Takeaways

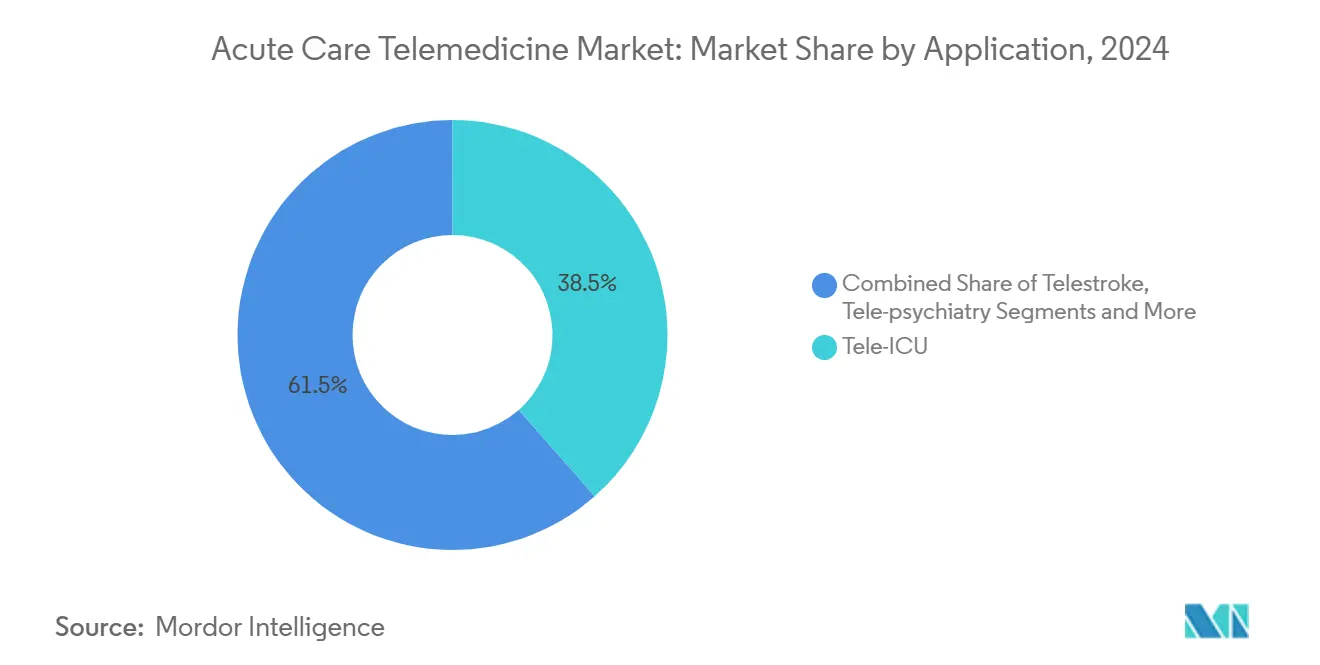

- By application, tele-ICU led with 38.5% of acute care telemedicine market share in 2024 and is advancing at a 12.4% CAGR to 2030.

- By service type, remote patient monitoring accounted for 41.6% share of the acute care telemedicine market size in 2024 and is projected to grow at 14.3% through 2030.

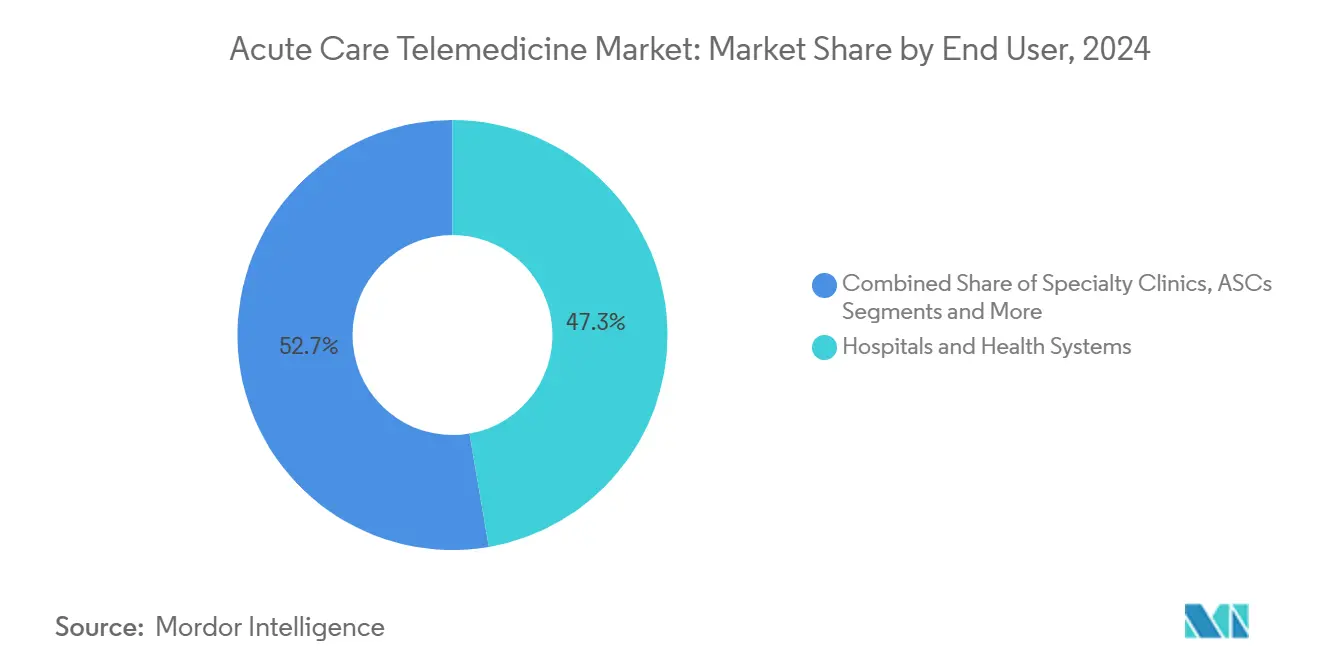

- By end user, hospitals and health systems commanded 47.3% revenue in 2024, while home-care programs show the highest forecast CAGR at 19.0% to 2030.

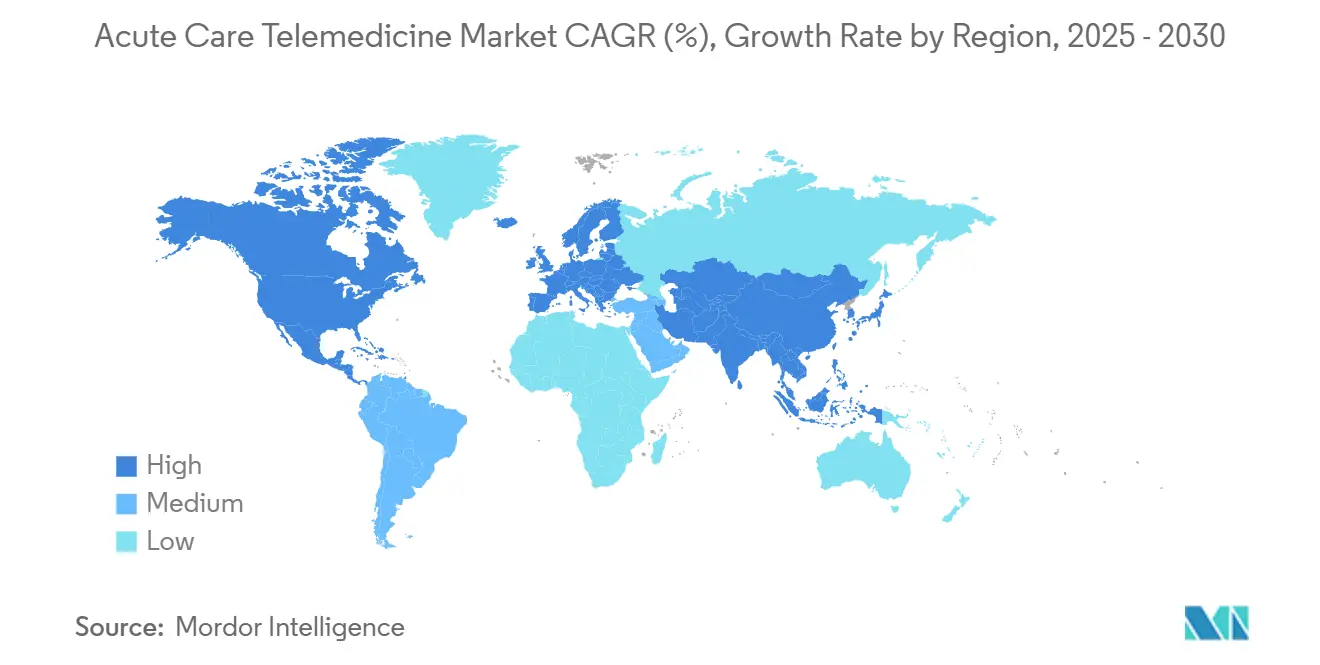

- By geography, North America captured 46.8% revenue in 2024; Asia Pacific is positioned to post the fastest 14.8% CAGR over the same horizon.

Global Acute Care Telemedicine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensivist Shortage & ICU Bed Pressure | +3.20% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Rising Hospital ROI Expectations | +2.80% | Global, led by North America | Short term (≤ 2 years) |

| Post-COVID Reimbursement Parity | +2.10% | North America, expanding to Europe | Medium term (2-4 years) |

| Cloud-Native Telehealth Platforms | +1.90% | Global, APAC adoption accelerating | Long term (≥ 4 years) |

| AI-Driven Early-Warning Systems | +1.70% | North America & APAC core markets | Long term (≥ 4 years) |

| Satellite Expansion To Remote/Offshore Sites | +1.40% | Global, rural and developing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensivist Shortage & ICU Bed Pressure

Tele-ICU hubs allow one board-certified intensivist to oversee multiple ICUs, mitigating the projected U.S. deficit of 35,000 intensivists by 2030. A mature program at the University of Minnesota’s Fairview system runs 24/7 nurse staffing and reports annual operating costs of USD 25,926 per tele-ICU bed after start-up. Meta-analysis shows a pooled 0.75 odds ratio for reduced ICU mortality in hospitals with tele-ICU oversight, benefits that are most pronounced where pre-implementation observed-to-predicted mortality exceeded 1.0. Virtual nursing complements physician coverage, with a Guthrie Clinic hub logging a 43% attrition drop and USD 7 million in labor savings after adding remote critical-care RNs.[1]American Hospital Association, “Guthrie Clinic Adds Virtual Care Hub to Address Nursing Shortage,” aha.org Together, these data points underscore why the acute care telemedicine market remains tightly linked to ongoing clinician shortages.

Rising Hospital ROI Expectations

Hospitals face razor-thin margins and view tele-ICU investments through a financial lens that weighs avoided transfers, lower mortality, and shorter ICU length of stay. A multi-center economic review pegged tele-ICU cost-effectiveness at USD 45,320 per additional quality-adjusted life year while documenting a 58% reduction in ICU mortality odds after deployment. Telestroke, often bundled under acute care billing, demonstrates even sharper returns: Massachusetts General Hospital’s 34-site network routinely achieves 38-minute door-to-needle times, well inside the American Stroke Association’s 60-minute goal and with 90% patient satisfaction. These savings and outcome gains prime financial officers to keep funding virtual-critical-care build-outs, reinforcing structural demand in the acute care telemedicine market.

Post-COVID Reimbursement Parity

The 2025 Medicare Physician Fee Schedule preserved audio-only billing codes and added caregiver-training consults to the telehealth list, cementing revenue predictability for critical-care consult codes.[2]U.S. Department of Health & Human Services, “Medicare Payment Policies,” telehealth.hhs.gov UnitedHealthcare echoed that stance in its April 2025 policy update, broadening commercial coverage for remote critical-care encounters. The fee for a telehealth originating site remains at 80% of USD 31.01, giving hospitals a modest but reliable facility payment that helps offset monitoring infrastructure. State laws such as California’s universal-coverage statute are closing parity gaps, creating a reimbursement scaffolding that propels the acute care telemedicine market even after public-health emergency waivers sunset.

AI-Driven Early-Warning Systems

Hospitals now feed continuous ventilator, monitor, and EHR data into cloud-hosted analytics engines that surface deterioration risks hours earlier than traditional vital-sign thresholds. Philips and Mass General Brigham showcased a real-time analytics platform that centralizes cardiac telemetry and ventilatory waveforms to generate actionable alerts for bedside and tele-ICU teams. Early adopters have documented 40% fewer unplanned ICU readmissions and reduced false-alarm fatigue because algorithms throttle non-actionable alerts. Teladoc Health’s AI-enabled virtual-sitter service lets one centralized technician monitor 25% more rooms without compromising fall-prevention metrics. These advances tighten the link between data science and bedside action, adding a durable innovation pillar within the acute care telemedicine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-Border Licensure Complexity | -1.80% | Global, acute in North America | Medium term (2-4 years) |

| Data-Privacy & Cybersecurity Gaps | -2.30% | Global, regulatory focus in US/EU | Short term (≤ 2 years) |

| Tele-Clinician Alarm Fatigue | -1.50% | Global, critical care environments | Medium term (2-4 years) |

| Bundled-Payment Reimbursement Limits | -1.20% | North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cross-Border Licensure Complexity

Only 37 U.S. states participate fully in the Interstate Medical Licensure Compact, and specialties such as emergency neurology face additional credentialing hurdles that stall real-time consults across state lines. Hospitals must still secure separate privileges for each remote physician, ballooning administrative work and introducing delays that undermine time-critical interventions. During regional COVID-19 surges, these licensing seams limited the rapid redeployment of idle intensivists to hot-spot ICUs, illustrating how regulation throttles otherwise elastic virtual capacity. Unless federal or multistate reform accelerates, licensure friction will continue to shave points off the acute care telemedicine market’s potential expansion trajectory.

Data-Privacy & Cybersecurity Gaps

Proposed HIPAA security-rule amendments call for end-to-end encryption, zero-trust network architectures, and 24-hour breach-notification windows, changes that the Office for Civil Rights estimates could cost providers USD 9.3 billion in year one. Smaller rural hospitals—often prime candidates for tele-ICU partnerships—lack capital and security staff, making them prime ransomware targets and discouraging deployment. Cyber-insurance premiums rose 13% in 2024 for hospitals with remote-monitoring interfaces, reflecting actuarial concern over real-time data flows that hackers can exploit. Consequently, board-level risk committees sometimes defer telemedicine investment until cybersecurity posture improves, tightening a restraint on the acute care telemedicine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Tele-ICU Dominance in Critical Care

Tele-ICU programs captured 38.5% of the acute care telemedicine market share in 2024, a leadership position built on more than a decade of peer-reviewed outcome data. The segment’s contribution to the acute care telemedicine market size is forecast to expand at 12.4% CAGR as additional community hospitals link to hub-and-spoke command centers for around-the-clock intensivist oversight. Adoption gains momentum in facilities where observed-to-predicted mortality remains high, because management teams can point to published odds-ratio reductions to justify capital spend. Telestroke follows as the fastest-growing application, with an 18.7% rate propelled by time-to-therapy imperatives and a widening rural hospital footprint that depends on rapid neurologic expertise.[3]American Medical Association, “Telestroke Case Study,” ama-assn.org Emergency tele-psychiatry and tele-pharmacy round out the application slate, underscoring the acute care telemedicine industry’s evolution from broad ICU monitoring toward subspecialty-driven virtual services.

Second-generation tele-ICU suites now bundle predictive analytics dashboards, ventilator waveform capture, and medication-dosing decision support that help bedside teams forecast deterioration hours in advance. Hospitals deploying these capabilities report average ICU length-of-stay declines of 0.9 days and bed-turnover gains that spill over to revenue cycle improvements. Meanwhile, telestroke services benefit from streamlined DICOM image sharing that accelerates neurologist reads, saving an average of 22 transfer minutes per case. Such performance metrics solidify each application’s role inside the broader acute care telemedicine market and signal continued segmentation maturity.

By Service Type: Remote Monitoring Enables Continuous Surveillance

Remote patient-monitoring dashboards accounted for 41.6% of the acute care telemedicine market in 2024, reflecting the clinical need to stream physiologic data from disparate devices into a single command interface. That dominance is set to hold, with the service line tracking a 14.3% CAGR through 2030 as AI-triaged alerting trims false positives and keeps tele-clinicians engaged. Telenursing stands out as the fastest grower at 20.5%, propelled by empirical evidence that experienced RNs can manage 67% of admissions and discharges remotely while granting on-site staff an extra 45 minutes per patient episode.

Real-time virtual consultation remains mission-critical for emergent cardiology or trauma cases requiring specialist input within minutes, while store-and-forward services carve a smaller niche in acute radiology and dermatology. Mobile health adjuncts help transition patients out of the ICU sooner by providing structured symptom tracking during the first 30 days post-discharge, another proof point that the acute care telemedicine market is no longer limited to hospital walls. Together, these service-line dynamics illustrate how technology layers converge to form an integrated, end-to-end acute care telemedicine industry ecosystem.

By End User: Hospital Systems Drive Institutional Integration

Hospital and health-system command centers generated 47.3% of the total 2024 revenue, and their installed base gives them unmatched influence over vendor road maps and interoperability standards. Boards increasingly embed acute-care telemedicine metrics—remote-supervised ICU beds, tele-nurse coverage ratios, and telestroke response times—into quality dashboards, reinforcing internal commitment. Home-based acute-care programs register the highest 19.0% CAGR because payers now reimburse remote physiologic monitoring and post-ICU check-ins, which frees capacity and reduces readmissions that would otherwise dent DRG margins. Specialty clinics and ambulatory surgery centers use ad-hoc critical-care consults to stabilize adverse events without emergency transfers. This demonstrates the peripheral but fast-moving edge of the acute care telemedicine market.

Employer coalitions and managed-care organizations are also piloting virtual rapid-response teams that intervene before beneficiaries reach high-cost emergency rooms, a model that may further diversify the end-user mix. These structural shifts show how the acute care telemedicine market size is distributed across increasingly heterogeneous care venues, each requiring tailored workflow, credentialing, and security constructs yet all contributing to a single continuum of virtual critical-care delivery.

Geography Analysis

North America captured 46.8% of global 2024 revenue, buoyed by 50-plus tele-ICU networks that collectively supervise roughly 5,800 ICU beds. Long-standing reimbursement parity and enterprise-grade cloud infrastructure have smoothed the implementation path, though market expansion now tilts toward rural hospitals that remain off-grid from marquee academic hubs. Regulatory consistency—exemplified by Medicare maintaining consult codes and states enshrining service-parity laws—supports predictable cash flows that keep North American adoption steady even as absolute growth moderates.

Asia Pacific ranks as the fastest-growing theater, clocking a 14.8% CAGR off a smaller installed base as policymakers earmark funding for ICU capacity and digital-health rails. China alone is steering portions of its projected RMB 205 trillion health-expenditure outlay toward tele-intensive-care pilots, while India’s National Digital Health Mission promotes FHIR-based data exchange that dovetails with cloud-hosted tele-ICU hubs. Health ministries across Southeast Asia are likewise trialing satellite backhaul to connect island provinces to mainland command centers, a move that underlines the acute care telemedicine market’s resilience in infrastructure-weak geographies.

Europe focuses on cross-border critical-care collaboration, leveraging the European Health Data Space framework to permit cardiology or trauma specialists in one member state to consult on a case in another within GDPR safeguards. Middle Eastern and African systems are experimenting with Starlink-powered connectivity to offset terrestrial limitations, while Brazil’s Ministry of Health concluded a 15-ICU tele-care roll-out that treated 5,471 patients and logged high clinician satisfaction. These blended use cases illustrate how regional policy, infrastructure, and reimbursement landscapes modulate the acute care telemedicine market’s rhythm worldwide.

Competitive Landscape

North America captured 46.8% of global 2024 revenue, buoyed by 50-plus tele-ICU networks that collectively supervise roughly 5,800 ICU beds. Long-standing reimbursement parity and enterprise-grade cloud infrastructure have smoothed the implementation path, though market expansion now tilts toward rural hospitals that remain off-grid from marquee academic hubs. Regulatory consistency—exemplified by Medicare maintaining consult codes and states enshrining service-parity laws—supports predictable cash flows that keep North American adoption steady even as absolute growth moderates.

Asia Pacific ranks as the fastest-growing theater, clocking a 14.8% CAGR off a smaller installed base as policymakers earmark funding for ICU capacity and digital-health rails. China alone is steering portions of its projected RMB 205 trillion health-expenditure outlay toward tele-intensive-care pilots, while India’s National Digital Health Mission promotes FHIR-based data exchange that dovetails with cloud-hosted tele-ICU hubs. Health ministries across Southeast Asia are likewise trialing satellite backhaul to connect island provinces to mainland command centers, a move that underlines the acute care telemedicine market’s resilience in infrastructure-weak geographies.

Europe focuses on cross-border critical-care collaboration, leveraging the European Health Data Space framework to permit cardiology or trauma specialists in one member state to consult on a case in another within GDPR safeguards. Middle Eastern and African systems are experimenting with Starlink-powered connectivity to offset terrestrial limitations, while Brazil’s Ministry of Health concluded a 15-ICU tele-care roll-out that treated 5,471 patients and logged high clinician satisfaction. These blended use cases illustrate how regional policy, infrastructure, and reimbursement landscapes modulate the acute care telemedicine market’s rhythm worldwide.

Acute Care Telemedicine Industry Leaders

Teladoc Health

Philips

Amwell

GE HealthCare

Hicuity Health (Advanced ICU Care)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Philips and Mass General Brigham partnered to build an AI-powered insights engine that fuses ventilator and monitor data for continuous critical-care decision support.

- February 2025: Teladoc Health acquired Catapult Health for USD 65 million, adding lab-quality at-home diagnostics to its acute-care telemetry stack.

- January 2025: Avel eCare purchased Amwell Psychiatric Care, expanding virtual behavioral-health crisis coverage across 46 states.

- November 2024: Teladoc Health released an AI-enabled virtual-sitter service that lets a single technician oversee 25% more rooms without degrading fall-prevention metrics.

Global Acute Care Telemedicine Market Report Scope

| Tele-ICU |

| Telestroke |

| Tele-psychiatry |

| Tele-dermatology |

| Tele-pharmacy |

| Remote Patient Monitoring |

| Real-time Virtual Consultation |

| Store-and-Forward |

| mHealth Services |

| Telenursing |

| Hospitals & Health Systems |

| Specialty Clinics |

| Ambulatory Surgery Centers |

| Home-care Settings |

| Payers & Employer Networks |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Tele-ICU | |

| Telestroke | ||

| Tele-psychiatry | ||

| Tele-dermatology | ||

| Tele-pharmacy | ||

| By Service Type | Remote Patient Monitoring | |

| Real-time Virtual Consultation | ||

| Store-and-Forward | ||

| mHealth Services | ||

| Telenursing | ||

| By End User | Hospitals & Health Systems | |

| Specialty Clinics | ||

| Ambulatory Surgery Centers | ||

| Home-care Settings | ||

| Payers & Employer Networks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is acute care telemedicine expected to grow by 2030?

Global revenue is projected to rise from USD 31.70 billion in 2025 to USD 98.98 billion by 2030, reflecting a 15.2% CAGR over the five-year span.

Which application currently leads adoption in acute care telemedicine?

Tele-ICU services account for 38.5% of 2024 revenue, making them the largest and most established virtual critical-care application worldwide.

What financial returns do hospitals see from tele-ICU programs?

Economic studies place cost-effectiveness near USD 45,320 per additional quality-adjusted life year, with documented 58% drops in ICU mortality odds and shorter lengths of stay that free up beds.

How does reimbursement parity influence virtual critical-care uptake?

Medicare's 2025 fee schedule and parallel commercial-payer policies sustain billing codes for remote critical-care consults, giving hospitals predictable revenue streams that justify new deployments.

Why is Asia Pacific viewed as the fastest expanding region?

Government digital-health funding, rapid ICU capacity growth, and supportive telehealth policies push regional revenue forward at a 14.8% CAGR through 2030.

What cybersecurity hurdles must providers clear when launching tele-ICU platforms?

Proposed HIPAA security-rule updates mandate end-to-end encryption and could cost U.S. hospitals about USD 9.3 billion in first-year compliance, making robust cyber defenses a prerequisite for scaling.

Page last updated on: